Healthcare Fraud Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.23 Billion |

| Market Size (2031) | USD 9.22 Billion |

| Growth Rate (2026 - 2031) | 23.36% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Fraud Analytics Market Analysis by Mordor Intelligence

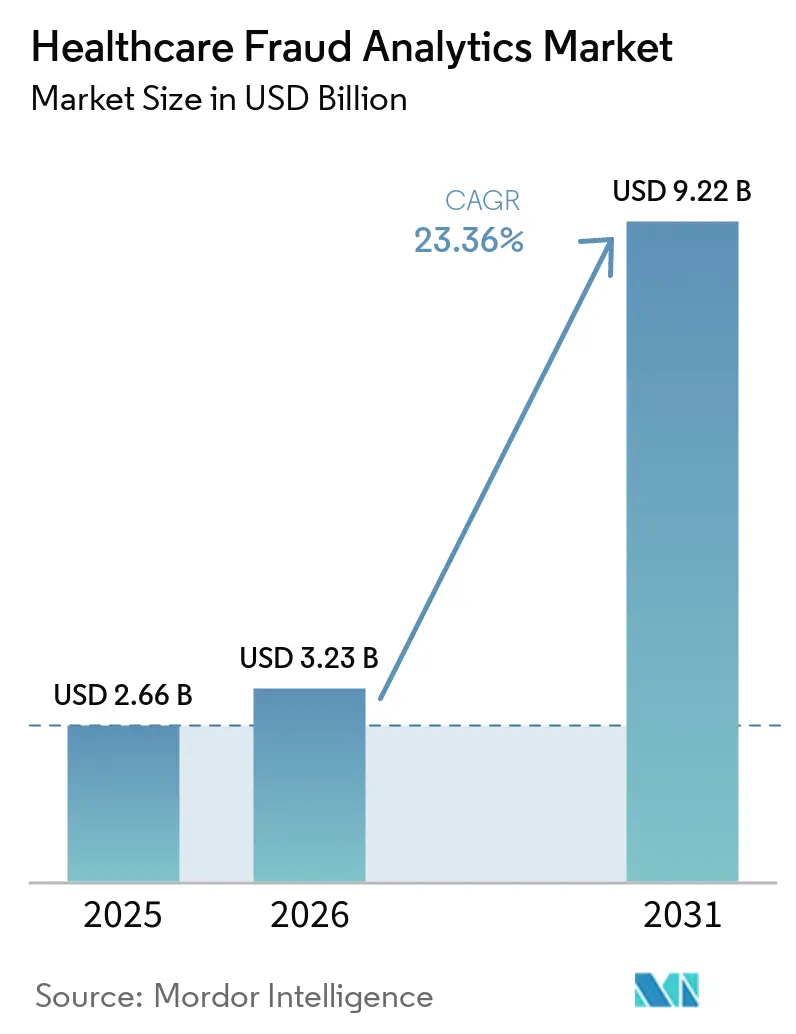

The Healthcare Fraud Analytics Market size is projected to expand from USD 2.66 billion in 2025 and USD 3.23 billion in 2026 to USD 9.22 billion by 2031, registering a CAGR of 23.36% between 2026 to 2031.

Growth in the healthcare fraud analytics market is being supported by higher payer losses, stronger enforcement activity, and a wider shift from retrospective recovery toward prepayment controls and real-time review workflows. The healthcare fraud analytics market is also benefiting from buyer demand for tools that can connect claims, pharmacy activity, and provider behavior in a single investigation path, which is where graph-based models and stronger case management are gaining attention. North America remained the largest regional base in 2025, while Asia-Pacific is set to grow fastest through 2031 as insurance pools expand and digital health systems mature, even though basic data capture gaps still limit model depth in many markets. The market also reflects a buying shift toward solutions that can explain alerts clearly, fit into existing payment workflows, and support audit readiness without forcing long implementation cycles. Competitive activity in the healthcare fraud analytics market remains moderately concentrated, with established payment integrity vendors defending share while managed services, cloud delivery, and newer AI architectures widen the opportunity set for specialist providers.

Key Report Takeaways

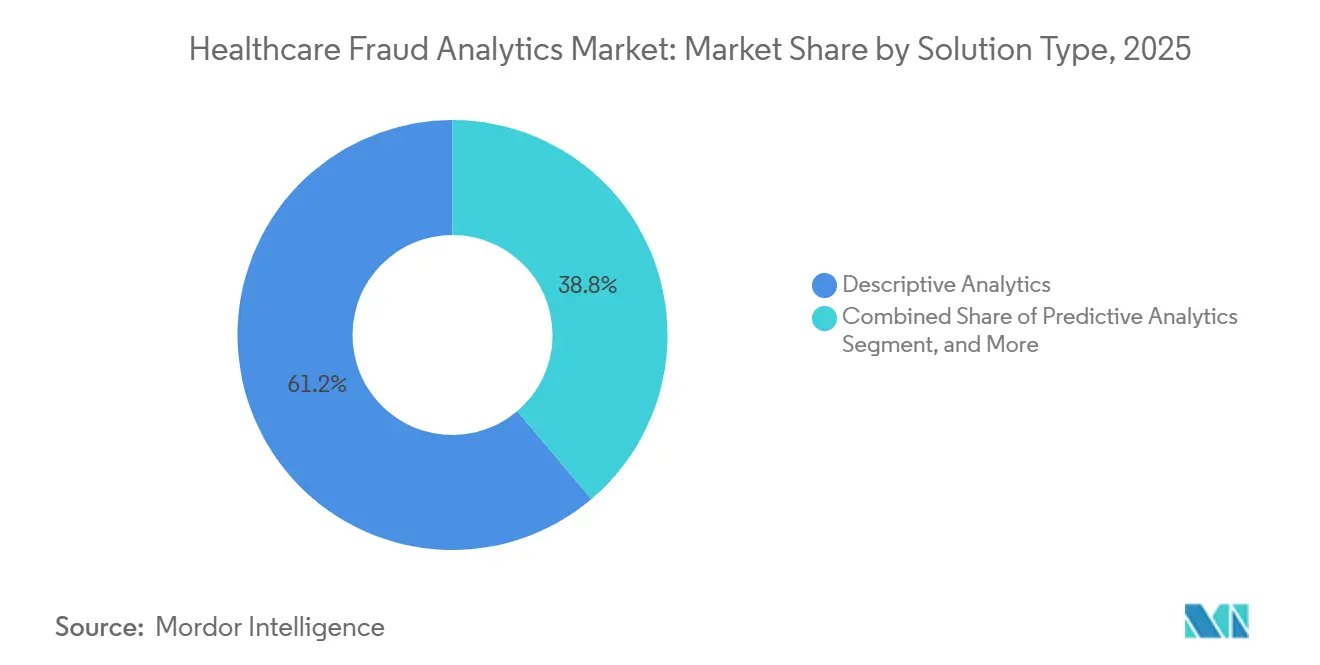

- By solution type, descriptive analytics led with 61.17% share in 2025, while predictive analytics recorded the highest projected CAGR at 24.37% through 2031.

- By deployment mode, on-premises held 54.68% share in 2025, while cloud-based deployment is forecast to expand at 26.06% CAGR through 2031.

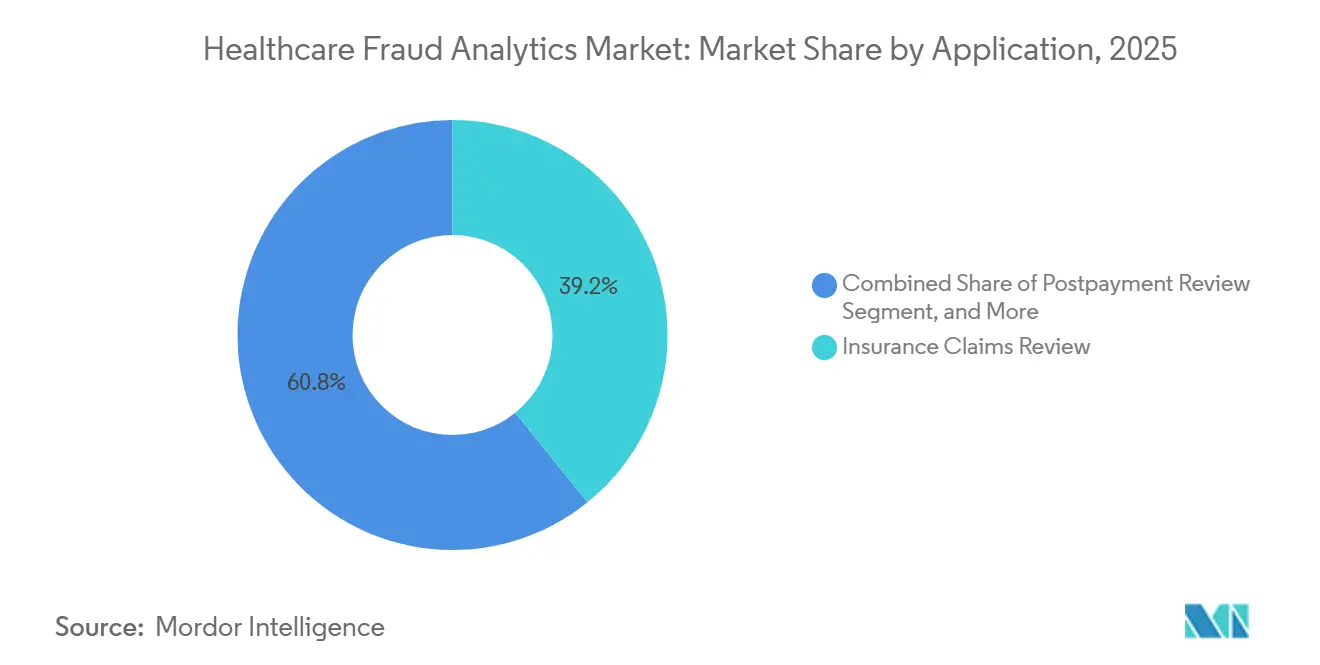

- By application, insurance claims review accounted for 39.16% share in 2025, while pharmacy billing misuse is projected to grow fastest at 24.06% CAGR through 2031.

- By end user, insurance companies held 33.62% share in 2025, while third-party service providers are expected to advance at the highest CAGR of 27.29% through 2031.

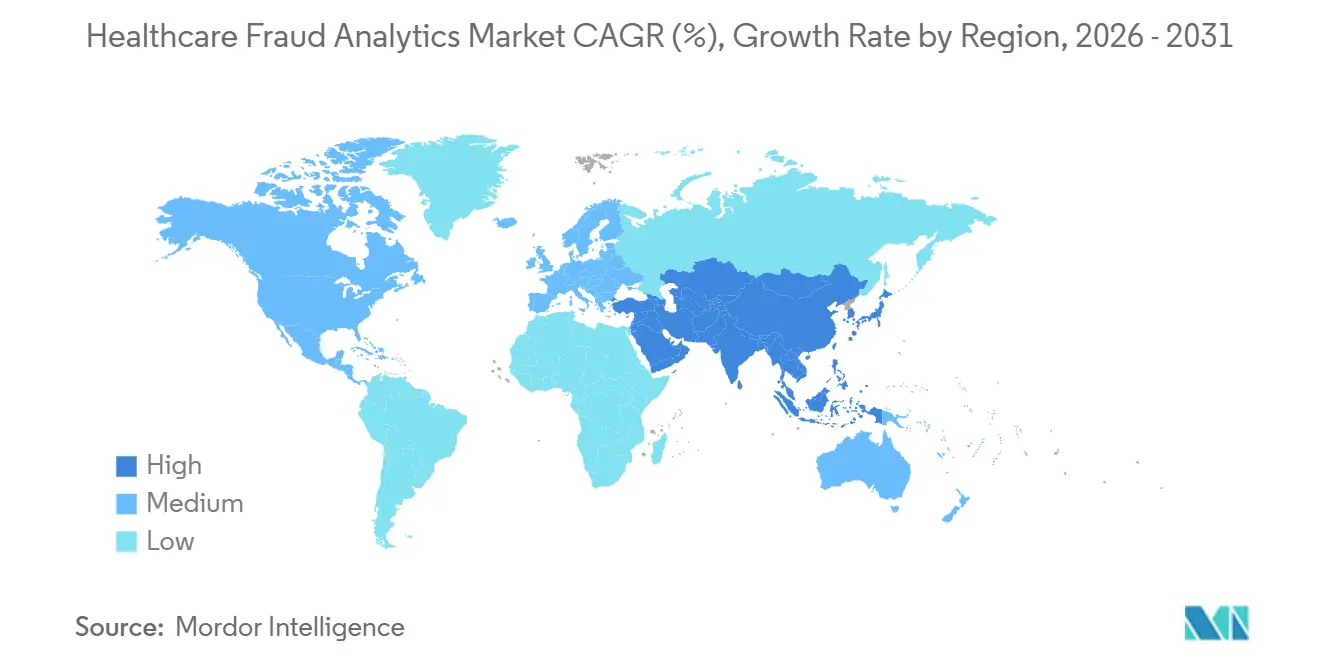

- By geography, North America held 43.64% share in 2025, while Asia-Pacific recorded the highest projected CAGR at 25.66% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Fraud Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Fraud Complexity Across Claims and Payment Workflows | +5.2% | Global, with peak intensity in North America and APAC | Short term (≤ 2 years) |

| Expansion of AI-Based Anomaly Detection in Healthcare Payments | +6.8% | North America and Europe, with spillover into APAC | Medium term (2-4 years) |

| Growth in Real-Time Prepayment Controls by Payers | +4.1% | North America, with early gains in India and Australia | Short term (≤ 2 years) |

| Regulatory Pressure for Program Integrity and Audit Readiness | +3.9% | North America and Europe | Medium term (2-4 years) |

| Cross-Channel Fraud Linkage Across Pharmacy and Medical Claims | +2.1% | North America, with spillover into South Korea and Japan | Medium term (2-4 years) |

| Demand for Graph-Based Provider-Patient-Network Intelligence | +1.8% | North America and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Fraud Complexity Across Claims and Payment Workflows

The healthcare fraud analytics market is expanding because fraudulent behavior now moves across claims, payment channels, provider entities, and pharmacy transactions instead of staying inside one isolated billing event. CMS said the Fraud Defense Operations Center suspended USD 5.7 billion in suspected fraudulent Medicare payments and generated 372 referrals tied to USD 3.7 billion in billing during 2025, which shows how broad and connected current fraud patterns have become.[1]Centers for Medicare & Medicaid Services, “Trump Administration Prioritizes Affordability by Announcing Major Crackdown on Health Care Fraud,” CMS Newsroom, cms.gov A 2025 Scientific Reports paper showed that heterogeneous graph neural network models can detect fraud at the activity level within medical claims, which reflects the growing need to trace relationships rather than only inspect line-item anomalies. That matters because payers are no longer dealing only with isolated coding mistakes or simple overbilling behavior. They are reviewing coordinated activity across providers, patients, services, and submission paths that can look normal when each claim is viewed on its own. As a result, the healthcare fraud analytics market is moving toward continuously updated models and broader data linkages that can adapt faster than manual rule libraries and static watch lists.

Expansion of AI-Based Anomaly Detection in Healthcare Payments

The healthcare fraud analytics market is also gaining momentum as AI-based anomaly detection becomes more practical in daily payment review and investigative workflows. A 2025 review in the Journal of Big Data found that advanced machine learning approaches outperformed many older classifiers in healthcare fraud detection tasks, which supports the ongoing move away from basic rule engines alone. A 2025 paper in Information said federated learning can expand model training across decentralized insurer datasets without exposing raw patient data, which is important in heavily regulated care and insurance environments. A 2024 systematic review in Artificial Intelligence in Medicine also found that limited labeled fraud outcomes still constrain model calibration, which keeps validation quality central to platform selection. These findings support broader use of AI in the healthcare fraud analytics market because they reduce dependence on static alert libraries and narrow retrospective audits. Vendors that can pair anomaly detection with explainable outputs, investigator workflow support, and stable model governance are likely to gain buyer trust more quickly than vendors offering detection scores alone.

Growth in Real-Time Prepayment Controls by Payers

The healthcare fraud analytics market is being pushed forward by payer demand for real-time prepayment controls that can act before funds leave the system. CMS is seeking stronger analytics, prepayment claim edits, and payment suspension tools through the CRUSH initiative, which shows that upstream prevention is moving into policy expectations as well as technology road maps.[2]KFF, “What to Know About Recent Federal Actions Involving State Medicaid Program Integrity,” KFF, kff.org Optum said payers are shifting fraud prevention upstream with AI strategies that review claims before payment rather than waiting for post-payment recovery programs to find misuse later. ConnectiveRx and EagleForce launched ShieldRx in April 2026 as an in-workflow tool that scores pharmacy claims in seconds before payment is released, which shows how quickly live adjudication controls are moving into production settings. This model reduces the time between claim submission and intervention, which matters when misuse is concentrated in high-cost drug and specialty channels. It also raises the baseline for the healthcare fraud analytics market because real-time scoring is becoming a standard procurement requirement rather than a feature reserved for only the largest buyers.

Regulatory Pressure for Program Integrity and Audit Readiness

Regulatory pressure continues to shape buying behavior across the healthcare fraud analytics market, especially in public programs and payer environments that face direct oversight. CMS launched the Fraud Defense Operations Center in March 2026 and tied it to a broader crackdown focused on affordability, program integrity, and quicker action on suspicious billing patterns. KFF said recent federal actions are increasing attention on Medicaid program integrity, which keeps state agencies and managed care organizations focused on audit readiness and payment accuracy. Organizations therefore need systems that can record why a claim was flagged, how a payment was paused, and whether investigators can defend the decision later. That requirement favors platforms with strong documentation, case management, and reporting controls rather than simple detection dashboards. It also helps keep demand firm in the healthcare fraud analytics market even when buyers slow discretionary spending in other analytics categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability Gaps Between Claims, EHR, and Pharmacy Data | -3.2% | APAC, with spillover into MEA and fragmented European markets | Medium term (2-4 years) |

| High Tuning Burden for False Positive Reduction | -2.1% | Global, with heavier pressure in mid-market payer environments | Medium term (2-4 years) |

| Privacy, Data Residency, and Model Governance Constraints | -1.8% | Europe and APAC, especially Japan, South Korea, and Australia | Long term (≥ 4 years) |

| Limited Access to Labeled Fraud Outcomes for Model Training | -1.4% | Global, with acute pressure in emerging insurance markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interoperability Gaps Between Claims, EHR, and Pharmacy Data

Interoperability remains a major brake on the healthcare fraud analytics market because claims, clinical, and pharmacy data often sit in separate systems that do not connect well enough for full fraud review. The Asian Development Bank found that 90% of surveyed Asia-Pacific insurers do not collect the ICD or DRG codes needed for deeper fraud analysis, which sharply limits model training and benchmarking depth. That gap weakens the ability to compare behavior across providers, treatments, and payment types, especially in markets where digital records are still incomplete. Germany's statutory insurer federation has pushed for broader billing data pooling because single insurers cannot easily see organized patterns that spread across multiple payers. When records remain fragmented, analysts spend more time stitching files together and less time validating suspicious activity. This slows deployment in the healthcare fraud analytics market and gives a structural advantage to vendors that already hold wider benchmark data and stronger data-integration tools.

High Tuning Burden for False Positive Reduction

The healthcare fraud analytics market also faces a high tuning burden because false positives are costly for payers, providers, and investigators that must review every alert. A 2024 systematic review found that weak access to standardized labeled fraud outcomes hurts calibration and makes precision harder to sustain across different settings, product lines, and claims types. The same issue means many models need repeated adjustment before users can trust them in live production environments. A 2025 study in Information pointed to privacy-preserving collaboration methods as one path to better training depth, but it also showed that deployment quality still depends on governance quality and local data readiness.[3]MDPI, “Next-Generation Machine Learning in Healthcare Fraud Detection, Current Trends, Challenges, and Future Research Directions,” Information, mdpi.com Buyers, therefore, look beyond raw detection power and ask whether a tool can reduce unnecessary alerts without slowing claims operations or straining investigator capacity. In the healthcare fraud analytics market, vendors that cannot manage this balance may struggle to keep long contracts even when their models appear strong in controlled testing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Descriptive Dominates as Predictive Analytics Scales Rapidly

Descriptive analytics held 61.17% of healthcare fraud analytics market share in 2025, which kept it as the largest solution type in the market. Its position came from long use in retrospective claims review, payment pattern analysis, and billing anomaly checks across payer and public program audit settings. Many organizations still depend on descriptive tools because they support repeatable reporting, historical comparisons, and investigator workflows that have been built over many years. Predictive analytics is projected to grow at 24.37% CAGR through 2031, and the healthcare fraud analytics market size for this solution is rising as payers look for earlier warning signals that can surface abnormal behavior before claims move through full payment cycles. Prescriptive analytics remained the smallest segment, but it is gaining attention in environments where platforms can recommend claim holds, payment pauses, and case routing actions inside the review workflow.

Research in the Journal of Big Data found that deep learning and meta-learning approaches can outperform many legacy models in fraud detection tasks, which supports continued movement toward predictive capability. MDPI also noted that federated learning could widen model training across insurers without requiring raw patient data to be shared, which is important in privacy-sensitive health systems. These developments support the shift from descriptive review toward predictive action in the healthcare fraud analytics industry, especially where payers want stronger prepayment controls without losing explainability. Even so, descriptive tools should remain important because many buyers still need a clear historical evidence base before they expand into more automated intervention models. The near-term balance across solution types suggests gradual modernization rather than abrupt replacement, which supports steady renewal demand across the healthcare fraud analytics market.

By Deployment Mode: On-Premises Leadership Gives Way to Cloud Momentum

On-premises deployment held 54.68% share in 2025, which kept it ahead of cloud-based models across the healthcare fraud analytics market. Government programs, federal contractors, and large payer organizations still prefer tighter local control when audit trails, security reviews, and procurement rules are strict. Existing infrastructure investments also support this position because large institutions often connect fraud systems to broader payment and claims administration environments that are already hosted internally. Cloud-based deployment is forecast to grow at 26.06% CAGR through 2031, and this pace reflects demand from mid-sized payers, administrators, and regional insurers that want faster rollout and lower infrastructure burden. The growth gap shows that deployment flexibility is becoming more important as buyers seek AI capability without waiting for long internal build cycles.

Cognizant said Bupa Hong Kong selected an AI-driven BPaaS model in December 2025 that combines claims automation, fraud, waste, and abuse detection, and compliance tooling in a cloud-led delivery structure. That example shows how the market is increasingly packaging analytics, process change, and managed operations into one contract. Cloud growth is also supported by buyers who need elastic computing power for model training and live scoring, but do not want to manage large internal teams for maintenance. On-premises systems should remain relevant in large government programs and tightly regulated environments, but growth is likely to stay stronger in cloud deployments. This leaves the healthcare fraud analytics industry with a mixed deployment path rather than a single uniform shift, which should keep both hosting models commercially relevant through the forecast period.

By Application: Insurance Claims Review Anchors Share While Pharmacy Billing Misuse Surges

Insurance claims review accounted for 39.16% share in 2025, which made it the largest application area in the healthcare fraud analytics market. Its lead reflects the fact that claims review remains the usual starting point for fraud, waste, and abuse programs across commercial payers, Medicare, Medicaid, and related audit environments. The category is broad enough to cover inpatient, outpatient, professional, and ancillary billing activity, which helps explain why it still anchors most platform deployments. Pharmacy billing misuse is forecast to expand at 24.06% CAGR through 2031, showing where incremental spending is moving fastest as buyers confront misuse in specialty drugs, compounding, and benefit design workarounds. Payment integrity, postpayment review, and prepayment review continue to support demand because buyers need both recovery tools and prevention tools rather than one operating model alone.

Cotiviti GOV Services received CMS Recovery Audit Contractor contracts for Regions 3, 4, and 5 in May 2025, which reinforced the scale of claims-focused audit work in the United States. ConnectiveRx and EagleForce launched ShieldRx in April 2026 to score pharmacy transactions before payment, which shows how misuse control is moving into live claim workflows instead of staying in later audit layers. Optum has also argued for shifting fraud prevention upstream, which supports continued buyer interest in prepayment and pharmacy-focused tools. Together, these patterns keep the healthcare fraud analytics market broad across applications while concentrating the fastest growth in pharmacy-related use cases that need rapid in-workflow decisioning. The application mix, therefore, remains anchored in core claims review, but the strongest expansion is clearly moving toward areas where misuse is costly and traditional audits react too slowly.

By End User: Insurance Companies Lead as Third-Party Providers Emerge as the Growth Engine

Insurance companies held 33.62% share in 2025, which made them the largest end-user group in the healthcare fraud analytics market. Their lead comes from large claim volumes, direct financial exposure, and constant pressure to manage payment accuracy while meeting audit and compliance expectations. Commercial health plans, Medicare Advantage organizations, and Medicaid managed care operators also face practical pressure to act earlier in the payment cycle when recovery rates are uncertain after funds have already been disbursed. Third-party service providers are projected to grow at 27.29% CAGR through 2031, which makes them the fastest-expanding buyer group in the healthcare fraud analytics market. This pattern shows that many payers prefer outside specialists when internal data science capacity, fraud investigation staffing, or model governance experience is limited.

Cotiviti introduced 360 Pattern Review in November 2024 as a managed service that combines prepay automation with postpay investigation in a closed-loop model backed by credentialed analysts. That approach fits buyer demand for one contract that can cover detection, triage, review, and follow-through without forcing major internal team expansion. Healthcare providers and government organizations still represent important parts of the customer base because both groups need stronger audit defense, coding oversight, and payment control capabilities. The healthcare fraud analytics market is therefore widening across end users, but outsourced service models are scaling fastest because they reduce implementation burden and shorten time to operational value. This shift should keep managed analytics, investigator support, and service-linked software offerings central to competitive positioning over the next several years.

Geography Analysis

North America held 43.64% of the healthcare fraud analytics market share in 2025, which kept it as the largest regional base in the market. CMS said the Fraud Defense Operations Center suspended USD 5.7 billion in suspected fraudulent Medicare payments and generated 372 referrals tied to USD 3.7 billion in billing during 2025, underscoring the region's strong enforcement intensity and data-driven oversight model. This enforcement depth gives the United States the region's clear lead in the healthcare fraud analytics market because public programs and private payers both need stronger detection and audit support. Canada and Mexico remain smaller markets, but payer digitization and public sector modernization continue to support adoption in specific workflows tied to claims review and payment control. Procurement in North America is closely linked to compliance, audit readiness, and the need to act on suspicious claims before payment rather than relying only on later recovery efforts.

Europe remained the second-largest regional base in the healthcare fraud analytics market, supported by national insurance systems that already use structured fraud controls and formal review frameworks. France reported a higher level of detected and prevented health insurance fraud in 2025, which shows that public payers are expanding analytical oversight and dedicated anti-fraud activity. Germany also reported its highest tracked billing fraud total and is seeking broader data pooling to improve cross-insurer detection, which points to a wider regional need for shared visibility across fragmented payer structures. The Middle East, Africa, and South America are still early-stage markets, but health system digitization in the Gulf and private insurance development in Brazil are creating a practical base for gradual adoption. These regions are smaller today, yet their path into the healthcare fraud analytics market is becoming clearer as digital claims administration improves and fraud controls become more formalized.

Asia-Pacific is projected to grow at 25.66% CAGR through 2031, and the healthcare fraud analytics market size in the region is rising faster than in any other geography in the study period. The Asian Development Bank said fraud, waste, and abuse account for 30-40% of health insurance claims costs across Asia-Pacific, while 90% of surveyed insurers do not collect ICD or DRG codes, which shows both the scale of the problem and the depth of the data gap. Nature reported that China is advancing digital health governance through a whole-of-society approach, which supports broader use of AI in claims oversight and audit systems as health data infrastructure becomes more coordinated. Growth in this region comes from expanding insurance pools, public digital health programs, and strong pressure to replace manual review with scalable analytics that can work across large beneficiary populations.

Competitive Landscape

The healthcare fraud analytics market is moderately consolidated, with Cotiviti, Optum, and IBM holding strong positions in large payer and government accounts. Their advantage comes from benchmark data, workflow integration, and the ability to support both prepayment and postpayment use cases inside broader payment integrity operations. Cotiviti strengthened its public sector position in May 2025 when its GOV Services unit received CMS Recovery Audit Contractor contracts for Regions 3, 4, and 5, which extended its role in large-scale federal claims review. IBM expanded its healthcare AI portfolio in January 2025 with enhanced predictive analytics modules for payer fraud detection across North America and Europe, showing how large incumbents are deepening product coverage to protect strategic accounts. These moves show that large vendors are expanding through product depth, managed capability, and contract reach rather than relying on price competition alone.

The healthcare fraud analytics market still leaves room for smaller specialists that focus on graph analytics, case explainability, or narrow fraud programs that large suites may not address as deeply. A 2025 paper in Scientific Reports showed that heterogeneous graph neural network models can detect and explain fraud at the medical claim activity level, which is highly relevant where organized rings are missed by line-by-line review methods. That capability matters because many fraud schemes only become visible when providers, patients, locations, treatments, and submission timing are reviewed together. Newer entrants can use this gap to compete in targeted use cases even when enterprise-wide contracts remain concentrated among larger incumbents. This keeps innovation active in the healthcare fraud analytics market even though the biggest revenue pools still sit with established payment integrity vendors.

Managed service delivery is becoming a key competitive lever in the healthcare fraud analytics market, especially among buyers that do not want to build full internal AI and investigation teams. Cognizant said Bupa Hong Kong selected its AI-driven BPaaS solution in December 2025, which shows that buyers are willing to purchase detection, claims automation, and process redesign together. Cotiviti also launched 360 Pattern Review in November 2024 with prepay automation and postpay investigation in one service line, which shows how managed fraud programs are being packaged as operational outcomes rather than only software modules. Competitive position in this market will continue to depend on cross-payer data access, audit-grade workflow design, and the ability to lower false alerts without slowing payment operations.

Healthcare Fraud Analytics Industry Leaders

Change Healthcare

Conduent Incorporated

IBM Corporation

Optum Inc.

Wipro Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ConnectiveRx and EagleForce launched ShieldRx, an AI-driven prepayment detection platform targeting USD 5 billion in annual pharmacy misuse losses. The tool delivers real-time, in-workflow risk scoring with pass or fail decisions in seconds, shifting pharmacy fraud controls upstream for the first time at commercial scale.

- February 2026: CMS established the Fraud Defense Operations Center and launched the CRUSH initiative, which led to the suspension of USD 5.7 billion in suspected fraudulent Medicare payments and 372 law enforcement referrals covering USD 3.7 billion in billing. This marks the largest coordinated analytics-led fraud enforcement action in CMS history.

- February 2025: Bupa Hong Kong selected Cognizant to implement an AI-driven BPaaS solution integrating cloud-native claims automation with fraud, waste, and abuse detection and regulatory compliance tooling. The contract represents Cognizant's first BPaaS deployment in Asia-Pacific, signaling commercial viability of the managed-service model in the region's health insurance sector.

- May 2025: Cotiviti GOV Services was awarded CMS Recovery Audit Contractor contracts for Regions 3, 4, and 5, extending its government analytics mandate and covering a substantial portion of the United States Medicare claims geography.

Global Healthcare Fraud Analytics Market Report Scope

The Healthcare Fraud Analytics Market is a multi-billion dollar sector focused on using artificial intelligence (AI), machine learning, and data mining to detect, prevent, and mitigate fraudulent medical claims.

The Healthcare Fraud Analytics Market is segmented by solution type, deployment mode, application, end user, and geography, reflecting the diverse strategies used to combat fraud across healthcare systems. By solution type, it includes Descriptive Analytics, Predictive Analytics, and Prescriptive Analytics, ranging from retrospective analysis to advanced fraud prevention models. By deployment mode, solutions are offered as On‑Premises or Cloud‑Based, with cloud adoption accelerating due to scalability and cost efficiency. By application, fraud analytics is applied in Insurance Claims Review, Postpayment Review, Prepayment Review, Pharmacy Billing Misuse, Payment Integrity, and Other Applications. By end user, the market serves Healthcare Providers, Insurance Companies, Government Organizations, and Third‑Party Service Providers.

Geographically, the market spans North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia‑Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of Middle East & Africa), and South America (Brazil, Argentina, Rest of South America).

| Descriptive Analytics |

| Predictive Analytics |

| Prescriptive Analytics |

| On-Premises |

| Cloud-Based |

| Insurance Claims Review |

| Postpayment Review |

| Prepayment Review |

| Pharmacy Billing Misuse |

| Payment Integrity |

| Other Applications |

| Healthcare Providers |

| Insurance Companies |

| Government Organizations |

| Third-Party Service Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution Type | Descriptive Analytics | |

| Predictive Analytics | ||

| Prescriptive Analytics | ||

| By Deployment Mode | On-Premises | |

| Cloud-Based | ||

| By Application | Insurance Claims Review | |

| Postpayment Review | ||

| Prepayment Review | ||

| Pharmacy Billing Misuse | ||

| Payment Integrity | ||

| Other Applications | ||

| By End User | Healthcare Providers | |

| Insurance Companies | ||

| Government Organizations | ||

| Third-Party Service Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 size of the healthcare fraud analytics space?

The healthcare fraud analytics market stands at USD 3.23 billion in 2026 and is forecast to reach USD 9.22 billion by 2031 at a 23.36% CAGR.

Which region is growing fastest through 2031?

Asia-Pacific is the fastest-growing region, with a projected 25.66% CAGR through 2031, supported by insurance expansion and digital health investment.

Which solution type leads current demand?

Descriptive analytics led with 61.17% share in 2025 because many payers still rely on historical claims review and pattern-based audit workflows.

Where is the strongest application growth coming from?

Pharmacy billing misuse is growing fastest at 24.06% CAGR, reflecting rising scrutiny of specialty drug claims and the shift toward live prepayment controls.

Why are real-time prepayment controls becoming more important?

Buyers want to stop suspicious claims before payment, and CMS, as well as major vendors, are now pushing upstream fraud prevention into normal payment operations.

What are the main barriers to wider adoption?

The biggest barriers are fragmented data, weak coding capture in some markets, and the ongoing burden of reducing false positives without slowing claim processing.

Page last updated on: