Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

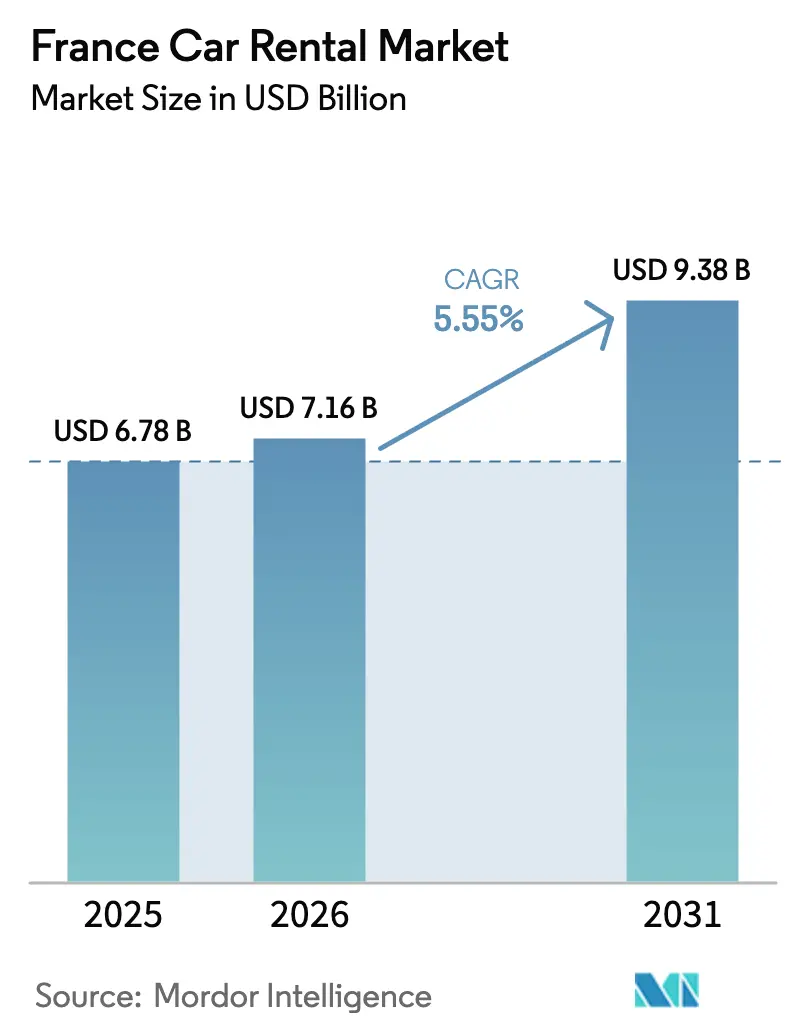

| Base Year Market Size (2025) | USD 6.78 Billion |

| Market Size (2026) | USD 7.16 Billion |

| Market Size (2031) | USD 9.38 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

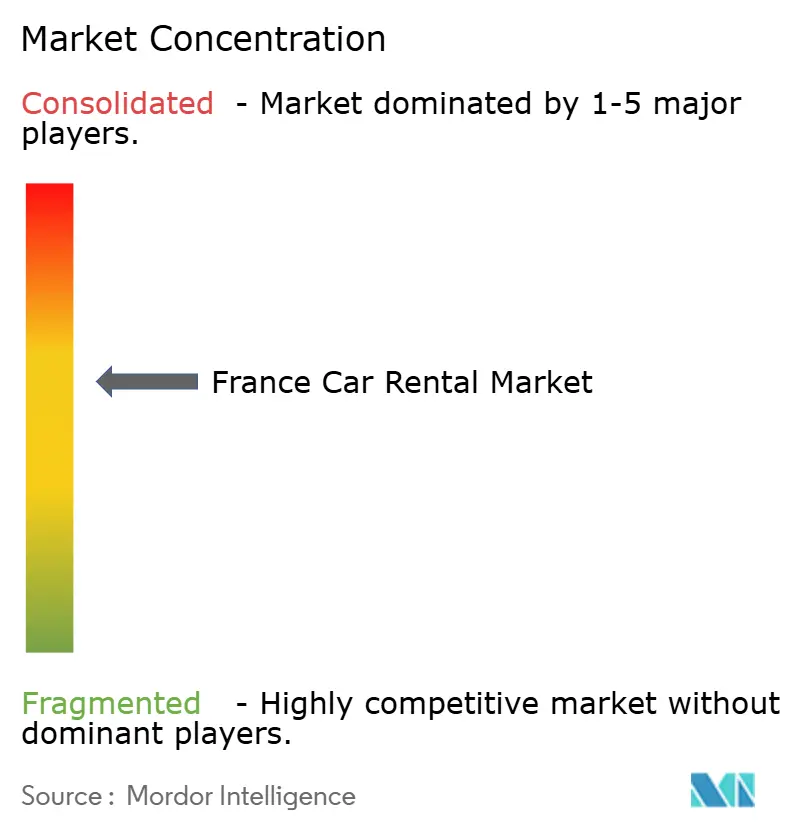

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Car Rental Market Analysis by Mordor Intelligence

The France Car Rental Market size is expected to grow from USD 6.78 billion in 2025 to USD 7.16 billion in 2026 and is forecast to reach USD 9.38 billion by 2031 at 5.55% CAGR over 2026-2031. Robust inbound tourism, stricter low-emission zone rules, and rapid digital adoption sustain this growth path. The market benefits from the 100 million international visitors welcomed in 2024, renewed domestic travel, and the government’s EUR 1.9 billion Destination France program that upgrades tourism assets. At the same time, 25 active low-emission zones that start restricting Crit’Air 3 vehicles in 2025 accelerate fleet renewal toward cleaner powertrains.

Key Report Takeaways

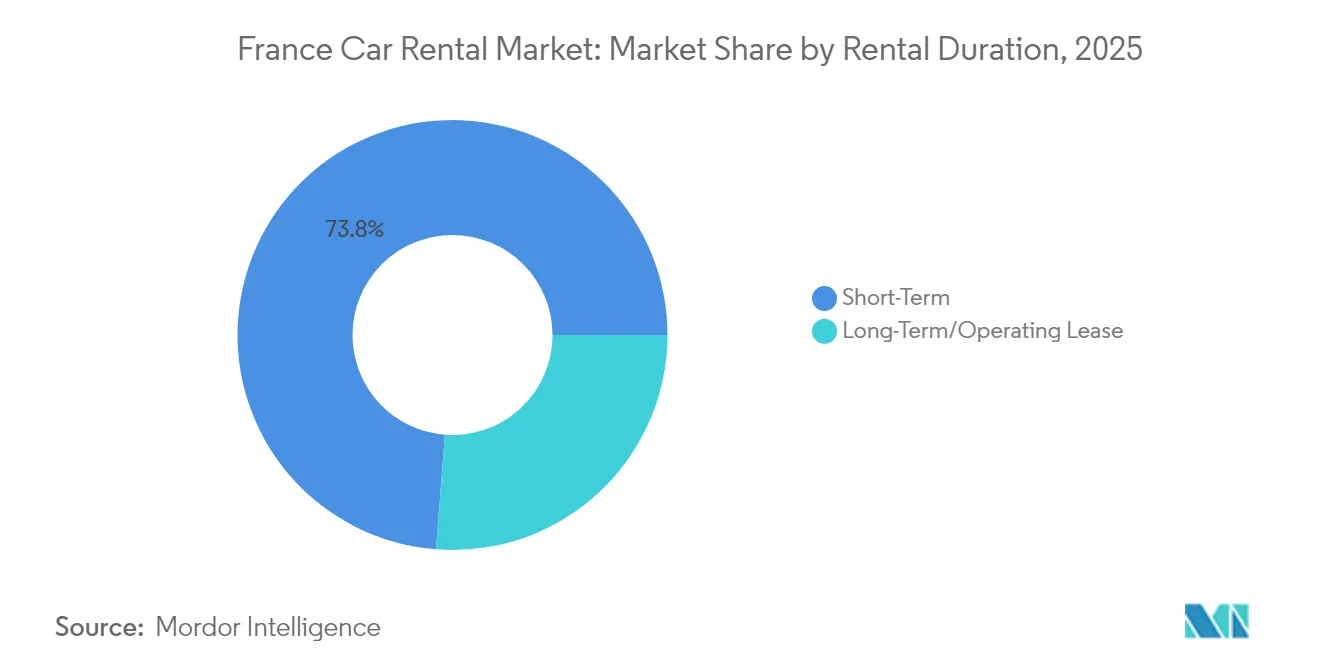

- By rental duration, short-term services held 73.78% of the France car rental market share in 2025, whereas long-term contracts are poised to grow at a 9.05% CAGR through 2031.

- By booking channel, online platforms commanded 64.10% of the France car rental market share in 2025; the same channel is projected to expand at 9.76% CAGR to 2031.

- By application, leisure and tourism accounted for 58.10% of the France car rental market size in 2025, while business and corporate demand is advancing at an 8.55% CAGR.

- By vehicle class, budget and economy cars led with a 68.15% of the France car rental market share in 2025; premium and luxury rentals are forecast to climb at a 12.08% CAGR.

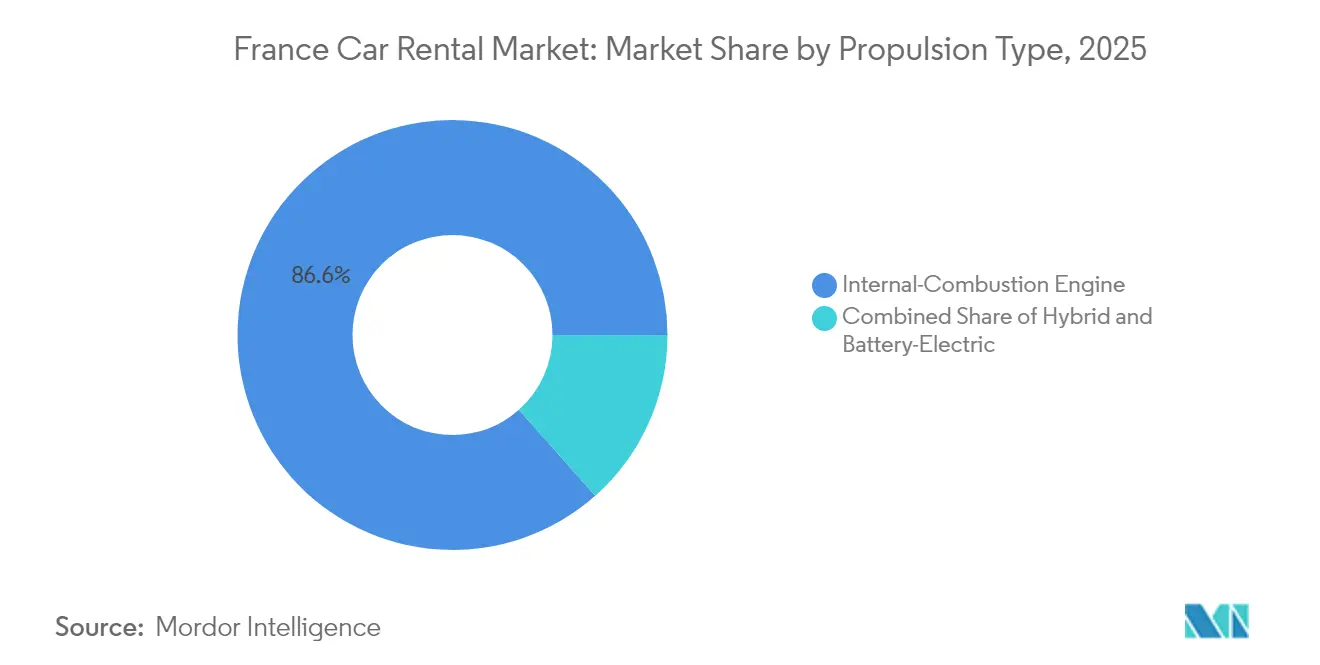

- By propulsion, internal combustion engines still represent 86.55% of the France car rental market share in 2025, yet battery-electric vehicles are growing fastest at a 15.30% CAGR.

- By pickup location, airports supplied 53.05% of the France car rental market share in 2025, whereas off-airport sites are set to post a 9.15% CAGR.

- By client type, individual renters controlled 70.65% of the France car rental market share in 2025, while corporate fleets are expected to rise at an 11.22% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Car Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Inbound and Domestic Tourism Flows | +1.4% | National, with concentration in Paris, Nice, Lyon | Medium term (2-4 years) |

| Surge in On-demand, App-based Booking Platforms | +1.2% | Urban centers, expanding to rural areas | Short term (≤ 2 years) |

| Corporate Demand for Flexible Mobility Solutions | +0.9% | Business districts in Paris, Lyon, Marseille | Medium term (2-4 years) |

| Government Incentives for Electric-Vehicle (EV) Rentals | +0.6% | National, with higher uptake in ZFE cities | Long term (≥ 4 years) |

| ESG-Driven Fleet Electrification Targets of Corporates | +0.5% | Corporate headquarters in major cities | Long term (≥ 4 years) |

| Multi-Modal Packages with Rail and Air Operators | +0.4% | Airport hubs and SNCF stations nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in inbound & domestic tourism flows

Tourism returned to record performance as France hosted 100 million overseas visitors in 2024, generating EUR 71 billion in receipts in the same year.[1]“Où trouver des informations statistiques officielles sur le tourisme ?”, Ministère de l'Économie, economie.gouv.fr The Destination France plan channels EUR 1.9 billion into hospitality upgrades, while events such as the Rugby World Cup and the 2024-25 Olympic cycle elevate global exposure. Rural regions that lack dense public transit particularly benefit as travelers secure cars for winery, heritage, and ski itineraries. The World Travel & Tourism Council projects sector GDP contribution to rise to EUR 310.5 billion by 2034, a signal of durable demand.[2]“France’s Travel & Tourism Broke All Records Last Year,” WTTC, wttc.org This tourism momentum underpins consistent leisure rental volumes and lengthier bookings in secondary cities.

Surge in on-demand, app-based booking platforms

Free2move’s new mobility app aggregates rental, car-sharing, and subscription vehicles, accessing more than 500,000 units worldwide.[3]“Free2move Launches the New Mobility App,” Stellantis, stellantis.com Getaround’s global app overhaul, backed by USD 20 million financing, underscores the competitive edge of mobile-first design. Integrated payment, one-click insurance, and real-time vehicle tracking lower acquisition costs and improve fleet utilization. Traditional agencies lagging on user-interface upgrades risk customer churn as peer-to-peer platforms expand inventory transparency and social reviews.

Corporate demand for flexible mobility solutions

Enterprise clients are migrating from ownership to usage-based contracts. Enterprise Mobility recorded a 15% jump in corporate program membership, citing stronger sustainability alignment and lower total cost of mobility. Mobilize Financial Services expanded operational leases by 35% in H1 2024, financing 101,450 vehicles and targeting a one-million-unit fleet by 2030. Companies favor predictable monthly charges that shift fleet costs from capex to opex while meeting ESG milestones. This tilt increases average revenue per unit and encourages operators to offer bundled charging, telematics, and consolidated invoicing.

Government incentives for electric-vehicle rentals

The EUR 100-per-month social leasing scheme drew more than 90,000 applications in six weeks, forcing a temporary halt and highlighting pent-up demand for affordable EV access. An added EUR 200 million under the ADVENIR program targets 400,000 public chargers by 2030, backing fleet electrification. Battery-electric models therefore post the highest CAGR even though ICE units dominate today. Rental firms that front-load EV acquisitions gain preferential entry to ZFE cities and secure subsidies that cushion total cost of ownership.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Competition | -1.2% | Urban centers, particularly Paris and Lyon | Short term (≤ 2 years) |

| High Operating and Fleet Depreciation Costs | -1.1% | National, affecting all operators | Medium term (2-4 years) |

| Shifts Toward Car-Free Urban Lifestyles | -0.7% | Metropolitan areas with strong public transport | Long term (≥ 4 years) |

| Low-Emission-Zone (ZFE) Restrictions on ICE Rentals | -0.6% | 25 ZFE cities, expanding to 40+ by 2025 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying competition from ride-hailing & car-sharing

Ride-hailing apps and car-sharing fleets erode traditional rental share in dense urban cores. Turo’s acquisition of peer-to-peer pioneer OuiCar added thousands of privately owned cars available from EUR 20 per day, widening price points and vehicle variety. Getaround’s Europe-focused overhaul, combined with Heetch’s licensed nighttime services, raises convenience expectations among millennial users. This competitive mix compresses margins at airport counters and forces incumbents to bundle loyalty perks, valet delivery, or premium subscription tiers that justify higher daily rates.

High operating & fleet depreciation costs

Financing rates jumped from 2% to 8% between 2022 and 2024, inflating vehicle holding costs across the France car rental market. Hertz’s decision to sell 20,000 EVs and record a USD 245 million impairment underscores risk when battery models face unexpected repair bills and residual value swings. Automakers are prioritizing higher-trim production, which compels rent-a-cars to acquire costlier vehicles that may not align with economy travelers. Smaller operators unable to absorb depreciation volatility are poised to exit, tightening supply but also concentrating bargaining power among major brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rental Duration: Long-Term Gains Momentum

Short-term hire retained 73.78% share of the France car rental market in 2025, a reflection of tourist-heavy demand patterns. Nonetheless, long-term and operating leases are projected to expand at 9.05% CAGR and will lift the France car rental market size for contracted rentals to USD 2.28 billion by 2031. Adoption is driven by corporate fleet outsourcing and subscription programs that sidestep depreciation risk.

Long-term contracts appeal to businesses that track emissions under ESG targets and require predictable monthly charges. Mobilize Financial Services’ portfolio growth demonstrates the shift, while leisure travelers continue to favor day-based rentals for quick getaways. The France car rental market therefore balances steady tourist volume with higher-margin corporate agreements.

By Booking Channel: Digital Dominance Accelerates

Online portals delivered 64.10% of the France car rental market share in 2025 and will add another USD 1.62 billion to the France car rental market size by 2031. The channel’s 9.76% CAGR is sustained by mobile payments, biometrics, and instant damage recording that cut counter wait times.

Offline counters at airports and train stations still attract walk-in customers and travelers unfamiliar with local apps. Yet most incumbents now pursue omnichannel strategies, ensuring that the same promotion codes, loyalty points, and optional coverages align across digital and physical points of sale, preserving brand consistency.

By Application: Business Segment Emerges

Leisure travel contributed 58.10% of France car rental market revenue in 2025, anchored by resilient tourism flows. Corporate travel, however, grows faster at an 8.55% CAGR and will nudge its share to nearly one-third of the France car rental market size by 2031.

Company travel policies increasingly substitute mileage reimbursement with on-demand rental allowances or pooled subscription vehicles. Integrated expense software and centralized billing shorten administration cycles and incentivize finance departments to switch from gray-fleet arrangements.

By Vehicle Class: Premium Segment Accelerates

Budget and economy cars comprised 68.15% of the France car rental market share in 2025, yet premium and luxury models climb at a 12.08% CAGR, lifting their slice of France car rental market value by 2031. High-net-worth travelers on the French Riviera and corporate executives on tight itineraries request advanced safety tech, brand prestige, and concierge delivery.

Economy units remain indispensable for cost-sensitive backpackers and domestic road trippers, but margin compression persists as fuel prices and insurance outlays outpace daily rates. Operators offset this by upselling GPS, child seats, and zero-excess packages.

By Propulsion Type: Electric Revolution Begins

Internal combustion vehicles still hold an 86.55% France car rental market share in 2025 because of lower acquisition costs and dense refueling infrastructure; however, tightening emissions rules and corporate ESG mandates push fleets toward hybrids and full electrics. Plug-in hybrids offer a transitional option for long-distance travelers wary of charge-point queues, while connected-car data lets agencies monitor state of charge and reroute vehicles to fast chargers during idle time.

Battery-electric vehicles contributed little to overall rentals in 2025, but they delivered the segment’s fastest CAGR at 15.30%, setting the France car rental market size for EV fleets on a path to nearly triple by 2031.

By Pickup Location: Off-Airport Gains Traction

Airport counters generated 53.05% of 2025 France car rental market share and remain the entry point for most long-haul visitors due to integrated desks at Charles de Gaulle, Orly, Lyon–Saint-Exupéry, and Marseille Provence terminals. These locations benefit from established shuttle loops and airline codeshare promotions, locking in high-margin ancillary sales such as zero-excess insurance and GPS units.

Off-airport branches already post a 9.15% CAGR and are forecast to capture an additional USD 675 million of France car rental market size by 2031. Operators deploy digital key boxes in hotel lobbies, railway stations, and underground garages, trimming shuttle costs and freeing scarce airport real estate for premium upgrades.

By Client Type: Corporate Growth Accelerates

Individual renters accounted for 70.65% of total France car rental bookings in 2025, driven by France’s record 100 million tourist arrivals and a domestic culture that favors weekend road trips. Tourists typically opt for compact petrol cars to manage fuel costs and avoid unfamiliar charging etiquette, preserving volume and baseline fleet turnover. Families booking in advance through airline portals still generate the bulk of prepaid revenue and fill vehicles with high mileage during summer peaks.

Corporate fleet customers, though still smaller, are expanding at an 11.22% CAGR and will lift their slice of France car rental market share to almost one-third by 2031. Enterprise Mobility’s 15% annual jump in French corporate memberships stems from ESG-linked reporting tools that track CO₂ per kilometer and consolidate invoices for finance teams.

Geography Analysis

The French car rental market revolves around Île-de-France, with Paris airports serving as gateways for bookings. Charles de Gaulle facilitates multi-brand pick-up plazas where global loyalty members bypass counters through smartphone verification. Lyon and Marseille emerge as secondary hubs, combining robust corporate districts and expanding cruise traffic that feeds weekend rentals.

Southeast regions led by Nice, Cannes, and Monaco command premium rates, often 45% above the national daily average, due to their concentration of luxury tourism. Winter peaks in Alpine départements double fleet utilization for SUVs fitted with snow chains, while Bordeaux and Burgundy wineries drive shoulder-season demand.

ZFE rollout introduces a patchwork of compliance requirements. Paris and Lyon begin Crit’Air 3 restrictions in 2025, compelling operators to allocate newer Euro 6 or electric vehicles to these cities. Service design therefore adapts: fleets rotate older diesels toward rural branches and move EVs to urban depots equipped with fast chargers. Operators with nationwide networks gain efficiency by repositioning assets around evolving local rules.

Competitive Landscape

The France car rental market is moderately concentrated. International majors—Enterprise Holdings, Hertz, Europcar Mobility Group, and SIXT—leverage airport concessions, scale purchasing power, and recognizable brands. SIXT’s order for up to 250,000 Stellantis cars ensures connected vehicles and fuels European expansion while phasing out Teslas due to high repair bills. Enterprise Mobility posted record global revenue above USD 38 billion in FY24, achieving double-digit growth in France through technology upgrades and differentiated service tiers.

Digital challengers intensify rivalry. Free2move’s integrated app now covers rental, car-sharing, and subscription from a single login, reflecting convergence of mobility products. Peer-to-peer sharing gains legitimacy after Turo’s acquisition of OuiCar, adding community trust and nationwide insurance packages.

Rising capital requirements from fleet electrification and the need for advanced telematics likely push smaller independents toward exit or acquisition. Meanwhile, premium positioning and flexible subscriptions provide revenue resilience for brands that can sustain investment in both EV infrastructure and intuitive apps.

France Car Rental Industry Leaders

SIXT SE

Avis Budget Group

The Hertz Corporation

Europcar Mobility Group

Enterprise Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Free2move launched an integrated mobility app offering access to more than 500,000 vehicles worldwide, combining car-sharing and rental functions and illustrating platform convergence.

- February 2024: The French government temporarily suspended its EUR 100-per-month electric-vehicle social leasing scheme after receiving over 90,000 applications, twice the initial allocation.

- January 2024: SIXT reached agreement with Stellantis for purchase of up to 250,000 vehicles through 2026, supporting global expansion strategy and fleet electrification goals while phasing out Tesla vehicles due to high repair costs.

France Car Rental Market Report Scope

Car renting refers to the business of leasing and renting a car from rental service providers based on some valuation. This renting can be on an hourly basis or for a longer time span.

The car renting market is segmented by rental duration type, booking type, application type, driving type, and vehicle type. By rental duration type, the market has been segmented into short-term and long-term. By booking type, the market has been segmented into online and offline. By application type, the market has been segmented into leisure/tourism and business and by vehicle type, the market is segmented into budget/economy and premium/luxury. For each segment, the market sizing and forecasting are based on value (USD billion).

By Rental Duration

| Short-Term (Less than or equal to 30 days) |

| Long-Term / Operating Lease (More than 30 days) |

By Booking Channel

| Online |

| Offline |

By Application

| Leisure / Tourism |

| Business / Corporate |

By Vehicle Class

| Budget / Economy |

| Premium / Luxury |

By Propulsion Type

| Internal-Combustion Engine |

| Hybrid |

| Battery-Electric |

By Pickup Location

| Airport |

| Off-Airport (Rail-Station, Downtown, Hotel, etc.) |

By Client Type

| Individual |

| Corporate Fleet |

| By Rental Duration | Short-Term (Less than or equal to 30 days) |

| Long-Term / Operating Lease (More than 30 days) | |

| By Booking Channel | Online |

| Offline | |

| By Application | Leisure / Tourism |

| Business / Corporate | |

| By Vehicle Class | Budget / Economy |

| Premium / Luxury | |

| By Propulsion Type | Internal-Combustion Engine |

| Hybrid | |

| Battery-Electric | |

| By Pickup Location | Airport |

| Off-Airport (Rail-Station, Downtown, Hotel, etc.) | |

| By Client Type | Individual |

| Corporate Fleet |

Key Questions Answered in the Report

What is the current size of the France car rental market and how fast is it growing?

The market is worth USD 7.16 billion in 2026 and is forecast to reach about USD 9.38 billion by 2031 on a 5.55% CAGR trajectory.

Which factors are driving the strongest demand for rental cars in France?

Record tourism of 100 million overseas visitors in 2024, the EUR 1.9 billion Destination France program, and 64.10% online booking uptake are the main growth engines.

How quickly are electric vehicles gaining share in French rental fleets?

Battery-electric rentals are advancing at a 15.30% CAGR and are expected to nearly triple their fleet footprint by 2031, helped by EV leasing incentives and expanding charge points.

What impact will low-emission zones (ZFE) have on rental operations?

From January 2025, 25 ZFEs will restrict Crit’Air 3 cars, compelling agencies to deploy cleaner vehicles but granting those fleets unrestricted city-center access.

Why are off-airport pickup sites becoming more popular?

Off-airport locations are growing at a 9.15% CAGR as travelers avoid congestion fees and favor digital key boxes in city centers for faster, cheaper vehicle release.

How fast is corporate demand for rental cars expanding?

Corporate fleet clients are rising at an 11.22% CAGR through 2031, driven by companies replacing owned cars with long-term rental contracts that include CO₂ tracking and consolidated billing.

Page last updated on: