Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

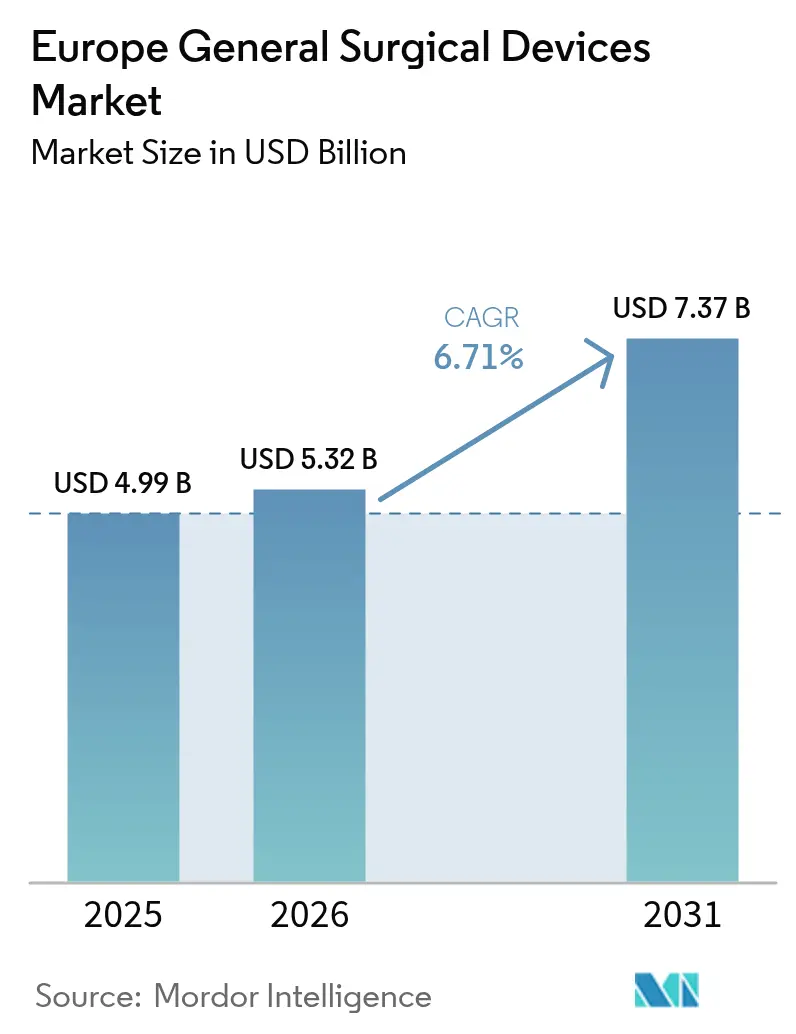

| Base Year Market Size (2025) | USD 4.99 Billion |

| Market Size (2026) | USD 5.32 Billion |

| Market Size (2031) | USD 7.37 Billion |

| Growth Rate (2026 - 2031) | 6.71% CAGR |

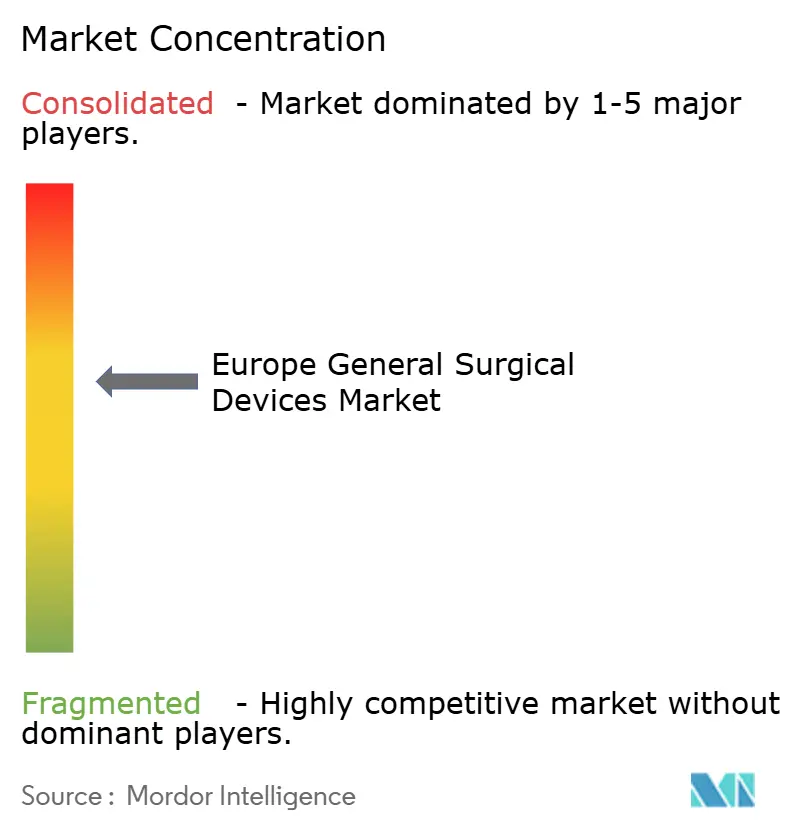

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe General Surgical Devices Market Analysis by Mordor Intelligence

The Europe General Surgical Devices Market size was valued at USD 4.99 billion in 2025 and estimated to grow from USD 5.32 billion in 2026 to reach USD 7.37 billion by 2031, at a CAGR of 6.71% during the forecast period (2026-2031). Robust procedure growth in minimally invasive and robotic platforms, coupled with a rapidly aging population and widening clinical indications, underpins this expansion. EU-MDR compliance costs have simultaneously driven strategic consolidation, positioning well-capitalized multinationals to absorb regulatory overheads while smaller firms either exit or seek partnerships. Hospital purchasers intensify price negotiations, yet procedure volumes keep climbing as health systems shift toward day-case models to relieve capacity constraints. Supply-chain resilience has become a board-level priority, with manufacturers now directing 3–5% of annual revenue to logistics diversification.

Key Report Takeaways

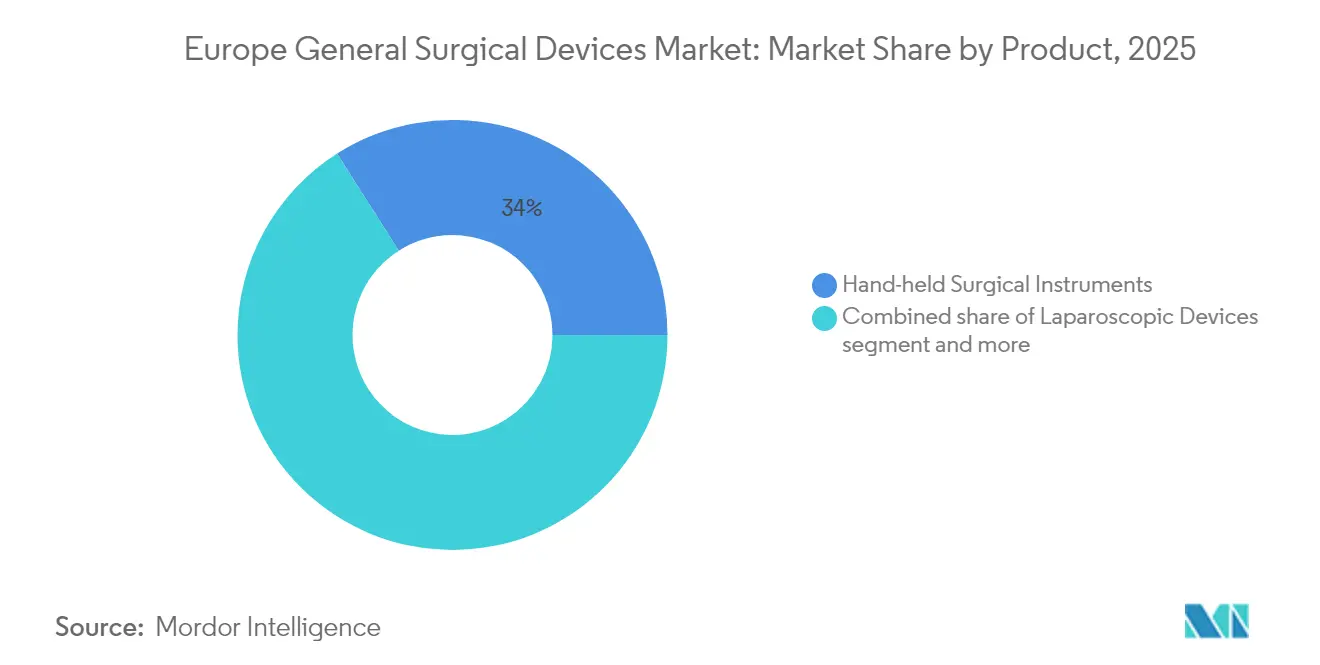

- By product type, hand-held surgical instruments led with 34.02% of the Europe general surgical devices market share in 2025, while robotic and computer-assisted systems are projected to expand at a 8.96% CAGR through 2031.

- By procedure approach, minimally invasive surgery accounted for 71.62% of the Europe general surgical devices market size in 2025 and is growing at an 8.08% CAGR to 2031.

- By application, orthopedic procedures held 26.72% of the Europe general surgical devices market size in 2025; general and bariatric surgery is the fastest-growing segment at an 8.71% CAGR.

- By end user, hospitals commanded 68.55% share of the Europe general surgical devices market in 2025, whereas ambulatory surgery centers are advancing at a 8.83% CAGR through 2031.

- By Country, Germany held a dominant share of 22.05% in 2025 of the Europe general surgical devices market; France is anticipated to grow with the fastest CAGR of 8.59% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe General Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for minimally-invasive procedures | +1.8% | Global, with strongest adoption in Germany, UK, France | Medium term (2-4 years) |

| Aging population & procedure volume growth | +1.5% | EU-wide, particularly acute in Germany, Italy, Spain | Long term (≥ 4 years) |

| Rapid innovations in laparoscopic & robotic systems | +1.2% | Core markets: Germany, UK, France, with spillover to Nordic countries | Medium term (2-4 years) |

| Shift toward day-case surgeries & disposable kits | +0.9% | UK leading, followed by Netherlands, Germany | Short term (≤ 2 years) |

| Favourable, procedure-linked reimbursement structures | +0.7% | Variable by country: strong in Germany, Netherlands; challenged in France, Italy | Medium term (2-4 years) |

| Expansion of private hospital groups and ambulatory surgery centres | +0.6% | Germany, UK, Spain leading; emerging in Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for minimally invasive procedures

Healthcare providers across Europe continue to transition from open to minimally invasive techniques, aiming to cut recovery times and free inpatient capacity. NHS England projects 500,000 robotic-assisted operations annually by 2035, signaling a steep adoption curve that will accelerate capital equipment refresh cycles.[1]Source: Digital Health, “NHSE projects 500k robotic assisted operations a year by 2035,” digitalhealth.net Nordic centers mirror this trend, installing more than 120 robotic platforms to support hernia repairs and other soft-tissue interventions. Energy-based devices such as Olympus ESG-410, which combine hybrid, bipolar, and ultrasonic modalities, are benefiting from the broader shift as surgeons seek multifunctional tools. Hospitals deploying Boston Scientific workflow-advisory solutions report 40% higher transcatheter volumes, illustrating how digital integration multiplies throughput.

Aging population & procedure volume growth

Citizens aged ≥ 65 represent a fast-growing cohort, particularly in Germany, Italy, and Spain, and this demographic shift fuels an uptick in joint replacements, cardiovascular interventions, and complex oncology resections. France still ranks 8th among OECD nations for hip replacement rates despite reimbursement cuts, underscoring latent demand.[2]Source: Medical Technology, “France Faces Orthopaedic Implant Shortage Risk in 2025,” medical-technology.nridigital.com Ambulatory surgery centers (ASCs) have flagged cardiology as their highest-growth specialty, aided by favorable Medicare-aligned payments and private equity investment. Intensivist shortages prompt a tighter integration of surgery and critical-care services, with anesthesiologists now managing 70% of ICU beds across Europe.

Rapid innovations in laparoscopic & robotic systems

Technology suppliers increasingly address ergonomic and cost barriers linked to earlier robotic generations. The Hugo robotic system has reduced median console times for inguinal hernia repair to 37 minutes for unilateral cases in European studies. Single-port solutions expand indications in colorectal and urologic surgery. Johnson & Johnson’s Polyphonic digital ecosystem pilots a fully connected OR, leveraging AI-driven analytics to improve decision-making and asset utilization. EU-funded HoloSurge integrates holographic visualization for liver and pancreatic cases, promising safer resections through real-time 3D anatomy guidance.

Shift toward day-case surgeries & disposable kits

With 69.27% of procedures still performed inside hospitals, European payers encourage migration to outpatient settings to ease budget stress. The United Kingdom leads in promoting day-case pathways, spurring demand for disposable instrument kits that bypass sterilization backlogs. Private-equity-backed operators are rolling out ASC networks focused on spine, orthopedics, and gastroenterology, mirroring U.S. models. Manufacturers like Lexington Medical have secured fresh capital to expand single-use stapling portfolios across 35+ countries. Advances in low-thermal-injury sealing technologies enable faster discharge protocols, further boosting outpatient share.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-MDR compliance costs & approval delays | -1.4% | EU-wide, particularly affecting SMEs and innovative device categories | Medium term (2-4 years) |

| Purchasing-group price pressure on OEM margins | -0.8% | Germany, France, UK leading; spreading to other major markets | Short term (≤ 2 years) |

| OR staff shortages constraining throughput | -0.6% | EU-wide, with acute shortages in France, Germany, UK | Medium term (2-4 years) |

| Persistent supply-chain vulnerabilities | -0.4% | EU-wide, with particular exposure in Eastern Europe and supply-dependent markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU-MDR compliance costs & approval delays

Conformity assurance can cost from EUR 5,000 for basic analyses to EUR 500,000 for Class III trials, squeezing SME cash flows and prompting portfolio rationalization.[3]Source: EuroDev, “EUMDR 2017/745 Compliance: Cost, Regulations, Requirements,” eurodev.com Only 43 notified bodies remain to review an estimated 500,000 devices, leading to extended approval cycles and deferred launches. Industry surveys show half of device makers plan to withdraw or limit EU portfolios due to regulatory burdens.

Purchasing-group price pressure on OEM margins

France has mandated a 25% reimbursement cut for orthopedic implants starting 2025, and the Economic Committee for Health Products seeks 11% additional price reductions by 2027. Group-purchasing organizations across Germany and the UK are adopting similar tactics, compelling vendors to offer deeper discounts or bundled service agreements. Device Benefit Management firms now mediate negotiations to enhance pricing transparency. Advanced prostheses risk withdrawal if reimbursement fails to cover cost-to-serve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Robotics Drive Innovation Despite Hand-Held Dominance

Hand-held instruments retained a 34.02% Europe general surgical devices market share in 2025, reflecting their ubiquity in routine interventions. Robotic and computer-assisted systems, however, are set to outpace all categories at a 8.96% CAGR to 2031, powered by broader clinical acceptance and falling per-procedure costs. Olympus THUNDERBEAT and VISERA 4K platforms illustrate how imaging and energy technologies converge to enhance tissue handling and visualization. Medtronic’s PlasmaBlade operates at significantly lower temperatures than legacy electrocautery, reducing collateral damage. Hybrid devices that integrate sensors and wireless connectivity are poised to stretch the competitive gap between premium and value tiers.

Second-generation robotics address prior cost and footprint limitations, opening adoption among mid-sized centers. Europe general surgical devices market vendors increasingly bundle capital equipment with digital workflow software to create stickier customer relationships. Virtual-Ports’ CE-marked laparoscopic accessories and Johnson & Johnson’s Ottava-compatible generator exemplify targeted product updates that fit new robotic ecosystems. Wound-closure systems and trocar lines benefit from the day-case push, with single-use options mitigating sterilization bottlenecks and infection risk.

By Procedure Approach: Minimally Invasive Surgery Reshapes Operating Theaters

Minimally invasive techniques accounted for 71.62% of the Europe general surgical devices market size in 2025 and are advancing at an 8.08% CAGR, consolidating their position as the preferred standard of care. Improved optics, energy delivery, and haptic feedback allow surgeons to tackle complex pathologies with smaller incisions. Open surgery maintains a vital role for trauma and large tumor resections but is ceding volume steadily.

Fast docking times reported for the Hugo platform illustrate cumulative efficiency gains that reduce anesthesia duration and improve turnover. HoloSurge’s 3D holography enters pilot phases, supporting safer resection planes in hepatobiliary cases. Europe general surgical devices market participants invest heavily in training centers to help surgeons climb new learning curves quickly, a prerequisite for payer support and technology credentialing.

By Application: Bariatric Surgery Outpaces Traditional Orthopedic Leadership

Orthopedic interventions captured 26.72% of the Europe general surgical devices market size in 2025, driven by aging demographics and active-lifestyle expectations. Reimbursement cuts in France signal cost headwinds, but elective volumes remain resilient. By contrast, bariatric and general surgery is surging with an 8.71% CAGR as obesity prevalence rises and metabolic surgery guidelines broaden eligibility.

Ambulatory centers target sleeve gastrectomy and gastric bypass as anchor procedures, rationalizing investments in energy devices and stapling platforms tailored for thicker tissue profiles. Europe general surgical devices market vendors see cross-selling potential into revision surgeries, which often require advanced access tools and powered staplers. Oncology, neurology, and gynecology continue steady growth, each influenced by screening uptake and site-of-care shifts.

By End User: ASCs Challenge Hospital Dominance Through Efficiency Gains

Hospitals still generated 68.55% of Europe general surgical devices market revenue in 2025 due to their comprehensive acute-care infrastructure. Yet ASCs are expanding at a 8.83% CAGR and progressively moving up the acuity ladder. Site-neutral payment proposals and surgeon ownership models make the setting attractive for high-volume procedures such as joint arthroplasty and cardiovascular interventions.

Efficiency programs have become a strategic lever; Italian facilities deploying Boston Scientific analytics lowered warehouse time by 87% and expanded throughput by 40%. Specialty clinics occupy a niche for dermatologic, ophthalmologic, and fertility procedures, offering tailored care pathways. Europe general surgical devices market suppliers tailor commercial models—leasing, pay-per-use, or service bundles—to match disparate cash-flow profiles across settings.

Geography Analysis

Germany anchors the Europe general surgical devices market with its deep manufacturing base and supportive reimbursement frameworks. Germany held a share of 22.05% in 2025 of the Europe market; France is anticipated to grow with the fastest CAGR of 8.59% from 2026 to 2031. Karl Storz’s EUR 2.17 billion turnover in 2023 reinforces the domestic innovation ecosystem and accelerates technology diffusion into university hospitals. Procedure volumes remain buoyant despite budget restraint measures, as demographic trends amplify demand.

France retains significant weight even after a 25% cut to orthopedic implant tariffs in 2025, forcing providers to weigh cost versus clinical benefit rigorously. Hip replacement incidence still ranks among OECD front-runners, indicating structural demand. The United Kingdom leads robotic adoption; a ten-fold growth to 500,000 robotic cases per year by 2035 will require sustained investment in surgeon credentialing and maintenance contracts.

Italy and Spain represent high-growth territories as public-private hospital partnerships modernize infrastructure. Italian centers adopting efficiency software cut non-clinical workload, freeing capacity for additional surgical lists. Spanish private operators such as Fresenius Helios recorded 8% revenue growth in 2024 driven by procedure mix optimization. Nordic countries, though smaller, exhibit outsized appetite for advanced robotics, piloting single-port and endoluminal platforms early in the life cycle.

Competitive Landscape

Competitive intensity in the Europe general surgical devices market is moderate with a tilt toward consolidation. Johnson & Johnson, Medtronic, and Stryker leverage expansive portfolios to negotiate multi-year framework agreements, but niche innovators chip away at specialized segments. Teleflex’s EUR 760 million buyout of BIOTRONIK’s vascular unit strengthens its coronary and peripheral line-up, illustrating portfolio realignment toward high-growth endovascular therapy.

Digital enablement differentiates offerings beyond hardware. Boston Scientific packages analytics that lifted European procedure volumes by 40%, signaling a shift to service-led value propositions. Brainlab’s planned EUR 200 million IPO underlines investor appetite for software-first surgical guidance platforms, a field expected to grow alongside AI adoption.

Regulatory hurdles favor large incumbents able to absorb EU-MDR costs, yet startups secure capital by focusing on unmet needs such as colorectal anastomosis protection (SafeHeal) or compact robotic arms (Moon Surgical). Procurement bans on Chinese suppliers alter sourcing calculus, potentially opening share for European mid-tier manufacturers with cost-competitive lines.

Europe General Surgical Devices Industry Leaders

Boston Scientific Corporation

Johnson & Johnson (Ethicon / DePuy Synthes)

B. Braun SE

Medtronic plc

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: EU votes to exclude China from medical device procurement, upending supply chains across the bloc.

- April 2025: Baxter launches room-temperature Hemopatch Sealing Hemostat across Europe, enhancing intra-operative bleed control.

- May 2023: Olympus rolls out POWERSEAL Sealer/Divider across EMEA to support open and laparoscopic specialties.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Europe's general surgical devices market as the yearly spend on reusable or single-use mechanical, powered and energy-based instruments that surgeons rely on during open or minimally invasive procedures inside hospitals, ambulatory centers and specialty clinics. The covered basket includes hand-held tools, laparoscopic kits, electrosurgical generators, wound-closure aids, trocars, access ports and entry-level robotic adjuncts.

Scope exclusion: implantable hardware, imaging consoles, patient monitors and dedicated ENT or cardiovascular tool sets sit outside this analysis.

Segmentation Overview

- By Product Type

- Hand-held Surgical Instruments

- Laparoscopic Devices

- Electrosurgical Devices

- Wound-Closure Devices

- Trocars and Access Systems

- Robotic and Computer-Assisted Systems

- Other Products

- By Procedure Approach

- Open Surgery

- Minimally Invasive Surgery

- By Application

- Gynecology and Urology

- Cardiology

- Orthopedic

- Neurology

- General and Bariatric Surgery

- Oncology

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured conversations with surgeons, OR managers, purchasing heads and regulators across Germany, the United Kingdom, France, Italy and Spain. These first-hand insights validated adoption curves, price dispersion and EU-MDR replacement timing that desk work alone cannot capture.

Desk Research

We began by pairing Eurostat surgery counts with OECD and WHO health-outlay series, then mapped import volumes under EU CN codes 9018/9019 and patent trends from the European Patent Office. Public releases from MedTech Europe, Germany's BMEL and country tender dashboards revealed procurement cycles and price drifts. Company 10-Ks, peer-reviewed journals and investor decks framed unit economics, while paid feeds such as D&B Hoovers and Volza helped us verify supplier revenues. These examples illustrate a broader evidence pool our team consulted; many other open records underpinned cross-checks.

Market-Sizing & Forecasting

We launch every model with a top-down demand pool: annual procedure counts multiplied by device-use ratios, then test totals through selective supplier roll-ups. Key inputs include laparoscopy penetration, average kit cost, elective backlog clearance, hospital capital cycles, EU-MDR action dates and euro-dollar swings. A multivariate regression anchors the baseline value, and scenario analysis projects value through the forecast period.

Data Validation & Update Cycle

Outputs pass anomaly checks against import tallies, public filings and hospital budget cues before senior review sign-off. We refresh figures each year and issue interim updates whenever material events shift the baseline.

Why Mordor's Europe General Surgical Devices Baseline Commands Reliability

Published estimates often diverge because firms mix product baskets, freeze exchange rates or refresh models sporadically, whereas we benchmark every assumption and update annually.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.99 B (2025) | Mordor Intelligence | - |

| USD 5.19 B (2024) | Regional Consultancy A | Adds sutures and staplers; relies on 2021 surgery ratios |

| USD 24.70 B (2025) | Trade Journal B | Bundles consumables, implants and robotics; scales Europe from a global share |

According to Mordor Intelligence, this disciplined scope, variable-level modeling and regular refresh give decision-makers a transparent, repeatable baseline that traces back to public statistics and verified price points.

Key Questions Answered in the Report

What operational challenge do EU surgical device manufacturers rank as the most disruptive in 2025?

Rising EU-MDR compliance costs and lengthy notified-body queues top the list because they delay product launches and force portfolio cuts.

How are hospitals mitigating staff shortages in operating rooms across major European markets?

Facilities are adopting workflow-automation software and robotic platforms that shorten case times and reduce reliance on hard-to-recruit scrub nurses and anesthetists.

Why are ambulatory surgery centers expanding faster than traditional hospitals in Europe?

Payers favor day-case models that lower inpatient stays, and surgeons value the streamlined scheduling and ownership stakes ASCs can provide.

Which technology feature is most sought after when European buyers evaluate next-generation laparoscopic systems?

Surgeons increasingly prioritize integrated energy devices that deliver ultrasonic and bipolar modalities through a single handpiece, enhancing speed and vessel-sealing reliability.

How are group-purchasing organizations influencing device design choices in France and Germany?

By mandating price ceilings, they push vendors to develop cost-efficient, single-use instruments that fit bundled-payment thresholds without compromising clinical performance.

Page last updated on: