HLA Typing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

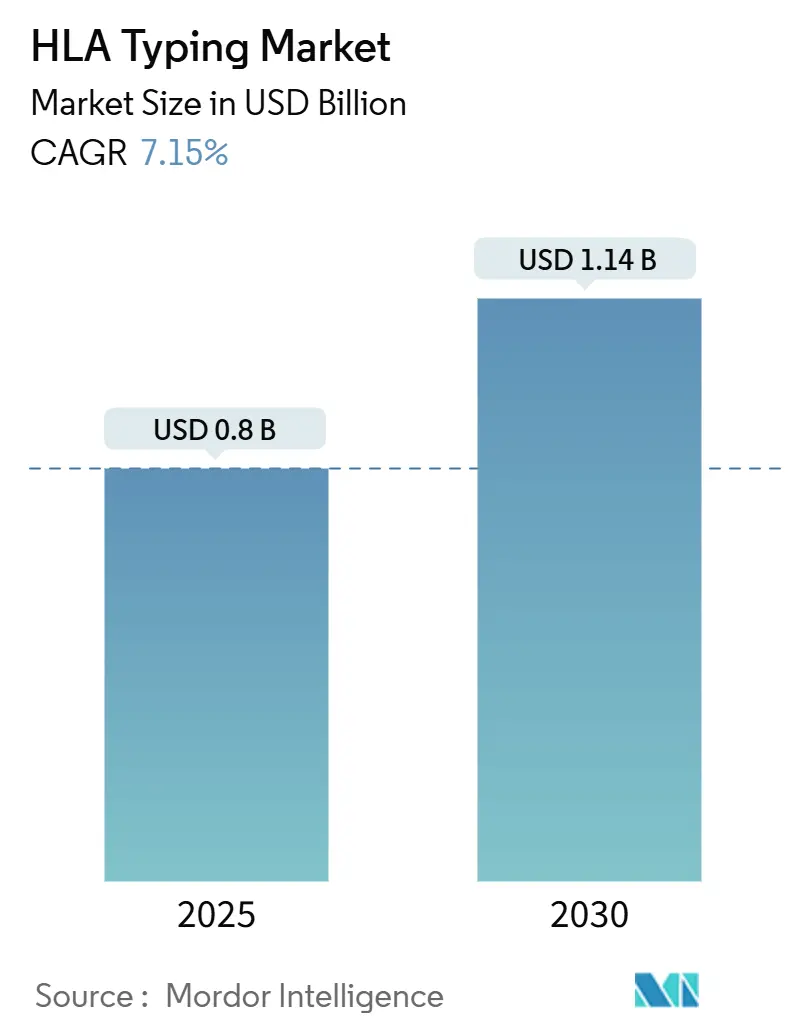

| Market Size (2025) | USD 0.8 Billion |

| Market Size (2030) | USD 1.14 Billion |

| Growth Rate (2025 - 2030) | 7.15% CAGR |

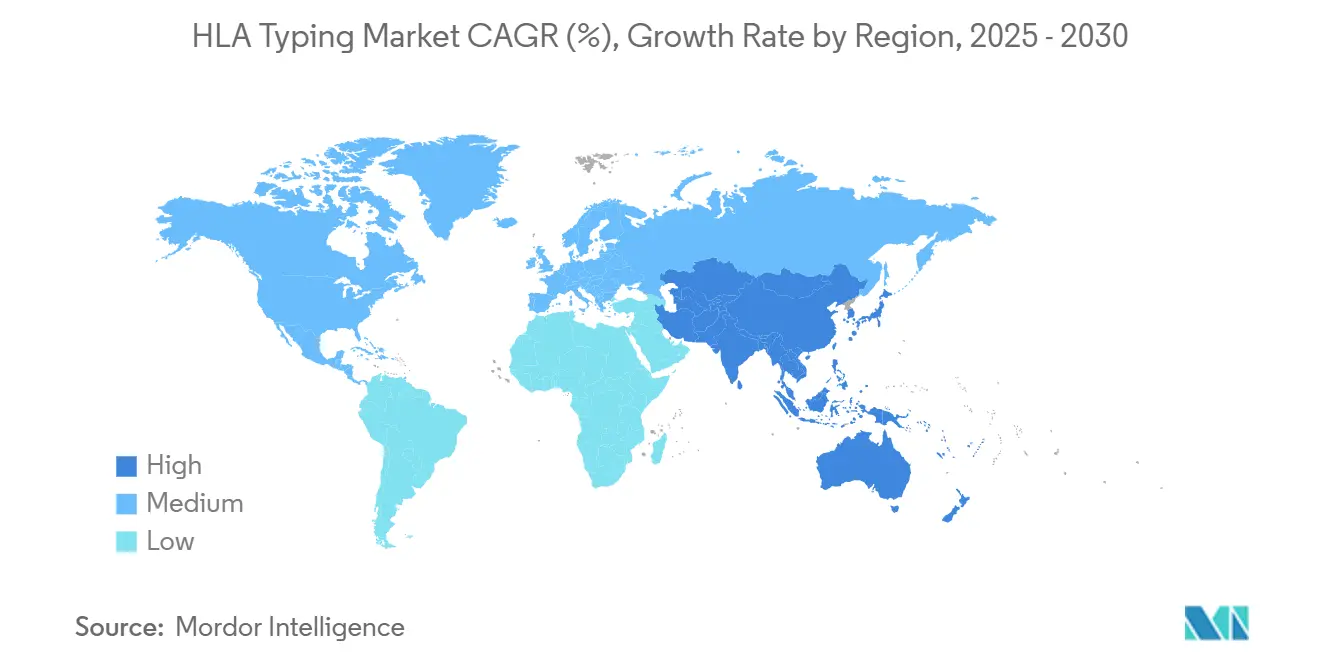

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HLA Typing Market Analysis by Mordor Intelligence

The HLA typing market size stands at USD 0.80 billion in 2025 and is projected to reach USD 1.14 billion by 2030, reflecting a 7.15% CAGR. Record organ-transplant volumes, the mainstreaming of precision medicine, and a rapid move from serological kits to next-generation sequencing platforms underpin this trajectory. High-throughput molecular assays reduce turnaround times and improve match accuracy, encouraging their uptake among transplant programs. Venture investment and acquisitions signal rising confidence, while policy shifts such as the Medicare IOTA Model reward precise HLA matching through performance-based hospital payments[1]Federal Register, “Kidney Transplant Payment Model (IOTA),” federalregister.gov. At the same time, donor-registry interoperability and cloud bioinformatics expand global testing reach, especially for ethnically diverse populations that struggle to find matches. Cost pressures remain a constraint in low-resource settings, yet tiered product portfolios and pooled-service laboratories are lowering access barriers.

Key Report Takeaways

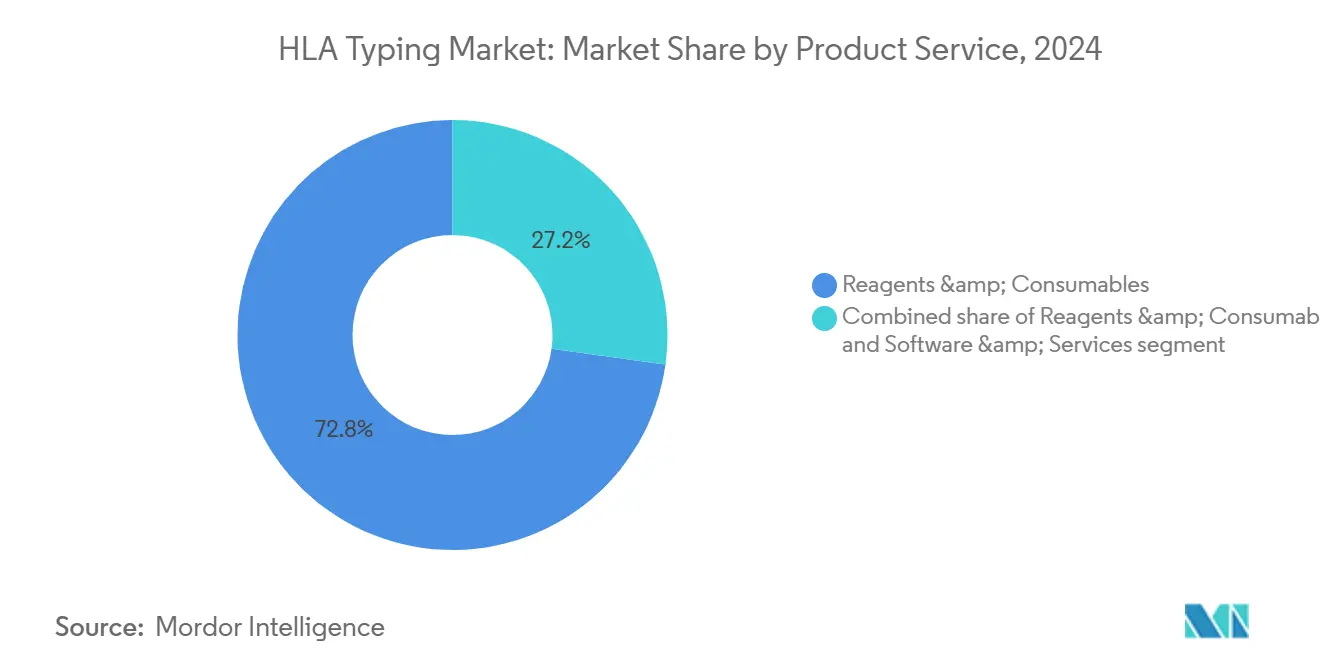

- By product, reagents and consumables led with 72.89% revenue share in 2024; software and services are forecast to expand at a 9.56% CAGR through 2030.

- By technology, molecular assays held 58.45% of revenue in 2024, while non-molecular serological methods are advancing at an 8.77% CAGR.

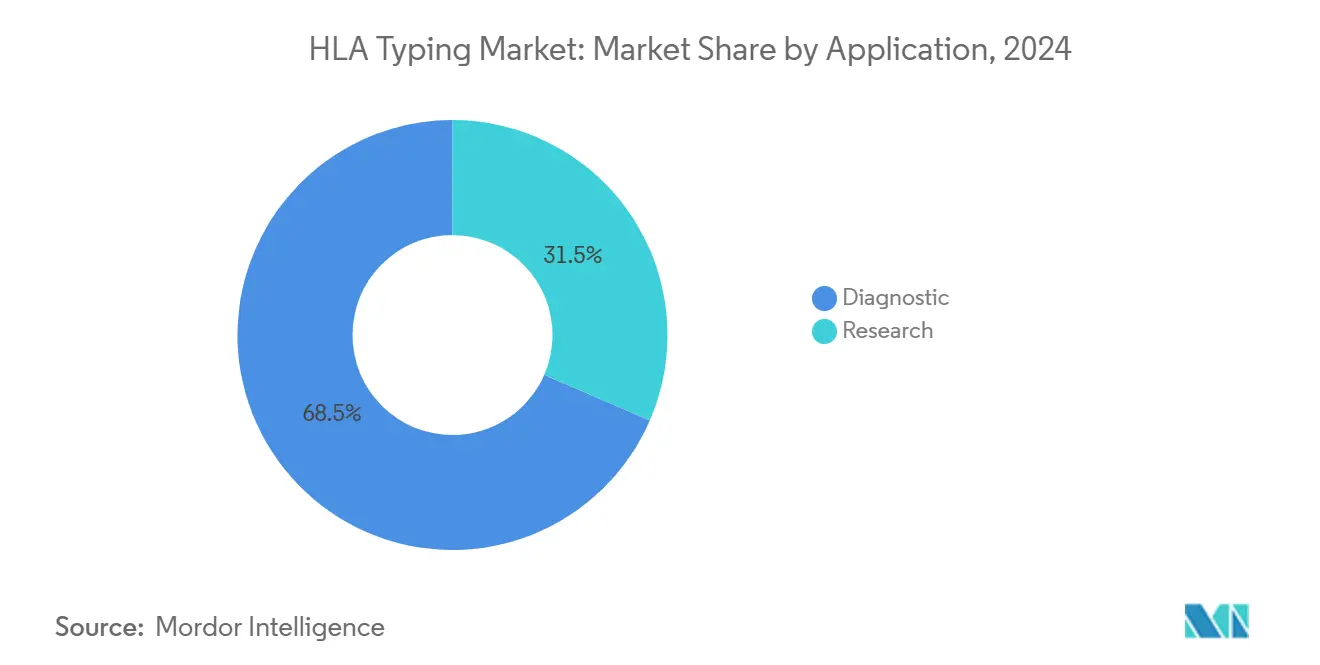

- By application, diagnostic testing accounted for 68.54% of total demand in 2024, whereas research use is set to grow at a 10.32% CAGR.

- By end user, commercial service providers captured 46.67% of the HLA typing market share in 2024, while research and academic laboratories are projected to register a 10.45% CAGR to 2030.

- By geography, North America retained 44.56% revenue share in 2024, though Asia-Pacific is on track to post an 8.76% CAGR to 2030.

Global HLA Typing Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of chronic diseases necessitating transplantation | +1.8% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Technological advancements in high-throughput genotyping | +2.1% | Global, led by North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Increasing healthcare expenditure and insurance coverage | +1.2% | North America and Europe primary, emerging in Asia-Pacific | Medium term (2-4 years) |

| Expansion of global donor registries and biobank networks | +0.9% | Global, with accelerated growth in Asia-Pacific | Long term (≥ 4 years) |

| Growing adoption of personalized and precision medicine | +1.5% | North America and Europe core, expanding globally | Long term (≥ 4 years) |

| Supportive government policies for transplant safety and efficacy | +0.8% | Global, with regional variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence Of Chronic Diseases Necessitating Transplantation

Chronic kidney and liver failure continue to swell waitlists, with more than 105,000 patients seeking transplants in the United States in 2025. Older recipient cohorts add immunological complexity, pushing labs toward high-resolution matching that reduces rejection risk. Global diabetes and hypertension trends enlarge the candidate pool, while xenotransplant research introduces novel cross-species compatibility questions. These conditions sustain year-round testing demand, shielding the HLA typing market from broader healthcare spending cycles.

Technological Advancements In High-Throughput Genotyping

Next-generation sequencing now delivers two-field or higher allele resolution in a single run, shortening decision windows from days to hours. Roche’s sequencing-by-expansion platform improves read-accuracy at high throughput, and Illumina’s DRAGEN HLA Caller auto-phases 11 loci simultaneously . Oxford Nanopore’s real-time long reads hit 96% concordance for non-DRB genes. AI classifiers such as Orthanq integrate uncertainty metrics that flag borderline calls for review. Automation mitigates personnel shortages and supports distributed service-provider networks that feed into centralized bioinformatics pipelines.

Increasing Healthcare Expenditure And Insurance Coverage

The Medicare IOTA Model ties reimbursement to graft-survival metrics, encouraging transplantation programs to adopt higher-accuracy typing. Emerging economies raise public-health budgets, with Asia-Pacific healthcare outlays projected at USD 138 billion by 2027. Private insurers increasingly deem high-resolution typing medically necessary, broadening patient access. Value-based models funnel savings from avoided rejection episodes back into advanced testing budgets, reinforcing uptake across hospital systems.

Expansion Of Global Donor Registries And Biobank Networks

The National Marrow Donor Program’s “Donor for All” initiative shows that widening acceptable match windows can cover nearly every patient but requires standardized high-resolution typing. WHO’s global transplantation strategy mandates each member state to meet domestic needs by 2035 through improved typing infrastructure[2]World Health Organization, “Global Strategy on Donation and Transplantation,” who.int. Modernized OPTN contracts integrate hundreds of histocompatibility labs into a single data backbone to enhance match algorithms[3]Health Resources & Services Administration, “OPTN Modernization Initiative,” hrsa.gov. International proficiency schemes harmonize quality, making cross-border organ sharing viable.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of next-generation HLA typing platforms | -1.4% | Global, most pronounced in emerging markets | Short term (≤ 2 years) |

| Shortage of skilled laboratory and bioinformatics personnel | -1.1% | Global, acute in Asia-Pacific and MEA | Medium term (2-4 years) |

| Stringent and divergent regulatory approval pathways | -0.7% | Global, regional complexity variations | Long term (≥ 4 years) |

| Limited testing accessibility in low-resource settings | -0.9% | Asia-Pacific, MEA, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost Of Next-Generation HLA Typing Platforms

Capital outlays approach USD 500,000 per sequencer, with per-sample consumables above USD 200 in many laboratories. Infrastructure upgrades for temperature and data storage add hidden expenses, perpetuating a two-tier ecosystem where resource-constrained sites cling to serology. Academic funding softness, highlighted in Bio-Rad’s 2025 results, further delays procurement cycles. Vendors counter with reagent-rental models, yet ownership costs remain a hurdle through 2026.

Shortage Of Skilled Laboratory And Bioinformatics Personnel

Global health-workforce deficits near 10 million by 2030, and histocompatibility crosses immunology and data science, shrinking the eligible talent pool. Poland’s lab system shows how financing shortfalls and staffing gaps can compromise quality despite oversight. Automation eases workload but does not yet replace expert review, making recruitment and retention central to scaling the HLA typing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Consumables Dominance Meets Software Acceleration

Reagents and consumables retained 72.89% revenue share in 2024 as every test run consumes locus-specific primers, enzymes, and sequencing reagents. The HLA typing market size for consumables is on course to expand steadily alongside global test-volume growth. Software and services, though smaller, are rising at a 9.56% CAGR as laboratories prioritize data-interpretation tools that resolve ambiguous calls and automate report generation.

Demand patterns underline a pivot from data generation to data insight. Cloud-hosted analytics now allow small-volume sites to upload raw reads and receive curated allele calls within hours. Commercial providers bundle wet-lab reagents with subscription software, transforming revenue into recurring streams. Integrated service packages, from sample logistics to interpretive support, appeal to hospitals that lack in-house specialists. Instruments remain essential as enablers, yet vendors increasingly offer reagent-rental schemes that shift capital costs into operating budgets, broadening entry points for new laboratories.

By Technology: Molecular Methods Lead Despite Serological Resurgence

Molecular assays captured 58.45% of revenue in 2024, cementing their status as the performance benchmark for transplant programs. Rapid turnaround and allele-level precision elevate their use in time-critical kidney and heart allocations, keeping the HLA typing market on a high-accuracy trajectory.

Serological tests, however, post an 8.77% CAGR as budget-sensitive facilities in emerging economies weigh affordability over resolution. Hybrid models are gaining ground, where a serology screen triages samples needing deeper molecular follow-up. The FDA’s 2024 Laboratory Developed Test rule exempted certain transplant assays from added oversight, incentivizing continued innovation without prolonged regulatory drag. Sequencing costs are trending lower, yet reagent reuse and simplified workflows must continue to narrow the cost gap to accelerate molecular dominance.

By Application: Diagnostic Leadership Challenged by Research Expansion

Diagnostic use commanded 68.54% of total tests in 2024 as transplantation and transfusion safety demands remain non-negotiable. The HLA typing market size for diagnostic services is projected to grow in line with rising organ-failure incidence and improved insurance coverage.

Research applications are advancing at a 10.32% CAGR, driven by immunotherapy development where HLA presentation dictates drug efficacy. The FDA clearance of Thermo Fisher’s SeCore CDx HLA A Sequencing System as a companion diagnostic in synovial sarcoma validates the role of HLA typing in oncology. Biobanks now mandate HLA profiles for stored specimens to enable future retrospective analyses. Pharmaceutical pipelines increasingly include peptide-based vaccines that require precise HLA target mapping, expanding research demand beyond academic centers.

By End User: Commercial Providers Lead Academic Acceleration

Commercial service providers held 46.67% revenue share in 2024, reflecting economies of scale in centralized testing models. Outsourcing relieves hospitals of capital and staffing burdens, and bundled post-transplant monitoring further locks in client relationships.

Research and academic laboratories are growing at 10.45% CAGR, buoyed by grant funding and lower-cost benchtop sequencers. The HLA typing market share of these labs is expected to rise as campus-based precision-medicine initiatives internalize genotyping to safeguard data sovereignty. Hospital labs maintain steady volumes for urgent pre-transplant typing, while blood banks adopt HLA screening to prevent platelet transfusion refractoriness. Donor registries increasingly perform their own high-throughput typing to speed listing readiness.

Geography Analysis

North America led with 44.56% revenue share in 2024 thanks to mature transplant networks, more than 250 accredited hospitals, and comprehensive insurance reimbursement. Ongoing OPTN modernization injects advanced matching algorithms and funds laboratory upgrades, keeping adoption momentum high. Workforce shortages and budget scrutiny temper equipment purchase cycles, yet performance-linked payment models provide a counterbalancing pull toward precise typing.

Asia-Pacific is the fastest growing region at an 8.76% CAGR toward 2030. Government investment, rising chronic-disease prevalence, and donor-registry expansions underpin demand. China scales nationwide organ-sharing platforms, Japan leverages biotechnology depth, and India widens access through public-private transplant centers. Cost sensitivity drives uptake of mixed serology-molecular workflows, yet falling sequencing costs and cloud analytics are closing the affordability gap.

Europe shows steady expansion anchored in stringent quality standards and cross-border organ-sharing frameworks such as Eurotransplant. High proficiency-testing compliance drives laboratories toward high-resolution assays. Economic headwinds in certain member states delay top-tier instrumentation purchases, encouraging vendors to roll out reagent-rental and pay-per-use models. Regional participation in WHO’s global transplant strategy positions European expertise as a technical support hub for developing regions.

Competitive Landscape

Competition is moderate, with the top tier comprising Thermo Fisher Scientific, Bio-Rad Laboratories, and CareDx. Each company orchestrates a full-stack offering that blends instruments, consumables, and informatics into turnkey solutions. Strategic consolidation continues; Werfen acquired Omixon for USD 25 million in 2024 to marry its transfusion-diagnostics reach with next-generation sequencing depth. Illumina purchased Conexio Genomics to couple its hardware with specialized HLA software that accelerates allele calling.

Technology roadmaps prioritize automation and AI-driven analytics to relieve staffing bottlenecks. Bio-Rad’s collaboration with Oncocyte couples droplet digital PCR with cell-free DNA monitoring, broadening post-transplant surveillance applications. Cloud-based platforms lower entry barriers for small labs and expand total addressable volume. White-space opportunities include affordable sequencers for emerging markets and turnkey bioinformatics pipelines that minimize IT overhead. Regulatory clarity after the 2024 Laboratory Developed Test rule rewards incumbents with compliance infrastructure yet opens windows for nimble entrants.

HLA Typing Industry Leaders

Thermo Fisher Scientific Inc.

Bio-Rad Laboratories Inc.

Qiagen N.V.

Caredx Inc.

Illumina Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Roche launched sequencing by expansion, slashing run time while boosting accuracy for HLA typing.

- January 2025: FDA issued draft donor-eligibility guidance that updates screening requirements impacting typing workflows.

- December 2024: Medicare IOTA Model finalized, linking transplant payments to HLA match quality.

- October 2024: CareDx partnered with Dovetail Genomics to integrate Hi-C-based haplotyping into AlloSeq Tx 17.

- August 2024: QIAGEN broadened its AstraZeneca collaboration to co-develop companion diagnostics on QIAstat-Dx.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the HLA typing market as every instrument, reagent, consumable, software module, and related laboratory service used to assign human-leukocyte-antigen alleles through molecular assays or serological methods for transplantation matching, disease risk assessment, and supporting research.

Scope exclusion: outsourced histocompatibility testing bundled inside full transplant packages is not counted.

Segmentation Overview

- By Product & Service

- Instruments

- Reagents & Consumables

- Software & Services

- By Technology

- Molecular Assays

- Non-Molecular / Serological

- By Application

- Diagnostic

- Research

- By End User

- Hospitals & Transplant Centers

- Commercial Service Providers

- Research & Academic Laboratories

- Blood Banks & Donor Registries

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed histocompatibility lab directors, transplant surgeons, procurement officers, and regional distributors across North America, Europe, and Asia-Pacific. They then ran a web survey with molecular lab managers. These conversations clarified kit pricing bands, procedure frequencies, and technology switch-over timelines that desk work alone could not pin down.

Desk Research

We opened with tier-1 public sources such as the WHO Global Observatory on Donation and Transplantation, World Marrow Donor Association files, the U.S. FDA 510(k) and de novo databases, Euro-CE records, and journals including Transplantation. Company 10-Ks, investor presentations, and respected trade newsletters enriched revenue splits, while Dow Jones Factiva and D&B Hoovers flagged shipment and deal signals. Patent streams harvested through Questel helped us trace next-generation workflows. The sources listed are illustrative; many additional publications informed data collection, validation, and interpretation.

Market-Sizing & Forecasting

We start top-down with annual solid-organ and stem-cell transplant counts plus new donor-registry enrollments. We multiply them by test panels per patient and marry the totals with region-specific average kit prices. Selective bottom-up supplier shipment samples act as a reasonableness check. Key variables modeled include registry size, NGS platform penetration, reimbursement shifts in the United States and China, rapid PCR uptake in low-resource centers, and currency movements. Multivariate regression supported by scenario analysis projects each driver and reconciles gaps where bottom-up evidence is sparse.

Data Validation & Update Cycle

Outputs pass anomaly scans against independent transplant statistics and public company disclosures, followed by multi-analyst review. Reports refresh each year, with interim updates triggered by material regulatory or technological events. A final pass before delivery ensures clients receive the latest view.

Why Our HLA Typing Baseline Commands Confidence

Published estimates often diverge because every firm chooses a different scope, baseline year, and price assumption. For instance, one external study pegs the 2024 market at USD 1.6 billion, while another lists USD 1.64 billion for the same year.

Key gap drivers include whether prenatal or autoimmune HLA panels are counted, the breadth of consumables captured, exchange-rate treatment, and refresh cadence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.8 billion (2025) | Mordor Intelligence | - |

| USD 1.6 billion (2024) | Global Consultancy A | Includes prenatal/autoimmune kits, single global ASP, older baseline |

| USD 1.64 billion (2024) | Trade Journal B | Bundles non-HLA immunogenetic tests, uses 2020 exchange rates, infrequent refresh |

The comparison shows that when a narrower clinical-grade scope, current transplant counts, and dual-validated pricing are applied, Mordor Intelligence provides a balanced, transparent baseline our clients can track and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the HLA typing market?

The market is valued at USD 0.80 billion in 2025 and is projected to reach USD 1.14 billion by 2030.

Which product category generates the most revenue?

Reagents and consumables account for 72.89% of 2024 revenue due to their recurrent use in every test run.

Why is Asia-Pacific the fastest-growing region?

Rising chronic disease prevalence, government investment in transplant capacity, and expanding donor registries support an 8.76% CAGR through 2030.

How are next-generation sequencing platforms influencing the market?

They provide higher allele resolution and faster turnaround times, enabling real-time donor-recipient matching and driving laboratory upgrades.

What are key restraints on market growth?

High capital costs for advanced platforms and shortages of skilled laboratory and bioinformatics personnel remain the primary hurdles.

Which companies lead the competitive landscape?

Thermo Fisher Scientific, Bio-Rad Laboratories, and CareDx are among the leading players, with recent consolidation moves by Werfen and Illumina strengthening market positions.

Page last updated on: