Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.85 Billion |

| Market Size (2031) | USD 18.24 Billion |

| Growth Rate (2026 - 2031) | 10.96% CAGR |

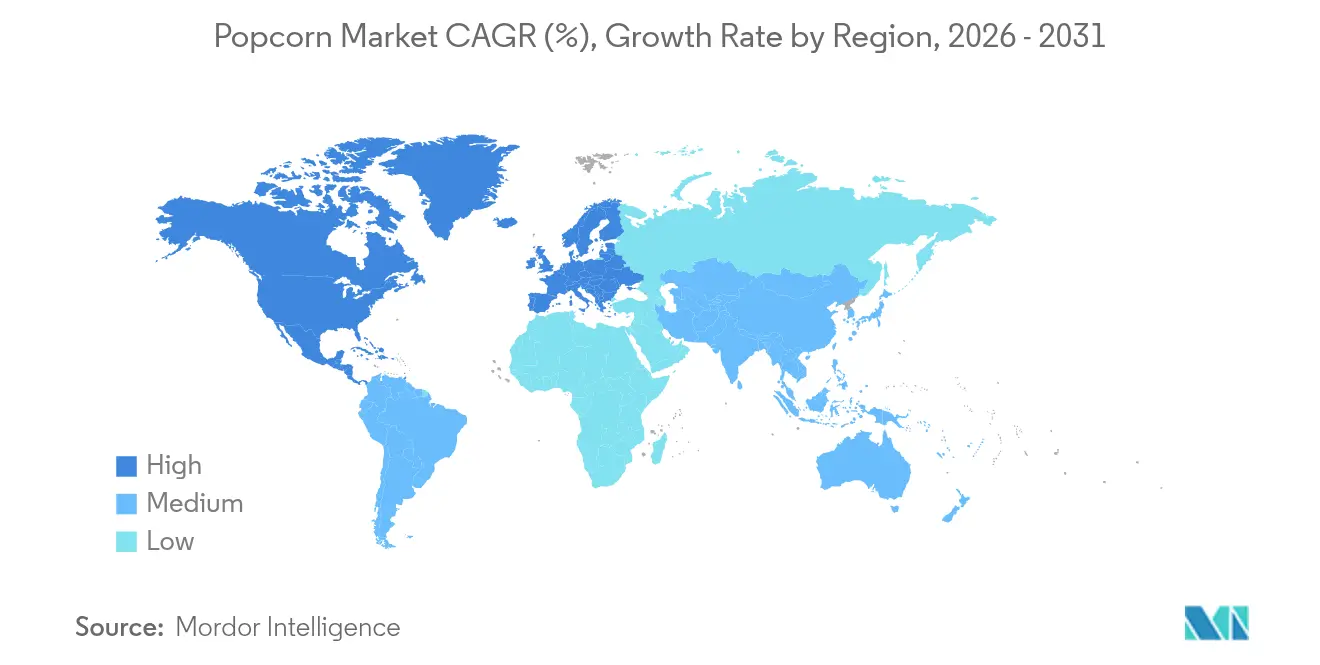

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Popcorn Market Analysis by Mordor Intelligence

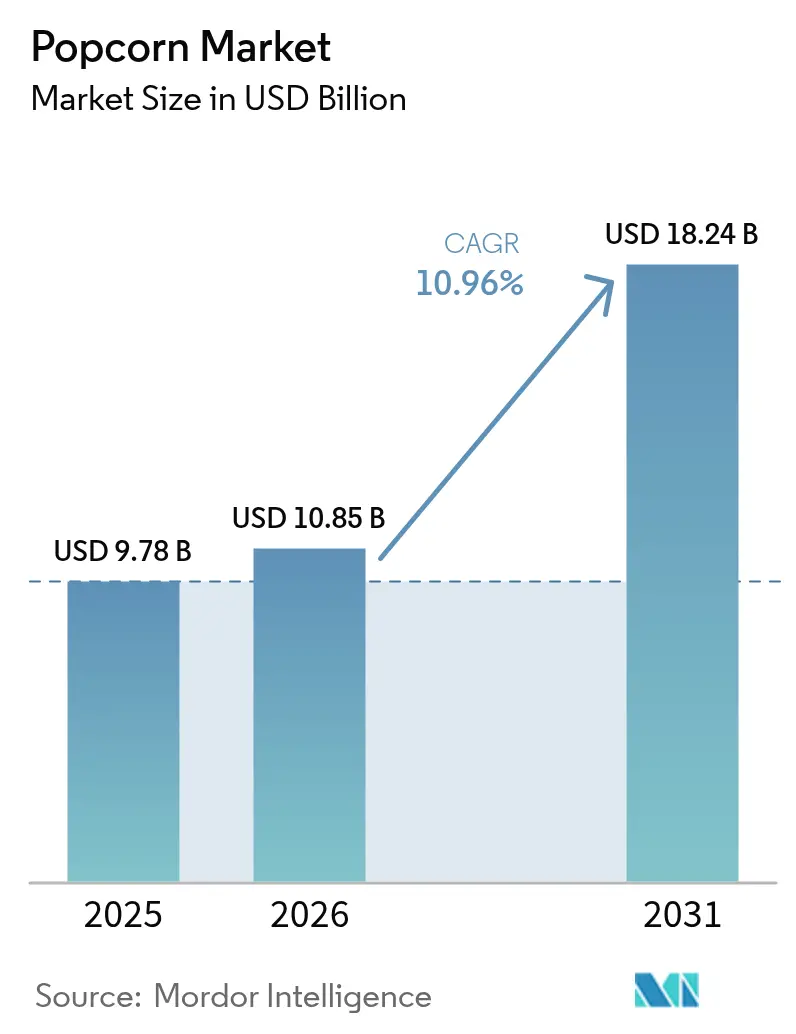

In 2025, the popcorn market size was valued at USD 9.78 billion. The popcorn market is expected to grow from USD 9.78 billion in 2025 to USD 10.85 billion in 2026 and is forecast to reach USD 18.24 billion by 2031 at 10.96% CAGR over 2026-2031. This growth is buoyed by trends like premiumization, strategic entertainment partnerships, and plant-level automation, ensuring consistent quality across a diverse flavor range. Investors are keenly eyeing this trajectory, with major food conglomerates snapping up niche assets for broader reach and a vertically integrated supply chain. North America leads in revenue, but the Asia Pacific is witnessing the swiftest demand surge, suggesting a strategy that marries scale with regional nuances. As consumers increasingly gravitate towards organic and clean-label products, established brands are responding by diversifying their offerings, introducing premium formulations that promise better margins. The International Food Information Council reported that in 2023, about 29% of U.S. consumers regularly purchased food and beverages for their "clean ingredients" labels[1]Source: International Food Information Council, "Food & Health Survey 2023", ific.org.

Key Report Takeaways

- Ready-to-Eat products captured 56.78% of the popcorn market share in 2025, and microwave formats are projected to expand at a 12.45% CAGR through 2031.

- Conventional popcorn accounted for 85.20% of the popcorn market size in 2025, yet organic variants are set to grow at a 13.55% CAGR during the same window.

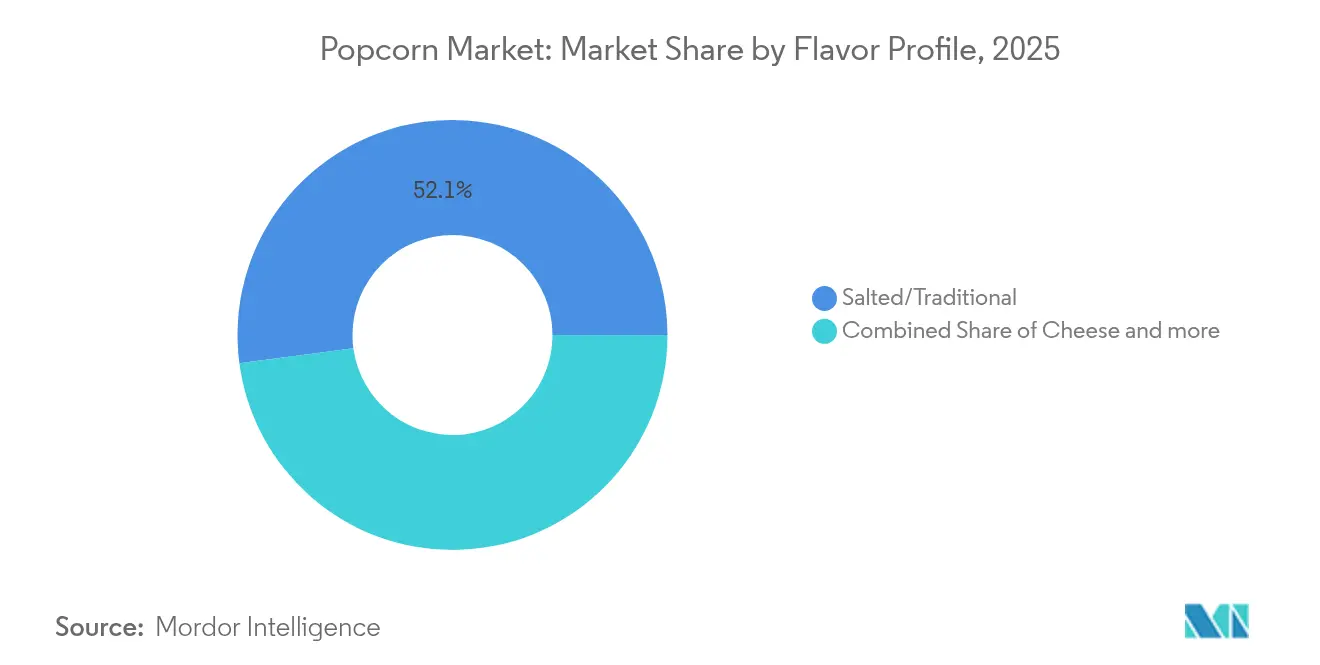

- Traditional salted flavors held 52.10% share of the popcorn market size in 2025, while cheese flavors are advancing at a 12.20% CAGR to 2031.

- Multi-serve packs represented 47.05% of popcorn market share in 2025, and single-serve units led growth at 12.95% CAGR.

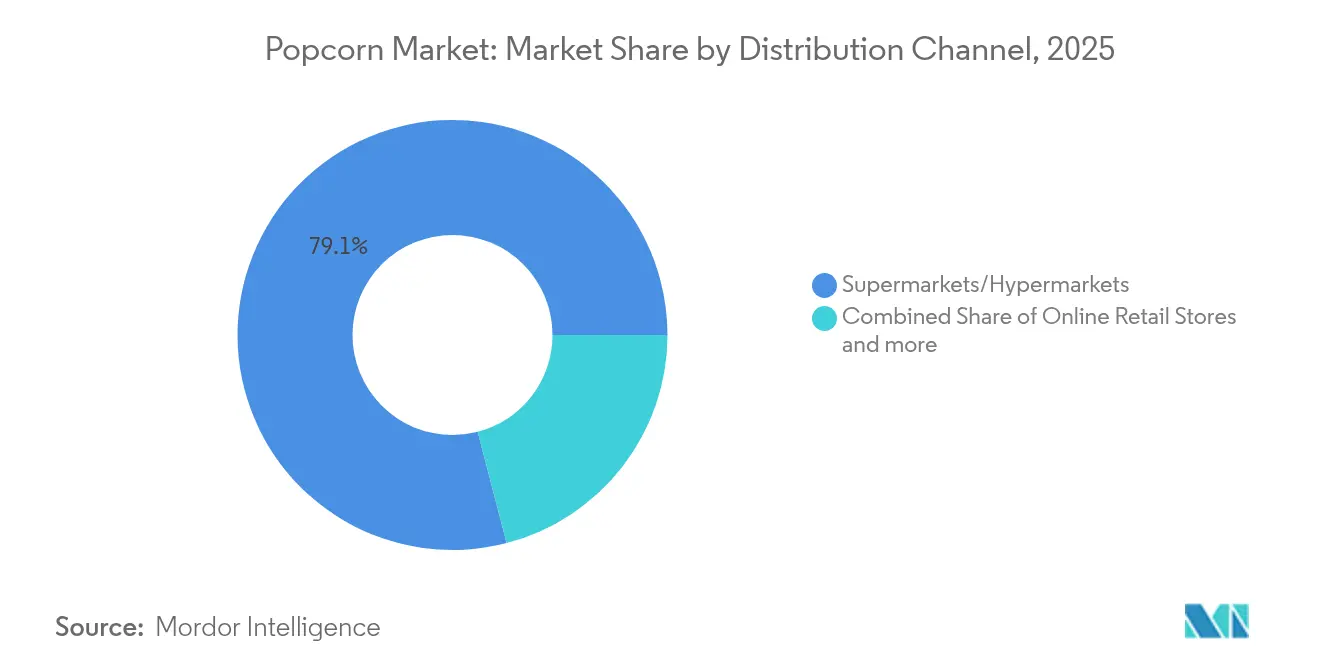

- Supermarkets and hypermarkets contributed 79.05% of the popcorn market size in 2025, whereas online retail is scaling fastest at 13.45% CAGR.

- North America controlled 32.10% of the popcorn market share in 2025; Asia Pacific is pacing the field with a 12.25% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Popcorn Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Innovations in flavor and product types | +1.8% | Global, with premium markets leading adoption | Medium term (2-4 years) |

| Environmental sustainability and packaging innovation | +1.5% | Europe and North America primarily, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growth of at-home entertainment and streaming services | +2.1% | Global, with developed markets showing the highest correlation | Short term (≤ 2 years) |

| Strategic marketing and collaborations | +1.2% | Global, with entertainment hub regions leading | Medium term (2-4 years) |

| The premiumization of snacking | +1.9% | North America, Europe, urban Asia-Pacific centers | Medium term (2-4 years) |

| Increased efficiency through automation and robotics | +1.4% | Manufacturing hubs in North America, Europe, and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Innovations in Flavor and Product Types

Flavor innovation has become a pivotal strategy for differentiation, with manufacturers increasingly turning to co-branding partnerships to capture consumer interest and command premium prices. In October 2024, Starco Brands introduced a Garlic Butter flavor for its Winona Popcorn Spray. This move underscores a focused approach to product development, ensuring even coverage of kernels through an air-powered application. Notably, the product emphasizes health-conscious attributes, boasting non-GMO and gluten-free formulations. The pandemic acted as a catalyst for collaborative flavor innovations. For instance, Smartfood teamed up with Cap'n Crunch to create a Crunch Berries popcorn mix, while Frito-Lay expanded its Cheetos Popcorn line with Flamin' Hot variants. Such moves highlight how established snack brands are using popcorn as a canvas for flavor exploration. These innovations not only cater to the consumer's craving for unique taste experiences but also empower manufacturers to set premium prices, especially when positioned as limited editions with broad appeal.

Environmental Sustainability and Packaging Innovation

Regulatory pressures and heightened environmental awareness among consumers have spurred rapid advancements in sustainable packaging within the popcorn industry. Bad Monkey Popcorn has pioneered the world's first heatable, 100% compostable wood-fiber bag for pre-popped popcorn. Meanwhile, Braskem America has introduced WENEW, a bio-circular polypropylene sourced from used cooking oil, marking a significant step in reducing fossil fuel reliance for snack packaging. The European Union's Packaging and Packaging Waste Regulation (EU 2025/40), set to take effect in August 2026, imposes sustainable design mandates and binding reuse targets, signaling a shift in packaging strategies throughout the popcorn supply chain. In response, manufacturers are pivoting towards recyclable solutions. Notably, KYSU is set to debut airtight, reusable paper cans crafted from 100% recycled materials in October 2024, aiming to combat plastic pollution without compromising product freshness or visual appeal.

Growth of At-Home Entertainment and Streaming Services

Streaming platforms have reshaped snacking habits, driving a consistent demand for convenient, shareable popcorn during binge-watching sessions. In a clear nod to this trend, Netflix partnered with India's premium snacking brand, 4700BC, rolling out exclusive flavors like Sweet and Salty and Cheese and Caramel. This move underscores entertainment giants' recognition of popcorn's pivotal role in the viewing experience and their intent to capitalize on it. Research highlights a surge in snacking among global adults during the pandemic, with factors like TV watching and distractions amplifying consumption. In response, manufacturers are pivoting, optimizing packaging for multi-serve formats and crafting flavors tailored for prolonged snacking, moving away from the traditional single-serve cinema model.

Strategic Marketing and Collaborations

Partnerships in the entertainment industry have shifted from mere movie theater concessions to intricate brand collaborations, harnessing the power of intellectual property and cultural moments. AMC Theatres is venturing into grocery retail with its "Perfectly Popcorn" line, delivering theater-quality flavors for home enjoyment. They've cleverly preserved their brand's cinema essence with "Heat and Eat" instructions. Commemorative popcorn buckets have emerged as a lucrative revenue stream for exhibitors. In 2024, AMC reported a merchandise revenue of around USD 65 million, largely fueled by limited-edition designs. These designs not only spark social media buzz but also command secondary market premiums of USD 50-210 on platforms like eBay. Such collaborations highlight how popcorn brands are tapping into entertainment properties, creating urgency, encouraging repeat purchases, and broadening their distribution horizons.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuations in raw material prices | -1.6% | Global, with North American producers most exposed | Short term (≤ 2 years) |

| Intense competition from alternative snacks | -1.3% | Developed markets primarily, expanding globally | Medium term (2-4 years) |

| Negative perception of additives | -0.9% | Europe and North America leading, Asia-Pacific following | Long term (≥ 4 years) |

| Strict regulations on labeling and ingredients | -0.7% | Europe most stringent, North America moderate, Asia-Pacific emerging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuations in Raw Material Prices

Popcorn manufacturers grapple with persistent corn price volatility. USDA projects corn prices stabilizing at around USD 4.35 per bushel by 2025. The World Bank reported that in 2024, maize averaged USD 191 nominal per metric ton[2]Source: World Bank, "World Bank Commodities Price Forecast", thedocs.worldbank.org. While forecasts hint at a return to historical price norms, uncertainties in trade policies, such as reciprocal tariffs and retaliatory measures, amplify price risks. An analysis from the University of Illinois warns the industry might endure a multi-year lower-price phase, echoing patterns from 1985-1992 and 1998-2005. However, this trend could be swiftly upended by supply shocks, be it from weather anomalies or geopolitical tensions. Manufacturers lacking hedging capabilities feel the pinch during price surges, facing margin compression. In contrast, those boasting integrated supply chains or long-term contracts enjoy a competitive edge amidst the volatility.

Intense Competition from Alternative Snacks

As consumers in developed markets increasingly prioritize nutritional profiles and clean-label attributes, traditional popcorn products face mounting competitive pressure from a surge of healthy snacking alternatives. Research shows that consumers are more swayed by processing claims and ingredient lists that align with clean-label standards than by conventional nutrient content claims. This shift has compelled popcorn manufacturers to rethink their product formulations and marketing tactics. Competing directly for the same consumption occasions and retail shelf space, nuts, vegetable chips, and protein-based snacks boast a more favorable nutritional positioning. Data from the Natural Resources Institute Finland highlights that in 2024, nut consumption reached two kilograms per person[3]Source: Natural Resources Institute Finland, "Consumption of food commodities per capita (kg/year)", statdb.luke.fi. This challenge is especially pronounced in premium segments, where consumers are willing to pay a premium for perceived health benefits. This trend intensifies the pressure on popcorn brands to innovate, pushing them to move beyond traditional formulations and craft products that align with evolving wellness standards, all while ensuring they don't sacrifice taste appeal.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: RTE Dominance Faces Microwave Resurgence

In 2025, Ready-to-Eat (RTE) popcorn commands a dominant 56.78% market share, riding the wave of convenience trends and impulse buying that favor grab-and-go formats. Meanwhile, microwave popcorn is on a resurgence, boasting a robust 12.45% CAGR through 2031. This growth is fueled by the rising trend of at-home entertainment and packaging innovations that tackle past concerns over chemical additives. The revival of the microwave segment underscores manufacturers' commitment to addressing these concerns. A case in point is Coop Denmark's reintroduction of microwave popcorn, now packaged in Liven's cellulose-based bags. These bags not only sidestep PFAS worries but also ensure fat impermeability. While unpopped kernels cater to niche markets like bulk foodservice and artisanal producers, they grapple with competition from automated systems that lean towards processed formats.

Product type segmentation highlights varied consumption trends across demographics and occasions. RTE popcorn, with its strategic placement in bustling retail spots and portion-controlled packaging, dominates impulse buys. In contrast, microwave popcorn is favored for planned home entertainment consumption. Automation in manufacturing is increasingly skewed towards RTE production, emphasizing consistent quality and packaging efficiency. Facilities like Bratney's turnkey operation boast an impressive 99.9% perfect product rate, thanks to their integrated processing and packaging systems. The competitive landscape is witnessing a wave of consolidation, with major brands snapping up specialized manufacturing capabilities. A prime example is Hershey's acquisition of Weaver Popcorn facilities in October 2023, a move aimed at bolstering the SkinnyPop brand and tightening supply chain control.

By Nature: Organic Momentum Challenges Conventional Dominance

In 2025, conventional popcorn dominates the market with an 85.20% share, bolstered by established supply chains and cost advantages that facilitate competitive pricing in mass-market channels. Meanwhile, organic popcorn is making waves, growing at a robust 13.55% CAGR. This surge underscores consumers' readiness to pay a premium for health and environmental benefits. Such growth mirrors the broader clean-label movement, which emphasizes natural ingredients and transparent sourcing over mere cost-cutting. Highlighting this trend, the International Federation of Organic Agriculture Movements reported that in 2023, per capita organic food consumption in the EU-27 hit a decade-high at approximately EUR 104.

However, the organic segment's growth isn't without challenges. Specialized corn varieties demand unique farming methods and dedicated processing facilities to uphold certification standards. This premium positioning allows organic brands to set higher prices, with some artisanal producers reaping margins 2-3 times that of conventional counterparts, thanks to direct-to-consumer sales and niche retail collaborations. Furthermore, regulatory frameworks, like the USDA National Organic Program standards, not only bolster consumer trust in organic certification but also erect barriers. These barriers shield established organic brands from conventional players eyeing the premium market, especially those unwilling to heavily invest in certified supply chains.

By Flavor Profile: Traditional Foundations Support Cheese Innovation

In 2025, salted and traditional flavors command a dominant 52.10% market share, setting the standard for consumer expectations and appealing to a wide demographic. Meanwhile, cheese flavors are rapidly gaining traction, boasting a robust 12.20% CAGR, fueled by premiumization and innovative flavoring that stands out in competitive retail spaces. Barbecue and butter flavors enjoy a consistent market presence, bolstered by regional preferences and brand loyalty. The "Others" category, featuring exotic and limited-edition flavors, captivates consumers and garners attention on social media.

Flavor development increasingly leans on co-branding partnerships, tapping into established profiles from related categories. For instance, Smartfood's tie-up with Cap'n Crunch and Krispy Kreme showcases how popcorn brands can venture into new flavor realms, reaping the benefits of their partners' brand clout and marketing prowess. The cheese segment's ascent highlights a shift towards more nuanced flavor appreciation, moving beyond just salted. Caramel flavors, straddling the line between sweet and savory, are adeptly positioning themselves for varied consumption moments. However, crafting these specialty flavors demands investment in versatile coating systems and stringent quality controls to prevent ingredient cross-contamination.

By Packaging Type: Single-Serve Growth Challenges Multi-Serve Leadership

In 2025, multi-serve packaging captures a 47.05% market share, mirroring family consumption trends and offering cost-per-serving benefits that resonate with budget-conscious buyers. Meanwhile, single-serve formats are on a growth trajectory, expanding at a 12.95% CAGR. This surge is fueled by a rising preference for portion control, the convenience of on-the-go consumption, and snacking habits at work that lean towards individual packaging. Family and bulk pack formats cater to both institutional clients and households aiming for value. However, their growth is tempered by challenges like storage constraints and concerns over maintaining freshness in larger packages.

Today's packaging innovations go beyond merely adjusting sizes; they also address sustainability and functional enhancements, elevating the overall consumer experience. Studies indicate that packaging attributes play a pivotal role in consumption volumes. Specifically, larger package sizes and the availability of multiple packages can boost intake, independent of portion size considerations. In response to the European Union's stringent new packaging regulations, which emphasize recyclability and set thresholds for recycled content, manufacturers are pivoting. They're crafting mono-material structures that not only ease recycling but also uphold the barrier properties vital for ensuring product freshness and extending shelf life.

By Distribution Channel: Online Retail Disrupts Traditional Supermarket Dominance

In 2025, supermarkets and hypermarkets dominate the distribution landscape, commanding a substantial 79.05% market share. They achieve this by capitalizing on extensive shelf space, strategically positioning products for impulse purchases, and aligning with established consumer habits that favor in-person selections. Meanwhile, online retail stores are surging ahead, boasting a robust 13.45% CAGR. This growth, spurred by the pandemic's e-commerce boom, underscores a shift in consumer preferences towards the convenience of home delivery, sidelining traditional shopping trips. Convenience and grocery stores cater to immediate consumption needs, especially in areas with limited supermarket access. Other distribution avenues include specialty retailers, foodservice operations, and direct-to-consumer sales.

These shifts in distribution dynamics mirror evolving consumer behaviors and technological advancements, particularly in last-mile delivery for packaged snacks. A case in point: Cinemark's November 2023 move to broaden its third-party delivery collaborations with DoorDash, Grubhub, and Uber Eats. This highlights how traditional concessionaires are pivoting to cater to at-home consumption, extending their footprint beyond just physical venues. The e-commerce boom not only opens doors for premium and specialty brands to engage directly with consumers but also allows them to enjoy fatter margins by sidestepping intermediary costs. However, this direct approach mandates a robust investment in digital marketing and fulfillment infrastructure, essential to rival the logistics prowess of established retail giants.

Geography Analysis

In 2025, North America held a dominant 32.10% share of the popcorn market, bolstered by a deep-rooted snacking culture and elevated per-capita consumption rates. The U.S. leverages integrated farm-to-factory corridors, reducing raw-material delays and swiftly rotating SKUs for seasonal events. Canada boosts regional growth with efficient cross-border distribution, while Mexico broadens its market presence with value-centric pack sizes, catering to the expansion of modern trade. Recent manufacturing investments, like Weaver Popcorn’s upgraded plant in Indiana (May 2024), underscore the region's long-term confidence, enhancing packaging capabilities for premium offerings.

Asia Pacific is set to lead with the highest absolute volume growth, projected at a 12.25% CAGR through 2031. China's burgeoning cinema scene and a middle class willing to splurge on snacks are paving the way for both mainstream and premium popcorn offerings. Flavors like Sichuan peppercorn are striking a chord with local tastes. While popcorn's presence in India's snack repertoire is modest, the growth trajectory is promising; 4700BC’s ambitious revenue targets hint at the potential for scaling with broader distribution. Meanwhile, Japan and South Korea are increasingly favoring packaging innovations that cater to convenience store layouts and safety standards, driving demand for compact, resealable formats.

Europe is maintaining a steady pace, driven by regulatory initiatives promoting recyclable materials and enhanced nutrient profiles. Germany and the U.K. are pushing volumes through mainstream supermarket placements, while France and Italy are leaning towards organic and artisanal brands. The Nordic countries, with their keen focus on environmental standards, have swiftly adopted PFAS-free microwave packaging, setting a compliance benchmark for the continent. Looking ahead, the EU's stringent packaging directive, set to take effect in 2026, is poised to ignite further substrate innovations, potentially giving compliant exporters a competitive edge.

Regulatory Landscape

Regulatory Landscape Regulation affecting popcorn spans food safety, labeling, packaging sustainability, and commodity-program compliance. In the United States, the Popcorn Promotion, Research, and Consumer Information Order (7 CFR Part 1215) requires mandatory assessments from processors, with exemptions for smaller marketers and certain operations under approved USDA National Organic Program plans; in March 2026, USDA's Agricultural Marketing Service finalized an increase in the assessment rate from 5 cents to 6 cents per hundredweight, funding category promotion and research.

Labeling and packaging rules materially shape formulation and pack architecture for microwave and ready-to-eat products sold into major markets. The US FDA set January 1, 2028 as the uniform compliance date for final food labeling regulations published between January 1, 2025 and December 31, 2026, influencing timelines for nutrition and claims updates across branded portfolios. In Europe, the EU Packaging and Packaging Waste Regulation (EU 2025/40) is scheduled to take effect in August 2026, tightening sustainable design and reuse requirements and accelerating shifts toward recyclable, compostable, or reusable formats. For cross-border trade and inspection, popcorn kernels typically move under maize classifications (for example HS 1005.90 with country-specific subcodes), while key importing markets apply their own food standards and enforcement frameworks, such as China's GB 2762 (contaminant limits), GB 2760 (additives), and GB 7718 (prepackaged labeling) overseen by the State Administration for Market Regulation (SAMR).

Competitive Landscape

Multinational conglomerates are reshaping the popcorn market, which is witnessing a moderate concentration. In 2024, Mars made headlines with its USD 35.9 billion acquisition of Kellanova, bolstering its global snacking presence and consolidating premium popcorn brands. Conagra Brands strategically pairs the renowned Orville Redenbacher label with Angie’s Boomchickapop, catering to both value and premium segments. Meanwhile, Hershey’s foray into the popcorn realm with SkinnyPop enriches its portfolio of healthier snack options. Together, these top five players command about 55% of the global popcorn market, signaling potential for new entrants.

Automation emerges as a pivotal differentiator; firms boasting high-throughput, low-defect facilities can competitively price against artisanal counterparts while upholding quality standards that safeguard brand reputation. Private equity's robust interest is evident in Weaver Popcorn’s acquisition, channeling funds for tech advancements and broader market reach. Collaborating with entertainment franchises for co-branding presents another avenue for market share expansion; such partnerships enhance shelf visibility, a feat often elusive for smaller competitors due to licensing expenses.

Major retailers are increasingly prioritizing sustainability in their tender processes. Brands that champion compostable or mono-material packaging not only align with corporate CSR objectives but also secure coveted long-term shelf placements. The focus of innovation is shifting towards clean-label seasonings and methods that use less oil for popping. While smaller craft brands carve a niche through local sourcing and direct consumer engagement, their growth may hit a ceiling unless they collaborate with or sell to larger entities.

Popcorn Industry Leaders

-

Conagra Brands, Inc.

-

Campbell Soup Company

-

PepsiCo Inc.

-

Weaver Popcorn Bulk, LLC

-

The Hershey Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Market Opportunities and Future Outlook Premium and entertainment-linked popcorn brands continue drawing strategic capital and new distribution pathways, creating whitespace for portfolio expansion across RTE, microwave, and adjacent snack formats. In January 2026, Marico signed definitive agreements to acquire a 93.27% stake in Zea Maize Private Ltd (4700BC) from PVR INOX, highlighting how large FMCG players are using acquisitions to access premium popcorn brand equity and scale distribution beyond cinema-linked channels. Similar collaboration-led demand creation remains visible in entertainment tie-ins already used in-market, including Netflix-linked flavor launches with 4700BC, which reinforces popcorn's role in at-home viewing occasions and supports limited-edition rotation as a shelf and online traffic driver.

Upstream modernization and domestic kernel ecosystem building, particularly in India, opens opportunities for manufacturers to secure quality and reduce import dependence through science-led sourcing and mechanization. Companies such as Gourmet Popcornica have worked with ICAR-IIMR on hybrid seed and farmer partnership initiatives, and in June 2026 began efforts to mechanize harvesting for a portion of its popcorn maize acreage, reflecting a shift toward agronomy, mechanization, and sorting investments as competitive levers for consistent expansion, popping performance, and food-safety control. In parallel, small and mid-sized producers are still expanding capacity to serve wholesale and regional demand, as shown by Carrolls Corn's April 2026 property purchase to support over 100 wholesale accounts, indicating room for localized manufacturing and co-packing models alongside global brands. Regulatory change on packaging, including the EU rule effective August 2026, also creates a near-term product and packaging redesign cycle where compostable, reusable, and mono-material structures can differentiate offerings in modern trade and e-commerce.

Recent Industry Developments

- May 2026: PepsiCo announced PopCorners Protein, extending the PopCorners platform into protein-positioned snacks with 9 grams of protein per serving. The launch broadens popcorn-based snacking into functional propositions that compete more directly with protein-forward alternatives and helps defend shelf space in premium snack aisles.

- April 2026: Carrolls Corn completed a property purchase to support over 100 wholesale accounts, indicating room for localized manufacturing and co-packing models alongside global brands.

- August 2024: Campbell completed the divestiture of its Pop Secret popcorn business to independent snack company Our Home. The transaction reshaped participation in the microwave popcorn segment by moving a legacy brand to a focused snack operator, potentially changing investment intensity in innovation and distribution partnerships for that portfolio.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the popcorn market covers the value of popcorn sold for home consumption and out of home use, including ready-to-eat, microwave packs, and unpopped kernels, across retail and foodservice channels worldwide.

Scope exclusions: We exclude home popping accessories, seasoning blends sold separately, and cinema ticket revenue that is not tied to popcorn sales.

Segmentation Overview

-

By Product Type

- Ready-to-Eat (RTE) Popcorn

- Microwave Popcorn

- Unpopped Kernel

-

By Nature

- Conventional

- Organic

-

By Flavor Profile

- Salted/Traditional

- Caramel

- Barbecue

- Cheese

- Butter

- Others

-

By Packaging Type

- Single-Serve

- Multi-Serve

- Family/Bulk Packs

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- New Zealand

- Rest of Asia Pacific

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Saudi Arabia

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to map the category and set realistic input ranges before modeling. We reviewed public statistics and references such as FAOSTAT for maize supply signals, UN Comtrade for trade flows of relevant corn and snack items, and USDA data for crop, price, and consumption context where available.

To keep assumptions grounded, we also used sources such as national customs portals, food and beverage trade associations, peer-reviewed nutrition and food science journals, and public company filings and investor presentations that discuss snack performance and pricing. In addition, a paid subscription for company financials and intelligence, plus a paid import and export shipment-level database, were used selectively to cross-check revenues, routes, and channel exposure. These sources are illustrative only, and other public references were also used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually counted as popcorn revenue, and what is better treated as adjacent snacks or ingredients. We spoke with participants across branded snack suppliers, private label manufacturers, distributors, retail category teams, and foodservice operators, covering APAC, EMEA, and the Americas so regional pricing and channel mix differences could be tested and then reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 13% | APAC: 39% |

| Mid tier: 55% | Functional/Unit leaders: 41% | EMEA: 37% |

| Smaller Players: 15% | Managers: 46% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where consumption and availability signals are reconstructed by region, and then translated into value using channel-specific pricing. As inputs, we track indicators such as snack penetration by channel, at-home versus out-of-home mix, average selling price ranges for ready-to-eat and microwave packs, pack size shifts (single-serve versus multi-serve), and trade and supply signals that influence cost and shelf pricing.

Those totals are corroborated using selective bottom-up checks, including sample revenue roll-ups for key suppliers, distributor channel checks, and volume times ASP approximations for a short list of representative SKUs. Where a bottom-up view is missing for smaller countries or fragmented channels, we use proxy variables such as retail snack sales growth, urbanization, and modern trade share, and then re-test the assumptions with interview feedback.

For forecasting, scenario analysis is used to reflect different outcomes for input-cost pass-through and demand elasticity, followed by a multivariate regression layer to keep the trajectory aligned with drivers such as disposable income, retail expansion, and snacking frequency. We also apply consistency checks so flavor and packaging shifts do not create unrealistic price jumps year to year.

Data Validation & Update Cycle

Outputs are checked in steps so one unusual input does not distort the final totals. We compare the model against independent signals such as snack category growth, regional channel expansion, and the expected balance between retail and foodservice, and then investigate variances that fall outside reasonable ranges.

Before sign-off, the work goes through peer review where assumptions, conversions, and year-on-year movements are re-checked, and any sensitive gaps trigger follow-up calls with experts. Reports are refreshed annually, with interim updates when material events occur, such as large pricing resets, trade disruptions, or notable channel shifts. Right before delivery, a fresh pass is completed so the latest view available at that time is reflected in the final outputs.

Mordor Intelligence's Popcorn Market Size Versus Other Published Estimates

It is normal to see different market sizes for popcorn because sources do not always count the same products, channels, and geographies, and they also pick different base years and price assumptions. Variations can also come from how much primary validation is done on pricing, private label, and foodservice share.

By tracking pack type and channel-level ASP movements and then rechecking them through expert calls, Mordor Intelligence keeps the 2025 total tied to popcorn-only revenue rather than wider snack mixes that may include neighboring categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.78 B (2025) | |

| Industry Research Publisher A | USD 14.90 B (2025) | Uses a broader counted set centered on microwave and ready-to-eat formats, and the value line can expand when on-trade, households, and commercial scopes are combined with less explicit treatment of unpopped kernels and price ladders by channel. |

| Global Publisher B | USD 6.81 B (2024) | Uses an earlier base year and a tighter counted scope that can understate value when modern retail and premium ready-to-eat pricing are not fully captured across regions, which can compress the starting market size even before forecasting begins. |

Taken together, the spread is mainly explained by scope boundaries, the choice of base year, and how pricing is carried through by channel and pack size. A value that is traceable to clear product forms, channel mix, and repeatable pricing checks tends to be more stable for planning, especially when inflation and mix shifts are happening at the same time.

Key Questions Answered in the Report

How large is the popcorn market in 2026?

The popcorn market size reached USD 10.85 billion in 2026 and is projected to grow at a 10.96% CAGR to 2031.

Which product type is growing fastest?

Microwave popcorn is forecast to lead growth at a 12.45% CAGR as consumers seek theater-style experiences at home.

What region offers the highest growth potential for popcorn brands?

Asia Pacific is set to deliver the fastest expansion with a 12.25% CAGR through 2031 thanks to rising disposable incomes and urban snacking habits.

How are sustainability trends influencing popcorn packaging?

Brands are shifting to compostable or mono-material packs in response to new EU rules and consumer demand for eco-friendly solutions.

Which flavor segment shows the strongest momentum?

Cheese variants are advancing at a 12.20% CAGR driven by consumer appetite for gourmet savory profiles beyond traditional salted options.

What role do entertainment partnerships play in popcorn sales?

Collaborations with cinemas and streaming services boost brand visibility, generate limited-edition collectibles, and reinforce popcorn’s role in at-home viewing occasions.

Page last updated on: