Car Covers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

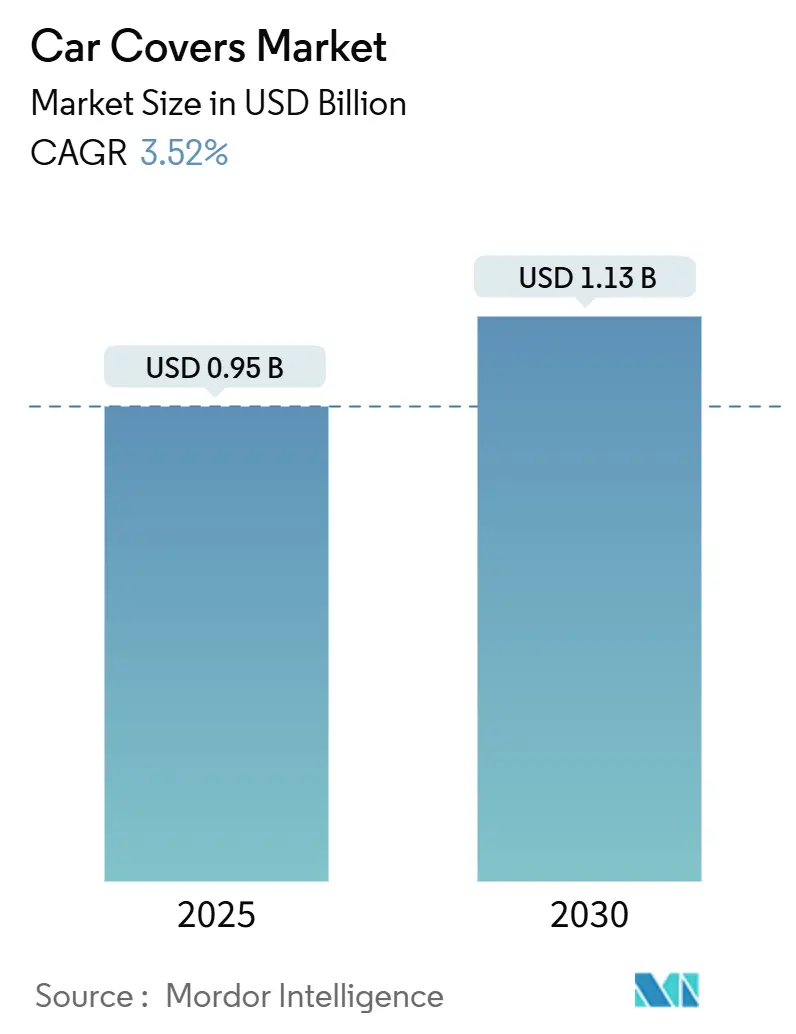

| Market Size (2025) | USD 0.95 Billion |

| Market Size (2030) | USD 1.13 Billion |

| Growth Rate (2025 - 2030) | 3.52% CAGR |

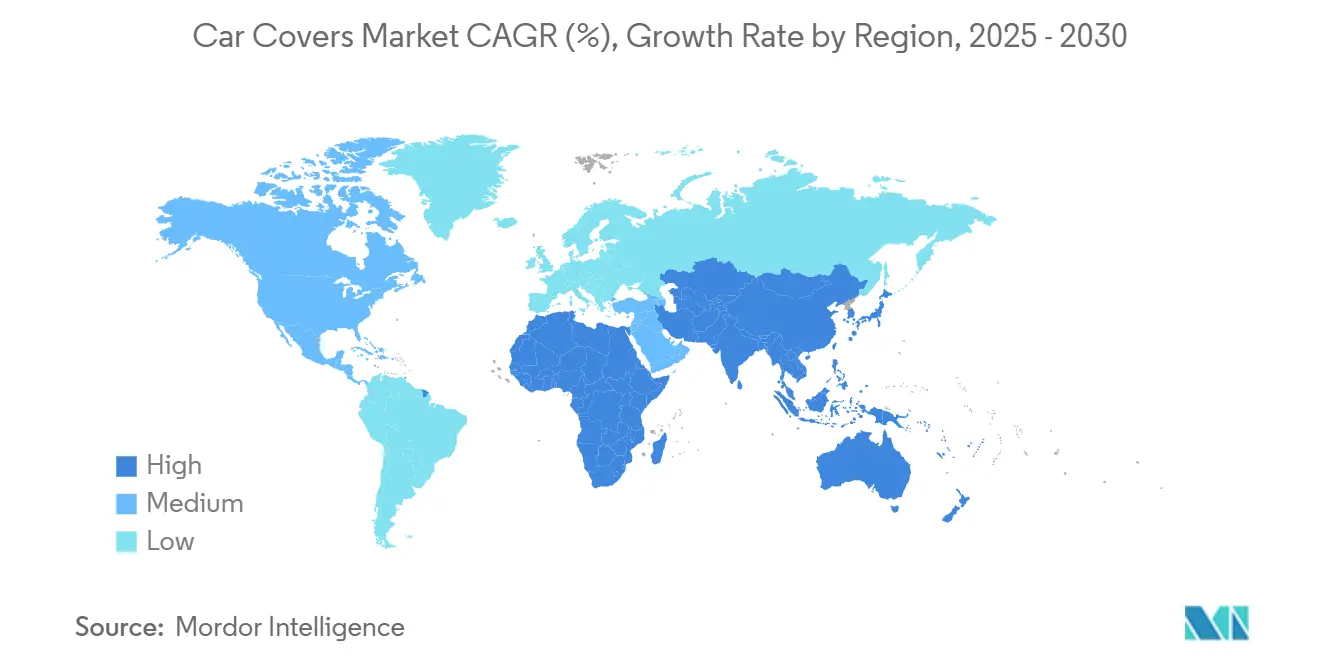

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

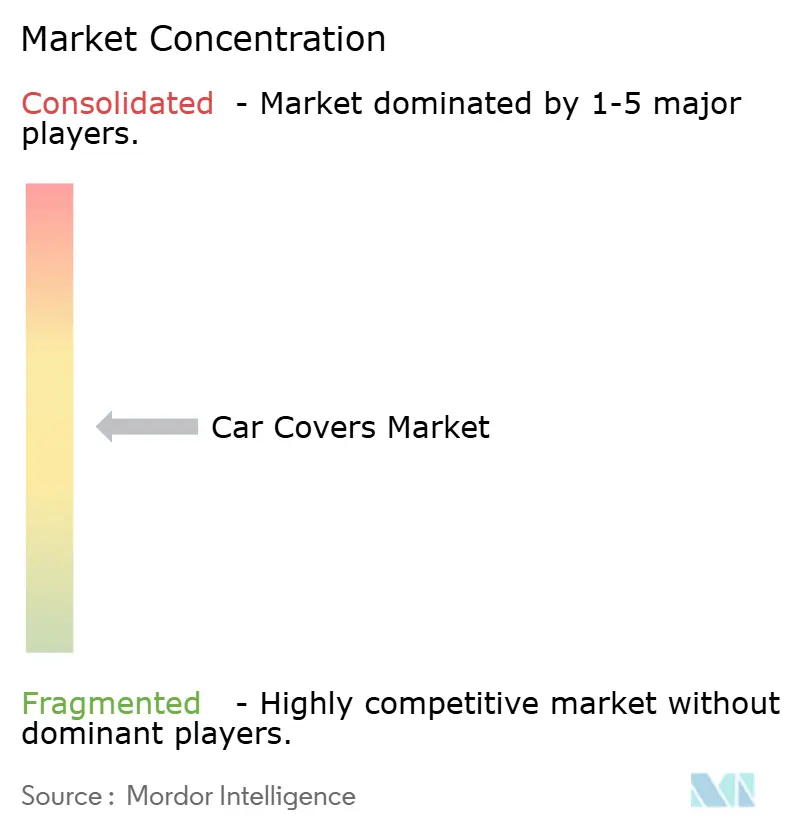

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Car Covers Market Analysis by Mordor Intelligence

The Car Covers Market size is estimated at USD 0.95 billion in 2025, and is expected to reach USD 1.13 billion by 2030, at a CAGR of 3.52% during the forecast period (2025-2030). This steady expansion mirrors the sector’s migration from basic protective sheets to digitally enabled, subscription-ready products that resonate with shifting ownership patterns and climate-resilience priorities. E-commerce propels massive growth in online aftermarket sales, trimming distribution frictions while broadening global reach. Material innovation, notably multilayer composites and antimicrobial coatings, elevates performance benchmarks, and automated deployment systems entice consumers who prioritize convenience. Although pricing pressure from low-cost imports persists, sustained acceptance of larger vehicles, rising hail-related insurance claims, and growing recognition of protective gear’s value continue to underpin demand for the car covers market.

Key Report Takeaways

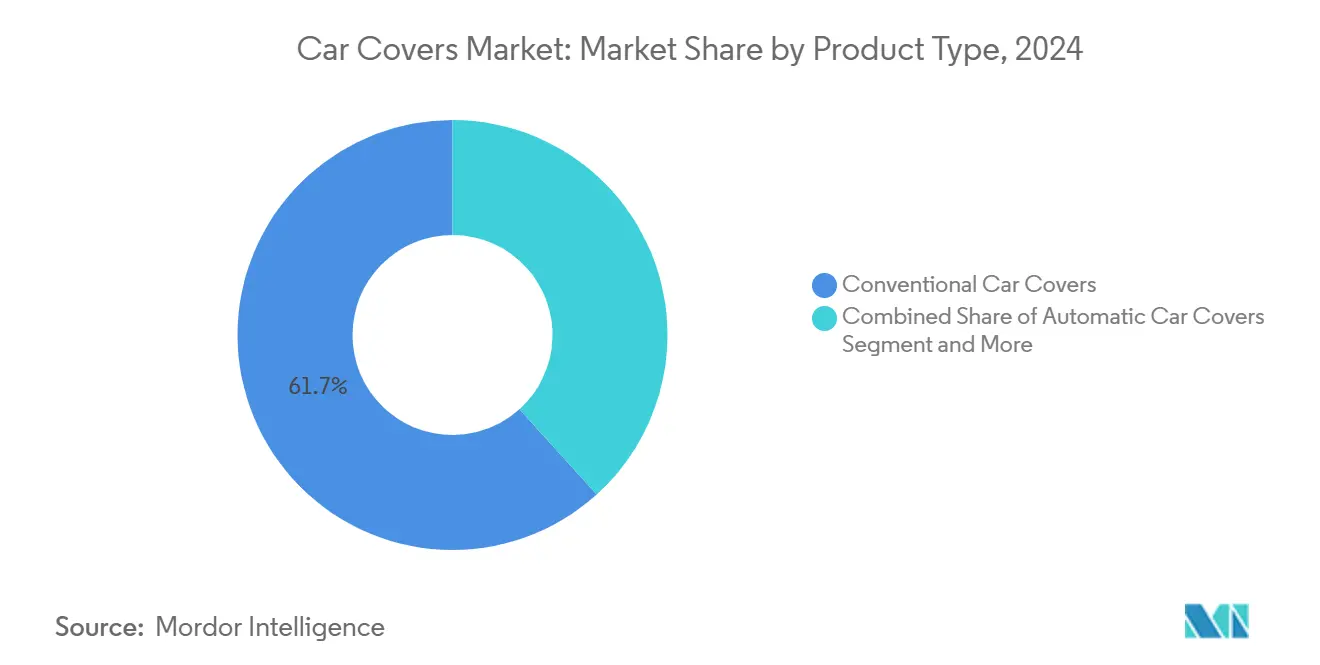

- By product type, conventional covers led with 61.73% of the car covers market share in 2024; automatic variants are projected to record the fastest 3.55% CAGR through 2030.

- By material, polyester accounted for 46.55% of the car covers market share in 2024, while multilayer composite fabrics are advancing at a 3.66% CAGR.

- By vehicle type, sedan covers captured 36.51% of the car covers market share in 2024; SUV/MUV covers are forecast to expand at a 3.57% CAGR.

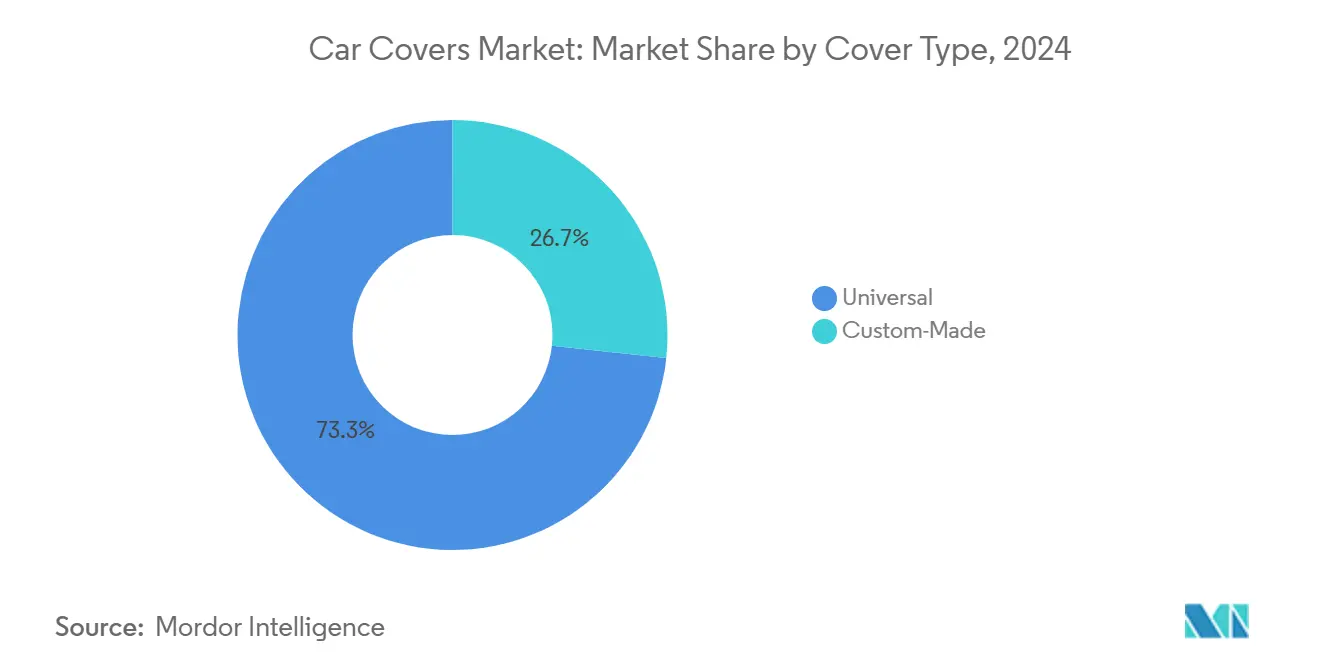

- By cover type, universal models dominated with a 73.25% of the car covers market share in 2024, whereas custom-made designs will grow at a 3.59% CAGR to 2030.

- By distribution channel, offline outlets retained 66.72% of the car covers market share in 2024; online platforms will post a 3.61% CAGR.

- By geography, North America held 37.66% of the car covers market share in 2024, while the Middle East and Africa registered the highest 3.63% CAGR through 2030.

Global Car Covers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Vehicle Ownership | +0.8% | Global, with a concentration in Asia Pacific and MEA | Medium term (2-4 years) |

| E-Commerce Penetration | +0.6% | North America and EU leading, Asia Pacific accelerating | Short term (≤ 2 years) |

| Extreme Weather Events | +0.5% | Global, particularly Australia, the Southern US, and Europe | Long term (≥ 4 years) |

| Retractable Solar-Integrated Smart Covers | +0.3% | North America and EU early adoption, Asia Pacific manufacturing | Medium term (2-4 years) |

| Antimicrobial and Self-Healing Polymer Coatings | +0.2% | Global, with premium segments in developed markets | Long term (≥ 4 years) |

| Subscription-Based Cover-As-A-Service For Shared Fleets | +0.1% | Urban centers in North America, the EU, and select Asia Pacific cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Ownership & Aging Fleet

A 12.5-year average U.S. light-vehicle age in 2023 underscores the aftermarket’s longevity focus. Aging assets encourage owners to prioritize exterior preservation over replacement, particularly in emerging economies where financing constraints extend vehicle lifespans. Fleet composition tilts toward larger formats, with SUVs and light trucks representing two-fifths U.S. registrations. In the Philippines, vehicle registrations climbed nearly one-tenth in 2022 amid average lifespans surpassing 15 years. Outdoor parking prevalence in congested cities amplifies exposure risk, reinforcing protective-cover adoption. As disposable incomes rise in APAC and MEA cities, premium multilayer fabrics gain traction, intensifying competition among regional suppliers.

E-Commerce Penetration Expanding Aftermarket Reach

Digital marketplaces are reshaping the car covers market, enabling direct manufacturer-to-consumer models and eroding traditional retail margins. AI-driven inventory tools lower stockouts for custom SKUs, while mobile apps integrate vehicle compatibility checks that reduce return rates. Chinese exporters harness cross-border platforms, pushing auto-parts shipments exponentially between January and July 2024. Click-and-collect programs merge online convenience with in-store reassurance, capturing DIY buyers who still value tactile evaluation. Enhanced product visualization and augmented-reality fit guides further accelerate consumer migration to online channels[1]Li Wei, “China Auto-Parts Exports Surge in 2024,” Sina Finance, finance.sina.com.cn.

Extreme Weather Events Increasing Protective-Gear Spend

Twenty-eight billion-dollar weather disasters in 2023 highlighted climate volatility. Germany’s June–July 2021 hailstorms alone generated a huge amount in claims close to 2 lakh vehicles, spurring demand for padded hail-defense covers. Australian sellers command for thick-quilted variants tailored to severe hail belts[2]“Hailstorm Damage Report 2021,” German Insurance Association, gdv.de . Elevated UV indices propel the uptake of solar-reflective coatings, mitigating cabin heat and paint degradation. Insurers in Europe now explore premium discounts for covered vehicles, embedding economic incentives alongside climate resilience benefits.

Retractable Solar-Integrated Smart Covers

Connected accessories redefine user expectations as integrated photovoltaic cells maintain battery charge during extended parking. Tesla owners pay extra for powered sunshades that link to vehicle apps and curb HVAC loads. IoT sensors enhance theft alerts, temperature monitoring, and remote diagnostics, while voice-control modules streamline deployment. As battery tech advances, solar-assisted recharging will migrate from niche EV owners to mainstream consumers, widening the premium-cover addressable base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal Demand Volatility | -0.4% | Temperate climate regions, particularly North America and Europe | Short term (≤ 2 years) |

| Price Pressure From Low-Cost Imports | -0.3% | Global, most acute in price-sensitive segments | Medium term (2-4 years) |

| Micro-Plastic Regulations | -0.2% | EU leading, with spillover to North America and Asia Pacific | Long term (≥ 4 years) |

| Paint-Protection Films | -0.2% | North America and EU premium segments, urban centers globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Seasonal Demand Volatility

Sales peaks preceding winter and storm seasons strain manufacturing throughput and warehouse capacity. Retailers overstock to meet surges yet risk long inventory tails in mild seasons, tying up working capital. These cycles hinder hail-focused SKUs that sell briskly in storm-prone months yet stagnate afterward despite year-round exposure risks, and delayed consumer purchases during temperate conditions further challenge demand forecasting. Manufacturers adopting modular, quick-build lines and data-driven replenishment mitigate volatility but incur added complexity.

Price Pressure From Low-Cost Imports

Aggressive cross-border pricing squeezes mid-tier brands already absorbing compliance costs tied to EU microplastic reporting and digital product passports. Counterfeit covers undermine consumer confidence, especially when substandard materials fail prematurely. Established suppliers emphasize warranty support, fit accuracy, and sustainable credentials to justify premiums. Governments in the U.S. and EU explore stricter port-of-entry inspections, yet enforcement gaps still allow non-compliant stock to permeate marketplaces.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automation Drives Premium Segment Growth

Based on established price-to-performance acceptance, the conventional line retained 61.73% of the car covers market share in 2024. Meanwhile, automatic systems are forecast to clock a 3.55% CAGR, buoyed by electric-motor assemblies that unfurl in under 10 seconds and integrate seamlessly with mobile apps. Semi-automatic units appeal to mid-range buyers seeking partial labor savings without the full premium.

Automation benefits from small-format lithium-ion packs and optional solar trickle-charging that extend standby life, alleviating range anxiety for EV owners. Manufacturers tout noise levels below 50 dB to assuage residential-area concerns. Over time, enhanced battery densities and falling actuator prices are expected to narrow cost differentials, positioning automatic options for broader mainstream uptake.

By Material Type: Composite Innovation Challenges, Polyester Dominance

Polyester commanded 46.55% of the car covers market size in 2024, favored for affordability and tested weather resistance. Still, multilayer composites are expanding at a 3.66% CAGR, leveraging nanotechnology membranes that repel water yet vent moisture. Cotton retains indoor niches, while vinyl tackles severe-weather outliers.

EU microplastics policies elevate compliance burdens for pure synthetics, nudging producers toward bio-based fiber blends. Composite developers incorporate recycled PET and cellulose layers to meet circular-economy mandates without forfeiting durability. Although unit prices run two-fifths higher than single-material peers, discerning consumers accept premiums when extended life and multifunctionality offset replacement cycles.

By Vehicle Type: SUV Adoption Mirrors Fleet Shifts

Sedan covers held 36.51% of the car covers market size in 2024, underscoring entrenched compact-vehicle penetration across Europe and Asia. SUV/MUV models, however, lead growth at 3.57% CAGR as households favor larger cabins and higher ground clearance. Hatchback owners gravitate to lightweight, quick-deploy editions that fit constrained urban parking spots.

The shift toward electrified SUVs introduces design angles such as charging port access, zippers, and enhanced ventilation that moderate battery pack temperatures during summer. Enthusiast sports-car owners pay premiums for form-fitting Lycra blends that preserve paint luster, illustrating tailored cover-up-selling potential across vehicle categories.

By Cover Type: Customization Rises Despite Universal Convenience

Universal variants captured 73.25% of the car covers market size in 2024 due to shelf availability and simplified retailer SKUs. Custom-made formats, growing at a 3.59% CAGR, lure owners who prioritize snug fits, reduced flapping, and aesthetics. Digital pattern libraries now exceed 3 lakh vehicle profiles, often trimming production lead times to under five days.

E-commerce configurators harness VIN decoding and 3D visualizations to cut ordering errors, lowering returns and bolstering customer satisfaction. Enthusiast communities embrace photo-realistic graphics and logo licensing, spawning ancillary revenue streams without eroding protective performance.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Offline storefronts still account for 66.72% of car covers market sales in 2024, sustained by installation services and hands-on evaluations. Online channels will, however, advance at a 3.61% CAGR as fitment algorithms and same-day fulfillment build trust. Marketplaces integrate AR overlays that show precise coverage on user-uploaded vehicle images, curbing mis-sizing risk.

Cross-border sellers strike wholesale deals with domestic warehouses, slashing delivery times from Asia to U.S. buyers to as few as three days. Omnichannel pioneers marry live chat, curbside pickup, and hassle-free returns, neutralizing legacy objections around sensory evaluation and post-purchase support.

Geography Analysis

North America generated 37.66% of the car covers market revenue in 2024, propelled by high per-capita vehicle ownership, hail-prone weather patterns, and mature e-commerce logistics. Aging fleets encourage preservation spending, and regional insurers increasingly spotlight protective gear in loss-mitigation advisories. Environmental consciousness sparks interest in recycled fabrics, though regulatory barriers remain low relative to the EU.

The Middle East and Africa log the fastest 3.63% CAGR through 2030. Expanding vehicle fleets, extreme heat, and frequent sandstorms heighten the appeal of UV-reflective and dust-proof covers. Infrastructure projects elevate outdoor parking exposure, while rising disposable incomes in Gulf states and key African metros support premium purchases. Local distributors partner with Asian OEMs to introduce composite fabrics tailored to arid climates.

Europe advances steadily and is shaped by sustainability directives such as the forthcoming digital product passport. Manufacturers must itemize material origins and recyclability, favoring composite fabrics featuring bio-based or recycled inputs. Meanwhile, Asia Pacific operations supply cost-optimized volumes to global buyers. Intra-regional demand hinges on the prevalence of compact cars and dense urban settings that benefit from lightweight, portable designs.

Competitive Landscape

The sector exhibits moderate fragmentation as regional specialists compete alongside diversified aftermarket conglomerates. Covercraft Industries maintains an expansive custom template library and North American manufacturing footprint, leveraging scale to service OEM accessories programs. RealTruck’s acquisition of Vehicle Accessories Group at the beginning of the year broadens its portfolio into SUVs and sedans, signaling consolidation momentum[3]“RealTruck to Acquire Vehicle Accessories Group,” RealTruck Inc., realtruck.com .

Technological differentiation drives premium positioning. Brands integrating IoT modules, UV-blocking nanocoatings, and self-healing films justify double-digit price premiums while fostering brand stickiness. Yet price-sensitive tiers remain contested by Asian exporters whose direct-to-consumer strategies capitalize on cross-border platform efficiencies. Established Western firms counter with multi-year warranties, certified sustainability claims, and domestic fulfillment to buttress value propositions.

Service-based models emerge as a new battleground. Pilot Cover-as-a-Service packages target urban fleet operators seeking operating-expense solutions for asset protection. Early trials highlight the importance of telematics-driven maintenance scheduling and automated billing. Firms that harmonize product engineering with digital-service architectures may carve out resilient competitive moats.

Car Covers Industry Leaders

Covercraft Industries LLC

Coverking Inc.

Budge Industries LLC

RealTruck Holdings Inc.

Zhejiang Mingfeng Industrial Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The European Union introduced textile low-carbon transition regulations, requiring exporters to implement carbon management systems and disclose their product footprints. These regulations affected car-cover producers reliant on synthetic fabrics.

- January 2025: RealTruck, Inc. agreed to acquire Vehicle Accessories Group, marking its largest purchase and extending coverage from trucks and Jeeps into SUV/CUV and sedan accessories.

Global Car Covers Market Report Scope

| Conventional Car Covers |

| Semi-Automatic Car Covers |

| Automatic Car Covers |

| Polyester |

| Cotton |

| Vinyl |

| Nylon |

| Multilayer Composite Fabrics |

| Hatchback |

| Sedan |

| SUV / MUV |

| Sports Cars |

| Universal |

| Custom-Made |

| Online |

| Offline |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Conventional Car Covers | |

| Semi-Automatic Car Covers | ||

| Automatic Car Covers | ||

| By Material Type | Polyester | |

| Cotton | ||

| Vinyl | ||

| Nylon | ||

| Multilayer Composite Fabrics | ||

| By Vehicle Type | Hatchback | |

| Sedan | ||

| SUV / MUV | ||

| Sports Cars | ||

| By Cover Type | Universal | |

| Custom-Made | ||

| By Distribution Channel | Online | |

| Offline | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How significant will global demand for car covers be by 2030?

The car covers market is projected to reach USD 1.13 billion by 2030, advancing at a 3.52% CAGR from 2025.

Which product segment is expanding fastest?

Automatic car covers are forecast to grow at a 3.55% CAGR through 2030, outpacing conventional and semi-automatic formats.

Why are multilayer composite fabrics gaining popularity?

They deliver enhanced UV blocking, breathability, and multi-functionality, driving a 3.66% CAGR despite higher unit costs.

What region offers the highest growth potential?

The Middle East and Africa lead with a 3.63% CAGR, propelled by extreme climate conditions and rising vehicle ownership.

How are stricter EU textile rules affecting suppliers?

Producers must disclose carbon footprints and reduce microplastic content, spurring a shift toward bio-based or recycled materials.

Are car-cover subscription services viable for fleets?

Early pilots indicate promise when integrated with telematics, but profitability hinges on scaling maintenance and education programs.

Page last updated on: