Market Overview

| Study Period | 2021 - 2031 |

|---|---|

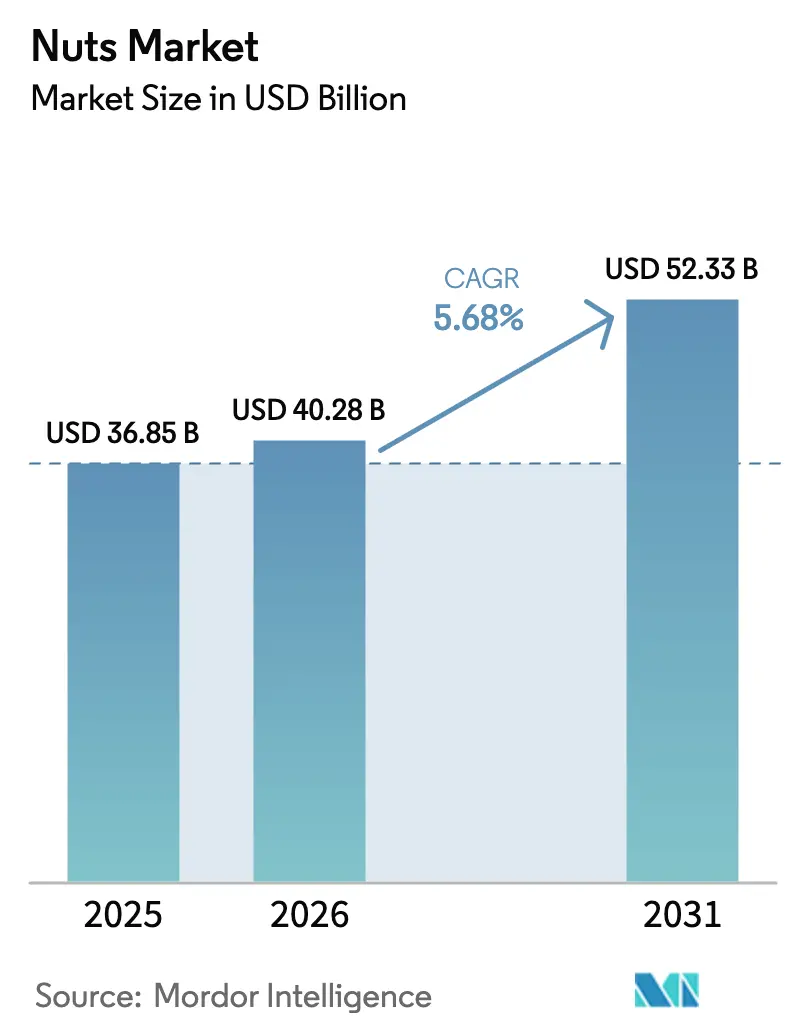

| Market Size (2026) | USD 40.28 Billion |

| Market Size (2031) | USD 52.33 Billion |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

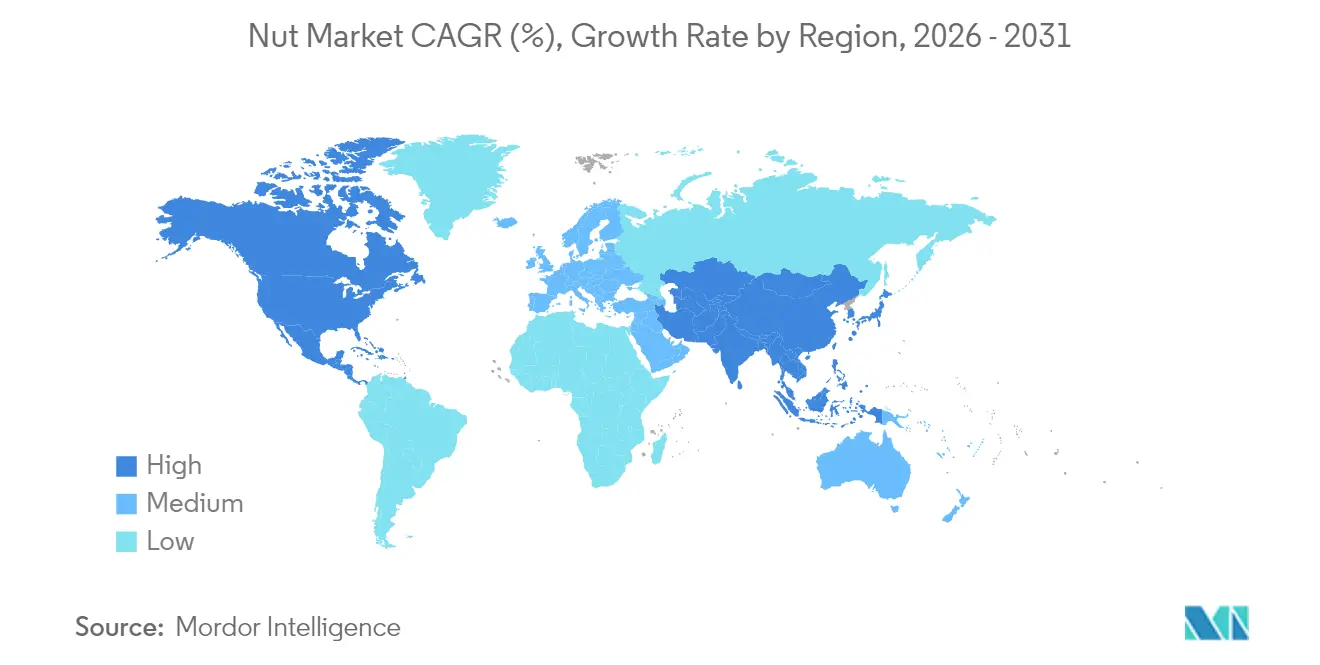

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nuts Market Analysis by Mordor Intelligence

The Nuts Market size is projected to expand from USD 36.85 billion in 2025 and USD 40.28 billion in 2026 to USD 52.33 billion by 2031, registering a CAGR of 5.68% between 2026 to 2031. Accelerating demand for protein-dense snacks, the 2025 FDA “healthy” claim revision that explicitly covers tree nuts, and the 2025-2030 Dietary Guidelines for Americans positioning nuts as a core protein source are lifting retail visibility and institutional procurement. Policy tailwinds converge with tightening California water allocations that curbed 2024 almond output by 8% and sustained spot-price strength. Premiumization is evident in the rapid uptake of organic, flavored, and functional extensions, while e-commerce broadens the assortment beyond what physical shelves can support. Vertical integration among leading growers insulates supply chains yet raises industry entry barriers, keeping competitive intensity moderate.

Key Report Takeaways

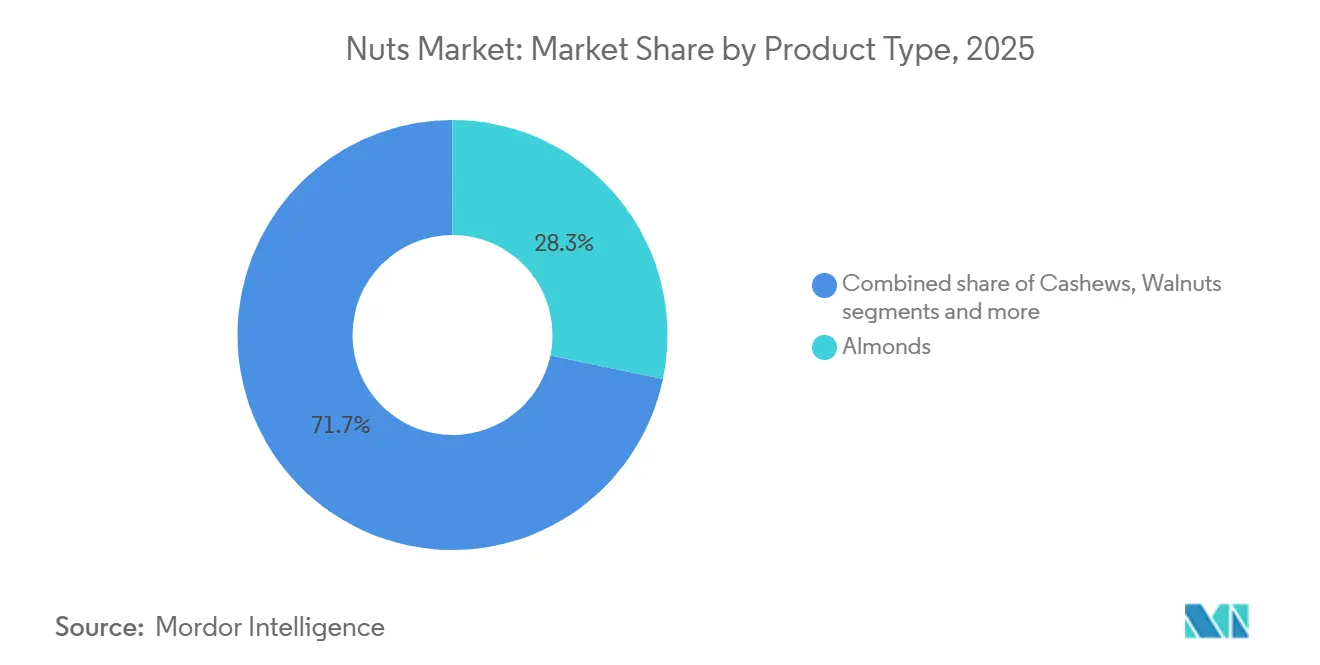

- By type, almonds led with 28.28% of the nuts market share in 2025, while pistachios are forecast to post the highest CAGR at 6.45% through 2031.

- By category, conventional offerings held 75.22% of the Nuts market size in 2025, and organic products are projected to grow at 7.03% CAGR to 2031.

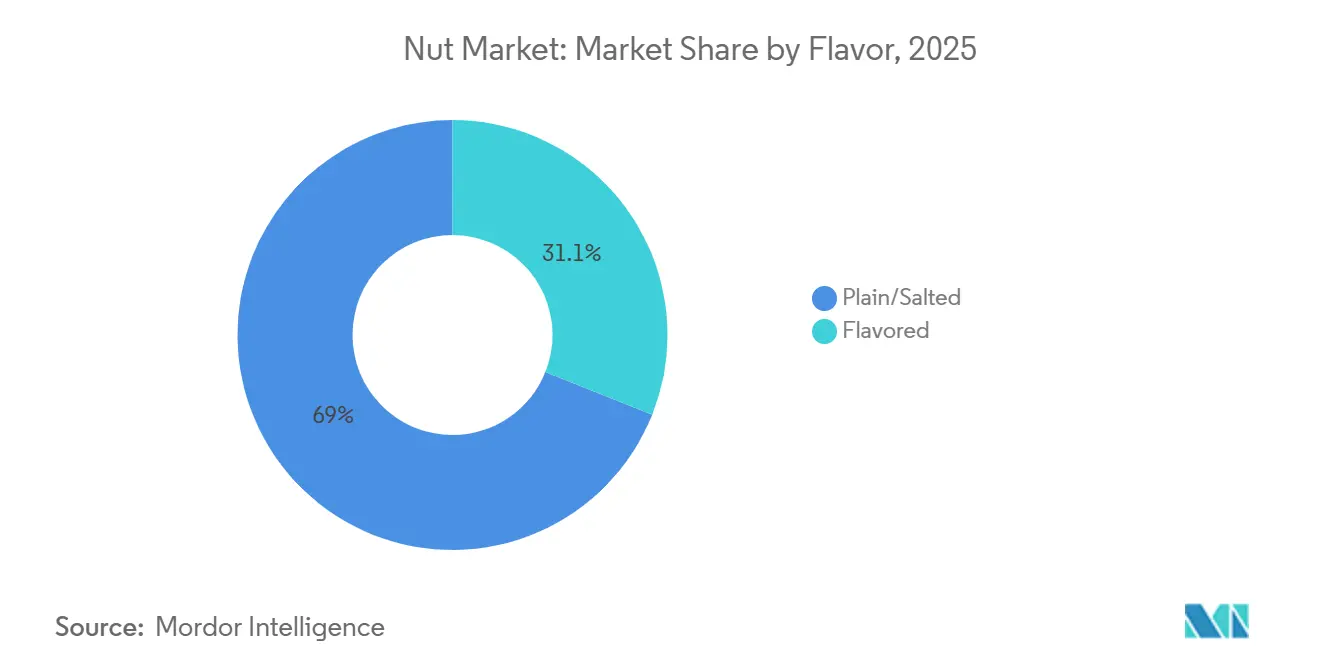

- By flavor, plain and salted formats captured 68.95% revenue in 2025; flavored variants are advancing at a 6.63% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets accounted for 48.23% of 2025 sales, whereas online retail is expanding at 7.02% CAGR over 2026-2031.

- By geography, Europe commanded 40.28%nuts market share in 2025, and Asia-Pacific is projected to be the fastest-growing region with a 6.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nuts Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nutritional Benefits Associated with Nuts Consumption | +0.8% | Global, with peak adoption in North America and Europe | Medium term (2-4 years) |

| Convenience and On-the-Go Snacking | +0.7% | Global, strongest in urban centers across Asia-Pacific and North America | Short term (≤ 2 years) |

| Product Innovation and Flavor Diversification | +0.6% | North America and Europe lead; Asia-Pacific following | Medium term (2-4 years) |

| Increased Interest in Organic and Natural Products | +0.5% | North America and Europe core; emerging in Asia-Pacific | Long term (≥ 4 years) |

| Technological Advancements in Packaging | +0.4% | Global, with regulatory push in EU and North America | Medium term (2-4 years) |

| Rising Demand for Raw and Minimally Processed Nuts | +0.5% | North America and Europe; niche adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nutritional Benefits Associated with Nuts Consumption

Peer-reviewed meta-analyses published in 2024 and 2025 demonstrate that daily consumption of 28 grams of tree nuts reduces low-density lipoprotein cholesterol by 4% to 6% and lowers cardiovascular event risk by approximately 20% over five years, prompting cardiologists to recommend nuts as a first-line dietary intervention before statin therapy. The FDA's 2025 revision of its "healthy" claim criteria now permits manufacturers to highlight nuts' unsaturated fat profile on front-of-pack labels, a regulatory shift that elevates shelf appeal and justifies premium pricing[1]Source: U.S. Food and Drug Administration, “Use of the Term ‘Healthy’ in Food Labeling,” fda.gov. The 2025-2030 Dietary Guidelines for Americans explicitly list nuts among preferred protein sources, embedding them into school lunch programs and institutional foodservice contracts that collectively serve over 30 million meals daily. This policy endorsement creates a halo effect, as consumers perceive nuts as government-sanctioned health foods rather than indulgent snacks. Emerging research links pistachio consumption to improved glycemic control in pre-diabetic adults, opening pathways into clinical nutrition channels and diabetes-management programs. The convergence of regulatory approval, clinical evidence, and institutional adoption positions nuts as functional foods, driving sustained volume growth across demographic segments.

Convenience and On-the-Go Snacking

Urbanization and longer commute times have compressed meal occasions, with 42% of United States consumers reporting they skip breakfast at least twice weekly, creating demand for portable, nutrient-dense alternatives, according to the USDA Economic Research Service. Single-serve nut packs, typically 28 to 42 grams, fit into car cup holders, laptop bags, and gym lockers, aligning with micro-snacking behaviors that fragment traditional three-meal patterns. Retailers have responded by expanding checkout and impulse zones dedicated to grab-and-go formats, which command 15% to 20% price premiums over bulk packaging yet turn inventory faster. The rise of hybrid work schedules in 2025 further accelerates this trend, as employees stock home offices with shelf-stable snacks that require no refrigeration or preparation. Manufacturers are investing in resealable pouches and portion-control packaging that preserves freshness across multiple consumption occasions, addressing the key friction point of stale product after opening. Convenience stores in Asia-Pacific markets, particularly Japan and South Korea, now dedicate entire aisles to nuts and seeds, reflecting their integration into daily routines rather than occasional indulgence

Product Innovation and Flavor Diversification

Flavor innovation has migrated beyond salt and honey-roasted to include sriracha-lime, truffle-parmesan, and Korean gochugaru blends, targeting millennials and Gen Z consumers who prioritize novel taste experiences over brand heritage. Blue Diamond's 2025 launch of a bold-flavored almond line featuring globally inspired seasonings achieved distribution in over 15,000 United States retail outlets within six months, demonstrating retailers' appetite for differentiated SKUs. The Wonderful Company introduced a pistachio-based protein powder in early 2026, extending the ingredient into smoothie and baking categories and capturing incremental occasions beyond snacking. Flavor diversification also serves a strategic purpose: it fragments the market, making it harder for private-label competitors to replicate entire portfolios and thereby protecting branded players' shelf space. Smaller producers leverage co-manufacturing relationships to test limited-edition flavors, matcha-wasabi, and maple-bourbon, using social media pre-orders to validate demand before committing to full production runs. This agile approach reduces inventory risk and generates buzz among food influencers, who amplify reach at minimal cost.

Increased Interest in Organic and Natural Products

USDA-certified organic nut acreage in California expanded by 12% between 2024 and 2025, driven by grower premiums that average 30% to 40% above conventional pricing and consumer willingness to pay retail premiums of 25% to 35%[2]Source: U.S. Department of Agriculture and U.S. Department of Health and Human Services, “Dietary Guidelines for Americans 2025-2030,” dietaryguidelines.gov. Organic certification prohibits synthetic pesticides and fertilizers, appealing to health-conscious buyers who perceive these products as safer and more environmentally sustainable. Retailers such as Whole Foods Market and Trader Joe's allocate disproportionate shelf space to organic nuts, reinforcing the perception that organic is the default choice for discerning shoppers. The European Union's Farm to Fork strategy, which targets 25% of agricultural land under organic management by 2030, is accelerating organic nut imports from Turkey and the United States to meet rising European demand. Clean-label trends intersect with organic growth, as consumers scrutinize ingredient lists and reject products containing artificial flavors, colors, or preservatives. Brands that combine organic certification with minimal processing—dry-roasted without oil, lightly salted—capture the intersection of health, transparency, and environmental stewardship, a positioning that commands loyalty and reduces price sensitivity.

Restaint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Disruptions and Raw Material Shortages | -0.6% | North America (California), Middle East (Iran), Vietnam | Short term (≤ 2 years) |

| Tree Nut Allergies | -0.5% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Competition from Fresh Nuts | -0.3% | North America and Europe with robust cold-chain infrastructure | Medium term (2-4 years) |

| Processing Complexity and Cost | -0.4% | Global, with margin pressure most severe in fragmented markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Disruptions and Raw Material Shortages

California produces approximately 80% of the world's almonds and 50% of the United States pistachios, yet the state's 2024 almond harvest fell 8% below the five-year average due to drought-induced water allocations that restricted irrigation during the critical bloom period. The California Department of Water Resources projects that 2026 allocations will remain 20% below historical norms, compelling growers to fallow marginal acreage and prioritize high-value pistachio orchards over almonds. Iran, the world's largest pistachio exporter, faced export disruptions in 2024 due to geopolitical tensions and banking sanctions that delayed shipments and elevated freight costs by 15% to 25%. Vietnam's cashew processing sector, which handles 60% of global raw cashew imports, experienced labor shortages in 2025 as workers migrated to higher-wage manufacturing jobs, raising processing costs and extending lead times, according to the Vietnam Cashew Association[3]Source: Vietnam Cashew Association, “Industry Statistics,” vinacas.org.vn. These supply-side shocks compress processor margins and force brands to either absorb cost increases or pass them to consumers, risking volume declines in price-sensitive segments.

Tree Nut Allergies

Tree nut allergies affect 0.5% to 1.0% of the United States population, with prevalence rising among children born after 2010, and reactions range from mild hives to anaphylaxis requiring emergency epinephrine administration. The Food Allergen Labeling and Consumer Protection Act mandates that manufacturers declare tree nuts on ingredient panels and implement rigorous cleaning protocols to prevent cross-contact in shared facilities, adding compliance costs estimated at 5% to 8% of production expenses. Schools and daycare centers increasingly ban nuts to protect allergic children, eliminating a significant consumption occasion and reducing household purchase frequency. Foodservice operators face liability exposure, prompting many to remove nuts from menus or confine them to isolated prep areas, which shrinks the addressable market. Emerging immunotherapy treatments show promise in desensitizing allergic individuals, yet widespread adoption remains years away, leaving allergen concerns as a persistent headwind that constrains category penetration and innovation in multi-ingredient products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Pistachios Outpace Almonds on Health Halo

In 2025, almonds accounted for 28.28% of the market share, driven by their adaptability in snacking, baking, and plant-based milk. However, pistachios are expected to lead growth among all nuts, with a projected CAGR of 6.45% through 2031. Recent studies, including one published in the Journal of Nutrition, associate pistachios with benefits such as enhanced glycemic control and reduced inflammation markers, positioning them as a preferred functional snack for health-conscious and pre-diabetic consumers. The Wonderful Company leverages its vertically integrated operations, from California orchards to retail packaging, to drive innovation, as demonstrated by its planned 2026 launch of a pistachio-based protein powder, which expands pistachio applications into smoothies and baking. Walnuts appeal to older consumers seeking omega-3 fatty acids for cardiovascular health, but their shorter shelf life and susceptibility to rancidity limit their distribution in warmer regions without cold-chain infrastructure. Peanuts, though technically legumes, are perceived as tree nuts by consumers and dominate value-driven segments due to their lower production costs.

However, they face challenges from allergen concerns and a perception of lower nutritional value compared to tree nuts. Other nuts, such as hazelnuts, pecans, and macadamias, occupy niche markets: hazelnuts are prominent in European confectionery, pecans are popular in U.S. holiday baking, and macadamias are favored in Asia-Pacific premium gifting. California's 2024 pistachio harvest reached a record 1.6 billion pounds, reflecting a 10% increase from 2023, supported by favorable weather and maturing orchards planted in the early 2010s. This supply growth coincides with increasing consumer awareness of pistachios' protein content, 6 grams per ounce compared to 4 grams for cashews, creating a balanced demand-supply dynamic that supports volume growth without significant price increases. At the same time, almond processors, facing tighter margins due to drought-related yield declines, are shifting toward almond flour and almond butter to target higher-value applications. This strategic move helps stabilize revenue even as whole-nut sales stagnate. The contrasting trends of abundant pistachio supplies and limited almond availability are reshaping competitive dynamics, with brands reallocating marketing budgets to the rapidly growing pistachio segment to optimize returns.

By Category: Organic Premiums Justify Certification Costs

Conventional nuts held 75.22% of market share in 2025, reflecting their price accessibility and ubiquity across retail channels, yet organic variants are expanding at 7.03% CAGR through 2031 as consumers prioritize transparency and environmental stewardship. USDA-certified organic nut acreage in California grew 12% between 2024 and 2025, driven by grower premiums averaging 30% to 40% above conventional pricing, which offset the higher labor and input costs associated with organic farming. Retailers such as Whole Foods Market allocate disproportionate shelf space to organic nuts, reinforcing consumer perception that organic is the default choice for health-conscious shoppers. The European Union's Farm to Fork strategy, targeting 25% of agricultural land under organic management by 2030, is accelerating organic nut imports from Turkey and the United States to meet rising European demand. Organic certification prohibits synthetic pesticides and fertilizers, appealing to buyers who perceive these products as safer and more environmentally sustainable, even as peer-reviewed studies find minimal nutritional differences between organic and conventional nuts. The willingness to pay retail premiums of 25% to 35% for organic nuts signals that purchasing decisions are driven by values and identity as much as by functional benefits, a dynamic that insulates organic players from price-based competition.

Clean-label trends intersect with organic growth, as consumers scrutinize ingredient lists and reject products containing artificial flavors, colors, or preservatives. Brands that combine organic certification with minimal processing, dry-roasted without oil, and lightly salted capture the intersection of health, transparency, and environmental stewardship. Conventional nuts remain dominant in foodservice and industrial channels, where cost considerations outweigh certification, yet even these segments are witnessing gradual organic penetration as institutional buyers respond to sustainability mandates and consumer pressure. The organic-conventional price gap has narrowed from 40% in 2020 to 30% in 2025, driven by scale economies as more acreage converts and processing infrastructure expands, suggesting that organic could approach parity in select categories by 2030.

By Flavor: Plain leads while spicy and sweet coatings penetrate

Plain and salted nuts commanded 68.95% of market share in 2025, anchored by their versatility and broad demographic appeal, yet flavored varieties are projected to grow at 6.63% CAGR through 2031 as brands target millennials and Gen Z consumers who prioritize novel taste experiences. Flavor innovation fragments the market, making it harder for private-label competitors to replicate entire portfolios and thereby protecting branded players' shelf space and pricing power. Smaller producers leverage co-manufacturing relationships to test limited-edition flavors, matcha-wasabi, and maple-bourbon, using social media pre-orders to validate demand before committing to full production runs, an agile approach that reduces inventory risk and generates buzz among food influencers. Honey-roasted variants remain popular in North America, yet their higher sugar content conflicts with clean-label trends, prompting reformulations that use date syrup or monk fruit as natural sweeteners.

Globally inspired flavors reflect increasing culinary diversity and travel exposure, with consumers seeking authentic taste profiles that evoke specific cuisines or regions. Tandoori-spiced cashews, za'atar almonds, and chili-lime peanuts bridge snacking and meal occasions, positioning nuts as accompaniments to craft beer or charcuterie boards rather than standalone snacks. This repositioning elevates nuts from commodity to premium, justifying price points 20% to 30% above plain varieties. Plain and salted formats retain dominance in foodservice and industrial channels, where cost and versatility outweigh flavor differentiation, yet even these segments are witnessing gradual flavor penetration as operators seek menu differentiation. The flavor-plain price gap has widened from 15% in 2020 to 25% in 2025, driven by higher ingredient costs and smaller production runs, suggesting that flavored nuts will remain a premium tier rather than mass-market default.

By Distribution Channels: E-Commerce Disrupts Shelf Allocation

Supermarkets and hypermarkets accounted for 48.23% of distribution in 2025, leveraging their scale to negotiate favorable terms with suppliers and offer competitive pricing, yet online retail is expanding at 7.02% CAGR through 2031 as consumers prize convenience and assortment breadth. Amazon's Subscribe & Save program, which offers 5% to 15% discounts on recurring nut deliveries, has captured an estimated 12% of United States online nut sales, creating predictable revenue streams for brands and reducing customer acquisition costs. Direct-to-consumer brands such as NatureBox and Thrive Market bypass traditional retail, using subscription models to build customer databases and gather zero-party data that inform product development and personalized marketing. E-commerce platforms enable long-tail assortment, heirloom walnut varieties, single-origin cashews, and rare macadamias that physical stores cannot economically stock, appealing to enthusiasts willing to pay premiums for provenance and uniqueness.

Convenience and grocery stores captured a smaller share but serve critical impulse and top-up occasions, particularly in urban centers where consumers shop multiple times weekly. These channels prioritize single-serve formats and high-turnover SKUs, limiting assortment but achieving higher sales per square foot than larger formats. Other distribution channels, including specialty stores, health food outlets, and vending machines, cater to niche segments and premium positioning, often featuring organic, raw, or exotic nut varieties. Vending machines in gyms and office buildings have increasingly stocked nuts as healthier alternatives to chips and candy, reflecting institutional wellness initiatives and consumer demand for protein-rich snacks. Supermarkets and hypermarkets retain advantages in price competitiveness and immediacy, yet their share erosion to online and convenience channels signals a fragmentation of shopping behaviors that requires omnichannel strategies to maintain market presence.

Geography Analysis

In 2025, Europe accounted for 40.28% of global revenue, with Germany and the UK surpassing an annual intake of 3 kilograms per capita. The EU's 'Farm to Fork' strategy is driving an increase in organic imports from Turkey and the U.S., aiming to promote sustainable food systems. Additionally, France's strong demand for protected-designation hazelnuts sustains a significant 30-40% price premium, reflecting the value placed on quality and origin. Spain's extensive almond orchards play a crucial role in supporting intra-EU trade, while the Netherlands has established itself as a vital re-export hub, facilitating the distribution of nuts across Europe.

Asia-Pacific, led by China's expanding middle class and India's cultural tradition of festive gifting, is experiencing the fastest growth with a 6.89% CAGR. Chinese e-commerce giants are leveraging holiday seasons by bundling nuts with dried fruits in promotional packages, enhancing consumer appeal. In India, cashew processing not only anchors local employment but also presents untapped potential for increased household consumption. Japan's aging population is driving demand for walnuts due to their omega-3 health benefits, while South Korea's preference for honey-butter almonds highlights the growing importance of flavor localization in the region. Australia's macadamia exports cater to the premium gifting market in Asia, and Vietnam's large-scale processing capabilities remain a cornerstone of the global cashew supply chain, ensuring consistent supply to international markets.

North America, with a stable per-capita consumption of 2.5 kilograms, continues to achieve mid-single-digit growth, fueled by the rising popularity of organic products and innovative flavor options. Canada remains a net importer of nuts, while Mexico's young and urban demographic is increasingly adopting nuts as a healthier snacking alternative, reflecting a shift in dietary preferences. In South America, although overall consumption remains modest, it is steadily increasing. Brazil is leveraging its native Brazil nuts to strengthen its position in the market, while Argentina is showing a growing inclination toward almonds and walnuts. In the Middle East, the hospitality sector demonstrates a strong preference for premium pistachios and almonds, driven by consumer demand for high-quality products. Furthermore, Saudi Arabia's Vision 2030 initiative is actively investing in domestic roasting capacities, aiming to enhance value retention and reduce reliance on imports.

Competitive Landscape

The nuts market, marked by its high level of fragmentation, presents significant opportunities for both market consolidation and the development of specialized strategies across various product categories and geographic regions. This fragmentation arises primarily from the agricultural nature of the industry, where production occurs across a wide range of climatic zones and farming operations, making centralized control and standardization a complex endeavor. Furthermore, the processing and distribution stages demand a nuanced understanding of local market dynamics and supply chain intricacies, which further amplifies the fragmented structure of the market.

Prominent industry players such as Blue Diamond Growers, Hormel Foods Corporation, and Wonderful Company capitalize on vertical integration to maintain product quality, manage operational costs, and streamline their processes. In contrast, numerous regional processors and niche brands establish their market presence by focusing on differentiation, leveraging innovation, and implementing strategies that cater to specific consumer demands and preferences.

In this competitive and evolving landscape, the integration of advanced technology has emerged as a critical factor in driving operational efficiency and ensuring superior product quality. Companies are increasingly investing in state-of-the-art automated processing systems designed for grading, sorting, roasting, seasoning, and packaging. These technological advancements not only help reduce labor costs but also ensure consistent product quality, which is vital for building consumer trust and complying with stringent regulatory requirements. By adopting such innovations, companies are better positioned to meet the growing demand for high-quality nuts while maintaining a competitive edge in the market.

Nuts Industry Leaders

Blue Diamond Growers

Hormel Foods Corporation

The Wonderful Company

Baja Food Industries Company

Mariani Nut Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Blue Diamond Growers, the world's top almond marketer and processor, has teamed up with Mike's Hot Honey, America's premier and original hot honey brand, to unveil a new flavor: Hot Honey Almonds. This daring snack harmoniously fuses the unique tastes of honey and chili with Blue Diamond's almonds, resulting in a delectable sweet-and-spicy treat.

- December 2024: Emerald Nuts, a Flagstone Foods subsidiary, has introduced two new nut varieties: Absolutely Everything Almonds & Cashews and Hot Honey Cashews. The company asserts that both offerings are non-GMO and devoid of high-fructose corn syrup, artificial flavors, preservatives, and synthetic colors.

- April 2024: Planters, a Hormel Foods brand, has unveiled its latest innovation in snack nuts: the "Plant Nut Duos Snacks". The new lineup features enticing combinations such as Buffalo Cashews paired with Ranch Almonds, Cocoa Cashews alongside Espresso Hazelnuts, and Parmesan Cheese Cashews teamed with Peppercorn Pistachios.

- April 2024: Blue Diamond Growers, the world's largest almond marketer and processor, announced its new Almond Breeze® partner, Kagome Co., Ltd. for all production and distribution in Japan. The new partnership will focus on accelerating market growth and driving new demand for Almond Breeze®.

Global Nuts Market Report Scope

Nuts are fruits that consist of a shell protecting a kernel that is generally edible. Nuts are a rich source of vitamins, protein, antioxidants, fiber, and other essential minerals, offering health benefits such as enhanced energy, and stamina, providing better digestion and overall health. Nuts can be easily transported at room temperature, stored for a long period of time, and consumed with minimum preparation. The Global Nut market (henceforth referred to as the market studied) is segmented by type, category, coating type, form, end-user, distribution channel, and geography. By type, the market is segmented into almonds, brazil nuts, cashews, chestnuts, hazelnuts, hickory nuts, macadamia nuts, pecans, pine nuts, pistachios, walnuts, peanuts, and others. By category, the market is bifurcated into conventional and organic. By coating type, the market is bifurcated into coated and uncoated. By form, the market is segmented into whole, diced/cut, roasted, and granular. By End-user, the market is segmented into household/retail and food service sector. Based on the distribution channel, the market studied is segmented into offline and online channels. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, Middle East, and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Type

| Almonds |

| Cashews |

| Walnuts |

| Peanuts |

| Pistachios |

| Other Product Types |

By Category

| Conventional |

| Organic |

By Flavor

| Plain/Salted |

| Flavored |

By Distribution Channels

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Type | Almonds | |

| Cashews | ||

| Walnuts | ||

| Peanuts | ||

| Pistachios | ||

| Other Product Types | ||

| By Category | Conventional | |

| Organic | ||

| By Flavor | Plain/Salted | |

| Flavored | ||

| By Distribution Channels | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the global Nuts market in 2031?

The market is forecast to reach USD 52.33 billion by 2031.

Which nut type is expected to grow fastest to 2031?

Pistachios are projected to advance at a 6.45% CAGR through 2031.

How large is the organic share within the category?

Organic products represented 24.78% of 2025 sales and are expanding at a 7.03% CAGR.

Which region shows the highest growth outlook?

Asia-Pacific is set to grow at a 6.89% CAGR between 2026-2031.

Page last updated on: