Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

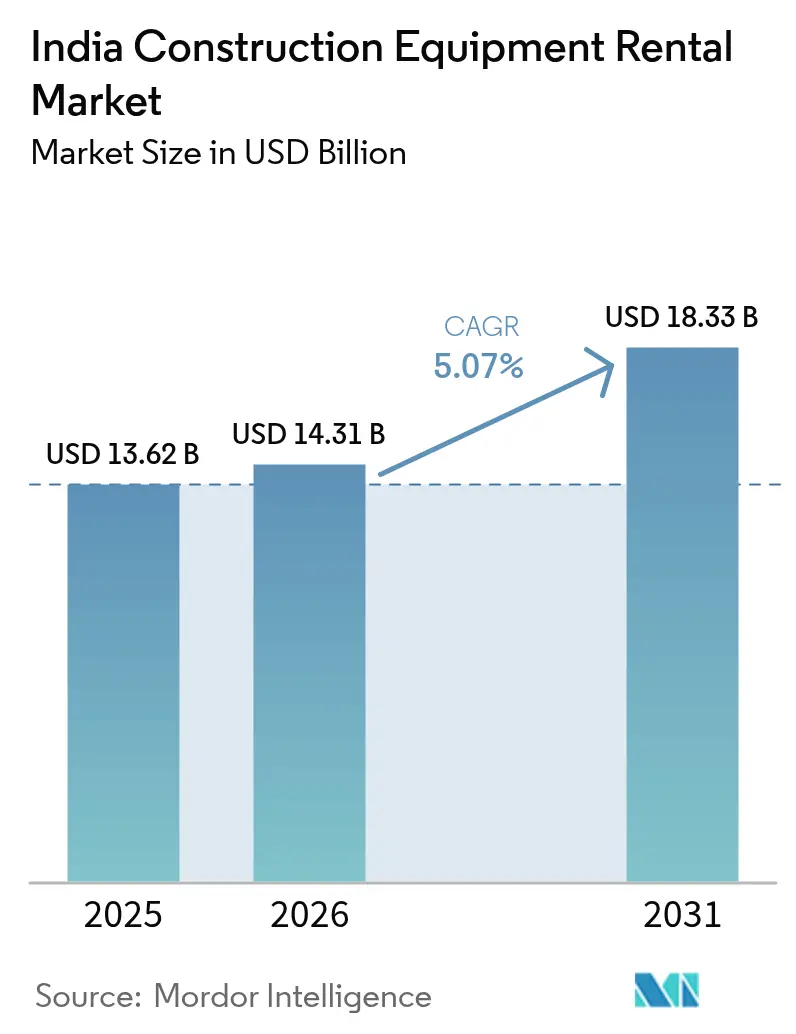

| Base Year Market Size (2025) | USD 13.62 Billion |

| Market Size (2026) | USD 14.31 Billion |

| Market Size (2031) | USD 18.33 Billion |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Construction Equipment Rental Market Analysis by Mordor Intelligence

India Construction Equipment Rental Market size in 2026 is estimated at USD 14.31 billion, growing from 2025 value of USD 13.62 billion with 2031 projections showing USD 18.33 billion, growing at 5.07% CAGR over 2026-2031. Steady capital formation under the National Infrastructure Pipeline (NIP) and PM Gati Shakti’s multimodal coordination platform are reshaping procurement behavior from ownership to rental. Rental penetration of barely less than one-tenth—well below global norms—suggests an expansive runway as asset-light strategies gain favor, especially among mid-sized contractors challenged by rising equipment prices, working-capital limitations, and Stage V emission mandates. Digital marketplaces are compressing search frictions, improving fleet utilization, and fostering transparent pricing, while OEMs are bundling uptime-guarantee service contracts with rentals to defend share. Nevertheless, election-year pauses, fragmented fleet ownership, and uneven charging infrastructure for electric equipment temper near-term momentum even as the long-term trajectory remains firmly positive for the India construction equipment rental market.

Key Report Takeaways

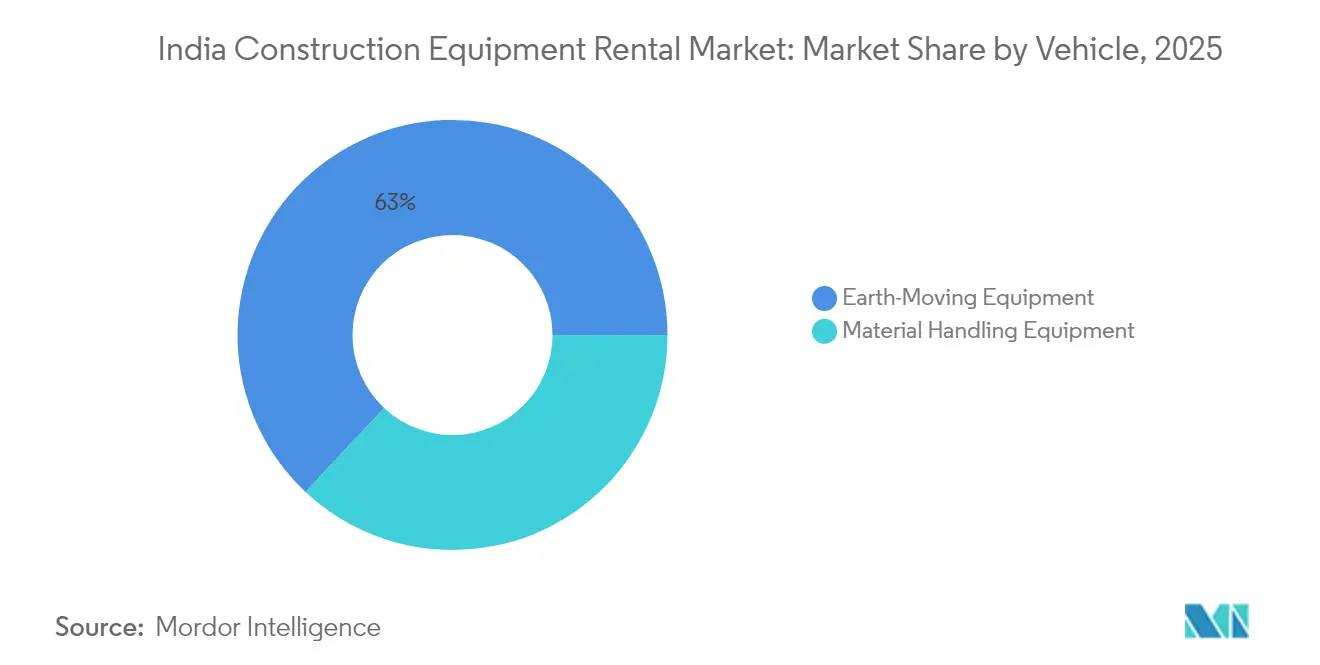

- By vehicle type, earth-moving equipment held 63.02% share of India construction equipment rental market in 2025 and is expected to expand at a 5.12% CAGR during the forecast period (2026-2031).

- By drive type, internal-combustion engines captured 86.55% share of India construction equipment rental market in 2025, while electric and hybrid alternatives is expected to grow at a 5.18% CAGR during the forecast period (2026-2031).

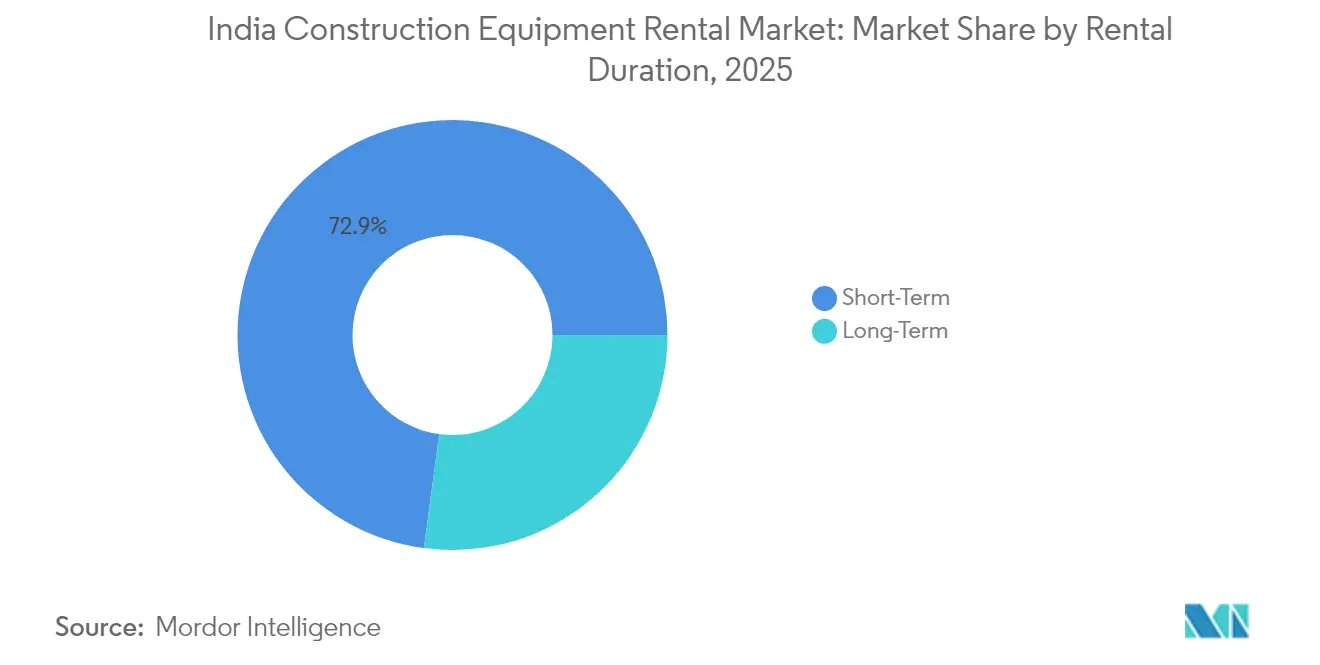

- By rental duration, short-term contracts commanded 72.88% share of India construction equipment rental market in 2025; long-term agreements are projected to advance at 5.24% CAGR during the forecast period (2026-2031).

- By end user, infrastructure accounted for 54.02% share of India construction equipment rental market in 2025, whereas mining and quarrying is expected to grow at 5.16% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Construction Equipment Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Infrastructure Pipeline | +1.8% | National, with concentration in UP, Maharashtra, Telangana | Long term (≥ 4 years) |

| Smart-City And Affordable-Housing Projects | +0.9% | Urban centers, Tier-1 and Tier-2 cities | Medium term (2-4 years) |

| Rising Preference For Asset-Light, Pay-Per-Use Models | +0.7% | National, stronger adoption in metropolitan areas | Short term (≤ 2 years) |

| Digital Rental Marketplaces | +0.5% | National, with faster penetration in tech-savvy regions | Medium term (2-4 years) |

| Tightening Emission Norms | +0.4% | National, with stricter enforcement in NCR and major cities | Long term (≥ 4 years) |

| OEM Service Contracts Bundled With Rentals | +0.3% | National, led by organized rental companies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Infrastructure Pipeline (NIP & PM Gati Shakti)

India is ramping up its national infrastructure initiatives, bolstered by digital planning platforms that enhance project transparency and integrate large-scale developments. With the expansion of rail networks and a more streamlined process, project execution has become increasingly predictable. This newfound stability is proving advantageous for equipment rental companies, leading to consistent fleet utilization and prompting them to make larger capital investments. These developments underscore a significant shift towards long-term infrastructure planning, heightened execution efficiency, and a surging demand for specialized construction machinery. The rail ministry’s CAPEX is Rs 2.65 lakh crore (USD 32 Billion) for FY 2024-31 pipeline further anchors demand for specialized tampers, pavers, and tunnel-boring units[1] “PM Gati Shakti Update,” Press Information Bureau, pib.gov.in.

Smart-City & Affordable-Housing Projects Accelerate Demand

Smart-city programs have sanctioned a huge amount across 100 cities, with three-fifth of projects in execution, locking-in urban equipment demand cycles. Tamil Nadu’s approval of five rental-housing clusters totaling thousands of units exemplifies state-level momentum. Contractors increasingly rely on rentals for specialized formwork and high-reach platforms not justified for outright purchase[2]“PMAY-U Progress Report 2025,” Ministry of Housing & Urban Affairs, mohua.gov.in .

Rising Preference for Asset-Light, Pay-Per-Use Models

In India, the construction sector is witnessing a steady uptick in rental equipment usage, particularly in smaller cities. This shift is largely attributed to tax reforms that render short-term rentals more economical than outright asset purchases. Contractors are now emphasizing financial flexibility, opting to channel their capital into new projects instead of tying it up in depreciating machinery. Moreover, comprehensive rental packages, encompassing maintenance, trained operators, and insurance, are boosting equipment uptime. This makes rentals increasingly appealing to firms that lack the resources to manage fleets independently. Such dynamics are not only reshaping the construction equipment landscape but also amplifying the demand for scalable, service-centric rental models.

Digital Rental Marketplaces Expanding Equipment Access

Online portals match idle fleets with distant projects, democratizing access and shrinking dead-haul distances. IoT-enabled listings provide hour-meter data, predictive-maintenance alerts, and usage-based invoicing. Rural internet penetration above three-fifth per JCB India sales data now allows real-time sourcing for projects under the Pradhan Mantri Gram Sadak Yojana, reducing lead times and stabilizing pricing, vital for the India construction equipment rental market’s maturation[3]“Stage V Construction Machines Launch,” JCB, jcb.com .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction Sector Cyclicality And Election-Year Pauses | -0.8% | National, with higher impact in states with frequent elections | Short term (≤ 2 years) |

| Highly Fragmented Supply Base Limits Nationwide Fleet Depth | -0.6% | National, more pronounced in Tier-2 and Tier-3 cities | Medium term (2-4 years) |

| Low Residual-Value Perception Hampers Equipment Financing | -0.4% | National, with acute impact in rural and semi-urban markets | Medium term (2-4 years) |

| Scarcity Of Skilled Operators | -0.3% | National, with severe shortages in Tier-2 and Tier-3 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction Sector Cyclicality & Election-Year Pauses

India's construction equipment sector is feeling the pinch from the country's general election cycle. Although rental turnover has held steady, equipment sales have taken a hit, largely due to policy approval delays tied to the Model Code of Conduct. It's common for project initiations to decelerate during election seasons, leading to decreased equipment utilization and a subsequent dip in rental prices. Furthermore, with staggered state elections in pivotal regions such as Uttar Pradesh, Maharashtra, and Telangana, demand patterns have become erratic, posing challenges for rental companies in fleet deployment and planning.

Highly Fragmented Supply Base Limits Nationwide Fleet Depth

In India, most equipment operators oversee modest fleets, primarily centered on basic machinery like backhoe loaders. Yet, the scarcity of specialized unit, like large excavators, high-reach booms, and tunnel-boring machines, compels engineering and construction firms to juggle multiple vendors. This not only heightens logistical challenges but also inflates operational costs. Furthermore, impending regulatory changes, notably stricter emission standards, mandate capital investments that pose a challenge for many smaller rental firms. As a result, the market is witnessing a wave of consolidation, with tech-savvy players poised to seize a larger share and adapt to shifting project requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle: Earth-Moving Equipment Drives Mechanization Transition

Earth-moving machines captured 63.02% India construction equipment rental market share in 2025 and will expand at a 5.12% CAGR. Backhoe loaders remain the workhorse in rural road layouts, while 20-35 ton excavators see rising dispatches to coal blocks targeting more than billion tons of extraction by 2025. Material handling hardware—mobile cranes, tower cranes, telehandlers—gains from smart-city high-rise shells. Dump trucks profit from NIP road packages that lifted aggregate haulage. Dozers and graders, though smaller in volume, are critical to the India construction equipment rental market size for highway sub-grade preparation and will benefit from the Bharatmala highway densification program.

Automated grade-control systems installed on dozers have cut re-work by a quarter, persuading contractors to lease technologically richer gear rather than buy dated units. JCB India’s Stage V lineup, released January 2025, offers one-tenth better fuel economy—an immediate cost lever for renters. Telematics downloads inform predictive-maintenance schedules, enabling rental companies to offer iron-clad uptime commitments that justify premium tariffs within the India construction equipment rental market.

By Drive Type: Electric Transition Accelerates Despite ICE Dominance

Internal-combustion engines represented 86.55% of 2025 revenue, but electric and hybrid units will rise fastest at 5.18% CAGR through 2031. Battery prices, falling toward USD 75/kWh by 2028, narrow total-cost-of-ownership gaps. Hydrogen combustion prototypes under JCB’s banner sync with India’s National Hydrogen Mission, bringing zero-carbon possibilities to heavy digging. Range concerns remain; nevertheless, rental depots are uniquely positioned to house centralized charging or hydrogen refueling bays and amortize station costs across fleets. For metro tunneling, drivetrain electrification offers ventilation savings that offset higher lease fees, making it compelling inside densely populated cities where emission caps are strictest.

Rental companies marketing hybrid solutions trail pure electrics yet appeal to long-haul quarry tasks requiring continuous duty cycles. Diesel-electric hybrids post one-fifth fuel savings, meeting Stage V CO₂ thresholds and cushioning renters from diesel price shocks. Regulatory nudges and corporate decarbonization pledges should nudge adoption beyond pilot stage within the India construction equipment rental market.

By Rental Duration: Long-Term Contracts Gain Strategic Importance

Short tenure remains dominant at 72.88% of 2025 turnover, but long-term agreements should climb 5.24% CAGR as Gati Shakti’s integrated planning reduces schedule risk. In India's construction equipment sector, long-term rental contracts are becoming increasingly popular. These contracts not only provide substantial day-rate discounts but also guarantee consistent revenue for lessors. Companies like Vision Infra Equipment, boasting extensive fleets, are showcasing the benefits of scale by forging long-term ties with prominent engineering and construction firms. Such multiyear contracts facilitate improved asset management, minimize idle periods, and bolster connections with key clients. This trend underscores a broader industry movement towards more professional and service-oriented rental models.

OEM-backed rental packages now include operator training, telematics dashboards, and preventive-maintenance kits, creating an equipment-as-a-service proposition. Predictable billing matched to project milestones allows contractors to align equipment costs with receivables, smoothing cash flow. Seasonal idle time risk shifts to rental companies, which redeploy fleets across staggered regional projects within the India construction equipment rental market.

By End User: Mining Emerges as Growth Catalyst

Infrastructure absorbed 54.02% revenue in 2025, fueled by a huge capital outlay in Budget 2025-26 for roads, rail, and metro linkages. Backhoe loaders, motor graders, and batching plants see steady call-offs under EPC contracts. Real-estate and commercial builds maintain brisk crane leasing, supported by PMAY-Urban housing and smart-city community facilities.

Mining and quarrying, growing at 5.16% CAGR during the forecast period (2026-2031), require 100-ton excavators, 60-ton dumpers, and surface drill rigs that miners prefer to rent for project-specific deployments. Critical-mineral exploration for EV batteries elevates demand for core drills and geophysical survey rigs. Flexible rental contracts fit volatile commodity cycles, cushioning miners from capital-spending spikes and fostering specialized niches within the India construction equipment rental market.

Geography Analysis

Northern and western states—Uttar Pradesh, Maharashtra, Gujarat—together account for nearly three-fifth of public capex, anchoring equipment demand density. NIP road corridors crisscross Uttar Pradesh, while Maharashtra’s coastal infrastructure and Mumbai metro expansions call for specialized crawler cranes and TBMs. Southern hubs such as Telangana and Karnataka benefit from IT‐driven urbanization, generating consistent high-rise crane uptake and concrete-pump rentals.

Eastern terrain, rich in coal and iron ore, drives large excavator and haul-truck rentals, with Jharkhand and Odisha leading dispatches linked to coal-belt output expansion. Connectivity works under the Act East policy spur rock-breaker and piling-rig hires in Assam and Mizoram, though logistic costs inflate operator margins. Port-led industrial corridors in Gujarat and Tamil Nadu elevate reach-stacker and forklift leasing for container handling.

Emission-control regimes differ: NCR restricts diesel engines older than 10 years, compelling renters to deploy Stage V or electric fleets, whereas tier-3 cities retain legacy equipment. BharatNet’s fiber backhaul has improved equipment-tracking across state lines, allowing fleets to migrate seasonally without losing telematics oversight. These dynamics underpin regional fleet redeployments central to maximizing India construction equipment rental market utilization.

Regulatory Landscape

Construction equipment rentals in India operate under a tightening compliance stack covering on-road safety standards for construction equipment vehicles (CEVs), product quality controls, and city-level emission enforcement. MoRTH AIS standards such as AIS-160 (safety requirements for CEVs) and AIS-174 (electric CEV-specific requirements) continue to shape equipment specifications and retrofitting decisions, while NCR and other large-city enforcement for older diesel equipment accelerates the shift toward newer Stage V-compliant fleets and electrified machines in rental depots.

A near-term inflection is BIS conformity assessment under the Machinery and Electrical Equipment Safety (Omnibus Technical Regulation) Order 2024, which expands mandatory certification coverage for categories of construction and mining machinery. The cited compliance deadline of 1 September 2026 for mandatory BIS certification is likely to affect both domestic supply and imports. Import economics also influence fleet choices, with capital equipment imports governed via DGFT processes and duties, and schemes such as EPCG enabling 0% basic customs duty for eligible importers meeting export obligations, which can reduce acquisition cost for organized rental operators building specialized fleets.

Value Chain Analysis

The value chain starts with OEMs and component suppliers, with a significant share of high-value hydraulics, undercarriages, and electronics sourced through imports by value. Equipment financiers, dealers, and refurbishers then channel new and pre-owned machines into rental fleets. Organized rental companies (L&T Rentals, Quippo, Sanghvi Movers, Vision Infra Equipment, Gemini Equipment) and a long tail of regional lessors deploy equipment to EPC contractors, infrastructure developers, real estate builders, and miners, typically bundling maintenance, operators, telematics, and insurance into service-led contracts. Digital marketplaces and OEM service ecosystems increasingly sit between fleet owners and contractors, compressing search and mobilization lead times while improving utilization through cross-state matching.

Downstream, utilization and collections depend on project governance and contract administration. Industry bodies such as the Construction Equipment Rental Association (CERA) support standardization through model hiring agreements that help reduce disputes around confinement, downtime, and payment delays. Bottlenecks include specialized equipment scarcity outside metro clusters, operator availability for advanced machines, and parts availability for imported subsystems, which increases the value of regional service networks, spares stocking, and uptime-guarantee programs for renters handling time-bound road, rail, metro, and mining packages.

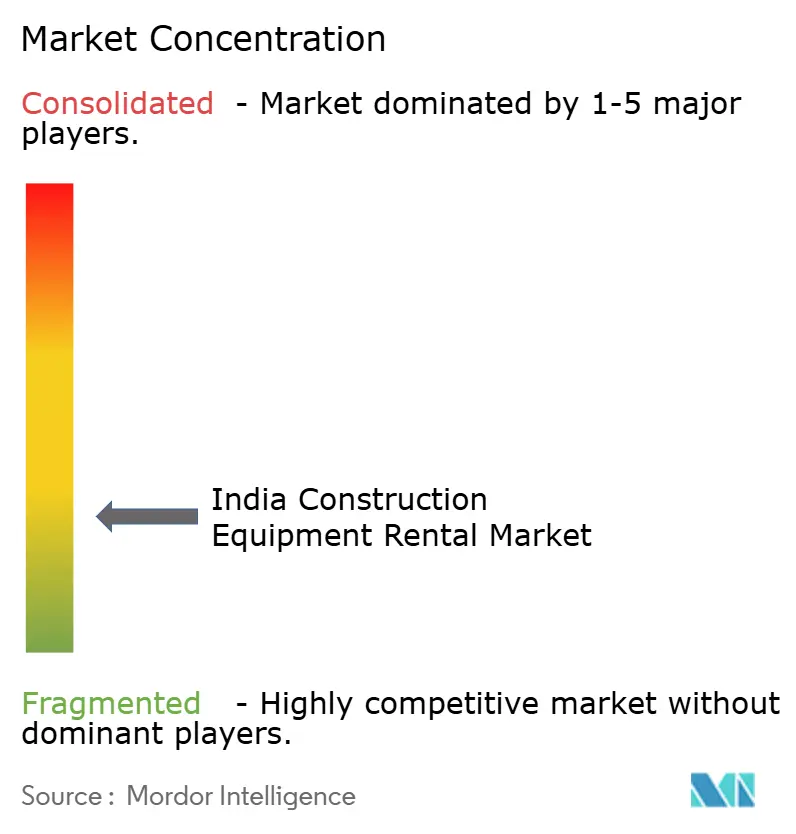

Competitive Landscape

The India construction equipment rental market is highly fragmented. Top five organized companies hold less than one-fifth combined share, with L&T Rentals, Quippo, Sanghvi Movers, Vision Infra Equipment, and Gemini Equipment occupying leadership pockets. Most others operate regionally, restricting their equipment mix to backhoe loaders and pick-and-carry cranes. Consolidation pressure is mounting because Stage V upgrades, priced more than one-tenth higher, strain smaller balance sheets. Larger players leverage scale to negotiate OEM rebates and secure fleet-wide service contracts that guarantee more than four-fifth uptime.

Technology adoption defines emerging competitive advantage. IoT sensors deliver real-time engine alerts, enabling predictive maintenance that cuts unplanned downtime by three-tenth. Digital portals such as InfraMart and Rentomojo Construction verticals list idle assets nationally, shrinking lead times to 24 hours in metro clusters. OEMs encroach via captive rental arms; JCB’s tie-up with Shriram Automall channels refurbished equipment into short-tenor leases, expanding addressable budgets.

White-space opportunities persist in specialized TBMs, high-reach demolition excavators, and battery-electric loaders—areas underserved due to high ticket size and uncertain residuals. Disruptors aggregating data-driven demand signals can curate capex and outmaneuver legacy rent-brokers. Investors eyeing resilient infra pipelines view the India construction equipment rental market as a proxy on national build-out without direct construction risk.

India Construction Equipment Rental Industry Leaders

Volvo Construction Equipment

Sanghvi Movers Limited (SML)

MYCRANE

Jindal Infrastructure Pvt. Ltd.

ABC Infra Equipment Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large, execution-backed infrastructure packages continue to create opportunities for rental penetration, especially in specialized equipment categories that remain under-supplied in fragmented fleets. For example, the Cabinet Committee on Economic Affairs approved major NHAI works on 1 July 2026, including the 117.7 km Kanpur-Kabrai (NH-34) four-lane highway (Rs 7,145.14 crore) and the 8.1 km NH-148AE Delhi twin-tube road tunnel (Rs 6,969.67 crore). These projects pull demand for higher-capability earthmoving fleets, pavers, compactors, lifting solutions, and tunneling-adjacent equipment, supporting organized lessors that can mobilize multi-location fleets with service-level commitments.

A second opportunity is service-led, usage-based offerings that reduce contractor working-capital stress while improving equipment uptime through telematics and maintenance bundling. Evidence of the model shift includes Volvo Construction Equipment India reporting that its Equipment-as-a-Service (EaaS) model surpassed INR 100 crore in revenue by December 2025, indicating growing adoption of pay-per-use structures alongside traditional rentals. Compliance-driven fleet renewal under BIS certification requirements and city-level emission enforcement also widens the addressable base for organized players scaling newer Stage V and electric/hybrid fleets. Partnerships across OEMs, refurbishers, and digital platforms further expand access to pre-owned machines and help standardize service delivery across Tier-2 and Tier-3 markets.

Recent Industry Developments

- May 2026: Sanghvi Movers Limited management highlighted in its Q4 FY2026 earnings discussion that the crane rental business contributed 65% of operating revenue for the year ended March 31, 2026. The disclosure underscores how heavy-lift rentals remain a core earnings engine, supporting continued fleet and service investments aligned to infrastructure and industrial project execution.

- December 2025: Volvo Construction Equipment India reported that its Equipment-as-a-Service (EaaS) model surpassed INR 100 crore in revenue, with services contributing 30% of total revenue. The milestone reinforces the shift toward usage-based contracts and digitally monitored uptime offerings that compete directly with conventional rental propositions.

- September 2024: SAMIL and Volvo Construction Equipment announced a strategic partnership to scale the pre-owned construction equipment ecosystem. The initiative supports a more liquid secondary market for machines, improving trade-in and refurbishment pathways that can feed organized rental fleets with better-documented equipment histories.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from renting construction equipment in India, including short-term and long-term rentals for earth-moving and material-handling fleets, with or without bundled services that are priced as part of the rental contract.

Scope exclusions: equipment sales, leasing that is accounted for as a financial product, and rentals for non-construction uses are excluded where they cannot be clearly tied to construction activity.

Segmentation Overview

- By Vehicle

- Earth-Moving Equipment

- Backhoe Loaders

- Loaders (Wheeled & Skid-Steer)

- Crawler & Wheeled Excavators

- Others (Dozers, Graders)

- Material Handling Equipment

- Mobile & Tower Cranes

- Dump Trucks & Tippers

- Others (Telehandlers, Forklifts)

- Earth-Moving Equipment

- By Drive Type

- Internal-Combustion Engine

- Electric / Hybrid

- By Rental Duration

- Short-Term

- Long-Term

- By End-User

- Infrastructure (Roads, Rail, Metro)

- Residential & Commercial Real-Estate

- Industrial & Energy

- Mining & Quarrying

Data Sources, Market Sizing, and Validation

Desk Research

To shape the market boundary and build the first set of inputs, we start with public information that tracks construction activity and equipment usage signals. Common reference points include sources such as the Ministry of Road Transport and Highways project updates, National Statistical Office construction and capital formation series, Ministry of Coal and mining statistics, India Infrastructure and project pipeline releases, and customs trade data for equipment categories.

We also review company annual reports, investor presentations, and trusted press coverage to map rental penetration patterns and typical fleet utilization cycles. Where available, paid subscriptions for company financials and intelligence, shipment-level import and export records, and tender and contract databases help cross-check project starts, equipment demand timing, and fleet additions. These desk research sources are illustrative, and we refer to additional materials during data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the model assumptions that desk research cannot fully explain, especially around realized day rates, fleet utilization, and how rental duration shifts across infrastructure, real estate, industrial, and mining work. We speak with rental fleet owners, regional rental houses, dealers with rental arms, contractors, and site managers across key demand pockets in North, West, South, and East India, so the assumptions do not tilt toward one corridor.

These conversations help align price progression with actual billing practices, validate the share of equipment rented with operators, and confirm how quickly fleets are added or retired during heavy project cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | |

| Mid tier: 50% | Functional/Unit leaders: 27% | |

| Smaller Players: 14% | Managers: 60% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where the demand pool is reconstructed from construction output and project activity, then translated into equipment rental needs using rental penetration and typical equipment intensity for major job types. Because the market is rental-led, the model leans on utilization and pricing logic, and then it is checked against selective bottom-up approximations such as sampled fleet counts by equipment class, channel checks on average day rates, and revenue ranges seen for representative rental operators.

Inputs that are tracked and refreshed include infrastructure award and execution pace, equipment operating hours and utilization ranges, typical rental duration mix, realized day rates by key equipment groups, and the share of wet rental where operators and maintenance are billed with the equipment. For forecasting, scenario analysis is used to reflect different project execution outcomes, and the price path is supported by interview consensus on fuel, labor, and maintenance pass-through behavior. Where bottom-up visibility is uneven for small local fleets, gaps are handled by applying region and equipment-specific utilization bands rather than forcing a full operator roll-up.

Data Validation & Update Cycle

Model outputs are validated through triangulation against independent signals such as equipment import trends, major project award flow, and observed rental pricing movement in active corridors. When variances appear, assumptions are rechecked, outliers are challenged, and follow-up calls are triggered to understand whether the change is structural or only timing related.

Before sign-off, the numbers go through multi-step analyst review so scope, units, and conversions remain consistent across the historical series and the forecast. The report is refreshed annually, and interim updates are made when material shifts happen in project pipelines, policy, or input costs. Right before delivery, a final update pass is done so clients receive the most current view available.

Mordor Intelligence's India Construction Equipment Rental Market Size Compared With Other Published Estimates

Published market sizes for India construction equipment rental often do not line up because the scope and the pricing math are treated differently, even when the topic name looks identical. The differences usually come from what gets counted as rental revenue, which year is used for currency conversion, and how fast rental rates are assumed to move.

A refresh-led gap is also common because rental day rates, utilization, and the wet versus dry mix can change within a year, which shifts the value quickly. By keeping FX timing consistent with the stated base year, rechecking ASP progression against recent project demand, and re-contacting sources when price or utilization moves look unusual, Mordor Intelligence lands at a 2026 value that stays tied to observed billing and fleet-use patterns.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.31 B (2026) | |

| Industry Publisher A | USD 12.47 B (2024) | Uses an earlier base year and a longer forecast window, which can embed older utilization and rate levels, and it does not clearly spell out how wet rental and bundled services are treated in revenue. |

| Research Publisher B | USD 2.80 B (2024) | Appears to apply a narrower service boundary or a different revenue recognition approach, which can exclude parts of rental billing like operator and maintenance packages, and it may undercount smaller regional fleets. |

Across the three figures, most of the spread can be explained by base-year timing, what is included as rental revenue, and how rental rates are stepped forward. Our approach keeps assumptions visible, ties pricing to actual rental billing behavior, and uses repeated validation checks so the final number is easier to trace and maintain during updates.

Key Questions Answered in the Report

What is the forecast value of the India construction equipment rental market in 2031?

The market is projected to reach USD 18.33 billion by 2031, advancing at a 5.07% CAGR.

Which vehicle category holds the largest share in India’s rental segment?

Earth-moving machines lead with 63.02% share in 2025 and continue to grow faster than other categories.

How do emission norms influence rental demand?

Stage V regulations effective 2025 drive interest in electric and hybrid rentals, as contractors avoid capex on soon-to-be non-compliant diesel fleets.

Why are long-term rental contracts gaining popularity?

Integrated project planning under PM Gati Shakti makes timelines predictable, allowing contractors to lock in 15-25% cost savings through multi-year rentals.

Which end user will grow fastest through 2031?

Mining and quarrying, supported by ambitious thermal-coal and critical-mineral extraction targets, is projected to grow at 5.16% CAGR.

How fragmented is the competitive landscape?

Highly; most operators manage fewer than 200 machines, giving the market a concentration score of 3 on a 1–10 scale.

Page last updated on: