Healthcare Prescriptive Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

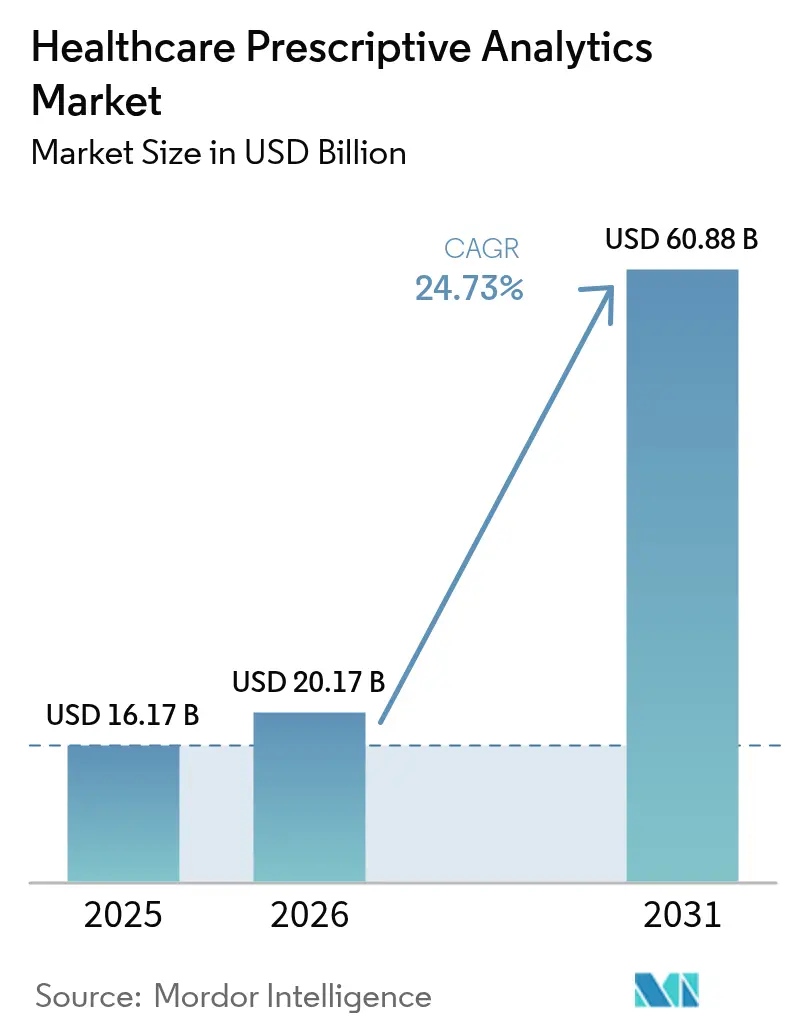

| Market Size (2026) | USD 20.17 Billion |

| Market Size (2031) | USD 60.88 Billion |

| Growth Rate (2026 - 2031) | 24.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Prescriptive Analytics Market Analysis by Mordor Intelligence

Healthcare Prescriptive Analytics market size in 2026 is estimated at USD 20.17 billion, growing from 2025 value of USD 16.17 billion with 2031 projections showing USD 60.88 billion, growing at 24.73% CAGR over 2026-2031.

Growth is propelled by real-time prescription benefit mandates, the rapid uptake of patient digital twins, and the integration of artificial intelligence into everyday clinical workflows. Vendors that pair advanced algorithms with deep clinical workflow knowledge gain an edge, while cloud scalability, hybrid deployment options, and robust security frameworks shape purchasing decisions. Competitive activity intensifies as established electronic health record (EHR) providers race against cloud-native newcomers, and acquisition momentum signals a shift toward integrated analytics platforms.

Key Report Takeaways

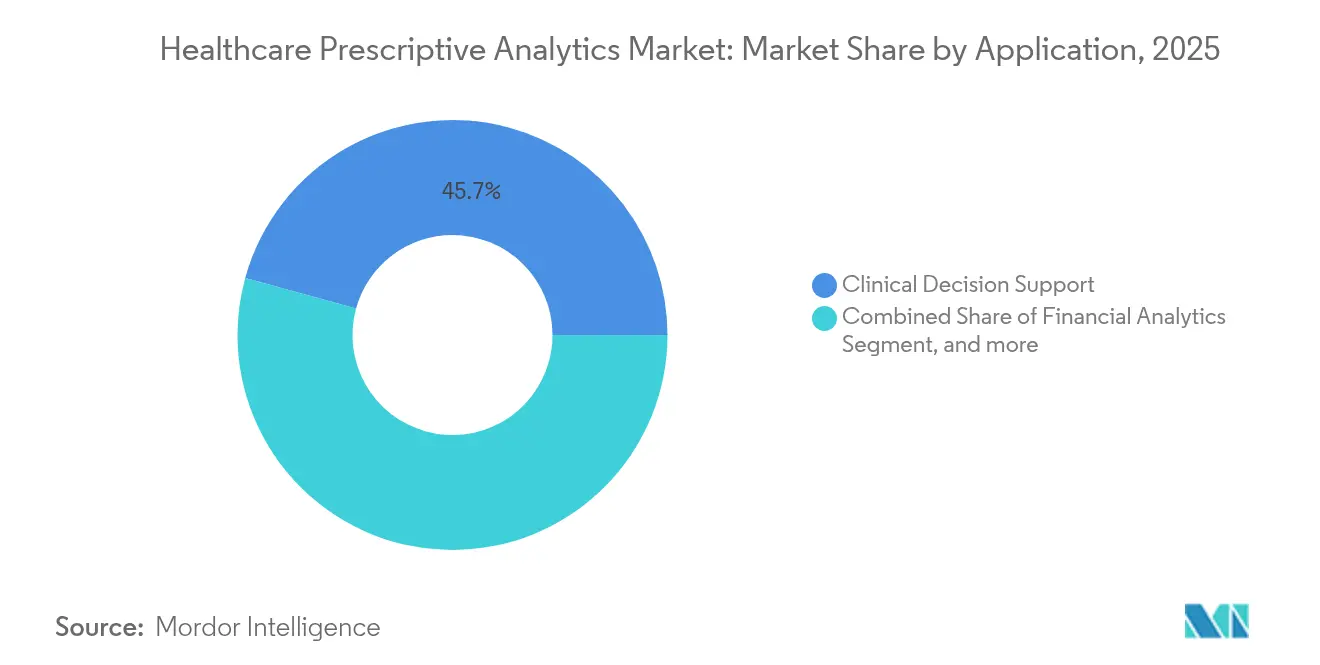

- By application, clinical decision support held 45.72% of the healthcare prescriptive analytics market share in 2025; research & population health analytics is projected to expand at a 26.31% CAGR through 2031.

- By product, services accounted for 63.77% of the healthcare prescriptive analytics market size in 2025 and are advancing at a 26.03% CAGR to 2031.

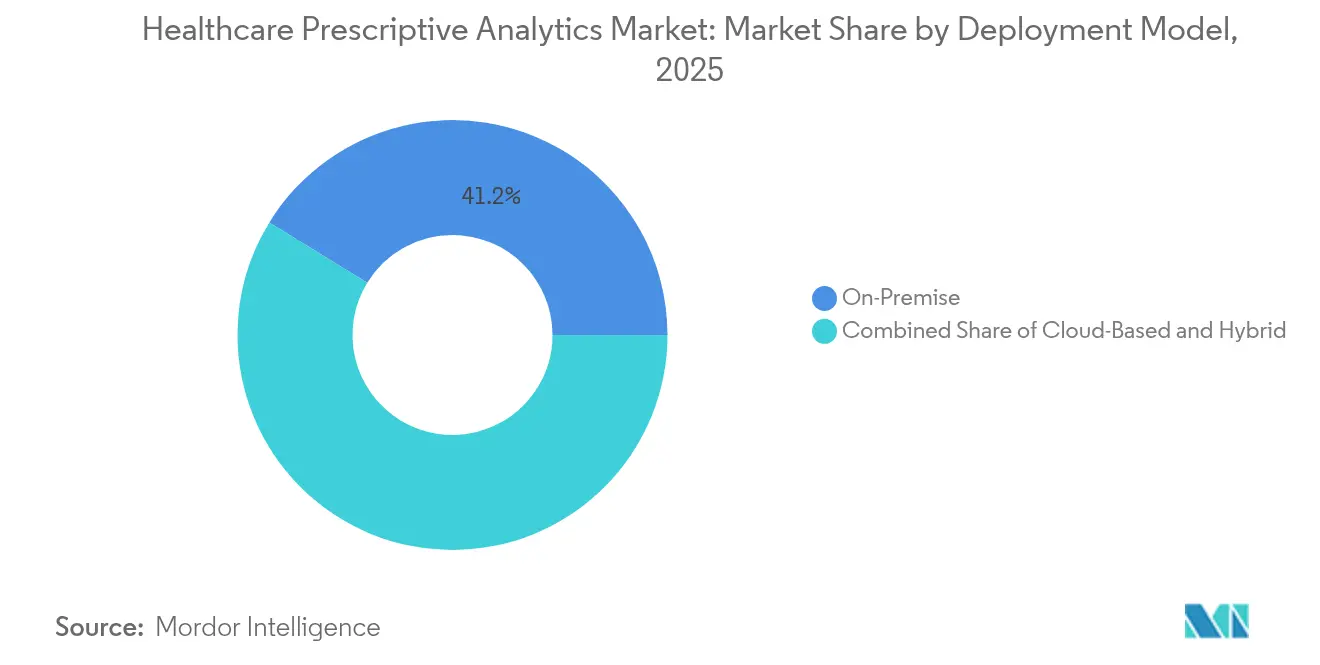

- By deployment model, on-premise solutions led with 41.23% revenue share in 2025, while cloud-based platforms post the highest projected CAGR of 28.33% through 2031.

- By end user, healthcare providers commanded 64.78% of 2025 revenue; pharmaceutical and life-sciences companies recorded the fastest growth, at a 24.93% CAGR.

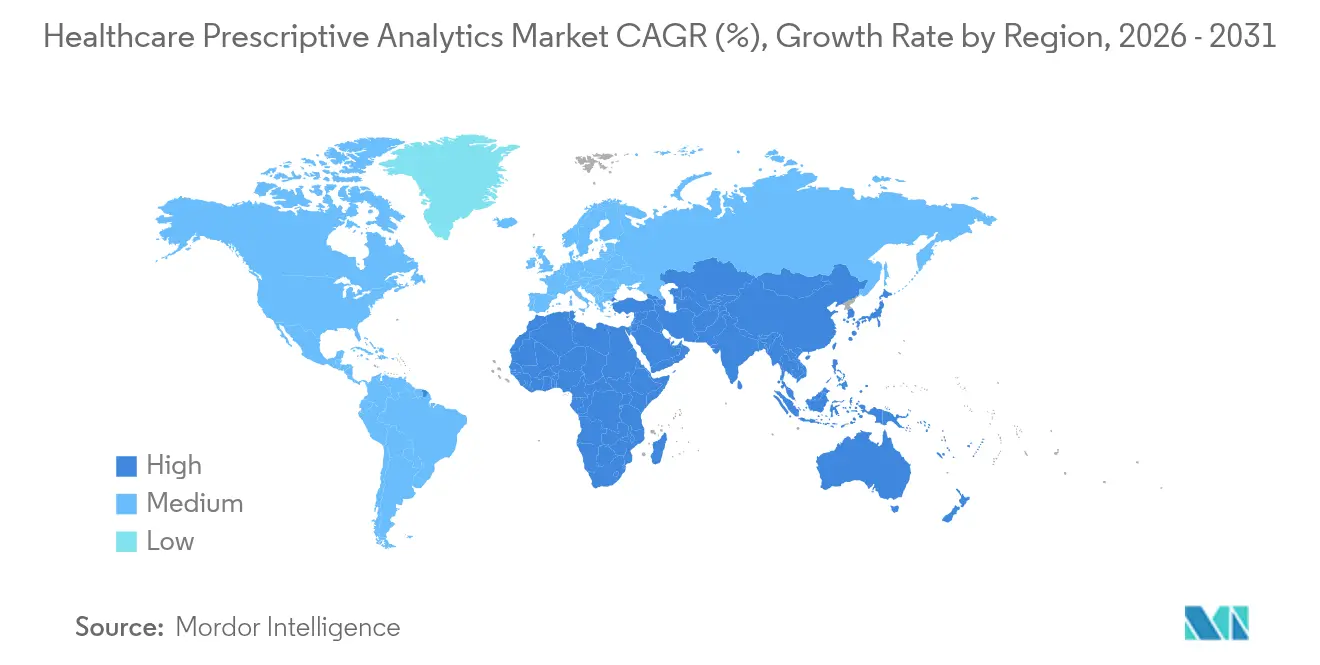

- By geography, North America contributed 40.45% of total revenue in 2025, yet Asia-Pacific is forecast to grow at 29.70% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Prescriptive Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of big data and AI in healthcare | +8.2% | North America and Europe | Medium term (2-4 years) |

| Cost containment and operational efficiency needs | +6.8% | North America | Short term (≤ 2 years) |

| Incentives for value-based care and outcome reimbursement | +5.4% | North America, expanding in Europe | Medium term (2-4 years) |

| Rise of patient digital twins for therapy optimization | +3.7% | North America and Europe | Long term (≥ 4 years) |

| Real-time prescription benefit mandates | +2.9% | United States, spillover to Canada | Short term (≤ 2 years) |

| Growing chronic disease burden | +4.1% | Developed markets worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration of Big Data and AI in Healthcare

Health systems recognize that traditional analytics cannot process the velocity and complexity of genomic data, continuous monitoring feeds, and unstructured clinical notes. Platforms that fuse large-scale data pipelines with artificial intelligence now deliver prescriptive recommendations in real time. Epic Systems’ 2024 release of its AI Trust and Assurance Suite gives hospitals tools to test and monitor algorithm performance before clinical deployment. As these capabilities mature, clinicians transition from retrospective reporting to point-of-care interventions that personalize treatment based on patient-specific risk signals. Early adopters report higher diagnostic accuracy and targeted therapeutic selection, provided data quality and workflow integration hurdles are addressed.

Growing Need for Cost Containment and Operational Efficiency

Labor costs approach 50% of total hospital expenses while patient volumes remain volatile. Prescriptive analytics models shorten revenue-cycle timelines, optimize staffing rosters, and reduce supply chain waste. The American Hospital Association estimates that 25% of U.S. healthcare spending is lost to administrative inefficiencies.[1]American Hospital Association, “Administrative Simplification Studies,” aha.org Real-time location systems coupled with analytics dashboards keep track of beds, clinicians, and high-value equipment, enabling dynamic resource allocation that lowers operational expenses and frees capacity for higher-acuity cases.

Incentives for Value-Based Care and Outcome-Focused Reimbursement

By 2030, the Centers for Medicare & Medicaid Services aims to place every Medicare beneficiary in an accountable care relationship. Organizations in such models already report 30.1% fewer inpatient admissions compared with fee-for-service cohorts.[2]Centers for Medicare & Medicaid Services, “Strategic Plan 2025–2030,” cms.gov To meet stringent quality benchmarks, providers are embedding prescriptive analytics that stratify risk, surface care gaps, and recommend targeted interventions based on social determinants of health. The global expansion of value-based contracts accelerates demand for platforms that couple financial incentives with measurable clinical outcomes.

Rise of Patient Digital Twins for Therapy Optimization

Digital twin technology synthesizes EHR data, wearable sensor feeds, and genomic profiles to create virtual replicas of individual patients. Mayo Clinic’s digital twin pilots illustrate how oncologists can simulate multiple treatment regimens and select the course with the highest projected efficacy.[3]Mayo Clinic Platform, “Digital Twin Initiative,” mayoclinicplatform.org As regulatory confidence in model accuracy increases, digital twins are poised to transform cardiology, oncology, and chronic disease management by forecasting therapy response before initiating treatment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data security and HIPAA/GDPR compliance | -4.3% | Europe and North America | Short term (≤ 2 years) |

| Analytics talent shortage in clinical settings | -3.8% | Worldwide, acute in developing markets | Medium term (2-4 years) |

| Model explainability limits physician trust | -2.9% | Europe | Medium term (2-4 years) |

| High up-front investment costs | -2.1% | Emerging markets, small providers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Security and Compliance Challenges

The European Union’s Artificial Intelligence Act now classifies clinical AI as high-risk, mandating transparency and oversight. Simultaneously, the European Health Data Space regulation approved in March 2025 introduces cross-border sharing rules while preserving patient privacy. These frameworks raise compliance hurdles, forcing vendors to hard-wire audit trails, consent engines, and de-identification modules into analytics platforms. Hospitals that lack robust privacy controls face implementation delays and potential penalties.

Shortage of Analytics Talent in Clinical Settings

Healthcare organizations compete with technology firms for data scientists capable of blending statistical expertise with clinical knowledge. Smaller hospitals often rely on external managed services, elevating deployment costs and slowing internal capability building. Healthcare organizations increasingly compete with technology companies for data science talent, driving up compensation costs and creating retention challenges. The shortage particularly affects smaller healthcare systems that cannot offer competitive packages or advanced analytics career paths. This talent gap forces organizations to rely heavily on external consultants and managed services, increasing implementation costs and creating dependency on third-party expertise. The constraint becomes more pronounced as analytics requirements become more sophisticated, requiring specialized knowledge of clinical workflows, regulatory requirements, and healthcare-specific data challenges that traditional data scientists may lack.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Clinical Workflows Drive Market Leadership

Clinical Decision Support applications generated the most significant revenue in 2025, capturing 45.72% of the healthcare prescriptive analytics market. Hospitals prioritize decision support to reduce medication errors and standardize evidence-based protocols, while funding initiatives such as the U.S. real-time prescription benefit program stimulate adoption at the point of care. Research & Population Health Analytics is the fastest-growing application, expanding at a 26.31% CAGR as payers and providers shift toward proactive, community-level interventions. Population-scale datasets such as Epic Cosmos, which holds de-identified records for more than 246 million individuals, illustrate the scale required to model disease patterns and inform public-health actions.

The convergence of individual-level decision support with population analytics lets organizations derive insights across macro and micro lenses. Integrated platforms that map care pathways for single patients and entire cohorts are increasingly favored, supporting both treatment personalization and regional health-planning efforts.

By Product: Services Dominate Implementation Landscape

Services accounted for 63.77% of the healthcare prescriptive analytics market size in 2025 and are forecast to post a 26.03% CAGR through 2031. Complex regulatory frameworks, legacy EHR environments, and clinician adoption hurdles make implementation know-how more valuable than the underlying software. Software licenses remain essential yet are frequently bundled with long-term advisory and managed services agreements. Hardware spending focuses on high-performance storage and GPUs that support training and inference workloads.

Health systems such as Duke Health have entered multi-year partnerships with analytics vendors to access specialized expertise while reducing internal burdens. These service-oriented models provide hospitals with sustained guidance on model governance, workflow redesign, and change management.

By Deployment Model: Cloud Migration Accelerates Despite Security Concerns

On-premise installations held 41.23% revenue share in 2025, reflecting ongoing anxiety about clinical data security. Yet cloud-based solutions exhibit a 28.33% CAGR as pay-for-use compute, elastic storage, and continuous updates outweigh perceived risks. Hybrid architectures, where sensitive identifiers stay in local data centers while de-identified information processes in the cloud, are now standard. PwC highlights that modernizing electronic health records through cloud services bolsters scalability and enables advanced analytics applications.

Hospitals balancing performance with privacy increasingly adopt zero-trust frameworks and bring-your-own-key encryption to satisfy regulatory mandates while still benefiting from cloud economics.

By End User: Pharma Drives Innovation While Providers Dominate Volume

Providers represented 64.78% of 2025 revenue thanks to extensive patient volumes and the clinical urgency of timely decision support. Pharmaceutical and life-sciences firms, however, achieve a 24.93% CAGR through 2031 as they apply AI to accelerate drug-discovery pipelines and generate real-world evidence. Accenture calculates that AI-enabled discovery can shave several years off traditional timelines, generating profound cost savings. Payers focus on fraud detection and risk adjustment analytics, whereas public-health agencies harness large-scale data to monitor outbreaks and guide policy.

The overlap between clinical and research analytics deepens as pharma uses provider-generated real-world data to validate therapeutic effectiveness, creating symbiotic data-sharing models that amplify demand for secure, interoperable platforms.

Geography Analysis

North America generated 40.45% of global sales in 2025. The United States sets the pace with mandatory real-time prescription benefit implementation scheduled for full rollout by 2027, which embeds analytic rules directly into e-prescribing workflows. Over 620,000 U.S. prescribers already use real-time prescription benefit tools. Canada’s provincial health programs invest in data interoperability, and Mexico’s private hospital chains deploy analytics-enabled revenue cycle platforms to counterbalance rising operating expenses.

Europe prioritizes data privacy and model transparency. The European Health Data Space allocates EUR 810 million to create a secure environment for secondary data use, enabling researchers and clinicians to exchange anonymized datasets across borders. Germany, the United Kingdom, and France devote national funding to hospital digitalization and AI pilots. Compliance with the EU Artificial Intelligence Act spurs demand for audit-ready platforms that log every algorithmic recommendation.

Asia-Pacific is the quickest-expanding region, advancing at a 29.70% CAGR. China’s local governments subsidize AI-enhanced hospital systems, Japan’s aging population drives telemedicine and analytics investment, and India’s National Digital Health Mission underwrites data-exchange infrastructure. Australia and South Korea fund precision-medicine projects that rely on longitudinal datasets, while Singapore acts as a test-bed for regional AI governance frameworks. Brazil’s 2024 Clinical Research Law accelerates approvals for digital health studies, drawing analytics vendors into Latin America.

Regulatory Landscape

In the European Union, regulatory requirements for prescriptive analytics are tightening as clinical AI is treated as high-risk under the EU Artificial Intelligence Act. This expands obligations around transparency, human oversight, and risk management for healthcare deployments. The European Health Data Space regulation (approved March 2025) also formalizes rules for cross-border secondary use of health data, which is pushing vendors and providers to operationalize consent, de-identification, and audit-ready data access to support analytics at scale.

In the United States, oversight spans healthcare IT rules and medical-device style controls when functionality crosses into regulated clinical decision support. FDA guidance has advanced lifecycle-oriented governance for AI-enabled tools, including the final guidance (December 2024) on Predetermined Change Control Plans that allow planned algorithm updates without repeated submissions when adequately pre-specified, alongside continued Total Product Life Cycle expectations aligned with QMSR and ISO 13485:2016. On the health IT side, ONC requirements for certified modules, including Decision Support Intervention transparency and risk management practices, are shaping procurement and documentation needs for prescriptive analytics integrated into EHR workflows.

Competitive Landscape

The healthcare prescriptive analytics market contains a mix of incumbent health-IT providers, cloud hyperscalers, and focused analytics specialists. Epic Systems leverages its dominant EHR footprint to embed AI models inside clinician workflows, while IBM Merative applies natural-language processing to unstructured data. Cloud-native entrants emphasize elastic scalability and microservice architectures, differentiating through rapid deployment cycles and pay-as-you-grow pricing.

Strategic alliances are common. Duke Health’s collaboration with SAS showcases health system–vendor partnerships that combine domain expertise with advanced analytical tooling. Private equity activity signals confidence in scalability: KKR’s USD 11 billion investment in Cotiviti funds expansion into multi-payer analytics solutions. M&A momentum continues as Oracle explores a USD 1 billion purchase of Veradigm and McKesson finalizes its USD 850 million acquisition of PRISM Vision Holdings.

Product roadmaps now focus on model explainability dashboards, synthetic-data generation, and low-code authoring tools to let clinicians craft bespoke rules without programming skills. Vendors that secure robust data-ingestion pipelines, comply with evolving regulations, and embed prescriptive insights into native clinical workflows are positioned to capture long-term share.

Healthcare Prescriptive Analytics Industry Leaders

Allscripts Healthcare Solutions

Oracle Corporation

IBM

McKesson Corporation

Epic Systems Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-by-design analytics is a clear opportunity, particularly when it can be deployed inside certified clinical workflows without introducing new governance bottlenecks. In the United States, the ONC HTI-1 final rule set the Decision Support Intervention (DSI) certification criterion (45 CFR 170.315(b)(11)), requiring developers to provide transparency about the design, development, training, and evaluation of predictive algorithms, and to tie risk practices to Intervention Risk Management aligned with the NIST AI Risk Management Framework. This creates room for vendors that productize model documentation, bias monitoring, and audit trails for health systems adopting AI-enabled decision support at point of care.

Interoperability-driven scale-up is another growth lever where prescriptive recommendations rely on longitudinal, multi-source data. ONC adoption of USCDI v3 within the Health IT Certification Program (effective January 1, 2026) reinforces the need for standardized data capture and exchange, supporting prescriptive analytics that span clinical, operational, and financial use cases across provider networks. As organizations consolidate tools, demand is shifting toward end-to-end architectures that connect structured EHR data with unstructured clinical content, creating space for retrieval-augmented workflows and semantic normalization layers that reduce integration friction and improve traceability of recommendations.

Recent Industry Developments

- July 2026: Cleveland Clinic and IBM announced a 10-year partnership to create a Discovery Accelerator center built around AI and hybrid cloud capabilities. The partnership focuses on enterprise-grade analytics and prescriptive decision support for life sciences and care delivery, combining clinical-scale data assets with advanced compute and model development infrastructure.

- May 2026: Epic Systems launched 20 AI-powered programs, including MyChart agents to guide patients through self-care tasks and automated insurance eligibility checks. By embedding automation into patient access and administrative workflows, Epic broadened how prescriptive analytics can affect operational decisions within the EHR environment.

- September 2024: Oracle Health expanded its platform with voice-enabled command features and biometric logins as part of a broader AI-enabled clinician workflow strategy. The update supports faster interaction with clinical data and is intended to operationalize prescriptive recommendations across care teams.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue earned from prescriptive analytics used in healthcare to recommend actions, not just describe trends. It includes software and related services that turn clinical, operational, and financial data into step-by-step decision guidance used by healthcare stakeholders.

Scope exclusions: We exclude tools that only provide dashboards or descriptive reporting, and models that stop at prediction without recommending an actionable next step.

Segmentation Overview

- By Application

- Clinical Decision Support

- Financial Analytics

- Administrative / Operational Analytics

- Research & Population Health Analytics

- By Product

- Hardware

- Software

- Services

- By Deployment Model

- On-Premise

- Cloud-Based

- Hybrid

- By End User

- Healthcare Providers

- Healthcare Payers

- Pharmaceutical & Life-Sciences Companies

- Government & Public-Health Agencies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with mapping demand signals for healthcare analytics adoption and the surrounding digital health environment, since prescriptive tools are usually sold with broader data and workflow programs. We used public sources such as the World Health Organization, OECD health statistics, Centers for Medicare and Medicaid Services datasets, the US FDA databases (for software guidance and regulated use cases), and peer-reviewed health informatics journals to ground adoption context and definitions.

We also reviewed public company filings, investor presentations, association websites, and reputable press coverage to understand purchasing patterns, typical contract structures, and how revenues are recognized across software and services. In parallel, we referenced paid subscriptions used for company financials and intelligence, news and financials, and patent databases to cross-check product positioning and the timing of new capability launches. These examples are not exhaustive, and many other public and paid sources were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what buyers count as prescriptive analytics in real procurement processes, and how spend splits between platform licenses, implementation, and ongoing managed services. We spoke with a mix of healthcare providers, payers, and solution delivery experts across APAC, EMEA, and the Americas, so assumptions on adoption pace, pricing, and usage intensity could be checked and then aligned to the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 13% | APAC: 45% |

| Mid tier: 45% | Functional/Unit leaders: 33% | EMEA: 29% |

| Smaller Players: 21% | Managers: 54% | Americas: 26% |

Market-Sizing & Forecasting

The core sizing started with a top-down approach where healthcare analytics spending pools and digitization readiness indicators were reconstructed by region, then filtered to the prescriptive layer using adoption and use-case intensity inputs. After the first pass, the totals were corroborated using selective bottom-up checks, including sampled vendor revenue exposure, typical deal values, and estimated active-customer counts in key end-user groups.

Inputs used in the model included hospital and payer digital investment direction, cloud adoption in healthcare IT, the share of analytics programs that include optimization or workflow recommendations, implementation effort levels, and average pricing progression for subscription and services over time. Where bottom-up evidence was thin for smaller geographies, gaps were handled through regional peer proxies, then rechecked with interview feedback before being carried into the final roll-up.

For forecasting, we used scenario analysis supported by expert consensus on how quickly prescriptive analytics penetrates clinical, operational, and financial workflows. Growth rates were adjusted by region based on policy direction, data interoperability progress, and measured uptake of advanced analytics capabilities, then stress-tested so the projected curve stayed consistent with realistic budgeting cycles.

Data Validation & Update Cycle

Validation was done through triangulation across independent signals so that single-source bias did not drive the final number. Outputs were checked against proxy indicators like enterprise analytics budgets, healthcare IT spending direction, and observed pricing ranges, and then anomalies were flagged for deeper review before sign-off.

A multi-step internal review was followed, and re-contact triggers were used when a key assumption moved outside expected bounds, such as sudden pricing shifts, regulatory changes affecting data use, or a step change in cloud adoption. Reports are refreshed annually, with interim updates for material events, and a final pre-delivery pass completed so clients receive the most current view available.

Mordor Intelligence's Global Healthcare Prescriptive Analytics Market Market Size Measured Against Other Published Estimates

Published market values for healthcare prescriptive analytics can look far apart because each publisher draws the boundary differently and applies different timing for adoption and pricing changes. In many cases, the gap is created by what is counted as prescriptive, what gets bundled with broader analytics, and how services revenue is treated.

In this market, key gap drivers usually include whether decision-optimization workflows are required for inclusion, whether adjacent predictive-only tools are counted, and whether implementation and managed services are included at full value. Currency conversion timing, the choice of base year, and how fast ASPs are assumed to rise with cloud delivery can also move the final value by a noticeable amount.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 20.17 B (2026) | |

| Industry Publisher A | USD 3.60 B (2023) | Uses an earlier base year and is commonly interpreted as a narrower demand pool, which can happen when only select use cases or buyer groups are counted and broader service revenues are not fully captured. |

| Global Publisher B | USD 12.90 B (2024) | The estimate is anchored to a different base year and may apply a different inclusion rule for what qualifies as prescriptive versus predictive-only analytics, which shifts the counted revenue and the implied adoption level. |

Signals such as the observed expansion in enterprise healthcare analytics budgets and verified uptake of optimization-led workflow deployments are the checks that keep Mordor Intelligence tied to a prescriptive-only revenue pool that includes related services when they are delivered as part of actionable decision support. Taken together, the table suggests that year selection and category boundaries are the biggest drivers of spread, so using clear inclusion rules and repeatable demand indicators helps keep the outcome stable and easy to audit.

Key Questions Answered in the Report

What is the current size of the healthcare prescriptive analytics market?

The market is valued at USD 20.17 billion in 2026.

How fast will the market grow through 2031?

Revenue is projected to reach USD 60.88 billion by 2031, representing a 24.73% CAGR.

Which application contributes the most revenue?

Clinical Decision Support led with 45.72% of 2025 revenue.

Which region is expanding the quickest?

Asia-Pacific is forecast to grow at 29.70% CAGR through 2031.

Why are services so dominant in spending?

Successful deployments hinge on domain expertise, change management, and regulatory compliance, making services the preferred investment.

What major regulatory trend affects adoption?

The EU Artificial Intelligence Act classifies clinical AI as high-risk, driving demand for transparent, explainable analytics platforms.

Page last updated on: