Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

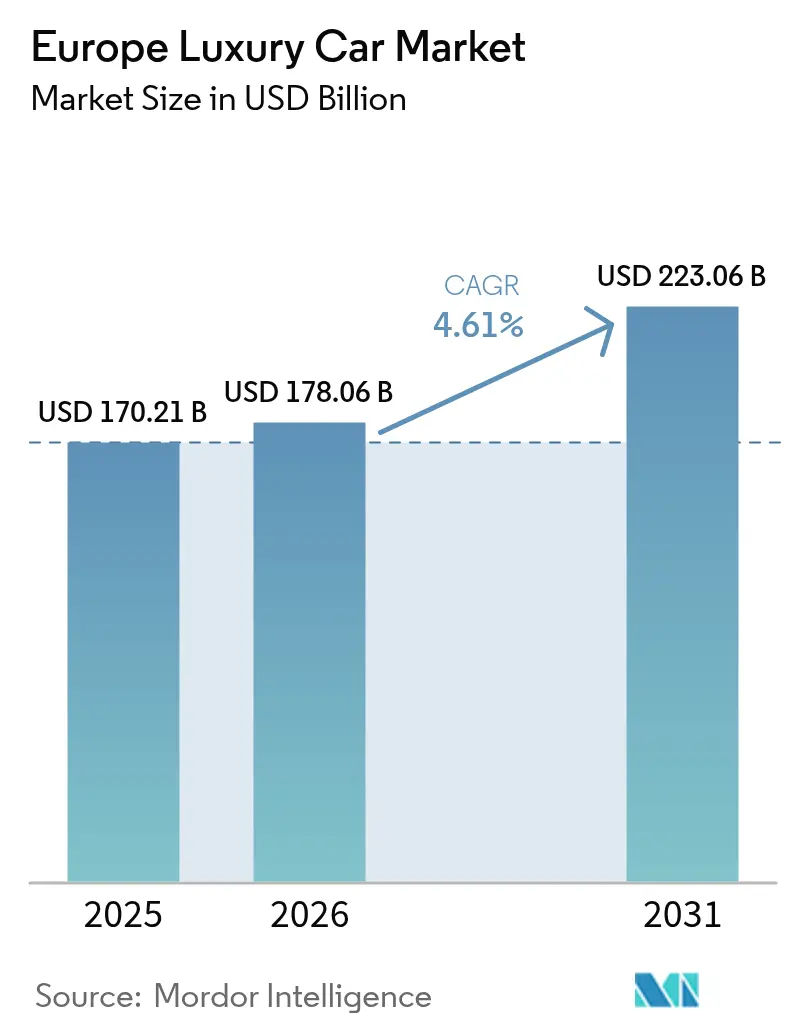

| Base Year Market Size (2025) | USD 170.21 Billion |

| Market Size (2026) | USD 178.06 Billion |

| Market Size (2031) | USD 223.06 Billion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Luxury Car Market Analysis by Mordor Intelligence

The European luxury car market size was valued at USD 170.21 billion in 2025, and is anticipated to reach USD 223.06 billion by 2031, from USD 178.06 billion in 2026, growing at a CAGR of 4.61% from 2026 to 2031. Rising electrification, the shift toward flexible ownership, and competitive pressure from new Chinese entrants are reshaping the European luxury car market in real time. Demand skews toward high-riding Sport Utility Vehicles that blend status, practicality, and winter drivability, while residual range anxiety keeps many buyers anchored to combustion engines for long-distance touring. Ownership patterns are also changing, as finance and lease agreements dominate corporate fleets and wealthier private buyers experiment with subscription services that unbundle usage from traditional ownership. Regulatory actions ranging from city-center zero-emission zones to fleet-average CO₂ limits accelerate battery-electric adoption, yet uneven charging infrastructure rollouts create geographic imbalances that every automaker must navigate.

Key Report Takeaways

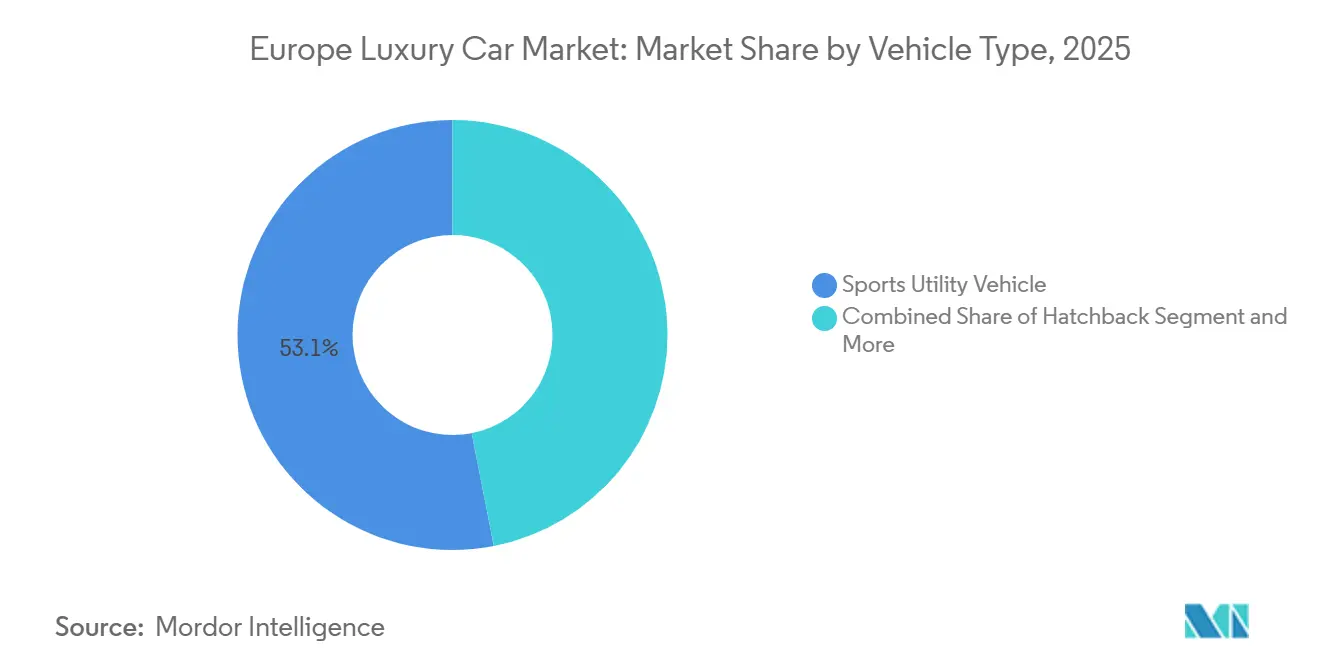

- By vehicle type, SUVs captured 53.07% of the European luxury car market share in 2025; coupé and convertible models are projected to expand at a 6.39% CAGR through 2031.

- By powertrain, internal combustion engines accounted for 77.24% of the 2025 European luxury car market, whereas battery-electric vehicles are forecast to post a 10.29% CAGR through 2031.

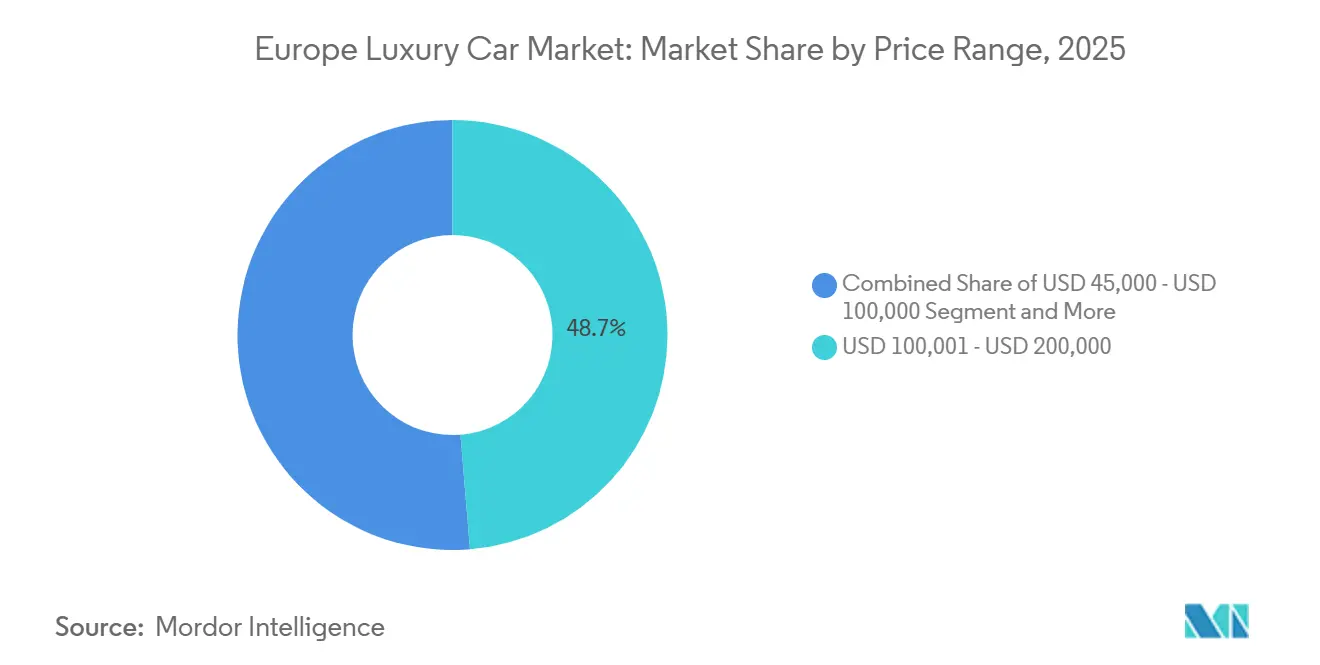

- By price range, the USD 100,000–200,000 bracket accounted for 48.71% of the European luxury car market size in 2025; models priced above USD 200,000 are growing fastest at a 6.22% CAGR to 2031.

- By ownership model, finance/lease contracts accounted for 57.17% of 2025 deliveries, while subscription services are set to grow at a 6.63% CAGR over the forecast horizon.

- By country, Germany led the European luxury car market with 29.27% market share in 2025, and Norway is on track for the fastest national CAGR at 6.49% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Luxury Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Electrification | +1.8% | Germany, Norway, Netherlands, United Kingdom, France | Medium term (2-4 years) |

| Rising UHNWI and HNWI Population | +1.2% | Switzerland, United Kingdom, Germany, Monaco, France | Long term (≥ 4 years) |

| Digital In-Car Experience Demand | +0.9% | Germany, Sweden, Norway, United Kingdom, Netherlands | Medium term (2-4 years) |

| Subscription and Fractional-Ownership Models | +0.7% | Germany, United Kingdom, Sweden, Denmark, Netherlands | Long term (≥ 4 years) |

| Micro Market-Specific Incentives | +0.6% | Norway, Germany, France, Netherlands, Belgium, Austria | Short term (≤ 2 years) |

| Monetization of Connected-Vehicle Data Streams | +0.4% | Germany, France, United Kingdom, Sweden | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification of Luxury Segment

Luxury OEMs are funding new battery-electric platforms that match combustion-engine range and cut DC fast-charge times, reinforcing momentum behind zero-emission goals. Early adopters in Norway and Germany demonstrate that regulatory deadlines can translate into real demand when fiscal incentives and public charging infrastructure align. As platforms converge on 20-minute charging and 500-kilometer range, the addressable audience for electric luxury expands well beyond tech enthusiasts. Yet electrification also divides the European luxury car market: volume-luxury brands wrestle with compressed margins, while ultra-luxury marques monetize exclusivity by adding limited-run electric grand tourers.

Rising Population of UHNWIs and HNWIs

Growth in private wealth across Switzerland, Monaco, Germany, and the United Kingdom sustains appetite for bespoke vehicles that emphasize craft over cost. These buyers prize carbon-neutral production and recycled interiors, signaling a shift from pure performance toward demonstrable sustainability. Waiting lists stretch well beyond a year for special editions, allowing manufacturers to command higher margins and hedge against cyclical downturns among mass-affluent segments. The enlarging pool of wealthy consumers underpins long-term demand resilience, adding significantly to projected growth.

Digitally Enabled In-Car Experience Demand

Connected-car cabins now mirror smartphone ecosystems, featuring voice-first interfaces and augmented-reality navigation. Automakers monetize software post-sale, offering on-demand features that convert one-time purchases into steady subscription revenue. Buyers value seamless over-the-air updates that future-proof hardware, yet react negatively when charged twice for pre-installed components, forcing careful price-architecture design. The demand for digital sophistication reshapes R&D priorities and feeds strategic alliances with tech firms.

Subscription and Fractional-Ownership Models

Flexible access plans resonate with urban professionals who reject tying capital into depreciating assets. By bundling insurance, maintenance, and concierge services, OEMs secure predictable cash flows and capture data that refines future product decisions. Dealers express concern over channel conflict, but pilot programs demonstrate higher fleet utilization and customer lifetime value. Geography dictates uptake: Germany and the Nordics lead, while Southern Europe remains tentative.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Purchase Cost and Tightening Credit | -0.8% | United Kingdom, Italy, Spain, France, Germany | Short term (≤ 2 years) |

| Residual-Value Volatility | -0.6% | Germany, United Kingdom, Netherlands, Norway, Sweden | Medium term (2-4 years) |

| Macroeconomic Uncertainty and Inflation | -0.5% | Italy, Spain, France, United Kingdom, Germany | Short term (≤ 2 years) |

| Carbon-Intensity Taxes | -0.3% | France, Belgium, Netherlands, Denmark, United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Purchase Cost and Tightening Credit

As policy rates climb and borrowing costs surge, affordability wanes for mid-luxury buyers, compounded by high battery-pack premiums. With lenders tightening their underwriting standards, there's been a noticeable dip in motor-finance penetration, pushing replacement cycles further out. Automakers are increasingly compelled to subsidize finance offers to attract buyers or risk reduced showroom traffic, which could significantly impact their margins. This challenging environment is expected to persist until monetary policy becomes more accommodative, which will create additional pressure on the market in the near term.

Luxury-EV Residual-Value Volatility

Leasing firms, facing eroded resale confidence due to rapid tech updates, are now demanding higher risk premiums or residual-value guarantees. Concerns deepen as early-generation battery-electric models struggle with limited secondary-market liquidity, making it challenging to predict their long-term value. Fleet managers, uncertain about potential depreciation risks, are hesitant to transition their portfolios to electric vehicles. This hesitation slows the adoption of luxury EVs, creating a ripple effect across the market and impacting growth momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUVs Dominate, Coupes Accelerate

Sport Utility Vehicles accounted for 53.07% of the European luxury car market size in 2025. The high-riding format satisfies family practicality, winter traction, and a perception of safety that resonates across Northern Europe. Automakers therefore prioritize electric SUV launches, confident that consumer familiarity will speed adoption of new powertrains. Meanwhile, coupe and convertible niches act as brand halos, drawing attention even when volumes are modest.

Coupes and convertibles are projected to record the fastest segment growth at a 6.39% CAGR through 2031. Wealthy enthusiasts view limited-run electric grand tourers as collectible assets and accept long waiting periods. Manufacturers leverage this demand to test cutting-edge battery and lightweight technologies, which later cascade into higher-volume body styles. As a result, every marquee now links its design-studio narrative to a flagship two-door model, ensuring innovation credibility with loyal patrons.

By Powertrain Type: ICE Dominance Erodes as BEVs Surge

Internal-combustion engines retained a 77.24% share of the European luxury car market size in 2025. Range security, refueling convenience, and a thick network of service stations keep many affluent drivers loyal to proven technology. Brands continue to refine efficient V-configuration engines to satisfy enthusiasts who equate engine note with status. Yet every OEM publicly aligns future strategy with emissions compliance, signaling an eventual pivot.[1]“Transport and Environment Reporting Mechanism,” European Environment Agency, eea.europa.eu

Battery-electric vehicles have the fastest growth trajectory, with a 10.29% CAGR to 2031. Dedicated skateboard platforms raise cabin comfort levels, and rapid charging times rival traditional fuel stops in the most developed networks. Early adopter feedback shapes software roadmaps that deliver continuous upgrades via the cloud. As regulatory milestones tighten and charging spreads, BEVs shift from a compliance necessity to an aspirational choice in the showroom.

By Price Range: Mid-Luxury Anchors Volume, Ultra-Luxury Accelerates

The USD 100,000–USD 200,000 band accounted for 48.71% of the European luxury car market size in 2025. Corporate fleets and affluent professionals gravitate here because the specification-to-cost ratio aligns with benefit-in-kind taxation thresholds. Automakers differentiate by layering software subscriptions that unlock optional driver-assistance features post-sale, stretching revenue across the vehicle lifecycle. However, discount pressure rises as new entrants undercut list prices with technology-rich alternatives.

Above-USD 200,000 models will outpace all other tiers, with a 6.22% CAGR through 2031. Ultra-High-Net-Worth buyers treat individualized vehicles as mobile art, demanding carbon-neutral build processes and made-to-order interiors. Limited production volumes shield pricing power, while electrification brings silent torque that enhances the luxury experience. This rarefied segment, therefore, preserves automaker prestige and funds next-generation R&D.

By Ownership Model: Finance Dominates, Subscription Emerges

Finance and lease arrangements accounted for 57.17% of European luxury car transactions in 2025. Corporations optimize working-capital budgets through operating leases, and private buyers preserve liquidity by replacing large down payments with more predictable terms. Banks and captives bundle residual-value insurance to stabilize monthly outflows, reinforcing the appeal of multi-year plans tied to new-model cycles.

Subscription schemes represent the fastest climb, set for a 6.63% CAGR through 2031. High-density urbanites view a rolling-monthly contract as the antidote to parking shortages and shifting lifestyle demands. Automakers mine usage data to tailor future fleets and refine retention tactics such as loyalty upgrades. Although penetration remains single-digit, the model’s success with tech-savvy consumers foreshadows broader adoption once pricing normalizes.

Geography Analysis

Germany commanded 29.27% of the European luxury car market size in 2025, due to the domestic stronghold of Mercedes-Benz, BMW, Audi, and Porsche, each running extensive R&D programs to defend home-field advantage[2]“Vehicle Registration Statistics,” European Automobile Manufacturers' Association, ACEA.auto. The country hosts dense supply networks and brand museums that reinforce customer loyalty. Yet, it also serves as the primary beachhead for price-aggressive Chinese competitors eager to showcase value against storied badges. Regional policymakers support battery-electric adoption through tax credits, but Germany’s broad highway system continues to favor long-range combustion models, creating a dual-powertrain landscape that automakers balance carefully.

Norway delivers the fastest regional momentum, with a 6.49% CAGR forecast to 2031. Comprehensive incentives, zero value-added tax on zero-emission cars, free toll passage, and an unrivaled charging grid, drive battery-electric penetration to levels approaching ubiquity. Luxury SUV buyers embrace the environmental narrative without surrendering performance, setting a precedent that regulators in other Nordic countries aim to replicate. Automakers treat Norway as a living laboratory for digital-first sales strategies, generating data that shapes pan-European rollout plans.

Southern Europe, led by Italy, Spain, and France, trails in charging density, so combustion and plug-in hybrids maintain stronger footholds. However, coastal zero-emission zones in metropolitan hubs push local demand toward smaller electric crossovers, incrementally raising the European luxury car market’s BEV share. The United Kingdom occupies a middle position: incentives are less generous than in Norway, but policy certainty remains higher than on the continent, encouraging steady migration to electric powertrains. Across all geographies, uneven infrastructure forces automakers to customize powertrain mixes and marketing narratives, fragmenting a market once served by uniform product lines.

Competitive Landscape

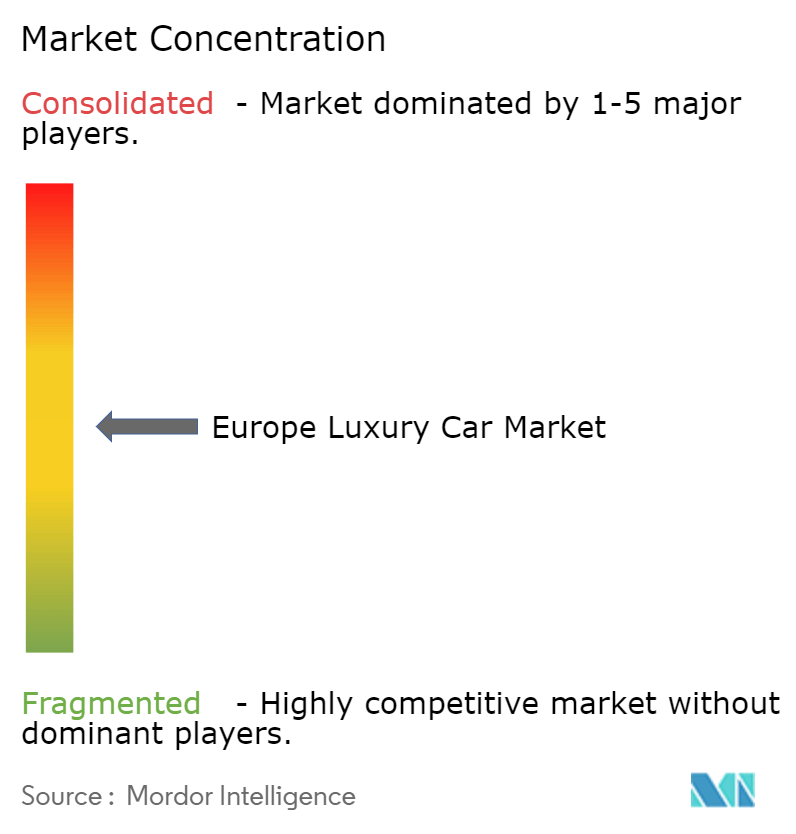

The competitive field scores a mid-level 5 for concentration: the top five brands control a significant share, but none exceed commanding dominance. German incumbents invest heavily in in-house battery plants and software stacks to counter feature-rich Chinese imports, priced lower on average. Software-defined vehicle platforms enable pay-as-you-go upgrades, an area where newcomers and legacy players converge in strategy despite divergent cost bases. Chinese challengers accelerate European assembly plans to bypass tariffs, compelling local manufacturers to compress product-development cycles without sacrificing design integrity.

Tesla retains first-mover brand equity in battery-electric luxury, yet its migration toward mass-market volumes blurs positioning against bespoke European marques. Start-ups such as Polestar exploit minimalist design and digital-only retail to court younger buyers, though limited after-sales reach still constrains volume. Traditional luxury builders hedge risk by spreading bets: they keep flagship combustion engines alive for enthusiasts while simultaneously previewing carbon-neutral grand tourers for collectors.

Regulation acts as a market maker: fleet-average CO₂ caps penalize laggards at EUR 95 per excess gram, so alliance formations around shared EV architectures intensify. Charging-network co-investments multiply as brands recognize that infrastructure reliability underpins customer satisfaction more than headline acceleration metrics. Ultimately, the European luxury car market rewards those able to blend heritage craftsmanship with tech agility, a balance few have yet mastered.

Europe Luxury Car Industry Leaders

Mercedes-Benz Group AG

BMW AG

Audi AG

Porsche AG

Tesla Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Zeekr, the electric vehicle brand of Geely, has made its debut in Italy, partnering with Jameel Motors Italia for local distribution.

- January 2026: Renault took the wraps off 'Filante', its latest premium crossover and the fifth addition to its International Game Plan 2027 lineup. With cutting-edge design, state-of-the-art technology, and a robust 250 hp E-Tech hybrid engine, Filante is tailored for a luxurious experience and targets markets beyond Europe.

- September 2025: Hongqi, the luxury arm of China's FAW Group, revealed plans to introduce 15 electric and hybrid models across 25 European markets by 2028, simultaneously debuting its compact electric SUV, the EHS5.

- September 2025: Lucid launched sales of its Gravity large SUV in Europe, pricing it at EUR 116,900 (~USD 123,000) in Germany and positioning it against premium offerings from Audi and Mercedes-Benz.

Europe Luxury Car Market Report Scope

Luxury cars, known for their superior comfort, high-end amenities, and top-notch performance, often carry a prestigious status that sets them apart from their more affordable counterparts. In Europe, the luxury car market boasts high-end models renowned for their unparalleled comfort and reliability, crafted from the finest materials. Dominating this elite market are renowned players like Porsche, Ferrari, BMW, and Mercedes-Benz.

The European Luxury Car market is segmented by vehicle type, powertrain type, price range, ownership model, and country. By Vehicle Type, the market is segmented into Hatchback, Sedan, Sport Utility Vehicle (SUV), Multi-purpose Vehicle, and Coupe and Convertible. By Powertrain Type, the market is segmented into Internal-Combustion Engine (ICE), Hybrid Electric Vehicle, Plug-in Hybrid Electric Vehicle, and Battery Electric Vehicle. By Price Range, the market is segmented into USD 45,000 - USD 100,000, USD 100,001 - USD 200,000, and above USD 200,000. By Ownership Model, the market is segmented into Outright Purchase, Finance/Lease, Subscription, and Fractional and Club Ownership. By Country, the market is segmented into Germany, the United Kingdom, France, Italy, Spain, the Netherlands, Sweden, Denmark, Belgium, Switzerland, Austria, Norway, Russia, and the Rest of Europe.

Market forecasts are provided in terms of Value (USD) and Volume (Units).

By Vehicle Type

| Hatchback |

| Sedan |

| Sport Utility Vehicle (SUV) |

| Multi-purpose Vehicle (MPV) |

| Coupe and Convertible |

By Powertrain Type

| Internal-Combustion Engine |

| Hybrid Electric Vehicle (HEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Battery Electric Vehicle (BEV) |

By Price Range

| USD 45,000 - USD 100,000 |

| USD 100,001 - USD 200,000 |

| Above USD 200,000 |

By Ownership Model

| Outright Purchase |

| Finance/Lease |

| Subscription |

| Fractional and Club Ownership |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Denmark |

| Belgium |

| Switzerland |

| Austria |

| Norway |

| Russia |

| Rest of Europe |

| By Vehicle Type | Hatchback |

| Sedan | |

| Sport Utility Vehicle (SUV) | |

| Multi-purpose Vehicle (MPV) | |

| Coupe and Convertible | |

| By Powertrain Type | Internal-Combustion Engine |

| Hybrid Electric Vehicle (HEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | |

| Battery Electric Vehicle (BEV) | |

| By Price Range | USD 45,000 - USD 100,000 |

| USD 100,001 - USD 200,000 | |

| Above USD 200,000 | |

| By Ownership Model | Outright Purchase |

| Finance/Lease | |

| Subscription | |

| Fractional and Club Ownership | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Denmark | |

| Belgium | |

| Switzerland | |

| Austria | |

| Norway | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large will the European luxury car market?

The market, valued at USD 178.06 billion in 2026, is anticipated to reach USD 223.06 billion by 2031, registering a CAGR of 4.61% during the forecast period.

Which body style holds the largest share in 2025?

Sport Utility Vehicles lead, accounting for 53.07% of 2025 sales across the Europe luxury car market.

Why is Norway important to automakers?

Norway’s near-universal BEV adoption and supportive incentives make it a real-world test bed for electric-only sales models and charging solutions.

What ownership model is gaining popularity among urban buyers?

Subscription services are emerging quickly, projected to expand at a 6.63% CAGR as city dwellers favor flexibility over long-term ownership.

Which price tier is expected to grow the fastest?

Vehicles priced above USD 200,000 are set to rise at a 6.22% CAGR, driven by demand from Ultra-High-Net-Worth collectors seeking exclusivity and sustainability.

Page last updated on: