Deli Meat Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

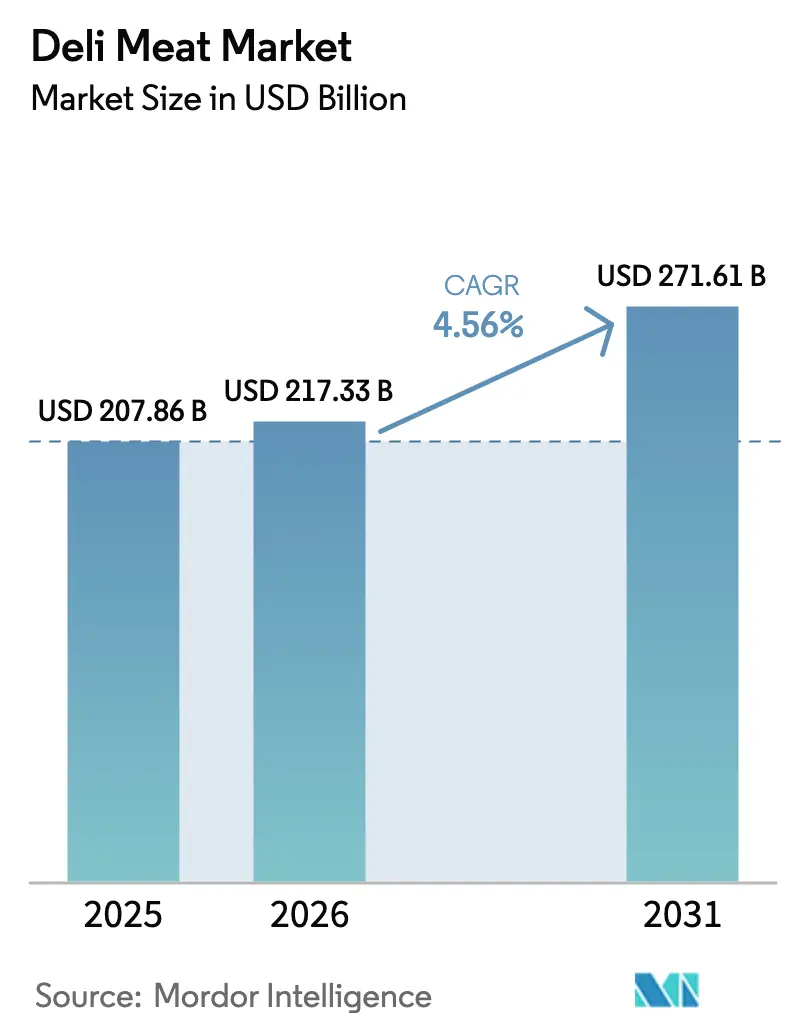

| Market Size (2026) | USD 217.33 Billion |

| Market Size (2031) | USD 271.61 Billion |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Deli Meat Market Analysis by Mordor Intelligence

The deli meat market size was valued at USD 207.86 billion in 2025 and estimated to grow from USD 217.33 billion in 2026 to reach USD 271.61 billion by 2031, at a CAGR of 4.56% during the forecast period (2026-2031). The surge in demand can be attributed to premium snacking trends among younger consumers, a rising inclination towards high-protein diets, and a persistent social media buzz around charcuterie boards. Retailers are reaping the rewards of this 'trading-up' behavior, with customers increasingly gravitating towards artisanal cuts. In response to regulatory guidance, processors are pivoting towards clean-label reformulations, particularly focusing on sodium and nitrosamine content. The market landscape is characterized by fragmented competition and persistent supply-chain challenges. These dynamics not only present acquisition opportunities for multinationals but also carve out niches for innovative players looking to expand their market share.

Key Report Takeaways

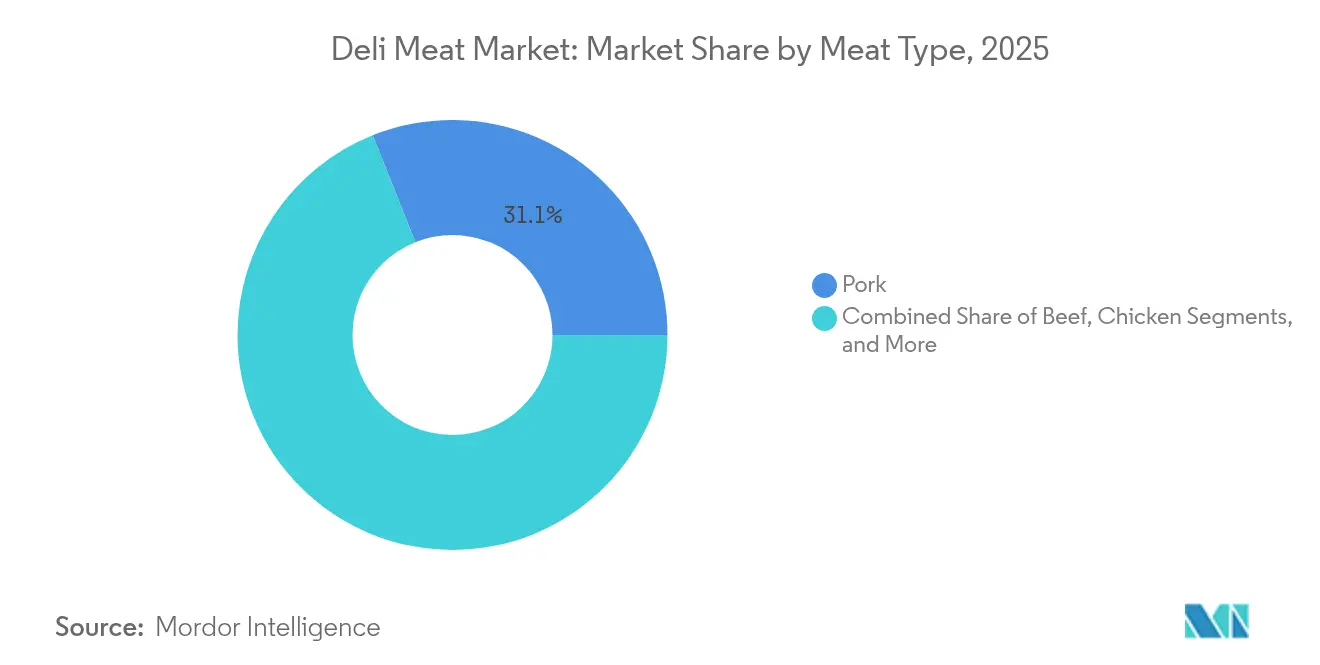

- By meat type, pork led with 31.05% of deli meat market share in 2025; chicken is projected to expand at a 6.75% CAGR to 2031.

- By product type, ham captured 27.55% share of the deli meat market size in 2025; chicken breast is forecast to advance at a 7.22% CAGR through 2031.

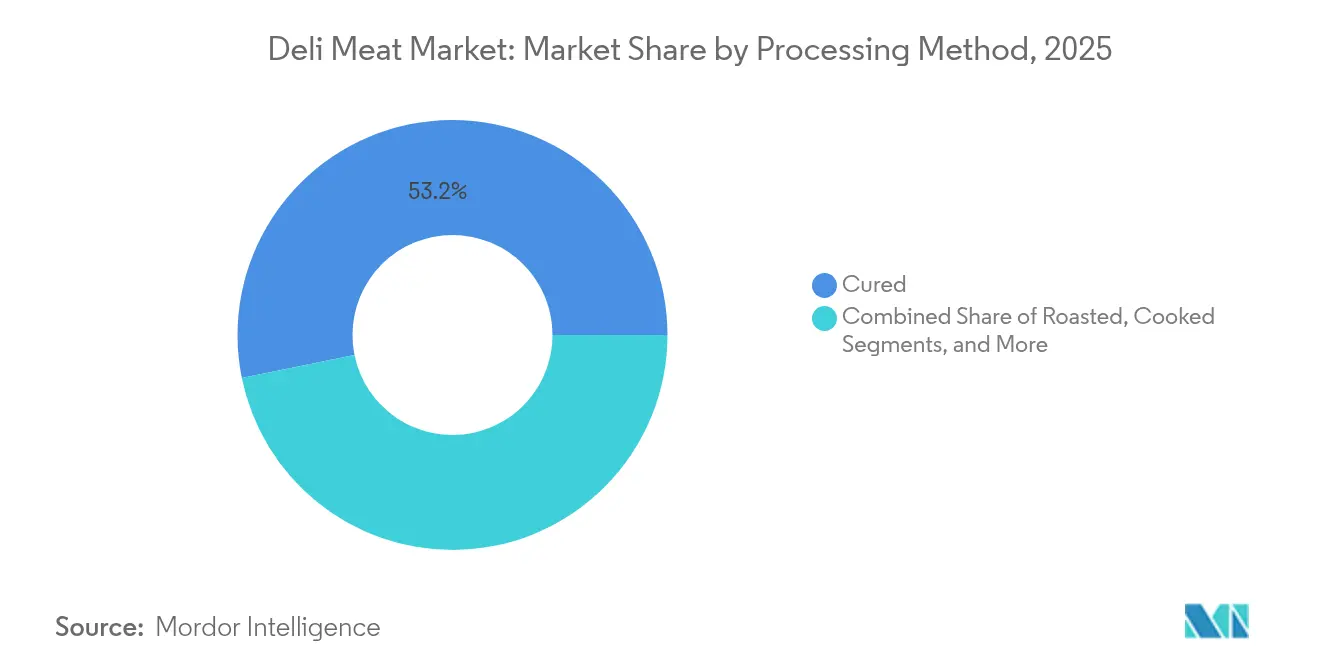

- By processing method, cured products accounted for 53.20% share of the deli meat market size in 2025; uncured products are set to rise at a 8.62% CAGR between 2026 and 2031.

- By end user, retail held 62.10% of the deli meat market share in 2025; the HoReCa channel is expected to grow at a 6.05% CAGR through 2031.

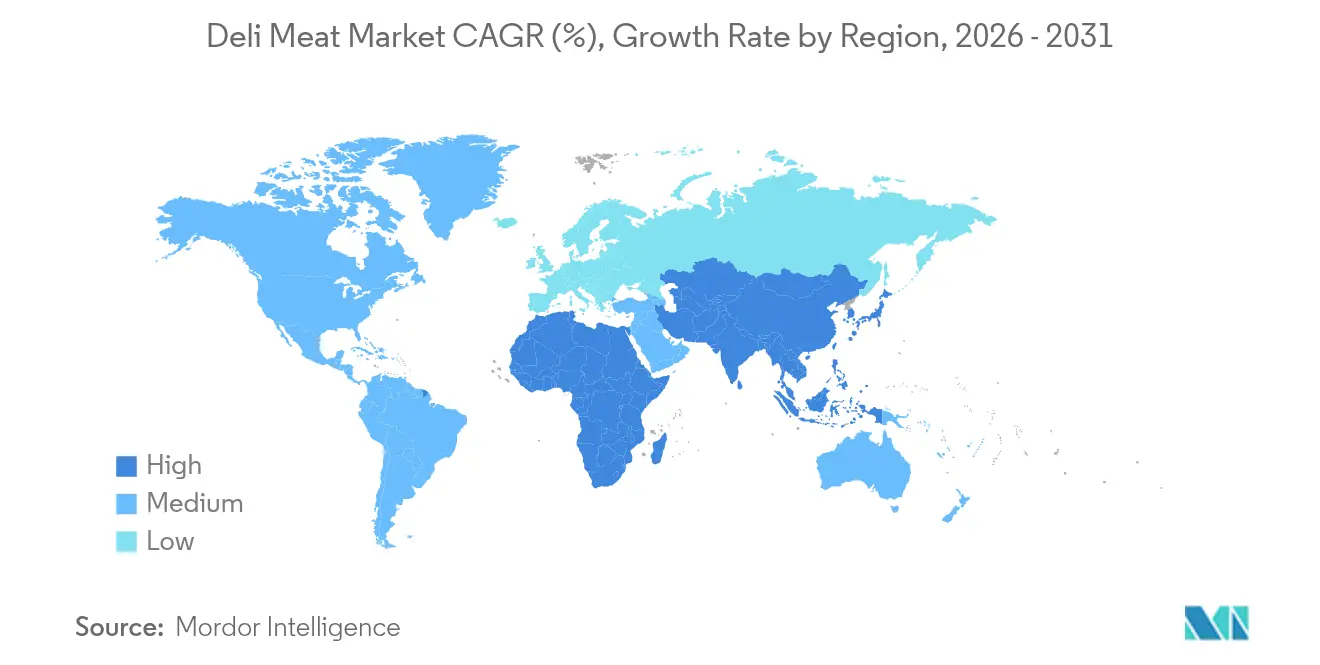

- By geography, Europe dominated with a 32.85% share of the deli meat market in 2025; Asia-Pacific exhibits a 7.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Deli Meat Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium-ization of meat snacking culture among Gen Z and Millennials | +1.2% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Rising demand for clean-label, nitrate-free packaged deli meats | +0.8% | Global, strongest in North America and EU | Long term (≥ 4 years) |

| Growth of "grazing boards" and social-media-driven charcuterie trends | +0.6% | North America and Europe, urban centers | Short term (≤ 2 years) |

| Expansion of high-protein diets (keto, paleo) into mainstream retail | +0.9% | Global, led by North America | Medium term (2-4 years) |

| Product Innovation Shaping Consumer Choices in the Deli Meat | +0.5% | Global | Medium term (2-4 years) |

| Transparency and Ethical Sourcing | +0.4% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium-ization of Meat Snacking Culture Among Gen Z and Millennials

Generation Z consumers are not just dabbling but diving deep into the world of artisanal deli meats, showcasing an unprecedented willingness to pay premium prices. This shift isn't limited to traditional sandwich applications. Kretschmar's "Made for More" campaign, for instance, is pioneering this trend, introducing innovative products like Lemon and Cracked Pepper Turkey Breast and Spiced Pineapple Ham. These aren't just deli meats; they're crafted for creative meal preparations, signaling a broader culinary exploration by the younger generation. The trend of premiumization, closely tied to the influence of social media, sees consumers gravitating towards premium products, often swayed by targeted marketing efforts. This evolving consumer behavior is not just a fleeting trend; it's reshaping the very priorities of product development. Brands, recognizing this shift, are channeling investments into crafting unique flavor profiles and designing Instagram-worthy packaging, all in a bid to carve out a significant share in the lucrative premium segment. As the lines between traditional and innovative culinary applications blur, the market watches closely, anticipating the next wave of artisanal offerings that will capture the Gen Z palate.

Rising Demand for Clean-Label, Nitrate-Free Packaged Deli Meats

Responding to heightened consumer health awareness and regulatory pressures, manufacturers are increasingly favoring clean-label formulations, with uncured products leading the charge at a notable 9.13% CAGR. By 2024, Dietz & Watson had fully transitioned to nitrate-free formulations, eliminating additives from its turkey, chicken breast, ham, and roast beef offerings. This shift was achieved without compromising taste, thanks to the company's cherished family recipes and natural preservation techniques. In 2024, the FDA rolled out voluntary sodium reduction guidelines, specifically targeting commercially processed foods. These guidelines incentivize manufacturers to reformulate their products, all while upholding stringent food safety standards, as noted in the Federal Register[1]Source: FDA, “Voluntary Sodium Reduction Goals,” fda.gov. True Story Foods is riding this wave, broadening its reach to 4,000 stores. Their offerings, including Uncured Wildflower Honey & Maple Ham and Organic Thick Carved Oven Roasted Chicken Breast, cater to a discerning clientele that prioritizes humane practices, as highlighted by Meat + Poultry. The clean-label trend not only offers a competitive edge to its early adopters but is also setting new benchmarks in the industry for transparency and ingredient simplicity.

Growth of "Grazing Boards" & Social-Media-Driven Charcuterie Trends

Social media platforms are reshaping charcuterie consumption, pushing it beyond just traditional meal times. As a result, sales in deli entertaining have surged. This shift is largely driven by consumers' growing appreciation for visually appealing food presentations and communal dining experiences. Columbus Craft Meats champions charcuterie as a refined culinary art, enhancing the overall consumer experience. Retailers, recognizing this trend, are establishing dedicated charcuterie sections, aiming to elevate both sales and average transaction values. Today's charcuterie boards are evolving; consumers are moving past the classic meat-and-cheese duo, opting instead for a variety of accompaniments and seasonal items, leading to more frequent purchases. In response, brands are rolling out pre-made board selections and seasonal products. Notably, Hormel is introducing holiday-themed items, while Volpi Foods is emphasizing convenience. This evolving consumption trend not only yields higher profit margins compared to traditional deli sales but also opens doors for cross-merchandising. Retailers can now pair charcuterie with artisanal cheeses, gourmet crackers, and specialty condiments for a more enticing offering.

Expansion of High-Protein Diets (Keto, Paleo) Into Mainstream Retail

High-protein dietary trends drive deli meat consumption as consumers prioritize protein content for health, muscle development, and weight management applications. Stryve Foods' distribution expansion into major retail chains, including Southeastern Grocers and Albertsons, reflects growing demand for high-protein, low-carb meat snacks suitable for Keto and Paleo diets. Retailers report strong sales growth in protein-enriched products across categories, with deli meats benefiting from consumer perception linking protein consumption to health benefits. The mainstream adoption of specialized diets creates opportunities for product innovation and targeted marketing, with manufacturers developing products specifically formulated for dietary restrictions while maintaining broad appeal. Consumer education about balanced nutrition becomes crucial as retailers market protein content and position deli meats as convenient protein sources for busy lifestyles. This trend supports premium pricing strategies as consumers willingly pay higher prices for products aligned with their dietary goals and health objectives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating adoption of plant-based alternatives | -0.7% | Global, strongest in Europe and North Americ | Medium term (2-4 years) |

| Heightened retailer scrutiny over nitrosamine and sodium content | -0.5% | Global, regulatory focus in EU and North America | Long term (≥ 4 years) |

| Supply Chain Disruptions Significantly Impact the Deli Meat | -0.6% | Global, acute in North America and Asia-Pacific | Short term (≤ 2 years) |

| Regulatory and Compliance Challenges | -0.4% | Global, stringent in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of Plant-Based Alternative

Despite recent sales declines, plant-based meat alternatives are holding their ground in the market. According to Deloitte, 46% of consumers occasionally buy these options, and 51% are willing to pay a premium for better formulations. The plant-based meat substitute market is particularly robust in Europe, where sustainability concerns heavily influence purchasing decisions. Tofurky's unveiling of its Next Generation Plant-Based Deli Slices at the National Restaurant Association Show 2024 underscores the industry's commitment to innovation. Consumer tests reveal a 59-81% preference for these new slices over older versions. Meanwhile, HappyVore's plant-based ham, dubbed "Taste of the Year 2025," boasts 20 grams of protein per 100 grams and produces four times fewer emissions than its traditional counterpart, as highlighted by Trend Hunter. As plant-based products enhance their nutritional profiles and overcome taste challenges, the competitive landscape becomes more intense. To fend off the rising sophistication of plant-based alternatives, traditional deli meat producers must pivot towards sustainability and health-centric innovations.

Heightened Retailer Scrutiny Over Nitrosamine and Sodium Content

In 2024, a listeria outbreak linked to Boar's Head led to the recall of over 7 million pounds of products and the indefinite closure of a plant. This incident underscored the significant reputational and financial risks tied to food safety failures, as highlighted by Art of Procurement. The FDA has set voluntary sodium reduction targets, aiming for an average intake of 2,750 mg/day in its Phase II goals. This move places compliance pressures on manufacturers, who must balance these guidelines with stringent food safety standards. In response to the outbreak, the USDA's Food Safety and Inspection Service revised its sampling procedures and inspection protocols, signaling a heightened regulatory oversight and the potential for increased liability. Additionally, trade restrictions on sodium nitrite imports from China and Germany, where dumping margins could reach as high as 237%, are straining the supply chains of manufacturers reliant on these imported preservatives. Given this regulatory landscape, manufacturers are compelled to boost investments in quality control, enhance traceability systems, and explore alternative preservation methods. While these measures are essential for compliance and safety, they risk squeezing profit margins and raising entry barriers for smaller players in the industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Meat Type: Pork Dominance Challenged by Chicken Innovation

Pork retained a 31.05% slice of the deli meat market in 2025, benefiting from established curing infrastructure. Yet, chicken posted the fastest 6.75% CAGR, propelled by consumer perceptions of leaner protein and Tyson Foods’ USD 100 million plant upgrades to elevate supply reliability. Beef products face headwinds from cattle supply constraints, with USDA forecasting a 4.2% production decline in 2024 and wholesale prices reaching USD 400/cwt for 81CL coarse ground beef, representing a 25% year-over-year increase, according to Provisioner Online.

Turkey products demonstrate resilience through premium positioning, with Jennie-O Turkey investing USD 30 million in 2024 in plant expansion to modernize operations and improve processing efficiencies. Consumer experimentation with specialty meats such as lamb remains niche, though premium price points compensate for limited throughput. JBS deployed USD 200 million in Italian dry-aged lines featuring automated guided vehicles to boost consistency and reduce labour overhead. These technology installs are critical as the deli meat market pursues operational efficiency without sacrificing artisanal appeal.

By Product Type: Ham Leadership Faces Chicken Breast Disruption

In 2025, ham products hold a 27.55% market share, bolstered by established consumption patterns and their adaptability in both retail and foodservice channels. Yet, chicken breast products are outpacing with a robust 7.22% CAGR growth rate projected through 2031, fueled by a surge in health-conscious consumers and a broader shift towards protein-centric diets. In a nod to premium innovation, Kentucky Legend debuted its bourbon barrel-smoked ham and bacon in 2024, harnessing upcycled bourbon barrels for distinct flavor profiles. Notably, 91% of ham consumers express intent to repurchase. Meanwhile, Carnegie Deli, in collaboration with Costco, is rolling out exclusive pastrami and corned beef combo packs, a strategic move to bolster brand visibility and accessibility.

Salami products enjoy consistent performance, riding the wave of artisanal positioning and the burgeoning charcuterie trend. In contrast, roast beef grapples with challenges stemming from cattle supply constraints and price fluctuations. Turkey breast products are on the rise, thanks to a health-centric image and innovative processing. Manufacturers are increasingly leaning towards clean-label formulations and eco-friendly packaging. The competitive arena heats up as brands roll out flavor innovations, with Land O'Frost leading the charge as the first national brand to infuse hot honey into packaged deli meats, as reported by Meat + Poultry. Product development now prioritizes distinctive flavor profiles, user-friendly packaging, and nutritional boosts, aiming to attract premium segments and stand out from commodity products. This segment's evolution underscores a growing consumer appetite for variety, convenience, and food experiences that elevate meal times and foster social sharing.

By Processing Method: Uncured Revolution Transforms Traditional Curing

Cured products maintain 53.20% market dominance in 2025, leveraging traditional preservation methods and established flavor profiles that resonate with consumer preferences. The uncured segment emerges as the fastest-growing category at 8.62% CAGR through 2031, reflecting consumer health consciousness and regulatory pressure to reduce nitrate and nitrite usage. Dietz & Watson's complete transition to uncured formulations across its product line demonstrates industry commitment to clean-label positioning while maintaining taste and safety standards. Smoked products benefit from artisanal positioning and flavor differentiation, with manufacturers investing in natural smoking processes and premium wood selections to enhance product appeal.

Roasted and cooked products serve convenience-focused consumers seeking ready-to-eat solutions, with processing innovations enabling extended shelf life and improved texture. The FDA's nitrosamine impurity guidance creates compliance requirements that favor manufacturers with advanced quality control systems and alternative preservation technologies. Scientific research reveals geographic variations in nitrite and nitrate levels, with average nitrite content at 13.7 ppm in processed meats compared to 1.7 ppm in meat analogues, highlighting regulatory compliance challenges as per Scientific Reports. Processing method selection increasingly influences brand positioning, with uncured products commanding premium prices while traditional cured products maintain volume leadership. The segment's transformation reflects broader industry trends toward transparency, health consciousness, and regulatory compliance as manufacturers balance consumer preferences with operational requirements and safety standards.

By Distribution Channel: Online Retail Accelerates Digital Transformation

In 2025, the retail channel captures a dominant 62.10% market share, riding the wave of consumer trends favoring home meal preparation and convenient shopping. Supermarkets and hypermarkets lead the retail space, boasting vast product ranges and competitive prices. Meanwhile, specialty stores carve out a niche, appealing to premium customers with curated selections and expert services. Yet, the HoReCa segment stands out, projected to grow at a robust 6.05% CAGR through 2031. This growth is fueled by foodservice operators on the hunt for convenient, high-quality ingredients to elevate their menus. Online retail is witnessing a surge, with consumers turning to e-commerce not just for specialty products but also for subscription services, ensuring a steady supply of premium deli meats.

Convenience and grocery stores capitalize on their grab-and-go appeal, enticing impulse purchases. As the foodservice sector rebounds, HoReCa operators are increasingly prioritizing convenience and quality, aiming to deliver restaurant-quality meals. Tofurky's launch of Next Generation Plant-Based Deli Slices is a strategic move, directly targeting foodservice operators and underscoring the industry's acknowledgment of specific channel needs and growth prospects. Distribution strategies are evolving, with a pronounced shift towards omnichannel approaches. These strategies seamlessly blend retail and foodservice capabilities, all while catering to distinct customer needs and operational demands. This evolution in channels mirrors shifts in consumer behavior, rapid tech adoption, and industry consolidation, as manufacturers fine-tune their distribution networks for enhanced efficiency and broader market reach.

Geography Analysis

In 2025, Europe commands a dominant 32.85% market share, capitalizing on its rich charcuterie traditions, robust regulatory frameworks, and discerning consumers who champion premium product innovation. The region's artisanal branding and products with protected designations fetch higher prices, and a unified regulatory approach boosts cross-border commerce and market penetration. Meanwhile, the Asia-Pacific region is on a rapid ascent, projected to grow at a 7.44% CAGR until 2031, fueled by increasing disposable incomes, urban migration, and a shift towards Western dietary habits.

A testament to this trend, JBS has poured USD 100 million into meat processing facilities in Vietnam, strategically positioning them to cater to Southeast Asian demands, all while sourcing raw materials from Brazil, as highlighted by JBS Foods. North America is witnessing steady growth, driven by innovative product development and streamlined distribution channels. Manufacturers are ramping up investments in automation and expanding capacities to cater to domestic needs. Yet, the region grapples with challenges like cattle supply shortages and regulatory scrutiny. Despite these hurdles, robust consumer spending and a trend towards premiumization bolster market growth. Highlighting the region's resilience, McKinsey's research reveals a notable 8.6% surge in European grocery sales in 2023, even amidst economic headwinds. Notably, private label products have captured a significant 38% market share, underscoring consumers' quest for value without compromising on quality. South America, along with the Middle East and Africa, presents burgeoning opportunities, buoyed by a rising middle class and heightened protein demand. However, challenges like infrastructural bottlenecks and intricate regulations temper their immediate growth prospects. The global economic landscape, intertwined with trade dynamics and cultural nuances, shapes product innovation and market entry strategies for global players.

Competitive Landscape

In 2024, the deli meat market was found to be fragmented, with the presence of many small and medium-scale players operating in the market. Tyson Foods, in Q2 2025, reported a 27% surge in adjusted operating income, crediting this leap to diversification efforts and a strategic USD 100 million upgrade at its chicken plant. This upgrade is poised to yield an impressive USD 200 million in annual logistics savings by 2030, as reported on tysonfoods.com. JBS, on the other hand, is making waves with a hefty investment in automation, channeling USD 200 million into its Italian dry-cured operations. This move not only aims to shrink per-unit labor costs but also to bolster product consistency, as highlighted by meatpoultry.com.

Hormel is capitalizing on seasonal innovations, rolling out limited-edition charcuterie kits to elevate its higher-margin SKUs. In a bid to capture the millennial demographic, Land O’Frost debuted the category’s inaugural hot-honey deli meats in April 2025, a move reported by meatpoultry.com. Meanwhile, disruptors like True Story Foods are shaking up the scene with direct-to-consumer models, boasting a presence in 4,000 U.S. stores by emphasizing humane sourcing and organic claims.

As firms chase 3-4% yield gains and aim to mitigate recall risks, technologies like digital twins, predictive maintenance, and collaborative robots are becoming staples on processing lines. The competitive landscape is increasingly defined by those who can swiftly convert technological advancements and transparency into tangible brand equity. As the deli meat market evolves, the interplay of innovation, investment, and strategic positioning becomes evident. With established players diversifying and automating, and newcomers carving niches, the market's future promises both challenges and opportunities. The emphasis on technology and transparency suggests a trend where brand equity will be as much about what’s in the product as how it’s produced.

Deli Meat Industry Leaders

Tyson Foods Inc.

Hormel Foods Corp.

JBS S.A.

WH Group Limited

The Kraft Heinz Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: JBS USA announced a USD 135 million investment in a new sausage production facility in Perry, Iowa, expected to process 500,000 sows annually, strengthening the company's pork processing capabilities and rural community presence

- April 2025: Land O'Frost introduced Hot Honey Chicken Breast and Hot Honey Ham, becoming the first national lunch meat brand to offer hot honey in packaged deli meats, targeting consumer demand for flavor variety and premium positioning.

- March 2025: JBS signed a memorandum of understanding with the Vietnamese government to invest USD 100 million in two meat processing plants, expanding Southeast Asian market presence and enhancing food security through Brazilian raw material imports

- March 2025: Carnegie Deli launched an exclusive Pastrami and Corned Beef Combo Pack at over 350 Costco locations nationwide, priced at USD 17.99 for 1.5-pound packages, expanding brand accessibility and retail presence

Global Deli Meat Market Report Scope

| Pork |

| Beef |

| Chicken |

| Others |

| Ham |

| Salami |

| Corn Beef |

| Roast Beef |

| Chicken Breast |

| Turkey Brest |

| Others |

| Cured |

| Uncured |

| Smoked |

| Roasted |

| Cooked |

| HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Specialty Stores | |

| Online Retail | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Indonesia | |

| Japan | |

| Australia | |

| Thailand | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Meat Type | Pork | |

| Beef | ||

| Chicken | ||

| Others | ||

| By Product Type | Ham | |

| Salami | ||

| Corn Beef | ||

| Roast Beef | ||

| Chicken Breast | ||

| Turkey Brest | ||

| Others | ||

| By Processing Method | Cured | |

| Uncured | ||

| Smoked | ||

| Roasted | ||

| Cooked | ||

| By End User | HoReCa | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Specialty Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Indonesia | ||

| Japan | ||

| Australia | ||

| Thailand | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the deli meat market?

The deli meat market generated USD 217.33 billion in 2026 and is projected to reach USD 271.61 billion by 2031 at a 4.56% CAGR.

Which region holds the largest deli meat market share?

Europe led with 32.85% share in 2025 owing to long-standing charcuterie traditions and premium PDO products.

Which segment is growing fastest within the deli meat market?

Uncured products are expanding at a 8.62% CAGR through 2031 as consumers shift toward clean-label, nitrate-free options.

Which distribution channel is gaining momentum?

HoReCa is projected to grow at 6.05% CAGR as restaurants and caterers seek premium, labor-saving protein solutions.

Page last updated on: