Halal Meat Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

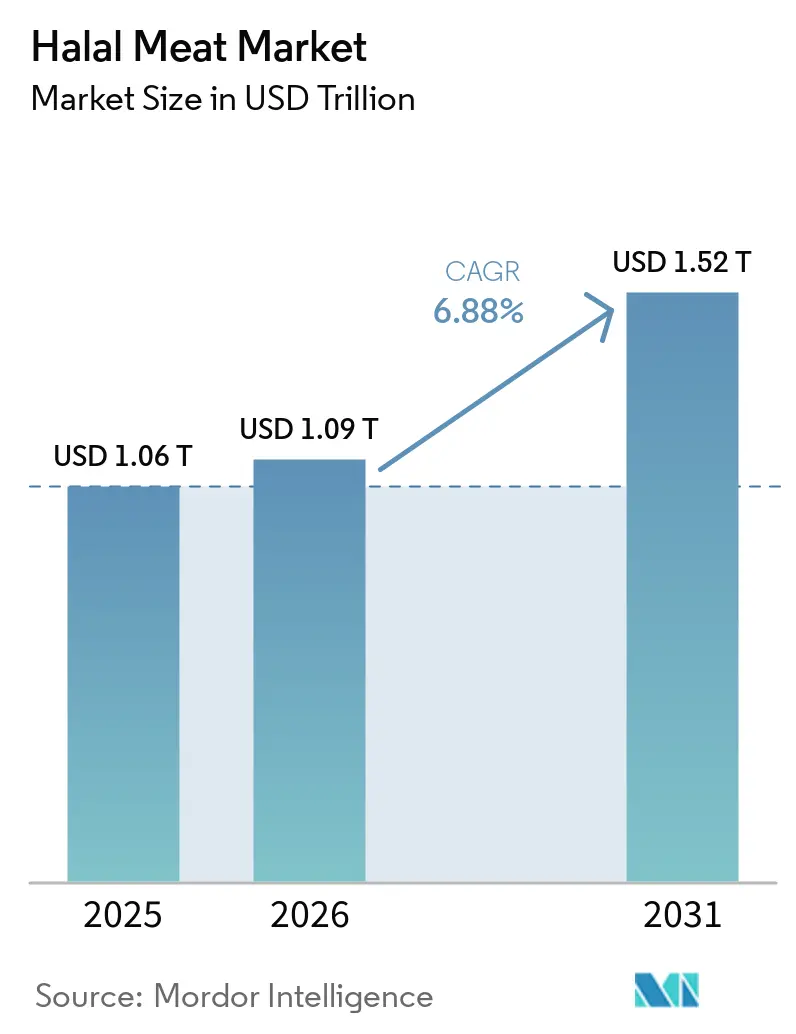

| Market Size (2026) | USD 1.09 Trillion |

| Market Size (2031) | USD 1.52 Trillion |

| Growth Rate (2026 - 2031) | 6.88% CAGR |

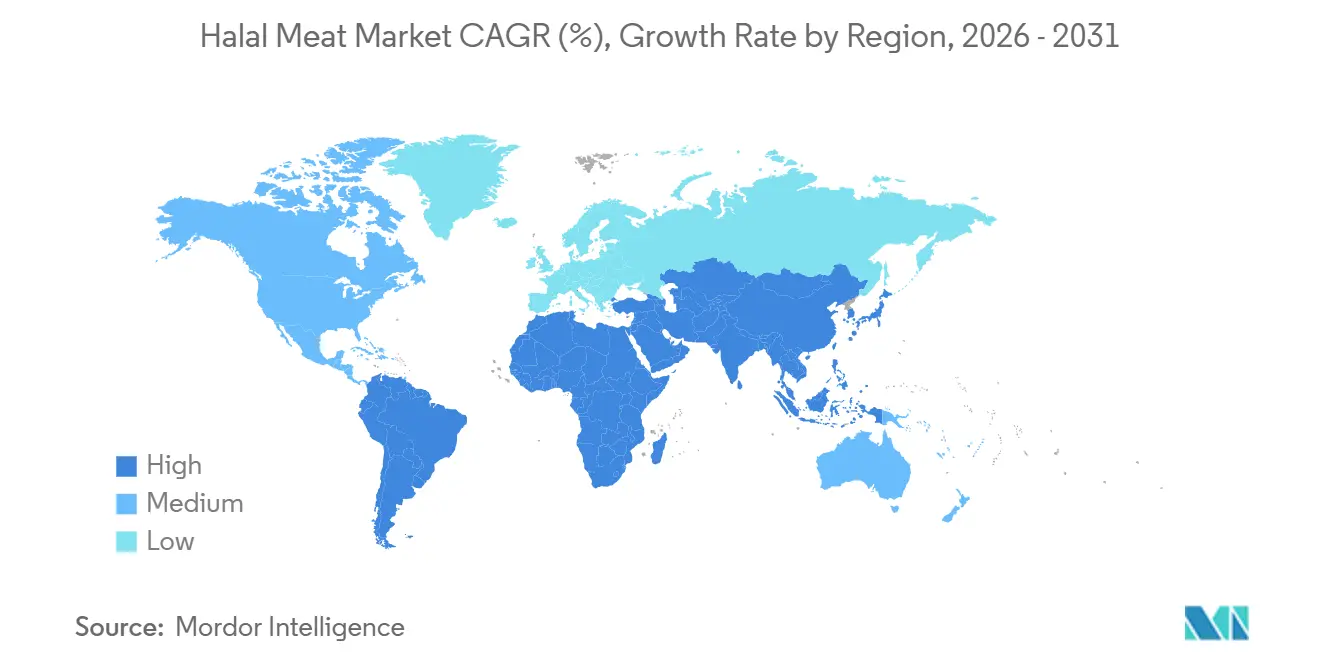

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Halal Meat Market Analysis by Mordor Intelligence

The halal meat market was valued at USD 1.06 trillion in 2025 and is estimated to grow to USD 1.09 trillion in 2026, with projections reaching USD 1.52 trillion by 2031, at a CAGR of 6.88% during 2026-2031. This growth is driven by increasing demand for halal-certified products, fueled by the expanding Muslim population and rising awareness of halal standards among non-Muslim consumers. Sovereign wealth funds are collaborating with multinational protein companies to relocate processing facilities to Muslim-majority countries, leveraging certification synergies, reducing freight costs, and ensuring adherence to halal compliance. The Middle East and Africa are witnessing the fastest growth, driven by initiatives such as Saudi Arabia's USD 2 billion livestock city, which aims to enhance local production capacity, and an increase in halal tourism, which boosts demand for halal food products. Poultry remains the dominant meat type due to its affordability, ease of preparation, and widespread cultural acceptance across various regions. The foodservice sector, particularly HoReCa, plays a key role in promoting halal products globally by catering to diverse consumer preferences and expanding halal menu options. In Europe, varying stunning regulations and fragmented national halal standards pose challenges to export flexibility but provide opportunities for companies capable of achieving multi-jurisdictional compliance, enabling them to access a broader market base.

Key Report Takeaways

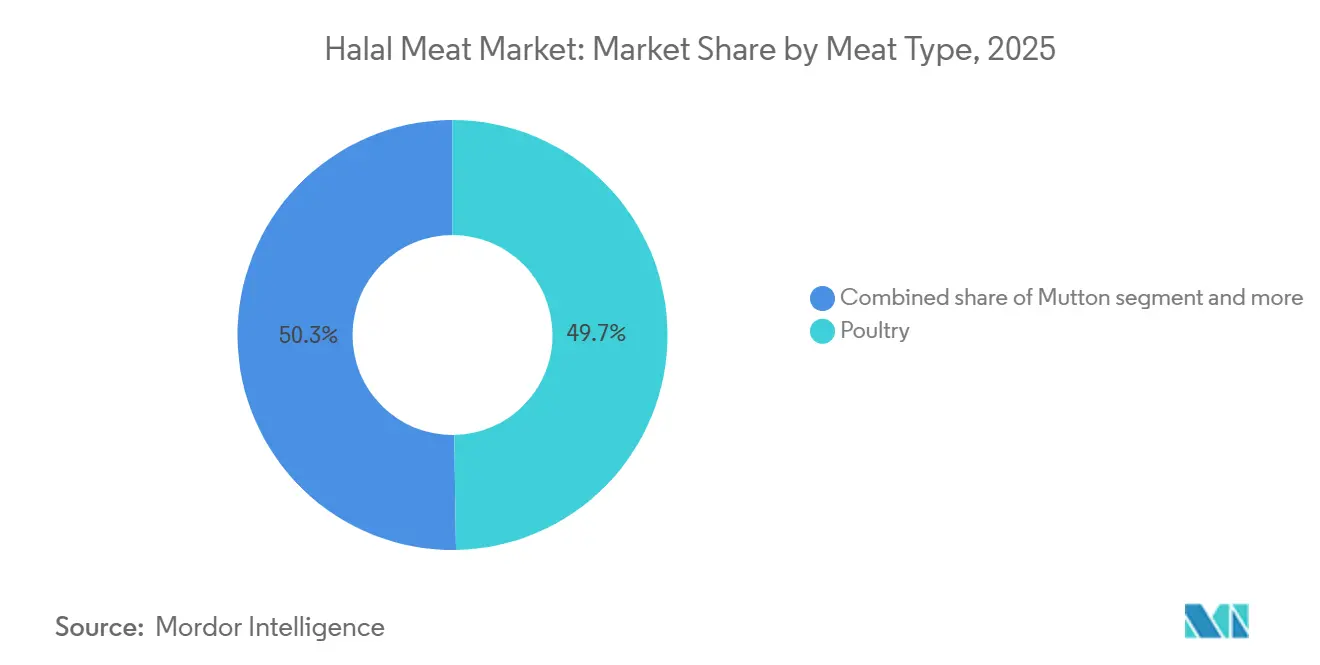

- By meat type, poultry led with 49.74% of the halal meat market share in 2025; mutton is poised to expand at a 3.56% CAGR through 2031.

- By form, fresh and chilled products held 49.21% of revenue in 2025, while processed lines are forecast to grow at a 2.97% CAGR through 2031.

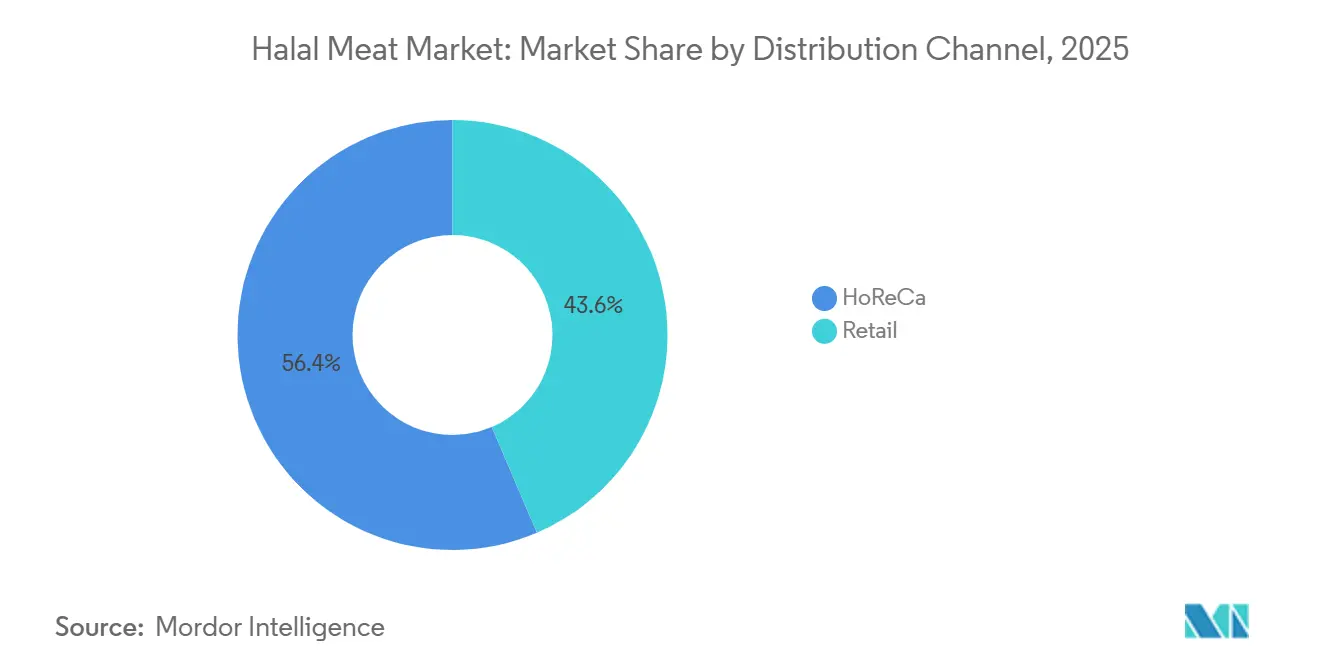

- By distribution channel, HoReCa controlled 56.4% of value in 2025; retail is expected to rise at a 3.21% CAGR supported by e-commerce and specialty outlets.

- By region, Asia-Pacific accounted for 49.52% of 2025 turnover; Middle East and Africa are expected to witness the fastest growth at a 2.89% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Halal Meat Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising awareness of halal certification | +1.2% | Asia-Pacific and Middle East | Medium term (2-4 years) |

| Expansion of halal food-service chains | +0.9% | North America, Europe, GCC (Gulf Cooperation Council), urban Asia-Pacific | Short term (≤2 years) |

| Government-backed halal ecosystems | +1.1% | Saudi Arabia, Oman, Nigeria, Indonesia | Long term (≥4 years) |

| Tourism growth in Muslim destinations | +0.8% | Saudi Arabia, United Arab Emirates, Turkey, Indonesia | Medium term (2-4 years) |

| Processed and packaged innovation | +0.7% | GCC, North America, Europe | Medium term (2-4 years) |

| Gen-Z demand for clean-label convenience | +0.6% | GCC, North America, Europe, urban Asia-Pacific | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Awareness of Halal Certification and Practices

Regulatory momentum is compressing certification timelines and expanding market access for compliant processors. India's Directorate General of Foreign Trade launched the I-CAS halal certification scheme in October 2024 and extended it to 20 additional countries in February 2026, enabling Indian exporters to bypass multiple bilateral audits and accelerate entry into Gulf and Southeast Asian markets[1]Source: Government of India, "Streamlining of Halal Certification Process for Meat and Meat Products-reg", apeda.gov.in . Indonesia's mandatory halal certification, administered by BPJPH (Badan Penyelenggara Jaminan Produk Halal) and MUI (Indonesian Ulema Council), reaches its October 2026 enforcement deadline, requiring all food products sold domestically to carry halal labels and creating a compliance floor that favors large-scale processors with in-house certification labs over artisanal producers[2]Source: Makarim & Taira S., “Halal Certification in Indonesia: Compliance Reminder and Upcoming Deadlines,” makarim.com. Malaysia's JAKIM (Jabatan Kemajuan Islam Malaysia) standard remains the de facto benchmark for cross-border trade, and its integration into ISO frameworks is pushing European and North American plants to adopt JAKIM-equivalent protocols to preserve export optionality, creating a compliance floor that favors large-scale processors with in-house certification labs over artisanal producers.

Expansion of Halal-Certified Foodservice Chains

Quick-service and fast-casual chains are embedding halal sourcing as a standard operating procedure rather than a niche accommodation, reshaping procurement patterns and elevating volume thresholds for suppliers. The Halal Guys announced 400 franchise locations in development across the United States in 2025, with new openings in Boston, Chicago, and Dallas, and Shah's Halal Foods committed to 50 new sites in the United Kingdom in 2025, signaling that halal-certified menus now drive unit economics in high-Muslim-population metros[3]Source: The Halal Guys, “A premium franchise opportunity with global momentum,” franchise.thehalalguys.com. Cargill supplies halal-compliant beef and chicken to McDonald's for select United States markets, demonstrating that tier-1 global chains are willing to bifurcate supply chains to capture incremental Muslim and non-Muslim consumers who associate halal with animal welfare and food safety. Chains' reliance on centralized distribution and long-term contracts favors processors with cold-chain infrastructure and traceability systems, effectively raising barriers for spot-market suppliers.

Government Initiatives Nurturing Halal Ecosystems

National strategies are channeling public capital into halal infrastructure to reduce import bills and position domestic industries as regional export hubs. Nigeria's National Halal Strategy targets a USD 1.5 billion GDP contribution by 2027 and USD 12 billion by 2030, with investments in slaughter facilities, cold storage, and certification bodies to formalize the informal halal trade and capture value currently leaking to imports. Saudi Arabia's Vision 2030 underpins JBS's USD 85 million Jeddah and Dammam expansion, which will double local poultry capacity by end-2026 and create 500 direct jobs, and Almarai's SAR 18 billion commitment to lift annual poultry output from 250 million to 450 million birds by 2026, both framed as food-security imperatives that also position the Kingdom as a re-export platform for Africa and South Asia. These state-backed partnerships reduce political risk for foreign investors while locking in long-term supply agreements that insulate host governments from import-price volatility.

Growth of Tourism in Muslim-Majority Countries

Inbound tourism is driving per-capita halal protein consumption in destinations that historically relied on imports to serve seasonal visitor surges. Mastercard and CrescentRating's Global Muslim Travel Index 2025 recorded 176 million Muslim arrivals in 2024, a 25% increase versus 2023, and projects 245 million arrivals by 2030 with aggregate spending reaching USD 230 billion, concentrated in Saudi Arabia, United Arab Emirates, Turkey, Indonesia, and Malaysia. Japan's Muslim population stood at 350,000 in 2024, with Tokyo hosting 298 halal-certified restaurants, and the 2026 Asian Games expected to accelerate halal food-service infrastructure in Aichi and surrounding prefectures. The Middle East and Africa region reflects this tourism multiplier, as hotel and catering contracts favor processors with JAKIM (Jabatan Kemajuan Islam Malaysia) or ESMA (Emirates Authority for Standardization and Metrology) certification and the cold-chain capacity to deliver consistent quality during peak pilgrimage and holiday periods. The interplay between religious tourism and halal demand also creates procurement volatility, with processors needing to balance year-round export commitments against seasonal spikes that can double local offtake within weeks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Conflicting halal standards | −0.5% | Asia-Pacific, Middle East, Europe, North America | Long term (≥4 years) |

| High certification costs | −0.4% | SMEs (Small Manufacturing Enterprises) in Asia-Pacific, Africa, emerging markets | Medium term (2-4 years) |

| Animal-welfare activism on stunning | −0.3% | Netherlands, Belgium, France, spillover to North America | Medium term (2-4 years) |

| Cold-chain gaps in emerging hubs | −0.3% | Kenya, Nigeria, Pakistan | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Fragmented and conflicting global halal standards

The absence of a unified halal standard forces processors to navigate a patchwork of national certifiers, each with distinct slaughter protocols, ingredient blacklists, and audit frequencies that inflate compliance costs and delay market entry. Malaysia's JAKIM certification is recognized across Southeast Asia and parts of the Middle East, but Indonesia's BPJPH (Badan Penyelenggara Jaminan Produk Halal) and MUI (Indonesian Ulema Council) require separate audits even for JAKIM (Jabatan Kemajuan Islam Malaysia)-certified plants, and the United Arab Emirates's ESMA (Emirates Authority for Standardization and Metrology) and Saudi Arabia's SFDA (Saudi Arabia Food and Drug Authority) impose additional documentation for imported products, effectively requiring exporters to maintain parallel certification tracks for each destination. EU case law lets member states mandate pre-slaughter stunning, splitting Belgium and the Netherlands from France and Germany. This divergence penalizes mid-sized processors that lack the legal and technical resources to manage multi-jurisdictional compliance, and it creates arbitrage opportunities for large integrators that can shift production across borders to exploit regulatory gaps.

High certification and documentation compliance costs

Certification fees and recurring audit expenses disproportionately burden small and medium enterprises, raising the floor for market entry and consolidating share among vertically integrated players. In the United States, halal certification costs range from USD 500 to USD 2,500 for initial applications, USD 1,000 to USD 5,000 for on-site audits, and USD 500 to USD 3,000 for annual renewals, with a typical first-year total of approximately USD 2,900 for a small bakery, USD 14,700 for a medium manufacturer, and USD 128,000 for a large multinational. Indonesia's BPJPH (Badan Penyelenggara Jaminan Produk Halal) charges IDR 300,000 to IDR 12.5 million for applications and IDR 700,000 to IDR 2.45 million for certification. A 2025 study of Indonesian MSMEs (Micro, Small, and Medium Enterprises) found that financial constraints, digital literacy gaps, and regulatory complexity were the primary barriers to halal certification adoption, suggesting that the current fee structure effectively excludes informal producers who dominate local supply in emerging markets. These cost dynamics favor processors with captive certification labs and legal teams, accelerating consolidation and reducing supplier diversity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Meat Type: Poultry Dominates, Mutton Gains Premium Traction

In 2025, poultry held 49.74% of the market share due to affordability, Islamic acceptance, and efficient broiler operations. JBS's USD 85 million Saudi expansion and Almarai's SAR 18 billion investment will boost poultry output by 2026, positioning the Kingdom as a re-export hub for Africa and South Asia. Beef remains significant in markets like Brazil, Australia, and the United States, leveraging JAKIM (Jabatan Kemajuan Islam Malaysia) and ESMA (Emirates Authority for Standardization and Metrology) certifications to access Gulf and Southeast Asian buyers.

Mutton is projected to grow at a 3.56% CAGR through 2031, driven by its premium status in Middle Eastern and South Asian cuisines and limited supply elasticity. JBS's joint venture with Oman Food Capital includes Al Bashayer Meat Company's Thumrait facility, targeting a daily throughput of 5,000 lambs and positioning Oman as a regional lamb hub. Halal-certified mutton offers margins for processors focusing on traceability, though its market is limited to affluent households and special occasions.

By Form: Fresh/Chilled Leads, Processed Gains on Convenience

Fresh and chilled halal meat, with a 49.21% share, benefited from perceived quality, traditional butchery ties, and preservative-free appeal, though it faced margin pressures from cold-chain costs and spoilage risks. Frozen halal products dominated export corridors and long-haul trade routes, supported by innovations in blast-freezing and modified-atmosphere packaging that preserved quality and enabled inventory management during low-cost periods.

Processed halal meat is projected to grow at a 2.97% CAGR through 2031, driven by urbanization, dual-income households, and demand for convenience in ready-to-eat and ready-to-cook formats. MBRF's Sadia Halal expanded capacity with a 25,000-tonne Kezad facility and a planned 40,000-tonne Jeddah plant to boost processed share and reduce exposure to chicken-price volatility. Companies like Midamar and Cargill are incorporating clean-label and plant-based attributes into halal products to attract health-conscious consumers, though SKU (Stock Keeping Units) proliferation.

By Distribution Channel: HoReCa Dominates, Retail Accelerates Online

In 2025, HoReCa channels captured 56.4% of the market share, driven by quick-service restaurants, hotel catering, and airline provisioning in Muslim-majority nations and high-Muslim-population metros. The expansion of The Halal Guys and Shah's Halal Foods, along with Cargill's supply agreements with McDonald's, highlights the growing importance of halal-certified menus and bifurcated supply chains to attract both Muslim and non-Muslim consumers. Centralized procurement and long-term contracts favor large integrators with cold-chain infrastructure and traceability systems, raising barriers for smaller suppliers.

Retail is projected to grow at a 3.21% CAGR through 2031, led by online platforms, specialty stores, and supermarket halal sections targeting diaspora households and non-Muslim consumers. United States halal e-commerce platforms reported significant growth in 2024, with Amazon and DagangHalal showing notable increases in halal-related searches and sales. Supermarkets are expanding halal aisles and partnering with specialty brands, while specialty stores retain loyal customers but face competition from online platforms.

Geography Analysis

In 2025, Asia-Pacific held a 49.52% market share, driven by Indonesia's mandatory halal certification deadline in October 2026, favoring large-scale processors over artisanal producers. India's I-CAS halal scheme expansion to 20 export markets by February 2026 positions it as a cost-effective alternative to Australian and Brazilian suppliers. Malaysia's JAKIM (Jabatan Kemajuan Islam Malaysia) standards dominate cross-border trade, while QL Resources' RM 1.3 billion Innofood Park highlights the capital intensity required for halal production. Japan's Muslim population of 350,000 in 2024 and the 2026 Asian Games are spurring halal infrastructure development, even in low-Muslim-share markets. China, Australia, Thailand, and Singapore hold smaller shares, with China's Henan plant by MBRF enabling local processing for domestic and regional buyers.

The Middle East and Africa are projected to grow at a 2.89% CAGR through 2031, driven by Saudi Vision 2030 and Oman Vision 2040, which aim to reduce import dependency and establish the Gulf as a re-export hub. JBS's USD 235 million investment in Saudi and Omani facilities targets a 300,000-tonne multi-protein platform and expanded poultry capacity by 2026. MBRF's USD 2.07 billion Sadia Halal joint venture with Saudi Arabia's Public Investment Fund aims to create the world's largest halal chicken company, with a 2027 Riyadh IPO planned Global Business Outlook. Nigeria's National Halal Strategy targets USD 1.5 billion GDP by 2027 and USD 12 billion by 2030, while Turkey's Banvit brand bridges European and Middle Eastern supply chains Nigeria National Halal Strategy.

North America, Europe, and South America account for the remaining market share, driven by diaspora demand and non-Muslim consumers associating halal with ethical sourcing. The United States halal food market, supported by a growing Muslim population and rising non-Muslim interest. Europe faces regulatory challenges, but the United Kingdom.'s 88% pre-stunned halal share and France's permissive stance offer opportunities. Brazil remains the largest halal meat exporter, with MBRF and JBS shifting investments into Gulf manufacturing to capture higher margins and mitigate freight-cost volatility.

Competitive Landscape

The halal meat market exhibits a fragmented competitive structure with a low concentration score, yet the past 18 months have witnessed a consolidation wave driven by sovereign wealth funds and multinational protein majors deploying balance-sheet heft to build greenfield halal hubs in the Gulf. JBS committed USD 235 million to Saudi and Omani facilities, Tyson Foods acquired 60% of Saudi processor Supreme Foods and formed a 50:50 joint venture with Tanmiah to explore global halal opportunities, and MBRF injected USD 2.07 billion of Middle Eastern assets into a joint venture with Saudi Arabia's Public Investment Fund and Halal Products Development Company, creating the Sadia Halal entity with a planned 2027 Riyadh Initial Public Offering. These partnerships reflect a strategic pivot from export-led models to in-region manufacturing, reducing freight exposure and capturing certification efficiencies.

White-space opportunities exist in processed halal products, plant-based halal proteins, and blockchain traceability, with Midamar Corporation's all-natural halal beef jerky and Cargill's deployment of farm-to-table verification systems illustrating how mid-tier players are carving defensible niches through transparency and ingredient simplicity rather than volume Halal Times. Emerging disruptors include specialty halal-only brands leveraging e-commerce and social media to capture Gen-Z and non-Muslim consumers who associate halal with ethical sourcing, and regional processors in Nigeria, Kenya, and Pakistan that are formalizing informal supply chains with public capital and targeting domestic and sub-Saharan African export markets.

Technology adoption is bifurcating the industry, with large integrators deploying Industry 4.0 solutions-IoT sensors, RFID tags, AI-driven quality monitoring, and blockchain traceability to manage multi-jurisdictional compliance and reduce spoilage, while smaller players rely on manual audits and paper-based documentation that limit export reach and raise per-unit costs. Janan Meat Limited's deployment of blockchain QR codes that link each package to farm and slaughter records demonstrates how traceability technology can command premiums in diaspora and health-conscious segments, yet the absence of interoperable standards means that each processor's blockchain remains a proprietary silo that limits network effects and raises switching costs for buyers.

Halal Meat Industry Leaders

-

JBS S.A.

-

BRF S.A.

-

Midamar Corporation

-

Al Islami Foods

-

Almarai Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: JBS S.A. announced an investment of approximately USD 85 million to expand its poultry processing operations in Saudi Arabia. The expansion aims to significantly increase production capacity at its Jeddah facility.

- November 2025: Deli Halal launched a new range of halal-certified sliced meat products across the United Kingdom. The product line features ready-to-eat deli-style meats that comply with strict halal certification standards, while focusing on enhanced ingredient quality.

- January 2025: Cargill acquired two case-ready meat plants from Ahold Delhaize United States, boosting the Northeast United States supply of packaged beef, pork, and value-added halal lines.

Global Halal Meat Market Report Scope

Halal meat is defined as meat prepared in compliance with Islamic dietary laws (Shariah). This requires the animal to be healthy at the time of slaughter, killed by a Muslim while invoking the name of Allah, and fully drained of blood. Pork and other prohibited animals are excluded. The Halal Meat market is segmented by meat type, form, distribution channel, and geography. By meat type, the market is segmented by poultry, beef, mutton, and others. By form, the market is segmented by fresh/chilled, frozen, and processed. By distribution channel, the market is segmented by HoReCa and retail. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The report offers market size and forecasts in value (USD million) and volume (Tons) for the above segments.

| Poultry |

| Beef |

| Mutton |

| Others |

| Fresh/Chilled |

| Frozen |

| Processed |

| HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Speciality Stores | |

| Online Retail Stores | |

| Other Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Africa |

| By Meat Type | Poultry | |

| Beef | ||

| Mutton | ||

| Others | ||

| By Form | Fresh/Chilled | |

| Frozen | ||

| Processed | ||

| By Distribution Channel | HoReCa | |

| Retail | Supermarkets/Hypermarkets | |

| Speciality Stores | ||

| Online Retail Stores | ||

| Other Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast will the halal meat market grow between 2026 and 2031?

It is set to expand from USD 1.09 trillion to USD 1.52 trillion at a 6.88% CAGR.

Which meat type is projected to climb the quickest?

Mutton will advance at a 3.56% CAGR through 2031 on Middle Eastern and South Asian premium demand.

What channel leads current sales?

HoReCa holds 56.4% of 2025 revenue due to scale procurement by restaurants and caterers.

Which region will record the highest growth rate?

Middle East & Africa will rise at a 2.89% CAGR as Gulf investments boost local supply.

Page last updated on: