People Analytics In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

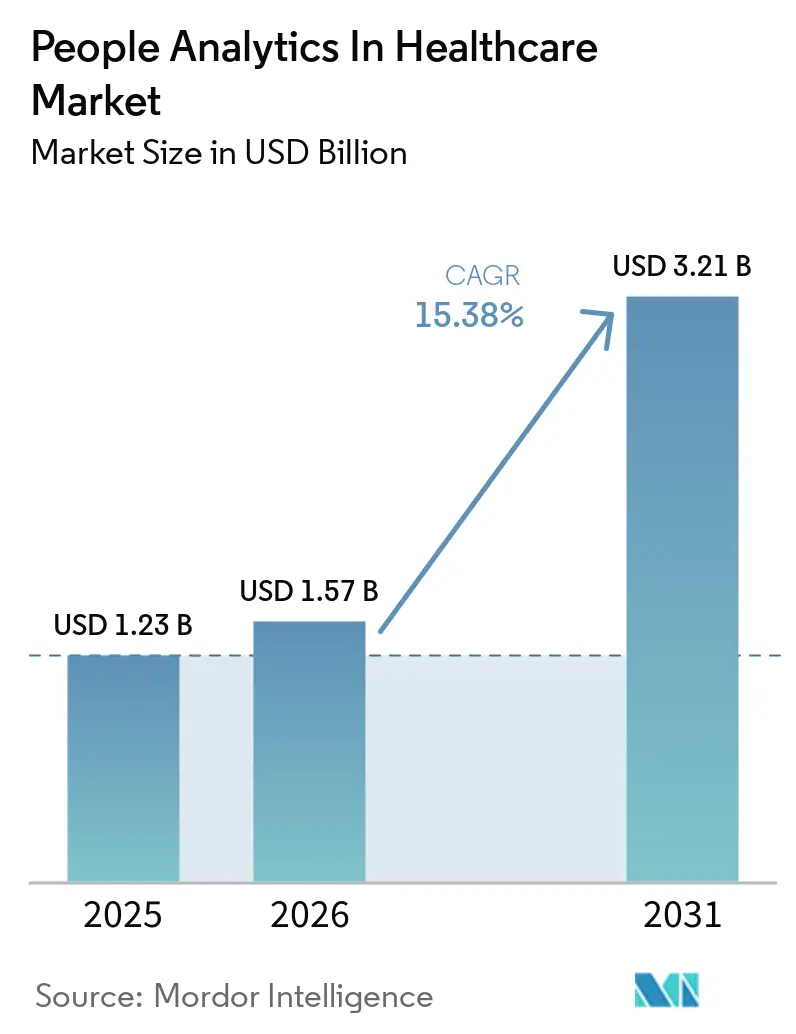

| Market Size (2026) | USD 1.57 Billion |

| Market Size (2031) | USD 3.21 Billion |

| Growth Rate (2026 - 2031) | 15.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

People Analytics In Healthcare Market Analysis by Mordor Intelligence

The people analytics market in healthcare is projected to expand from USD 1.23 billion in 2025 and USD 1.57 billion in 2026 to USD 3.21 billion by 2031, registering a CAGR of 15.38% between 2026 and 2031. The people analytics in the healthcare market is moving up the priority list for health systems because workforce costs now absorb a very large share of operating budgets, and margins remain under pressure. Adoption is also rising because provider organizations need better visibility into staffing patterns, overtime, retention risk, and compliance exposure across multi-site care networks. Cloud-linked workforce platforms are gaining traction as providers seek to connect payroll, scheduling, credentialing, and performance data into a single operating view. Competition is shifting as large HCM vendors bundle analytics into broader workforce suites, while healthcare-focused vendors continue to win on clinical workflow depth and healthcare-specific configurability. Demand is also expanding beyond major hospitals as smaller providers, home-based care organizations, and distributed care settings seek shared analytics infrastructure to support workforce planning without large in-house data teams.

Key Report Takeaways

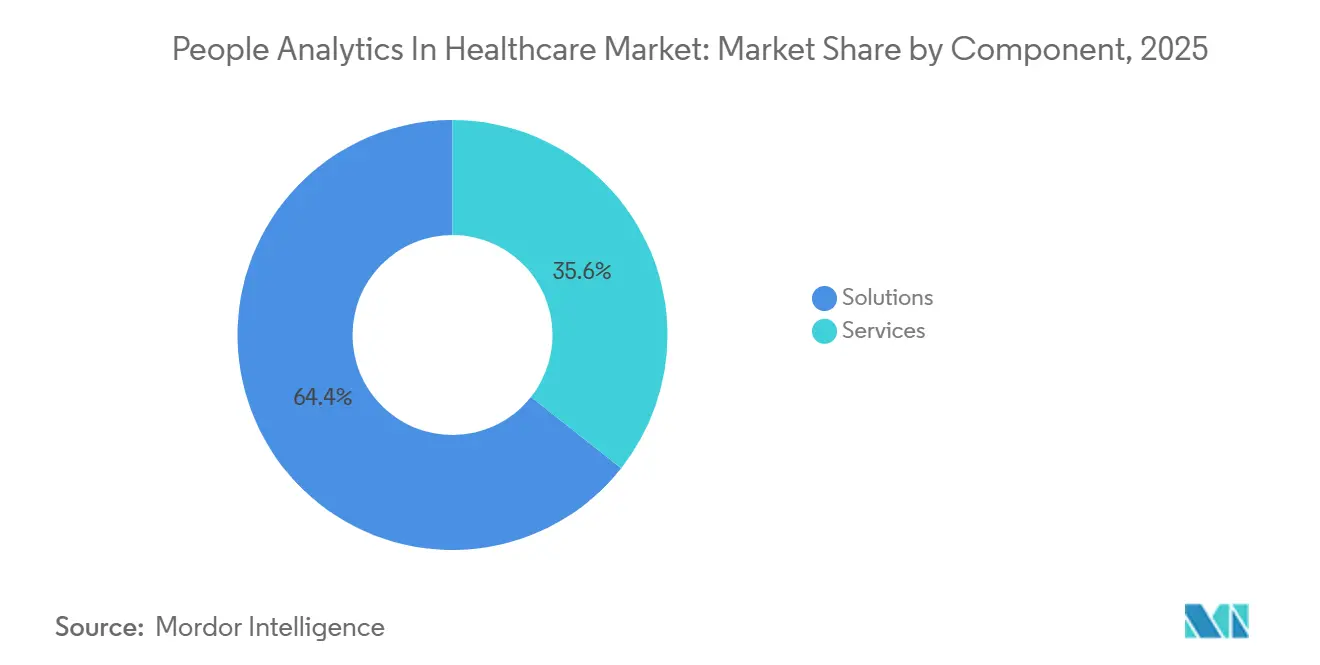

- By component, software led with 64.37% share in people analytics in the BFSI space in 2025, while services are projected to expand at a 16.47% CAGR through 2031.

- By deployment model, cloud-based deployment held 69.41% share in 2025, while hybrid deployment is projected to grow at a 17.63% CAGR through 2031.

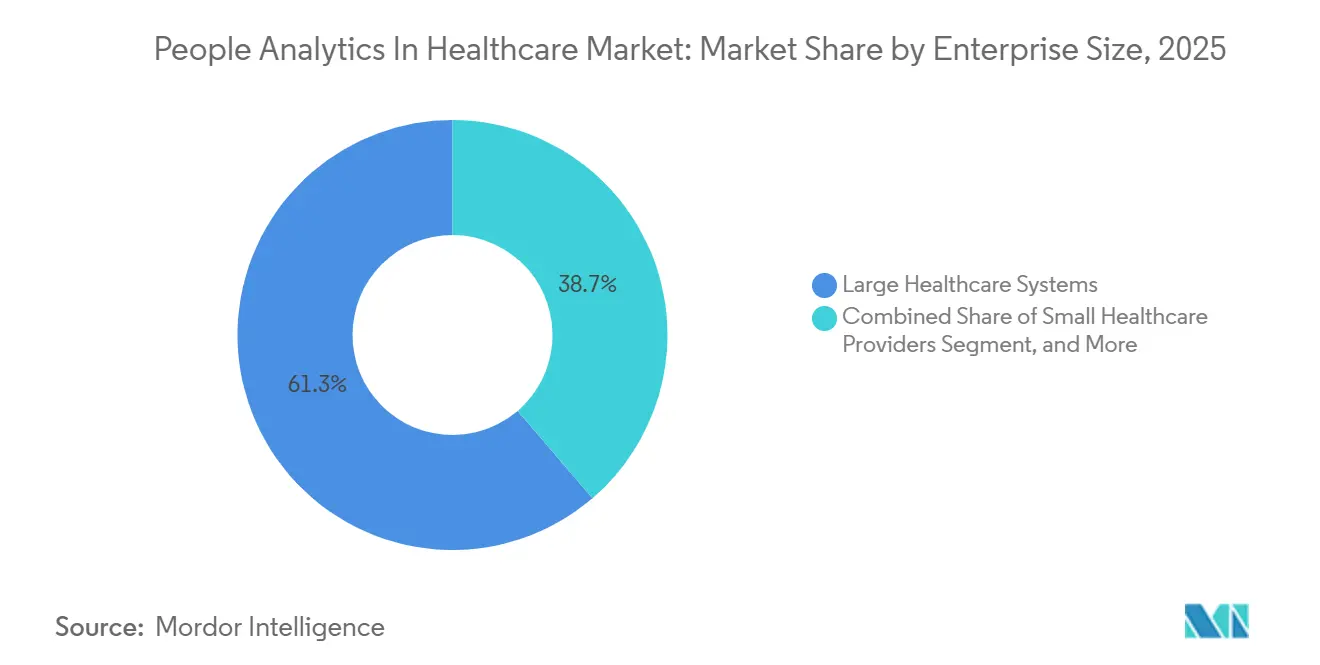

- By enterprise size, large healthcare systems accounted for 61.29% of the market in 2025, while small healthcare providers are projected to grow at a 18.21% CAGR through 2031.

- By solution module, workforce management and scheduling analytics captured 24.87% share in 2025, while labor cost, time, and attendance analytics are projected to grow at a 19.17% CAGR through 2031.

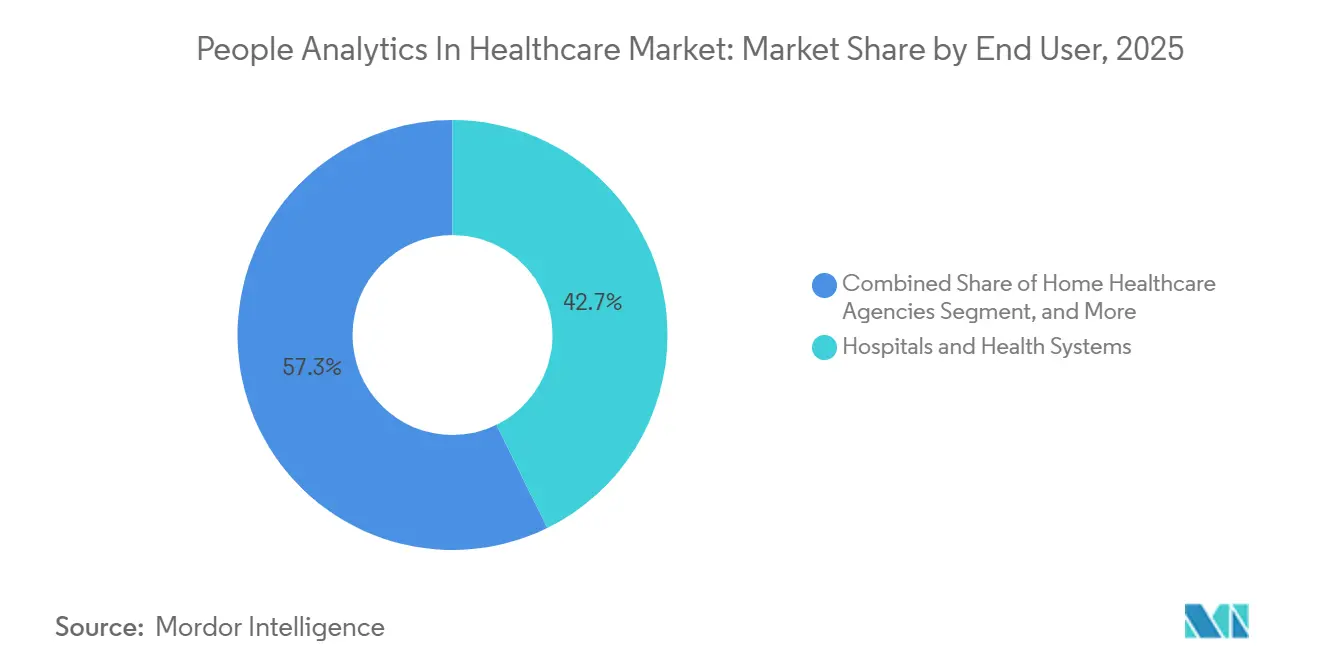

- By end user, hospitals and health systems accounted for 42.73% of the market in 2025, while home healthcare agencies are projected to expand at a 16.39% CAGR through 2031.

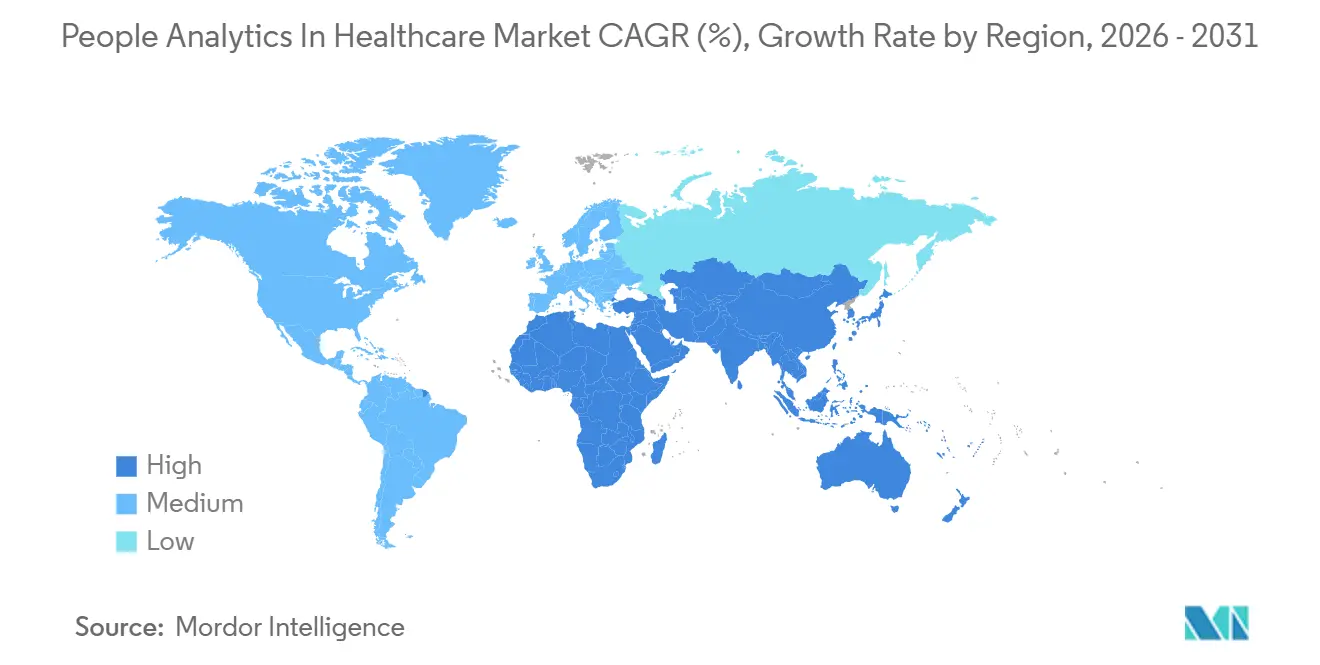

- By geography, North America held 38.43% of the people analytics market share in healthcare in 2025, while Asia-Pacific is projected to expand at a 17.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global People Analytics In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Healthcare Labor Cost Pressures | +3.8% | Global, with highest intensity in North America and Western Europe | Short term (= 2 years) |

| Persistent Clinical Workforce Shortages and Burnout | +3.2% | Global, acute in North America, EU, and South-East Asia | Medium term (2-4 years) |

| Growing Need for Regulatory Compliance and Safe Staffing Visibility | +2.4% | North America and EU core, spillover to Australia and New Zealand | Short term (= 2 years) |

| Accelerating Cloud-Based Workforce Platform Adoption | +2.1% | Global, led by North America and APAC core | Medium term (2-4 years) |

| Expansion of Internal Float Pools and Skills-Based Deployment Analytics | +1.6% | North America and Western Europe | Medium term (2-4 years) |

| Real-Time Clinician Credential Data Networks Improving Workforce Planning | +1.2% | North America, with early traction in EU and APAC | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Rising Healthcare Labor Cost Pressures

The people analytics in the healthcare market is benefiting from the fact that labor now sits at the center of financial recovery plans across provider organizations. Workforce costs accounted for 60% of total U.S. hospital expenses in 2025, and aggregate labor spending exceeded USD 1 trillion, up 5.6% and outpacing hospital price growth.[1]American Hospital Association, “Costs of Caring: Challenges Facing America's Hospitals as They Care for Patients in 2026,” American Hospital Association, aha.org U.S. hospital labor expenses rose 10.1% between Q4 2023 and Q4 2025, while benefits expense per adjusted patient day increased 12% over the same period. Larger systems carried even more pressure, with organizations above USD 1 billion in net operating revenue reporting 16% growth in benefits costs alone. This gap between reimbursement growth and wage inflation is pushing health systems toward shift-level productivity analysis, premium labor reduction, and float pool optimization, which are core use cases for people analytics in the healthcare market. Half of hospital finance leaders identified labor as a top 2026 priority, supporting continued investment in workforce analytics as a financial control tool rather than solely an HR reporting layer.

Persistent Clinical Workforce Shortages and Burnout

People analytics in the healthcare market is also benefiting from the continued shortage of clinicians across multiple workforce categories. Projections show a shortfall of 187,130 full-time equivalent physicians by 2037, and 302,440 LPN positions, equal to a 36% shortage, will go unfilled.[2]Health Resources and Services Administration, “State of the U.S. Health Care Workforce, 2024,” HRSA, hrsa.gov By 2029, nearly 40% of the nursing workforce intends to leave or retire, with 41.5% citing stress and burnout as the main reason. Burnout-driven attrition is estimated to cost healthcare systems at least USD 36,918 per nurse each year in replacement costs, further strengthening the case for retention and engagement analytics. The global nursing shortage is expected to narrow only to 4.1 million by 2030, indicating that supply pressure will remain a long-term demand driver for people analytics in the healthcare market. As a result, providers are treating predictive turnover tracking, staffing resilience analysis, and burnout monitoring as operational capabilities that support continuity of care as much as labor efficiency.

Growing Need for Regulatory Compliance and Safe Staffing Visibility

People analytics in the healthcare market is increasingly tied to compliance, as staffing regulations now require auditable workforce visibility. In May 2024, minimum staffing rules required long-term care facilities to deliver 3.48 nursing hours per resident day and maintain 24/7 registered nurse coverage, affecting more than 79% of U.S. nursing facilities at the time. Maryland’s Safe Staffing Act of 2026 requires licensed hospitals to establish clinical staffing committees and implement evidence-based staffing plans, with reporting beginning in 2030. New Mexico’s 2026 Safe Staffing Act further requires the collection and publication of retention rates, traveler nurse use, vacancy data, and turnover statistics beginning in July 2026. Staffing data has also been linked to public reporting and value-based purchasing, making workforce compliance visible to regulators, patients, payers, and investors simultaneously. That shift is pushing people analytics in the healthcare market toward real-time dashboards, evidence-based staffing reports, and governance-ready documentation, rather than delayed, retrospective reporting.

Accelerating Cloud-Based Workforce Platform Adoption

People analytics in the healthcare market is moving toward cloud-linked operating models because disconnected workforce data is hard to use at scale. In 2026, new platforms were launched on major cloud providers to create a single, canonical data model across HR, pay, and scheduling, with more than 1,000 organizations already live and another 1,000 in migration.[3]Google Cloud, “How UKG Taps Workforce Intelligence with the Agentic Data Cloud,” Google Cloud Blog, cloud.google.com Other vendors expanded unified workforce platforms and reported that predictive tools reached up to 96% accuracy in forecasting patient volume and staffing needs 120 days in advance. These examples show why providers are adopting cloud layers that can unify scheduling, payroll, staffing, and engagement signals without waiting for full replacement of older systems. National health authorities have also reinforced this direction by supporting facilities that implemented workforce management tools across hundreds of public health establishments. Even when providers retain on-premises EHR environments, they are still adopting cloud analytics overlays, which help expand people analytics in the healthcare market through hybrid deployment rather than only through full cloud migration. The result is a broader installed base for analytics platforms that can work across multiple data estates while still supporting healthcare-specific governance rules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Cybersecurity Risks in Employee and Payroll Data | -1.8% | Global, highest risk exposure in North America and EU | Short term (= 2 years) |

| Complex Integration with EHR, Payroll, and Legacy HRIS Systems | -1.5% | Global, most acute in fragmented health systems in APAC and South America | Medium term (2-4 years) |

| Algorithmic Bias and HR AI Governance Scrutiny | -0.9% | North America and EU, emerging in APAC | Medium term (2-4 years) |

| Employee Monitoring Backlash in Clinical Workflows | -0.6% | North America and Western Europe | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Cybersecurity Risks in Employee and Payroll Data

People analytics in the healthcare market faces a significant adoption constraint because workforce platforms consolidate sensitive employee, payroll, and credential data in a single environment. Healthcare payroll and HR vendor-related cyberattacks increased 400% over two years, while third-party vendor breaches rose from 10% in H1 2019 to 21% in H1 2023.[4]Censinet, “Healthcare Payroll and HR Vendor Risk Management: Employee Data Protection,” Censinet, censinet.com These incidents affected an average of 304,191 individuals per breach, which helps explain why procurement teams are increasing scrutiny of workforce technology vendors. In the people analytics in healthcare market, this means security reviews are becoming more thorough, subcontractor oversight is becoming more detailed, and vendor access controls are receiving greater weight in purchase decisions. Providers also now recognize that a compliant Business Associate Agreement does not remove supply-chain exposure when multiple software layers touch employee information. This security burden does not stop adoption, but it does slow deal cycles and increase the importance of vendors with strong security governance and cleaner integration architectures.

Complex Integration With EHR, Payroll, and Legacy HRIS Systems

People analytics in the healthcare market also face friction due to the difficulty of linking workforce, payroll, and clinical systems that were not built to operate together. A 2025 systematic review identified semantic misalignment, lack of API standardization, and fragmented cross-system exchange as core blockers in building digital health data integration ecosystems. That challenge is especially relevant when scheduling signals must be combined with HCM, payroll, and credential data inside healthcare settings that still rely on older enterprise applications. A 2025 study found that 95% of HR and IT professionals in surveyed districts cited unreliable high-speed internet as a major barrier, while 86% cited a lack of uninterrupted power supply. People analytics in the healthcare market, therefore, expand faster in organizations that already have a stable digital infrastructure and more slowly in settings where basic connectivity and interoperability remain unresolved. Vendors are responding with pre-built connectors and standards-based data layers, but integration complexity still stretches deployment timelines, raises implementation costs, and limits near-term penetration in fragmented provider environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Retains Leadership While Services Gain Ground on Execution Needs

Software held 64.37% of the component segment in 2025, giving it the largest market share within the people analytics in healthcare market by component. This dominance reflects the fact that scheduling engines, retention models, compliance dashboards, and forecasting tools comprise the core system layer for workforce decision-making in healthcare organizations. In many provider settings, software became the first practical way to standardize labor visibility across sites, departments, and clinician groups. The software base also benefits from recurring subscription models, faster update cycles, and tighter integration with payroll and HR records than service-only engagements can provide. As the people analytics in the healthcare market has matured, software has remained the starting point for adoption because providers generally buy a platform before they scale advisory or optimization support.

Services are projected to expand at a 16.47% CAGR during 2026-2031, making them the fastest-growing component, even though software remains larger. This reflects a clear shift in buyer behavior, because many health systems now want implementation, benchmarking, training, and model-tuning support alongside their licenses. In 2026, half of hospital finance leaders prioritized productivity governance and labor benchmarking, and those goals usually require continuous advisory support rather than a one-time system launch. One Midwest health system improved employee net promoter scores over 3 years and maintained average staff tenure at 3-4 times the industry norm through a sustained analytics-led workforce program. That pattern supports hybrid software-plus-services models inside the people analytics in healthcare market, where buyers increasingly pay for execution support that helps turn platform data into measurable retention, productivity, and staffing outcomes.

By Deployment Model: Cloud Leads Adoption While Hybrid Grows Faster on Practical Integration Needs

Cloud-based deployment accounted for 69.41% of the people analytics market in healthcare in 2025, making it the leading deployment model. Health systems favored cloud platforms because they reduce local infrastructure burden, support multi-site visibility, and let vendors deliver updates faster. Cloud delivery also aligns with the need to unify data across scheduling, payroll, credentialing, and workforce engagement layers that are often spread across separate systems. The dominance of cloud shows that buyers now see SaaS delivery as the most efficient path for workforce analytics at scale. It also reflects the broader movement in the healthcare people analytics market toward operating models that support continuous analytics rather than periodic manual reporting.

Hybrid deployment is projected to grow at a 17.63% CAGR during 2026-2031, which indicates that many organizations are not moving in a single step from legacy systems to fully cloud-native architectures. Instead, they are keeping on-premises EHR or HR systems in place while adding cloud analytics layers that can federate and analyze data across existing environments. New platforms illustrate why hybrid-ready architectures are gaining strategic value by connecting previously separated HR, pay, and scheduling data into unified models. National health authorities have also shown that workforce digitalization can advance through staged adoption paths rather than complete infrastructure replacement. On-premises deployment remains relevant in data-sensitive environments, but the people analytics market in healthcare is increasingly shaped by buyers who want cloud flexibility without forcing immediate change across every legacy system.

By Enterprise Size: Large Systems Hold Scale Advantages While Small Providers Post Faster Growth

Large healthcare systems accounted for 61.29% of the enterprise-size segment in 2025, indicating that the people analytics market in healthcare remains anchored by organizations with complex staffing and larger IT budgets. These systems manage high-volume labor data across hospitals, clinics, service lines, and regional campuses, making it easier to justify the value of centralized workforce analytics. They also have stronger negotiating power with enterprise vendors and more internal resources for implementation, governance, and change management. Systems with more than USD 1 billion in net operating revenue reduced management headcount by 1.9% while increasing patient-facing staff headcount by 2.1%, suggesting the operational importance of analytics-guided workforce redesign. As a result, large systems continue to provide a stable revenue base for people analytics in the healthcare market and remain key reference customers for platform vendors.

Small healthcare providers are projected to grow at a 18.21% CAGR during 2026-2031, making them the fastest-rising enterprise-size group. Their growth is tied to a practical need for automation, as documentation, scheduling, and staffing compliance tasks scale poorly when handled manually. Staffing rules and related reporting requirements have increased the need for auditable workforce records across care settings, even in organizations without deep analytics teams. Modular SaaS pricing is also lowering entry barriers, which lets smaller operators adopt targeted capabilities such as scheduling analytics, overtime control, and credential visibility without large capital spending. Mid-sized organizations sit between these two groups and often expand through shared services or phased deployment models. That creates a broader buyer base for people analytics in the healthcare market, as adoption is no longer limited to large integrated delivery networks.

By Solution Module: Scheduling Analytics Leads While Labor Cost Analytics Advances Fastest

Workforce management and scheduling analytics held the largest share of the solution module at 24.87% in 2025, indicating this category accounted for the largest slice of the people analytics market at the module level. Scheduling sits at the center of workforce operations, so it is often the first area where providers seek better data quality, staffing visibility, and labor control. It is also one of the few workforce datasets that many providers digitized early, even when broader analytics maturity remained limited. That early digital footprint helped scheduling analytics become the operational foundation for coverage management, shift balancing, and safe staffing execution. The people analytics in the healthcare market, therefore, continues to rely on scheduling tools as the gateway module through which providers expand into broader retention, compliance, and workforce intelligence use cases.

Labor cost, time, and attendance analytics are projected to grow at a 19.17% CAGR during 2026-2031, making it the fastest-growing module. One reason is that the shift away from contract labor has made employee compensation and benefits costs more important to measure in detail. Median contract hours per adjusted patient day fell 29% between 2023 and 2025, which moved more staffing costs back into employed labor lines that require tighter tracking and forecasting. Burnout and workforce stability are also related modules, because 41.5% of nurses planning to leave cited stress and burnout, while physician burnout fell from 63% in 2021 to 48.2% in 2023. This means people analytics in the healthcare industry is expanding across both operational and forward-looking modules, with labor cost visibility, burnout monitoring, predictive planning, and workforce risk analysis converging in a single decision environment.

By End User: Hospitals Remain the Core Buyer Group While Home Healthcare Agencies Expand Rapidly

Hospitals and health systems accounted for 42.73% of end-user demand in 2025, keeping them in the lead in the people analytics in healthcare market. Their leadership is tied to scale, regulatory burden, and the high financial cost of poor staffing decisions in inpatient settings. Large health systems run complex rosters across nursing, allied health, physicians, and support staff, so even small errors in scheduling or overtime control can affect quality and margins. They also face the most visible scrutiny from regulators, boards, payers, and the public on issues such as turnover, staffing adequacy, and care continuity. As a result, hospitals continue to anchor the installed base of people analytics in the healthcare market and often shape product design across the rest of the sector.

Home healthcare agencies are projected to grow at a 16.39% CAGR during 2026-2031, making them the fastest-growing end-user segment. Growth in this group reflects the shift toward distributed care delivery, where providers must coordinate staff across homes, communities, and decentralized service locations. These organizations need strong scheduling, travel optimization, credential validation, and workforce visibility because their labor model is inherently more dispersed than the hospital model. Long-term care and skilled nursing facilities also remain important buyers because minimum staffing rules and related turnover measures have made workforce documentation and staffing compliance much more demanding. Outpatient visits rose 9.8% in 2025, supporting broader demand in ambulatory and community-based settings that are managing higher care volumes with limited staffing resources. This shift broadens the people analytics in the healthcare market beyond inpatient providers and creates room for vendors that can support workforce planning across hospital, home-based, and non-acute care environments.

Geography Analysis

North America held 38.43% of the people analytics market share in healthcare in 2025, making it the largest regional market. The region leads because it combines large integrated delivery networks, a dense vendor ecosystem, and rising regulatory pressure on staffing visibility. Minimum staffing rules have already turned workforce reporting into a high-priority issue for long-term care providers, and state legislation is extending similar expectations into hospital settings. Vendor penetration is also deep, with nearly 90% of the largest U.S. healthcare systems using leading workforce analytics solutions, and more than 4,500 healthcare organizations reported by major providers. This maturity means the people analytics in the healthcare market in North America is moving from basic adoption toward deeper integration, AI-enabled forecasting, and governance-focused reporting.

Europe remains a strategically important second-tier region for people analytics in the healthcare market because workforce reporting and public-sector staffing oversight are becoming more formalized. France’s national workforce reporting framework covers 171 indicators across public hospital establishments, supporting demand for systems that can produce repeatable, audit-ready workforce reporting. A 2025 European policy review found that 23 of 33 EU member countries had legislation or formal policy on safe staffing, but only 9 used a nationally approved staffing calculation methodology, leaving room for analytics tools that can standardize planning approaches. Switzerland’s national nursing staff monitoring initiative also shows that workforce analytics outputs are increasingly expected to support public policy, not only hospital management decisions. The region, therefore, offers steady demand for vendors that can align workforce analytics with public reporting, safe staffing policy, and local data governance requirements.

Asia-Pacific is projected to grow at a 17.89% CAGR during 2026-2031, which makes it the fastest-growing region in the people analytics in healthcare market. The global average stood at 37.1 nurses per 10,000 population, with a tenfold gap between high-income and low-income countries, and workforce shortages remain a structural issue across health systems. This gap is pushing providers to automate planning, retention tracking, and skills deployment as demand rises amid an aging population and uneven clinician supply. The commercial opportunity is strongest where healthcare delivery is expanding, but workforce planning is still moving from basic operational reporting toward predictive analytics. South America is still earlier in adoption, but governance reforms and institutional workforce planning needs are creating a foundation for future demand. The Middle East is also generating interest through healthcare capacity expansion and workforce localization programs, while Africa remains an early-stage opportunity with commercial potential concentrated in more urbanized private care markets. Across these regions, the people analytics in the healthcare market will expand first in organizations that can combine staffing pressure with enough digital infrastructure to support integrated workforce data.

Competitive Landscape

The people analytics in the healthcare market remains moderately concentrated at the top and fragmented across the middle tier. A small group of vendors holds a strong position in large provider organizations because they can connect scheduling, payroll, compliance, and workforce planning in broader suites. At the same time, the market still includes specialized firms that compete through focused clinical depth or differentiated analytics capabilities. This structure means buyers often choose between breadth and specialization rather than between a few near-identical platforms. It also means the people analytics in the healthcare market continues to reward vendors that can show both healthcare workflow relevance and credible integration depth.

One of the strongest strategic moves in the current cycle was the launch of a unified workforce data platform in April 2026, which consolidated more than 12,000 database instances into a common model and was already serving more than 1,000 live organizations. Another major vendor responded with a certified HCM integration in May 2026, giving healthcare providers a tighter link across HR records, scheduling, timekeeping, and payroll. These moves show that the people analytics in the healthcare market is increasingly being shaped by ecosystem strategy, where interoperability and shared data models matter as much as standalone analytics features. They also raise the competitive bar for smaller vendors that must now prove they can fit into broader enterprise workflows.

Another visible trend is that vendors are embedding analytics into day-to-day work rather than keeping insights inside separate dashboards. Recent updates have enabled workforce intelligence to be accessed within enterprise AI search environments, suggesting a more embedded usage model. Other providers are moving in a similar direction by combining workforce planning, scheduling, and automation within unified operating environments for healthcare organizations. Industry consolidation also signals that healthcare-specific workforce platforms have strategic value beyond organic growth alone, especially when they hold strong positions in clinical scheduling and provider operations. The remaining white space in the people analytics in healthcare market is strongest in non-hospital environments, such as home health, senior living, and community-based care, where many platforms still lack vertical depth. Over time, compliance expectations, AI governance rules, and enterprise integration demands are likely to favor vendors with stronger capital, broader partner ecosystems, and a proven ability to operate in sensitive healthcare data environments.

People Analytics In Healthcare Industry Leaders

QGenda, LLC

symplr software LLC

UKG Inc.

RLDatix Holdings Limited

WorkForce Software, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: QGenda announced a certified integration with Workday Human Capital Management, creating a unified workforce ecosystem that links employee records, scheduling, timekeeping, and payroll for over 4,500 healthcare organizations. The integration, available via the Workday Marketplace, directly reduces premium labor cost exposure and strengthens compliance auditing capabilities.

- May 2026: Symplr was named a U.S. Best Managed Company for the third consecutive year, and received a Gold Stevie Award for its Operations Platform and MedTech Breakthrough recognition for Smart Square, underscoring sustained product and commercial momentum.

- May 2026: Cross Country Healthcare expanded its Intellify AI-powered workforce intelligence platform through an exclusive 36-month partnership, adding Optimé workforce strategy and planning capabilities for forecasting, analytics, and open-shift optimization.

- April 2026: Visier launched the next generation of its Workforce AI platform at the Outsmart conference, including a new Glean MCP Connection enabling access to workforce intelligence directly within enterprise AI search, and enhanced workforce planning capabilities spanning demand, skills, action, and organizational design.

Global People Analytics In Healthcare Market Report Scope

People analytics in the healthcare market refers to technology platforms and services that enable healthcare organizations to collect, analyze, and interpret workforce data to improve operational efficiency, employee well-being, and patient care outcomes. These solutions encompass modules such as workforce scheduling, labor cost management, talent acquisition and retention, skills and capability analytics, productivity measurement, burnout monitoring, compliance, and predictive workforce intelligence. Delivered through cloud, on-premises, or hybrid models, they serve hospitals, clinics, long-term care facilities, home healthcare agencies, and senior living providers of all sizes. The core purpose of this market is to help healthcare enterprises optimize staffing, reduce attrition, enhance workforce engagement, and align human capital strategies with clinical and organizational performance.

The People Analytics in Healthcare Market is segmented by Component (Software, and Services), Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Healthcare Systems, Mid-Sized Healthcare Organizations, Small Healthcare Providers), Solution Module (Workforce Management and Scheduling Analytics, Labor Cost, Time and Attendance Analytics, Talent Acquisition, Retention and Internal Mobility Analytics, Learning, Skills and Workforce Capability Analytics, Workforce Productivity and Performance Analytics, Employee Engagement and Burnout Analytics, Compliance and Workforce Risk Analytics, and Predictive Workforce Intelligence and Forecasting), End User (Hospitals and Health Systems, Clinics and Ambulatory Care Centers, Long-Term Care and Skilled Nursing Facilities, Home Healthcare Agencies, and Senior Living and Assisted Living Facilities), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Healthcare Systems |

| Mid-Sized Healthcare Organizations |

| Small Healthcare Providers |

| Workforce Management and Scheduling Analytics |

| Labor Cost, Time and Attendance Analytics |

| Talent Acquisition, Retention and Internal Mobility Analytics |

| Learning, Skills and Workforce Capability Analytics |

| Workforce Productivity and Performance Analytics |

| Employee Engagement and Burnout Analytics |

| Compliance and Workforce Risk Analytics |

| Predictive Workforce Intelligence and Forecasting |

| Hospitals and Health Systems |

| Clinics and Ambulatory Care Centers |

| Long-Term Care and Skilled Nursing Facilities |

| Home Healthcare Agencies |

| Senior Living and Assisted Living Facilities |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Enterprise Size | Large Healthcare Systems | |

| Mid-Sized Healthcare Organizations | ||

| Small Healthcare Providers | ||

| By Solution Module | Workforce Management and Scheduling Analytics | |

| Labor Cost, Time and Attendance Analytics | ||

| Talent Acquisition, Retention and Internal Mobility Analytics | ||

| Learning, Skills and Workforce Capability Analytics | ||

| Workforce Productivity and Performance Analytics | ||

| Employee Engagement and Burnout Analytics | ||

| Compliance and Workforce Risk Analytics | ||

| Predictive Workforce Intelligence and Forecasting | ||

| By End User | Hospitals and Health Systems | |

| Clinics and Ambulatory Care Centers | ||

| Long-Term Care and Skilled Nursing Facilities | ||

| Home Healthcare Agencies | ||

| Senior Living and Assisted Living Facilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of people analytics in healthcare?

The people analytics in healthcare market was valued at USD 1.23 billion in 2025, reached USD 1.57 billion in 2026, and is projected to reach USD 3.21 billion by 2031 at a 15.38% CAGR.

Which region leads global demand for healthcare workforce analytics platforms?

North America led with 38.43% share in 2025 because of large integrated delivery networks, stronger vendor penetration, and tighter staffing compliance requirements.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to grow at a 17.89% CAGR through 2031, supported by workforce shortages, uneven nurse density, and rising demand for automated planning tools.

Which component is expanding faster, software or services?

Software remained the largest component in 2025 with 64.37% share, while services are projected to grow faster at a 16.47% CAGR as providers seek implementation and analytics support.

Why are hospitals investing more in workforce analytics tools?

Hospitals are under pressure from labor inflation, staffing regulation, turnover risk, and margin compression, so they are using analytics to improve scheduling, retention, compliance, and labor cost visibility.

Which end-user group is seeing the fastest adoption?

Home healthcare agencies are projected to grow at a 16.39% CAGR through 2031 as care delivery becomes more distributed and workforce coordination grows more complex.

Page last updated on: