Market Overview

| Study Period | 2020 - 2031 |

|---|---|

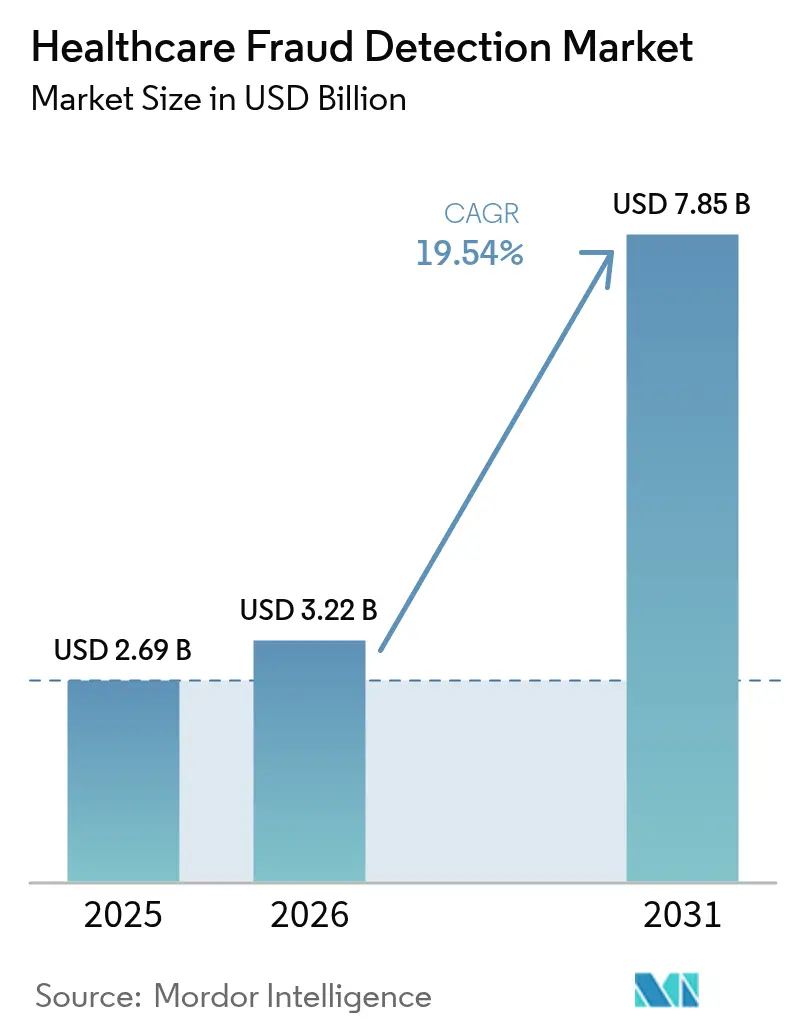

| Market Size (2026) | USD 3.22 Billion |

| Market Size (2031) | USD 7.85 Billion |

| Growth Rate (2026 - 2031) | 19.54% CAGR |

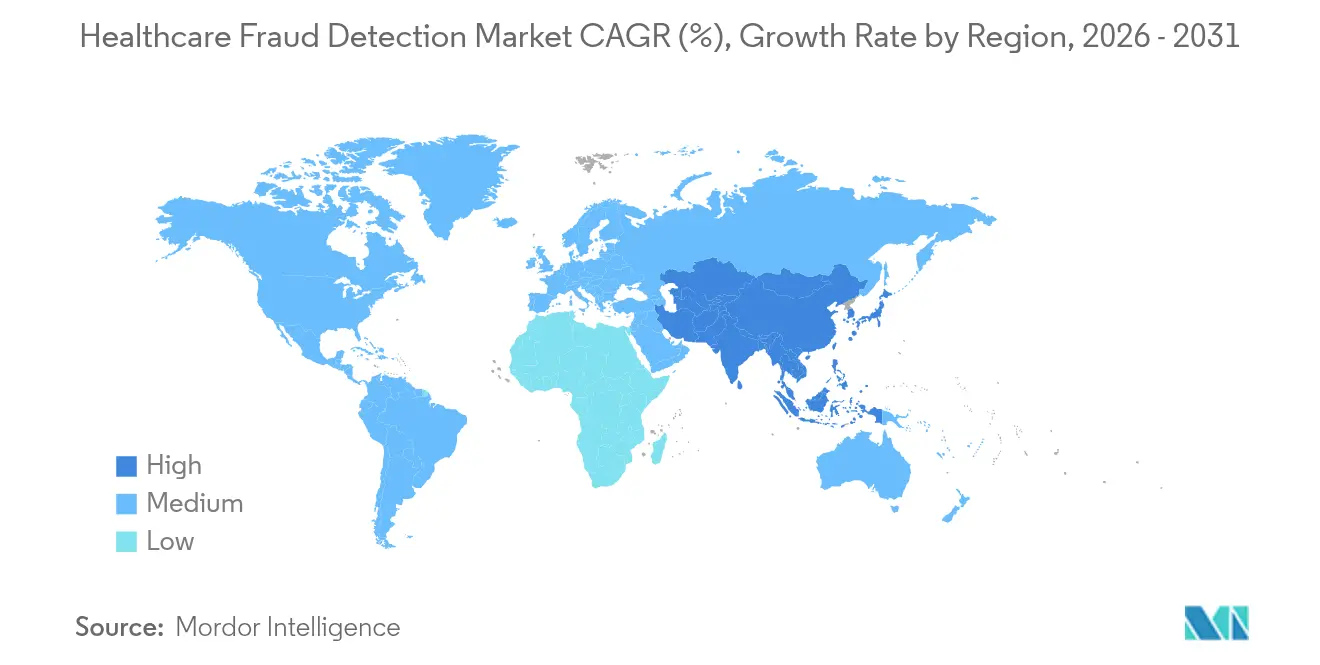

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

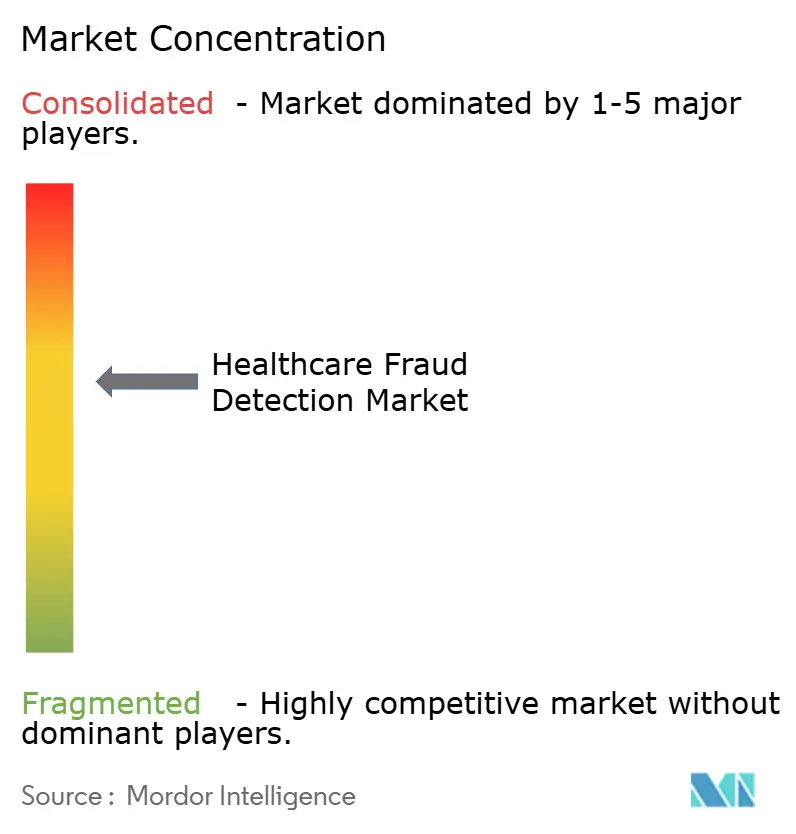

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Fraud Detection Market Analysis by Mordor Intelligence

Healthcare fraud detection market size in 2026 is estimated at USD 3.22 billion, growing from 2025 value of USD 2.69 billion with 2031 projections showing USD 7.85 billion, growing at 19.54% CAGR over 2026-2031. Across the forecast window, payers and providers are expanding data-driven fraud and payment-integrity programs in response to an estimated USD 100 billion in annual fraud losses.[1]Centers for Medicare & Medicaid Services, “Crushing Fraud, Waste, & Abuse,” cms.gov Wider adoption of real-time analytics, cloud infrastructure, and FHIR-based interoperability is turning fraud-detection from an after-the-fact review into a proactive risk-control discipline. Government audits are intensifying—CMS alone will raise its medical-record review workforce from 40 to 2,000 coders—which, in turn, is spurring technology vendors to embed machine learning and generative AI into core claims workflows. Competitive differentiation now hinges on rapid model deployment, partner ecosystems, and the ability to process unstructured clinical data at scale. Implementation challenges remain—especially around data integration, transparency mandates, and staff change-management—yet the cost-benefit equation increasingly favors automated fraud detection as a must-have, not a “nice-to-have,” capability.

Key Report Takeaways

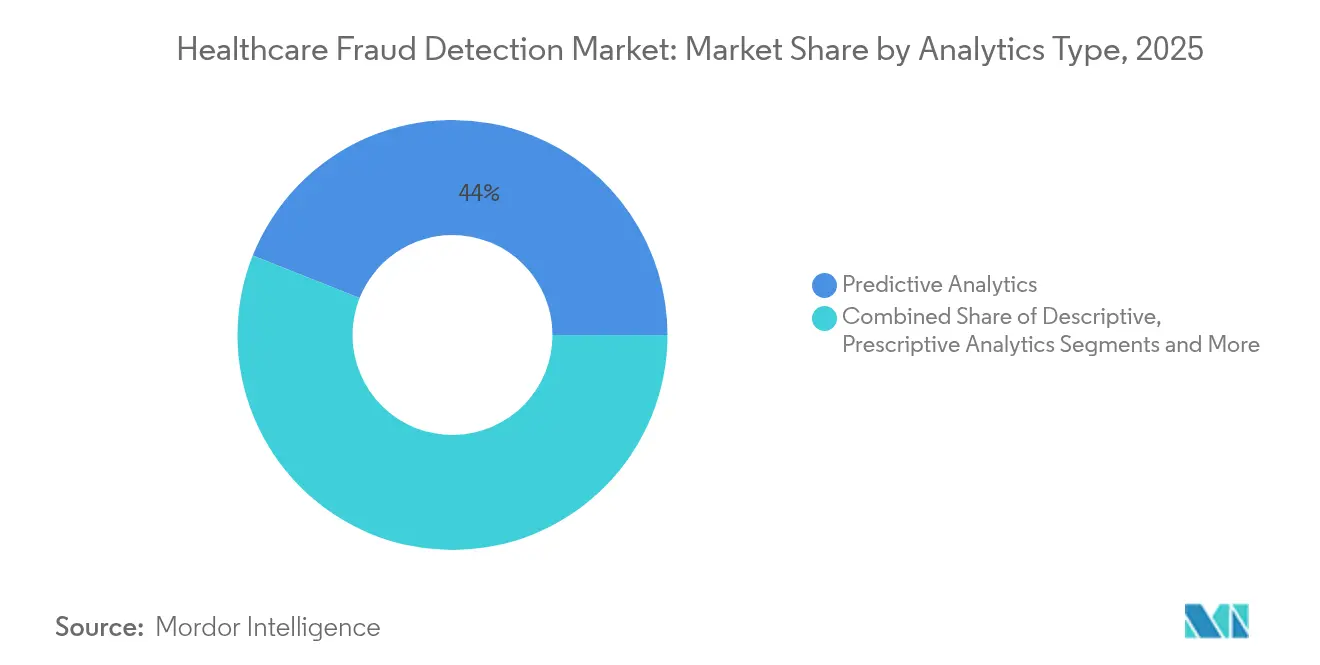

- By analytics type, predictive analytics led with 43.98% revenue share in 2025, while real-time streaming analytics is poised for a 23.7% CAGR through 2031.

- By component, software platforms held 59.10% of the healthcare fraud detection market share in 2025 and cloud services are expanding at 22.95% CAGR to 2031.

- By deployment mode, cloud deployments commanded 57.12% of the healthcare fraud detection market size in 2025 and will advance at 22.4% CAGR through 2031.

- By application, review of insurance claims captured 49.90% share of the healthcare fraud detection market size in 2025, whereas pharmacy benefit management is accelerating at a 21.55% CAGR.

- By end user, private insurance payers accounted for 47.20% revenue share in 2025, with government agencies registering the fastest 22.05% CAGR.

- By geography, North America led with 41.30% 2025 share, while Asia-Pacific is forecast to post a 20.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Fraud Detection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising healthcare expenditure | +3.2% | Global, highest in North America & Europe | Medium term (2-4 years) |

| Increasing fraudulent activities in healthcare | +4.1% | Global, concentrated in mature markets | Short term (≤ 2 years) |

| Growing pressure to reduce healthcare spending | +2.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Surge in health-insurance enrolment & claims volumes | +3.5% | Global, APAC strongest | Long term (≥ 4 years) |

| Real-time claims adjudication via FHIR APIs | +2.9% | North America & EU leading | Medium term (2-4 years) |

| Synthetic data generation for cross-institution detection | +1.8% | Global, early adoption in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Healthcare Expenditure

Spending growth is sharpening executive focus on fraud because each lost percentage point equals billions in avoidable cost. CMS has earmarked USD 941 million for fraud and abuse control in fiscal 2025, signaling that analytics-driven prevention is now central to cost-containment. Private payers echo this urgency as value-based contracts expose them to downside risk. Organizations are finding that anomaly-detection algorithms reveal savings opportunities invisible to manual reviewers. Countries with aging populations feel the pressure most because chronic-care and drug claims dominate expenditure. As a result, budget growth and fraud-control investment move in lockstep, reframing fraud analytics as defensive infrastructure.

Increasing Fraudulent Activities in Healthcare

Fraudsters exploit technology faster than legacy, rule-based systems can respond, forcing a shift toward AI-enabled monitoring. The Medicare Transaction Fraud Prevention Act prioritizes artificial intelligence after CMS flagged anomalous billing for intermittent urinary catheters, a tactic that triggered improper payments. Healthcare networks now combine cross-provider claims data with synthetic datasets to uncover patterns spanning geographies. Deep-learning approaches such as autoencoders have achieved F1-scores of 0.97 in spotting overutilized procedure codes.[2]Michael Suesserman, Samantha Gorny, Daniel Lasaga, John Helms, Dan Olson, Edward Bowen, and Sanmitra Bhattacharya, “Procedure Code Overutilization Detection from Healthcare Claims Using Unsupervised Deep Learning Methods,” BMC Medical Informatics and Decision Making, biomedcentral.com This arms race accelerates investment as stakeholders see reactive reviews as an insufficient defense.

Growing Pressure to Reduce Healthcare Spending

Cost-containment mandates push fraud analytics from discretionary spend to operational necessity. Highmark Health’s collaboration with Epic and Google Cloud saved USD 2.7 million by streamlining administrative steps. When predictive models surface high-risk cases, providers intervene earlier and avoid expensive procedures. Unions back these tools, funding second-opinion programs that cut overtreatment and reduce employer liability. Fraud analytics also trims false positives in prior authorizations, allowing physicians to focus on care rather than paperwork. The market therefore links analytics adoption directly to measurable operating savings.

Surge in Health-Insurance Enrolment & Claims Volumes

Rapid enrolment inflates daily claim counts beyond what batch systems can handle. India’s Ayushman Bharat Digital Mission has issued health IDs to more than 500 million citizens, a data influx that demands scalable analytics. Medicare Advantage plans in the United States face similar volume spikes amid tighter audits. Stream-processing platforms such as Apache Kafka route data for adjudication within seconds rather than hours.[3]Arti Rana, “Real-Time Claims Processing in Healthcare: Leveraging Stream Processing Technologies for Faster Payment Adjudication,” International Journal of Innovative Research in Management, Planning and Social Sciences, ijirmps.org To keep pace, organizations are adopting cloud architectures and embedding fraud-scoring logic at intake. Without automation, large payers risk delays, payment errors, and regulatory penalties.

Restraints Impact Analysis*

| Restraint | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unwillingness to adopt analytics solutions | -2.1% | Global, higher resistance in traditional markets | Short term (≤ 2 years) |

| High implementation & integration costs | -2.8% | Global, hardest on smaller organizations | Medium term (2-4 years) |

| Data-privacy & compliance concerns (HIPAA / GDPR) | -1.9% | North America & EU first | Long term (≥ 4 years) |

| AI-model bias & false positives triggering scrutiny | -1.5% | Global, regulator focus in developed regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Unwillingness to Adopt Analytics Solutions

Smaller providers fear that sophisticated fraud platforms will disrupt familiar workflows and demand scarce technical skills. This mirrors findings in Asian finance, where more than half of institutions still forgo AI in anti-money-laundering programs despite clear benefits. Healthcare staff often equate new tools with added administrative burden rather than relief. Moreover, leadership teams struggle to quantify undetected fraud, making ROI appear speculative. Successful pilot programs that deliver quick wins typically shift perception and encourage wider rollout, yet change-management remains a barrier.

High Implementation & Integration Costs

License fees are only the beginning; data-warehouse modernization, cloud migration, and user training quickly swell budgets. Mass General Brigham’s effort to integrate 27,000 data elements illustrates the resource intensity of building a fraud-ready data backbone. Specialized talent—data scientists, informaticists, compliance officers—commands premium salaries. Smaller organizations often lack the scale to justify such outlays even though regulatory obligations apply equally. Without low-touch integration and managed-service options, cost will slow adoption among mid-tier providers and regional health plans.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Analytics Type: Real-Time Processing Drives Innovation

The healthcare fraud detection market size for analytics platforms was led by predictive tools, which captured 43.98% share in 2025. These models profile historical claims to forecast risk before payment. Nonetheless, demand is shifting toward real-time streaming analytics, forecast to climb at 23.7% CAGR through 2031. Organizations increasingly view millisecond-level scoring as essential for intercepting evolving schemes.

Stream-processing stacks such as Kafka and Flink underpin this pivot, enabling dynamic ingestion of unstructured notes, device data, and FHIR messages. Early adopters report materially lower overpayment rates once detections occur pre-payment rather than in retrospective audits. Descriptive analytics remains relevant for compliance reporting, while prescriptive models are emerging among mature payers seeking automated adjudication recommendations. Vendors that knit predictive, prescriptive, and real-time workflows into a single fabric are shaping the next wave of differentiation in the healthcare fraud detection market.

By Component: Cloud Services Accelerate Deployment

Software suites dominated the component landscape with 59.10% 2025 share, reflecting entrenched demand for end-to-end investigation platforms. Yet cloud services are the fastest-growing slice at 22.95% CAGR, propelled by migration away from rigid on-premise stacks. Payers cite elastic scaling, lower upfront cost, and faster update cycles as prime incentives.

Major alliances—Humana and Google Cloud, Oracle Health and G42—aim to marry deep health data with hyperscale infrastructure. This ecosystem approach lowers barriers for mid-market insurers that lack vast internal IT. In parallel, managed-service providers bundle model governance, system tuning, and regulatory reporting, thereby reshaping total-cost calculations. As health plans consolidate point solutions into unified SaaS platforms, cloud services are likely to become the de-facto delivery model for the healthcare fraud detection market.

By Deployment Mode: Hybrid Models Enable Flexibility

Cloud deployments already account for 57.12% of the healthcare fraud detection market size and are projected to keep expanding at 22.4% CAGR. Even so, on-premise installations persist inside organizations with stringent data-sovereignty mandates. Hybrid architectures reconcile these needs, allowing sensitive identifiers to stay in local vaults while compute-heavy analytics runs in the cloud.

The rise of FHIR-native APIs from vendors such as Health Samurai simplifies secure data exchange between environments. Hybrid designs also help firms throttle cloud spending by off-loading only peak-time workloads. Over the forecast horizon, regulators’ evolving stance on cross-border data transfer will likely determine how fast pure cloud deployments outpace hybrid models, but flexibility will remain an essential buying criterion.

By Application: Pharmacy Benefits Drive Growth

Claims review retained 49.90% share in 2025, anchoring the healthcare fraud detection market. Yet pharmacy benefit management (PBM) solutions will expand at 21.55% CAGR, mirroring the surge in prescription-drug spend and scrutiny of high-cost therapies. Fraud models tuned to formulary management detect doctor-shopping, refill abuse, and coupon gaming that ordinary claims edits overlook.

CMS investigations into anomalous catheter billing underscore how device-specific schemes can slip through generic rule sets. With real-time PBM analytics, payers flag suspect prescriptions at the pharmacy counter, averting waste before dispensing. Adjacent use cases—payment integrity, provider audit, and revenue recovery—continue to mature, creating a continuum of prevention, detection, and recoupment applications inside the broader healthcare fraud detection market.

By End User: Government Agencies Accelerate Adoption

Private insurance payers dominated demand with 47.20% revenue share in 2025 because commercial plans historically invested earliest in analytics. However, government agencies will log the fastest 22.05% CAGR as Medicare and Medicaid scale machine-learning audits. CMS’s Data Analytics and Systems Group exemplifies this shift, coordinating cross-program integrity efforts with advanced modeling.

Providers are also stepping up investment to tighten revenue-cycle management under value-based contracts. Meanwhile, employers and unions deploy member-centric fraud tools to curb premium growth. This widening stakeholder roster broadens addressable demand and diversifies solution requirements, reinforcing the need for configurable platforms within the healthcare fraud detection market.

Geography Analysis

North America held 41.30% share of the healthcare fraud detection market in 2025, anchored by robust enforcement frameworks and funding. CMS is channeling USD 941 million into fraud-control activities for fiscal 2025, and regulations such as the 21st Century Cures Act mandate interoperability and algorithm transparency. High EHR penetration and a dense vendor ecosystem speed adoption cycles. Canada and Mexico follow the U.S. trajectory as cross-border claims rise and shared data lakes emerge.

Asia-Pacific is the fastest-growing region with a 20.8% CAGR, fueled by nationwide digital-health missions, expanding insurance pools, and cloud-first IT strategies. India’s 500-million-plus health IDs, China’s AI productivity gains among clinicians, and Japan’s insurer-led generative-AI pilots exemplify momentum. Australia and South Korea add regulatory clarity and public grants that accelerate vendor uptake.

Europe maintains solid growth underpinned by GDPR-aligned privacy safeguards. Member states adopt privacy-preserving analytics and synthetic data to reconcile fraud prevention with stringent data-protection norms. Germany, United Kingdom, and France lead deployments through national digitization roadmaps, while Southern and Eastern European markets show steady demand as health-insurance coverage broadens. South America and the Middle East & Africa remain nascent but attractive, given rising private insurance penetration and government e-health agendas that will require fraud controls.

Regulatory Landscape

In the United States, healthcare fraud detection is shaped by expanding program-integrity enforcement and formal requirements to use advanced analytics in Medicare oversight. The legal framework includes 42 U.S. Code 1320a-7m, which directs the use of predictive analytics and related technologies to identify and prevent waste, fraud, and abuse in Medicare fee-for-service, while CMS has operationalized more real-time detection through efforts such as the Fraud Defense Operations Center (FDOC), established in March 2025. In 2026, CMS actions such as the CRUSH initiative (with a stakeholder Request for Information) and publishing revoked Medicare enrollments on data.cms.gov add both rulemaking momentum and new transparency signals for automated screening and enrollment-risk scoring.

Europe is tightening the baseline for auditability and secure data governance that underpins fraud analytics. Regulation (EU) 2025/327 requires EHR systems to implement security and logging mechanisms, including capabilities to review and analyze log data, aligning health IT functionality with investigative and compliance needs. In April 2026, Implementing Regulation (EU) 2026/771 established the European Health Data Space (EHDS) Board, reinforcing coordinated application of health-data rules and setting clearer expectations for interoperable, governed data access that fraud detection solutions depend on.

Value Chain Analysis

The value chain begins with data creation and capture (EHR and revenue-cycle workflows, eligibility and enrollment records, pharmacy and prior-authorization events), then moves into data aggregation and governance (payers data warehouses, government repositories such as CMS data assets, identity proofing and provider enrollment controls), and into analytics execution (rules engines, predictive models, and real-time scoring embedded in claims intake and adjudication). Platform vendors and systems integrators configure and deploy these tools across cloud, on-premise, and hybrid environments, followed by investigation and recovery operations where alerts feed case management, documentation requests, payment suspensions, and referral pathways to special investigative units and law enforcement. Distribution increasingly includes public procurement channels for government users, alongside partner ecosystems with EHR vendors such as Epic and Oracle Health and hyperscalers that provide scalable compute for streaming and unstructured data.

A key chain-wide enabler is data sharing and compute access across agencies and counterparties, which is becoming more formalized and operationally central. In June 2026, DOJ entered interagency data-sharing agreements with CMS, DHS, and FTC to leverage big data and AI for healthcare fraud detection, and DOJ and CMS finalized an arrangement giving DOJ cloud computing capacity within CMSs Integrated Data Repository to apply advanced analytics. Bottlenecks remain concentrated in interoperability and integration work (normalizing multi-source claims and clinical data, connecting via FHIR APIs, and maintaining model governance and audit trails), which raises the role of managed services and modular, cloud-native deployments for organizations that lack internal data-science and compliance capacity.

Competitive Landscape

Competition clusters around integrated, AI-driven platforms supplied by global technology houses, legacy healthcare-IT vendors, and nimble startups. Market leaders pursue acquisitions and alliances to fill capability gaps and strengthen cloud and analytics depth. HEALWELL AI’s USD 165 million takeover of Orion Health underscores a consolidation trend toward data-interoperability plus AI bundles.

Oracle Health’s partnership with Cleveland Clinic and G42 signals a push to co-develop nation-scale AI applications that incorporate fraud-scoring at their core. UnitedHealth Group, with more than 1,000 AI use cases live, illustrates the capital intensity required to sustain leadership.

Emerging disruptors differentiate via cloud-native, microservice architectures that slash deployment time and enable rapid algorithm iteration. White-space opportunities include synthetic-data generators, bias-auditing toolkits, and pre-payment “Point-Zero” integrity models like Codoxo’s newly launched service. Overall, buyers weigh vendor roadmaps, explainability features, and multi-channel data ingestion more heavily than initial software cost when selecting platforms in the healthcare fraud detection market.

Healthcare Fraud Detection Industry Leaders

CGI Inc.

DXC Technology Company

Mckesson

IBM

Exl Service

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major opportunity sits in prepayment and enrollment-linked controls that reduce improper payments before they occur, supported by visible policy moves toward moratoria, transparency, and real-time oversight. In 2026, CMS implemented a six-month nationwide moratorium on enrolling new DME providers and initiated a six-month nationwide moratorium on new Medicare enrollment for hospice and home health agencies, creating demand for tools that tighten identity verification, enrollment risk scoring, and ongoing monitoring once providers are active. The CRUSH initiative and its Request for Information also open whitespace for vendors that can package explainable, auditable AI models with workflow-ready controls for claims intake, PBM edits, and provider screening.

Cross-dataset fusion and interagency collaboration raise the ceiling for solutions that connect claims patterns to broader signals and support faster action. The June 2026 DOJ-CMS agreement that provides cloud computing capacity within CMSs Integrated Data Repository, combined with data-sharing arrangements involving DOJ, DHS, and FTC, strengthens demand for platforms that can operate on large government-scale datasets, manage privacy and governance, and produce investigation-ready outputs. The 2026 National Health Care Fraud Takedown (455 defendants charged involving USD 6.5 billion in false claims) reinforces the operational need for case management, evidence traceability, and analytics-to-referral pipelines that work across payers, providers, and enforcement partners rather than within siloed post-pay audits.

Recent Industry Developments

- April 2026: DXC Technology introduced Assure Smart Apps, an AI-enabled suite aimed at automating claims management and fraud detection for insurers. The launch supports more modular deployment of fraud controls within core claims workflows, aligning with buyer preference for faster implementation and configurable analytics across lines of business.

- January 2026: CGI announced its AI-powered Fraud, Waste and Abuse (FWA) Prevention Platform became available through the U.S. General Services Administration Financial Management Quality Service Management Office (FM QSMO) Marketplace. The listing simplifies procurement for public-sector buyers and can accelerate agency adoption of pre-disbursement improper-payment controls.

- December 2025: CGI renewed and expanded its partnership with Highmark to enhance claims payment programs using CGI ProperPay, adding deeper analytics and recovery audit capabilities. The expansion highlights continued investment by large payers in platform-based payment integrity programs that combine detection, workflow automation, and recoveries at scale.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market counts the revenues earned from software and related services that help healthcare organizations find, flag, and prevent fraud, waste, and abuse in claims and billing, either before payment or after payment recovery workflows.

Scope exclusions: We exclude generic payment integrity BPO services, broad financial crime platforms not tuned for healthcare claims, and non-health insurance fraud tools.

Segmentation Overview

- By Analytics Type

- Descriptive Analytics

- Predictive Analytics

- Prescriptive Analytics

- Real-time / Streaming Analytics

- By Component

- Software

- Services

- By Deployment Mode

- On-premise

- Cloud

- Hybrid

- By Application

- Review of Insurance Claims

- Payment Integrity

- Provider Audit & Revenue Recovery

- Fraud, Waste & Abuse Management

- Pharmacy Benefit Management

- By End User

- Private Insurance Payers

- Government Agencies

- Healthcare Providers

- Employers & Unions

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean view of the claims environment where fraud detection is used, and then mapping where spending actually sits across payers, public plans, and providers. We rely on public sources such as CMS program integrity releases, the US HHS OIG work plan and audit reports, the Department of Justice healthcare fraud case summaries, and research papers indexed in PubMed, which helps set realistic fraud patterns and enforcement focus.

To anchor adoption signals, we also review industry association websites (for example, health plan and hospital groups), standards bodies and coding references tied to claims processing, and public procurement notices where fraud analytics tools are bought. Company filings, annual reports, and investor decks are used to understand how solution revenues are described and where they are booked, and then a paid subscription for company financials and a patent database are used selectively to clarify product positioning and innovation pace. These desk sources are not exhaustive, and we also use other public and paid references to collect data, cross-check it, and close open questions.

Primary Interviews and Surveys

Primary calls and short surveys are used to confirm what gets counted as fraud detection revenue versus adjacent payment integrity work, and to pressure-test assumptions on pricing and deployment patterns. We speak with a mix of payer-side fraud and SIU leaders, provider revenue cycle owners, healthcare IT teams, and solution implementation partners across major regions, so the final model reflects practical buying behavior and how these tools are used.

Insights from these discussions are also used to validate regional split logic, typical contract terms, and where usage-based pricing is becoming more common, which then helps tighten the forecast assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 13% | APAC: 49% |

| Mid tier: 49% | Functional/Unit leaders: 38% | EMEA: 30% |

| Smaller Players: 19% | Managers: 49% | Americas: 21% |

Market-Sizing & Forecasting

Sizing begins with a top-down demand pool build where healthcare claims volumes and the share routed through advanced analytics are reconstructed by region, and then converted into spend using typical pricing structures. To keep the steps traceable, we model a few practical inputs, such as covered lives and plan enrollment trends, claim submission volumes and growth, the mix of prepay versus postpay detection, cloud versus on-premises deployment share, and average subscription or services intensity per customer.

Those totals are then checked with selective bottom-up approximations, using a sample of supplier revenue disclosures, channel feedback on deal sizes, and a simple ASP times client count logic where public indicators exist. When product bundles blur fraud detection with broader payment integrity, we apply split factors that were validated in interviews and rechecked against how offerings are described in filings.

For forecasting, scenario analysis is used, with base, conservative, and faster-adoption cases driven by variables like new regulatory enforcement cycles, prior authorization and claim edits adoption, AI-assisted investigation uptake, and healthcare IT spend direction. Assumptions are adjusted only after they align with interview feedback and observable policy and procurement signals.

Data Validation & Update Cycle

Validation is done in several passes so the outputs stay consistent with real-world signals. We compare the model totals against independent indicators like healthcare fraud enforcement activity, payer program integrity budgets where available, and shifts in claim denial and recovery workflows, and then investigate any region or year that moves outside expected ranges.

Before sign-off, another analyst reviews inputs, math, and narrative logic, and clarifying questions are sent back to experts if a key assumption changes the outcome. Reports are refreshed annually, and interim updates are made when material events occur, such as major policy changes, reimbursement shifts, or a step-change in deployment patterns. Right before delivery, a final review pass is completed so clients receive the most current view.

Mordor Intelligence's Healthcare Fraud Detection Market Size Versus Other Published Estimates

Published market values for healthcare fraud detection often do not match because researchers are not always counting the same revenue items, and they may also be using different base years and currency timing. Differences also show up when one estimate includes wider payment integrity work, while another counts only claims fraud analytics tools.

The largest gaps usually come from how scope is drawn around software versus services, whether provider-side billing integrity is counted alongside payer claim fraud, and how recurring subscription pricing is escalated over time. Some sources also take an aggressive adoption curve for AI-based detection, without checking it against practical buyer budgets and implementation timelines that can slow rollout.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.69 B (2025) | |

| Industry Research Publisher A | USD 3.60 B (2025) | This figure appears to use a broader revenue bucket that can pull in adjacent payment integrity and wider analytics spending, which lifts the total beyond claims fraud detection-specific tools. |

| Trade Publisher B | USD 3.62 B (2024) | This estimate is reported for an earlier year and may apply a wider definition of market revenues, so year alignment and included services can shift the value upward versus a tighter claims-focused scope. |

Taken together, the spread is largely explained by whether adjacent payment integrity work is bundled into the same bucket and by the base-year choice, and that separation is handled explicitly before totals are rolled up in Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the healthcare fraud detection market?

The market stands at USD 3.22 billion in 2026 and is projected to reach USD 7.85 billion by 2031, reflecting a 19.54% CAGR over 2026-2031.

Which analytics approach is growing fastest?

Real-time streaming analytics is the fastest-growing segment, expected to post a 23.7% CAGR through 2031.

Why are cloud services gaining traction in fraud detection?

Cloud platforms offer elastic scaling, lower upfront costs, and rapid deployment, supporting a 22.95% CAGR for cloud services within the market.

Which region will expand most quickly?

Asia-Pacific is forecast to grow at a 20.8% CAGR, propelled by large-scale digital-health programs and rising insurance coverage.

How are government agencies influencing market growth?

Agencies such as CMS are ramping up audits and funding; government end users are anticipated to witness a 22.05% CAGR in solution adoption.

What is the biggest barrier to adopting fraud-detection analytics?

High implementation and integration costs remain the primary restraint, particularly for smaller healthcare organizations.

Page last updated on: