Hydrogen Truck Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

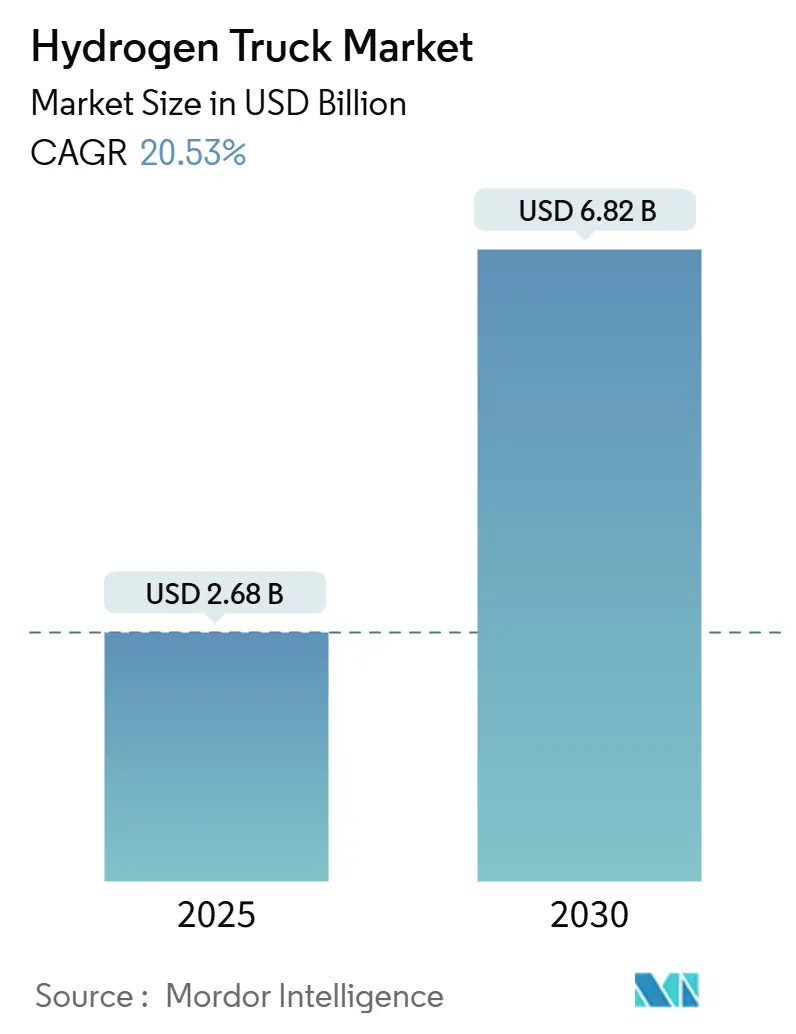

| Market Size (2025) | USD 2.68 Billion |

| Market Size (2030) | USD 6.82 Billion |

| Growth Rate (2025 - 2030) | 20.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

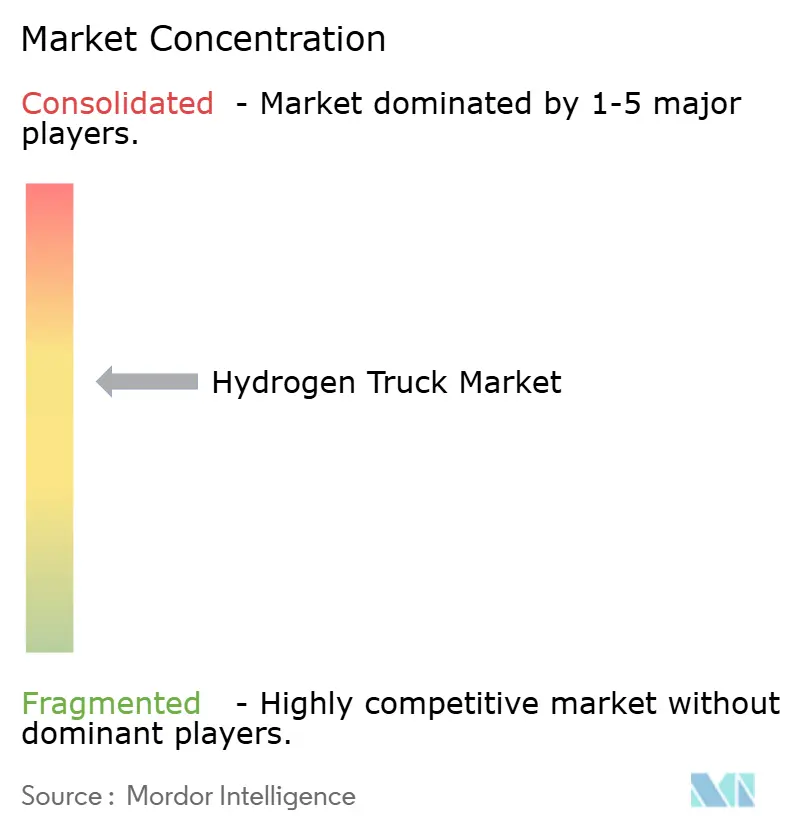

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydrogen Truck Market Analysis by Mordor Intelligence

The hydrogen truck market size stands at USD 2.68 billion in 2025 and is projected to reach USD 6.82 billion by 2030, advancing at a 20.53% CAGR. Growing policy mandates, falling green-hydrogen production costs, and the operational limits of battery electric trucks combine to sustain double-digit expansion. Freight operators favor hydrogen’s superior range and payload for long-haul duty cycles, while zero-emission freight corridors convert pilot deployments into commercial orders. Monetizing surplus renewable energy through hydrogen improves grid stability for utilities and secures fuel supply for fleets. OEM leasing models that shift residual-value risk from buyers to manufacturers lower capital barriers and accelerate adoption.

Key Report Takeaways

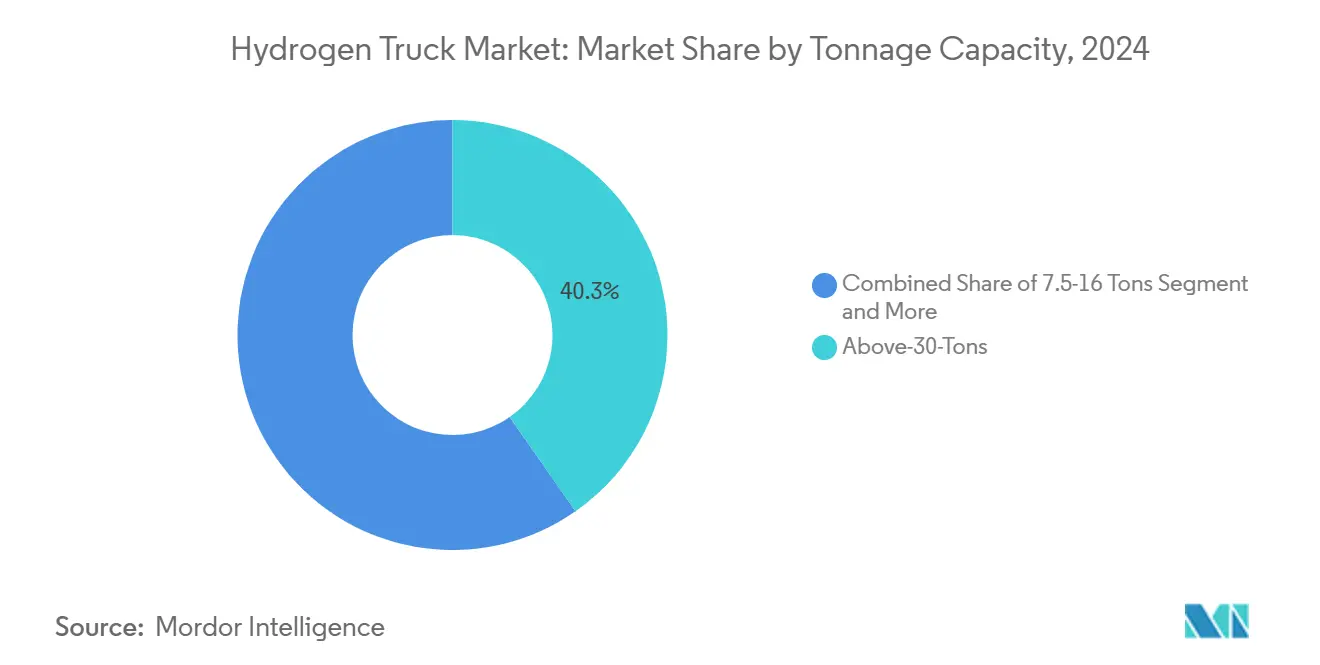

- By tonnage capacity, the above-30-tons category commanded a 40.33% share of the hydrogen truck market size in 2024 and is projected to expand at a 27.67% CAGR between 2025 and 2030.

- By range, the 300-500-mile segment captured 53.63% of the hydrogen truck market size in 2024, whereas the above-500-mile class is expected to rise at a 34.51% CAGR to 2030.

- By application, logistics accounted for a 56.88% share of the hydrogen truck market size in 2024, while mining is advancing at a 31.86% CAGR through 2030.

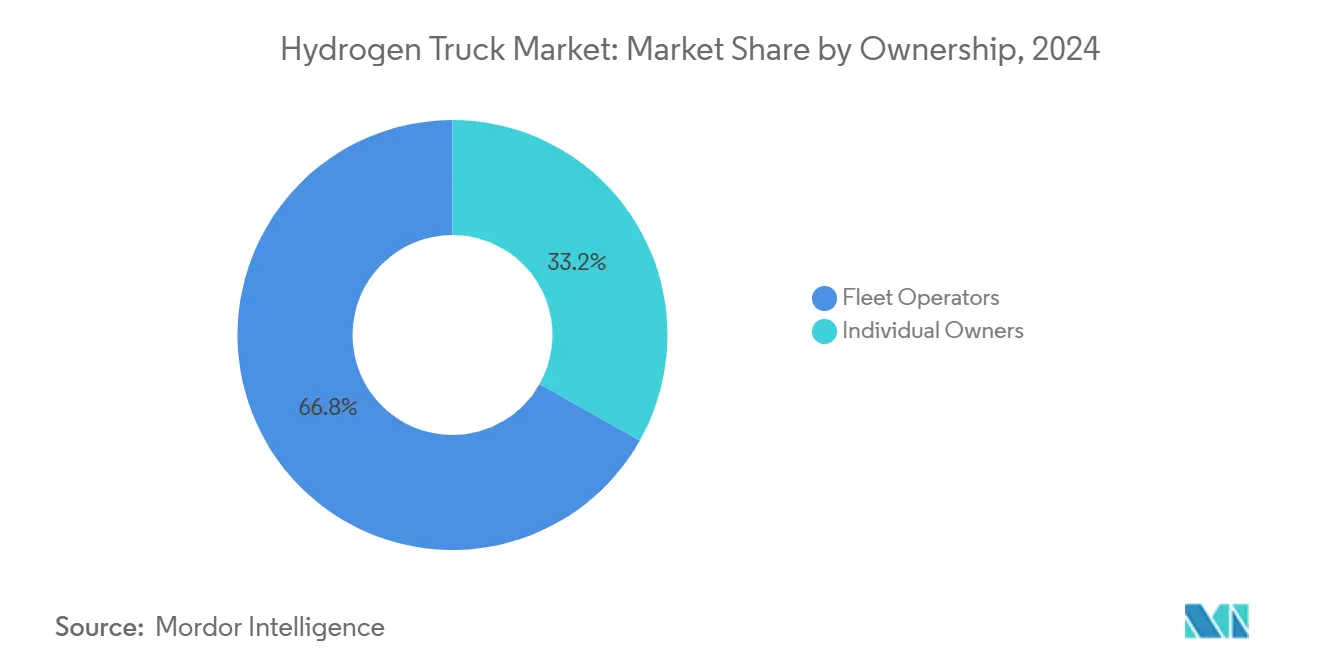

- By ownership, fleet operators led with a 66.83% share of the hydrogen truck market size in 2024 and exhibit a 29.31% CAGR outlook to 2030.

- By body type, box trucks dominated with a 36.66% share of the hydrogen truck market size in 2024; tankers posted the highest projected CAGR at 27.47% to 2030.

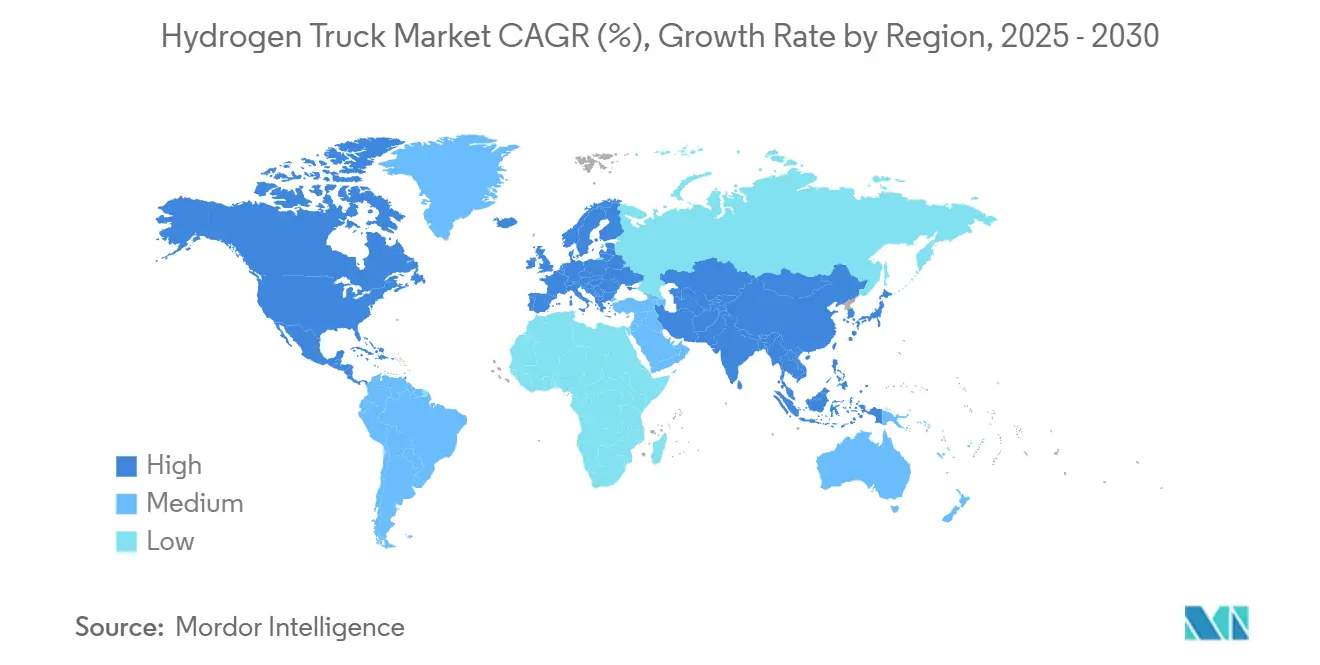

- By geography, Europe led with 44.73% share of the hydrogen truck market size in 2024, and Asia-Pacific is forecasted to register the fastest 25.14% CAGR through 2030.

Global Hydrogen Truck Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green-Hydrogen LCOH Decline | +6.8% | Global, with early gains in Europe, Asia-Pacific | Long term (≥ 4 years) |

| Zero-Emission Freight Corridors | +5.2% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| BEV-Range Limitations | +4.1% | Global | Short term (≤ 2 years) |

| Clean-Fuel Procurement Mandates | +2.9% | Global, with concentration in developed markets | Medium term (2-4 years) |

| Renewable-Energy "Curtailment" Monetization | +1.8% | APAC core, spill-over to Europe and North America | Long term (≥ 4 years) |

| Models Eliminating Residual-Value Risk | +0.7% | North America & EU, early adoption markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Decline in Green-Hydrogen LCOH (Levelized Cost of Hydrogen)

Electrolyzer efficiencies are improving while renewables continue to fall in cost, pushing green-hydrogen prices toward the USD 2-3 per kg threshold that unlocks cost parity with diesel. Japan’s long-term contract-for-difference scheme targets USD 2.2 per kg by 2030, signaling confidence that large-scale procurement can stabilize demand and accelerate industrial learning curves. India’s National Green Hydrogen Mission sets an even lower USD 1-2 per kg stretch goal, encouraging export-oriented production hubs tied to ultra-low-cost solar[1]“National Green Hydrogen Mission Guidelines,” Ministry of New and Renewable Energy, mnre.gov.in. Once regional cost hubs emerge, logistics operators can hedge fuel costs through offtake agreements that mirror today’s LNG contracting structures.

Expansion of Zero-Emission Freight Corridors

Coordinated public-private investment concentrates refueling stations along high-traffic routes, lifting station utilization, and de-risking early projects. The U.S. Department of Energy's funding to launch regional hydrogen hubs integrating production, storage, and dispensing focuses on corridor build-out from ports to inland warehousing centers[2]“Regional Hydrogen Hubs Investment Program,” U.S. Department of Energy, energy.gov. Europe’s Alternative Fuels Infrastructure Regulation mandates that hydrogen stations be placed every 200 km on the Trans-European Transport Network by 2030, creating contiguous coverage across borders[3]“Alternative Fuels Infrastructure Regulation Implementation,” European Commission, ec.europa.eu. Freight corridor visibility allows fleet managers to commit to hydrogen truck market deployments knowing that refueling access will match duty-cycle requirements. Higher utilization accelerates breakeven for station owners, crowding in private capital that scales networks beyond initial subsidies.

BEV Range Limitations for Long-Haul Duty Cycles

Battery electric platforms require around 8-12 tons of batteries to deliver 400-mile range, cutting payload capacity by up to 20%. Hydrogen trucks retain full payload while matching diesel refueling times, enabling trip schedules without extended charging downtime. For freight lanes above 300 miles, operational modeling shows hydrogen yields higher asset turns and revenue per truck despite higher per-mile fuel costs. Payload preservation is even more critical in bulk commodities and temperature-controlled freight where gross-vehicle-weight limits cap revenue. Utility-scale chargers also strain depot power connections, whereas onsite electrolysis or delivered hydrogen decouples fueling from peak electricity demand. Fleet operators in mining and construction report 10-15 minute refills that keep equipment in productive service around the clock, an uptime advantage that BEV architectures cannot replicate without expensive battery swaps.

Clean-Fuel Procurement Mandates from Global Shippers

Multinational shippers are embedding zero-emission clauses into transport contracts to meet 2040 net-zero pledges. Europe’s Corporate Sustainability Reporting Directive forces large companies to disclose Scope 3 logistics emissions, turning emissions data into a competitive tender criterion. Procurement mandates give carriers guaranteed offtake volumes, improving project finance terms for hydrogen infrastructure. Banks treat take-or-pay contracts similarly to power-purchase agreements, lowering the cost of capital for green-hydrogen hubs. Forward freight contracts that bundle fuel and haulage offer fleets price certainty, enabling them to amortize fuel-cell trucks over predictable cash flows. The resulting demand pull offsets early-stage cost premiums and establishes a virtuous cycle of higher station throughput and lower delivered hydrogen prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited H₂ Refuelling Network | -4.3% | Global, most acute in developing markets | Medium term (2-4 years) |

| Higher TCO Versus Diesel Subsidy | -3.1% | Emerging markets, rural areas | Long term (≥ 4 years) |

| Power-Train Durability | -1.8% | Global | Medium term (2-4 years) |

| H₂ Price Volatility | -1.2% | Regions dependent on gray hydrogen | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Public H₂ Refueling Network Density

Station scarcity forces route planning around fuel availability rather than logistics efficiency. In many developed markets, average spacing still sits at 200-300 miles, impeding cross-border freight where infrastructure investments remain uneven. Regulations such as the EU station spacing rule will close gaps by 2030, yet rural and secondary freight corridors risk falling behind. Private hubs that serve captive fleets improve economics, but broader adoption depends on open-access networks that match diesel’s ubiquity.

Higher TCO Versus Diesel in Low-Subsidy Regions

Hydrogen fuel costs between USD 8-15 per kg where supply relies on small-scale or gray-hydrogen feedstocks, translating into a 2-3× premium over diesel energy cost. Acquisition prices keep payback periods above six years if public incentives are absent. Extended warranties and maintenance packages mitigate operational risk, yet financing remains challenging for smaller operators outside high-subsidy jurisdictions. Continuous decline in electrolyzer capex and scaling of vehicle production are essential to close the TCO gap organically.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tonnage Capacity: Above 30 Tons Leads Market Share

The above-30-tons bracket represented 40.33% of the hydrogen truck market share in 2024 and is forecast to grow at a 27.67% CAGR. Industries moving steel coils, timber, and heavy machinery demand every pound of legal payload, making hydrogen’s lighter energy storage a competitive differentiator. Trials using sub-cooled liquid hydrogen tanks have matched diesel range across Alpine passes, confirming suitability for steep-grade freight. Insurance providers are now underwriting full-payload policies for these units, signaling acceptance of the technology’s safety profile. Infrastructure investors favor this segment because predictable long-haul lanes increase station utilization.

The 16-30 tons category services regional freight, ready-mix concrete, and tanker farms that typically stage vehicles at a fixed depot each night. These operators value hydrogen’s rapid refueling because trucks often cycle multiple deliveries per shift under tight construction timetables. Lighter segments address parcel and beverage distribution where stop-start patterns erode battery efficiency, yet hydrogen maintains cabin HVAC and lift-gate power without range anxiety. OEMs have begun offering modular stack packages so fleets can up- or down-rate vehicles without changing the chassis. As total-cost-of-ownership curves flatten, cross-segment migration is likely, but the heaviest classes will remain hydrogen’s primary beachhead.

By Range: 300-500 Miles Captures Largest Share

The 300-500-mile band accounted for 53.63% of the hydrogen truck market in 2024, aligning with round-trip lanes between ports, rail ramps, and inland distribution centers. Carriers in this mileage sweet spot need a single refuel daily, allowing asset dispatchers to retain current schedules and driver rosters. Hydrogen stations placed every 200 miles along freight corridors now cover most of these routes in Europe and California, minimizing detours. Cost models show fleets recover higher capital outlays within four years once diesel is priced for carbon, strengthening investment cases. Shipper sustainability clauses further reinforce adoption by guaranteeing load volumes on zero-emission tractors.

Segments exceeding 500 miles register the fastest 34.51% CAGR because corridor build-outs enable coast-to-coast planning without range anxiety. Pilot programs on the U.S. I-80 and Europe’s Rhine-Alpine artery demonstrate 900-mile operations with one mid-lane refuel, paving the way for broader long-distance freight. Routes below 300 miles remain contested by battery options, yet hydrogen retains niches in refrigerated and hazmat carriage where energy-hungry auxiliaries drain batteries quickly. Operators balancing mixed fleets note that hydrogen units backstop battery trucks when charger queues lengthen during peak electricity demand. As refueling redundancy increases, dispatch software can dynamically assign loads to whichever zero-emission tractor delivers the lowest trip cost.

By Application: Logistics Dominates with Mining Showing Fastest Growth

Logistics captured 56.88% of the hydrogen truck market size in 2024 because parcel, retail, and contract freight providers face intense pressure to decarbonize hub-and-spoke networks. Hydrogen tractors haul line-haul segments overnight, handing off to battery vans for last-mile delivery, optimizing each technology’s strengths. Corporate clients stipulate zero-emission service levels in tenders, effectively creating captive demand for hydrogen capacity on trunk routes. Dedicated fleet depots simplify station siting by aggregating fuel throughput in one location, enhancing project returns for infrastructure investors. Government clean corridor funding further subsidizes station construction along high-volume logistics lanes.

Mining shows the highest 31.86% CAGR because open-pit operations rely on massive haul trucks that cycle continuously and cannot wait hours to charge. Remote sites often lack grid capacity for megawatt-scale chargers, so many operators co-locate solar and electrolysis to produce fuel onsite. Hydrogen’s high gravimetric energy density also reduces vehicle mass, enabling heavier payloads per trip up inclined haul roads. Early adopters in Chile and Australia report maintenance savings due to fewer moving parts than in diesel engines, which is critical where downtime costs millions per hour. As more mines adopt hydrogen, suppliers are bundling mobile refuelers and modular electrolyzers to accelerate deployment timelines.

By Ownership: Fleet Operators Lead Adoption

Fleet operators held 66.83% of the hydrogen truck market size in 2024 and exhibit a 29.31% CAGR because centralized ownership allows high station utilization and bulk-fuel contracting. Many large carriers now sign ten-year take-or-pay agreements with fuel suppliers, locking in prices well below retail pump rates. Leasing packages that bundle the tractor, maintenance, and hydrogen simplify budgeting and shift technology risk back to OEMs. Integrated telematics platforms optimize refuel timing to coincide with driver breaks, ensuring asset uptime. Banks are increasingly willing to finance these contracts as they resemble power-purchase agreements in the renewable energy sector.

Individual ownership remains limited, yet interest is growing among hazmat haulers and specialized vocational operators that command fuel surcharges. Access to public stations still poses challenges, so regional cooperatives are emerging to co-fund depots near highway interchanges. Technology learning curves slowly cut sticker prices, enabling small business loans to cover longer amortization schedules. Government voucher programs in California and Germany likewise offset incremental capex for owner-operators. Over the forecast horizon, a gradual democratization of station access could narrow the gap between fleet and individual uptake, though fleets will likely maintain leadership.

By Body Type: Box Trucks Lead with Tankers Showing Highest Growth

Box trucks accounted for 36.66% of the hydrogen truck market in 2024, propelled by high e-commerce volumes and retail replenishment cycles. Their large, enclosed bodies pair well with palletized freight that demands tight delivery windows, so any reduction in loading time or route flexibility carries financial penalties. Hydrogen’s rapid refuel keeps these assets circulating through cross-dock hubs without queue-related idling. Temperature-controlled box variants leverage the fuel cell’s waste heat and electricity to power refrigeration units, extending cold-chain integrity during traffic delays. Municipal zero-emission zones in Europe further accelerate urban box-truck adoption by imposing surcharges on diesel entries.

Tankers register the steepest 27.47% CAGR as chemicals, fuels, and liquid food producers shift to low-carbon logistics under safety and ESG mandates. Fuel cells operate at lower combustion temperatures, mitigating ignition risks when transporting flammables, and hydrogen exhaust contains only water vapor, reducing contamination concerns. The reduced refuel time compared with battery trucks safeguards tight delivery slots at petrochemical terminals, where berth fees penalize delays. Specialized cryogenic tanker fabricators are already certifying hydrogen-ready trailers, facilitating fleet conversions without redesigning entire logistics schemes. Elsewhere, flatbed, tipper, and refrigerated bodies carve out roles in construction and agriculture, rounding out a diversified adoption landscape.

Geography Analysis

Europe remained the largest regional market with a 44.73% share in 2024. The Alternative Fuels Infrastructure Regulation and the Corporate Sustainability Reporting Directive jointly push carriers toward hydrogen to satisfy station density mandates and disclosure requirements. Germany spearheads infrastructure rollout through KfW-backed grants, and cross-border pilots such as the H2Haul program validate performance on pan-European freight corridors. OEM trials with Amazon and Air Products operate along Benelux-to-Germany lanes, demonstrating commercial payloads over Alpine passes.

Asia-Pacific posts the fastest 25.14% CAGR through 2030 as China subsidizes domestic fuel-cell truck production and Japan legislates long-term price guarantees for green hydrogen. South Korea expands stack production capacity and invests in port bunkering to support export shipping requiring zero-emission drayage. India’s green-hydrogen mission stimulates electrolyzer manufacturing and positions coastal states as export hubs for compressed hydrogen destined for Middle Eastern and European buyers.

North America grows on the back of federal hydrogen hubs. Canadian provinces co-fund corridor stations linking British Columbia ports with Alberta’s petrochemical centers. Mexico evaluates public-private frameworks to align with United States-Mexico-Canada Agreement sustainability clauses. South America and other regions show moderate growth as infrastructure development and policy support lag behind leading markets, while Brazil explores hydrogen for soy and iron-ore export corridors though remains in early feasibility stages.

Competitive Landscape

Market concentration remains moderate, creating opportunities for emerging competitors to establish regional strongholds or application-specific niches. Traditional truck makers leverage dealer networks to scale service coverage, whereas pure-play startups focus on vertical integration of stacks and storage to shorten learning curves. Strategic alliances proliferate; for example, a non-binding memorandum pairs General Motors' fuel-cell systems with Hyundai's chassis to accelerate homologation for the North American market.

Differentiation shifts from raw range claims to lifecycle economics. Subcooled liquid hydrogen tanks extend the range without adding cylinders, while proprietary power electronics enhance stack durability by 25,000 hours. Leasing and pay-per-mile models remove residual-value anxiety, enticing risk-averse fleets. Suppliers target niche verticals, mining for Anglo-Australian majors, port drayage in California, and Alpine transportation in Switzerland, to secure anchor customers before moving to volume segments.

Market entrants from China and India eye export opportunities as domestic scale drives down stack and balance-of-plant costs. Intellectual-property barriers remain in membranes and catalysts, yet global supply chains for carbon-fiber tanks and compressors encourage knowledge diffusion. Regulatory convergence on safety codes eases multi-region platform deployment, intensifying competition on price and after-sales support rather than technology access alone.

Hydrogen Truck Industry Leaders

Hyundai Motor Company

Nikola Corporation

Daimler Truck AG

Hino Motors (Toyota–Hino)

Hyzon Motors

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Toyota Motor Europe began operating five heavy-duty trucks equipped with hydrogen fuel-cell systems across Belgium, France, Germany, and the Netherlands in partnership with VDL Groep.

- May 2025: Adani Enterprises launched India’s first 40-ton hydrogen fuel-cell truck, featuring smart telemetry and three onboard tanks for 200 km range.

- April 2025: Hyundai Motor Company unveiled the next-generation XCIENT Fuel Cell Class-8 truck at the ACT Expo 2025 in Anaheim, expanding its North American roadmap.

- March 2025: Tata Motors initiated 24-month trials of 16 hydrogen-powered heavy-duty trucks with varied payload configurations for long-haul applications.

Global Hydrogen Truck Market Report Scope

| 3.5 to 7.5 Tons |

| 7.5 to 16 Tons |

| 16 to 30 Tons |

| Above 30 Tons |

| Below 300 miles |

| 300 to 500 miles |

| Above 500 miles |

| Logistics |

| Construction |

| Agriculture |

| Mining |

| Utility |

| Others |

| Fleet Operators |

| Individual Owners |

| Flatbed |

| Box Truck |

| Refrigerated |

| Tanker |

| Tipper |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Tonnage Capacity | 3.5 to 7.5 Tons | |

| 7.5 to 16 Tons | ||

| 16 to 30 Tons | ||

| Above 30 Tons | ||

| By Range | Below 300 miles | |

| 300 to 500 miles | ||

| Above 500 miles | ||

| By Application | Logistics | |

| Construction | ||

| Agriculture | ||

| Mining | ||

| Utility | ||

| Others | ||

| By Ownership | Fleet Operators | |

| Individual Owners | ||

| By Body Type | Flatbed | |

| Box Truck | ||

| Refrigerated | ||

| Tanker | ||

| Tipper | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the hydrogen truck market by 2030?

The hydrogen truck market is forecast to reach USD 6.82 billion by 2030 based on a 20.53% CAGR growth trajectory.

Why are fleet operators seen as the prime buyers?

Fleet operators capture 66.83% share because centralized ownership optimizes refueling infrastructure and leverages OEM leasing to reduce capital outlay.

Which region is expanding fastest through 2030?

Asia-Pacific is projected to post the quickest 25.14% CAGR, driven by strong policy incentives in China, Japan, South Korea, and India.

What infrastructure trend supports hydrogen truck deployment?

Zero-emission freight corridors backed by government funding create contiguous refueling networks that reduce range-anxiety barriers for long-haul carriers.

How does hydrogen compare with battery electric for payload?

Hydrogen trucks preserve full payload capability because fuel cells weigh far less than the large battery packs required for 400-mile BEV range.

Page last updated on: