Hummus Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.43 Billion |

| Market Size (2031) | USD 6.02 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hummus Market Analysis by Mordor Intelligence

The hummus market size is expected to grow from USD 4.17 billion in 2025 to USD 4.43 billion in 2026 and is forecast to reach USD 6.02 billion by 2031 at 6.33% CAGR over 2026-2031. This market growth is heavily fueled by Dietary recommendations advocating for increased legume consumption and a decrease in red meat intake are fueling this growth. Plant-based snacks are gaining rapid consumer traction due to their clean labels, elevated protein content, and lower saturated fat profiles compared to conventional spreads, supporting growth in the hummus market. To capture this demand, grocery retailers are expanding their refrigerated dips sections, strategically placing products at eye level, and employing cross-merchandising tactics to amplify impulse buys. Thanks to advancements in high-pressure processing (HPP) technology has successfully extended product, the shelf life without the need for preservatives. This innovation facilitates smoother distribution across the hummus market via e-commerce and quick-commerce platforms. By diversifying flavor offerings and emphasizing sustainable sourcing, manufacturers are not only navigating the challenges of fluctuating raw material prices but also preserving their premium pricing strategy.

Key Report Takeaways

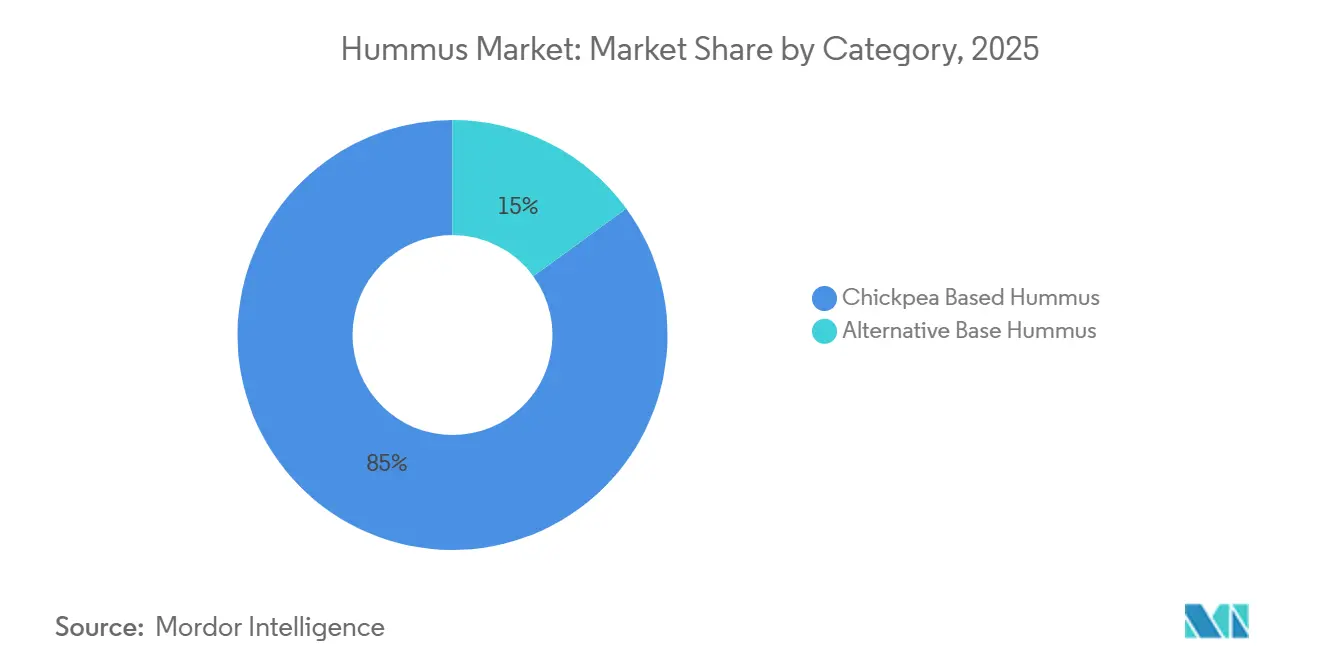

- By category, chickpea-based products led with 85.01% of the hummus market share in 2025; alternative-base hummus is forecast to expand at a 7.89% CAGR through 2031.

- By flavor type, original variants held 38.11% revenue share in 2025, while black-olive profiles are advancing at an 8.03% CAGR to 2031.

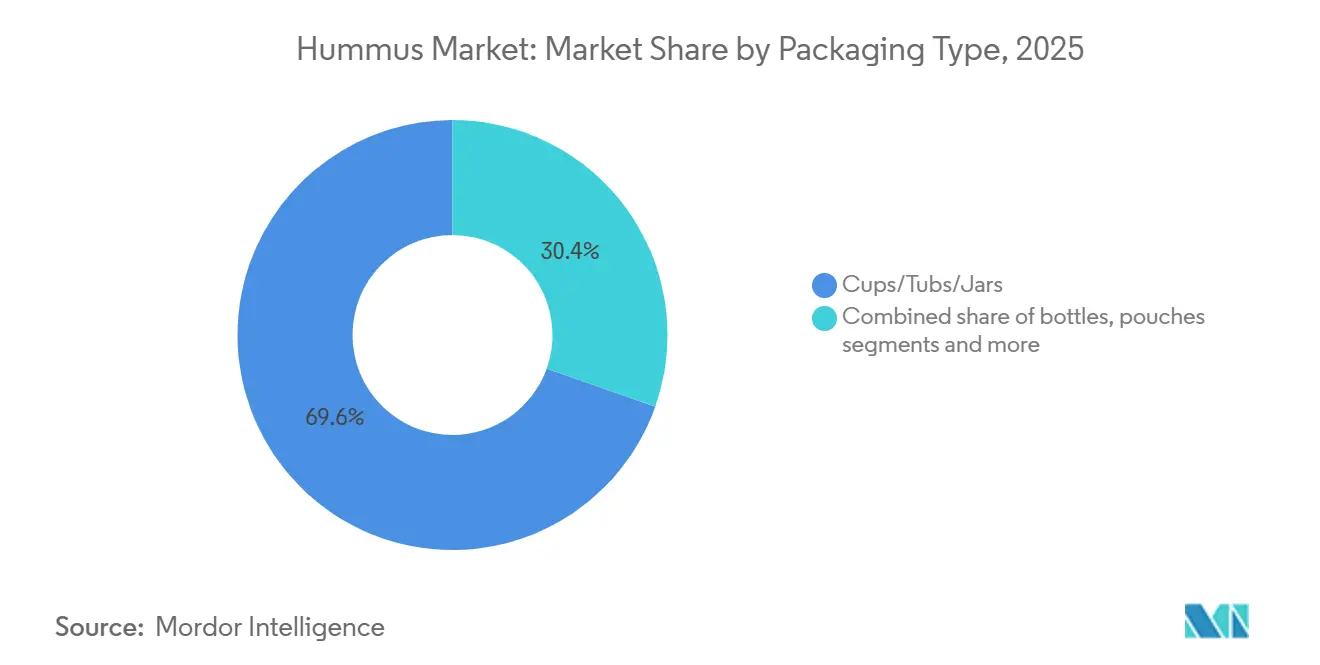

- By packaging, cups/tubs/jars accounted for 69.58% of the hummus market size in 2025; bottle formats will record the fastest 7.66% CAGR during 2026-2031.

- By distribution channel, off-trade captured 82.43% share in 2025; on-trade is projected to grow fastest at 8.14% CAGR to 2031.

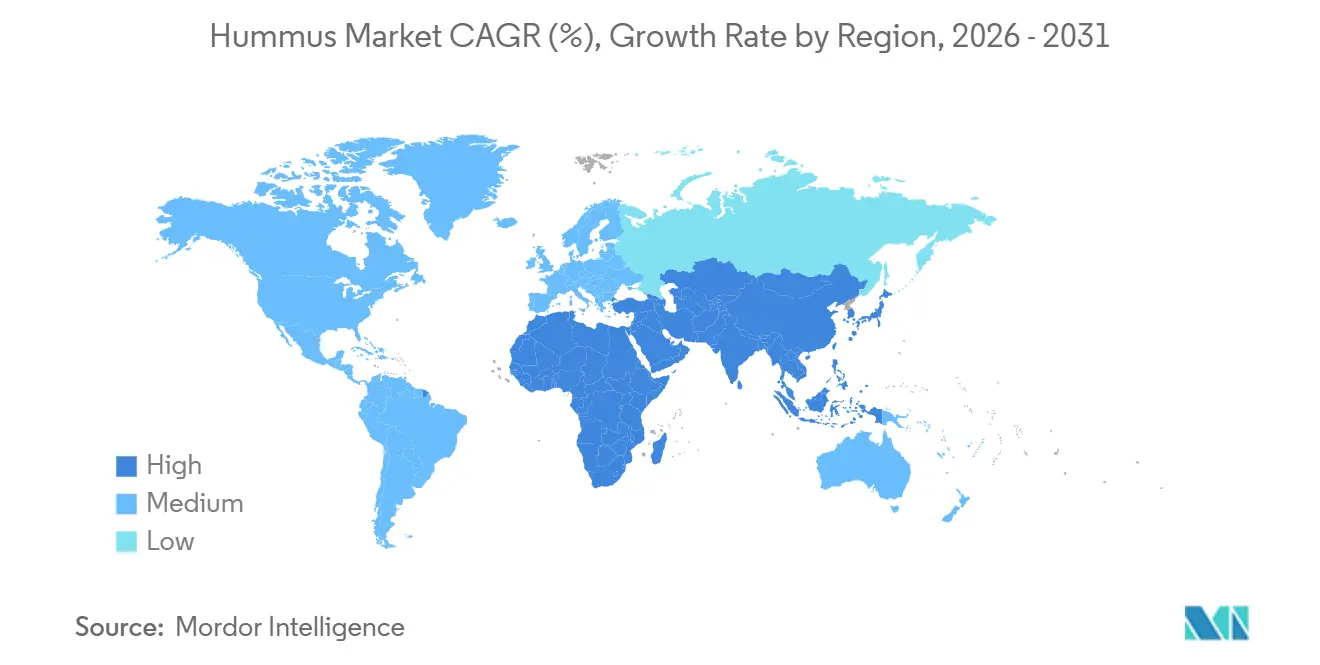

- By geography, North America commanded 38.45% of global value in 2025; the Middle East and Africa region is set to post the highest 8.47% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hummus Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer preference for plant-based and vegan foods | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rising awareness of health benefits of chickpeas, such as high protein and fiber content | +0.9% | Global | Long term (≥ 4 years) |

| Rising global ethnic cuisine interest, leading to new product launches and flavor innovation | +1.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising adoption of Mediterranean diet trends across Europe and North America | +0.8% | Europe and North America | Long term (≥ 4 years) |

| Growth in fast-casual and QSR outlets offering hummus-based products | +1.3% | North America, Europe, Middle East | Short term (≤ 2 years) |

| Demand for clean-label and preservative-free hummus | +1.0% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing consumer preference for plant-based and vegan foods

The increasing consumer preference for plant-based and vegan foods is a key driver of the hummus market, as these diets align closely with the product’s natural, protein-rich, and plant-based profile. According to the Good Food Institute 2024 report, around 60% of U.S. households purchased some type of plant-based food, indicating a significant shift toward plant-forward eating habits[1]Source: Good Food Institute, “U.S. retail market insights for the plant-based industry”, gfi.org. In Europe, the trend is similarly strong, with the ProVeg International 2024 report noting that approximately 27% of Europeans identify as flexitarians, while nearly 40% of consumers in Germany follow a flexitarian diet, making it one of the largest plant-based consumer markets in the region[2]Source: Proveg International, “The new flexitarian consumer: insights from ProVeg’s Veggie Challenge”, proveg.org. This growing adoption of plant-forward and vegan diets is driving demand for convenient, nutritious, and versatile products like hummus, which can serve as a healthy snack, spread, or dip. Manufacturers are responding by expanding product lines, offering innovative flavors, and emphasizing clean-label and natural ingredients. The rise in plant-based awareness is particularly influencing retail, online, and foodservice channels, further boosting hummus consumption

Rising awareness of health benefits of chickpeas, such as high protein and fiber content

The rising awareness of the health benefits of chickpeas, particularly their high protein and fiber content, is a key driver of the hummus market. Chickpeas provide 19–25% protein, 12–17% fiber, and essential micronutrients such as iron, zinc, and folate, making hummus a nutrient-dense, plant-based snack that aligns well with dietary guidelines emphasizing legume consumption. Despite these benefits, European dietary guidelines across 11 countries recommend 1–3 servings of legumes per week, yet studies from 2023–2024 indicate that only 37% of European adults meet these targets, highlighting a gap between recommendations and actual intake[3]Source: National Institute of Health, “Mediterranean Diet”, ncbi.nlm.nih.gov. This gap underscores significant untapped market potential, especially if consumer education and convenience barriers are addressed. As awareness grows, more health-conscious consumers are turning to hummus as an easy, tasty way to increase legume intake, particularly in snacks, spreads, and meal accompaniments, further strengthening the hummus market.

Rising global ethnic cuisine interest, leading to new product launches and flavor innovation

The rising global interest in ethnic and Mediterranean cuisine is a significant driver of the hummus market, encouraging manufacturers to introduce new products and innovative flavor profiles. As consumers increasingly explore international flavors, hummus has emerged as a versatile and familiar entry point into Middle Eastern-inspired foods. This trend has led to the launch of gourmet and specialty variants, such as roasted red pepper, black olive, beetroot, and spicy harissa, catering to adventurous and health-conscious consumers alike. Foodservice channels, including restaurants, cafes, and meal kit providers, are also incorporating hummus into fusion dishes, wraps, salads, and snack platters, further increasing exposure. Retailers across the hummus market are responding with ready-to-eat, single-serve, and multipack formats that make ethnic flavors more accessible to mainstream audiences. The growing curiosity for diverse culinary experiences, combined with the demand for plant-based, nutritious foods, is driving both flavor innovation and category expansion.

Rising adoption of Mediterranean diet trends across Europe and North America

The rising adoption of Mediterranean diet trends across Europe and North America is a key driver of the hummus market, as this diet emphasizes plant-based foods, legumes, healthy fats, and whole grains, core attributes of hummus. Consumers are increasingly seeking nutritious, heart-healthy, and protein-rich options, and hummus fits naturally into this dietary pattern as a versatile dip, spread, or snack. The popularity of Mediterranean-inspired meals in restaurants, cafes, and home cooking has also elevated demand in the hummus market, encouraging manufacturers to expand offerings with authentic and innovative flavors. Retailers are responding by stocking a wider range of ready-to-eat, single-serve, and multipack formats to meet the demand for convenient Mediterranean-style foods. Marketing campaigns emphasizing clean-label, plant-based, and nutrient-dense characteristics further reinforce consumer interest.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price volatility and supply shortages | -0.7% | Global, with acute impact in Middle East and North Africa | Short term (≤ 2 years) |

| Product adulteration and recalls | -0.5% | North America, Europe | Medium term (2-4 years) |

| Competition from alternative dips and spreads | -0.4% | North America, Europe | Long term (≥ 4 years) |

| Limited consumer awareness in emerging markets | -0.3% | Asia-Pacific, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw material price volatility and supply shortages

Raw material price volatility and supply shortages pose a significant restraint on the hummus market, affecting both production costs and profit margins. Chickpeas, the primary ingredient in hummus, are subject to fluctuations in global agricultural output due to weather variability, crop diseases, and changing cultivation patterns. Sudden increases in chickpea prices or disruptions in supply chains can lead to higher manufacturing costs, which may be passed on to consumers, potentially affecting demand. Additionally, reliance on imported chickpeas in key markets like North America and Europe makes manufacturers vulnerable to trade restrictions, transportation delays, and geopolitical factors. Limited availability of other key ingredients, such as tahini and olive oil, can further compound supply challenges. These factors create operational uncertainties for both large-scale producers and smaller regional brands, impacting production planning and inventory management.

Product adulteration and recalls

Product adulteration and recalls represent a significant restraint on the global hummus market, as they directly affect consumer trust and brand reputation. Instances of contamination with pathogens, undeclared allergens, or substandard ingredients can lead to product recalls, regulatory penalties, and negative media coverage. Such occurrences not only disrupt supply chains but also increase operational costs due to testing, quality control measures, and replacement logistics. Small and regional producers are particularly vulnerable, as they may lack advanced food safety infrastructure and rigorous monitoring systems. Even isolated incidents can influence consumer perception, causing hesitation in purchasing ready-to-eat dips and spreads. Moreover, stricter regulatory oversight in key markets mandates comprehensive traceability and batch testing, adding complexity and compliance costs. These factors underscore the importance of robust quality assurance and transparent sourcing practices to mitigate risks and maintain market confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Alternative Bases Challenge Chickpea Dominance

The chickpea-based hummus segment dominated the hummus market in 2025, capturing 85.01% of the total share, reflecting its status as the traditional and most widely consumed variant. Chickpeas are a rich source of protein, fiber, and essential nutrients, which enhances the nutritional appeal of hummus and drives consumer preference. This segment benefits from strong familiarity among consumers across North America, Europe, and the Middle East, where chickpea-based hummus has long been a staple in diets. Its versatility in sandwiches, dips, spreads, and snack recipes further supports consistent demand. In addition, the growing trend of plant-based and protein-rich diets has reinforced chickpea hummus’s popularity among health-conscious consumers. Manufacturers continue to innovate within this segment by introducing flavored and fortified varieties, expanding product offerings while maintaining its dominant market position.

In contrast, the alternative-base hummus segment is expected to register the fastest growth, with a projected CAGR of 7.89% through 2031, driven by increasing consumer interest in diverse plant-based ingredients. These variants use ingredients such as lentils, beans, peas, or vegetables as primary bases, catering to those seeking gluten-free, allergen-friendly, or novel flavor profiles. Rising awareness of dietary restrictions and clean-label preferences is encouraging experimentation with non-traditional bases, creating opportunities for product differentiation. Innovative formulations, such as beetroot, pumpkin, or black bean hummus, are attracting younger consumers and the flexitarian population. Additionally, the growth of specialty retail channels and online marketplaces has made alternative-base products more accessible to a wider audience.

By Flavor Type: Bold Profiles Outpace Original

The original hummus segment dominated the global hummus market in 2025, accounting for 38.11% of total revenue, reflecting its widespread popularity and status as the classic variant. Consumers prefer the original profile for its authentic taste, smooth texture, and versatility as a dip, spread, or accompaniment in meals. Its strong presence in both retail and foodservice channels has reinforced steady demand, particularly in regions with established hummus consumption such as North America, Europe, and the Middle East. The original flavor also serves as a base for recipe experimentation, allowing manufacturers to introduce new variants and meal pairings while maintaining consumer trust. Health-conscious and plant-based consumers further favor this variant for its natural ingredients and protein-rich content.

Conversely, black-olive flavored hummus is projected to be the fastest-growing segment, expanding at a CAGR of 8.03% through 2031, driven by increasing consumer interest in gourmet and bold flavors. This variant appeals to adventurous and premium-focused consumers seeking novel taste experiences and Mediterranean-inspired profiles. Its growth is supported by rising demand in foodservice outlets, specialty stores, and online retail platforms, where flavor diversity is highly valued. Black-olive hummus also benefits from the trend of incorporating functional ingredients, as olives are associated with antioxidants and heart-healthy properties. Manufacturers are expanding their flavor portfolio to include black-olive and other Mediterranean-inspired variants to capture this emerging demand.

By Packaging Type: Squeezable Bottles Gain Traction

The cups, tubs, and jars segment dominated the global hummus market in 2025, capturing 69.58% of total revenue, reflecting its widespread acceptance among consumers for convenience and portion control. These packaging formats are ideal for retail shelves and household use, offering easy storage, resealability, and the ability to maintain product freshness over multiple servings. Their popularity is further supported by ready-to-eat and grab-and-go consumption trends, particularly in North America and Europe. Manufacturers frequently use these formats to introduce multipacks, flavored assortments, and portion-controlled sizes, enhancing consumer appeal. Additionally, the sturdy and versatile design of cups, tubs, and jars allows for clear labeling, which supports clean-label and natural ingredient claims.

In contrast, bottle packaging formats are expected to witness the fastest growth, recording a CAGR of 7.66% between 2026 and 2031, driven by evolving consumer preferences for pourable and on-the-go formats. Bottles offer ease of dispensing, portion control, and minimal handling mess, making them particularly attractive for dressings, dips, and sandwich spreads. The rising demand for single-serve and travel-friendly packaging in convenience stores, cafeterias, and online retail is further fueling this segment’s adoption. Innovative designs, such as squeezable bottles with airtight caps, enhance freshness and usability, appealing to younger and busy consumers. Manufacturers are also leveraging bottle formats for premium or gourmet hummus variants, targeting niche and health-conscious segments.

By Distribution Channel: Foodservice Accelerates

The off-trade distribution channel dominated the global hummus market in 2025, accounting for 82.43% of total revenue, reflecting its strong presence in retail and e-commerce outlets. Supermarkets, hypermarkets, convenience stores, and online grocery platforms serve as the primary points of sale, offering consumers easy access to a wide range of hummus variants, including traditional and flavored options. The channel’s dominance is supported by bulk and multipack offerings, competitive pricing, and promotional campaigns, which encourage household purchases and repeat consumption. Off-trade formats also allow manufacturers to leverage attractive packaging and branding to influence buying decisions. Additionally, the growth of online grocery shopping has further strengthened this channel, providing convenience and wider availability across regions.

In contrast, the on-trade channel is expected to record the fastest growth, with a projected CAGR of 8.14% through 2031, driven by increasing consumption of hummus in restaurants, cafes, and foodservice establishments. Rising awareness of healthy snacking and plant-based menu options has encouraged foodservice operators to include hummus in appetizers, sandwiches, salads, and gourmet platters. Specialty restaurants, fast-casual chains, and cafes are experimenting with innovative flavors and presentation styles to appeal to diverse consumer preferences. Additionally, the expansion of dining-out culture and catering services is further boosting demand through this channel. On-trade distribution also benefits from consumer willingness to pay a premium for fresh, ready-to-eat, and artisanal hummus offerings.

Geography Analysis

North America held a commanding 38.45% share of the global hummus market in 2025, driven by strong consumer acceptance of ready-to-eat and plant-based products. The region benefits from high awareness of health and wellness trends, with hummus being popular as a protein-rich, low-calorie snack. Supermarkets, hypermarkets, and online grocery platforms dominate distribution, providing convenient access to a wide variety of flavors and packaging formats. Innovation in flavored hummus, portion-controlled packs, and clean-label products has further strengthened demand in the hummus market. Additionally, the rising popularity of Mediterranean and Middle Eastern cuisine has made hummus a staple in many households. North America’s well-established retail and foodservice infrastructure supports consistent growth and maintains its position as the largest regional market.

The Middle East and Africa region is projected to grow at the fastest pace, with a CAGR of 8.47% between 2026 and 2031, reflecting both cultural affinity and rising consumer demand. Hummus is traditionally popular in many Middle Eastern countries, and expanding urbanization, modern retail development, and international food trends are driving growth. The rise of convenience-oriented lifestyles and the adoption of packaged and ready-to-eat variants are further boosting sales across the hummus market. Foodservice channels, including restaurants, cafes, and catering services, are increasingly offering hummus as part of appetizers and meal accompaniments. Additionally, product innovation, including flavored and gourmet variants, is attracting younger consumers.

Other regions, including Asia-Pacific, Europe, and South America, are experiencing steady growth, though at a relatively moderate pace. In Europe, demand is supported by rising health-conscious eating habits, plant-based diets, and clean-label trends, particularly in Western countries. Asia-Pacific is witnessing growing adoption in urban centers, supporting expansion of the hummus market through increasing awareness of international cuisines and the expansion of retail and e-commerce channels. South America is gradually adopting hummus in foodservice and retail, driven by rising interest in protein-rich snacks and plant-based alternatives.

Competitive Landscape

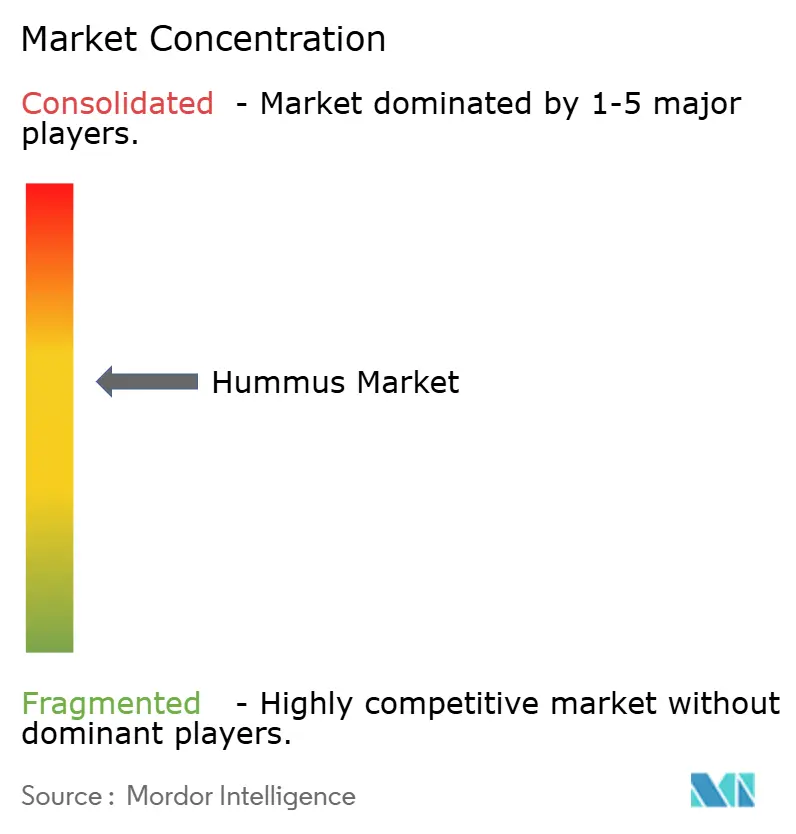

The hummus market is characterized by moderate fragmentation, reflecting the presence of both well-established international brands and numerous regional producers. International brands in the hummus market leverage broad distribution networks, extensive marketing campaigns, and product innovation to maintain visibility and cater to evolving consumer preferences. Their offerings often include a wide variety of flavors, packaging formats, and portion sizes designed to meet the demands of retail and foodservice channels. These companies also focus on maintaining high quality standards and consistency, which helps build trust and loyalty among consumers seeking reliable, ready-to-eat products.

Regional players, on the other hand, play a significant role in catering to local tastes and niche segments. They often introduce unique flavor variants inspired by traditional recipes, catering to culturally specific preferences or regional cuisine trends. Due to their smaller scale, regional manufacturers tend to be more agile in responding to consumer demand shifts, experimenting with new ingredients, packaging formats, and healthier formulations. These players are increasingly focusing on clean-label, plant-based, and allergen-friendly options to attract health-conscious consumers and differentiate themselves from larger competitors.

The competitive landscape is further shaped by the growing trend of product diversification and innovation. Companies are investing in expanding flavor profiles, ready-to-eat formats, and convenient packaging to attract on-the-go consumers. Additionally, marketing strategies emphasizing natural ingredients, protein content, and plant-based benefits have become key tools for differentiation. While large brands dominate in terms of volume and reach, the agility of regional players and their ability to offer localized and innovative products ensure a dynamic and competitive market environment. This balance between global reach and local innovation defines the moderately fragmented nature of the hummus market.

Hummus Industry Leaders

PepsiCo, Inc. (Sabra Dipping Company)

Groupe Savencia

Lakeview Farms (Tribe Hummus)

Boar's Head Provision Co., Inc

Cedar’s Mediterranean Foods Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: BeanTastic Hummus launched “Buff Bean Hummus,” a new high-protein and high-fibre hummus product positioned as a healthier alternative to conventional snack and protein products. The company highlighted the product’s natural ingredient profile, absence of artificial preservatives, and nutritional positioning, targeting health-conscious consumers seeking functional and plant-based food options.

- March 2025: Cedar's Foods introduced Cedar's Reserve Hummus, a premium line crafted to deliver an elevated Mediterranean experience with unique, chef-inspired flavors and high-quality ingredients. According to the brand, this new range features small-batch recipes and bold taste profiles, aiming to set a new standard for hummus lovers seeking authenticity and sophistication.

- March 2025: Graza and Ithaca Hummus have teamed up to unveil their latest creation: the Olive Oil & Sea Salt Hummus. This new offering melds Ithaca's fresh, velvety hummus with Graza's premium extra virgin olive oil and a hint of sea salt, resulting in a dip that's both gourmet and flavorful. The companies tout the product's commitment to transparency and top-tier ingredients, aiming to deliver a gourmet experience reminiscent of homemade goodness. It's particularly tailored for health-conscious consumers in search of elevated staples for their daily meals.

- February 2025: ChicP unveiled its latest offerings: hummus and tortilla chip snack pots. These new packs come in two enticing flavors: Beetroot and Horseradish Hummus, and Velvet Hummus, both accompanied by gluten-free corn tortilla chips. Crafted from 100% natural ingredients and boasting a high vegetable content, these snack pots are marketed as a convenient and healthy option for busy individuals.

Global Hummus Market Report Scope

Hummus is a creamy, savory spread or dip made primarily from cooked and mashed chickpeas blended with tahini (sesame seed paste), olive oil, lemon juice, garlic, and various seasonings. The hummus market is segmented by category, flavor type, packaging type, distribution channel and geography. Based on category, the market is segmented into chickpea- based hummus and alternative base hummus. Based on flavor type, the market is segmented into roasted garlic, red pepper, black olive, original hummus and others. Based on packaging type, the market is segmented into cups/tubs/jars, bottles, pouches and others. Based on distribution channel, the market is segmented into on-trade and off-trade channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million).

| Chickpea- Based Hummus |

| Alternative Base Hummus |

| Roasted Garlic |

| Red Pepper |

| Black Olive |

| Original Hummus |

| Others |

| Cups/Tubs/Jars |

| Bottles |

| Pouches |

| Others |

| On-trade | |

| Off-trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Category | Chickpea- Based Hummus | |

| Alternative Base Hummus | ||

| By Flavor Type | Roasted Garlic | |

| Red Pepper | ||

| Black Olive | ||

| Original Hummus | ||

| Others | ||

| By Packaging Type | Cups/Tubs/Jars | |

| Bottles | ||

| Pouches | ||

| Others | ||

| By Distribution Channel | On-trade | |

| Off-trade | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the hummus market?

It is valued at USD 4.43 billion, on track to reach USD 6.02 billion by 2031.

What is the expected CAGR for global hummus sales through 2031?

The compound annual growth rate is projected at 6.33% from 2026-2031.

Which region will grow fastest over the forecast period?

The Middle East and Africa region is forecast to post an 8.47% CAGR.

Which category within hummus is expanding quickest?

Alternative-base recipes such as beetroot and fava bean are rising at 7.89% CAGR.

Page last updated on: