Osseointegration Implants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

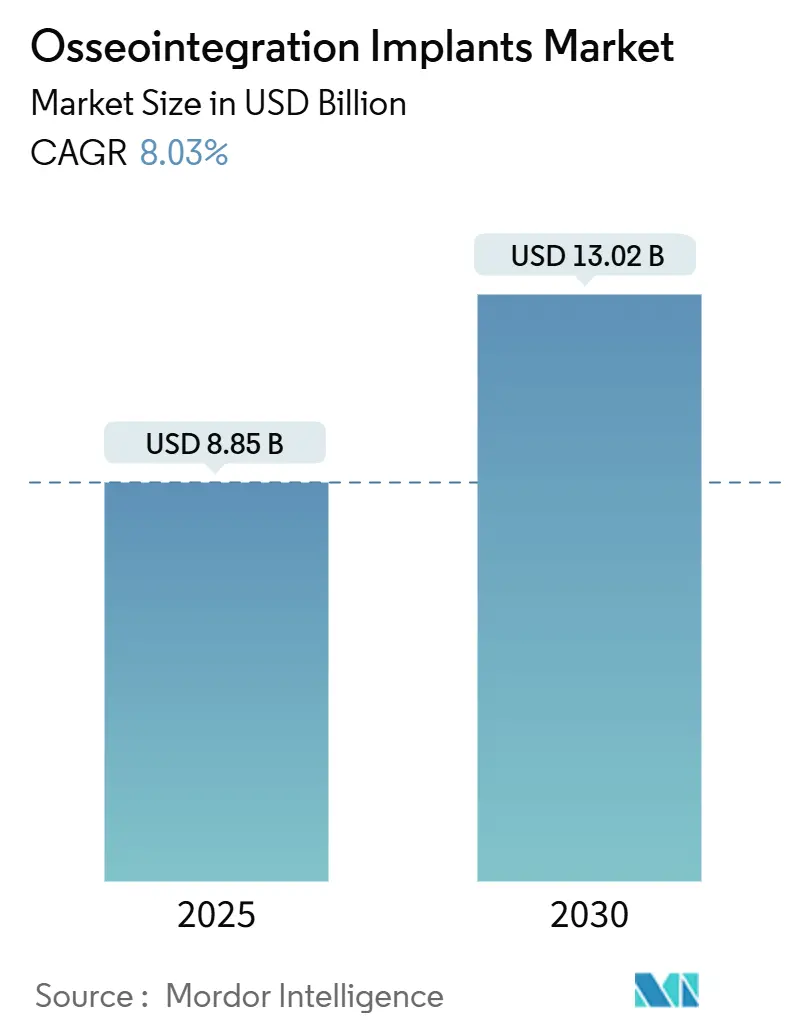

| Market Size (2025) | USD 8.85 Billion |

| Market Size (2030) | USD 13.02 Billion |

| Growth Rate (2025 - 2030) | 8.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Osseointegration Implants Market Analysis by Mordor Intelligence

The Osseointegration Implants Market size is estimated at USD 8.85 billion in 2025, and is expected to reach USD 13.02 billion by 2030, at a CAGR of 8.03% during the forecast period (2025-2030).

The market’s upward path reflects rising life expectancy, a steady shift toward fixed dental solutions, and growing clinical acceptance of bone-anchored prostheses for amputees. Intensifying innovation in surface engineering, the introduction of sensor-enabled implants, and broader reimbursement coverage in high-income economies also underpin demand. Conversely, peri-implant infection risks and uneven surgeon training availability temper the growth trajectory in several emerging nations.

Key Report Takeaways

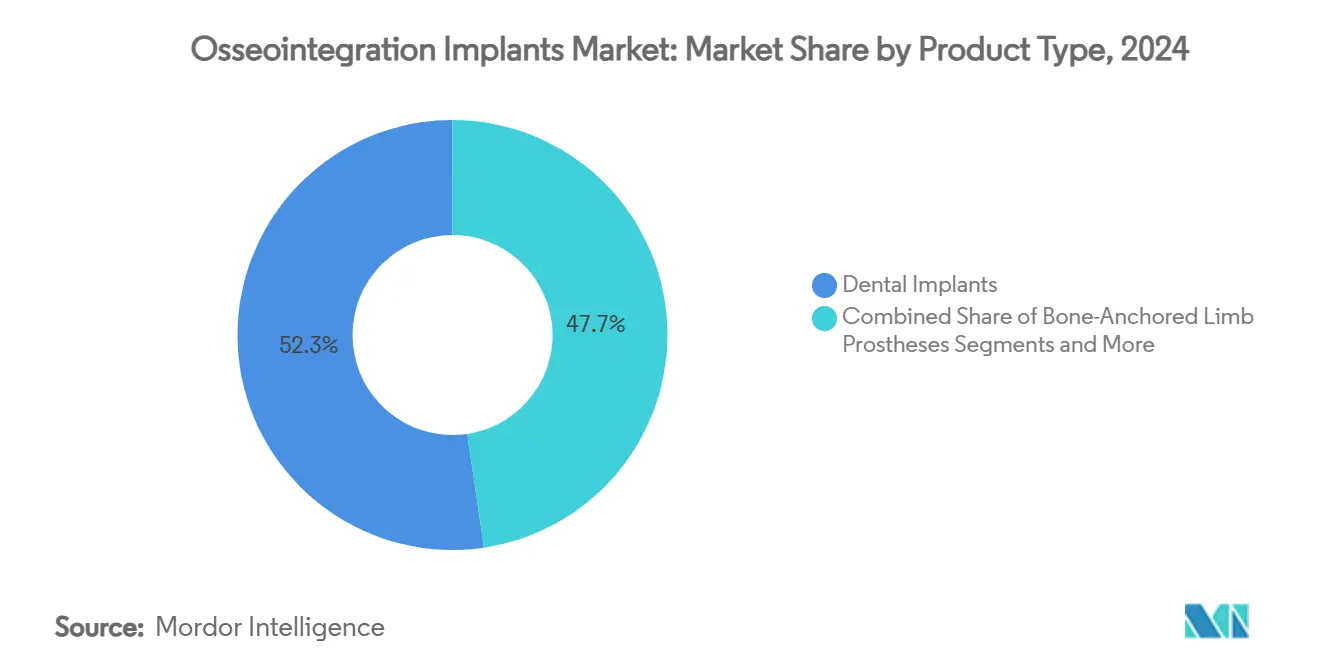

- By product type, dental implants led with 52.34% of the osseointegration implants market share in 2024, while bone-anchored limb prostheses are projected to expand at an 11.34% CAGR through 2030.

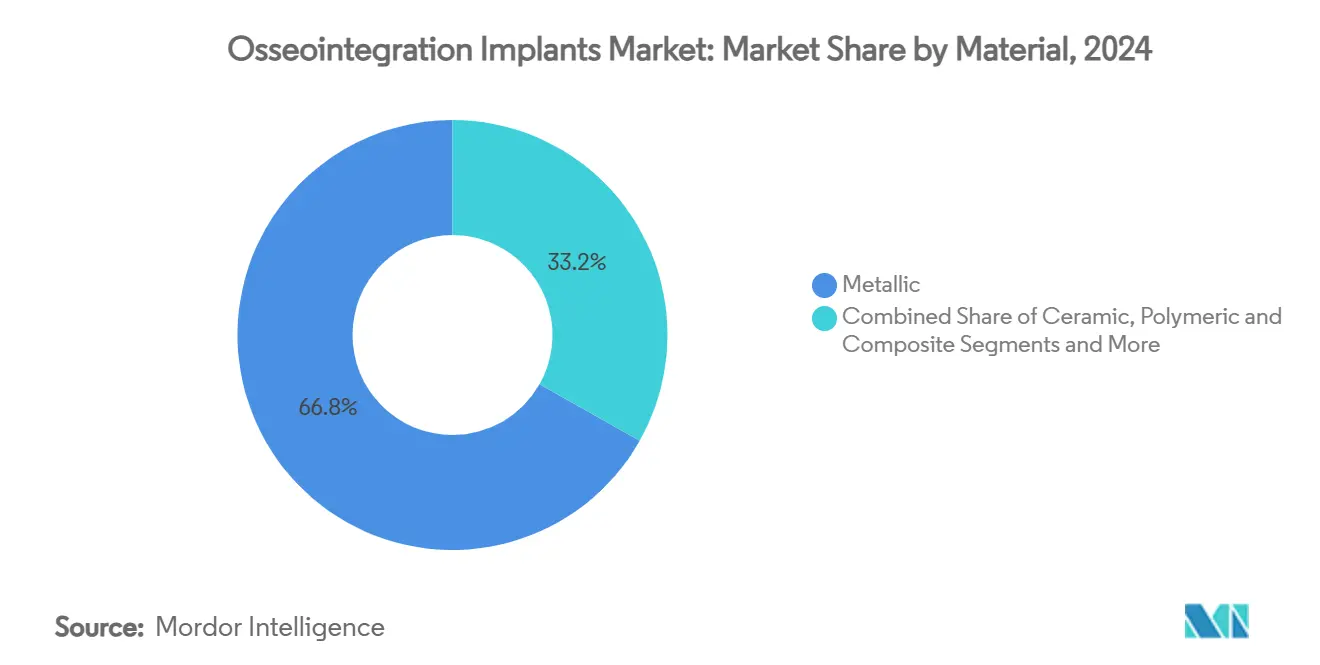

- By material, metallic systems commanded 66.81% share of the osseointegration implants market size in 2024; ceramic alternatives are projected to grow at a 12.64% CAGR to 2030.

- By end user, hospitals and ambulatory surgical centers accounted for 44.56% revenue in 2024; orthopedic and rehabilitation centers are set to rise at a 9.94% CAGR over the forecast period.

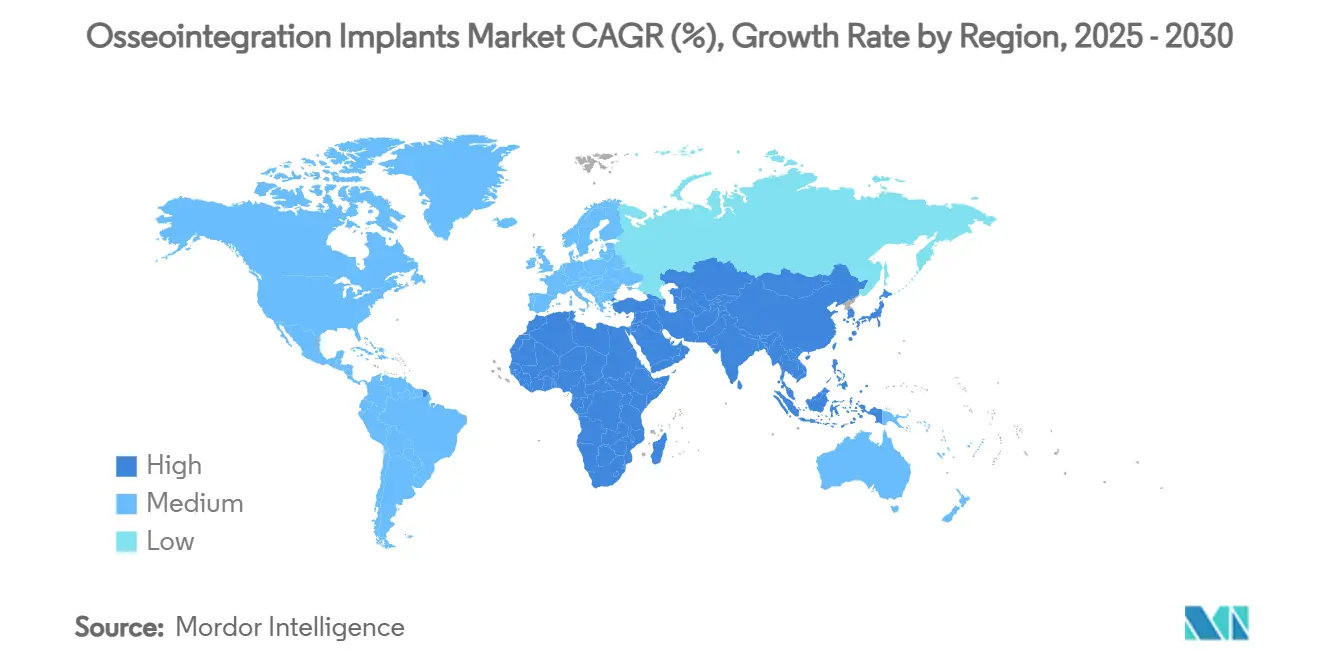

- By geography, North America captured 34.55% share in 2024, whereas Asia-Pacific is expected to register the fastest 10.63% CAGR to 2030.

Global Osseointegration Implants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Dental-Implant Procedures Among Ageing Population | +1.8% | Global, with concentrated impact in North America & Europe | Long term (≥ 4 years) |

| Surge In Limb Amputations Driving Bone-Anchored Prostheses Demand | +1.2% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Advancements In Titanium & Zirconia Surface Engineering | +1.0% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Emergence Of Sensor-Enabled "Smart" Osseointegration Implants | +0.8% | North America & Europe, with selective APAC adoption | Long term (≥ 4 years) |

| Military-Funded Limb-Reconstruction Programs | +0.6% | Primarily North America, with spillover to allied nations | Short term (≤ 2 years) |

| Integration Of Digital Workflows And Robot-Guided Implant Placement | +0.9% | Global, with faster adoption in technologically advanced markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Dental-Implant Procedures Among Ageing Population

Global life expectancy gains have increased the number of people over 65 who retain enough disposable income to seek fixed dental restorations rather than removable dentures. Greater awareness of oral-health quality-of-life benefits, combined with strong insurer coverage for restorative dentistry in the United States and Western Europe, keeps chair-time for implant placement consistently high. Advanced sand-blasted large-grit acid-etched surfaces now secure faster secondary stability in osteoporotic bone, enabling clinicians to treat elderly patients confidently.[1]Tomas Albrektsson, “Osteoimmune Regulation Underlies Oral Implant Osseointegration and Its Perturbation,” Frontiers in Immunology, frontiersin.org Growing preference for one-stage protocols further reduces visits, making premium implants the new norm for seniors and sustaining momentum across the osseointegration implants market.

Surge in Limb Amputations Driving Bone-Anchored Prostheses Demand

Combat injuries, traffic trauma, and diabetes complications lift above-knee amputation volumes each year, spurring interest in skeletal-anchored transfemoral prostheses that eliminate socket-related skin breakdown. U.S. military centers report faster rehabilitation and higher mobility scores after osseointegration surgery compared with conventional devices. Health-economic modeling indicates lifetime cost-utility benefits that offset the upfront surgical premium, catalyzing payer willingness to reimburse and widening the osseointegration implants market base in veteran and civilian cohorts alike.

Advancements in Titanium & Zirconia Surface Engineering

Nanoscale texturing, hybrid hydroxyapatite–chitosan coatings, and antibacterial silver-doped layers shorten healing by accelerating osteoblast activity while curbing biofilm formation.[2]Weilong Tang, “Hybrid Coatings on Dental and Orthopedic Titanium Implants: Current Advances and Challenges,” BMEMat, onlinelibrary.wiley.com For aesthetic zones, roughened acid-etched zirconia delivers high primary stability without the metallic glare of titanium, appealing to patients with thin gingival biotypes.[3]Abdulaziz Gulab, “Zirconia Dental Implants; The Relationship Between Design and Clinical Outcome: A Systematic Review,” Journal of Dentistry, sciencedirect.com These material gains open opportunities for smaller-diameter implants and immediate-loading protocols, supporting broader clinical indications and reinforcing growth for the osseointegration implants market.

Emergence of Sensor-Enabled “Smart” Osseointegration Implants

Bluetooth-equipped joint and dental systems now capture range-of-motion data, step counts, and implant temperature, offering clinicians objective insights during recovery. Zimmer Biomet’s FDA-cleared Persona IQ knee established the regulatory path for connected hardware that integrates seamlessly into electronic health records. Although cybersecurity standards are still evolving, early adopters report fewer unscheduled follow-ups thanks to proactive alerts, underpinning a value proposition likely to translate across dental and limb-anchor applications in the osseointegration implants market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure Cost & Patchy Reimbursement | -1.5% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| Peri-Implant Infection & Revision Risk | -1.2% | Global, with higher impact in regions with limited post-operative care | Long term (≥ 4 years) |

| Data-Privacy Concerns With Connected Implants | -0.8% | Primarily developed markets with strict data protection regulations | Short term (≤ 2 years) |

| Shortage Of Surgeons Trained In The Two-Stage Osseointegration Technique | -1.0% | Global, with acute shortages in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Procedure Cost & Patchy Reimbursement

Two-stage osseointegration surgery demands specialized theaters, multiple admissions, and prolonged physiotherapy that push hospital invoices well above socket-based prosthetics. Insurers in many developing economies still classify the modality as experimental, obliging patients to self-finance or forgo treatment. Even in the United States, Medicare approval is case-by-case, creating administrative hurdles that deter providers. Until bundled-payment models recognize long-run mobility gains, cost sensitivity will curb penetration of the osseointegration implants market in lower-income regions.

Peri-Implant Infection & Revision Risk

Biofilm-induced peri-implantitis affects up to 22% of implants and can halve survival rates when bone loss exceeds critical thresholds.[4]Sung Wook Hwang, “Survival Analysis of Implants after Surgical Treatment of Peri-implantitis,” BMC Oral Health, bmcoralhealth.biomedcentral.com Revision surgery often requires grafting and systemic antibiotics, adding clinical complexity and expense. While silver nanoparticles, graphene coatings, and galvanic cleaning systems reduce microbial adhesion, universal maintenance protocols remain inconsistent. Consequently, infection anxiety persists among surgeons and patients, restraining the overall osseointegration implants market in risk-averse clinical settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dental Dominance Drives Market Leadership

Dental implants account for 52 .34% of the global osseointegration implants market in 2024, reflecting decades of clinical familiarity and robust distribution networks. Chairside digital workflows, CBCT-guided positioning, and affordable bulk titanium blanks have cut surgery time, allowing general dentists to integrate implantology into routine practice. Robotic guidance delivers sub-2° angular deviation, enhancing confidence in immediate-loading arches and widening indications for those with limited bone. Patient preference for natural mastication and aesthetics sustains repeat demand, anchoring revenue for the osseointegration implants market.

Bone-anchored limb prostheses hold a smaller baseline but expand at an 11.34% CAGR, underscored by veteran rehabilitation programs and rising diabetes prevalence. Single-language surgical protocols such as the Compress system reduce inpatient stay, while 3D-printed connectors offer custom torsional damping that improves gait symmetry. Peer-reviewed cost-utility analysis reveals incremental cost-effectiveness ratios below USD 300 per QALY, strengthening payer negotiations. Together, these elements position product diversification as a central pillar of competitiveness within the osseointegration implants market.

By Material: Metallic Foundations With Ceramic Innovation

Metallic platforms, spearheaded by commercially pure titanium and Ti-6Al-4V alloys, represent 66.81% usage owing to unmatched tensile strength and corrosion resistance. Cold-spray hydroxyapatite layers now encourage earlier osteoid deposition, shortening loading times in full-arch reconstructions. Moreover, Ti-Zr blends achieve higher fatigue limits, making them suitable for narrow-ridge applications without compromising stability. These traits preserve titanium’s role as the backbone of the osseointegration implants market.

Ceramic implants grow at 12.64% CAGR as patients seek metal-free solutions and clinicians exploit zirconia’s low plaque affinity. Acid-etched roughened zirconia posts show marginal bone loss comparable to commercially pure titanium, easing concerns over long-term reliability. Innovations such as doped-yttria tetragonal zirconia polycrystal improve fracture resistance, while photodynamic waveguide concepts explore antibacterial therapy through the implant body itself. Combined, these advances diversify material choice and enrich the osseointegration implants market.

By End User: Hospital Integration Meets Specialized Growth

Hospitals and ambulatory surgical centers capture 44.56% of revenue, leveraging multispecialty teams, high-resolution imaging, and intensive care capabilities for complex bilateral cases. Tertiary centers often participate in clinical trials, ensuring early access to investigational implants and reinforcing patient inflow. Integration with same-day digital prosthetic labs further shortens restorative cycles, boosting throughput and stabilizing the osseointegration implants market.

Orthopedic and rehabilitation centers expand at a 9.94% CAGR as outpatient-focused business models align with payer incentives to lower total episode costs. Dedicated gait labs, virtual reality-based physiotherapy, and nurse-led home monitoring drive patient satisfaction, while modular operating theaters let surgeons perform high-volume bone bridge revisions. The growing network of such specialty hubs redistributes procedure volumes that were once the preserve of academic hospitals, enlarging the clinician base and deepening the osseointegration implants market.

Geography Analysis

North America remains the largest regional contributor with 34.55% share in 2024, anchored by early FDA approvals and comprehensive Veterans Affairs funding that legitimizes newer implant modalities. Robust dental insurance penetration and a high incidence of comorbidities requiring limb reconstruction sustain therapeutic demand. The presence of major manufacturers’ R&D headquarters fosters rapid product iterations that continually raise clinical performance benchmarks.

Asia-Pacific exhibits the fastest 10.63% CAGR to 2030 as rising disposable income intersects with public-sector investments in tertiary trauma care. China’s implant leaders doubled sales in metropolitan areas after rolling out targeted surgeon-training roadshows, a strategy mirrored by multinationals tapping into county-level hospitals. Japan pilots autonomous robotic zygomatic surgery, signalling a cultural preference for precision that could spill into limb-anchor cases. Meanwhile, India’s nascent private insurance sector begins to reimburse osseointegration, widening access beyond elite urban centers.

Europe maintains steady uptake on the back of stringent CE-mark requirements that push manufacturers to publish long-term data. Germany’s sickness funds reimburse a growing share of dental implants when clinically justified, while the United Kingdom trials outcome-based payments that reward providers for mobility gains. Scandinavian registries track infection and revision metrics comprehensively, informing continuous improvement and preserving public trust. Collectively, this mature regulatory ecosystem keeps procedure volumes resilient and underpins the osseointegration implants market across the continent.

Competitive Landscape

The competitive environment is moderately concentrated: the combined top five manufacturers account for roughly 65% of global revenue, yet niche innovators penetrate specific sub-segments through digital or material specialization. Zimmer Biomet leverages connected-implant analytics to strengthen its orthopedics franchise, whereas Straumann Group accelerates APAC expansion by partnering with local distributors and rolling out tiered product lines. Dentsply Sirona differentiates through chairside CAD/CAM ecosystems that lock dentists into proprietary consumables streams.

Strategic moves highlight portfolio broadening and vertical integration. Zimmer Biomet’s Persona SoluTion PPS femur cleared in late 2024 addresses nickel-sensitivity, capturing a patient subset underserved by conventional alloys. Straumann’s RevEX protocol marries fully digital planning with zirconia full-arch milling, raising laboratory efficiency and clinician adoption. Meanwhile, start-ups such as restor3d employ 3D-printed porous titanium in ankle fusion plates, competing on patient-specific geometry rather than scale manufacturing.

Market entrance barriers include multi-year post-market surveillance demands, steep surgeon learning curves, and payor evidence thresholds that favor incumbents with deep clinical datasets. Still, the rapid adoption of AI-guided planning software lowers infrastructure requirements, allowing agile firms to target under-served emerging-market niches. The resulting interplay of scale and specialization shapes an evolving but disciplined osseointegration implants market.

Osseointegration Implants Industry Leaders

Zimmer Biomet

Straumann Group

Envista

Dentsply Sirona

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: restor3d showcased the FDA-cleared Ossera AFX Ankle Fusion System at ACFAS 2025, highlighting 3D-printed porous architecture for faster fusion.

- February 2025: Maxx Orthopedics secured FDA 510(k) clearance for a porous titanium tibial baseplate within the Freedom Total Knee System, enabling a cementless tibiofemoral construct.

- February 2025: MIS launched the LYNX dental implant, offering broad dimensional compatibility and value pricing for immediate extraction-socket placement.

Global Osseointegration Implants Market Report Scope

| Bone-Anchored Limb Prostheses |

| Dental Implants |

| Spinal & Other Orthopedic Implants |

| Metallic (Titanium, Ti-Alloys) |

| Ceramic (Zirconia, Alumina) |

| Polymeric & Composite |

| Bio-active / Graphene-enhanced Coatings |

| Hospitals & Ambulatory Surgical Centers |

| Dental Clinics |

| Orthopedic & Rehabilitation Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Bone-Anchored Limb Prostheses | |

| Dental Implants | ||

| Spinal & Other Orthopedic Implants | ||

| By Material | Metallic (Titanium, Ti-Alloys) | |

| Ceramic (Zirconia, Alumina) | ||

| Polymeric & Composite | ||

| Bio-active / Graphene-enhanced Coatings | ||

| By End User | Hospitals & Ambulatory Surgical Centers | |

| Dental Clinics | ||

| Orthopedic & Rehabilitation Centers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is driving the rapid expansion of the osseointegration implants market in Asia-Pacific?

Healthcare infrastructure upgrades, rising disposable income, and broader surgeon training programs propel a 10.63% CAGR in the region, outpacing every other geography.

2. Why are ceramic implants gaining popularity over traditional titanium systems?

Zirconia offers metal-free aesthetics, low plaque affinity, and comparable osseointegration, leading to a 12.64% forecast CAGR for ceramic materials.

3. How significant is peri-implant infection as a market restraint?

Peri-implant disease affects up to 22% of cases and can reduce implant survival to 21.3% in severe stages, prompting cautious adoption in high-risk patients.

4. Which product segment is projected to grow the fastest through 2030?

Bone-anchored limb prostheses, propelled by military rehabilitation and diabetes-related amputations, are set to expand at an 11.34% CAGR.

5. What technological trend is reshaping post-operative monitoring?

Sensor-enabled “smart” implants that transmit real-time recovery metrics to clinicians are emerging, with early examples already cleared by the FDA.

Page last updated on: