Honey Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

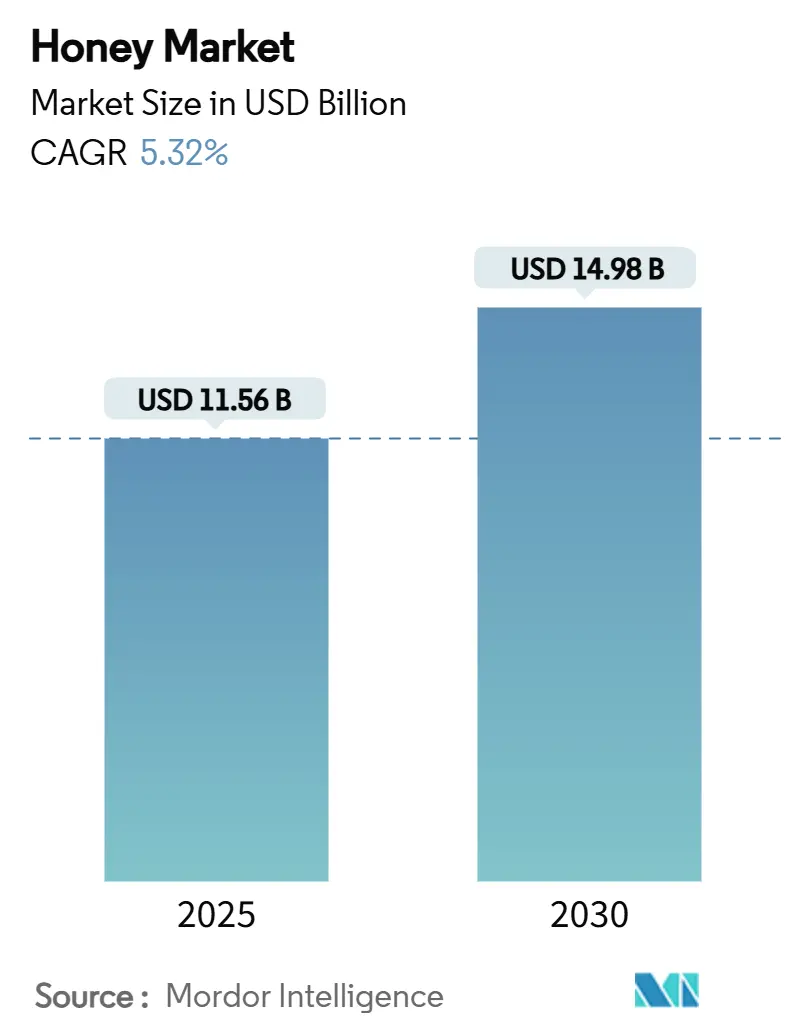

| Market Size (2025) | USD 11.56 Billion |

| Market Size (2030) | USD 14.98 Billion |

| Growth Rate (2025 - 2030) | 5.32% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Honey Market Analysis by Mordor Intelligence

The honey market size, valued at USD 11.56 billion in 2025, is expected to reach USD 14.98 billion by 2030, growing at a CAGR of 5.32%. This growth stems from the increased adoption of natural sweeteners, the expanded use of honey as a functional food, and higher demand from processed food manufacturers. The monofloral honey segment is experiencing substantial growth in the global market, driven by shifting consumer preferences toward premium and specialty varieties. These monofloral honeys, derived primarily from single floral sources like acacia, buckwheat, or clover, offer distinct flavors, aromas, and health benefits. The food and beverages segment maintains its dominant position in the global honey market, representing the highest consumption share. Manufacturers increasingly use honey as a natural sweetener and functional ingredient in baked goods, confectionery, dairy products, and beverages, including teas and health drinks. Despite market growth, challenges persist through supply limitations, authentication requirements, and premium pricing structures in this developing market.

Key Report Takeaways

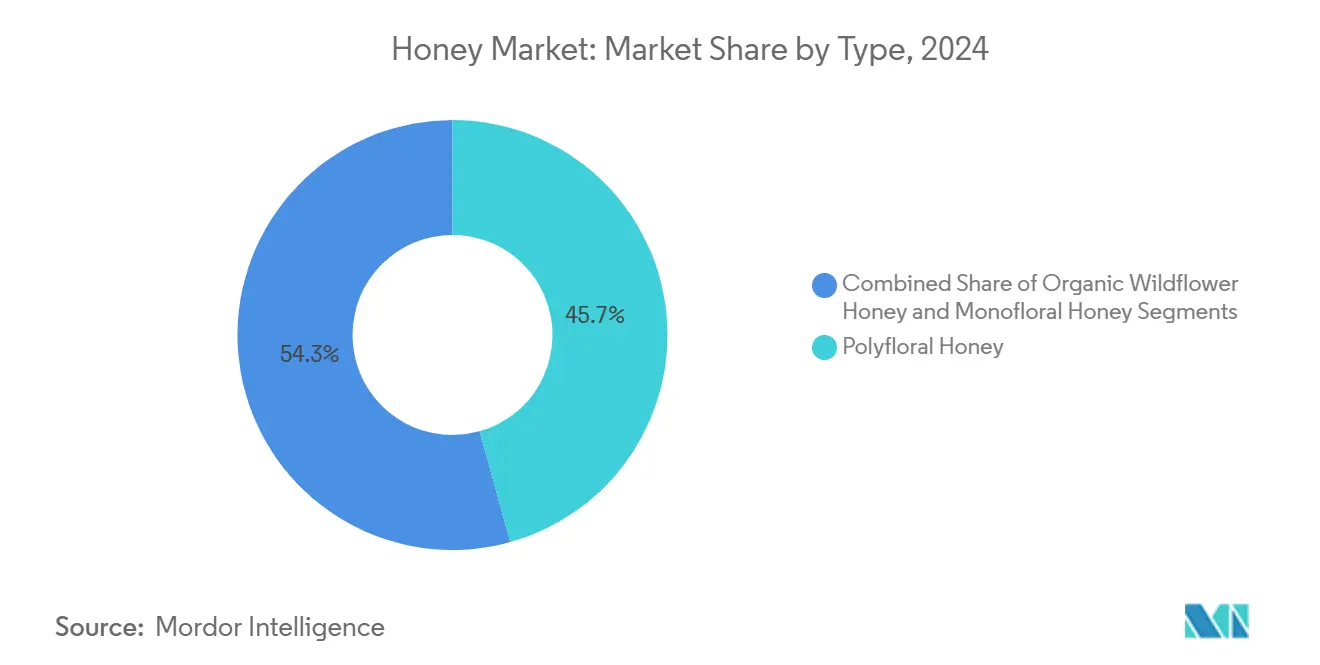

- By type, the polyfloral honey segment led with 45.66% of the 2024 honey market share, while organic wildflower honey is forecast to post an 8.80% CAGR from 2025-2030.

- By processing, conventional methods held 71.95% of the honey market share in 2024; organic processing is set to rise at 9.56% CAGR through 2030.

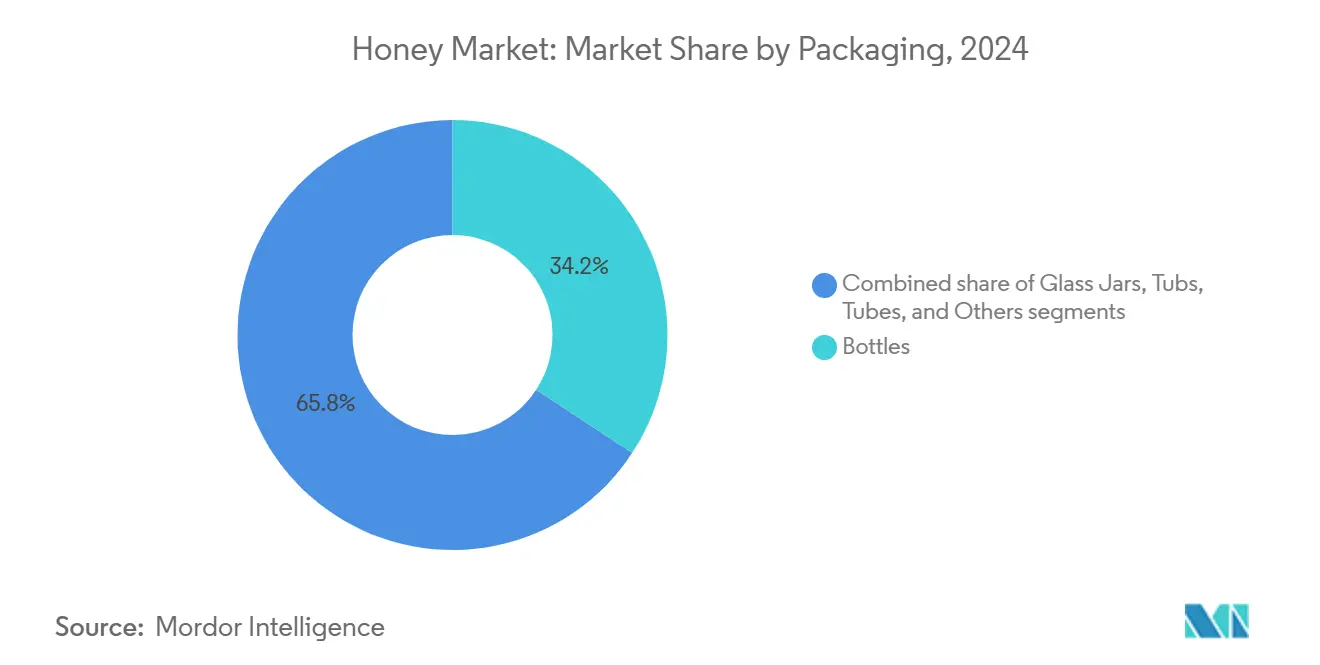

- By packaging, bottles commanded 34.23% revenue share in 2024, whereas glass jars are on track for 5.87% CAGR.

- By end use, retail accounted for 60.59% of the 2024 honey market size; foodservice/HORECA will expand at 8.74% CAGR during the outlook period.

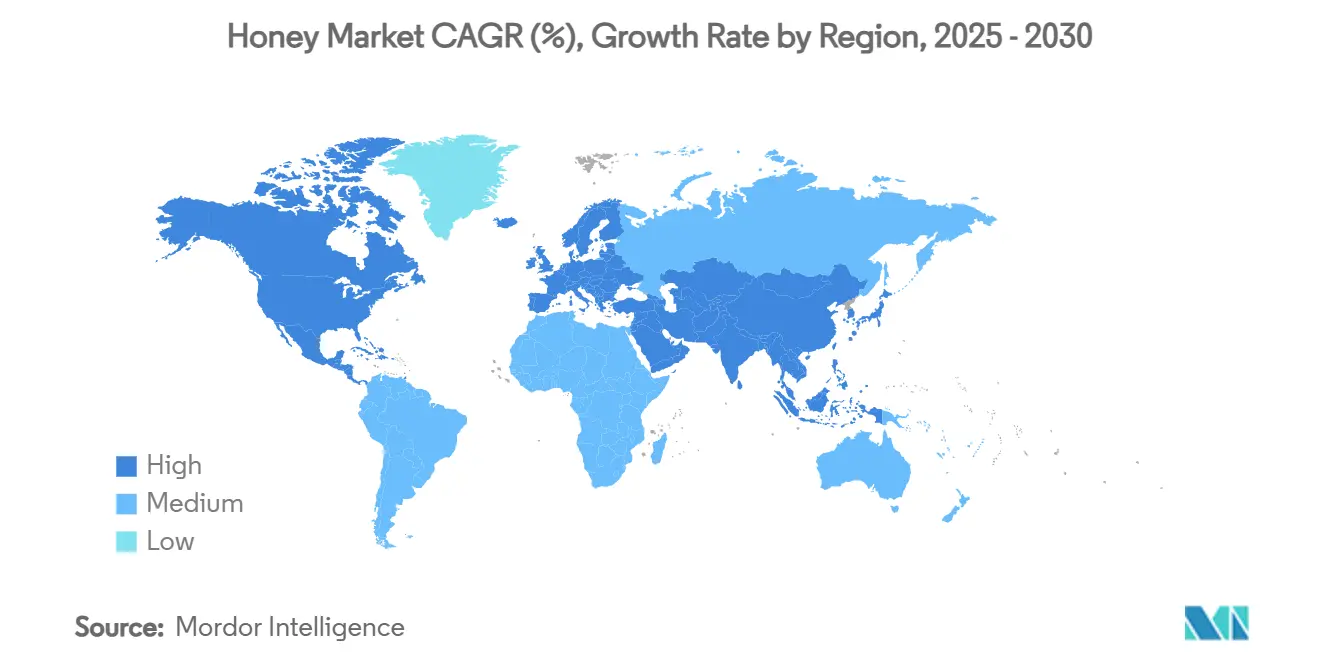

- By geography, Asia-Pacific secured 33.48% of 2024 sales, and the Middle East and Africa region is projected to log a 7.53% CAGR to 2030.

Global Honey Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer shift toward natural sweeteners | +1.2% | Global, with strongest adoption in North America and Europe | Medium term (2-4 years) |

| Heightened immunity-centric health consciousness | +0.8% | Global, particularly Asia-Pacific and North America | Short term (≤ 2 years) |

| Expansion of the food and beverage processing industry | +0.9% | Global, led by Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Government support and regulatory frameworks | +0.6% | Europe, North America, with spillover to other regions | Medium term (2-4 years) |

| Premiumisation via organic and certified honey lines | +0.7% | Europe, North America, Australia/New Zealand | Medium term (2-4 years) |

| Increasing adoption in pharmaceuticals and nutraceuticals | +0.5% | Global, with concentration in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Shift Toward Natural Sweeteners

The shift from artificial to natural sweeteners is driving increased honey demand, with the National Honey Board's 2024 consumer study showing honey as the preferred sweetener across meal occasions among United States consumers[1]Source: National Honey Board, "Attitudes & Usage Study - 2024," honey.com. Consumers favor honey for its natural properties, complex flavor profile, and purity - attributes that artificial sweeteners cannot match. The International Food Information Council's 2024 report shows that 26% of U.S. consumers link "natural" and "organic" terms with enhanced food safety, increasing confidence in products with these certifications[2]Source: International Food Information Council, "2024 IFIC Food & Health SURVEY," foodinsight.org. Food manufacturers are responding by reformulating products to meet clean-label requirements, creating new opportunities for industrial honey procurement beyond retail channels. The FDA's updated guidance on natural claims provides clear guidelines for honey-based product marketing. The economic impact is significant, as honey's premium pricing over conventional sweeteners enables higher margins across the supply chain while increasing its use in processed foods. This market evolution strengthens honey's position as both a functional ingredient and a trusted choice for consumers focused on food transparency and safety.

Heightened Immunity-Centric Health Consciousness

Post-pandemic health awareness permanently altered consumer behavior, positioning honey as a functional food rather than merely a sweetener, particularly for its perceived immune-supporting properties. This behavioral shift transcends demographic boundaries, with consumers increasingly willing to pay premiums for products containing honey, as evidenced by the National Honey Board's findings that significant portions of shoppers support bee-friendly causes. The pharmaceutical validation of honey's therapeutic properties, particularly Manuka honey's methylglyoxal and dihydroxyacetone compounds, provides scientific backing for consumer perceptions. This trend creates market differentiation opportunities, as producers leverage specific floral varieties and processing methods to enhance bioactive compound concentrations. The immunity focus also drives seasonal consumption patterns, with winter months showing elevated demand for honey-based remedies and supplements.

Expansion of the Food and Beverage Processing Industry

Industrial honey consumption is increasing as food processors incorporate natural ingredients to address consumer preferences and comply with regulations. According to the OECD-FAO Agricultural Outlook 2024-2033, global food consumption will grow by 1.2% annually, with emerging economies increasing their demand for processed foods containing natural sweeteners[3]Source: OECD, "OECD-FAO Agricultural Outlook 2024-2033," oecd.org. The industrial segment presents significant volume opportunities compared to retail channels, as manufacturers require steady, large-scale honey supplies for their product formulations. This trend benefits standardized honey varieties more than specialty products, as processors focus on functional properties and cost predictability rather than premium positioning. The growth in the processing industry is advancing technological developments in honey handling, storage, and quality control systems. This creates competitive advantages for suppliers who meet industrial specifications while preserving natural product integrity. The Federation of German Food and Drink Industries (BVE) reported that Germany's processed food and beverage production reached USD 252.1 billion (EUR 232.6 billion) in 2023, a 6% increase from 2022. This growth in one of Europe's major food manufacturing markets indicates the increasing industrial demand for natural ingredients like honey, as processors expand production for domestic and export markets. Honey suppliers who provide quality, traceability, and supply security are positioned to benefit from this industrial market growth.

Government Support and Regulatory Frameworks

Regulatory frameworks support honey production through direct subsidies and support mechanisms. The European Union increased apiculture funding from EUR 40 million in 2019 to EUR 60 million annually from 2021 under the Common Agricultural Policy[4]Source: European Commission, "Agriculture and rural development," europa.eu. These initiatives include research funding, training programs, and infrastructure development to strengthen the value chain. The EU established the Honey Platform in June 2024 to enhance industry support through authenticity controls and market development. Government support includes trade protection measures, such as U.S. antidumping duties on honey imports from Vietnam, Brazil, and Argentina, which help maintain stable prices for domestic producers. These regulatory developments demonstrate a policy commitment to honey industry sustainability, encouraging investment in production capacity and quality improvements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Honey adulteration and authenticity concerns | -0.9% | Global, particularly Europe and North America | Short term (≤ 2 years) |

| Bee-population decline and climate-related crop stress | -1.1% | Global, with severe impacts in North America and Europe | Medium term (2-4 years) |

| Dependence on supplemental feeding | -0.4% | Global, concentrated in intensive beekeeping regions | Medium term (2-4 years) |

| Sustainability and cost challenges in green transition | -0.6% | Europe, North America, with expansion to other developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Honey Adulteration and Authenticity Concerns

Honey adulteration and authenticity concerns constrain the global honey market by eroding consumer trust and industry credibility. Widespread adulteration practices make it challenging for consumers to identify genuine honey products, leading to reduced market demand. Inconsistent regulatory enforcement and varying quality standards across regions enable the proliferation of counterfeit products, particularly in markets with limited oversight. New regulations, such as the European Union's origin disclosure requirements effective mid-2026, increase compliance costs and may disrupt existing trade patterns. The authenticity concerns affect all market segments, with even premium products facing scrutiny that restricts market growth. Small-scale producers often cannot access the sophisticated testing technologies needed to verify honey authenticity. The absence of unified certification and quality assurance standards further impedes industry efforts to combat adulteration.

Bee-Population Decline and Climate-Related Crop Stress

The global honey market faces significant constraints due to declining bee populations and climate-related crop stress. Research from Washington State University entomologists indicates that honey bee colonies in the U.S. may decline by up to 70% in 2025, compared to the 40-50% annual losses observed in the past decade. Multiple factors contribute to this decline, including nutritional deficiencies, mite infestations, viral diseases, pesticide exposure, and habitat changes. Climate-related challenges intensify these issues by affecting the availability and quality of floral resources necessary for bee nutrition. Extreme weather events, disrupted flowering patterns, and habitat degradation reduce nectar and pollen sources, resulting in weakened bee colonies that become more susceptible to diseases and environmental toxins. While certain regions, particularly in Asia, maintain stable or increasing bee populations through favorable conditions and commercial beekeeping initiatives, the global situation remains problematic. The honey market may experience supply limitations, price fluctuations, and increased need for innovation in honey production and pollination management without proper conservation and sustainable beekeeping measures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Polyfloral Dominance Amid Organic Specialization

Polyfloral honey holds a 45.66% market share in 2024, driven by its wide application in food products and broad consumer acceptance. The segment's leadership position is attributed to its consistent flavor profile and cost-effectiveness, particularly in industrial food processing, where standardized taste is essential. Meanwhile, organic wildflower honey is projected to grow at 8.80% CAGR through 2030, driven by increasing demand for pesticide-free options.

The growth in organic wildflower honey aligns with the rising consumer preference for clean-label products and transparent production methods. Organic certification provides quality assurance and supports premium pricing strategies while creating market entry barriers for conventional producers. Regional preferences vary significantly, with European consumers favoring monofloral varieties and North American markets preferring polyfloral blends, influencing producers' market expansion strategies.

By Processing: Conventional Scale Versus Organic Premiums

The honey market shows a distinct split in processing methods, with conventional processing holding 71.95% market share in 2024, while organic processing grows at 9.56% CAGR through 2030. This growth in organic processing stems from consumers' readiness to pay higher prices for products they perceive as pure and environmentally friendly. Conventional processing remains dominant due to its economies of scale and established distribution networks, especially in industrial applications where cost efficiency is crucial.

The organic segment's expansion is supported by regulations and consumer awareness programs that emphasize processing method distinctions. According to the CBI Ministry of Foreign Affairs, Europe dominates organic honey imports with 48% of global certified honey imports, valued at EUR 986 million in 2023. This demonstrates strong market acceptance of premium products with specific origin and processing certifications. The processing divide also spurs innovation, as organic producers develop new preservation methods and quality control systems that maintain product purity without synthetic additives. This development benefits producers who can demonstrate effective organic processing while meeting large-scale production demands.

By Packaging: Sustainability Drives Glass Innovation

Bottles hold a 34.23% market share in 2024, maintaining their dominant position through cost efficiency and widespread consumer acceptance. Glass jars are projected to grow at a 5.87% CAGR through 2030, driven by increasing sustainability preferences in packaging choices. The packaging segment reflects environmental awareness trends, as consumers evaluate packaging materials and seek recyclable options that complement honey's natural attributes. Glass jars command premium positioning through their reusability and aesthetic appeal, particularly in gift and specialty honey segments.

Tubes and tubs address specific market needs, with tubes gaining adoption in foodservice applications where portion control and hygiene are essential, while tubs target bulk consumers prioritizing value. Packaging developments include integrated technology solutions for product authentication and traceability, addressing quality concerns, and improving consumer trust. Environmental regulations in Europe and North America support the growth of glass packaging, as producers align with circular economy requirements and use environmental performance for product differentiation.

By End Use: Foodservice Momentum Challenges Retail Dominance

The retail segment holds a 60.59% market share in 2024, supported by established distribution networks and consistent consumer purchasing patterns. Meanwhile, the foodservice/HORECA segments are projected to grow at 8.74% CAGR through 2030, driven by increased adoption of honey as a natural sweetener in restaurants and hotels. The retail segment's leadership position stems from honey's role as a household staple, with supermarket distribution enabling broad consumer access and product visibility.

The industrial segment serves food processing companies that require natural sweetener alternatives, operating under distinct pricing and quality requirements compared to consumer markets. The foodservice segment's expansion reflects the growing use of honey in professional kitchens as an ingredient that enhances flavors while meeting clean-label demands. Hotels and restaurants in the HORECA segment increasingly utilize specialty honey varieties to enhance their offerings and support premium pricing strategies.

Geography Analysis

Asia-Pacific dominates the global honey market with a 33.48% share in 2024. The region's leadership stems from extensive beekeeping infrastructure, favorable climatic conditions, and government support for agricultural exports. Quality concerns regarding Chinese honey create market segmentation between the commodity and premium segments. India emerges as a significant player in both production and consumption, with research on Apis cerana breeding optimization indicating continued investment in indigenous bee varieties that could reshape regional supply dynamics.

The Middle East and Africa achieve the highest regional growth at 7.53% CAGR through 2030, reflecting emerging market development and increasing consumer awareness of honey's health benefits. The UAE serves as a regional hub with USD 22 billion in agricultural imports during 2023, as reported by the United States Department of Agriculture (USDA) creating distribution opportunities for international honey suppliers seeking Middle Eastern market access. Europe and North America represent mature markets with distinct characteristics. Europe accounts for 52% of global honey imports, while North America, led by the United States, consumes over 400 million pounds annually against domestic production of only 140 million pounds as per the USA Customs Clearance 2023 report.

The European market emphasizes quality and authenticity, with new labeling requirements mandating origin disclosure by mid-2026 and EUR 60 million in annual apiculture support creating competitive advantages for domestic producers as per the European Commission. South America contributes significantly to global trade, with Argentina and Brazil ranking among top exporters despite facing U.S. antidumping duties. A recent study revealed 30.4% annual colony losses across Latin America, indicating production challenges that could affect global supply chains.

Competitive Landscape

The honey market demonstrates high fragmentation, indicating an industry where regional producers and multinational brands operate without any single company holding significant market dominance. This fragmentation results from diverse production regions, varying consumer preferences, and limited barriers to entry. The major players in the market include Hive & Wellness Australia Pty Ltd, Barkman Honey LLC, Dabur India, Comvita Limited, and J.M. Smucker Company.

Companies that effectively manage regulatory requirements while maintaining quality standards gain competitive advantages, as demonstrated by Comvita's B Corp certification in 2023, which strengthened its position in premium market segments through verified sustainability practices and ethical sourcing. Companies focus on vertical integration and geographic expansion strategies to control their supply chains from beekeeping operations to retail distribution and enter new consumer markets across different regions.

Market opportunities exist in pharmaceutical applications, where Manuka honey's medical properties command higher prices due to its proven antibacterial and wound-healing properties, and in industrial food processing, where demand for natural sweeteners drives volume growth across bakery, beverage, and confectionery sectors. Competition has intensified as specialty producers challenge established companies by utilizing organic certification, origin authentication, and direct-to-consumer distribution to gain market share in high-value segments, particularly in premium and therapeutic honey categories.

Honey Industry Leaders

-

Hive & Wellness Australia Pty Ltd

-

Barkman Honey LLC

-

J.M. Smucker Company

-

Comvita Limited

-

Dabur India Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Wisdom Natural Brands, parent company of SweetLeaf natural sugar substitutes, has launched Drizzle Honey in the U.S. market following its acquisition of the Canadian honey brand in November. The initial product lineup includes Golden Raw Honey, White Raw Honey, and Turmeric Gold Raw Honey, available at Fresh Thyme stores, Amazon, and the Drizzle Honey website. The company plans additional product releases and retail expansion throughout the year.

- January 2024: Dabur, one of the leading firms in the Ayurvedic and personal care space, recently invested approximately INR 135 crore in expanding its manufacturing facility in South India. This move is geared toward bolstering the production capacity of its flagship products, including Dabur Honey, Dabur Red Paste, and Odonil air fresheners.

- January 2024: APIS Honey launched Apis Organic Honey, which is sourced from Kashmir. The products are available in attractive glass bottles. The products are available in different retail channels across India.

- November 2023: Nutriplus has introduced Busy Bee Monofloral Honey, a range of 100% raw, organic, unpasteurized single-flower honeys. The products are sourced from ethical apiaries and rural cooperative communities. The honey is harvested at controlled hive temperatures and bottled without additives, preserving its natural composition of enzymes, 22 types of amino acids, vitamins, and 27 minerals, including calcium, iron, zinc, magnesium, potassium, B vitamins, and selenium.

Global Honey Market Report Scope

| Monofloral Honey |

| Organic Wildflower Honey |

| Polyfloral Honey |

| Conventional |

| Organic |

| Glass Jars |

| Bottles |

| Tubs |

| Tubes |

| Others |

| Retail |

| Industrial |

| Foodservice/HORECA |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Monofloral Honey | |

| Organic Wildflower Honey | ||

| Polyfloral Honey | ||

| By Processing | Conventional | |

| Organic | ||

| By Packaging | Glass Jars | |

| Bottles | ||

| Tubs | ||

| Tubes | ||

| Others | ||

| By End Use | Retail | |

| Industrial | ||

| Foodservice/HORECA | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the honey market?

The honey market is valued at USD 11.56 billion in 2025 and is projected to reach USD 14.98 billion by 2030.

Which region leads the honey market?

Asia-Pacific held 33.48% of global sales in 2024, driven by China’s dominant production and export capacity.

Why are glass jars gaining share in honey packaging?

Glass jars grow at 5.87% CAGR because consumers and regulators favor recyclable, premium-looking packaging that aligns with sustainability goals.

How will organic processing influence future growth?

Organic processing is forecast at 9.56% CAGR as certified products command significant price premiums and meet tightening residue regulations.

Page last updated on: