India Electric Vehicle Financing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

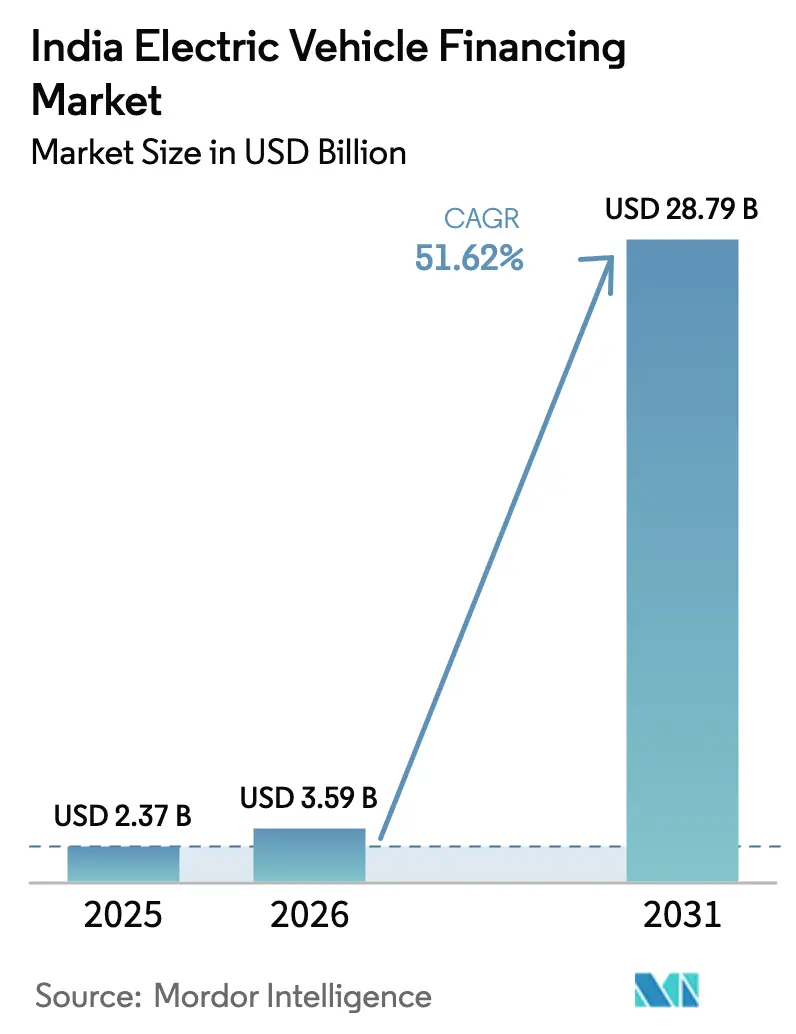

| Base Year Market Size (2025) | USD 2.37 Billion |

| Market Size (2026) | USD 3.59 Billion |

| Market Size (2031) | USD 28.79 Billion |

| Growth Rate (2026 - 2031) | 51.62% CAGR |

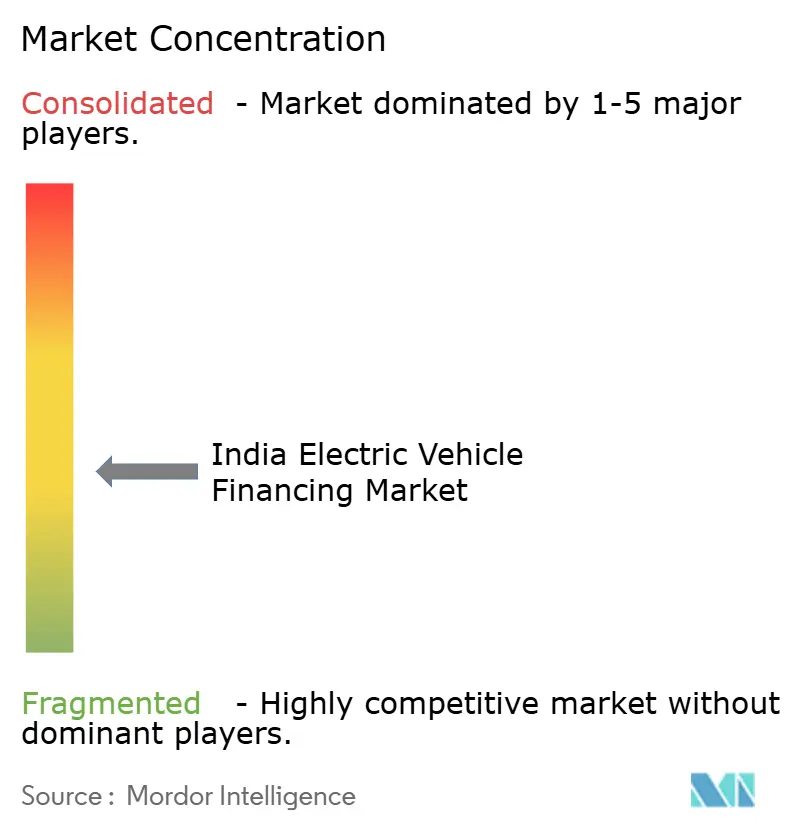

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Electric Vehicle Financing Market Analysis by Mordor Intelligence

The India electric vehicle financing market size in 2026 is estimated at USD 3.59 billion, growing from 2025 value of USD 2.37 billion with 2031 projections showing USD 28.79 billion, growing at 51.62% CAGR over 2026-2031. Rising government subsidies, rapid growth in digital lending, and aggressive electrification targets for two- and three-wheeler fleets are converging to unlock unprecedented volumes of credit demand. State–level incentive packages in Maharashtra, Gujarat, and Karnataka amplify federal support and have created localized lending hotspots. Fintech lenders are using AI-driven underwriting to compress approval times from weeks to minutes, eroding the traditional dominance of banks. Institutional capital is crowding in through green bonds and blended-finance vehicles, which are pushing down the overall cost of capital even as credit volumes rise. Heightened policy certainty through the PM E-DRIVE scheme and the Reserve Bank of India’s new Priority Sector Lending limits further reduces risk premiums and encourages product innovation across the India electric vehicle financing market.

Key Report Takeaways

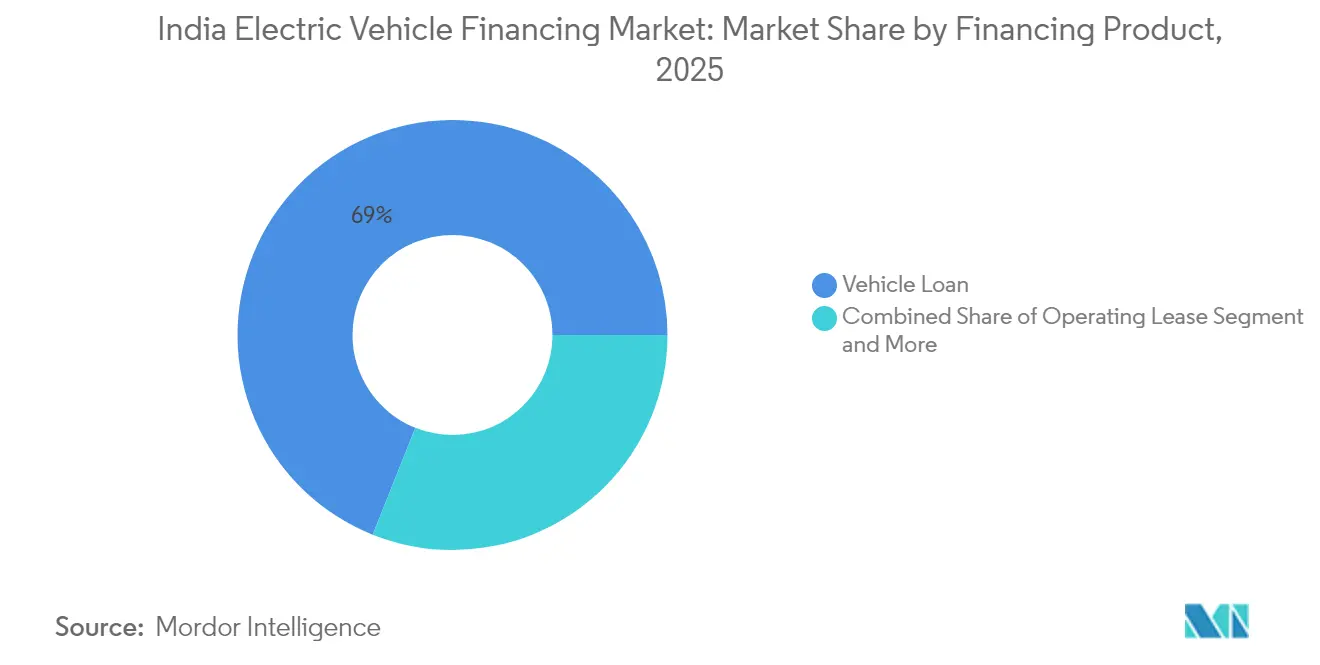

- By financing product, vehicle loans held 68.95% of the India electric vehicle financing market share in 2025, while operating leases are forecast to register the fastest 53.47% CAGR through 2031.

- By type, new vehicles accounted for 64.72% of the India electric vehicle financing market share in 2025, while used vehicles are forecast to register the fastest 54.18% CAGR through 2031.

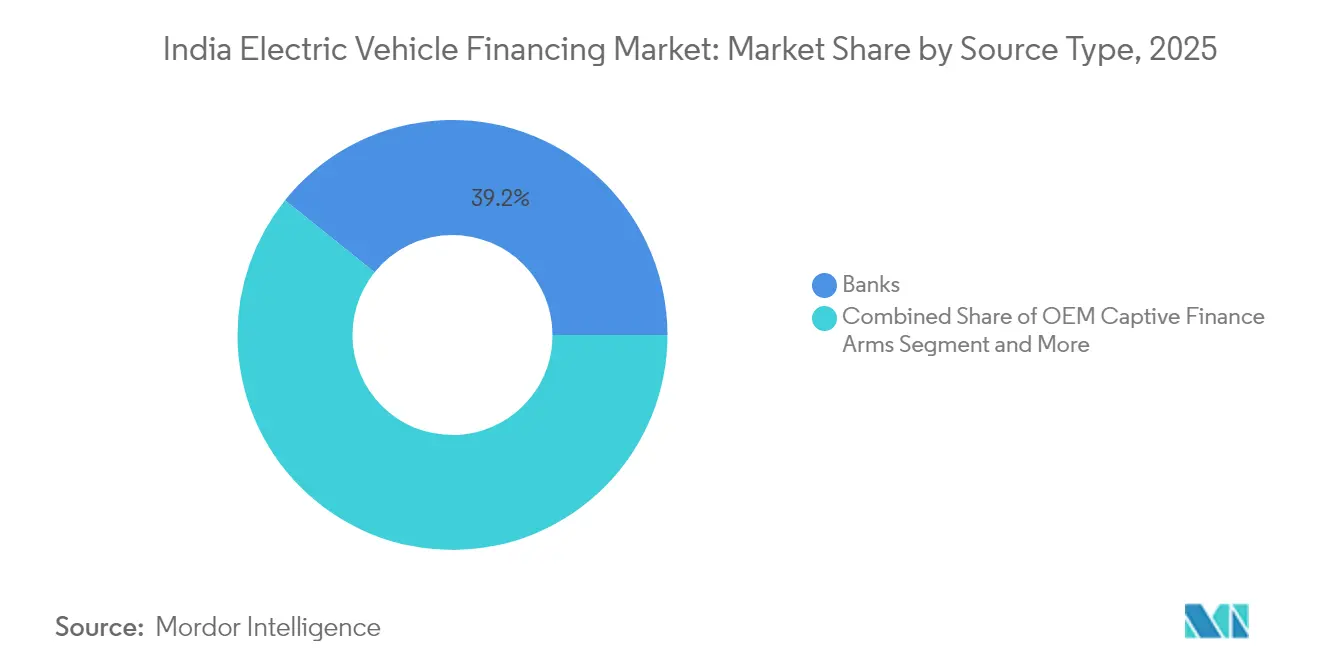

- By source type, banks commanded a 39.21% share of the India electric vehicle financing market size in 2025; fintech companies are advancing at a 52.74% CAGR to 2031.

- By vehicle type, two-wheelers led with 45.90% share of the India electric vehicle financing market size in 2025, whereas three-wheelers are projected to post the strongest 53.66% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on electric vehicle financing market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India Electric Vehicle Financing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Subsidies and Incentives | +10.5% | National, stronger in Maharashtra, Gujarat, Karnataka | Medium term (2-4 years) |

| Lower Battery Costs Drive EV | +8.2% | Manufacturing hubs in Gujarat, Tamil Nadu | Long term (≥ 4 years) |

| Companies Electrify Fleets Quickly | +7.8% | Delhi NCR, Mumbai, Bangalore, Hyderabad | Short term (≤ 2 years) |

| Fintech Platforms Enable Digital Lending | +6.3% | National, early uptake in Tier-1 and Tier-2 cities | Medium term (2-4 years) |

| Battery-As-A-Service Financing Expands | +4.1% | Pilot zones: Delhi, Mumbai, Pune, Chennai | Long term (≥ 4 years) |

| Green Bonds Lower Capital Costs | +3.2% | National, corporate lending pockets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies and Fiscal Incentives for EVs

The PM E-DRIVE scheme’s INR 10,900 crore (USD 1.31 billion) budget through 2028 directly reimburses manufacturers, which removes the liquidity gap that previously forced buyers to borrow higher loan principals. Maharashtra layers an additional INR 930 per kWh battery capacity subsidy, effectively lowering interest costs by 200-300 basis points for eligible borrowers [1]“Priority Sector Lending Guidelines 2025,” Reserve Bank of India, rbi.org.in. Policy duration to 2028 gives lenders a predictable runway to price multi-year products confidently. State-level fast-lane approvals reduce documentation cycles, further nurturing growth within the India electric vehicle financing market.

Falling Battery Costs Accelerating EV Adoption

Average pack prices declined from USD 137 per kWh in 2024 to a forecast of USD 89 per kWh by 2030, slicing upfront vehicle prices and improving loan-to-value ratios. Localized production under the Production-Linked Incentive scheme trims import reliance, resulting in steadier rupee pricing and enabling fixed-rate products with reduced currency-hedge costs. Two- and three-wheelers, where batteries form up to 40% of on-road cost, feel the greatest impact, unlocking wider borrower pools and enlarging the India electric vehicle financing market size.

Rapid Fleet Electrification by E-commerce and Logistics Firms

Large aggregators are ordering thousands of EVs to reduce delivery costs and meet sustainability pledges. Commercial operators borrow INR 2.5-4 million per vehicle batch, roughly triple a retail ticket, offering higher fee income and asset-backed security opportunities. Usage data from telematics feeds lenders’ risk engines, cutting default rates and attracting mainstream institutional funding into the India electric vehicle financing market.

Fintech-enabled Digital Lending Platforms

Digital lenders leverage utility payments, mobile top-ups, and e-commerce receipts to score thin-file customers, pushing approval rates 60-70% above bank averages. Real-time battery health data informs dynamic rate resets, aligning interest obligations with asset performance. The Reserve Bank of India sandbox lets firms pilot usage-based insurance bundling, fortifying cash-flow certainty and expanding the India electric vehicle financing industry’s product frontier.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Used Car Values Uncertain | -4.5% | National, sharper in Tier-2 and Tier-3 cities | Medium term (2-4 years) |

| Limited Public EV Charging | -3.8% | Rural and semi-urban belts, North and East | Long term (≥ 4 years) |

| Standardized Battery Health Lacking | -2.1% | Nationwide, all segments | Medium term (2-4 years) |

| Frequent Policy Revisions Raise Costs | -1.7% | National, heavier for smaller lenders | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Uncertain Residual Values for Used EVs

Limited transaction history leads lenders to discount collateral values to 60-70% of the invoice, compared with 80-85% for internal-combustion vehicles [2]“Second-Life Batteries and Residual Value,” Council on Energy, Environment and Water, ceew.org. Proprietary battery-health tools inhibit cross-brand benchmarking, elevating underwriting friction and slowing the secondary-financing flywheel that would otherwise recycle capital into the India electric vehicle financing market.

Limited Public Charging Infrastructure Coverage

Station density outside major metros averages 0.1-0.3 units per 100 km², throttling adoption in freight corridors. Sparse coverage elevates range-anxiety risk models, prompting lenders to tack on higher risk premiums. Filling the USD 2.9 billion funding gap for chargers is pivotal to unlocking latent rural demand and balancing the India electric vehicle financing market’s geographic mix.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Financing Product: Operating Leases Gain Traction

Vehicle loans accounted for 68.95% of the India electric vehicle financing market size in 2025, reflecting entrenched buyer preference for outright ownership. Growth momentum, however, is shifting: operating leases are projected to post a 53.47% CAGR through 2031 as fleet managers prioritize asset-light models. Lease structures limit balance-sheet strain, let operators rotate into newer battery chemistries, and mitigate residual-value uncertainty—an enduring pain point. For lenders, predictable lease cash flows align well with securitization structures now emerging in the India electric vehicle financing market.

Subscription plans bundle access, maintenance, and charging in one fee, catering to urban commuters seeking flexibility. Battery-swap-linked finance further blurs the line between mobility service and asset ownership, demanding nuanced risk models. Regulatory clarity under RBI’s revised Priority Sector Lending norms allows banks to book operating-lease receivables under renewable-energy quotas, enhancing capital efficiency. As familiarity grows, operating leases are likely to raise their India electric vehicle financing market share in metropolitan clusters first before cascading to Tier-2 urban pockets.

By Type: Used Vehicle Financing Emerges

Fresh-from-factory sales secured 64.72% of the India electric vehicle financing disbursements in 2025, but the secondary market is heating up with a forecast 54.18% CAGR. Certified pre-owned programs with warranty extensions demystify battery health concerns and draw first-time EV buyers priced out of new models. Lenders are piloting algorithms that parse State of Health metrics, charging cycles, and telematics-verified mileage, enabling tighter loan-to-value bands and competitive rates within the India electric vehicle financing market.

Improved diagnostic kiosks at dealer yards speed valuation, making auction-based price discovery viable in semi-urban regions. As diagnostic data pools lengthen, lenders anticipate sharpening residual-value tables, which should compress risk premiums and accelerate volume. Portfolio diversification into used vehicles also cushions lenders against supply fluctuations in new-vehicle production, adding resilience to the India electric vehicle financing industry.

By Source Type: Fintech Companies Disrupt Traditional Models

Banks retained 39.21% of the India electric vehicle financing market share in 2025, leveraging low-cost deposits and branch reach. Yet fintech originators are outpacing at a 52.74% CAGR, capturing digitally native borrowers through biometric KYC, e-signature execution, and sub-24-hour fund disbursal. Algorithmic scoring of non-traditional data—mobile wallet flows, utility bill payment regularity, and even ride-hail driver ratings—expands eligibility beyond formal-salary segments.

OEM-captive arms integrate financing at the point of sale, blending rate incentives with service packages that lock in aftermarket revenue. Non-bank finance companies focus on micro-entrepreneurs, using community-based collections to maintain sub-3% delinquency ratios. As scale arrives, securitization of fintech portfolios is lowering the cost of funds, enabling ever-sharper pricing across the India electric vehicle financing market.

By Vehicle Type: Three-Wheelers Lead Growth

Two-wheelers continue to dominate at 45.90% of the India electric vehicle financing market share in 2025, driven by affordability and ubiquitous usage in India’s congested cities. Ticket sizes between INR 0.8-1.5 lakh suit retail credit appetites and keep delinquencies low. Commercial three-wheelers, however, are growing fastest at 53.66% CAGR, buoyed by last-mile delivery economics that favor battery power over diesel. Higher daily utilization supplies lenders with richer telematics data, permitting usage-linked repayment schedules and dynamic rate resets.

Passenger-car uptake remains urban-premium, inhibited by parking and charging access constraints. Yet high-income metros showcase financing bundles with overnight home-charger installation, shaving perceived inconvenience. Heterogeneity across vehicle classes demands finely segmented underwriting, a capability in which data-centric fintech lenders are carving durable niches within the India electric vehicle financing market.

Geography Analysis

Maharashtra, Gujarat, and Karnataka collectively represented a significant share of 2024 loan disbursements, underscoring policy coherence, robust urban incomes, and manufacturing ecosystems. Maharashtra tops the leaderboard thanks to extra battery subsidies and expedited state tax rebates. Gujarat capitalizes on its EV assembly hubs and port logistics, funneling demand for both retail and commercial credit. Karnataka’s technology workforce and pro-innovation stance bolster premium-segment penetration, helping enlarge the India electric vehicle financing market size.

Delhi NCR and Tamil Nadu are set to outpace national averages through 2030. Delhi’s congestion-pricing and odd-even driving restrictions provide regulatory nudges, while Tamil Nadu’s supplier base and export orientation ensure production tailwinds. Development-finance vehicles, notably the Green Climate Fund’s USD 200 million risk-sharing program, reserve allocations for these high-impact corridors, insulating lenders against early-stage asset-quality swings.

Emerging states such as Rajasthan, Madhya Pradesh, and Uttar Pradesh are logging 45-50% forecast growth despite lower charging density. Rural electrification drives and decreasing battery prices are lowering the affordability threshold. Nonetheless, limited branch banking and lower formal incomes necessitate group-lending or agent-assisted digital models. Successful penetration here could tilt the India electric vehicle financing market toward a more balanced regional structure by decade-end.

Competitive Landscape

The India electric vehicle financing market remains moderately fragmented. Banks rely on legacy customer franchises and compliance infrastructure, but their manual processes lengthen turnaround times and inhibit subprime experimentation. Fintech challengers like RevFin and Ecofy secure venture backing to grow originations rapidly, while OEM captives such as Tata Motors Finance exploit brand synergies and after-sales data.

Strategically, incumbents pursue three pathways. First, partnership models: State Bank of India’s 2025 MoU with VinFast extends retail credit lines through the automaker’s dealer network. Second, platform integrations: Kotak Mahindra Prime embeds financing options directly into the Tesla India app, converting instant approvals into higher conversion rates. Third, institution-led scaling: the International Finance Corporation’s USD 400 million line to Bajaj Finance earmarks capital for EV portfolios, validating asset-class attractiveness [3]“IFC Bajaj Finance Partnership Press Release,” International Finance Corporation, ifc.org.

Technology is the decisive lever. AI credit engines ingest multi-source data to deliver risk-adjusted pricing, while geo-fencing and battery-health feeds trigger early-warning systems. As portfolios mature, seasoned lenders securitize lease receivables, freeing balance-sheet capacity for further expansion. Regulatory guardrails from the Reserve Bank of India, covering data privacy, co-lending, and asset-classification norms, ensure market discipline while fostering innovation. Collectively, these dynamics channel fresh capital and know-how, sharpening competitiveness across the India electric vehicle financing market.

India Electric Vehicle Financing Industry Leaders

State Bank of India

ICICI Bank

Mahindra & Mahindra Financial Services

Shriram Transport Finance Company

Tata Capital Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: VinFast Auto India signed an MoU with State Bank of India to roll out nationwide EV retail-financing solutions.

- July 2025: Kotak Mahindra Prime became Tesla’s first preferred financier in India, integrating loan approvals into Tesla’s web and app storefronts.

- March 2025: The Asian Development Bank and Shriram Finance closed a USD 150 million loan facility targeting MSME and EV credit expansion.

- January 2025: Montra Electric partnered with Shriram Finance to widen access to consumer EV finance through customized loan products.

India Electric Vehicle Financing Market Report Scope

Electric vehicle financing encompasses a range of financial services tailored to ease the purchase of electric vehicles. These services include loans, leasing options, and various credit facilities specifically crafted for EV buyers. Traditional banks, non-banking financial companies (NBFCs), fintech startups, and original equipment manufacturers (OEMs) — often through their financing divisions — alongside microfinance institutions, all play a role in providing EV financing. By addressing the typically higher upfront costs of EVs and bolstering essential infrastructure development, such as charging stations, these financial solutions strive to enhance the affordability and accessibility of electric vehicles.

The Indian electric vehicle financing market is segmented by type (new vehicle and used vehicle), source type (OEMs, banks, NBFCs, fintech companies, and microfinance institutions), and vehicle type (passenger cars, commercial vehicles, two-wheelers, and three-wheelers). For each segment, market sizing and forecast have been done on the basis of value in USD billion.

| Vehicle Loan |

| Operating Lease |

| Subscription / Battery-swap Plan |

| Hire-Purchase and Others |

| New Vehicles |

| Used Vehicles |

| OEM Captive Finance Arms |

| Banks |

| NBFCs |

| Fintech Companies |

| Micro-finance Institutions |

| Passenger Cars |

| Commercial Vehicles |

| Two-Wheelers |

| Three-Wheelers |

| By Financing Product | Vehicle Loan |

| Operating Lease | |

| Subscription / Battery-swap Plan | |

| Hire-Purchase and Others | |

| By Type | New Vehicles |

| Used Vehicles | |

| By Source Type | OEM Captive Finance Arms |

| Banks | |

| NBFCs | |

| Fintech Companies | |

| Micro-finance Institutions | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| Two-Wheelers | |

| Three-Wheelers |

Key Questions Answered in the Report

What is the projected value of India’s electric vehicle financing market by 2031?

The India electric vehicle financing market is expected to reach USD 28.79 billion by 2031, reflecting a 51.62% CAGR.

Why are operating leases growing so quickly in Indian EV finance?

Operating leases let fleet operators avoid residual-value risk and keep capital free for expansion, driving a 53.47% CAGR through 2031.

Which lender category is expanding fastest in EV financing?

Fintech companies are advancing at a 52.74% CAGR as AI-driven underwriting compresses approval times and broadens credit access.

How big is the two-wheeler share in India’s EV financing in 2025?

Two-wheelers account for 45.90% of total disbursements, making them the largest vehicle class in 2025.

Page last updated on: