Blood Group Typing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

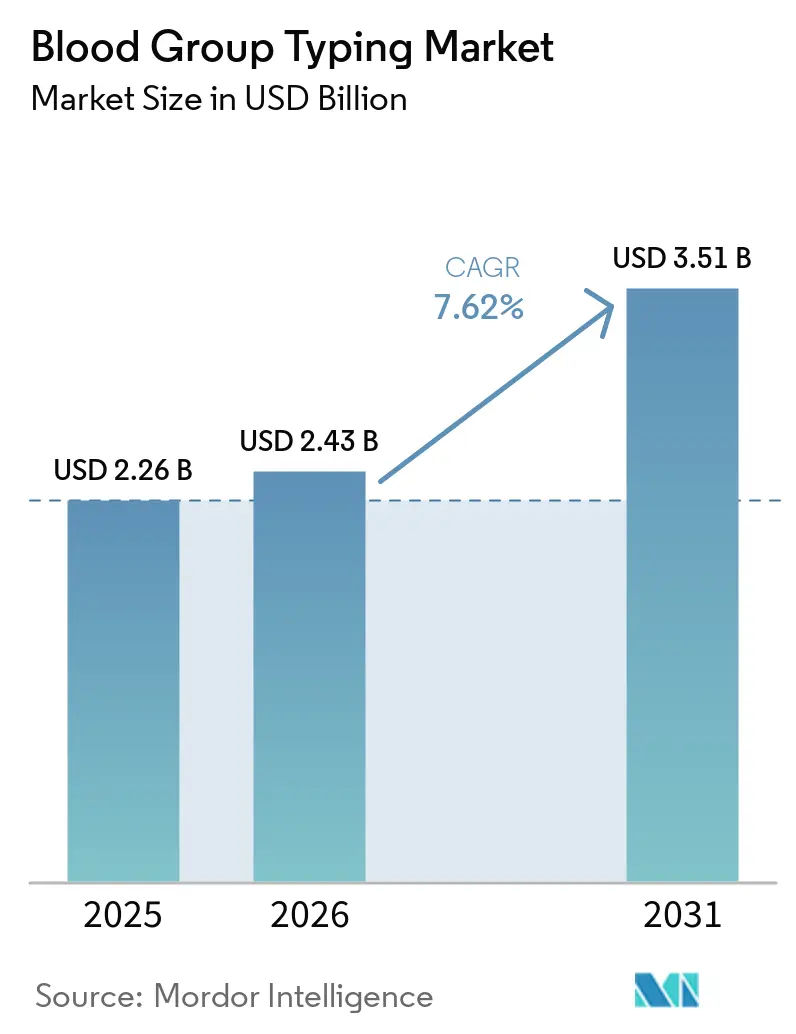

| Market Size (2026) | USD 2.43 Billion |

| Market Size (2031) | USD 3.51 Billion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

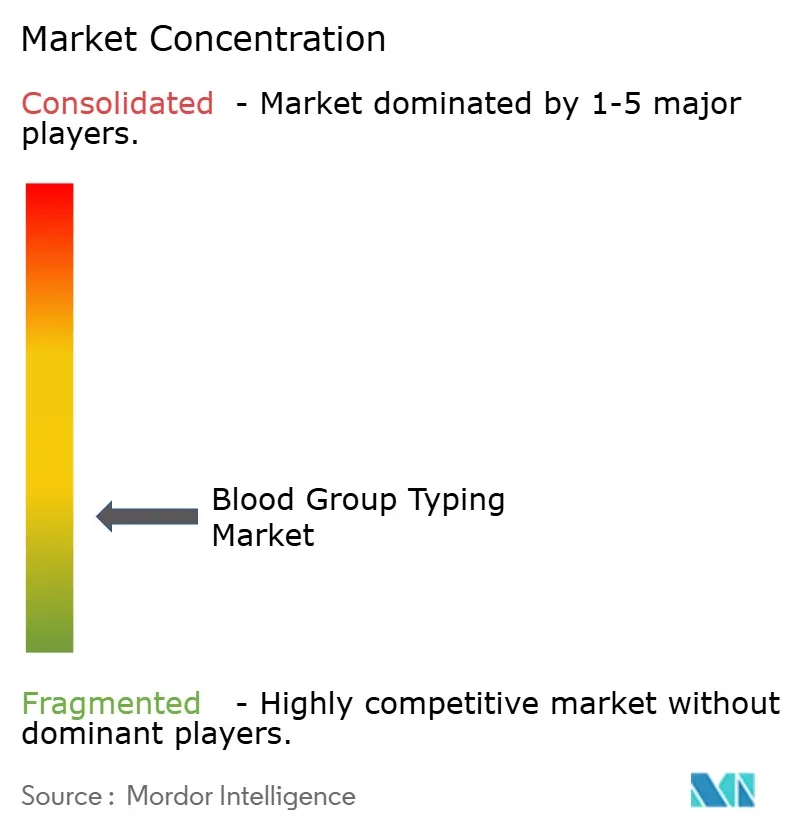

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Group Typing Market Analysis by Mordor Intelligence

Blood typing market size in 2026 is estimated at USD 2.43 billion, growing from 2025 value of USD 2.26 billion with 2031 projections showing USD 3.51 billion, growing at 7.62% CAGR over 2026-2031. Rising surgical volumes, higher life expectancy, and the clinical shift toward precision transfusion protocols underpin this steady expansion. Rapid technology adoption—from high-throughput serology analyzers to next-generation sequencing (NGS) platforms—strengthens test accuracy and throughput, while enabling laboratories to resolve complex antibody work-ups within hours instead of days. Demand also gains from government-funded blood donation drives, especially in Asia-Pacific, that channel large numbers of collected units into standardized testing workflows[1]World Health Organization, “Guidance on Implementing Patient Blood Management to Improve Global Blood Health Status,” who.int. Automation is closing the gap created by laboratory staffing shortages, with instrument vendors embedding robotics, advanced optics, and artificial intelligence to deliver faster results and lower per-test costs[2]U.S. Food and Drug Administration, “2025 Biological Device Application Approvals,” fda.gov. Hospital consolidation in North America and Europe further favors integrated platforms that combine instruments, reagents, middleware, and outsourced reference services under one purchasing contract.

Key Report Takeaways

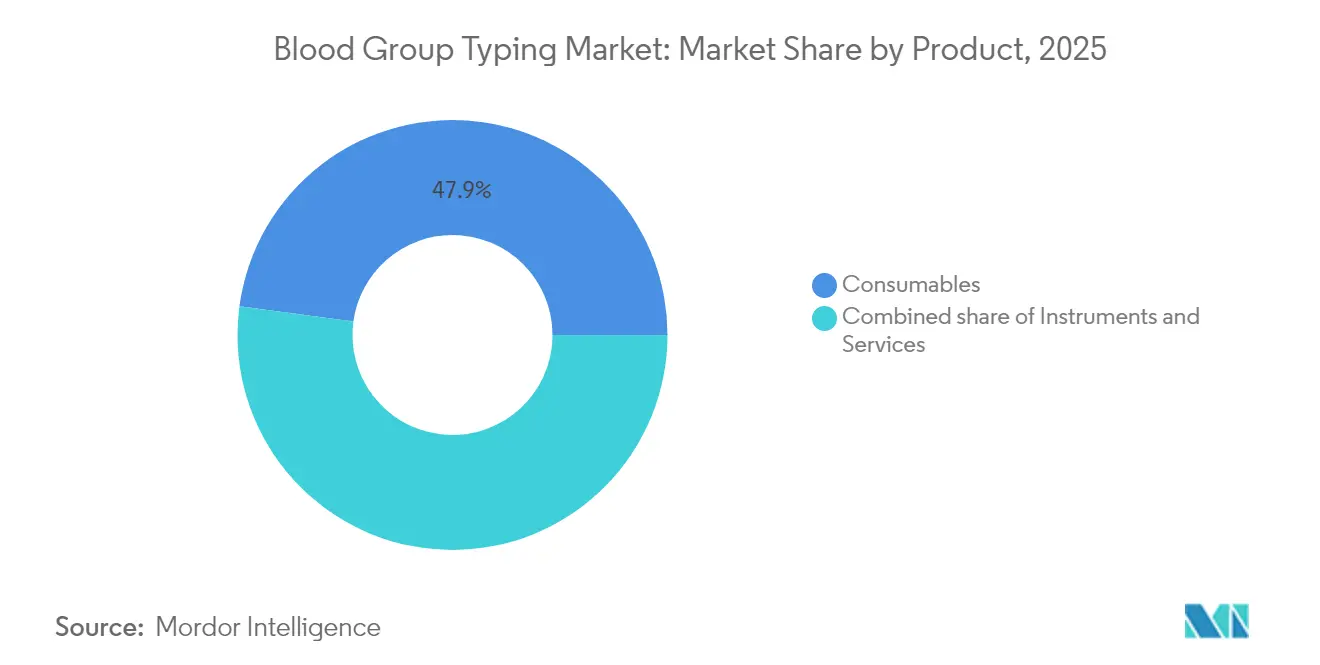

- By product, consumables led with 47.86% of blood typing market share in 2025; services are projected to rise at a 10.3% CAGR through 2031.

- By technique, PCR-based and microarray methods accounted for 36.78% revenue share in 2025, while NGS is poised for the fastest 12.21% CAGR to 2031.

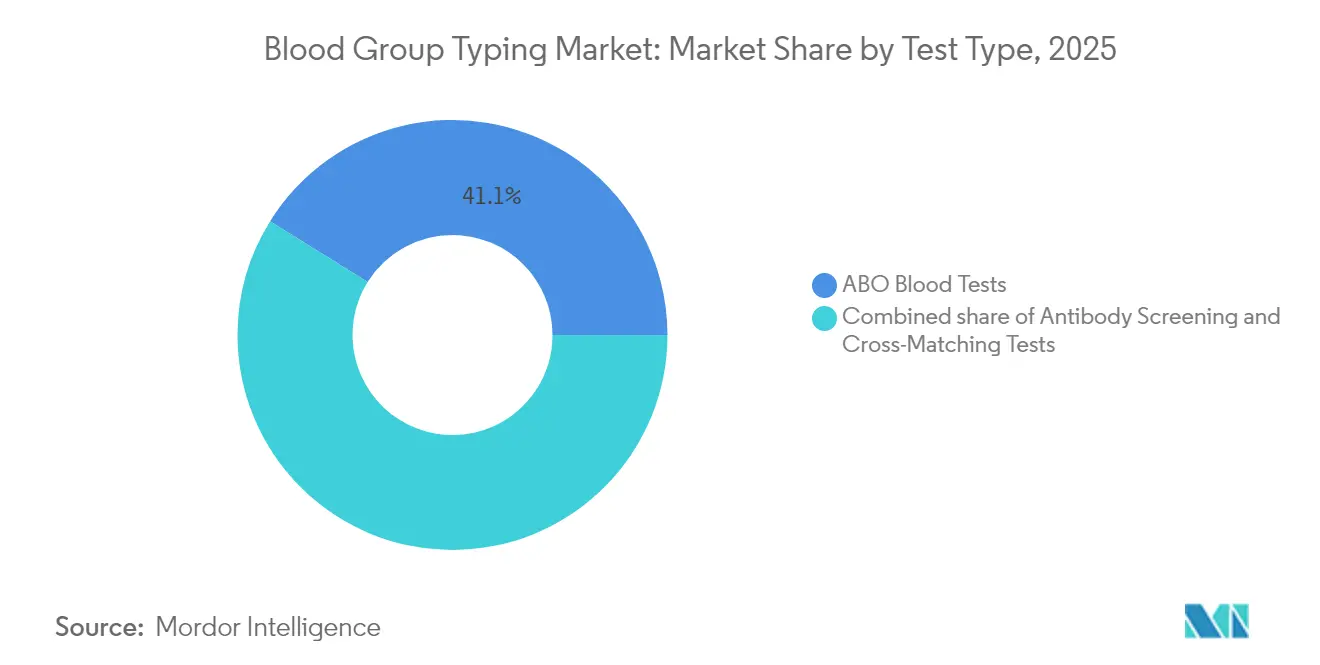

- By test type, ABO testing contributed 41.12% revenue share in 2025, whereas antigen typing is expanding at an 11.38% CAGR through 2031.

- By region, North America held 33.12% of blood typing market share in 2025; Asia-Pacific is forecast to post the strongest 8.68% CAGR to 2031.

- By end user, hospitals represented 52.10% of the blood typing market in 2025; diagnostic laboratories and other settings are slated for a 13.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blood Group Typing Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in global blood transfusion procedures | +1.8% | Global; highest in APAC and MEA | Medium term (2-4 years) |

| Rising prevalence of chronic and hematological disorders | +1.5% | Global; concentrated in aging North America and Europe | Long term (≥4 years) |

| Expansion of national blood donation programs | +1.2% | APAC core; spill-over to MEA and South America | Medium term (2-4 years) |

| Technological advancements in automated blood typing systems | +1.4% | North America and EU lead; rapid APAC adoption | Short term (≤2 years) |

| Increasing adoption of molecular diagnostics in transfusion medicine | +1.6% | Global; early gains in developed markets | Medium term (2-4 years) |

| Government initiatives for maternal and neonatal health | +0.9% | APAC, MEA, and South America focus | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growth in Global Blood Transfusion Procedures

Worldwide transfusion volumes continue to climb as complex cardiovascular, trauma, and oncological interventions become commonplace. Each transfusion episode triggers multiple compatibility checks, so even marginal increases in procedure counts magnify reagent and instrument demand. Emergency medicine now requires point-of-care analyzers that can process ABO-Rh typing in under five minutes, a capability that high-volume hospitals in the United States and Japan already view as essential[3]Pan American Health Organization, “Blood,” paho.org. Automated workflows are therefore replacing manual tube testing in both tertiary centers and regional trauma networks.

Rising Prevalence of Chronic and Hematological Disorders

Long-term transfusion support for thalassemia, sickle cell disease, and hematologic cancers is reshaping routine practice from basic ABO-Rh matching to extended antigen phenotyping. Molecular assays that read multiple blood group loci in a single run limit alloimmunization, a risk especially acute in multi-transfused pediatric patients. Oncology protocols are also adopting prophylactic typing to offset transfusion reactions during chemotherapy cycles.

Expansion of National Blood Donation Programs

Pursuit of 100% voluntary donation—as advocated by the World Health Organization—has prompted new collection centers across India, Indonesia, and Nigeria to procure fully automated analyzers, refrigerated centrifuges, and LIS-connected barcode readers. Emerging economies often purchase turnkey reagent-instrument bundles, benefiting vendors that offer scalable platforms able to process hundreds of samples per shift while maintaining strict quality metrics.

Technological Advancements in Automated Blood Typing Systems

Robotics, machine vision, and middleware now combine to produce closed-tube, walk-away analyzers that curtail transcription errors and address a 9.25% vacancy rate for laboratory technologists in the United States. Real-time result validation with AI algorithms is beginning to flag aberrant reaction patterns, freeing technologists for complex problem-solving rather than routine pipetting.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited healthcare infrastructure in low-income regions | −1.1% | Sub-Saharan Africa; parts of South Asia and South America | Long term (≥4 years) |

| Shortage of skilled laboratory personnel | −0.8% | Global; most acute in North America and Europe | Medium term (2-4 years) |

| High cost of advanced typing technologies | −0.9% | Global; heightened in resource-constrained markets | Short to medium term (≤4 years) |

| Stringent regulatory and compliance requirements | −0.7% | North America and Europe primarily; spreading to other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Healthcare Infrastructure in Low-Income Regions

Inconsistent electricity, inadequate cold chain capacity, and scarce maintenance expertise hamper reliable blood typing in a sizable share of African and rural South Asian facilities. Cap-ex hurdles slow adoption of NGS and even mid-tier automated serology systems, compelling many centers to rely on manual slide or rapid card tests with lower sensitivity.

Shortage of Skilled Laboratory Personnel

Accelerated retirements coupled with weak enrollment in medical laboratory programs restrict the number of qualified immunohematology technologists. Smaller hospitals struggle to staff 24-hour transfusion services, limiting in-house ability to manage complex antibody work-ups. Facilities frequently outsource advanced molecular typing to reference laboratories, stoking demand for send-out services but delaying real-time decision making in some care settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product – Services Outpace a Consumables-Dominated Base

Consumables accounted for 47.86% of blood typing market share in 2025, reflecting the high frequency of reagents used for routine gel card and microplate testing. The services category, however, is projected to post a 10.3% CAGR to 2031 as laboratories increasingly outsource NGS-based antigen panels and rare antibody identification. That outsourcing trend enlarges the blood typing market size for specialized reference providers, many of which package logistics, sequencing, and interpretive reports under subscription agreements. Instruments maintain mid-single-digit growth, driven by upgrades to AI-enabled analyzers that optimize reagent use and interface directly with hospital LIS platforms.

Laboratory managers cite the capital-intensive nature of NGS as the main reason for send-out adoption. Meanwhile, reagent suppliers face price pressure as automated analyzers become more frugal with micro-volume reaction pads. Despite that, rising total test volumes secure stable revenue streams for gel cards, buffers, and control sera. Instrument manufacturers differentiate through modular designs that expand from 96 to 384 well formats, aligning capacity with fluctuating seasonal demand.

By Technique – NGS Redefines the Molecular Frontier

PCR and microarray platforms delivered 36.78% of segment revenue in 2025, yet NGS is forecast to climb at a 12.21% CAGR, reflecting unrivaled depth of antigen coverage. The blood typing market size for NGS reagents is still below traditional serology reagents, but rapid uptake in reference centers is narrowing the gap. Multi-locus sequencing resolves Rh, Kell, Kidd, and Duffy variants in a single assay, which supports precision-matching policies for chronically transfused patients.

While serology remains the frontline workhorse for same-day ABO-Rh testing, clinicians now consider NGS confirmation indispensable for complex phenotyping. Microfluidics and lateral-flow cassettes keep a foothold in resource-constrained or emergency settings due to minimal training requirements. Hybrid workflows are therefore common: a slide or column agglutination test confirms immediate compatibility, with NGS data arriving a day later to refine extended match decisions.

By Test Type – Antigen Typing Accelerates Beyond ABO Dominance

ABO grouping generated 41.12% of 2025 revenues, a testament to its universal clinical necessity. Antigen typing nonetheless is projected for an 11.38% CAGR through 2031, outpacing the broader blood typing market. This trajectory stems from wider use of prophylactic phenotype matching in hemoglobinopathy care, where alloimmunization risk climbs after multiple transfusions. Cross-matching and antibody screening continue to anchor peri-operative protocols, yet hospitals now layer molecular antigen panels on top to ensure long-term compatibility.

The blood typing market size tied to antigen typing also benefits from prenatal testing, where fetal RHD genotyping guides anti-D immunoglobulin use. Manufacturers responding to this shift emphasize multiplex assay kits that cover 30+ clinically significant antigens without increasing sample input volumes. LIS-driven reflex rules then move positive screens straight into extended work-ups, preserving turnaround time.

By End User – Diversified Demand Beyond Hospital Labs

Hospitals held 52.10% of overall revenue in 2025, yet diagnostic laboratories, blood collection facilities, and academic centers are projected for the fastest 13.32% CAGR. Outsourcing by community hospitals funnels a growing number of samples into national reference labs, where high-throughput analyzers leverage economies of scale. Research institutions pursue grant-funded projects on blood group genomics, boosting demand for NGS library prep kits and bespoke bioinformatics pipelines.

Blood banks are deploying automated grouping instruments to accelerate donor unit release, integrating barcoded reagent packs and auto-validation middleware that synch with donor management software. This workflow modernization makes it possible to complete collection-to-issue cycles in under 24 hours, a target set by many national transfusion services.

Geography Analysis

North America controlled 33.12% of revenue in 2025 thanks to stringent regulatory oversight, high healthcare spending, and a mature hospital network that prioritizes fully automated immunohematology. FDA clearances in 2025 for integrated serology-molecular workstations illustrate the region’s appetite for technology that merges gel card processing with reflex NGS and AI-based interpretation. A tight labor market further accelerates instrument replacement cycles, as labs gravitate to walk-away analyzers that need fewer hands-on minutes.

Asia-Pacific is forecast to post the highest 8.68% CAGR through 2031. National blood donation expansion across India, Indonesia, and Vietnam is pouring large sample volumes into both public and private testing channels, while China is fast-tracking automated reagent rental programs in provincial centers. Japan holds the highest per-capita test penetration, driven by rapid uptake of molecular typing for oncology and transplantation. Local manufacturers in South Korea and China are entering the mid-range instrument tier, challenging Western incumbents on price and after-sales service.

Europe maintains steady mid-single-digit growth. Harmonized EU medical device regulations impose rigorous performance verification, yet reimbursement frameworks in Germany, France, and the Nordics support adoption of high-spec analyzers that reduce sample volume and waste. Meanwhile, the Middle East and Africa display uneven progress. Gulf Cooperation Council countries import top-end instruments for tertiary hospitals, whereas many sub-Saharan facilities rely on manual slide testing due to power instability. South America gains momentum as Brazil’s hemovigilance reforms channel capital into centralized testing hubs that serve multiple states.

Competitive Landscape

The blood typing market is fragmented. No single vendor controls more than one-fifth of global revenue, leaving room for both multinationals and niche specialists. Bio-Rad, Grifols, and Ortho Clinical Diagnostics anchor the top tier with broad serology menus, integrated middleware, and established reagent rental models. Grifols recently rolled out a compact, fully automated bench-top analyzer to capture mid-volume hospital segments, while Bio-Rad leveraged its 2025 purchase of Stilla Technologies to fold digital PCR into its transfusion portfolio.

Werfen’s acquisition of Omixon adds transplant-grade NGS capability, positioning the company for coverage across routine serology, molecular genotyping, and extended HLA work-ups. Abbott and Siemens Healthineers increasingly package coagulation and hematology assays alongside blood typing to offer end-to-end peri-operative solutions, a tactic that resonates with IDN purchasing groups in the United States.

Start-ups specializing in AI-based reaction grading and cloud-native LIS extensions are becoming attractive partners for instrument makers seeking to enhance post-analytic workflows. Regional firms in China and India exploit lower cost structures to penetrate public tenders, often bundling service contracts and reagent supplies under five-year agreements. Competitive intensity therefore centers on automation, molecular reach, and bundled service models rather than price alone.

Blood Group Typing Industry Leaders

Bio-Rad Laboratories Inc.

Grifols S.A.

Ortho Clinical Diagnostics

Danaher Corp. (Beckman Coulter)

Immucor Inc. (Werfen)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Bio-Rad Laboratories completed the acquisition of Stilla Technologies to add digital PCR capabilities supporting precision transfusion applications.

- May 2025: Siemens Healthineers launched the INNOVANCE Antithrombin Assay, an FDA-cleared companion diagnostic that complements blood typing services within integrated coagulation management.

- April 2025: Abbott Laboratories reported USD 2.054 billion diagnostics revenue in Q1 2025 and introduced mixed-reality donor engagement tools to improve repeat donation rates.

- March 2025: Werfen unified Immucor and other subsidiaries under a single brand to streamline its transfusion medicine portfolio across more than 30 countries.

- February 2025: Terumo Blood and Cell Technologies formed the Global Therapy Innovations business unit to expand therapeutic apheresis solutions, including for sickle cell disease.

- January 2025: Haemonetics sold its whole blood assets to GVS for USD 67.8 million to concentrate on core apheresis competencies, while GVS broadens blood processing reach.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the blood group typing market as global revenue generated from instruments, consumables, and related services that determine ABO, Rh, extended antigen, antibody, cross-match, and HLA groups in clinical, donor, and research settings. We count new unit sales plus pay-per-test reagent income collected by hospitals, blood banks, and reference laboratories.

Scope Exclusion: therapeutic apheresis devices and routine hematology analyzers are outside our scope.

Segmentation Overview

- By Product

- Instruments

- Automated Systems

- Semi-Automated Systems

- Manual Readers & Centrifuges

- Consumables

- Reagent Red Cells & Antisera

- Gel Cards & Microplates

- Molecular Assay Kits & Panels

- Services

- Instruments

- By Technique

- Serology Assay-Based

- PCR-Based & Microarray

- Massively Parallel / NGS

- Lateral-Flow & Microfluidic

- By Test Type

- ABO Blood Tests

- Antibody Screening

- Cross-Matching Tests

- HLA Typing

- Antigen Typing (Kidd, Duffy, Etc.)

- By End User

- Hospitals

- Blood Banks

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with hospital lab managers, regional blood-bank supervisors, reagent distributors, and service engineers across North America, Europe, Asia-Pacific, and Latin America. These conversations clarified price-per-test, lot utilization, and upcoming capital budgets, letting us validate and fine-tune every secondary datapoint.

Desk Research

We began with public datasets that map the testing pool, such as WHO voluntary donation volumes, the Global Observatory on Donation & Transfusion, and OECD surgical procedure counts. Regulatory filings in the US FDA 510(k) database, peer-reviewed adoption studies, and releases from AABB and ISBT anchored technology penetration. Company 10-Ks, investor decks, and our paid feeds from D&B Hoovers and Dow Jones Factiva informed average selling prices and revenue splits. Additional trade articles and customs data filled remaining gaps; the sources noted here are illustrative, not exhaustive.

Market-Sizing & Forecasting

We built a top-down and bottom-up hybrid. Country-level blood collection and surgical volumes were multiplied by verified tests-per-procedure ratios, then by confirmed average prices. Supplier shipment samples and analyzer installed-base roll-ups cross-checked totals. Key variables include donation growth, trauma surgery incidence, prenatal screening penetration, organ transplant counts, and automated system renewal cycles. A multivariate regression that incorporates GDP per capita and health spend projects five-year demand, while scenario analysis brackets regulatory shocks. Where unit data were patchy, region-specific reagent-to-instrument revenue ratios from interviews closed gaps.

Data Validation & Update Cycle

Outputs pass variance flags against import data and prior editions before senior analyst sign-off. Reports refresh annually, with interim updates for material events, and a final sweep ensures clients receive the latest view.

Why Mordor Blood Group Typing Baseline Stays Consistently Reliable

Published estimates often differ because firms apply dissimilar product mixes, price erosion curves, and refresh cadences. Our disciplined scope selection and rolling currency conversions limit such drift. Major gap drivers include whether molecular genotyping reagents are bundled with serology kits, if donor screening tests are blended with patient diagnostics, and the aggressiveness of price decay assumptions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.26 B | Mordor Intelligence | - |

| USD 2.30 B | Global Consultancy A | Bundles donor-screening reagents with patient diagnostics |

| USD 2.31 B | Industry Journal B | Uses static 2019 prices and fixed exchange rates |

By grounding every assumption in current usage metrics and verified prices, Mordor Intelligence delivers a balanced, transparent baseline that decision makers can trust.

Key Questions Answered in the Report

What is the expected growth rate of the blood typing market between 2026 and 2031?

The market is forecast to expand at a 7.62% CAGR, moving from USD 2.43 billion in 2026 to USD 3.51 billion by 2031.

Which product category is growing fastest?

Services, including outsourced molecular genotyping and reference testing, are projected for the highest 10.3% CAGR through 2031.

Why is Asia-Pacific the fastest-growing region?

Healthcare modernization, national donor programs, and rising surgical volumes drive an 8.68% CAGR in Asia-Pacific, the highest among all regions.

How are staffing shortages influencing technology adoption?

Laboratory vacancies encourage adoption of fully automated analyzers and AI-enabled result validation to maintain throughput with fewer technologists.

What role does NGS play in blood typing?

NGS provides comprehensive antigen profiles, enabling precision transfusion for chronically transfused patients and supporting a 12.21% CAGR within the technique segment.

Page last updated on: