Supercars Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

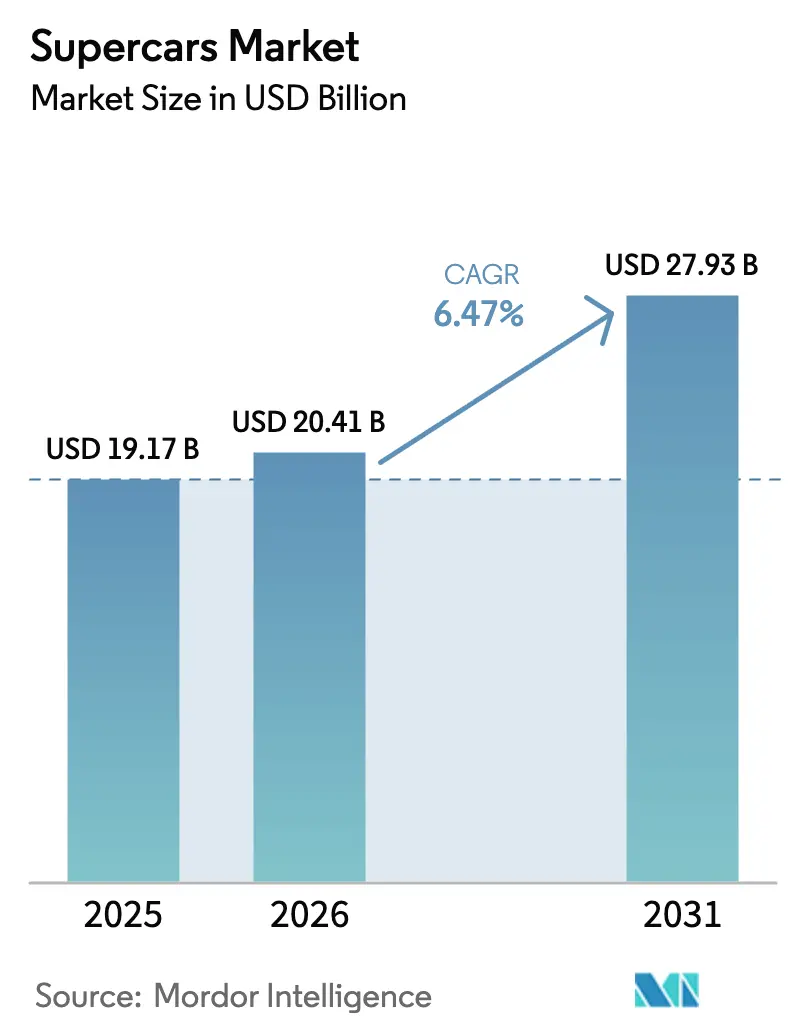

| Market Size (2026) | USD 20.41 Billion |

| Market Size (2031) | USD 27.93 Billion |

| Growth Rate (2026 - 2031) | 6.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Supercars Market Analysis by Mordor Intelligence

The Supercars market size is expected to grow from USD 19.17 billion in 2025 to USD 20.41 billion in 2026 and is forecast to reach USD 27.93 billion by 2031 at 6.47% CAGR over 2026-2031. Surging cryptocurrency fortunes, rising numbers of ultra-high-net-worth individuals, and performance-enhancing hybrid technologies are lifting demand even as economic headwinds persist. Non-convertible body styles and internal-combustion (IC) engines still dominate volumes, yet convertibles and battery-electric variants are growing fastest, underlining a shift toward experiential and sustainable luxury.

Key Report Takeaways

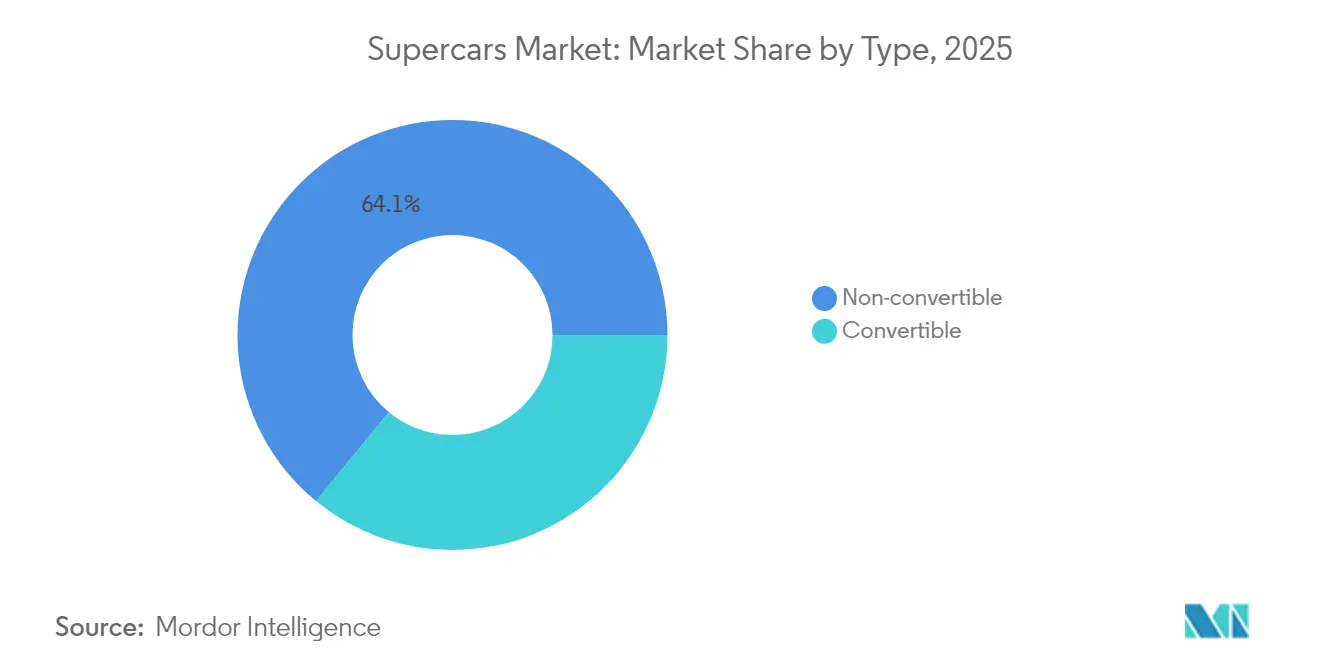

- By type, non-convertibles held 64.05% of the supercars market share in 2025, while convertibles are set to record the fastest 6.53% CAGR to 2031.

- By propulsion, IC engines accounted for 72.85% of the supercars market size in 2025; battery-electric models are on track for a 7.02% CAGR through 2031.

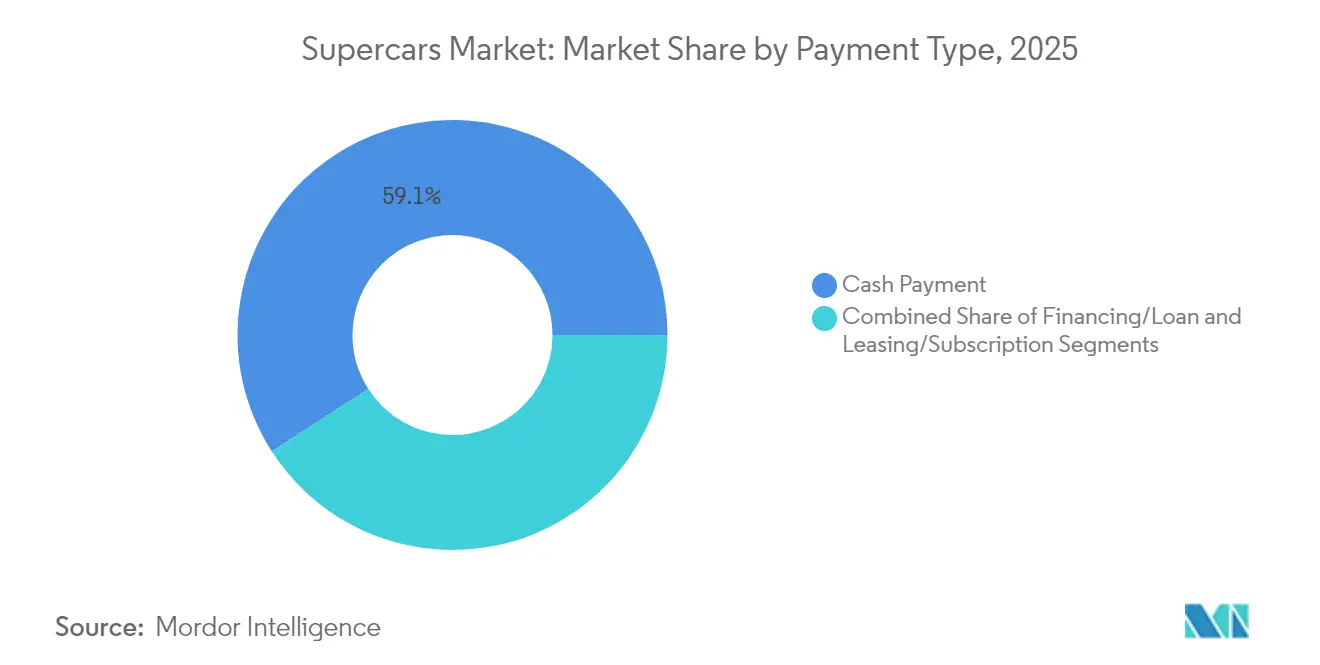

- By payment method, cash transactions captured 59.10% of the supercars market size in 2025, whereas leasing and subscriptions are forecast to rise at a 6.73% CAGR.

- By sales channel, dealerships controlled 75.92% of the supercars market share in 2025; direct-to-consumer sales are projected to climb at a 6.78% CAGR.

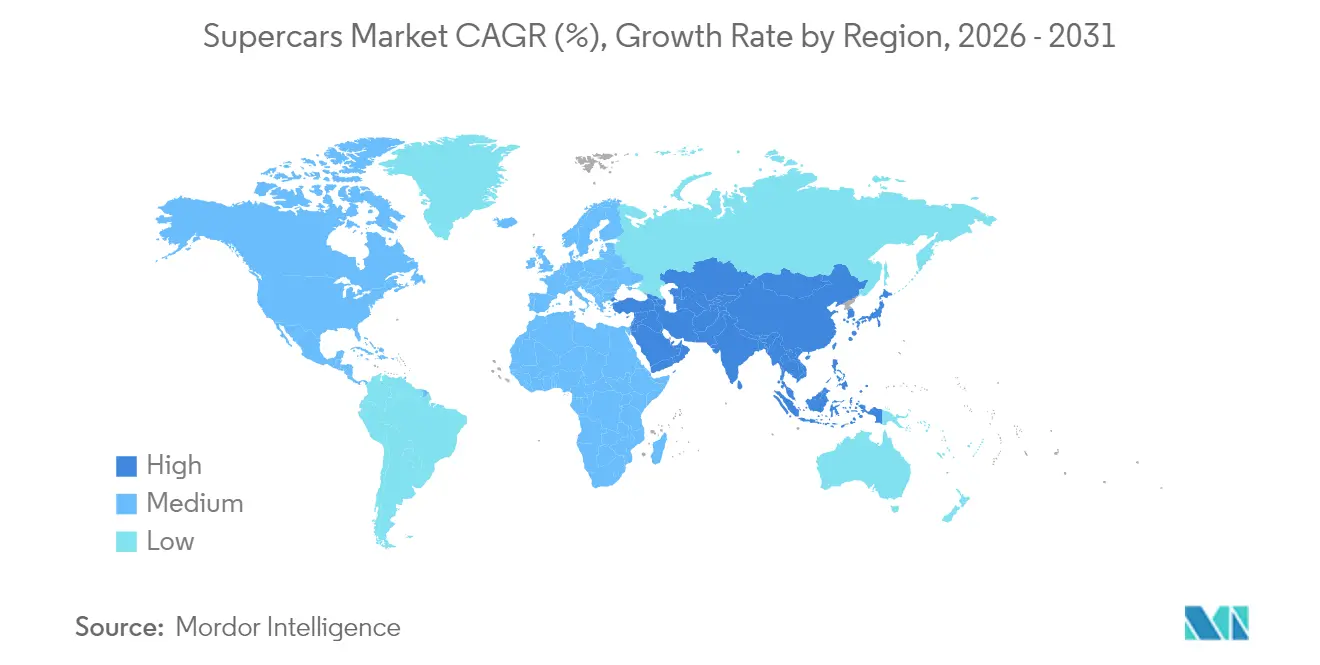

- By geography, Europe led with 38.30% revenue share in 2025, yet Asia-Pacific is projected to log the quickest 7.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Supercars Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Wealth of Ultra-High-Net-Worth | +1.8% | Global, concentrated in North America & APAC | Medium term (2-4 years) |

| Electrification & Hybrid Powertrains | +1.5% | Global, led by EU regulatory pressure | Long term (≥ 4 years) |

| Limited-Edition Models Viewed as Alternative Asset Class | +1.2% | Global, strongest in North America & Europe | Short term (≤ 2 years) |

| OEM–Motorsport Tech Transfer | +0.9% | Global, concentrated in Europe & North America | Medium term (2-4 years) |

| Bespoke Demand From Crypto-Millionaires | +0.7% | Global, highest in North America & APAC | Short term (≤ 2 years) |

| EU Carbon-Credit Loopholes | +0.4% | Europe primarily, limited global spillover | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Wealth of Ultra-High-Net-Worth Individuals

Crypto-enabled liquidity is broadening the supercars market beyond traditional finance. About 173,000 crypto millionaires now complement legacy wealth, and they convert gains into lifestyle assets far more quickly than equity investors, helping lift global supercar demand even when macroeconomic indicators soften. Their measured spending patterns still favor real estate, but many choose limited-edition vehicles as passion purchases that can appreciate. The buyer pool is larger, younger, and more geographically dispersed than ever, encouraging brands to diversify model mixes and regional allocations.

Electrification & Hybrid Powertrains Become Performance-Enhancers

Hybrid systems now sharpen, rather than blunt, supercar dynamics. Ferrari’s 296 Speciale couples a 120° V6 with electric assistance to deliver 880 hp while dropping 60 kg, demonstrating how instant electric torque eliminates turbo lag and raises rev ceilings without sacrificing emotion. Lamborghini’s Temerario follows a similar path by pairing a high-revving V8 with batteries for unprecedented track times. Hybrid prestige establishes tech leadership that supports premium list prices even under tightening emissions regulations. Brands that prioritize R&D investment can reap regulatory compliance and brand halo advantages.[1]“Q1 2025 Results,” Ferrari N.V., ferrari.com

Limited-Edition Models Viewed as Alternative Asset Class

Tight supply continues to transform halo cars into investment pieces. Ferrari’s EUR 3.8 million F80 sold out its 799-unit run quickly, underscoring how scarcity elevates long-term residual values. Although secondary-market prices for some nameplates such as the F8 Spider corrected 9.5% over the past 18 months, inflation-adjusted valuations remain close to pre-pandemic norms. This normalization pushes OEMs to fine-tune production volumes: too much stock erodes exclusivity, while too little foregoes near-term revenue. Investors now scrutinize announced allocations, driving manufacturers to publicize strict build caps.

OEM–Motorsport Tech Transfer Accelerates Innovation Cycles

Race-derived aerodynamics, composite materials, and energy-recovery electronics reach road cars faster than before. Lamborghini’s SC63 hypercar program pipelines active aero algorithms and advanced brake-by-wire systems directly to upcoming production models. Shorter transfer cycles elevate buyer expectations, compelling brands to refresh flagship lines more frequently. The supercars market harnesses this continuous innovation loop to justify six-figure price tags and retain customer loyalty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exorbitant Acquisition & Ownership Costs | -1.4% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Tightening Global Emissions | -1.1% | Global, led by EU and expanding to other regions | Long term (≥ 4 years) |

| Supply-Chain Bottlenecks | -0.8% | Global, concentrated in high-volume segments | Short term (≤ 2 years) |

| Surging Insurance Premiums | -0.6% | Global, most severe in North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening Global Emissions & Noise Standards

Euro 7 rules, effective November 2026, impose tougher limits on tailpipe, brake, and tire particulates, forcing costly re-engineering of low-volume platforms. Small carmakers face higher per-unit homologation expenses because they cannot spread R&D over millions of vehicles. The UK raised the tax on >255 g/km CO₂ cars to GBP 5,490 per year in April 2025, adding a meaningful lifetime cost. Compliance drives urgent hybrid or full-electric transitions, yet the development race strains capital budgets.[2]“Proposal for Euro 7 Standards,” European Commission, ec. europa.eu

Exorbitant Acquisition & Ownership Costs

Annual insurance for models such as the Ferrari 812 Superfast routinely tops USD 15,000, while hybrid-drive diagnostic tools push routine servicing invoices toward USD 8,000 per visit. Depreciation, storage, and specialized transport further inflate the total cost of ownership, discouraging aspirational buyers in emerging markets. Rising prices bolster subscription solutions that distribute outlays monthly and include maintenance, helping relieve buyer pain but requiring OEM fleet management capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Convertibles Balance Emotion and Engineering

Non-convertibles delivered 64.05% of 2025 unit deliveries and still anchor the supercars market thanks to lighter curb weight and superior torsional stiffness that translate into quicker lap times. Yet convertibles are expanding at a 6.53% CAGR as buyers prioritize immersive, open-air experiences over simulation-tested performance increments. The supercars market size for convertibles is expected to expand by USD 2.18 billion through 2031 as demographics skew younger and social-media visibility elevates lifestyle value.

Aerodynamic innovations such as McLaren’s single-piece folding roof and active buttresses offset drag penalties, narrowing real-world speed gaps to coupes. Profit margins trend higher on convertibles because buyers accept price premiums that exceed added bill-of-materials costs. Social proof and Instagramable content help brands leverage limited-edition spider variants each model cycle.

By Propulsion: Electric Surge Amid IC Dominance

IC engines still generated 72.85% of 2025 revenue, reflecting entrenched brand identities built on atmospheric V12 notes and gated shifters. However, battery-electric nameplates are gaining momentum, and they are projected to reach a mid-single-digit share of the supercars market size by 2031 on a 7.02% CAGR. The supercars market share for pure EVs will remain modest in the near term. Yet, their influence on model-development budgets is disproportionate, compelling every marque to outline an EV roadmap.

Range anxiety is shrinking as 800-V architectures enable 10-to-80% fast charging in under 20 minutes, while solid-state prototypes promise weight parity with mid-engine ICE vehicles. Ferrari aims to launch its first full EV in late 2025, whereas Lamborghini defers to 2029, citing customer readiness. Early adopters such as Rimac, already delivering the 1,900 hp Nevera, enjoy a halo status that stresses incumbents.

By Payment Type: Subscriptions Gain Credibility

Cash still funded 59.10% of 2025 deliveries, a testament to liquidity among global elite buyers. Leasing and subscription products nevertheless post a 6.73% CAGR, appealing to younger entrepreneurs who value access over ownership. Starting at USD 1,800 per month, Porsche Drive includes insurance, sets a segment benchmark, and influences competitor pilot programs.

Recurring revenues let OEMs monetize servicing and software updates, improving lifetime customer value. As depreciation risk shifts to manufacturers, residual-value management becomes strategic. Subscription fleets also supply certified-pre-owned inventory, smoothing cyclicality in the supercar market.

By Sales Channel: Digital Engagement Reshapes Transactions

Dealerships managed 75.92% of 2025 invoices, yet online configurators and virtual reality showrooms fuel the fastest 6.78% CAGR in direct-to-consumer sales. The supercars market values tactile events such as track days, but high-resolution digital twins now handle early-stage exploration, shortening deal cycles. Pagani’s real-time hypercar configurator illustrates immersive 3-D visualization that drives conversion despite seven-figure pricing.

Crypto-savvy buyers favor direct channels accepting digital-asset payment and bypassing paperwork, nudging brands toward in-house e-commerce checkouts. Dealer partners are repositioning as service hubs rather than sales monopolies, suggesting a hybrid retail landscape where physical and virtual touchpoints coexist.

Geography Analysis

Europe continues to lead with 38.30% revenue in 2025. Heritage marques, dense service networks, and an enthusiast culture sustain volume despite stringent Euro 7 obligations. Ferrari’s EMEA shipments climbed to 47% of its global mix in Q1 2025, proving pent-up demand even as regulators tighten oversight on noise and particulates. Premium pricing remains supported by craftsmanship values and multi-generation brand loyalty.

Asia-Pacific is powering the next growth wave, advancing at 7.01% CAGR. Rapid wealth accumulation in China, Singapore, and the United Arab Emirates shortens replacement cycles and broadens customer bases. Government-backed charging infrastructure in the UAE, moving from 0.7% EV sales in 2021 to 13% in 2023, signals readiness for electric supercars. Domestic luxury EV innovators such as BYD catalyze competitive benchmarking that pushes European brands to tailor region-specific tech features and digital ecosystems.

North America retains a deep collector culture and healthy dealer network, but soaring insurance and property taxes temper incremental growth. South America and selected African economies remain niche yet strategic for special-edition allocations that reinforce exclusivity messaging. Overall, the supercars market is rebalancing toward Asia while Europe safeguards value through regulation-driven innovation and heritage branding.

Competitive Landscape

Market concentration is moderate. Ferrari continues to uphold its scarcity-driven approach, maintaining carefully limited production growth to preserve exclusivity. Lamborghini follows a similar strategy, allowing measured volume increases while retaining its luxury positioning. Meanwhile, McLaren is pursuing revitalization through a strategic merger with EV startup Forseven, aimed at integrating advanced battery expertise and securing fresh capital for its next-generation lineup.

All leading marques are investing in hybrid drivetrains that balance performance and compliance. Supply chains pivot toward aerospace-grade forged composites to offset battery weight, yet access to these materials remains limited, creating collaboration opportunities with specialized suppliers. BMW’s agreement with Rimac Technology to co-develop high-voltage systems shows how legacy firms leverage external expertise to accelerate electrification roadmaps.

Direct-to-consumer pilots and subscription fleets are becoming differentiators. Brands testing factory-backed leasing accumulate customer data that feeds future product planning. Meanwhile, motorsport programs provide rapid prototyping fields; Lamborghini’s SC63 feeds aerodynamic learnings directly to street-legal models, compressing development cycles and bolstering marketing narratives around track credibility.

Supercars Industry Leaders

Ferrari SpA

Automobili Lamborghini SpA

Porsche AG

McLaren Group

Aston Martin Lagonda Global Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Ferrari unveiled the 296 Speciale, a plug-in hybrid Berlinetta producing 880 hp and 20% more downforce than the 296 GTB while reducing weight by 60 kg.

- April 2025: McLaren confirmed a merger with British EV startup Forseven to speed its electrification program.

- May 2024: Ferrari launched the 12Cilindri featuring an 819 hp 12-cylinder engine and a top speed above 211 mph.

- June 2024: Bugatti introduced the Tourbillon, a 1,775 hp V16 hybrid hypercar priced at USD 4.3 million and limited to 250 units.

Global Supercars Market Report Scope

A supercar is a high-performance sports car with superior speed, power, and handling characteristics designed for exceptional on-road performance. These cars typically feature cutting-edge technology, exotic materials, and aerodynamic designs.

The supercars market is segmented by type, propulsion type, payment type, and geography. By type, the market is segmented into convertible and non-convertible. By propulsion type, the market is segmented into IC engine, electric, and hybrid. By payment type, the market is segmented into cash payment, financing/loan, and leasing. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World.

The report offers market sizes and forecasts for all the above segments in value (USD).

| Convertible |

| Non-convertible |

| IC Engine |

| Electric |

| Hybrid |

| Cash Payment |

| Financing / Loan |

| Leasing / Subscription |

| Dealership |

| Direct-to-Consumer |

| Online Configurator |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Convertible | |

| Non-convertible | ||

| By Propulsion Type | IC Engine | |

| Electric | ||

| Hybrid | ||

| By Payment Type | Cash Payment | |

| Financing / Loan | ||

| Leasing / Subscription | ||

| By Sales Channel | Dealership | |

| Direct-to-Consumer | ||

| Online Configurator | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the supercars market and how fast is it growing?

The market generated USD 20.41 billion in 2026 and is projected to reach roughly USD 27.93 billion by 2031, advancing at a 6.47% CAGR.

Which region buys the most supercars today?

Europe leads with 38.30% of 2025 revenue, supported by heritage brands and mature wealth bases.

Where is demand expanding the fastest?

Asia-Pacific is set to post a 7.01% CAGR through 2031 as rapid wealth creation and tech-forward preferences lift sales.

How are hybrids and EVs shaping future product plans?

Hybrids already make up 49% of Ferrari’s shipments, and battery-electric models are forecast to grow at 7.02% CAGR, turning electrification into a performance asset rather than a compliance cost.

Why are leasing and subscription models gaining traction?

Younger affluent buyers prefer flexibility and lower upfront outlays; subscription revenues are climbing at a 6.73% CAGR while bundling insurance and maintenance.

What are the main risks facing supercar makers?

Stricter Euro 7 emissions rules and high insurance and maintenance costs raise ownership barriers, forcing brands to accelerate electrification and explore alternative retail models.

Page last updated on: