Hyper Car Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

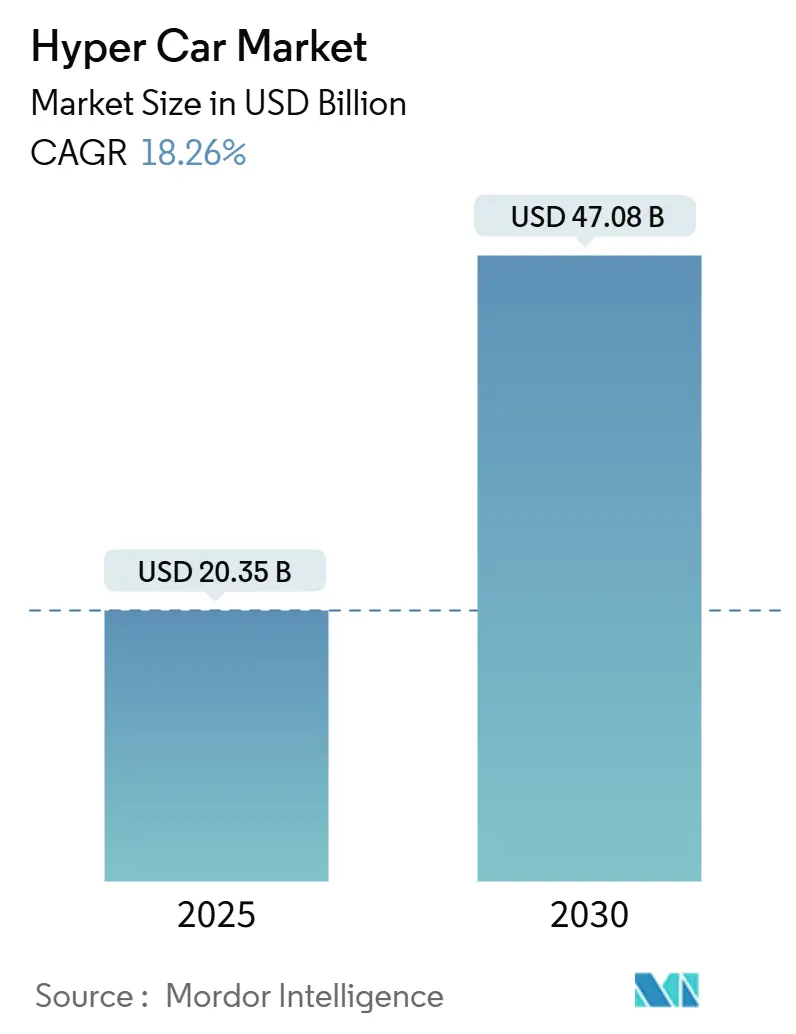

| Market Size (2025) | USD 20.35 Billion |

| Market Size (2030) | USD 47.08 Billion |

| Growth Rate (2025 - 2030) | 18.26% CAGR |

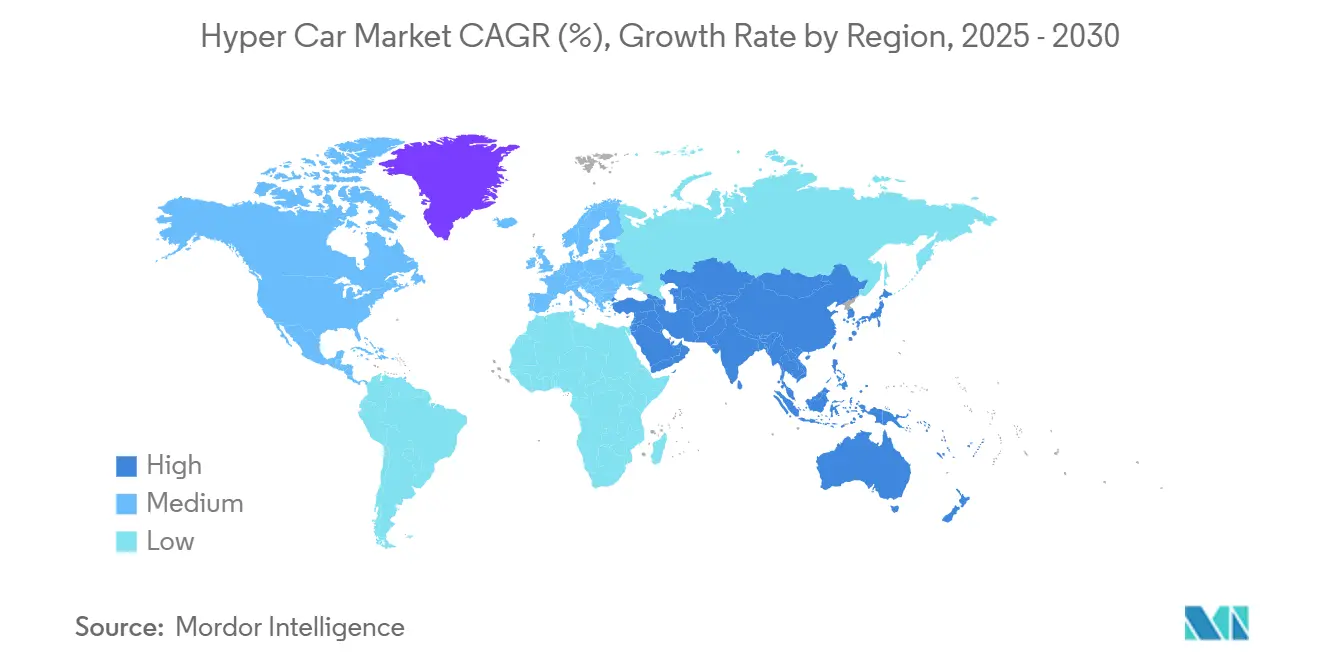

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

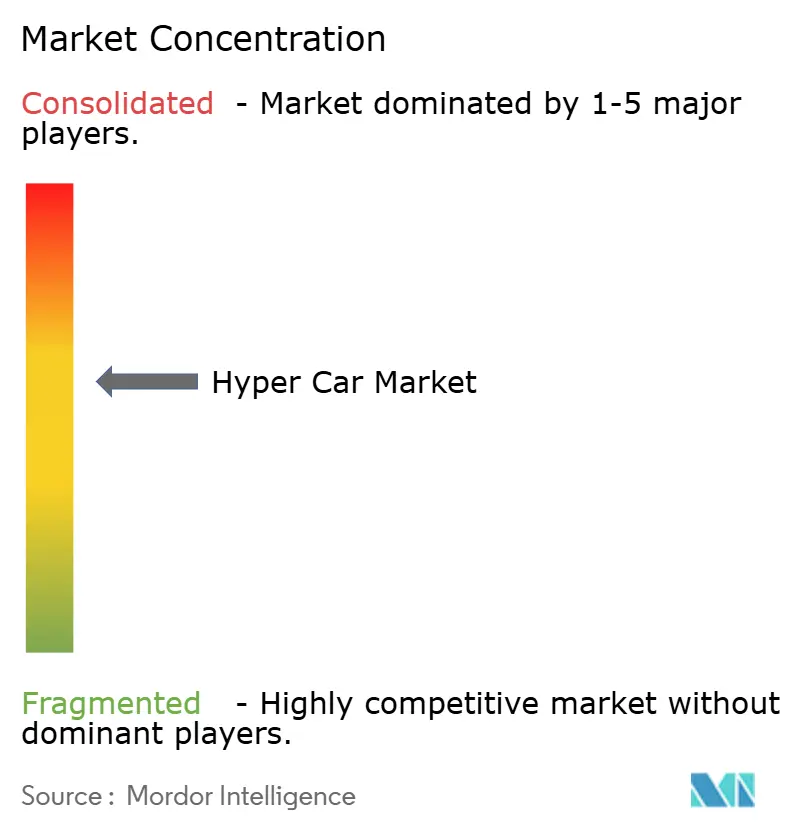

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hyper Car Market Analysis by Mordor Intelligence

The Hyper Car Market size is estimated at USD 20.35 billion in 2025, and is expected to reach USD 47.08 billion by 2030, at a CAGR of 18.26% during the forecast period (2025-2030). Wealth creation among ultra-high-net-worth buyers, technological spillovers from Formula 1, and rising acceptance of electrified drivetrains continue to propel value growth despite broader automotive volatility. Europe remains the epicenter of design and engineering excellence. At the same time, Asia Pacific evolves into the fastest-expanding demand node as crypto-wealth and family-office capital seek tangible, status-laden assets. Battery-electric hypercars prove that zero-emission propulsion can amplify rather than dilute performance, which shifts the competitive narrative from engine displacement to software-enabled power management. Supply-chain advantages in aerospace-grade composites and titanium sourcing increasingly define strategic differentiation, prompting vertically integrated players to lock in long-term contracts with material suppliers.

Key Report Takeaways

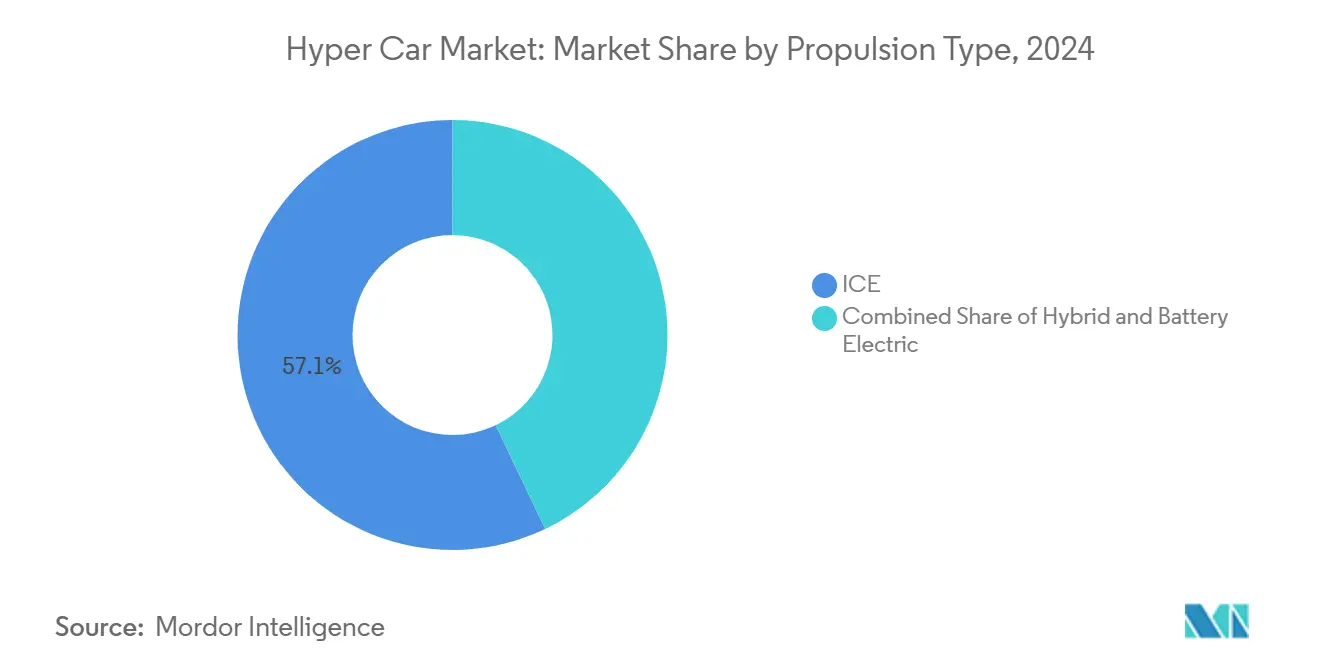

- By propulsion type, internal combustion engines led the hypercar market with 57.13% of the share in 2024, whereas battery-electric variants are advancing at an 18.28% CAGR through 2030.

- By end use, private ownership accounted for an 84.45% share of the hypercar market size in 2024, and racing programs are climbing at an 18.31% CAGR through 2030.

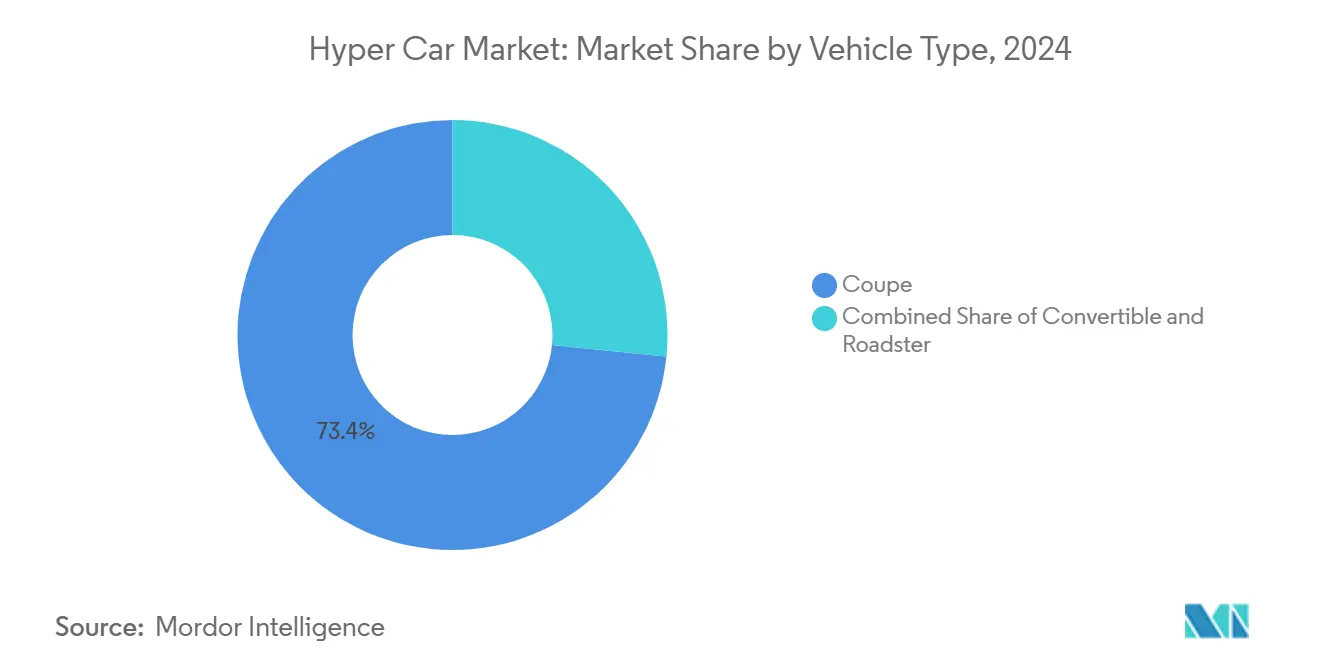

- By vehicle type, coupes controlled 73.41% of the hypercar market share in 2024, while roadsters are on course for an 18.33% CAGR to 2030.

- By engine capacity, powertrains above 2,500 cc held 86.81% of the hypercar market share in 2024, whereas sub-1,500 cc configurations are projected to expand at 18.34% CAGR to 2030.

- By region, Europe captured 38.77% of the hypercar market share in 2024, and Asia Pacific is forecast to register the quickest 18.37% CAGR through 2030.

Global Hyper Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Ultra-High-Net-Worth Individuals | +3.5% | Asia Pacific core, Middle East, spill-over to Europe | Short term (≤ 2 years) |

| Rising Demand For Ultra-Luxury Vehicles | +3.2% | Global, with concentration in North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Rapid Electrification | +2.8% | Global, led by Europe regulatory push, Asia Pacific adoption | Long term (≥ 4 years) |

| Breakthroughs In Lightweight Composite Structures | +2.1% | Global, manufacturing centers in Europe, North America | Medium term (2-4 years) |

| AI-Driven Aerodynamic Shortening Development Cycles | +1.9% | Global, R&D centers in Europe, North America | Long term (≥ 4 years) |

| NFT-Linked Limited Editions Unlocking New Buyer Pools | +1.7% | Global, concentrated in tech hubs and financial centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Ultra-High-Net-Worth Individuals in Asia Pacific and Middle East

According to local government migration filings, Dubai added almost four-fifths more ultra-rich residents in 2024, forming clusters of buyers willing to pay premiums for immediate delivery slots[1]“Annual Wealth Migration Report 2024,” Government of Dubai, dubai.gov.ae . Singapore recorded an uptick in luxury car registrations, even with strict Certificates of Entitlement, showing demand elasticity when status considerations eclipse cost[2]“Monthly Vehicle Statistics 2024,” Land Transport Authority Singapore, lta.gov.sg. Dealers such as Eurokars invested a considerable amount in regional showrooms to seize this momentum, and OEMs tailor paint-to-sample programs incorporating regional cultural motifs. Favorable import-duty treatment for limited-production vehicles in the Gulf Cooperation Council accelerates cross-border purchases, turning the Middle East into a secondary logistics hub next to Europe. The spatial re-distribution of wealth obliges brands to deepen after-sales footprints in Asia rather than rely solely on European factory deliveries.

Rising Demand for Ultra-Luxury High-Performance Vehicles

Ultra-high-net-worth collectors increasingly regard limited-run hypercars as portable stores of value that hedge against monetary debasement. Dealer allocations for Ferrari’s F80, priced at a reasonable rate, sold out before the public reveal, underscoring demand that chronically overshoots supply[3]“F80 Technical Specifications,” Ferrari S.p.A., ferrari.com. The global stock of collectible automobiles has swelled, and auction data show hypercars appreciating faster than comparable asset classes such as fine art and vintage watches. Manufacturers now examine subscription and fractional-ownership models that preserve exclusivity while broadening the addressable audience. Because values held steady through recent macro-shocks, buyers perceive hypercars as alternative investments rather than discretionary purchases, further anchoring long-term demand.

Rapid Electrification & Hybridization of Hypercars

Electric assistance enables power densities unreachable by combustion alone, repositioning electrification as a performance upgrade instead of a regulatory concession. The Rimac Nevera delivers 1,914 HP with instant torque, while Ferrari’s hybrid F80 couples a 3.0-liter V6 with three motors for 1,184 HP. OEMs tap Formula 1 battery expertise through suppliers like Williams Advanced Engineering, lowering the entry barrier for niche brands that cannot bankroll in-house cell programs. Ultra-fast chargers rated at 1 MW from BYD and 1.2 MW from Zeekr reduce range anxiety and track downtime, making pure-electric usage practical for wealthy owners with private charging suites. Zero-emission zones across major European capitals further strengthen the case for battery-electric hypercars that retain unrestricted urban access.

Breakthroughs in Lightweight Composite & Carbotanium Structures

Pagani’s carbotanium weave cuts chassis mass by two-fifths versus conventional carbon fiber while raising torsional rigidity, enabling higher cornering loads without compromising crashworthiness. Additive manufacturing allows Czinger to 3-D-print titanium subframes with geometry that is impossible under subtractive methods, trimming packaging volume and shortening tooling lead times. Graphene-enhanced panels improve heat dissipation around battery packs, an essential capability as EV hypercars push discharges well above 1 MW. Competition with aerospace and defense sectors for the same autoclave capacity intensifies supply tension, favoring builders that have secured multi-year composite contracts. The net result is lighter shells that offset battery penalties, yielding power-to-weight ratios unmatched by previous generations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extremely High R&D Cost | -2.9% | Global, concentrated in high-cost manufacturing regions | Medium term (2-4 years) |

| Supply-Chain Scarcity Of Aerospace-Grade Composites | -2.4% | Global, manufacturing bottlenecks in specialized facilities | Medium term (2-4 years) |

| Stringent Global Emissions | -2.1% | Europe, North America, expanding to Asia Pacific | Long term (≥ 4 years) |

| Immature Ultra-Fast-Charging Infrastructure | -1.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Extremely High R&D and Manufacturing Cost Base

Program budgets for next-generation hypercars can surpass the allocated amount due to powertrain validation, active-aero testing, and homologation across multiple jurisdictions. McLaren disclosed a GBP 276 million pre-tax loss in its latest fiscal year, with much of the deficit linked to product-development expenditures. Tesla’s 2024 R&D outlay has grown exponentially over the past few years, demonstrating the capital scale required to remain competitive at the technology frontier. However, hypercar builders lack volume amortization to dilute such costs. Digital-twin engineering trims development cycles from seven to roughly four years but necessitates heavy investment in simulation infrastructure upfront. Consequently, smaller marques seek joint ventures and component sharing to spread fixed expenses across more derivatives.

Supply-Chain Scarcity of Aerospace-Grade Composites & Titanium

Defense procurement of carbon prepreg and 6-Al-4-V titanium spikes during geopolitical tensions, squeezing civilian allocations and stretching lead times above 24 months for specific weave patterns. Hypercar OEMs sometimes stockpile raw rolls or lock in take-or-pay contracts to shield against price surges. When shortages bite, builders with vertically integrated autoclaves can prioritize their chassis while competitors defer launches, altering model-cycle cadence. The geographic concentration of smelting and resin facilities in Japan, the United States, and Germany introduces freight risk that became apparent during recent Red Sea shipping disruptions. Brands, therefore, explore recycled aerospace scrap and in-house filament winding to lessen vulnerability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Electric Acceleration Despite ICE Dominance

Internal combustion engines retained a 57.13% slice of the hypercar market in 2024, underscoring enduring buyer affinity for mechanical theatrics and exhaust timbre. Battery-electric competitors are climbing by 18.28% CAGR as real-world demonstrations show that instant torque elevates lap-time competitiveness without compromising range when paired with 800-V architectures. Hybrid powertrains act as transitional solutions that blend smaller displacement blocks with torque-vectoring e-axles to meet tightening emissions rules yet keep visceral driver feedback. OEMs extract additional margin through over-the-air software unlocks of performance modes, creating recurring revenue streams that did not exist under pure ICE economics. Racing series homologation also accelerates electric adoption because governing bodies increasingly award Balance-of-Performance allowances to lower-emission entrants.

Weight distribution remains the chief engineering hurdle for full electric platforms, but widespread carbon monocoques mitigate pack mass while preserving torsional stiffness. Williams Advanced Engineering’s skateboard chassis provides a turnkey entry point for niche brands, compressing program gestation to roughly 36 months. Ultra-fast chargers at 1 MW now populate private circuits in Abu Dhabi and Shanghai, allowing affluent owners to replenish almost four-fifths in under 12 minutes, nullifying earlier range apprehensions. Policy incentives such as zero-emission zones within central London and Paris further tilt long-term demand toward BEVs.

By End Use: Private Ownership Drives Volume While Racing Gains Momentum

Private collectors dominated with an 84.45% share of the hypercar market size in 2024, as vehicles function as portfolio diversifiers and social capital signals. Many buyers add bespoke one-of-five commissions that appreciate once allocations close, reinforcing scarcity value. Despite this lead, track homologation rules under Le Mans Hypercar and IMSA GTP stimulate an 18.31% CAGR in purpose-built racers, which must spawn road-legal twins. The cross-pollination lowers cost per unit by spreading powertrain R&D across street and circuit derivatives. Manufacturers also monetize factory-run client racing academies that charge six-figure participation fees, turning motorsport programs into profit centers.

The underlying business model for racing editions hinges on faster refresh cycles that keep attention on brand heroics. Ferrari’s 499P Le Mans triumph elevated resale premiums for its related road cars by double-digit percentages within six months of the win. Porsche targets Nürburgring record lifts for the upcoming Mission X to validate engineering bragging rights. Private owners likewise demand track telemetry suites and concierge logistics, which further blend recreational and competitive use cases. As circuit infrastructures proliferate in the UAE, China, and the United States, the addressable buyer pool for track-ready hypercars expands beyond professional drivers.

By Vehicle Type: Coupes Lead While Roadsters Command Premium Pricing

Coupes claimed 73.41% of the hypercar market size in 2024, exploiting their inherently favorable drag coefficients and torsional rigidity that permit aggressive aero loads. Roadsters rise at 18.33% CAGR through 2030, buoyed by consumer willingness to pay around one-fifths surcharges for open-air exhilaration that complements performance credentials. Engineering challenges around chassis flex are mitigated via carbon-fiber reinforcement rings and active-aero flaps that counter lift at speed. The McLaren Speedtail’s elongated teardrop proves that slipper shapes can coexist with convertible formats when form-finding uses CFD from the outset. Retractable hardtops integrate magnesium panels to limit unsprung mass, ensuring cornering balance remains intact when roofs stow.

Advances in electrochromic glazing allow roadsters to tint roofs instantly, narrowing climate-control gaps relative to coupes and enhancing daily usability. Pagani’s Huayra R Evo demonstrates that modern autoclaves can cure complex roll-over structures in single pieces, trimming assembly hours and raising structural consistency. Because affluent customers often keep multiple hypercars, roadsters rarely cannibalize coupe uptake; instead, they unlock incremental spend inside the same garages. Over time, OEM portfolios will likely twin every flagship coupe with a roadster variant to maximize sticker differentiation without additional powertrain investment.

By Engine Capacity: Large Displacement Dominates Despite Compact Growth

Powerplants exceeding 2,500 cc held 86.81% of the hypercar market share in 2024, reflecting historical associations between displacement and prestige. Yet sub-1,500 cc systems that rely on turbo compounding and electric boost are scaling at an 18.34% CAGR as they deliver equal or greater specific output with lower taxable displacement. Regulatory structures in markets such as Singapore levy engine-capacity-linked fees that favor downsized blocks when performance parity exists, accelerating acceptance.

Packaging benefits also arise because smaller engines lower the center of gravity and leave room for aerodynamic tunnels under rear decks. Compact hybrids can outperform large-bore engines on torque vectoring, granting higher exit speeds out of hairpins when combined with axial-flux motors. High-output alternators running 48-V electrical systems further downsize auxiliary loads and improve transient response. For buyers, the emotional pull of big cylinders remains, but performance quantification via telemetry is shifting loyalty toward whichever configuration posts a faster lap, irrespective of displacement branding.

Geography Analysis

Europe’s 38.77% of the hypercar market share in 2024 underscores the region’s fusion of heritage craftsmanship, motorsport technology, and discerning clientele concentrated in Italy, Germany, France, and the United Kingdom. Engineering collaborations with Formula 1 suppliers within the same industrial corridors enable faster iteration loops, allowing new models to debut every three to four years without diluting exclusivity. Tourist-friendly driving events along the French Riviera also sustain experiential marketing that anchors brand loyalty among legacy collectors.

Asia Pacific’s 18.37% CAGR trajectory reflects unprecedented economic ascendancy among technology entrepreneurs, crypto founders, and second-generation family offices. Mainland Chinese demand cooled for mainstream luxury sedans yet pivoted toward hypercars that carry cultural cachet through limited allocations and track credentials. Ultra-fast expressways in the Pearl River Delta support legal high-speed events that serve as rolling adverts for brands eager to showcase top speed superiority. Regulatory waivers for limited-production imports in the Gulf Cooperation Council attract Asia Pacific buyers who split residence between Singapore and Dubai, increasing vehicle transfers across continents.

North America maintains volume steadiness, supported by a robust collector-car culture that values provenance documentation and auction transparency. Technology CEOs in Silicon Valley routinely commission bespoke colorways that later fetch premiums on the secondary market. Texas oil capital cultivates a track-day scene centered around private circuits such as MSR Houston, encouraging owners to extract full performance potential. While U.S. federal rules permit low-volume exemptions, California’s Air Resources Board sets additional benchmarks that nudge builders toward plug-in hybrids for Golden State compliance. Canada experiences spillover demand concentrated in Toronto and Vancouver, where strong immigrant capital inflows fuel appetite for rolling art pieces that double as hedge assets.

Competitive Landscape

Competitive intensity is moderate because astronomical tooling budgets and regulatory compliance costs deter casual entrants. Ferrari, McLaren, Lamborghini, Bugatti, and Porsche preserve their incumbency through continuous motorsport participation, translating upgrades to limited-run road cars. Rimac, Aspark, and Czinger inject fresh rivalry by leveraging electric drivetrains, additive manufacturing, and AI-based aerodynamics to sidestep conventional cost curves. Vertical integration in battery modules, carbon prepreg, and titanium milling becomes a strategic moat as raw-material shortages loom. Companies that command in-house autoclaves and motor winding lines secure higher gross margins and delivery reliability.

Platform modularity rises as a hedge against spiraling R&D. Williams Advanced Engineering licenses a skateboard chassis usable by boutique brands for both coupe and roadster applications, slicing development time and letting newcomers focus capital on design differentiation. Incumbents answer by reusing hybrid drive units across successive launches, compounding learning curves and lowering warranty risk. Subscription models have begun to appear, allowing owners to rotate among different hypercars under manufacturer-managed fleets, which retain ownership and handle maintenance.

Strategic investments redefine ownership structures. CYVN Holdings acquired McLaren Automotive in April 2025, injecting liquidity that underwrites next-generation electrified models without diluting brand autonomy[4]“CYVN Holdings Investment Announcement,” McLaren Group, mclaren.com . Partnerships with semiconductor firms accelerate the shift to domain-controller architectures that permit real-time over-the-air updates, enhancing resale desirability. As emissions regimes tighten, competitive performance will hinge less on raw horsepower and more on integrated software that governs torque vectoring, energy recuperation, and active aero in millisecond cycles.

Hyper Car Industry Leaders

Ferrari

Bugatti Rimac

Automobili Lamborghini

McLaren

Porsche

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: CYVN Holdings completed its acquisition of McLaren Automotive and a non-controlling stake in McLaren Racing.

- October 2024: Ferrari took the wraps off its F80 hybrid hypercar, showcasing its commitment to innovation and sustainability in the automotive industry. The F80 combines cutting-edge hybrid technology with Ferrari's signature performance and design excellence, setting a new benchmark for hypercars.

- July 2024: Red Bull unveiled the RB17, a hypercar designed specifically for the track. This high-performance vehicle showcases advanced engineering and cutting-edge technology, emphasizing Red Bull's commitment to innovation in motorsport. The RB17 is expected to deliver exceptional speed and handling, catering to enthusiasts seeking a premium track experience.

Global Hyper Car Market Report Scope

| ICE |

| Hybrid |

| Battery Electric |

| Private |

| Racing |

| Coupe |

| Convertible |

| Roadster |

| Compact (Less than 1500 cc) |

| Mid-size (1500–2500 cc) |

| Full-size (More than 2500 cc) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Propulsion Type | ICE | |

| Hybrid | ||

| Battery Electric | ||

| By End Use | Private | |

| Racing | ||

| By Vehicle Type | Coupe | |

| Convertible | ||

| Roadster | ||

| By Engine Capacity | Compact (Less than 1500 cc) | |

| Mid-size (1500–2500 cc) | ||

| Full-size (More than 2500 cc) | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the 2025 value of the hypercar market?

The hypercar market size reached USD 20.35 billion in 2025.

How fast is the segment projected to grow?

Aggregate revenue is expected to increase by 18.26% CAGR from 2025 to 2030.

Which region is expanding the quickest in demand?

Asia Pacific is forecast to post the highest 18.37% CAGR through 2030 on the back of UHNW population growth.

What propulsion type is seeing the fastest uptake?

Battery-electric hypercars lead growth with an 18.28% CAGR due to performance gains and zero-emission rules.

Which body style currently commands the most significant share?

Coupe configurations held 73.41% of 2024 sales due to aerodynamic and structural advantages.

What is the primary barrier for new entrants?

High development costs create high financial hurdles that limit competitive entry.

Page last updated on: