Canned Meat Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 79.81 Billion |

| Market Size (2031) | USD 89.99 Billion |

| Growth Rate (2026 - 2031) | 2.43% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

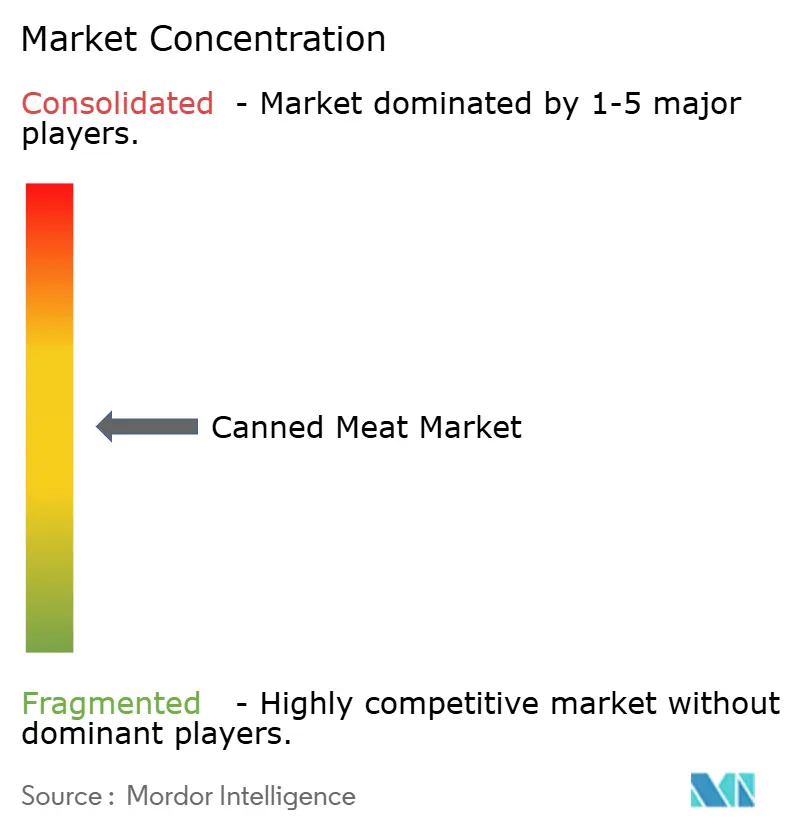

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canned Meat Market Analysis by Mordor Intelligence

The canned meat market size is expected to grow from USD 78.32 billion in 2025 to USD 79.81 billion in 2026 and is forecast to reach USD 89.99 billion by 2031 at 2.43% CAGR over 2026-2031. The market's growth is driven by increasing demand for shelf-stable protein options, particularly among governments, fitness-conscious consumers, and time-constrained households. Canned meat offers a practical solution by eliminating the need for cold-chain logistics, making it a preferred choice in various scenarios. Single-serve cans are gaining popularity, especially in urban areas where smaller household sizes are prevalent. Advancements in preservation technologies, such as high-pressure processing, microwave-assisted thermal sterilization, and cold-plasma surface treatment, are enhancing the shelf life of canned meat while maintaining its texture and flavor. Military and humanitarian agencies play a significant role in stabilizing demand through long-term contracts, which provide a steady foundation for production planning. Furthermore, sustainability trends are reshaping the market, with retailers increasingly requiring traceability, lower-sodium formulations, and (Bisphenol-A) BPA-free packaging.

Key Report Takeaways

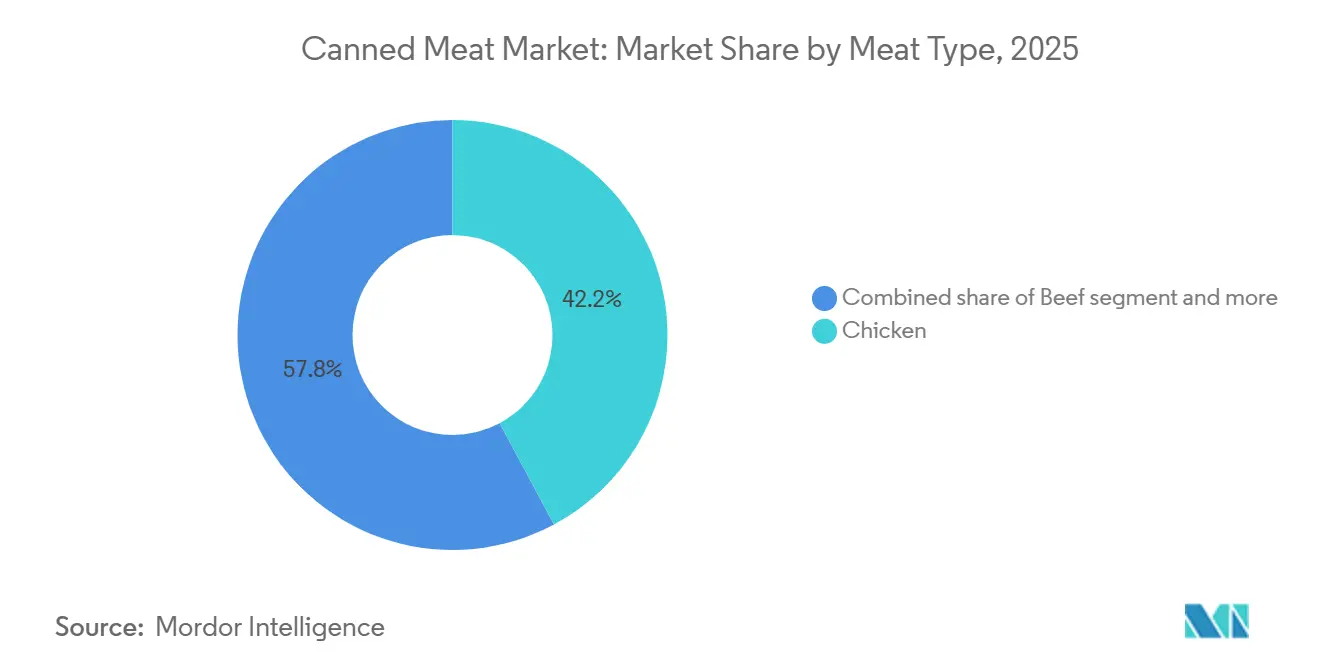

- By meat type, chicken led with 42.18% of the canned meat market share in 2025, whereas pork is forecast to grow at a 2.67% CAGR through 2031.

- By form, luncheon meat captured 43.05% of the revenue share in 2025; sausage is set to register the fastest CAGR of 2.98% to 2031.

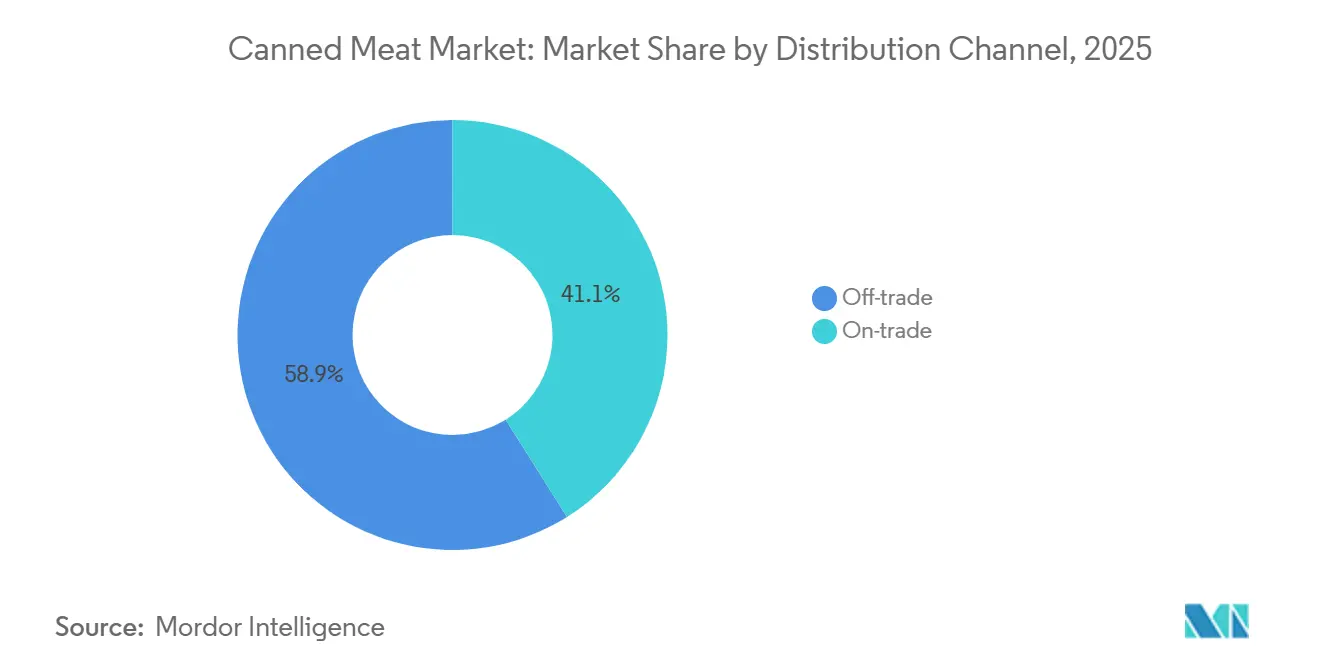

- By distribution channel, the off-trade segment held 58.97% share of the canned meat market size in 2025, while the on-trade segment is projected to expand at 3.03% through 2031.

- By geography, North America commanded 31.05% of the canned meat market in 2025; Asia-Pacific is poised for the highest 3.21% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Canned Meat Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Young consumers increasingly favor single-serve luncheon meats | +0.4% | North America, Europe, Asia Pacific (urban centers) | Short term (≤ 2 years) |

| Modern storage needs are being met by advanced preservation technologies | +0.5% | Global, with early adoption in North America, and Europe | Medium term (2-4 years) |

| Fitness enthusiasts are opting for protein-rich, shelf-stable diets | +0.3% | North America, Europe, and Australia | Short term (≤ 2 years) |

| Governments are procuring meats for military and disaster-relief stockpiles | +0.6% | Global | Long term (≥ 4 years) |

| Sustainability certifications and traceability are influencing consumer purchases | +0.3% | Europe, North America, Asia-Pacific premium segments | Medium term (2-4 years) |

| Convenience and extended shelf life are fueling the rise in canned meat consumption | +0.5% | Global, strongest in Asia-Pacific and urban North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Young consumers increasingly favor single-serve luncheon meats

Portion-controlled packaging is transforming retail assortments as millennials and Gen Z households increasingly focus on reducing waste and maintaining calorie transparency, moving away from bulk purchases. Single-serve cans, which do not require refrigeration after opening, are particularly appealing to urban apartment dwellers and mobile professionals who often lack consistent access to cold storage. This trend has driven a shift toward grab-and-go protein formats that fit conveniently into backpacks and office drawers. In response, manufacturers are innovating by introducing smaller can sizes and advanced resealable packaging technologies, improving product usability and extending shelf life after opening. Additionally, the growing urbanization in tier-1 and tier-2 cities, particularly in Asia, is leading to smaller kitchen spaces, further driving demand for single-serve canned products. These factors are contributing to the sustained growth and deeper market penetration of the canned meat segment.

Modern storage needs are being met by advanced preservation technologies

Advancements in preservation technologies, such as High-pressure Processing (HPP) and Microwave-Assisted Thermal Sterilization (MATS), are revolutionizing the canned meat market by extending shelf life without compromising nutrient retention. These innovations enable brands to expand their reach to remote markets, cruise lines, and e-commerce dark stores without relying on cold-chain logistics. Additionally, there are growing opportunities for integrating renewable energy solutions to reduce greenhouse gas emissions, aligning with global sustainability goals. While retort sterilization remains the industry standard, emerging technologies like cold plasma surface treatment are gaining traction, particularly in Europe, where regulatory frameworks support non-thermal interventions. These methods help preserve the color and flavor compounds often lost in conventional heat processing, enhancing product appeal. Furthermore, these advancements are driving premium product positioning. These technological developments also address urban storage constraints by reducing refrigeration needs for small households and facilitating e-commerce fulfillment.

Fitness enthusiasts are opting for protein-rich, shelf-stable diets

Athletes and active-lifestyle consumers are increasingly opting for protein-rich, shelf-stable canned meats as portable macro sources. Products like canned chicken breast, which deliver approx 20-25 grams of protein, have become meal-prep staples for bodybuilders and endurance training enthusiasts. According to the Organisation for Economic Co-operation and Development (OECD), global meat consumption is projected at 479 million metric tons by 2034, reflecting the growing demand for canned meat products [1]Source: Organisation for Economic Co-operation and Development, "Meat: OECD-FAO Agricultural Outlook 2025-2034", oecd.org. However, the health-conscious segment has shown increased sensitivity to sodium content and preservatives. This demographic change increasingly values transparency, prompting brands to incorporate QR codes on packaging that link to third-party lab results for protein content and heavy-metal testing. Additionally, the convenience and long shelf life of canned meats make them an attractive option for urban households with limited storage space. These factors, combined with the growing focus on clean-label products, are driving the adoption of premium SKUs in fitness-focused retail chains and online platforms.

Governments are procuring meats for military and disaster-relief stockpiles

Governments worldwide are increasing canned meat procurement for military and disaster-relief stockpiles, ensuring consistent demand that stabilizes production and supports capacity expansion for shelf-stable proteins capable of withstanding extreme conditions. For instance, the United States Defense Logistics Agency solicited bids for a USD 435 million food contract to provide full-line food distribution services to U.S. military and federal customers across South Korea, covering meats and perishables, including canned meat [2]Source: U.S. System for Award Management, “Solicitation/Request for Proposal (RFP) for Subsistence Prime Vendor (SPV) Support for Republic of Korea”, sam.gov. Similarly, countries like India maintain significant food reserves through organizations such as the Food Corporation of India (FCI), ensuring food security during emergencies. These contracts typically favor established manufacturers with robust food safety systems and the scale to meet large orders promptly, often excluding smaller producers lacking ISO 22000 certification. Additionally, the growing focus on emergency preparedness, driven by recent supply chain disruptions and natural disasters, has highlighted the strategic importance of shelf-stable protein sources.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Sodium content and preservatives in products shape consumer buying habits | -0.5% | North America, Europe, and Australia | Short term (≤ 2 years) |

| Disposing of metal cans poses environmental challenges, sparking sustainability debates | -0.3% | Europe, North America, Asia-Pacific (urban centers) | Medium term (2-4 years) |

| Fluctuating raw material prices hinder market expansion prospects | -0.4% | Global, acute in South America and Asia-Pacific | Short term (≤ 2 years) |

| Consumers increasingly favor fresh, unprocessed food items | -0.6% | North America, Europe, and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sodium content and preservatives in products shape consumer buying habits

Health-conscious consumers are increasingly scrutinizing nutrition labels, with sodium levels becoming a significant factor in purchasing decisions. This trend is particularly evident in markets where hypertension awareness campaigns have heightened sensitivity to dietary salt intake. Traditional canned meats often contain 600 to 900 milligrams of sodium per serving, accounting for 40% to 60% of the WHO (World Health Organization)-recommended daily limit of 2000 mg, highlighting the growing recognition of excessive sodium's adverse effects on cardiovascular health [3]Source: World Health Organization, "Reducing population sodium/salt intake", who.int. As a result, manufacturers are reformulating products to balance microbial safety with cardiovascular health messaging. Nitrate and nitrite preservatives, traditionally used to prevent botulism and maintain color, are facing increasing consumer backlash despite regulatory approval. In response, brands are experimenting with alternatives such as celery powder and sea salt, marketed as "natural" options. The market is also witnessing a divide between premium, low-sodium products and traditional, high-sodium offerings.

Consumers Increasingly Favor Fresh, Unprocessed Food Items

The clean-eating movement is influencing consumer preferences, shifting grocery budgets toward fresh meat counters and plant-based proteins. Younger demographics, in particular, are expressing skepticism toward ultra-processed foods, despite their convenience. Social media influencers and nutrition advocates often portray canned meat as nutritionally inferior, citing concerns such as BPA leaching from can linings and the loss of heat-sensitive vitamins during sterilization. However, studies indicate minimal health impact at typical consumption levels. This perception gap is more pronounced in affluent markets, where consumers can afford the higher price and shorter shelf life of fresh protein. In contrast, emerging economies with limited cold-chain infrastructure continue to rely heavily on shelf-stable formats due to their practicality and affordability. To address these concerns, processors are adopting strategies such as transparent sourcing narratives and reformulated products that emphasize simple ingredient lists like "just chicken and sea salt", to rebuild consumer trust.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Meat Type: Pork Gains Momentum Across Asia-Pacific

In 2025, chicken claimed the top spot in the canned meat market, seizing a notable 42.18% share. This dominance is driven by its cost advantage, religious neutrality, and versatility across global cuisines. Chicken's adaptability to diverse preservation methods, such as retort sterilization and high-pressure processing, allows manufacturers to offer various texture profiles, including shredded, chunk-style, and cold-plasma-cooked strips. These formats cater to a wide range of applications, from salads and sandwiches to keto snacks and casseroles. Additionally, the growing demand for protein-rich and convenient meal options has further solidified chicken's position in the market.

Conversely, pork is set to outpace all other meats, boasting a projected CAGR of 2.67% through 2031. Rising incomes in countries like China, Vietnam, and the Philippines are driving the consumption of luncheon meats and sausages that align with regional taste preferences. Pork's faster growth trajectory is tied to premiumization, as artisanal sausages and charcuterie-inspired canned products command higher margins compared to chicken. Pork-based SPAM variants dominate convenience stores across the Asia-Pacific region. In response to this momentum, processors are increasingly prioritizing pork in their production lines. The enduring appeal of beef-based canned products is attributed to their rich flavor and long shelf life, making them a staple in many households.

By Form: Sausage Innovations Drive Premium Segment Growth

In 2025, luncheon meat captured 43.05% of the market share, reflecting its entrenched position in breakfast and sandwich applications. This growth is supported by its affordability, long shelf life, and versatility, making it a convenient choice for consumers across various demographics. While the North American market shows signs of saturation with stable per-capita consumption, the Asia-Pacific region continues to drive volume growth. Urbanization and the expansion of convenience stores in this region have significantly boosted the demand for canned protein products.

Canned sausage is expected to grow rapidly, boasting a projected 2.98% CAGR through 2031. This surge is driven by innovation in flavor profiles and clean-label reformulations that appeal to younger, health-conscious buyers willing to pay premiums for organic or nitrate-free products. Manufacturers are introducing ethnic flavors, organic formulations, and reduced-sodium variants that command premium retail prices. For instance, Tyson Foods launched a line of chicken sausages featuring turmeric and black pepper blends inspired by Southeast Asian cuisines. Additionally, the growing popularity of ready-to-eat meals and snacks has further propelled the demand for canned sausages.

By Distribution Channel: On-Trade Recovery Accelerates Post-Pandemic

In 2025, off-trade distribution channels accounted for 58.97% of the total revenue in the canned meat market. Supermarkets and hypermarkets remain the dominant off-trade sub-channel, offering a wide variety of canned meat products at competitive prices. Additionally, online retailers are steadily capturing market share from traditional brick-and-mortar stores. These platforms benefit from lower overhead costs and data-driven personalization, enabling them to cater to specific consumer preferences. E-commerce penetration in the canned meat market is increasing, driven by subscription models, same-day delivery services, and the convenience of shopping from home. This shift reflects changing consumer behavior, as more individuals prioritize accessibility and time-saving solutions when purchasing canned meat products.

The on-trade distribution segment is expanding at a CAGR of 3.03% through 2031. This growth is fueled by the resurgence of the hospitality sector, where quick-service restaurants, hotels, cruise lines, and airline caterers are rebuilding inventories after pandemic-era disruptions. Foodservice operators value the operational simplicity of canned meat, which requires no thawing, minimal preparation, and offers extended shelf life. These attributes make canned meat a cost-effective and reliable protein source for high-volume kitchens serving schools, hospitals, and corporate cafeterias. The reopening of these channels has not only boosted demand but also encouraged suppliers to innovate and expand their product offerings. For instance, manufacturers are introducing premium canned meat options and flavor-enhanced variants to cater to the evolving needs of the foodservice industry and meet consumer expectations for quality and variety.

Geography Analysis

In 2025, North America holds a 31.05% market share, driven by entrenched household consumption, longstanding military contracts, and an omnichannel retail infrastructure that allots shelf space from dollar stores to premium grocery chains. U.S. Federal Emergency Management Agency’s stockpile expansion after violent hurricane seasons, along with Defense Logistics Agency awards, ensures a consistent baseline production run for major players like Hormel, Conagra, and Smithfield. The region benefits from supportive regulatory frameworks and industry consolidation, enabling cost efficiencies in production and distribution. Food and Drug Administration (FDA) sodium-reduction targets and BPA-free mandates require capital investment that most smaller labels cannot shoulder, further strengthening the position of established players in the canned meat market. Additionally, Canada’s Arctic territories rely heavily on canned protein due to prohibitive chilled-freight costs, maintaining high volume per capita despite the continent-wide pivot toward fresh meat and flexitarian lifestyles.

Asia-Pacific is emerging as the fastest-growing region, with a projected CAGR of 3.21% through 2031. This growth is fueled by urbanization, rising disposable incomes, and the rapid penetration of e-commerce, which is making shelf-stable protein accessible to tier-2 and tier-3 cities that were previously underserved by modern retail. The region's growth trajectory reflects a shift in dietary preferences, with greater diversification and a growing acceptance of Western food formats. For instance, China's pork-based luncheon meat consumption surged in 2025 as convenience stores proliferated in megacities, catering to the fast-paced lifestyles of urban consumers. Similarly, Indonesia, Vietnam, and the Philippines are emerging as high-growth markets where young, mobile workforces prioritize grab-and-go meals over traditional home cooking.

Europe's regulatory environment emphasizes clean-label formulations, recyclable packaging, and animal-welfare standards, pushing incumbents to reformulate products and invest in BPA-free can linings that comply with EU directives taking effect in 2027. Germany, the United Kingdom, and France lead per-capita consumption, with artisanal sausage and pâté formats commanding premium prices in specialty retailers. At the same time, Eastern European markets favor affordability-focused corned beef and luncheon meat, which remain staples in many households. The region also sees growing interest in organic and sustainably sourced canned meat products, reflecting broader consumer trends toward ethical and environmentally friendly food choices.

Competitive Landscape

The canned meat market exhibits moderate concentration, with multinational companies such as Hormel Foods Corporation, Tyson Foods, Inc., and JBS S.A. coexisting alongside regional specialists and private-label suppliers that capture market share through localized flavors and competitive pricing strategies. These key players leverage scale advantages in procurement, retort sterilization capacity, and distribution networks that span retail, foodservice, and government channels. However, smaller players are capitalizing on niche opportunities in organic, ethnic, and single-serve formats, where agility and innovation provide a competitive edge.

Leading companies are increasingly adopting vertical integration and advanced technologies to strengthen their market position while addressing evolving consumer preferences and regulatory requirements. For instance, JBS S.A. controls cattle ranching through processing and canning, which helps mitigate raw-material price volatility, while Tyson Foods utilizes MATS (Microwave-Assisted Thermal Sterilization) technology to achieve energy efficiency and product differentiation. The adoption of innovative technologies, such as high-pressure processing and blockchain-based traceability, is becoming a significant factor in gaining a competitive advantage.

Emerging players in the market include plant-based protein brands that are introducing shelf-stable, canned alternatives aimed at flexitarian consumers. Sustainability is becoming a central focus for market players, with companies investing in eco-friendly packaging and sustainable sourcing practices to align with consumer expectations. Additionally, the rise of e-commerce platforms is reshaping distribution strategies, enabling companies to reach a broader customer base more efficiently. Regulatory compliance remains a critical factor in the market. Adherence to ISO 22000 food safety standards and FSMA (Food Safety Modernization Act) preventive controls creates barriers to entry, favoring established players with robust quality assurance systems.

Canned Meat Industry Leaders

-

Tyson Foods, Inc.

-

JBS S.A.

-

Conagra Brands, Inc.

-

Hormel Foods Corporation

-

Bolton Group S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Tyson Foods, Inc. announced the launch of New Wright Brand Premium Smoked Sausage Links to meet consumer demand for high-quality smoked meat products, with 12-13g of protein. The new product line includes three distinct varieties of Applewood, White Cheddar, and Bacon, and Bacon, Cheddar, and Jalapeño sausage.

- May 2025: D’Artagnan, a leader in premium meats, has introduced a new range of gourmet canned meats. These products are made with high-quality ingredients and innovative flavors, targeting consumers seeking a premium alternative in the canned meat market.

- February 2025: JBS S.A. announced an investment of USD 200 million to expand US beef production at two facilities. USD 150 million will be used to build a new production floor and expand the beef room at its plant in Cactus, Texas, and an additional USD 50 million to construct a new distribution center in Greeley, Colorado.

Global Canned Meat Market Report Scope

Meat preserved in cans or tins is called canned meat. Meat is typically chopped and canned for long-term preservation, whether cooked or raw. The Canned Meat Market Report is Segmented by Meat Type (Beef, Chicken, and More), Form (Corned Beef, Luncheon Meat, Sausage, and More), Distribution Channel (Off-Trade and On-Trade), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Beef |

| Chicken |

| Pork |

| Others |

| Corned Beef |

| Luncheon Meat |

| Sausage |

| Others |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retailers | |

| Other Distribution Channels | |

| On-Trade |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Russia | |

| Norway | |

| Sweden | |

| Denmark | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Malaysia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of the Middle East and Africa |

| By Meat Type | Beef | |

| Chicken | ||

| Pork | ||

| Others | ||

| By Form | Corned Beef | |

| Luncheon Meat | ||

| Sausage | ||

| Others | ||

| By Distribution Channel | Off-Trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | ||

| Online Retailers | ||

| Other Distribution Channels | ||

| On-Trade | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Norway | ||

| Sweden | ||

| Denmark | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the canned meat market?

The canned meat market reached USD 79.81 billion in 2026 and is forecast to reach USD 89.99 billion by 2031.

Which region is growing fastest in canned meat sales?

Asia-Pacific is expected to post a 3.21% CAGR between 2026 and 2031, the highest among all regions.

Which meat type is expanding the quickest?

Pork is projected to grow at a 2.67% CAGR through 2031, outpacing chicken and beef segments.

What is driving the shift toward single-serve cans?

Waste reduction, calorie transparency, and urban apartment living encourage younger consumers to choose two-ounce pull-tab formats.

Page last updated on: