Organic Meat Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 23.59 Billion |

| Market Size (2031) | USD 34.43 Billion |

| Growth Rate (2026 - 2031) | 7.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Meat Market Analysis by Mordor Intelligence

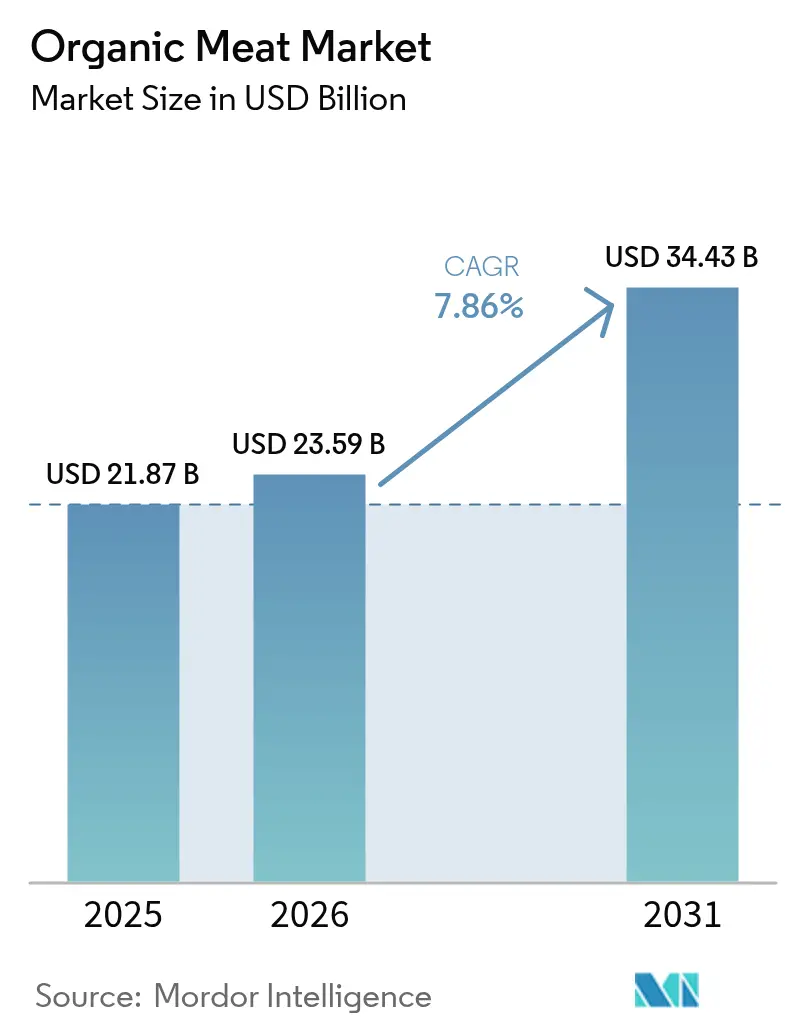

The organic meat market size was valued at USD 21.87 billion in 2025 and estimated to grow from USD 23.59 billion in 2026 to reach USD 34.43 billion by 2031, at a CAGR of 7.86% during the forecast period (2026-2031). This growth is driven by increasing health awareness, the expansion of high-income urban populations, and the enforcement of stricter organic certification standards. These factors are pushing consumers toward premium protein options that offer cleaner ingredient profiles and adhere to verifiable animal welfare practices. The adoption of technology-enabled traceability solutions, such as blockchain pilots by leading processors, is enabling brands to maintain price premiums in a fragmented yet highly dynamic market. Additionally, investors are actively funding capacity expansion projects in North America and Asia-Pacific, where demand continues to surpass supply. In the European Union, policy measures are incentivizing producers to convert more agricultural land to organic farming, further supporting market growth.

Key Report Takeaways

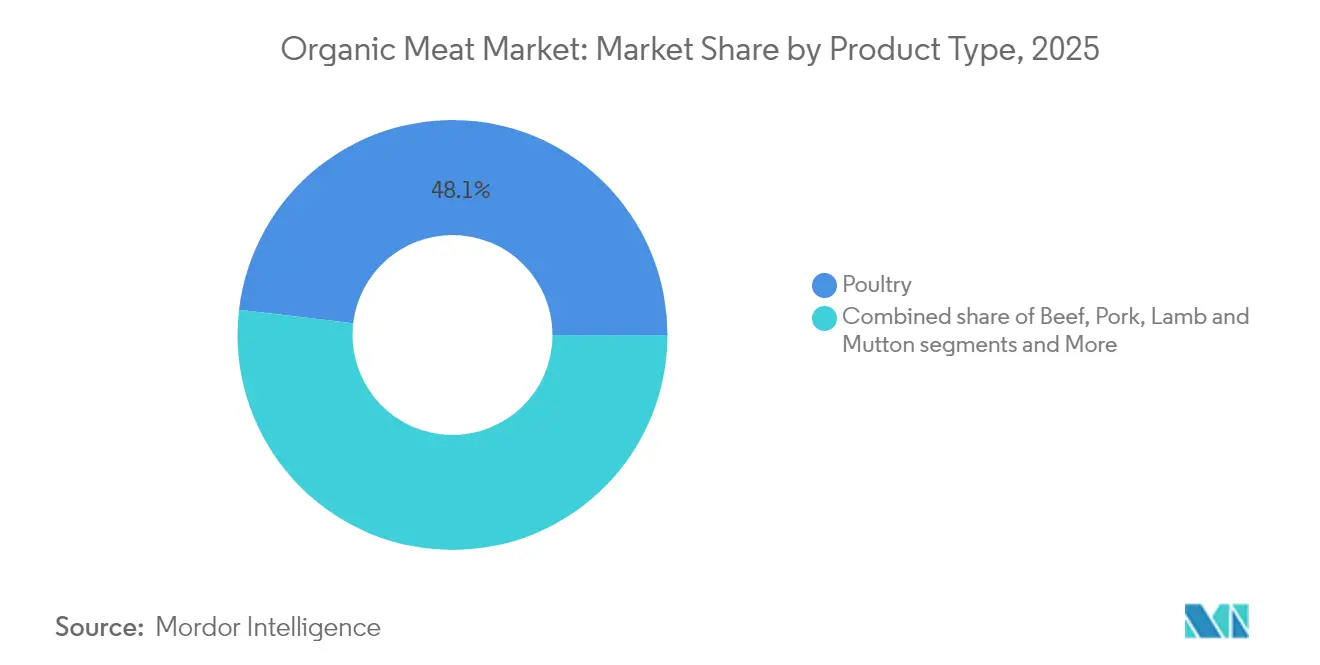

- By product type, poultry led with 48.12% revenue share in 2025; lamb and mutton are forecast to advance at a 11.92% CAGR to 2031.

- By product form, fresh and chilled products captured 61.05% of the organic meat market share in 2025, while frozen products are projected to grow at 10.05% CAGR through 2031.

- By packaging type, tray formats held 42.93% share of the organic meat market size in 2025; pouches are expected to expand at a 10.02% CAGR between 2026-2031.

- By distribution channel, off-trade retained 66.02% share of the organic meat market in 2025, whereas on-trade channels are forecast to post a 10.44% CAGR to 2031.

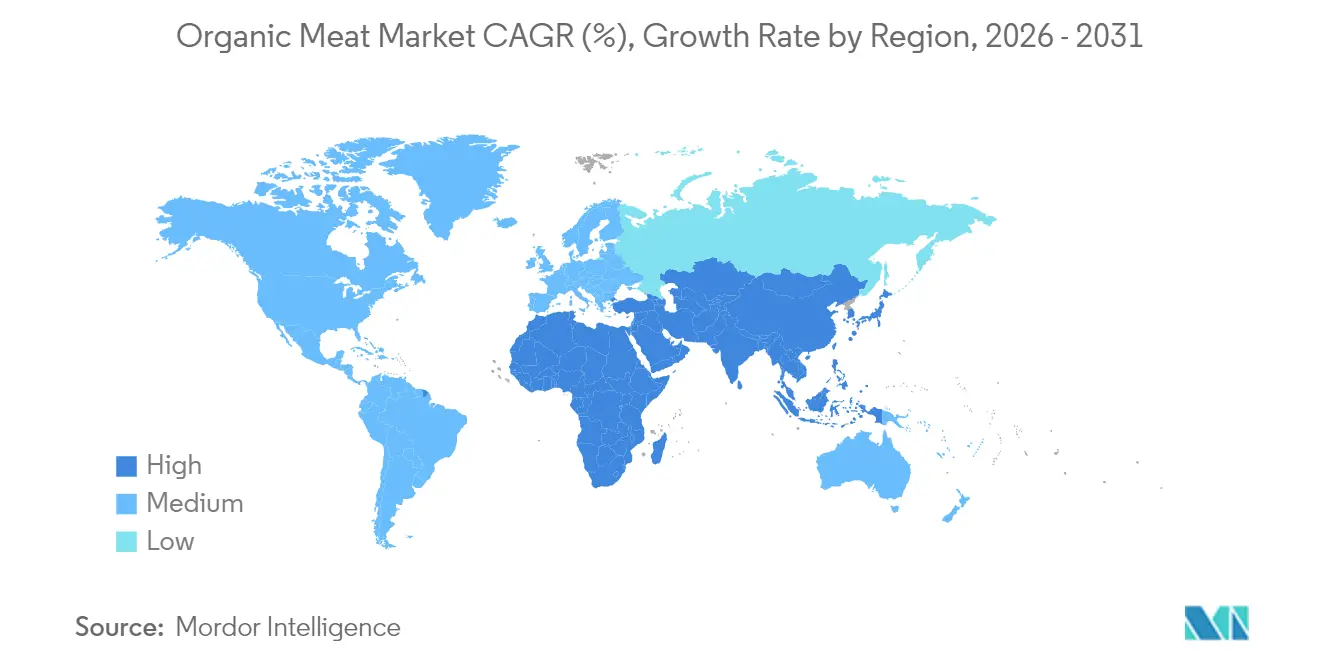

- By geography, North America commanded 38.74% share of the organic meat market in 2025, while Asia-Pacific is predicted to register the fastest growth at 9.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Organic Meat Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health benefits drive consumer preference for organic meat products | +2.1% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Environmental sustainability increases demand for organic livestock production | +1.8% | Global, particularly strong in European Union and Asia-Pacific | Long term (≥ 4 years) |

| Animal welfare awareness accelerates organic meat market growth | +1.3% | North America and European Union core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Premium positioning of organic meat products attracts quality-focused consumers | +1.7% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Regulatory framework and government support boost organic meat production | +1.4% | European Union and North America primarily, expanding globally | Long term (≥ 4 years) |

| Changing lifestyles and urbanization boost demand for premium organic products | +1.2% | Asia-Pacific core, spill-over to urban centers globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health benefits drive consumer preference for organic meat products

As consumer health consciousness continues to rise, organic meat has solidified its position as a preferred protein source, recognized for being free from synthetic hormones, antibiotics, and chemical residues. The Organic Trade Association underscores that US organic farmers adhere to rigorous standards, including raising livestock without antibiotics or synthetic growth hormones, providing 100% organic feed, and ensuring clean, cage-free living environments. These practices not only emphasize animal welfare but also align with the growing demand for transparency and sustainability in food production. Millennials and Gen Z consumers, in particular, are driving this demand, demonstrating a willingness to pay premium prices for products they perceive as healthier and ethically sourced. The appeal of organic meat is further reinforced by scientific studies linking its consumption to a reduced risk of chronic diseases, such as cardiovascular conditions and certain cancers. This evidence strengthens consumer trust and creates a self-reinforcing cycle where health-conscious buyers propel market growth while validating premium pricing strategies.

Environmental sustainability increases demand for organic livestock production

Environmental considerations have transitioned from being niche concerns to becoming significant drivers of purchasing decisions. Organic meat production offers distinct sustainability advantages over conventional methods. According to The Organic Center, organic meat practices actively support biodiversity by eliminating the use of harmful synthetic pesticides and fostering diversified habitats. Managed grazing, a key component of organic farming, enhances soil quality and reduces dependency on synthetic fertilizers, contributing to long-term agricultural sustainability. The EU's Organic Action Plan, which aims to convert 25% of agricultural land to organic farming by 2030, reflects a strong policy-level endorsement of organic farming's environmental benefits[1]European Commission, "Organic Action Plan", www.agriculture.ec.europa.eu. This regulatory push is expected to create favorable conditions for market expansion. Furthermore, corporate sustainability commitments are driving demand, as foodservice operators and retailers increasingly prioritize organic meat to meet environmental, social, and governance (ESG) targets while aligning with evolving consumer expectations. For climate-conscious consumers, purchasing organic meat is more than a dietary choice—it is viewed as a form of environmental activism.

Animal welfare awareness accelerates organic meat market growth

Animal welfare concerns have evolved from niche activist discussions to significantly influence mainstream consumer behavior. Organic certification now plays a pivotal role as a third-party assurance of humane treatment standards, addressing growing consumer demand for ethical practices. The USDA's finalized Organic Livestock and Poultry Standards provide clear guidelines, including specific indoor and outdoor space requirements, mandatory year-round outdoor access, and the prohibition of low-welfare practices such as caging breeding pigs. These regulatory updates aim to eliminate consumer confusion about organic standards while aligning with their expectations. Surveys consistently highlight animal welfare as one of the primary purchase drivers for organic meat consumers, underscoring its importance in decision-making. Retailers are responding to this shift, with Whole Foods Market leading the way by expanding its industry-leading animal welfare standards and incorporating third-party certifications to differentiate its organic offerings. This focus on welfare creates a strong emotional connection between consumers and products, enabling brands to command premium pricing while fostering long-term loyalty.

Premium positioning of organic meat products attracts quality-focused consumers

The premiumization trend in protein markets is driving substantial growth opportunities for organic meat brands, enabling them to command higher price premiums while sustaining strong consumer demand. Research consistently shows that attributes such as freshness, taste, safety, and tenderness are pivotal in shaping consumer preferences. Organic certification has become a critical quality marker, enhancing consumer trust and validating premium pricing strategies. Retail partnerships further illustrate this approach, with Verde Farms expanding its organic grass-fed beef offerings across major retailers like Target, Publix, and others. These products are strategically positioned at price points significantly higher than conventional alternatives, underscoring their premium value proposition. The emphasis on quality extends beyond basic food safety to include superior taste profiles, enhanced nutritional density, and greater culinary versatility, appealing to both food enthusiasts and health-conscious consumers. This premium positioning not only differentiates organic brands but also creates significant barriers to entry for conventional producers, fostering a sustainable competitive advantage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of organic meat limiting accessibility across income levels | -1.9% | Global, most pronounced in emerging markets | Short term (≤ 2 years) |

| Short shelf life due to absence of preservatives hinders growth | -1.1% | Global, particularly affecting distribution efficiency | Medium term (2-4 years) |

| Lack of standardized labeling confuses consumers and hampers trust | -0.8% | Global, with varying regional regulatory frameworks | Medium term (2-4 years) |

| Underdeveloped supply chain causing delays | -0.7% | Emerging markets and rural areas globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost of organic meat limiting its accessibility to consumers across different income levels

Price sensitivity remains the most significant barrier to the adoption of organic meat, as retail prices for organic options are considerably higher than conventional alternatives. This pricing disparity limits market penetration across various income groups. Economic pressures, particularly during inflationary periods, further exacerbate this issue. Consumers often prioritize essential spending, leading many to opt for cheaper protein sources despite a preference for organic products. The USDA's Organic Situation Report 2025 highlights a decline in price premiums for organic products, driven by increasing competition and the rise of alternative labels such as regenerative agriculture[2].U.S. Department of Agriculture, "Organic Situation Report, 2025 Edition", www.usda.gov This trend suggests that producers may need to compress margins to make organic meat more accessible to a broader audience. On the production side, high cost structures present additional challenges. Expenses related to organic feed premiums and certification processes limit producers' ability to lower prices without compromising profitability. These structural cost constraints create a significant impediment to achieving mass-market adoption of organic meat, underscoring the need for strategic interventions to balance affordability and profitability in the organic meat market.

Short shelf life of organic meat product due to the absence of preservatives hinders growth

Organic meat producers face significant logistical challenges due to the prohibition of synthetic preservatives, which increases costs and hampers distribution efficiency. These issues are particularly pronounced for smaller producers who lack access to advanced cold chain infrastructure. However, technological advancements are offering promising solutions to these constraints. Researchers at the University of Maryland have developed "flash heating" technology, which allows meat to be preserved at room temperature for up to 5 days without any loss of nutritional value. Similarly, IXON Food Technology has introduced a groundbreaking innovation with its patent-pending sous-vide aseptic packaging technology, enabling meat to be stored at room temperature for up to 2 years without refrigeration or preservatives. These preservation challenges disproportionately impact smaller organic producers, as they often lack the resources to invest in advanced packaging and distribution systems. This disparity creates a competitive edge for larger players with sophisticated supply chain capabilities. Retail partnerships further amplify this issue, as they demand reliable supply chains and consistent product availability. Consequently, the limited shelf life of organic meat becomes a significant barrier for smaller producers in securing premium retail placements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Poultry Leadership Drives Market Expansion

Poultry takes the lead with a commanding 48.12% market share in 2025, underscoring a consumer shift towards affordable organic proteins. This trend is bolstered by a well-established supply chain ensuring consistent retail availability. Technological strides and regulatory updates have propelled organic poultry production. Notably, the USDA's revamped Organic Livestock and Poultry Standards now emphasize space and environmental enrichment, echoing consumer demands for heightened animal welfare. While beef carves out a notable market presence with premium strategies, pork grapples with cultural dietary hurdles in burgeoning markets. Yet, pork's edge lies in processing innovations that set it apart.

Segments like lamb and mutton are on an upward trajectory, boasting a forecasted 11.92% CAGR through 2031. This surge is largely attributed to cultural preferences in the burgeoning Middle Eastern and South Asian markets, where organic certification fetches a premium. As urbanization and disposable incomes rise, so does the appetite for premium proteins, especially in regions where lamb is culturally revered. The segment enjoys a competitive edge due to limited supply challenges and robust export networks linking organic producers to lucrative global markets. Meanwhile, other organic meats, such as game and specialty proteins, carve out their niche. They leverage artisanal branding and direct-to-consumer sales, sidestepping traditional retail hurdles. Across the board, advancements in organic feed production and pasture management are slashing production costs, bolstering margins, all while upholding organic integrity standards.

By Product Form: Fresh Dominance Meets Frozen Innovation

Fresh and chilled organic meat products dominate the market with a 61.05% market share in 2025, driven by consumer preferences for superior quality and culinary flexibility, which justify premium pricing strategies. This dominance aligns with evolving retail trends, where experiential shopping and home meal preparation have gained traction, particularly following pandemic-induced lifestyle shifts. Consumers increasingly seek high-quality ingredients for home cooking, reinforcing the demand for fresh products. Retail partnerships further highlight this trend, with Verde Farms significantly expanding its fresh organic beef offerings across major supermarket chains such as Target, Publix, and Albertsons, achieving notable distribution growth through a premium fresh positioning strategy. Fresh products benefit from shorter supply chains, which help reduce transportation costs and maintain product integrity, enabling competitive pricing compared to frozen alternatives.

Frozen organic meat products are witnessing robust growth, with a projected CAGR of 10.05% through 2031. This growth is fueled by rising demand for convenience and advancements in technology that preserve nutritional value while extending shelf life. Frozen products also facilitate geographic market expansion, overcoming the distribution limitations faced by fresh products. This is particularly advantageous for smaller organic producers aiming to access national markets. Additionally, frozen organic meats appeal to cost-conscious consumers by offering organic benefits at more affordable price points, as they typically carry lower premiums than fresh alternatives. Advanced packaging technologies, such as vacuum sealing and modified atmosphere packaging, are enhancing the quality of frozen products, minimizing freezer burn, and preserving organic integrity over extended storage periods, thereby strengthening consumer trust and driving market adoption.

By Packaging Type: Tray Convenience Versus Pouches Innovation

In 2025, tray packaging, accounting for 42.93% of the market share, is favored for its alignment with retail display needs and the rising consumer demand for ready-to-cook, portion-controlled products. Supermarkets are drawn to trays not only for their visual appeal and stackability but also for the convenience they offer, especially with fresh organic meat products. Trays resonate with contemporary trends in meal planning and family dining, a sentiment echoed by health-conscious consumers. Yet, as the spotlight on environmental sustainability intensifies, traditional tray formats face scrutiny. This has spurred innovations towards recyclable and biodegradable materials, aiming to balance retail efficiency with a reduced environmental footprint.

Pouches are rapidly gaining momentum, emerging as the fastest-growing packaging format, boasting a projected CAGR of 10.02% through 2031. Their lightweight and flexible design translates to significant cost and space savings in production, storage, and distribution. Urban consumers, particularly those with eco-conscious mindsets, are drawn to pouches for their convenience, freshness, and portability. This is especially true for single-serve or on-the-go organic meat products. As organic meat producers increasingly pivot towards digital and direct-to-consumer sales, pouches are becoming the packaging of choice, adept at preserving product quality while aligning with sustainability objectives.

By Distribution Channel: Off-Trade Stability Meets On-Trade Acceleration

In 2025, off-trade channels command a 66.02% market share, underscoring the strength of established retail infrastructures and consumer habits that lean towards traditional grocery and specialty stores for organic meat purchases. Supermarkets and hypermarkets, with their dedicated organic sections and premium positioning, not only justify higher margins but also cultivate consumer trust through brand recognition. Whole Foods Market exemplifies this strategy, showcasing a range of organic meats, from Force of Nature Meats to various grass-fed options, blending product quality with retail acumen. Specialty stores, on the other hand, tap into niche markets, offering curated selections and expert advice to discerning consumers in search of specific organic meat varieties. Meanwhile, online retail channels are swiftly gaining traction, harnessing direct-to-consumer models and subscription services that emphasize convenience and foster strong customer relationships for repeat business.

On-trade channels are poised for significant growth, projected at a 10.44% CAGR through 2031. This surge is largely attributed to the foodservice sector's embrace of organic proteins, aligning with consumers' rising demand for sustainable dining. Restaurants and foodservice entities are increasingly featuring organic meats, not just to enhance their menus but to attract eco-conscious diners who are willing to pay a premium for ethical dining. This momentum in the on-trade sector mirrors a broader industry shift towards transparency and sustainability, especially resonating with younger diners who prioritize corporate responsibility. With chefs advocating for organic meats and highlighting their superior taste and cooking qualities, there's a growing demand that supports premium pricing.

Geography Analysis

In 2025, North America holds a leading 38.74% market share, driven by its well-established organic infrastructure and evolving regulatory frameworks, which have been strengthened since the inception of the USDA's National Organic Program. The region's competitive advantage is rooted in its comprehensive certification systems and recent regulatory advancements. The USDA has significantly increased funding for the National Organic Program and introduced new Organic Livestock and Poultry Standards, effective January 2024, as highlighted by the National Organic Coalition. Canada plays a pivotal role in this growth, with expanding livestock operations and leveraging NAFTA provisions to enhance cross-border organic meat distribution. The region's direct-to-consumer channels have matured beyond the pandemic-induced surge, with e-commerce platforms enabling rural producers to access urban premium markets while maintaining organic integrity throughout the supply chain.

Asia-Pacific is positioned as the fastest-growing region, with a projected 9.87% CAGR through 2031. This growth is fueled by rapid economic development and a cultural shift toward premium protein consumption in urban areas. India's organic food sector showcases immense potential, with metropolitan cities such as Mumbai, Pune, and Delhi leading in organic food searches, while non-metropolitan areas are also witnessing accelerated adoption. Investments in poultry infrastructure across the region are facilitating the integration of organic meat within South Asia and Southeast Asia. This growth is underpinned by a focus on local production to enhance food security. Additionally, cultural dietary preferences and traditional medicinal beliefs that emphasize food as medicine align naturally with the positioning of organic meat, enabling acceptance of premium pricing across diverse income segments.

Europe maintains a strong market presence, supported by the EU's ambitious Organic Action Plan, which aims to increase organic farming to 25% of agricultural land by 2030, up from the current 8.5%. The introduction of new EU organic regulations in January 2025 will impose stricter compliance requirements, presenting challenges for smaller producers but enhancing overall market integrity and consumer confidence. The region benefits from harmonized certification standards across member states, which facilitate cross-border trade and create economies of scale in organic meat production and distribution. Meanwhile, the Middle East and Africa are emerging as growth regions, driven by cultural preferences for lamb and mutton. South America, on the other hand, leverages its established livestock production capabilities and expanding export networks to meet the growing demand for traceable organic protein in developed markets.

Competitive Landscape

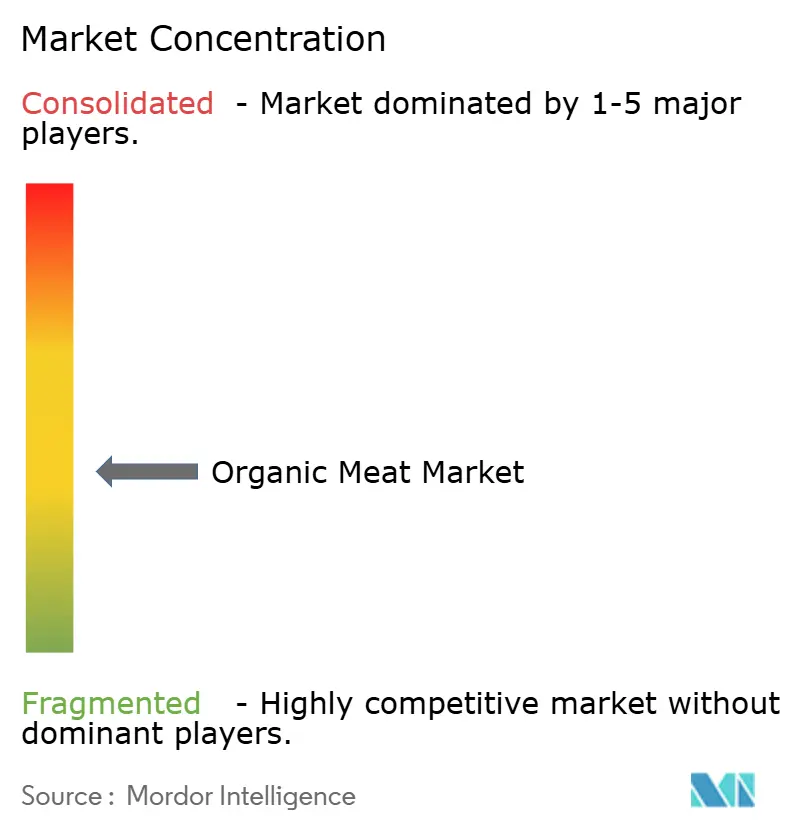

The organic meat market has low fragmentation, with both international players and emerging players striving for higher market shares in the organic meat industry. Some of the major players are Tyson Foods, Inc., JBS S.A., Perdue Farms, Inc., Cargill Incorporated, and Danish Crown A.m.b.a (Danpo), among others. These companies are targeting markets in both the developing and developed countries for business expansion, either by investing in a new production unit or acquiring established companies in the organic meat segment.

To maintain a competitive edge, companies are turning to strategies like acquisitions, product innovation, and market expansion. For instance, Tyson and Perdue are not just launching new products but also adopting advanced production technologies to boost efficiency and cater to evolving consumer preferences. Brands are diversifying their offerings, presenting unique cuts, flavored meats, and value-added products such as marinated or pre-seasoned organic meats. A case in point is Perdue Farms, which has introduced gluten-free, lightly breaded organic chicken nuggets, specifically targeting health-conscious consumers seeking convenience.

Brands are underscoring their commitment to sustainable farming, animal welfare, and sourcing locally. Tyson Foods stands out by spotlighting its initiatives aimed at reducing environmental impact and enhancing animal welfare in its marketing campaigns. By adopting innovative methods and technologies, brands are not only elevating their quality but also championing sustainability. For instance, Tyson Foods is harnessing advanced logistics and cold chain technologies, ensuring product freshness, minimizing waste, and upholding consistent quality.

Organic Meat Industry Leaders

-

Tyson Foods, Inc.

-

Perdue Farms, Inc.

-

JBS S.A.

-

Woolworths Group Limited

-

Hormel Foods Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hewitt Foods USA has launched a new organic meat brand called The Organic Meat Co., featuring USDA-certified organic, grass-fed, and finished beef with no antibiotics, added hormones, or feedlot confinement. The product line includes Organic Ground Beef (85/15), Organic Ground Beef Value Pack, and premium cuts such as Organic Sirloin, Ribeye, Tenderloin, and Strip Steaks.

- May 2025: Lidl has launched its first private-label meat line in the U.S., called Butcher’s Specialty. This new collection features a wide range of products, including USDA Choice beef, organic and grass-fed beef, antibiotic-free chicken, and all-natural pork, lamb, and veal. According to the brand, the line includes popular cuts such as ribeye steak, T-bone steak, beef chuck roast, ground lamb, whole chicken, chicken leg quarters, and seasoned skirt steak.

- May 2025: Perdue Farms has added Panorama Meats, the largest U.S. producer of certified organic beef that's both 100% grass-fed and grass-finished, to its Perdue Premium Meat subsidiary portfolio.

- March 2025: Force of Nature Meats has launched a new line of chicken products sourced exclusively from slow-growth, heritage breeds that are pasture-raised, organic-fed, and live 8–10 weeks—twice as long as industry-standard birds—resulting in stronger bones, healthier muscles, and richer nutrition.

Global Organic Meat Market Report Scope

Organic meat must be derived from livestock that is organically raised on certified organic land and fed organic feed without any antibiotics or added growth hormones. The scope of the report includes a segmentation analysis based on various types of meat, viz., poultry, beef, pork, and other types of meat.

The organic meat market is segmented by type (poultry, beef, pork, and other organic meat), distribution channel (hypermarkets and supermarkets, specialty stores, online retailing, and retail and departmental stores), and geography (North America, Europe, Asia-Pacific, South America, and Africa). The report offers market size and forecasts in terms of value(USD million) for all the above segments.

| Poultry |

| Beef |

| Pork |

| Lamb and Mutton |

| Other Organic Meats |

| Fresh/Chilled |

| Frozen |

| Vaccum-Pack |

| Trays |

| Cartons |

| Others |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| On-Trade |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Poultry | |

| Beef | ||

| Pork | ||

| Lamb and Mutton | ||

| Other Organic Meats | ||

| By Product Form | Fresh/Chilled | |

| Frozen | ||

| By Packaging Type | Vaccum-Pack | |

| Trays | ||

| Cartons | ||

| Others | ||

| By Distribution Channel | Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| On-Trade | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the organic meat market?

The organic meat market size reached USD 21.87 billion in 2025 and is estimated at USD 23.59 billion in 2026 and is projected to hit USD 34.43 billion by 2031 at a 7.86% CAGR.

Which region leads the organic meat market?

North America accounts for the largest regional share at 38.74%, supported by mature certification systems and consumers willing to pay premiums for verified animal-welfare standards.

Which meat type is growing fastest?

Lamb and mutton are forecast to record a 11.92% CAGR through 2031, reflecting rising demand in Middle Eastern and South Asian cities where these proteins hold cultural significance.

Why are frozen organic meats gaining traction?

Frozen formats benefit from improved preservation technologies that lock in nutrients, reduce waste, and widen distribution reach, underpinning a 10.05% forecast CAGR.

Page last updated on: