HLA Typing For Transplant Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.77 Billion |

| Market Size (2031) | USD 1.09 Billion |

| Growth Rate (2026 - 2031) | 7.22% CAGR |

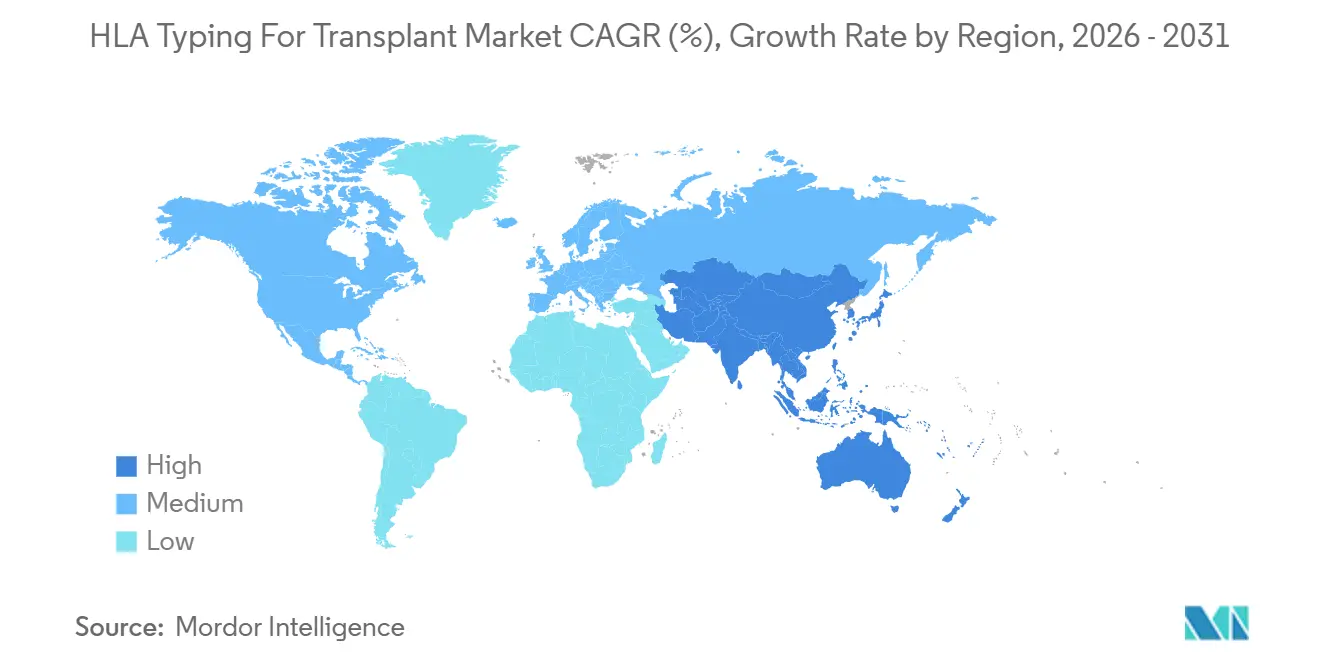

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HLA Typing For Transplant Market Analysis by Mordor Intelligence

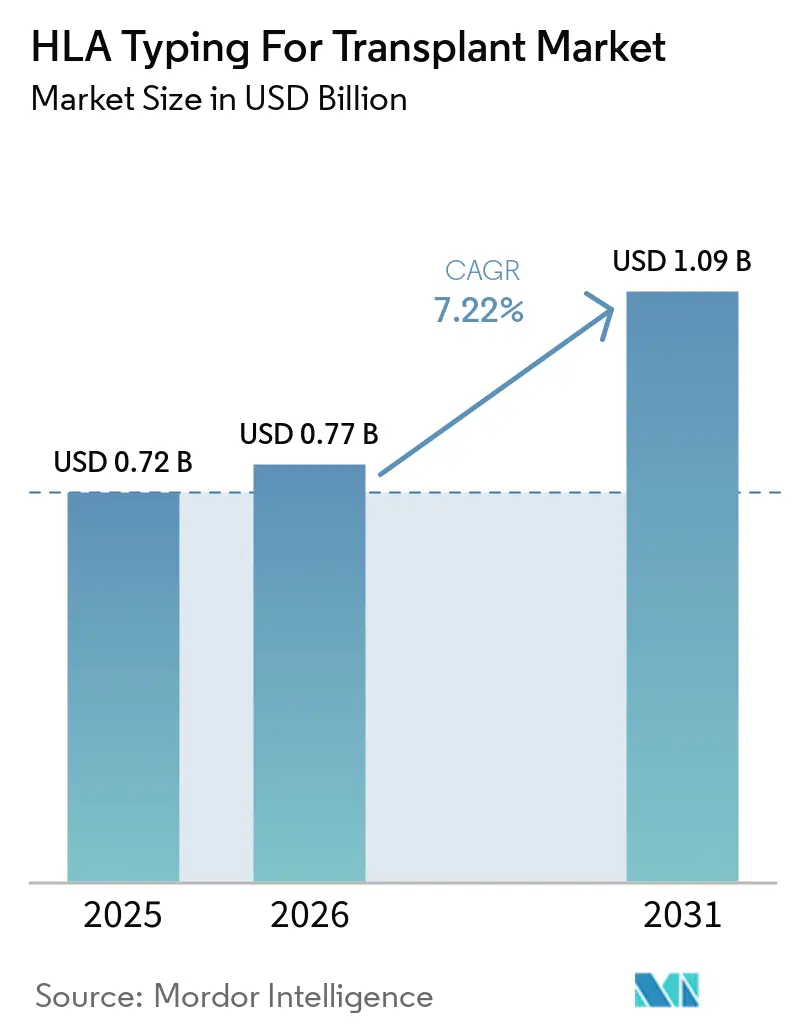

The HLA Typing For Transplant Market size is projected to expand from USD 0.72 billion in 2025 and USD 0.77 billion in 2026 to USD 1.09 billion by 2031, registering a CAGR of 7.22% between 2026 to 2031.

The market is being supported by record global transplant activity, with 173,727 solid organ transplants performed worldwide in 2024 and allogeneic hematopoietic cell transplantation in Europe reaching 21,023 procedures in the same year. The HLA Typing for Transplant market is also moving toward higher-resolution donor matching, which is widening the role of sequencing, bioinformatics, and multi-marker risk assessment in transplant workflows. Vendors are responding with broader NGS portfolios, long-read platforms, and more integrated software stacks, while acquisition activity is reshaping the reagent and workflow landscape. The HLA Typing for Transplant market still faces uneven reimbursement, integration gaps, and high migration costs for public and mid-volume laboratories, yet these same constraints are creating opportunities for large reference labs, premium assay vendors, and providers with end-to-end platforms.

Key Report Takeaways

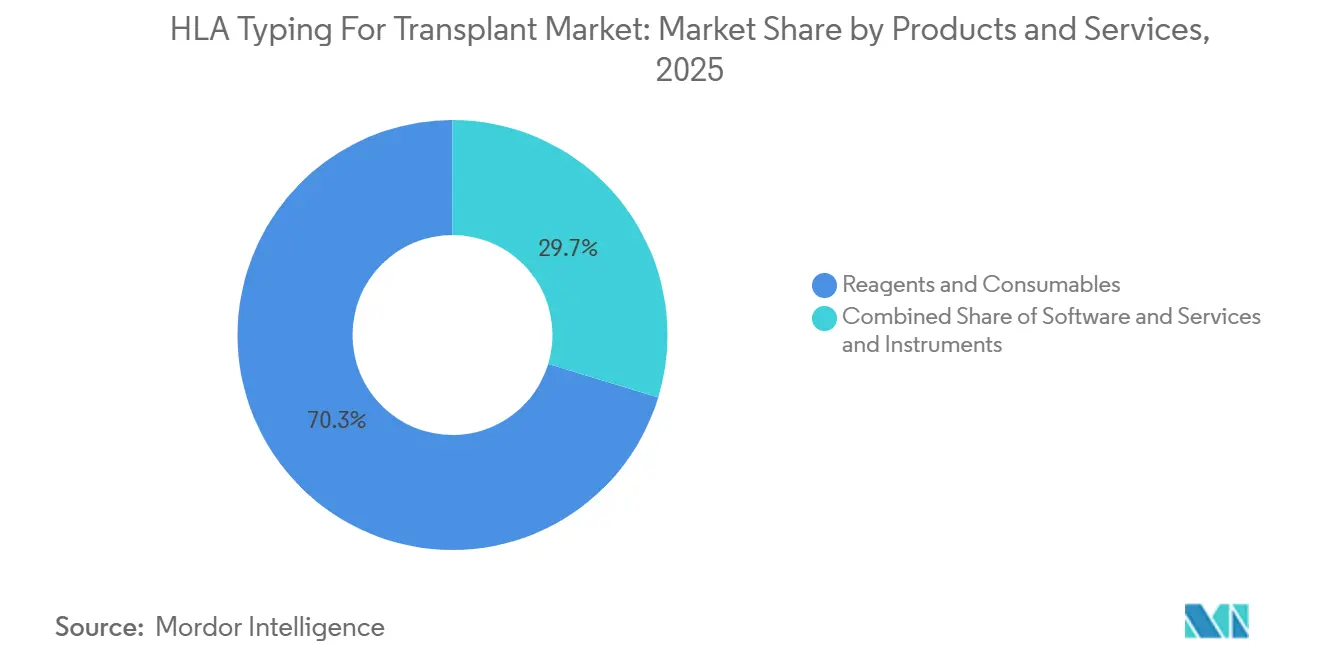

- By products and services, Reagents and Consumables held 70.31% revenue share in 2025, while Software and Services is projected to grow at 9.38% CAGR through 2031.

- By technology, Molecular Assay Technologies held 80.24% revenue share in 2025, while NGS-based HLA typing is projected to expand at 10.52% CAGR through 2031.

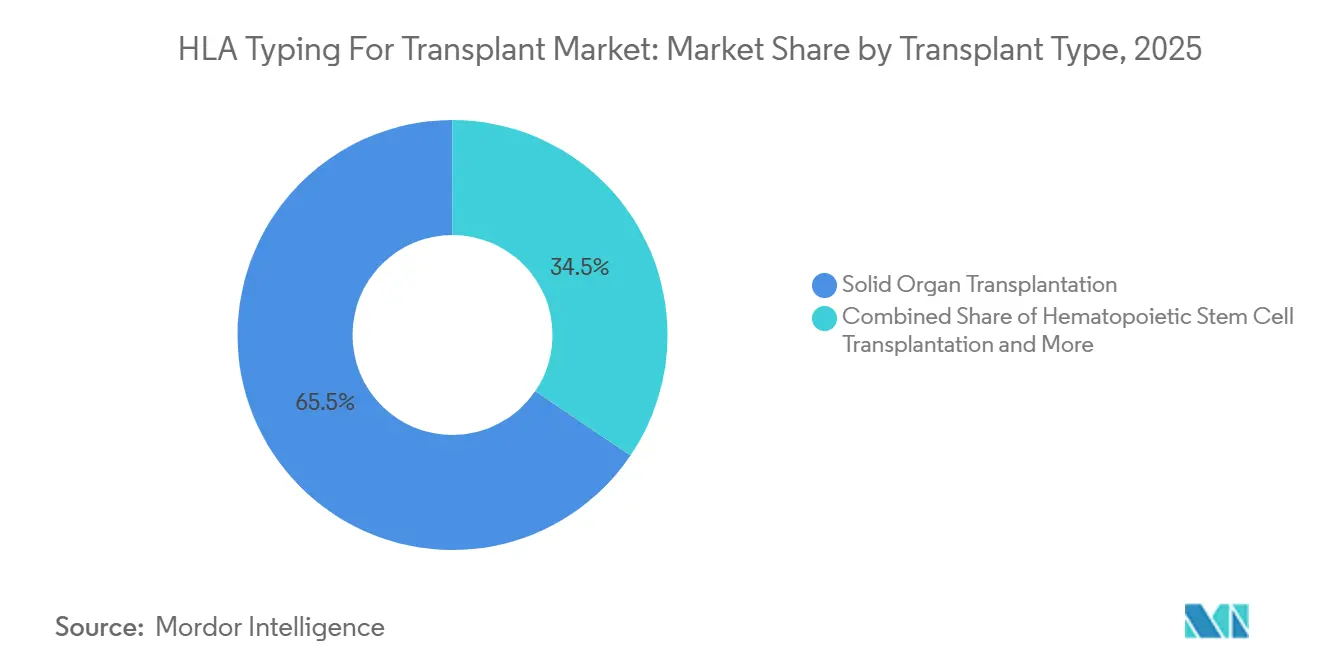

- By transplant type, Solid Organ Transplantation held 65.52% revenue share in 2025, while Hematopoietic Stem Cell Transplantation is forecast to grow at 9.25% CAGR through 2031.

- By end user, Hospitals and Transplant Centers held 42.34% revenue share in 2025, while Independent Reference Laboratories are projected to expand at 8.15% CAGR through 2031.

- By geography, North America held 45.22% of the HLA Typing for Transplant market share in 2025, while Asia-Pacific is projected to grow at 8.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HLA Typing For Transplant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Organ Transplant Volumes | +1.8% | Global | Short term (≤ 2 years) |

| Shift Toward Precise Donor-Recipient Matching | +1.5% | Global, led by North America and EU | Medium term (2-4 years) |

| Expansion of Molecular HLA Testing Adoption | +1.4% | Global, stronger uplift in APAC | Medium term (2-4 years) |

| Growth in Personalized Medicine and Immunogenomics | +0.9% | North America and EU | Long term (≥ 4 years) |

| Workflow Automation in High-Throughput Transplant Labs | +0.7% | North America and EU, with spillover to APAC | Medium term (2-4 years) |

| Rising Clinical Use of Post-Transplant Monitoring Panels | +0.6% | North America primarily, with EU expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Organ Transplant Volumes

The HLA Typing for Transplant market continues to gain volume support from the steady expansion of transplant procedures across major organ categories. Global solid organ transplants reached 173,727 procedures in 2024, which marked the highest level recorded by the Global Observatory on Donation and Transplantation. Kidney transplants reached 110,467, liver transplants reached 42,497, lung transplants reached 8,236, and heart transplants reached 10,287 in 2024, and each of these procedures required compatibility testing before transplantation. Donation after circulatory determination of death also expanded by 17% in 2024, which increased the share of time-sensitive deceased-donor typing events and pushed laboratories toward faster workflows[1]Global Observatory on Donation and Transplantation, “Organ Donation and Transplantation Worldwide: The Global Observatory on Donation and Transplantation 2024 Report,” Transplantation, pmc.ncbi.nlm.nih.gov. Japan’s revised 2025 heart transplantation guidelines further reinforced the clinical role of HLA matching for cardiac recipients, which added another high-value testing layer in a volume-constrained but quality-driven setting. As a result, the HLA Typing for Transplant market is seeing both higher unit demand and a stronger case for rapid, high-resolution assays.

Shift Toward Precise Donor-Recipient Matching

The HLA Typing for Transplant market is moving beyond basic compatibility and toward more precise donor-recipient evaluation. Transplant centers are using epitope-based matching and molecular mismatch scoring more often because these methods support the reduction of antibody-mediated rejection and sensitization events. Research published in 2026 showed that real-time molecular mismatch estimation using rSSO-defined HLA allele strings can be applied in deceased-donor allocation workflows without delaying organ placement. This change is pushing laboratories to supplement or replace PCR-SSP outputs with full-field NGS data, especially for retransplant candidates and sensitized patients. It is also widening the clinical scope of each pre-transplant workup because more data points are being used to judge transplant suitability. That shift is giving the HLA Typing for Transplant market a stronger pull toward premium assays and more advanced interpretation software.

Expansion of Molecular HLA Testing Adoption

The HLA Typing for Transplant market has reached a stage where routine molecular testing adoption is becoming harder to reverse. NGS is increasingly functioning as the preferred method for high-resolution typing, while Sanger sequencing is being retained more often as a backup or reference tool in resource-limited settings. A 2025 study on Chinese populations showed that optimized multiplex PCR-NGS protocols delivered phase-unambiguous genotyping across 6 HLA loci, which helped address allele ambiguity in highly polymorphic populations. The same structural shift is visible in unrelated donor registries, where high-resolution characterization across 6 or more loci keeps reference laboratories committed to scaled NGS capacity even when sample volumes vary. Research published in 2025 also showed that nanopore-based workflows could type up to 96 donor samples with 99.91% accuracy, which supported the case for larger batch operations. This is helping the HLA Typing for Transplant market move further away from residual PCR-SSO workflows in centralized laboratories.

Workflow Automation in High-Throughput Transplant Labs

The HLA Typing for Transplant market is also benefiting from workflow automation, especially in laboratories that process large sample volumes. Automation is reducing technician burden, shortening review cycles, and making high-resolution typing easier to scale across transplant networks. Faster software-assisted analysis is becoming an important part of this shift because reporting speed is increasingly tied to informatics performance and not only to wet-lab throughput. GenDx reported robust high-resolution HLA typing results across both Illumina short-read and Oxford Nanopore long-read platforms in 3 independent clinical laboratory validations, which points to a more operationally flexible workflow environment[2]GenDx, “Application Note, Robust HLA Typing with NGSgo-ProntoAmp,” GenDx, gendx.com. That operating flexibility matters because laboratories can expand menu depth and throughput without rebuilding every step of the process around a single platform. The HLA Typing for Transplant market therefore gains from automation not only through volume growth, but also through more durable demand for premium reagent and software contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of NGS-Based HLA Typing Workflows | -0.7% | Global, most acute in Middle East and Africa and South America | Long term (≥ 4 years) |

| Uneven Reimbursement and Procurement Cycles Across Regions | -0.5% | Europe, South America, and Middle East and Africa | Medium term (2-4 years) |

| Limited Donor Typing Infrastructure in Emerging Markets | -0.4% | Middle East and Africa, South America, and peripheral APAC | Long term (≥ 4 years) |

| Interoperability Gaps Between LIS, HLA Software, and Hospital Systems | -0.3% | Global, most acute in Europe and APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of NGS-Based HLA Typing Workflows

The HLA Typing for Transplant market still faces a meaningful cost barrier when laboratories move from older sequence-based methods to NGS. Comparative research published in 2024 showed that the transition brings more processing steps, more manual workload, and longer turnaround risk if workflows are not fully optimized. Laboratories also need to absorb maintenance expense, bioinformatics infrastructure, validation requirements, and long-term data retention obligations. In the United States, HLA typing for solid organ transplantation is treated under organ acquisition cost bundles in the Medicare MolDX framework rather than as a separately billable laboratory service, which limits direct recovery of NGS-specific costs. The cost gap remains more visible in smaller public-sector programs and lower-volume transplant centers than in large centralized reference networks. This restraint keeps the HLA Typing for Transplant market tilted toward laboratories that can spread platform and compliance costs across broader testing volumes.

Interoperability Gaps Between LIS, HLA Software, and Hospital Systems

The HLA Typing for Transplant market is also being slowed by persistent integration problems between laboratory information systems, HLA software, and hospital records. High-resolution typing creates a larger data burden, and the clinical value of that data drops when results cannot move quickly into allocation and treatment systems. HL7 International has advanced Histocompatibility and Immunogenetics reporting profiles within its genomics implementation guide, but laboratory-specific customization remains expensive and uneven across sites. Programs with bidirectional order-and-results integration can reduce transcription risk and allocation delays, while programs without that connectivity still depend on manual reconciliation. That difference is especially relevant in Europe and Asia-Pacific, where commercial software and national allocation systems do not always operate on the same data standards. This leaves the HLA Typing for Transplant market with a technical bottleneck that affects adoption speed even when clinical demand remains strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Products and Services: Reagents Anchor Revenue While Software Closes the Value Gap

Reagents and Consumables accounted for 70.31% share of the HLA Typing for Transplant market size in 2025, which kept this category in the leading revenue position. That share reflected the recurring purchasing pattern attached to molecular transplant diagnostics, where every workup requires fresh assay inputs across typing, crossmatch preparation, and antibody-related testing. The HLA Typing for Transplant market therefore gives reagents a more stable demand profile than instruments, because laboratories can postpone equipment upgrades but cannot avoid daily consumable use. The move toward broader and higher-resolution NGS assays is also lifting per-event reagent value because more loci are being typed and more complex compatibility questions are being addressed in routine workflows. Long-read platform launches are reinforcing that pattern because they expand the range of kits that can command premium pricing in the HLA Typing for Transplant market[3]Werfen, “Werfen Introduces NanoTYPE HLA-11 Plus CE, First CE-IVD HLA Typing Kit with Full-Gene Coverage for All 11 Classical HLA Genes,” Werfen, werfen.com.

Software and Services is projected to grow at 9.38% CAGR through 2031, which makes it the fastest-growing sub-segment in this part of the HLA Typing for Transplant industry. The traditional gap between assay value capture and informatics value capture is narrowing because NGS has made software central to the commercial proposition and not just to laboratory enablement. Analysis tools now help shape vendor choice, workflow speed, data interpretation, and platform stickiness. That shift is becoming more important as laboratories ask for integrated reporting and fewer handoffs between sequencing, allele calling, and final review. EuroBio Scientific’s April 2026 agreement to acquire CareDx’s transplant lab products division points to that broader convergence, because assay kits and related workflow assets are being consolidated under the GenDx commercial structure. The HLA Typing for Transplant market is therefore giving software and services a larger role in revenue mix as vendors compete to own more of the sample-to-report path.

By Technology: NGS Moves Ahead While Long-Read Validation Gains Pace

Molecular Assay Technologies held 80.24% revenue share in 2025, which kept this category at the center of the HLA Typing for Transplant market. That broad grouping includes PCR-based methods, NGS-based methods, and Sanger sequencing, but the internal growth balance is now shifting more clearly toward NGS. NGS-based HLA typing is projected to expand at 10.52% CAGR through 2031, which places the HLA Typing for Transplant market size for this sub-segment above the overall market growth rate. The main reason is clinical demand for high-resolution allele calls that can support better donor selection and reduce the need for retesting. PCR-based approaches still hold value in rapid or screening-oriented workflows, yet they are increasingly being used as complements to sequencing rather than as full substitutes for high-resolution analysis in the HLA Typing for Transplant market.

Long-read sequencing is also moving from research and validation settings into more visible clinical positioning. GenDx reported robust high-resolution results from blood and buccal swab samples across both Illumina and Oxford Nanopore platforms in 3 independent clinical laboratory validations, which supports a more platform-agnostic commercial environment. Werfen’s May 2026 launch of NanoTYPE HLA-11 Plus as a CE-IVD product marked an important regulatory step because it was presented as the first CE-IVD full-gene HLA typing kit across all 11 classical HLA genes. PacBio also remains relevant in this shift because its HiFi sequencing offering is being positioned around 99.9% accuracy and four-field allele resolution across classical HLA loci. Sanger-based typing and non-molecular methods still retain some presence in lower-infrastructure settings, but the HLA Typing for Transplant market is increasingly rewarding workflows that deliver full-gene resolution and stronger validation support.

By Transplant Type: Solid Organ Volume Leads While HSCT Raises Resolution Needs

Solid Organ Transplantation held 65.52% revenue share in 2025, which made it the largest transplant type in the HLA Typing for Transplant market. Kidney transplantation remains the main demand source within this category because 110,467 kidney transplants were performed worldwide in 2024, and those procedures require donor and recipient typing together with compatibility assessment. Liver and lung transplantation also added to testing demand in 2024, with 42,497 liver transplants and 8,236 lung transplants recorded globally. Donation after circulatory determination of death is adding another operational layer because a larger share of deceased-donor cases now requires rapid turnaround under tighter timing windows. This keeps solid organ transplantation as the volume anchor of the HLA Typing for Transplant market, even as technology needs become more demanding.

Hematopoietic Stem Cell Transplantation is projected to grow at 9.25% CAGR through 2031, which makes it the fastest-growing transplant type in the HLA Typing for Transplant market. This growth is linked to the higher resolution standards that HSCT workflows require, especially in unrelated donor settings. The 2024 EBMT activity report showed that allogeneic hematopoietic cell transplantation in Europe reached its highest annual level and that unrelated donor procedures represented 56% of the mix. That requirement for broader and deeper allele-level matching raises reagent value, strengthens the role of NGS, and keeps HSCT a premium segment for assay vendors. The HLA Typing for Transplant market is also seeing adjacent support from cellular therapy expansion because EBMT centers treated 6,082 first CAR-T patients in 2024. As these related therapy pathways expand, HSCT continues to raise the performance standard for the wider HLA Typing for Transplant industry.

By End User: Hospital Labs Hold Scale While Reference Networks Grow Faster

Hospitals and Transplant Centers held 42.34% revenue share in 2025, which made them the largest end-user group in the HLA Typing for Transplant market. Their lead reflected direct control over transplant decisions, patient workups, and the use of accredited histocompatibility laboratories inside major clinical centers. These accounts also carry higher value because they often buy across reagent, instrument, and software lines rather than through a single product category. The HLA Typing for Transplant market therefore favors suppliers that can support validated end-to-end workflows for transplant hospitals with complex testing requirements. Research laboratories and academic institutes remain smaller in direct revenue contribution, but they still influence technology adoption because they validate new long-read and high-resolution workflows before those tools spread more widely into routine use.

Independent Reference Laboratories are projected to grow at 8.15% CAGR through 2031, which makes them the fastest-growing end-user group in the HLA Typing for Transplant market. This rise reflects the structural decision by many mid-sized and emerging-market transplant programs to outsource high-resolution typing instead of building in-house NGS infrastructure. Public and regional centers can maintain core transplant capabilities while transferring advanced sequencing work to specialized networks. Brazil’s September 2025 transplant policy revision formalized HLA testing protocols across the national transplant system, which supports more organized demand for reference laboratory services. Similar outsourcing logic is becoming more visible in Europe and Asia-Pacific where ISO-accredited sequencing operations can be difficult to sustain at smaller sites. The HLA Typing for Transplant market is therefore pushing volume toward large certified reference providers even while hospitals remain the central requestors of testing.

Geography Analysis

North America held 45.22% share of the HLA Typing for Transplant market size in 2025, which kept it in the leading regional position. The United States remains the main contributor because its transplant ecosystem links organ procurement organizations, transplant centers, and ASHI-accredited histocompatibility laboratories in a structured way. The reimbursement framework also supports procurement continuity because HLA typing costs for solid organ transplantation are embedded within organ acquisition cost bundles under Medicare rules. That structure does not remove all pricing pressure, but it gives laboratories more visibility than in many other regions. Canada is adding to regional demand through continued investment in high-resolution typing capacity, while Mexico remains earlier in development with a smaller but growing private-sector transplant base.

Europe remained the second-largest regional block in the HLA Typing for Transplant market, with Germany, the United Kingdom, and France leading by testing sophistication and institutional depth. German university hospital laboratories such as Charité Berlin, University Medical Center Mainz, and University Hospital Leipzig operate accredited transplant immunology services that support high-resolution HLA typing in clinical practice. The regional product cycle is also becoming more active as vendors position their portfolios for the regulatory transition under IVDR, and Werfen’s CE-IVD long-read launch in May 2026 is a clear example of that push. Italy, Spain, and the wider Rest of Europe are increasingly important for outsourced high-resolution services because not every transplant center can sustain in-house NGS operations at accredited scale.

Asia-Pacific is projected to grow at 8.65% CAGR through 2031, which makes it the fastest-growing geography in the HLA Typing for Transplant market. China is a major part of that expansion because 15,387 combined kidney and liver transplants from deceased donors were recorded there in 2024. Japan also supports high per-procedure value through its transplant immunogenetics framework and its revised 2025 heart transplantation guidelines that include HLA matching considerations. India and South Korea are expanding transplant capacity quickly and are creating stronger demand for outsourced molecular typing, while South America and Middle East and Africa remain smaller regional pools with Brazil and GCC countries acting as the main points of structured investment.

Competitive Landscape

The HLA Typing for Transplant market shows moderate concentration at the platform tier, while assay supply and bioinformatics remain more dispersed. Thermo Fisher Scientific, QIAGEN, and Illumina continue to act as major workflow anchors because they combine instruments, consumables, and software capabilities across molecular testing. CareDx, Werfen, BAG Health Care, TBG Diagnostics, Immucor, and HistoGenetics compete across specific assay, service, and regional niches within the HLA Typing for Transplant market. This structure means competition is strongest where vendors can bind reagent sales to software and validated protocols. It also means smaller players can still win in focused areas where speed, compatibility, or regional distribution matter more than broad platform scale.

One major strategic move came in April 2026 when EuroBio Scientific signed a definitive agreement to acquire CareDx’s transplant lab product division, bringing NGS HLA typing kits and related workflow assets closer to the GenDx commercial infrastructure. Another important move came in April 2026 when CareDx introduced AlloSeq Nano, which expanded its HLA typing portfolio into long-read sequencing. Werfen then followed in May 2026 with the commercial availability of NanoTYPE HLA-11 Plus as a CE-IVD product, which strengthened the race to serve rapid and full-gene typing needs in Europe. These moves show that the HLA Typing for Transplant market is shifting from a method-based contest into a broader workflow and regulatory execution contest.

A second competitive theme is the growing value of software and data handling in the HLA Typing for Transplant market. Open and proprietary bioinformatics layers are both becoming more important as laboratories seek faster allele calling, cleaner integrations, and stronger validation evidence. PacBio’s positioning around high-accuracy immunogenomics sequencing is also giving academic and advanced clinical users another benchmark to compare against established short-read platforms. Vendors that can combine assay breadth, clinical validation, software interoperability, and regulatory readiness are likely to defend pricing better than those competing only on kit performance. The HLA Typing for Transplant market therefore remains competitive, but the advantage is moving toward suppliers that can control more of the workflow stack without adding operational friction.

HLA Typing For Transplant Industry Leaders

Thermo Fisher Scientific Inc.

QIAGEN N.V.

Illumina, Inc.

Bio-Rad Laboratories, Inc.

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Werfen launched NanoTYPE HLA-11 Plus, the first CE-IVD-certified HLA typing kit with full-gene coverage (5′UTR to 3′UTR) for all 11 classical HLA genes. It integrates with Oxford Nanopore platforms like MinION, GridION, and PromethION, positioning Werfen ahead in deceased-donor rapid typing before the EU IVDR deadline in December 2027.

- March 2025: Thermo Fisher Scientific introduced the One Lambda HybriType HLA Plus Typing Flex kit, an NGS hybrid-capture assay with ≥99.8% concordance. It processes whole blood or buccal swabs in under 5.5 hours, with less than 2.5 hours of hands-on time, supporting Class I (4-field) and Class II (3-field) analysis via TypeStream Visual NGS software.

Global HLA Typing For Transplant Market Report Scope

As per the scope of the report, HLA typing for transplant refers to the process of identifying an individual's human leukocyte antigen (HLA) profile to assess compatibility between donor and recipient. Accurate HLA typing helps predict the likelihood of a successful transplant and reduces the risk of rejection by matching similar HLA types between donor and recipient.

The segmentation of the HLA typing for transplant market is categorized by products and services, technology, transplant type, end user, and geography. By products and services, the market is divided into reagents and consumables, instruments, and software and services. By technology, it includes molecular assay technologies, PCR-based HLA typing, next-generation sequencing-based HLA typing, Sanger sequencing-based HLA typing, and other technologies. By transplant type, the segmentation covers solid organ transplantation, kidney transplantation, liver transplantation, heart transplantation, lung transplantation, and hematopoietic stem cell transplantation. By end user, the market is segmented into independent reference laboratories, hospitals and transplant centers, and research laboratories and academic institutes. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Reagents and Consumables |

| Instruments |

| Software and Services |

| Molecular Assay Technologies |

| PCR Based HLA Typing |

| Next Generation Sequencing Based HLA Typing |

| Sanger Sequencing Based HLA Typing |

| Other Technologies |

| Solid Organ Transplantation |

| Kidney Transplantation |

| Liver Transplantation |

| Heart Transplantation |

| Lung Transplantation |

| Hematopoietic Stem Cell Transplantation |

| Independent Reference Laboratories |

| Hospitals and Transplant Centers |

| Research Laboratories and Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Products and Services | Reagents and Consumables | |

| Instruments | ||

| Software and Services | ||

| By Technology | Molecular Assay Technologies | |

| PCR Based HLA Typing | ||

| Next Generation Sequencing Based HLA Typing | ||

| Sanger Sequencing Based HLA Typing | ||

| Other Technologies | ||

| By Transplant Type | Solid Organ Transplantation | |

| Kidney Transplantation | ||

| Liver Transplantation | ||

| Heart Transplantation | ||

| Lung Transplantation | ||

| Hematopoietic Stem Cell Transplantation | ||

| By End User | Independent Reference Laboratories | |

| Hospitals and Transplant Centers | ||

| Research Laboratories and Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current and forecast value of HLA typing for transplant?

The HLA Typing for Transplant market size stands at USD 0.72 billion in 2025, rises to USD 0.77 billion in 2026, and is forecast to reach USD 1.09 billion by 2031 at a 7.22% CAGR.

What is driving demand for transplant HLA typing solutions?

Demand is being supported by record transplant activity, with 173,727 global solid organ transplants in 2024, stronger use of high-resolution matching, and broader NGS adoption in transplant labs.

Which product group brings in the most revenue?

Reagents and Consumables lead with 70.31% of revenue in 2025 because transplant workflows require recurring assay purchases for each workup.

Which technology is growing the fastest in transplant compatibility testing?

NGS-based HLA typing is the fastest-growing technology sub-segment, with a projected 10.52% CAGR through 2031 as centers move toward higher-resolution allele calls.

Which transplant application is expanding the fastest?

Hematopoietic Stem Cell Transplantation is the fastest-growing transplant type at 9.25% CAGR through 2031 because it requires stricter allele-level donor matching.

Which region leads and which region is growing the fastest?

North America leads with 45.22% share in 2025, while Asia-Pacific is growing the fastest with an 8.65% CAGR through 2031 as transplant capacity and molecular diagnostics use expand.

Page last updated on: