Hematopoietic Stem Cell Transplantation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

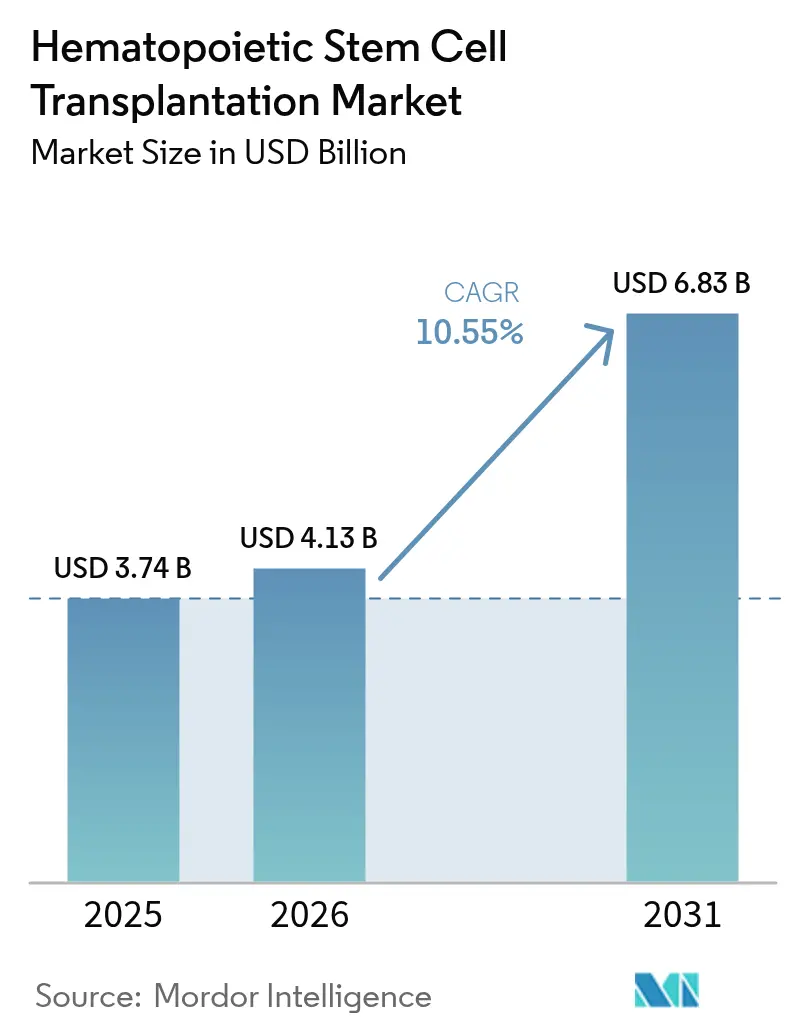

| Market Size (2026) | USD 4.13 Billion |

| Market Size (2031) | USD 6.83 Billion |

| Growth Rate (2026 - 2031) | 10.55% CAGR |

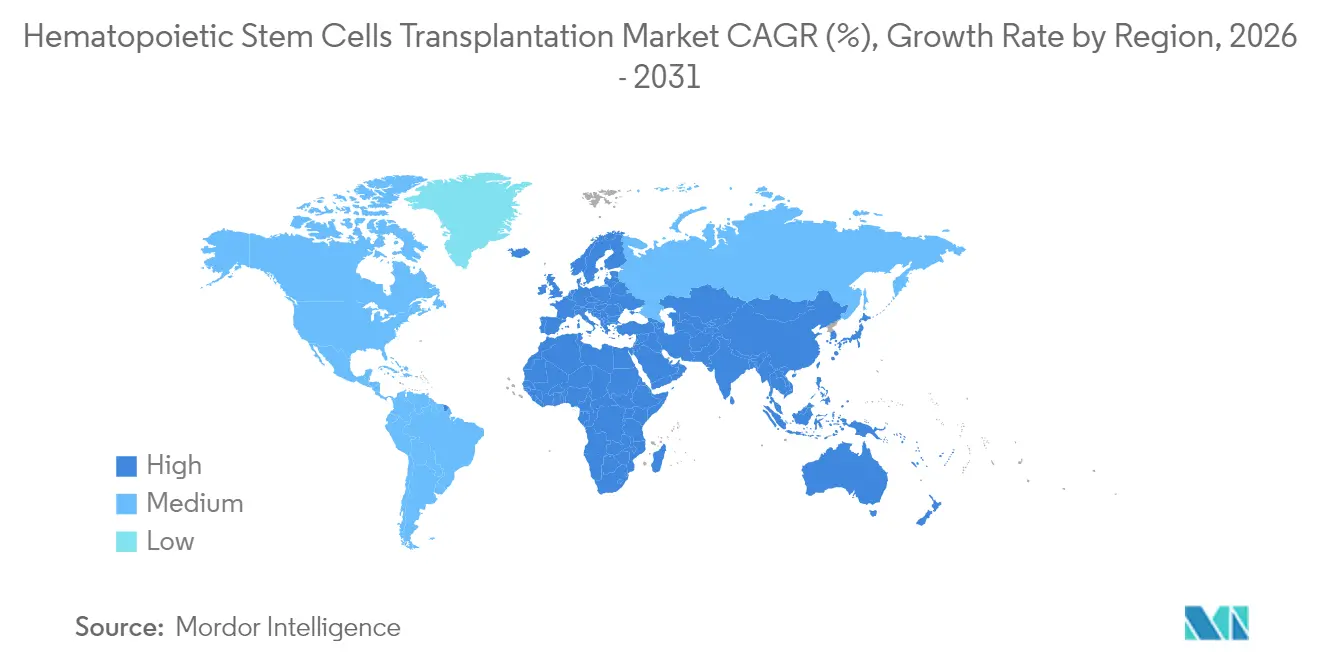

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hematopoietic Stem Cell Transplantation Market Analysis by Mordor Intelligence

The Hematopoietic Stem Cell Transplantation Market size was valued at USD 3.74 billion in 2025 and estimated to grow from USD 4.13 billion in 2026 to reach USD 6.83 billion by 2031, at a CAGR of 10.55% during the forecast period (2026-2031).

Expanding indications beyond hematologic malignancies, the convergence of reduced-toxicity conditioning agents, and wider donor-matching networks are moving the therapy from niche to mainstream. Momentum is bolstered by the use of HSCT as a bridging option before chimeric antigen receptor T-cell infusions, while next-generation AI tools accelerate donor–recipient matching for ethnically diverse populations. North America keeps a leadership position due to reimbursement clarity and clinical-trial density, yet Asia-Pacific is delivering the fastest procedural growth as healthcare systems invest heavily in transplant centers. Competitive intensity remains moderate because of high infrastructure and accreditation hurdles, though automated cell-processing platforms and cloud-based registry analytics are starting to reset operating cost curves.

Key Report Takeaways

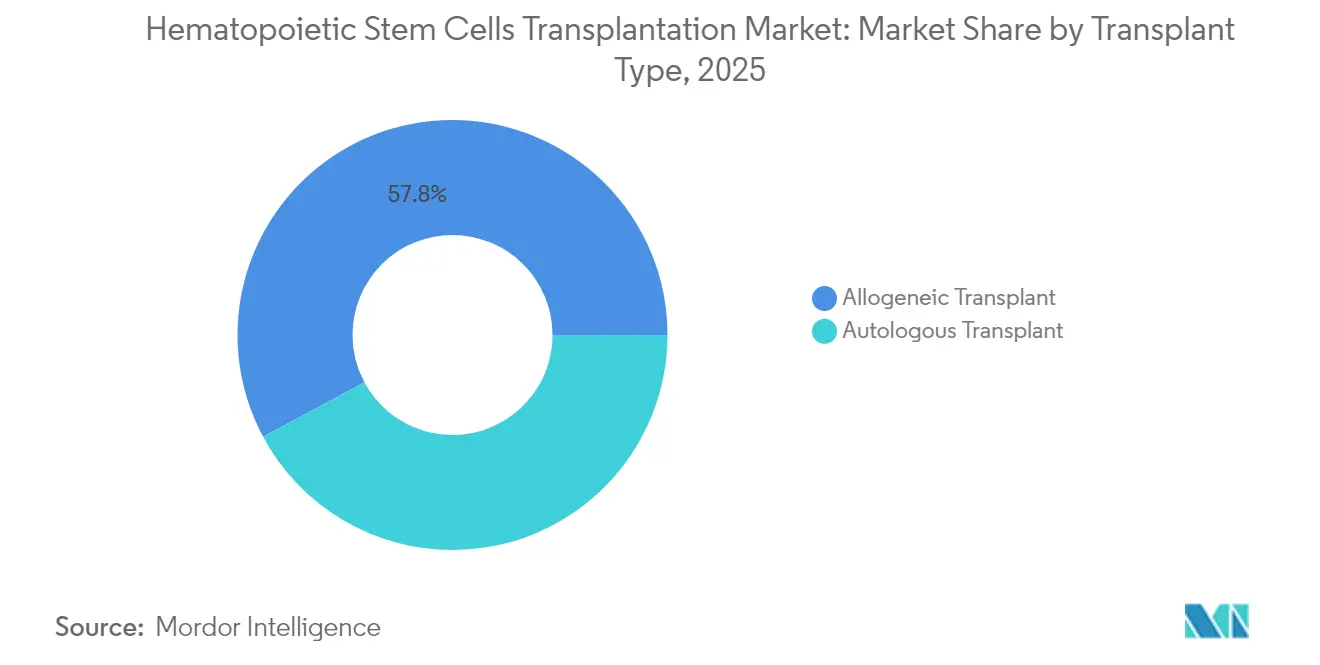

- By transplant type, allogeneic procedures held 57.84% of the Hematopoietic stem cells transplantation market share in 2025, while the same segment is forecast to expand at 11.05% CAGR through 2031.

- By stem cell source, peripheral blood accounted for 80.62% share of the Hematopoietic stem cells transplantation market size in 2025, whereas cord blood is projected to grow at 12.15% CAGR to 2031.

- By indication, leukemia dominated with 34.28% revenue share in 2025; non-malignant blood disorders are advancing at a 12.78% CAGR over the forecast horizon.

- By end user, transplant and cellular-therapy centers led with 44.73% share in 2025; academic and research institutes are poised for the fastest 13.92% CAGR through 2031.

- By geography, North America commanded 41.35% of the Hematopoietic stem cells transplantation market in 2025, while Asia-Pacific is set to grow at 14.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hematopoietic Stem Cell Transplantation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Incidence of Hematologic Malignancies | +2.8% | Global, with higher impact in aging populations of North America & Europe | Long term (≥ 4 years) |

| Advancements in Conditioning Regimens | +2.1% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Increased Investment in Regenerative Medicine and Cell Therapy R&D | +1.9% | North America, EU, Asia-Pacific core markets | Long term (≥ 4 years) |

| Expansion of International Donor Registries and HLA-Typing Technologies | +1.7% | Global, with significant impact in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Emergence of CAR-T Bridging Strategies | +1.4% | North America & EU, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Integration of AI and Machine Learning in Donor-Recipient Matching | +1.2% | Global, with early gains in North America, EU, and Asia-Pacific tech hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Incidence of Hematologic Malignancies

Cancer incidence reached 20 million new cases worldwide in 2024, and leukemias generate 34.65% of transplant procedures, reinforcing steady demand for the Hematopoietic stem cells transplantation market. Earlier detection protocols and Medicare’s 2024 coverage expansion for myelodysplastic syndromes have lowered access barriers in the United States.[1]Centers for Medicare & Medicaid Services, “Inpatient Prospective Payment System Rulemaking,” cms.gov An aging population in Europe and North America sustains a large eligible pool, and emerging markets are following suit as diagnostic infrastructures improve. Screening at earlier disease stages supports better conditioning-tolerance windows, enabling more transplants. Given the constant rise in disease incidence, this driver is expected to keep momentum beyond 2030.

Advancements in Conditioning Regimens

The January 2025 approval of treosulfan-based Grafapex enabled reduced-intensity conditioning with improved overall survival versus busulfan protocols, broadening the Hematopoietic stem cells transplantation market to frail or elderly patients.[2]U.S. Food and Drug Administration, “BLA Approvals for Hematopoietic Products,” fda.gov Precision pharmacogenomic testing now personalizes dosing and reduces organ toxicity. AI-directed regimen selection further lowers treatment-related mortality. Ongoing clinical programs are evaluating antibody-drug conjugate conditioning that targets malignant cells while sparing healthy tissue. Collectively, these innovations enlarge the candidate pool and cut inpatient lengths of stay.

Increased Investment in Regenerative Medicine and Cell Therapy R&D

A USD 50 million Series B in 2025 for Garuda Therapeutics typifies venture appetite for next-generation stem-cell platforms, indirectly aiding the Hematopoietic stem cells transplantation market as shared manufacturing assets come online. Lonza’s USD 1.2 billion acquisition of Roche’s Vacaville site in 2025 adds large-scale GMP suites that reduce production bottlenecks. Capital inflows accelerate innovation in cryopreservation, cell expansion and closed-system bioreactors, each improving transplant consistency. Public–private consortia are also steering funds toward autoimmune-disease protocols, which could unlock new patient pools. Strategic infrastructure investments are likely to keep supply-chain risk at manageable levels.

Expansion of International Donor Registries and HLA-Typing Technologies

The World Marrow Donor Association now coordinates over 39 million registrants, with algorithms cutting search times and broadening donor options for minority patients.[3]World Marrow Donor Association, “Annual Global Donor Registry Report,” wmda.info DKMS introduced the first cryopreserved peripheral-blood bank permitting transplants within days, streamlining urgent cases. Machine-learning models that accept partial HLA matches enlarge compatibility rates. Asia-Pacific registries have grown rapidly, reflecting targeted outreach in India and China. These initiatives fortify the Hematopoietic stem cells transplantation market by shortening wait lists and raising transplant success probabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of HSCT Procedures and Long-Term Post-Transplant Care | -1.8% | Global, with higher impact in emerging markets | Long term (≥ 4 years) |

| Limited Availability of Matched Donors | -1.2% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Growing Adoption of CAR-T and Other Cell Therapies | -1.1% | North America & EU primarily, with expansion to Asia-Pacific | Medium term (2-4 years) |

| Manufacturing and Regulatory Bottlenecks in GMP-Compliant Cell Therapy Facilities | -0.9% | Global, with acute impact in regions with limited manufacturing infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of HSCT Procedures and Long-Term Post-Transplant Care

Total episode spending often exceeds USD 400,000, straining both payers and patients. Proposed Medicare payment reforms now tie reimbursement to measurable outcomes, but uniform implementation remains elusive. Chronic graft-versus-host disease adds 50% to hospitalization expenses, with mean inpatient costs in the United Kingdom hitting GBP 18,567 in 2024. Emerging value-based contracts cover only a fraction of transplant centers, slowing widespread adoption. Financial toxicity is therefore likely to limit adoption in health systems with constrained budgets.

Limited Availability of Matched Donors

Despite registry expansion, patients from under-represented ethnic backgrounds still encounter lower match probabilities. The National Marrow Donor Program’s “Donor for All” research suggests 5/8 HLA mismatches could yield suitable donors for 99% of recipients, but clinical standardization is incomplete. Cord-blood doses remain insufficient for large adults, prompting research into ex vivo expansion platforms such as UM171, now under accelerated EMA review. Until these solutions mature, donor scarcity will act as a dampener on the Hematopoietic stem cells transplantation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transplant Type: Allogeneic Dominance Drives Innovation

Allogeneic procedures captured 57.84% of the Hematopoietic stem cells transplantation market in 2025 and are tracking an 11.05% CAGR to 2031, signaling enduring reliance on donor-sourced grafts. Orca-T posted superior Phase 3 survival and relapse outcomes versus standard care and showcases how selective graft engineering can cut graft-versus-host disease, further enlarging adoption. The segment benefits from registry growth, improved HLA-typing accuracy, and prophylaxis innovations like post-transplant cyclophosphamide.

Momentum is also evident in haploidentical protocols, where partial matches from relatives expand donor pools and reduce search times. A Johns Hopkins study documented 95% overall survival and 88% cure rates in sickle-cell disease using reduced-intensity, haploidentical bone-marrow transplantation. These outcomes reinforce the competitive edge of allogeneic grafts even as autologous approaches face substitution risk from CAR-T therapies. The Hematopoietic stem cells transplantation market therefore remains anchored by allogeneic innovation, with process automation and targeted conditioning poised to enhance margin profiles.

By Stem Cell Source: Peripheral Blood Leadership with Cord Blood Acceleration

Peripheral-blood procedures retained 80.62% share of the Hematopoietic stem cells transplantation market in 2025 due to rapid engraftment and donor convenience. Growth, however, is tilting toward cord-blood transplants, which are advancing at a 12.15% CAGR. The 2024 Omisirge approval shortened median neutrophil recovery to 12 days from 22 days for standard cord units, proving commercial viability for expanded grafts.

China has performed nearly 40,000 therapeutic cord-blood infusions, including 900 thalassemia transplants with 99% survival, illustrating how large-scale cord banking can propel the Hematopoietic stem cells transplantation market. Haplo-cord combinations now merge partial sibling grafts with cord units to solve cell-dose limitations in adults. Bone-marrow harvests remain relevant for indications requiring heightened graft-versus-leukemia effects, although their share continues to decline. Next-generation expansion platforms such as UM171 may further de-risk cord-blood usage in heavier patients.

By Indication: Leukemia Leadership with Non-Malignant Disorders Emerging

Leukemia accounted for 34.28% of total procedures in 2025, underlining its status as the largest revenue generator within the Hematopoietic stem cells transplantation market. Early-stage risk profiling now optimizes transplant timing, enhancing event-free survival. Consistent evidence supports tandem transplants and MRD-guided conditioning to curb relapse.

Non-malignant blood disorders are the fastest-growing indication, posting 12.78% CAGR as curative transplants for sickle-cell disease and thalassemia become routine. Gene-editing breakthroughs like exa-cel underscore curative potential, yet HSCT retains an edge on durability in many centers. Lymphoproliferative disorders hold moderate share, but competitive pressure from CAR-T products could temper future HSCT demand. Overall, the expanding indication mix keeps the Hematopoietic stem cells transplantation market diversified and resilient.

By End User: Transplant Centers Lead with Academic Institutes Accelerating

Dedicated transplant centers held 44.73% share in 2025, benefiting from multidisciplinary teams and economies of scale that align with accreditation metrics. Many of these centers integrate cell-processing suites, helping them capture downstream revenue and strengthen bargaining clout with payers. Standardization initiatives, such as the Joint Accreditation Committee for ISCT and EBMT, reinforce their dominant market position.

Academic institutions, advancing at 13.92% CAGR, are spearheading early-phase trials for antibody-based conditioning and graft engineering. The FDA authorization of Ryoncil for steroid-refractory acute GVHD stemmed directly from multicenter academic data sets asgct.org. Research-driven patient inflows accelerate adoption of novel regimens before community roll-out, driving above-market growth. Smaller multi-specialty hospitals remain constrained by capital investment requirements and staffing gaps, keeping the Hematopoietic stem cells transplantation market concentrated in high-volume hubs.

Geography Analysis

North America controlled 41.35% of the Hematopoietic stem cells transplantation market in 2025 thanks to favorable reimbursement mechanisms, a dense transplant-center network, and continuous trial activity. Medicare’s alignment of transplant payments with Diagnosis-Related Group revisions has improved provider liquidity, encouraging volume growth. The region also accounts for a sizable portion of global autologous transplants because of multiple myeloma prevalence.

Europe follows closely, backed by standardized EBMT guidelines and cross-border donor coordination. Adoption of treosulfan conditioning in Germany and Italy demonstrates how regulatory convergence accelerates technology diffusion. However, tighter budget caps in certain markets slow procedure growth compared with North America.

Asia-Pacific stands out with a 14.85% CAGR and is quickly narrowing the procedural-density gap. China’s National Health Commission has increased public funding for transplant infrastructure, while India introduced bundled-payment pilots that include long-term follow-up. New cord-blood labs in the United Arab Emirates rose from 2 to 8 after regulatory changes in 2020, showing how policy shifts can fast-track capacity. South America and the Middle East & Africa remain nascent but are positioned for double-digit growth as insurance coverage widens. Combined, these regional dynamics underscore the strategic importance of geographical diversity for companies targeting the Hematopoietic stem cells transplantation market.

Competitive Landscape

The Hematopoietic stem cells transplantation market is consolidated, with high barriers tied to capital-intensive GMP facilities and stringent regulatory oversight. Lonza’s USD 1.2 billion purchase of Roche’s Vacaville site expands integrated manufacturing offerings and secures long-term client contracts. Miltenyi Biotec struck a multi-year supply pact with Autolus Therapeutics to provide CliniMACS cell-processing hardware, locking in downstream consumable revenue.

Product innovation remains a differentiator. The FDA clearance of Omisirge, the first ex vivo expanded cord-blood graft, gives Gamida Cell a competitive edge, while Orca-T’s selective allograft architecture could redefine GVHD management. Automated closed-system technologies reduce labor costs and contamination risks, allowing smaller entrants to compete on efficiency. AI-powered donor-matching software licensed by registries in the United States and Germany is reducing search times and could become a standard add-on service.

Strategic partnerships help firms bridge capability gaps. Contract development and manufacturing organizations collaborate with hospital networks to embed processing suites inside transplant centers, shortening logistics. Companies also co-develop companion diagnostics for pharmacogenomic-based conditioning, reinforcing stickiness across the transplant continuum. Despite emerging threats from gene-editing and CAR-T modalities, synergies in sequential or combination therapy are driving cross-technology alliances that keep the competitive field active.

Hematopoietic Stem Cell Transplantation Industry Leaders

STEMCELL Technologies, Inc.

Pluristem Therapeutics, Inc.

Merck KGaA

ScienCell Research Laboratories, Inc.

Lonza Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Orca Bio announced positive results from its pivotal Phase 3 study of investigational Orca-T compared to allogeneic stem cell transplant for hematologic malignancies, demonstrating superior outcomes that could reshape treatment paradigms for high-risk patients requiring transplantation.

- March 2025: Garuda Therapeutics raised USD 50 million in funding and appointed a new CEO to advance its stem cell therapy pipeline, reflecting continued investor confidence in next-generation transplant technologies.

- February 2025: Johns Hopkins Kimmel Cancer Center published breakthrough results in The New England Journal of Medicine Evidence demonstrating 95% survival and 88% cure rates using reduced-intensity haploidentical bone marrow transplantation for sickle cell disease.

- February 2025: IN8bio presented positive Phase 1 data at TCT 2025 for its allogeneic gamma-delta T cell therapy INB-100, showing no relapses in AML patients after median follow-up of 20.1 months with 90.9% one-year progression-free survival.

- January 2025: FDA approved Grafapex (treosulfan) in combination with fludarabine for allogeneic hematopoietic stem cell transplantation in patients aged one year and older with AML or MDS, providing a new conditioning regimen option with improved safety profile.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the hematopoietic stem cell transplantation (HSCT) market as the value generated from autologous and allogeneic infusions of mobilized or harvested hematopoietic stem cells sourced from peripheral blood, bone marrow, or umbilical cord to re-establish hematopoiesis in patients with malignant and non-malignant disorders. Revenues include transplant-related cell processing, procurement, conditioning, and immediate post-infusion care that are tracked by Mordor Intelligence across 28 countries.

Exclusion note: Therapies based on gene-edited autologous cells that remain in phase I trials are outside this scope.

Segmentation Overview

- By Transplant Type

- Autologous Transplant

- Allogeneic Transplant

- By Stem Cell Source

- Peripheral Blood Stem Cell Transplant

- Bone Marrow Transplant

- Cord Blood Transplant

- By Indication

- Leukemia

- Lymphoproliferative Disorders

- Multiple Myeloma & Plasma-Cell Dyscrasias

- Non-Malignant Blood Disorders

- By End User

- Transplant & Cellular-Therapy Centers

- Academic and Research Institutes

- Multi-Specialty Hospitals & Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed transplant physicians, apheresis directors, payor case managers, and patient advocacy leads across North America, Europe, Asia, and Latin America. Their insights refined average selling prices, graft failure probabilities, and waiting list dynamics that do not surface in public datasets.

Desk Research

We began by mapping transplant procedure counts, survival statistics, and donor registry growth published by CIBMTR, EBMT, Global Observatory on Donation and Transplantation, and national health ministries. Clinical outcome meta-analyses from journals such as Blood and Bone Marrow Transplantation informed regimen success rates that affect demand. Company 10-Ks, FACT accreditation reports, and transplant center cost sheets gave us unit economics. To size ancillary spending, our team tapped D&B Hoovers and Dow Jones Factiva for audited financials of major cell processing suppliers.

Patent filings retrieved via Questel plus cord blood bank activity logs helped us gauge emerging inventory. These sources are illustrative; many additional publications supported data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down model converts national procedure volumes and average transplant invoices (USD) into baseline market value, which is then cross-checked with sampled bottom-up roll-ups of reagent kits, cord blood units, and cryogenic bag sales. Key variables include autologous to allogeneic mix, G-CSF vial utilization per harvest, average length of neutropenia, currency shifts, and cord blood bank expansion rates. Forecasts to 2030 rely on multivariate regression linking procedure growth to leukemia incidence, registry donor adds, and reimbursement revisions, with scenario analysis tested during expert calls. Where bottom-up totals lag clinical activity, gap factors are proportionally redistributed before finalization.

Data Validation & Update Cycle

Outputs pass variance checks against historic CIBMTR trendlines and World Bank health spend elasticities, followed by peer review among senior analysts. We refresh every twelve months and re-run interim updates whenever regulatory approvals or major reimbursement shifts alter fundamentals; a last mile review ensures clients receive the latest view.

Why Mordor's Hematopoietic Stem Cells Transplantation Baseline Commands Reliability

Published estimates often diverge because firms choose different transplant types, cost buckets, and refresh cadences. We openly align scope with real-world clinical practice, which keeps our baseline grounded.

Key gap drivers include: some publishers fold phase 2 gene therapy revenues into current sales, others apply static procedure prices, and several extrapolate global totals from limited U.S. samples without registry validation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.74 B (2025) | Mordor Intelligence | - |

| USD 3.56 B (2025) | Global Consultancy A | excludes cord blood transplants, applies fixed ASP across regions |

| USD 3.25 B (2024) | Regional Consultancy B | inflates volume by counting conditioning drugs twice |

| USD 2.60 B (2022) | Trade Journal C | back projects 2022 value without accounting for 2023 to 2025 registry growth |

In sum, our disciplined source mix, clinician validation, and annual refresh give decision makers a transparent, repeatable foundation that balances prudence with on-the-ground realities.

Key Questions Answered in the Report

What is driving growth in the Hematopoietic stem cells transplantation market?

Rising incidence of blood cancers, reduced-toxicity conditioning regimens, expanding donor registries and strong investment in cell-therapy infrastructure together push the market toward a 10.55% CAGR through 2031.

How large is the Hematopoietic stem cells transplantation market in 2026?

The Hematopoietic stem cells transplantation market size is valued at USD 4.13 billion in 2026 and is forecast to reach USD 6.83 billion by 2031.

Which segment holds the largest share of the Hematopoietic stem cells transplantation market?

Allogeneic transplants lead with 57.84% share in 2025, driven by improved donor-matching technologies and GVHD prophylaxis advances.

Where is the fastest regional growth occurring?

Asia-Pacific shows the fastest regional momentum with a projected 14.85% CAGR, supported by infrastructure investments and growing insurance coverage.

What recent regulatory approvals have influenced the market outlook?

Key approvals include Grafapex treosulfan conditioning, Omisirge expanded cord-blood grafts and Ryoncil for steroid-refractory acute GVHD, each broadening patient eligibility and improving outcomes.

How does HSCT compete with CAR-T and gene therapies?

Although CAR-T offers alternative autologous options, HSCT retains advantages in durability and curative potential for a broad range of hematologic diseases, and is increasingly used as a bridging or complementary therapy.

Page last updated on: