Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

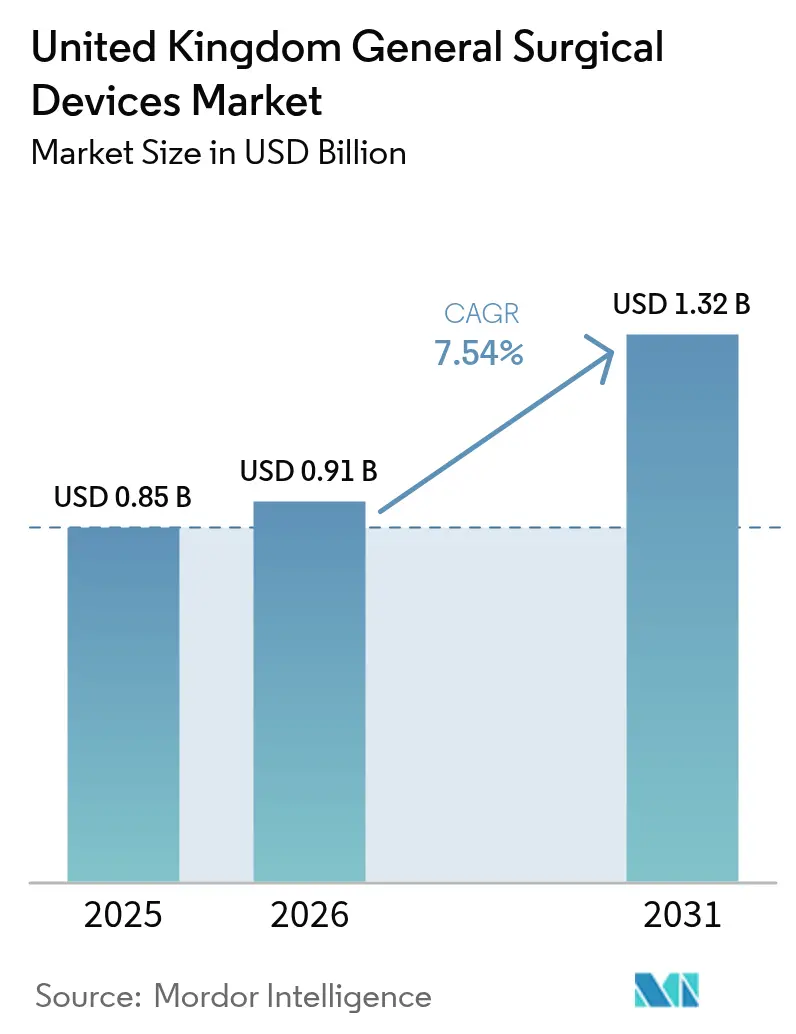

| Base Year Market Size (2025) | USD 0.85 Billion |

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.32 Billion |

| Growth Rate (2026 - 2031) | 7.54% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom General Surgical Devices Market Analysis by Mordor Intelligence

The United Kingdom General Surgical Devices Market size was valued at USD 0.85 billion in 2025 and estimated to grow from USD 0.91 billion in 2026 to reach USD 1.32 billion by 2031, at a CAGR of 7.54% during the forecast period (2026-2031). Growth is anchored in the National Health Service (NHS) pivot toward minimally invasive and day-case surgery, the rapid approval of 11 robotic systems by the National Institute for Health and Care Excellence (NICE),[1]Source: Digital Health, “NICE approves 11 robotic surgery systems for use in the NHS,” digitalhealth.net and sustained demand for data-rich surgical analytics despite capital budget headwinds. A rising trauma and chronic-disease burden, especially among an aging population, accelerates orthopedic and cardiovascular procedures, while carbon-footprint-linked procurement criteria advantage suppliers of reusable or low-waste instruments. Regulatory transitions to UKCA marking create short-term uncertainty, but phased implementation mitigates immediate supply shocks and favors incumbents with strong compliance infrastructure.

Key Report Takeaways

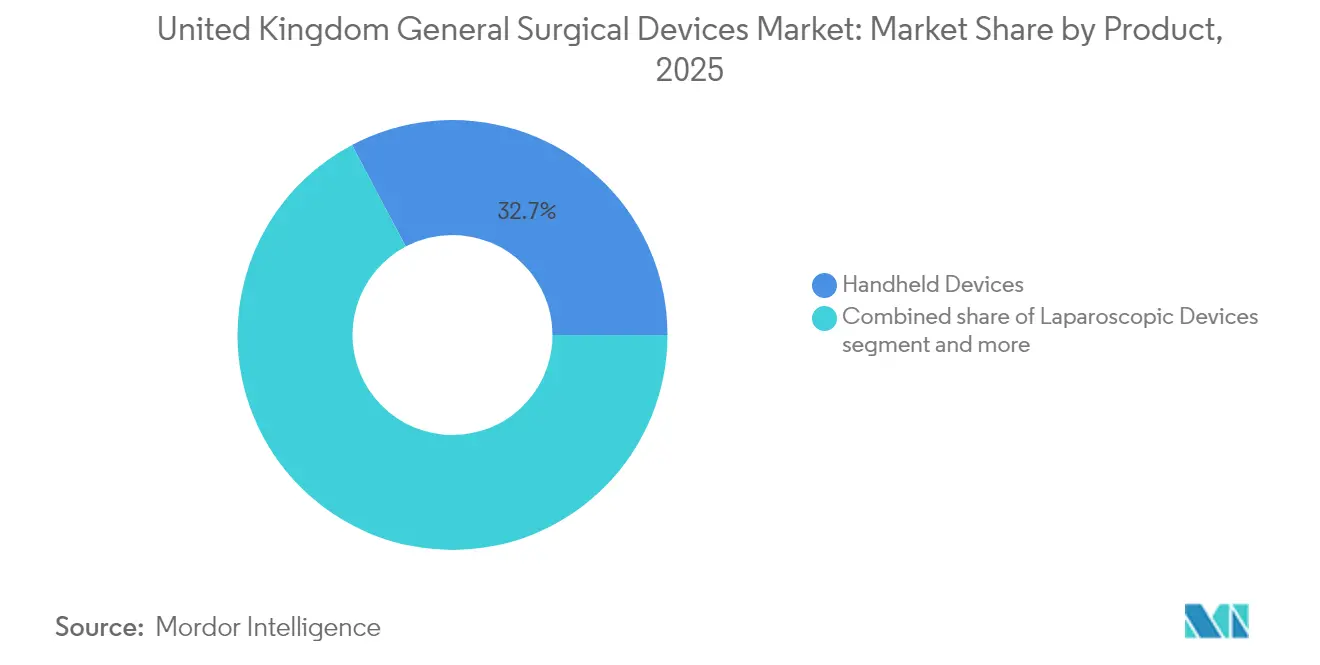

- By product, Handheld Devices led with 32.74% revenue share in 2025, while Wound Closure Devices are projected to grow at an 8.59% CAGR to 2031.

- By procedure approach, Minimally Invasive Surgery captured 72.88% of the UK general surgical devices market share in 2025 and is advancing at an 8.34% CAGR through 2031.

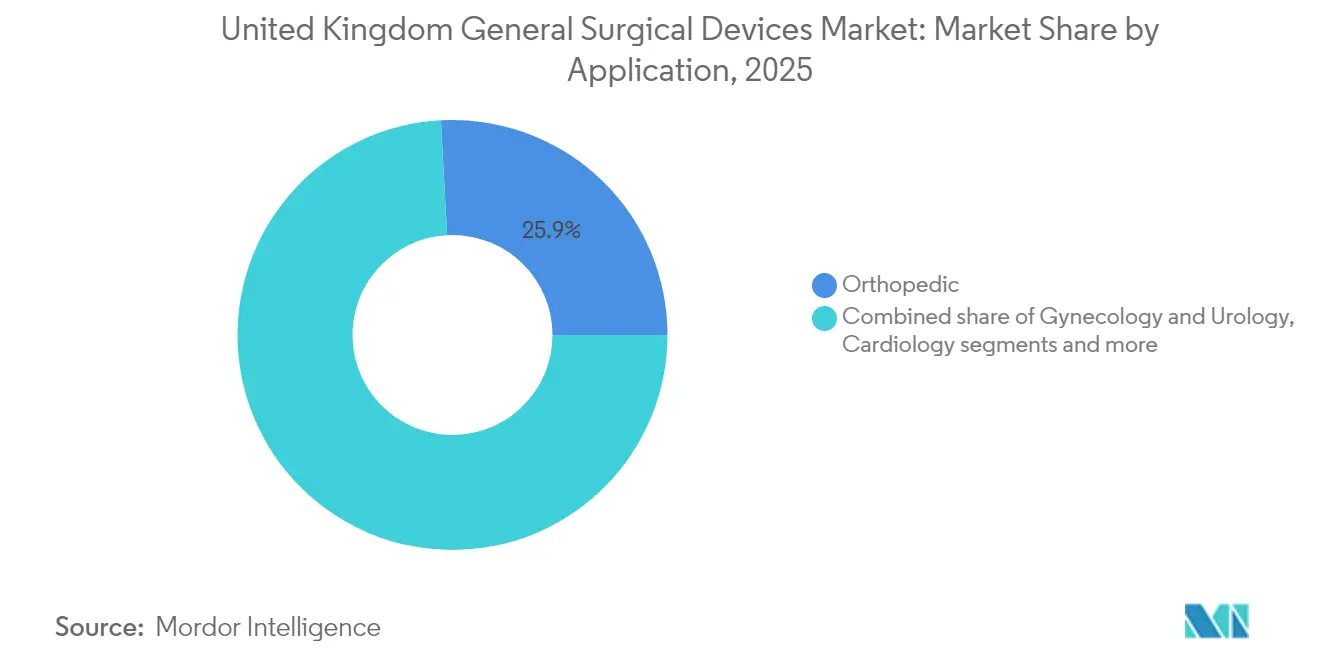

- By application, Orthopedic procedures accounted for a 25.86% share of the UK general surgical devices market size in 2025; Gynecology and Urology applications are expanding fastest at an 8.55% CAGR to 2031.

- By end user, hospitals held 71.12% share in 2025, whereas ambulatory surgical centres are poised for a 7.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom General Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for minimally-invasive devices | +2.1% | National, with concentration in major NHS trusts | Medium term (2-4 years) |

| Increasing prevalence of trauma & chronic diseases | +1.8% | National, with higher impact in aging population centers | Long term (≥ 4 years) |

| NHS long-term plan to cut inpatient stay via day-case surgery | +1.5% | National, with early adoption in specialized surgical centers | Medium term (2-4 years) |

| Shift to single-use instruments to mitigate hospital-acquired-infection risk | +1.2% | National, with priority in high-risk surgical departments | Short term (≤ 2 years) |

| OR digitalisation enabling device-level data analytics | +0.8% | National, with leading implementation in teaching hospitals | Medium term (2-4 years) |

| Carbon-footprint‐linked procurement scoring in NHS supply chain | +0.3% | National, with emphasis on sustainability-focused trusts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for minimally invasive devices

Robotic and laparoscopic platforms continue to displace open techniques, with Portsmouth’s Queen Alexandra Hospital converting all keyhole day-case procedures to Da Vinci systems and cutting length of stay for eligible patients. The Versius Surgical Registry recorded only 5.4% conversions in 2,083 procedures, underscoring reliability and surgeon acceptance. Paediatric adoption is growing after Southampton Children’s Hospital performed the UK’s first robotic kidney surgery in children. Integration of analytics modules, such as Versius Clinical Insights, supplies real-time benchmarks that shorten learning curves for new users.[2]Source: University Hospital Southampton, “Southampton Children's Hospital first in the UK to use pioneering robot for kidney surgery,” uhs.nhs.uk

Increasing prevalence of trauma & chronic diseases

Elective-care recovery plans highlight orthopedic robotics: Barking, Havering and Redbridge (BHR) Hospitals logged 100 robotic joint replacements by mid-2024 with the Mako robot, citing accuracy gains and faster mobilisation. Negative-pressure wound therapy systems like PICO Single Use are scaling for complex wounds, lowering infection incidence and length of stay. The geko neuromuscular stimulator improved venous-leg-ulcer healing probability by 68%, offering 15% cost offsets on long-term wound care.[3]Source: MedRxiv, “Cost-Effectiveness Analysis of the Geko Device (an NMES Technology) in Managing Venous Leg Ulcers in UK Healthcare Setting,” medrxiv.org Collectively, these dynamics lift procedure volumes and diversify device demand across hospitals.

NHS long-term plan to cut inpatient stay via day-case surgery

The NHS's systematic expansion of day-case surgery capabilities is reshaping device procurement priorities toward portable, efficient, and patient-friendly technologies. Remote-monitoring contracts published on the Find-a-Tender portal demonstrate NHS appetite for virtual wards and post-operative telehealth tools that pair with connected surgical devices. These priorities sustain demand for lightweight electrosurgical units, advanced hemostats and app-enabled wound closures.

Shift to single-use instruments to mitigate hospital-acquired-infection risk

Mandatory single-use protocols for tonsillectomy and other high-risk ENT procedures remain in force due to prion disease concerns. Multicentre evidence shows equivalent safety to reusable sets while removing cross-contamination risk. Sustainability pushes have catalysed hybrid approaches: life-cycle assessments indicate 38-56% lower carbon impact for reusable alternatives in some categories, spurring R&D into reprocessing-compatible alloys.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent MDR/UKCA regulatory timelines | -1.4% | National, with higher impact on smaller device manufacturers | Short term (≤ 2 years) |

| Capital-budget headwinds in NHS trusts | -1.1% | National, with acute pressure on foundation trusts | Medium term (2-4 years) |

| Supply chain vulnerabilities | -0.7% | National, with regional variations in supplier diversity | Short term (≤ 2 years) |

| Surgeons' skills gap for advanced robotics | -0.5% | National, with concentration in specialized surgical centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent MDR/UKCA regulatory timelines

Brexit-driven divergence requires UKCA marking for new devices from 2028, while transitional relief permits CE-marked products until then. Manufacturers must create incident-report data feeds conforming to new schemas by June 2025, elevating compliance costs. Overseas firms must appoint UK Responsible Persons, adding logistical layers and delaying launch timelines.

Capital-budget headwinds in NHS trusts

A USD 6.4 billion annual investment gap restricts equipment renewal, forcing trusts to chase 4% efficiency savings and favour outcome-based or lease contracts over outright purchases. Capital allocations for 2025-26 reach only USD 3.96 billion, underscoring scarcity relative to operating budgets.[4]Source: NHS Confederation, “2025/26 NHS priorities and operational planning guidance,” nhsconfed.org Surgical device manufacturers are responding by developing leasing programs, servitization models, and outcome-based contracts that align payment structures with clinical value delivery rather than upfront capital requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Handheld Devices Lead Market Share

Handheld Devices generated 32.74% of 2025 revenue within the UK general surgical devices market. The UK general surgical devices market size for this segment equated to USD 0.28 billion in 2025 and is projected to advance at 6.18% CAGR through 2031. Hospitals favour their portability and cross-specialty utility, which maximises usage rates versus capital-intensive robots. Wound Closure Devices, led by bioabsorbable electro-stimulation sutures, will climb fastest at 8.59% CAGR, backed by evidence of accelerated healing and lower infection risk.

Continuous innovation sustains demand for electrosurgical pencils, laparoscopic graspers and access trocars. Standardised procedure packs promoted by NHS Supply Chain strengthen procurement of bundled device kits that reduce set-up time and logistics complexity. Domestic producers are responding to import competition with quality-assured European steel and value-added servicing.

By Procedure Approach: Minimally Invasive Surgery Dominates

Minimally Invasive Surgery accounted for 72.88% of the UK general surgical devices market share in 2025; it is forecast to rise at an 8.34% CAGR, reflecting the NHS's strategic commitment to procedures that reduce patient trauma, accelerate recovery, and optimize resource utilization. Implementation of minimally invasive mitral valve surgery in novice centers demonstrated comparable outcomes to conventional approaches while achieving significant reductions in hospital stays from 7 to 5 days.

Open Surgery maintains relevance for complex cases requiring direct visualization and tactile feedback, representing the remaining market share with steady demand in trauma, emergency, and specialized procedures. The procedural shift toward minimally invasive approaches is creating training requirements for surgical teams, with AI-driven education systems demonstrating improved skill acquisition and retention in laparoscopic techniques.

By Application: Orthopedic Procedures Lead, Gynecology and Urology Surge

Orthopedics generated the single-largest revenue block at 25.86% in 2025 thanks to high joint-replacement volumes and trauma repairs. Cardiology applications maintain steady growth through continued innovation in minimally invasive cardiac procedures and device technologies. Neurology procedures benefit from precision requirements that favor robotic assistance and advanced imaging capabilities. Other Applications encompass diverse surgical specialties with varying growth trajectories based on technological advancement and clinical adoption patterns.

Gynecology and Urology together achieve the swiftest expansion at 8.55% CAGR, spurred by Olympus 4K endoscopy optics and first-in-region robotic hysterectomies. Narrow-band imaging and blue-light cystoscopy advance tumour detection rates, stimulating device upgrades at cancer hubs. Dartford and Gravesham NHS Trust performed the first robotic-assisted hysterectomy in Kent and Medway using the da Vinci system, demonstrating the expanding adoption of robotic technologies in gynecological procedures.

By End User: Hospitals Dominate, Ambulatory Centres Accelerate

Hospitals controlled 71.12% revenue in 2025 because complex robotics and vascular interventions remain inpatient-centric. Yet ambulatory surgical centres will grow 7.88% annually. The shift toward ambulatory care is supported by evidence showing that complex procedures like thyroidectomy, joint arthroplasty, and spinal surgery can be safely performed in day-case settings with appropriate patient selection and care protocols.

Trusts pursuing bed-capacity relief invest in portable anaesthesia, smart wound closure and remote-monitoring kits that enable safe discharge. Outcome-based contracts tie device payments to reduced readmissions, appealing in tight capital-budget settings. The British Association of Day Surgery's promotion of best practices and educational initiatives is facilitating the safe expansion of complex procedures into ambulatory settings, creating sustained demand for appropriate surgical technologies.

Geography Analysis

England comprises roughly 84% of the UK population and commands the lion’s share of the UK general surgical devices market, anchored by London, Manchester and Birmingham teaching hospitals that pioneer robotics and digital analytics. Guy’s and St Thomas’ adoption of the Versius robot exemplifies early-mover leverage over neighbouring trusts.

Scotland, Wales and Northern Ireland show differentiated procurement rules: Northern Ireland still adheres to EU MDR, requiring CE marking, whereas UKCA applies to Great Britain, creating dual-path compliance for multi-site vendors. Wales leads in digital performance analytics, with two health boards integrating Versius Clinical Insights for continuous quality improvement.

Regional integrated-care systems increasingly pool demand via collaborative tenders that weight carbon metrics, whole-life cost and clinical outcomes, favouring suppliers equipped with validated environmental data.

Competitive Landscape

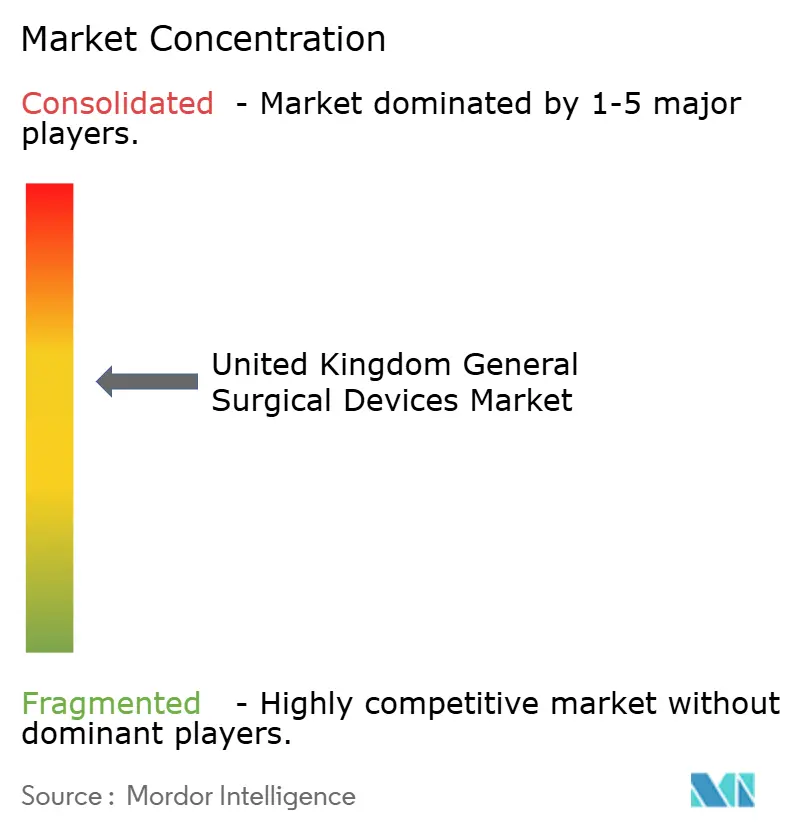

The UK general surgical devices market hosts moderate fragmentation: top five firms hold 48% revenue, with Intuitive Surgical, CMR Surgical, Stryker, Smith & Nephew and Medtronic in the lead. Hologic’s USD 310 million acquisition of Endomagnetics adds magnetic-tracing tech to its breast-surgery suite, signalling portfolio deepening. Smith & Nephew earmarked USD 3.92 billion for R&D and M&A to expand orthopedics and wound care, illustrating capital-intensive playbooks.

Emerging disruptor CMR Surgical combines ergonomic arm design with cloud-based analytics to lower operating height and deliver benchmarking dashboards that resonate with NHS digital roadmaps. Its mooted USD 4 billion sale could reshape bargaining power if a larger conglomerate absorbs its installed base.

Post-Brexit supply chain resilience has become a differentiator; vendors now dual-source critical components and hold six months’ inventory to mitigate port delays. Outcome-based pricing—where payment hinges on reduced complications or days-of-stay—gains favour as trusts pursue cost-containment without deferring innovation.

United Kingdom General Surgical Devices Industry Leaders

B. Braun SE

Stryker

Boston Scientific Corporation

Medtronic plc

Stryker Corporation

Johnson & Johnson (Ethicon)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: A UK-based medical device company, CMR Surgical initiated a USD 4 billion sale process, reflecting strong investor interest in the surgical devices sector and potential for market consolidation. The transaction could reshape competitive dynamics and create new partnership opportunities for NHS suppliers

- November 2024: Halma acquired Lamidey Noury Medical to bolster healthcare sector offerings, reflecting ongoing consolidation activity in the UK medical devices market and strategic portfolio expansion.

- March 2023: Bactiguard, in partnership with Quintess Medical and its affiliate, launched its line of wound care products in the United Kingdom and Ireland. This collaboration expanded the reach of Bactiguard's Wound Care offerings to a broader audience, including patients and other end users. The Bactiguard product line falls under the category of Class III medical devices, known for their non-toxic and eco-friendly attributes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom general surgical devices market as revenue generated from new, factory-built instruments purpose-designed for tissue cutting, grasping, sealing, access, and visualization during open or minimally invasive procedures performed across all surgical specialties.

Scope Exclusions: single-use drapes, sutures, and large capital robotics platforms are outside the value pool considered.

Segmentation Overview

- By Product

- Handheld Devices

- Laparoscopic Devices

- Electrosurgical Devices

- Wound Closure Devices

- Trocars and Access Devices

- Other Products

- By Procedure Approach

- Open Surgery

- Minimally Invasive Surgery

- By Application

- Gynecology and Urology

- Cardiology

- Orthopedic

- Neurology

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centres

- Other End Users

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed procurement leads at district general hospitals, biomedical engineers within private surgical centers, and senior product managers at domestic distributors across England, Scotland, Wales, and Northern Ireland. These conversations clarified average selling prices, refurbish cycles, and penetration of handheld versus powered devices, while short online surveys with colorectal and orthopedic surgeons validated utilization shifts toward day-case laparoscopy.

Desk Research

We started with core public datasets, including annual procedure volumes from NHS Digital, device recall and approval files published by the MHRA, import-export codes for HS-9018 and HS-9019 from HM Revenue & Customs, and hospital capital spend series available through the Office for National Statistics. Complementary insight came from peer-reviewed journals in the BMJ group, OECD Health Data, and selective company 10-K filings. Where market granularity was limited, our team accessed subscribed libraries such as Dow Jones Factiva for deal flow, D&B Hoovers for UK manufacturer revenues, and Questel to screen patent momentum around laparoscopic energy devices. The sources listed are illustrative, not exhaustive; many others informed data checks.

Market-Sizing & Forecasting

A top-down procedure-based model converts yearly NHS surgical counts into device demand using specialty-specific instrument sets, then multiplies by price curves adjusted for sterling inflation and tender discounts. Select bottom-up checks, supplier roll-ups of handheld forceps, channel audits for trocar kits, and sampled ASP × volume from three hospital groups align totals within an accepted variance band. Key drivers include laparoscopic share of abdominal cases, average device life, elective backlog clearance targets, hospital capital budgets, and import reliance ratios. Multivariate regression, supported by ARIMA smoothing for seasonality, projects each variable to 2030; assumptions are stress tested with scenario inputs gathered during primary research.

Data Validation & Update Cycle

Outputs pass a two-step analyst review: first for statistical anomalies versus external benchmarks, then for logical consistency across segments. Variances beyond five percent trigger re-contact of expert sources. We refresh every twelve months and issue mid-cycle revisions if material policy, currency, or reimbursement shifts emerge.

Why Our UK General Surgical Devices Baseline Commands Dependability

Published estimates often diverge because firms anchor on different device lists, price ladders, or update cadences. By adhering to a clearly declared scope and reconciling procedure data with channel checks, Mordor Intelligence delivers a balanced number buyers can trace and replicate.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.85 B (2025) | Mordor Intelligence | - |

| USD 1.60 B (2024) | Regional Consultancy A | counts single-use consumables and broad automation tools, no price deflator applied |

| USD 1.50 B (2024) | Trade Journal B | relies on import values only, excludes domestic OEM output and refurb sales |

The comparison shows how broader product baskets or partial data feeds inflate competitor values. Our disciplined alignment to surgical procedure demand, validated prices, and annual refresh cadence ensures a dependable baseline for planners and investors.

Key Questions Answered in the Report

What is the current size of the UK general surgical devices market?

The UK general surgical devices market size is USD 0.91 billion in 2026 and is projected to hit USD 1.32 billion by 2031.

Which product category leads revenue in 2025?

Handheld Devices hold the top position with 32.74% revenue share, driven by their cross-specialty versatility.

Why are data-enabled robotic systems gaining faster acceptance than earlier robotic generations?

The newest platforms bundle cloud analytics that benchmark surgeon performance and flag workflow bottlenecks, helping trusts justify capital outlays through measurable productivity gains and shorter learning curves.

How is the single-use versus reusable instrument debate evolving in UK theatres?

Infection-control protocols still favour single-use instruments for high-risk ENT and neurosurgery, yet trusts are piloting hybrid sets that combine critical disposable items with reprocessable handles to balance safety and environmental goals.

Page last updated on: