Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 52.33 Billion |

| Market Size (2026) | USD 57.19 Billion |

| Market Size (2031) | USD 89.18 Billion |

| Growth Rate (2026 - 2031) | 9.29% CAGR |

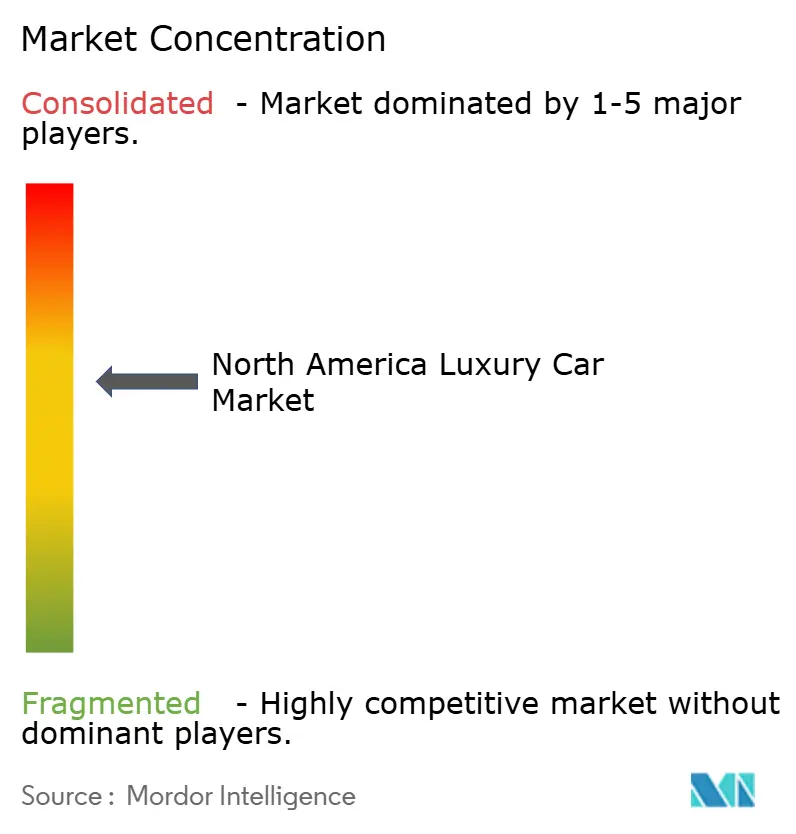

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Luxury Car Market Analysis by Mordor Intelligence

The North America luxury car market size was valued at USD 52.33 billion in 2025 and estimated to grow from USD 57.19 billion in 2026 to reach USD 89.18 billion by 2031, at a CAGR of 9.29% during the forecast period (2026-2031). The expansion rests on a generational shift as wealth moves to millennials and Gen-Z, who place a higher weight on digital integration, electrification, and responsible sourcing. Luxury nameplates are launching SUV-heavy portfolios, enlarging average selling prices, and protecting margins even as financing costs rise. The pivot toward battery-electric nameplates, spurred by Canadian purchase incentives and stricter fleet-emission rules, further elevates demand for premium EVs. Supply-side investments in localized battery packs, coupled with over-the-air upgrade revenues, allow automakers to absorb raw-material volatility while keeping profit pools attractive. Meanwhile, digital retail channels build relevance among affluent digital natives, accelerating a wider move away from exclusive reliance on franchised dealers.

Key Report Takeaways

- By vehicle type, SUVs and crossovers led with 55.18% of the North America luxury car market share in 2025 while recording a forecast of 10.52% CAGR through 2031.

- By drive type, battery-electric vehicles will post the fastest growth at an 10.76% CAGR, whereas internal-combustion engines retained 64.70% share of the North America luxury car market size in 2025.

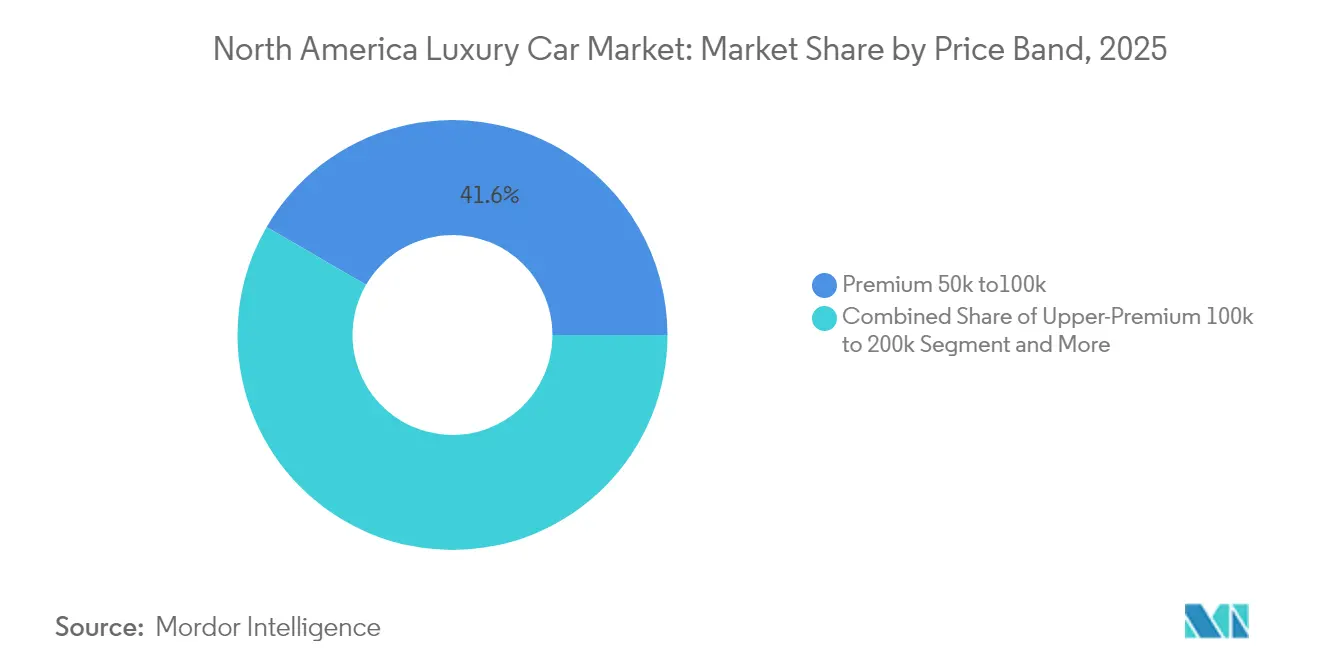

- By price band, the premium tier (USD 50,000-100,000) accounted for 41.62% of the North America luxury car market size in 2025; the upper-premium tier (USD 100,000-200,000) is projected to expand at 11.88% CAGR to 2031.

- By sales channel, franchised dealers held 60.92% revenue share in 2025, but online marketplaces are advancing at an 11.21% CAGR through 2031.

- By geography, the United States commanded an 82.10% share in 2025, whereas Canada is set to grow at a 10.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Luxury Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gen-Y / HNWI Premiumization | +2.1% | North America Metros | Medium term (2-4 years) |

| ≥50% Luxury EV Target | +1.8% | Global, faster in Canada | Long term (≥ 4 years) |

| SUV-Heavy Mix Lifts ASPs | +1.4% | US suburbs | Short term (≤ 2 years) |

| OTA Feature Revenues | +0.9% | Tech-forward regions | Medium term (2-4 years) |

| Luxury Ride-Hailing & Subs | +0.6% | Key US & CA cities | Long term (≥ 4 years) |

| Blockchain CPO Programs | +0.4% | Major North America metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premiumization Momentum Among Gen-Y/HNWIs

Wealth reallocation toward millennials and Gen-Z means that 40% of high-net-worth buyers choosing premium vehicles now come from these cohorts [1]“Consumer Checkpoint: Affluent Demographics and Spending,” Bank of America Institute, bankofamerica.com. Their purchase logic favors embedded software, green footprints, and personalized experiences, pushing brands to craft omnichannel storefronts, connected-service bundles, and subscription-based access models. The emphasis on technology platforms rather than static status symbols raises the strategic value of over-the-air update capability and service-based upselling.

Automaker Push Toward ≥50% Luxury EV Mix by 2030

BMW Group ties senior bonuses to electrified-vehicle penetration and has aligned North American launches accordingly [2]“Annual Report 2025,” BMW Group, bmwgroup.com. Canadian rebates magnify the effect, prompting faster model cadence in that market. While capital flows favor battery supply localization, firms must juggle near-term ICE profitability with heavy EV capex, making portfolio balancing a critical executive KPI.

SUV-Centered Product-Mix Realignment Raises ASPs

Affluent households prefer luxury SUVs for their commanding stance and lifestyle flexibility, enabling 15-20% higher transaction prices versus sedans. Carmakers leverage the roomier platforms to integrate flagship infotainment, sustainable interiors, and performance-oriented battery packs, reinforcing SUVs as the segment’s prestige backbone.

OTA-Driven Feature-on-Demand Revenue Streams

BMW reports early success monetizing driver-assist packages and enhanced infotainment through post-sale activations. Continuous software releases keep vehicles current and extend life-cycle value, creating a flywheel of higher gross margins while delivering personalized add-ons that resonate with tech-savvy owners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| APR Spikes | -1.6% | Across North America | Short term (≤ 2 years) |

| BEV Resale Doubts | -1.2% | Global, premium EV segments | Medium term (2-4 years) |

| Battery Origin Rules | -0.8% | United States, EV supply chains | Medium term (2-4 years) |

| ADAS Litigation Risk | -0.5% | North America, regulatory focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inflation-Induced APR Spikes Squeeze Leasing Uptake

Lease payments have risen 25-30% versus pre-inflation benchmarks, disproportionately affecting younger aspirational buyers and eroding the entry-luxury funnel. Automakers are countering with longer-tenor leases, subscription pilots, and interest-rate buydowns to protect volume.

BEV Resale-Value Uncertainty Dents Buyer Confidence

Rapid battery innovation and ambiguous second-life economics drive depreciation anxiety, amplifying hesitation in purchasing high-ticket EVs. In the ultra-luxury sphere, anticipated three-year maintenance bills can exceed USD 450,000, as seen with the Aston Martin Valkyrie. Manufacturers respond with buy-back guarantees and long-horizon battery warranties to safeguard brand equity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUVs Extend Market Leadership

The North America luxury car market size attributed to SUVs reached 55.18% in 2025, supported by a 10.52% forecast CAGR. Positioning SUVs as technology flagships unlocks superior margins, letting manufacturers offset electrification costs. Continuous EV SUV introductions by BMW, Mercedes-Benz, and newcomers sustain momentum. Sedans continue to resonate in densely populated metros yet yield ground to SUVs among younger families. Coupes, convertibles, and hatchbacks serve enthusiast niches, collectively under 5% of volume.

A longer wheelbase allows SUVs to house larger battery packs without cabin compromise. Consequently, battery-electric SUVs bridge performance expectations and environmental commitments, making them strategic launchpads for next-gen driver-assist suites. The emotional appeal of heightened seating and versatile cargo room cements the SUV as a luxury staple.

By Drive Type: ICE Holds Majority as EV Surges

Internal-combustion engines still represented 64.70% of the North America luxury car market share in 2025, but battery-electric vehicles will log an 10.76% CAGR through 2031. Hybrids provide a transitional hedge for buyers with occasional long-distance needs, while plug-in hybrids give daily electric range without charging network dependency. Lexus’ fuel-cell pilot remains limited by hydrogen infrastructure.

The regulatory blueprint in Canada and state-level zero-emission mandates in the United States compress timelines, motivating OEMs to accelerate dedicated EV platforms. Tesla’s entrenched mindshare forces incumbents to match over-the-air proficiency and charging ecosystems, intensifying capital deployment toward electrification.

By Price Band: Upper-Premium Accelerates Trading-Up Trend

The premium bracket (USD 50,000-100,000) remained the volume anchor at 41.62% of the North America luxury car market size in 2025. Yet the upper-premium tier grows the fastest at 11.88% CAGR as affluent buyers prioritize full-suite ADAS, bespoke interiors, and brand cachet over price sensitivity. Ultra-luxury vehicles priced above USD 200,000 entail extreme ownership costs, where maintenance alone can outstrip the original purchase price of many entry luxury cars.

Pared inventory strategies further propel trading-up behavior when consumers accept higher trims in exchange for shorter waiting times. Digital configuration tools showcasing premium materials and limited-edition specs reinforce upsell momentum.

By Sales Channel: Omnichannel Redefines Retail

Franchised outlets held a 60.92% share in 2025, yet online journeys now influence more than 80% of North America luxury car market purchase decisions. Tesla’s factory-direct model proved compelling, nudging incumbents to roll out reservation portals, remote paperwork, and at-home delivery. A younger demographic welcomes transparent pricing and time-efficient transactions, boosting online marketplaces at an 11.21% CAGR.

Subscription fleets introduce flexibility, bundling insurance, maintenance, and roadside assistance. For manufacturers, direct data capture from digital sales feeds analytics loops that guide personalized service offerings and service-based revenue streams, aligning with over-the-air monetization ambitions.

Geography Analysis

The North America luxury car market is geographically led by the United States, which controlled 82.10% share in 2025. High concentrations of millionaires, established dealer infrastructure, and long-standing brand hierarchies sustain luxury consumption. Yet, climbing student debt and rising mortgage costs place pressure on entry-level luxury adoption. American buyers particularly favor full-sized SUVs and pickup-derived luxury trucks, nudging OEMs to prioritize these body styles.

Canada, although smaller in absolute volume, is forecast to post a 10.55% CAGR as federal incentives of up to CAD 5,000 for zero-emission vehicles tilt the demand mix toward premium EVs. Urban hubs such as Toronto, Vancouver, and Montreal account for the lion’s share of orders, and buyers exhibit higher openness to European makes and electrified drivetrains. BMW Group already ranks among the best-selling premium brands in the country.

Mexico and the rest of North America remain nascent but strategically important. Rising disposable incomes in Mexico City, Monterrey, and Guadalajara encourage aspirational premium purchases, though currency swings and import tariffs introduce volatility. Over time, localized final-assembly initiatives could mitigate cost barriers and unlock mid-single-digit regional growth.

Competitive Landscape

The North America luxury car market features a crowded field of German stalwarts—BMW, Mercedes-Benz, and Audi—alongside American badges such as Cadillac and Lincoln, and pure-play electric specialists led by Tesla. Each marque guards long-standing brand equity while pursuing fresh digital storefronts that echo Tesla’s factory-direct experience. Newcomers Lucid and Rivian sharpen the contest by offering performance-first EVs paired with concierge-level after-sales touchpoints.

Incumbent automakers hedge their profitable ICE portfolios while assigning multibillion-dollar budgets to dedicated EV architectures, battery plants, and software-defined vehicle platforms. BMW Group directs a sizable North American capital program toward cell production and regionalized assembly to satisfy rules-of-origin provisions. Cadillac accelerates the Celestiq and Escalade IQ pipelines to reclaim premium-EV mindshare, whereas Mercedes-Benz scales its MB.OS operating system to unlock over-the-air monetization.

Regulation intensifies both opportunity and risk. NHTSA’s proposed automatic-emergency-braking mandate promises sizeable safety benefits but raises compliance thresholds that favor brands with mature ADAS stacks [3]“Automatic Emergency Braking Notice of Proposed Rulemaking,” National Highway Traffic Safety Administration, nhtsa.gov. Battery end-of-life rules are nudging firms to launch certified second-life programs that bolster sustainability narratives and reassure affluent buyers. In parallel, subscription-centric revenue models and performance-unlock downloads underscore a broader pivot toward software as a primary battleground for differentiation.

North America Luxury Car Industry Leaders

Tesla Inc.

BMW AG

Mercedes-Benz Group AG

Volkswagen AG

Toyota Motor Corporation (Lexus)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Ford Motor Company partnered with Nissan to leverage spare capacity at a Kentucky battery facility after booking USD 5 billion losses in its EV division during 2024 and projecting similar pressure for 2025, triggering a recalibration of Lincoln’s electrification timeline.

- March 2025: GMC confirmed the 2026 Sierra EV lineup will add off-road and entry trims to broaden the premium electric truck addressable market and challenge Ford’s Lightning and Rivian’s R1T.

- March 2025: Hyundai Motor Group committed USD 21 billion for US manufacturing through 2028, assigning USD 9 billion to expand Hyundai, Kia, and Genesis assembly in Alabama and Georgia, adding 14,000 jobs and boosting Genesis capacity.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study captures the North America luxury car market as all factory-new passenger vehicles retailing above USD 50,000, spanning sedans, coupes, convertibles, hatchbacks, and SUVs that are delivered through franchised or brand-owned outlets across the United States, Canada, and the rest of the region.

Scope exclusion: Pre-owned imports, commercial vans, rental fleets, and aftermarket accessories fall outside our boundary.

Segmentation Overview

- By Vehicle Type

- Sedan

- SUV/Crossover

- Hatchback

- Coupe

- Convertible

- By Drive Type

- Internal Combustion Engine (ICE)

- Mild/Full Hybrid

- Plug-in Hybrid Vehicle (PHEV)

- Battery-Electric Vehicle (BEV)

- Fuel-Cell Electric Vehicle (FCEV)

- By Price Band

- Premium 50k USD to 100k USD

- Upper-Premium 100k USD to 200k USD

- Ultra-Luxury Above 200k USD

- By Sales Channel

- Franchised Dealer

- Direct-to-Consumer

- Online Marketplace

- Subscription/Lease Fleet

- By Country

- United States

- Canada

- Rest of North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts spoke with luxury dealer principals, regional sales managers, premium-finance executives, and EV infrastructure planners across the United States and Canada. These conversations verified trim-level volumes, clarified discount structures that published MSRPs rarely show, and highlighted fast-moving demand pockets, thereby filling gaps left by secondary sources.

Desk Research

We anchored the desk phase on public data series from sources such as the US Bureau of Economic Analysis, Statistics Canada, the Bureau of Transportation Statistics, and the International Organization of Motor Vehicle Manufacturers, which outline new-vehicle registrations, price brackets, and propulsion splits. Trade association briefs (Alliance for Automotive Innovation, Global Automakers of Canada) and regulatory repositories (US EPA GHG filings) gave us penetration clues for hybrid and battery-electric trims.

Company 10-Ks, dealer group filings, brand presentation decks, and news archives accessed through Dow Jones Factiva and D&B Hoovers enriched revenue and average transaction price benchmarks, while Marklines helped us spot monthly model launches. This list is illustrative; many more publications informed data collection and sense-checks.

Market-Sizing & Forecasting

We start with a top-down reconstruction of demand that multiplies new-registration counts in the luxury segment by average retail transaction prices, adjusted for incentives. Results are then cross-checked against a sampled bottom-up roll-up of OEM wholesale shipments and channel checks. Variables that feed our model include luxury penetration within total light-vehicle sales, SUV share, BEV share, household disposable income, and federal funds rate trends, all projected through a multivariate regression blended with scenario analysis for fuel-price shocks. Where supplier roll-ups deviate materially, the delta is apportioned back to pricing or mix shifts before final lock.

Data Validation & Update Cycle

Outputs pass anomaly and variance screens, followed by multi-analyst review. We refresh the model annually and issue interim updates when incentives, trade rules, or model launches materially change baselines, ensuring clients receive the latest view before every delivery.

Why Our North America Luxury Car Baseline Earns Trust

Published numbers often diverge because firms apply different price cutoffs, include pre-owned or fleet channels, or refresh data on uneven cadences. We, however, lock scope to factory-new units, apply verified transaction prices, and revisit assumptions every year, which is where Mordor Intelligence distinguishes itself.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 52.33 B (2025) | Mordor Intelligence | |

| USD 160.10 B (2024) | Regional Consultancy A | Includes pre-owned sales and Mexico, limited primary validation |

| ~USD 150 B (2025) | Industry Association B | Counts fleet leasing and rental turnover, uses MSRP without discount checks |

The comparison shows that when scope broadens or prices are assumed at face value, totals inflate rapidly. Our disciplined segmentation and continuous primary verification give decision-makers a balanced, transparent baseline they can track and replicate.

Key Questions Answered in the Report

What is the current value of the North America luxury car market?

The market stands at USD 57.19 billion in 2026 and is forecast to reach USD 89.18 billion by 2031, marking a 9.29% CAGR.

Which vehicle type dominates sales?

SUVs lead with 55.18% share in 2025 and are projected to grow at a 10.52% CAGR through 2031.

How fast is the luxury EV segment expanding?

Battery-electric vehicles are set to grow at an 10.76% CAGR, the quickest among drivetrains, reflecting policy support and model proliferation.

What geographic market is growing the quickest?

Canada is the fastest-expanding geography, expected to post a 10.55% CAGR through 2031 due to generous EV incentives.

Page last updated on: