Pork Meat Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 416.12 Billion |

| Market Size (2031) | USD 466.13 Billion |

| Growth Rate (2026 - 2031) | 2.30% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pork Meat Market Analysis by Mordor Intelligence

The global pork meat market size was valued at USD 406.76 billion in 2025 and estimated to grow from USD 416.12 billion in 2026 to reach USD 466.13 billion by 2031, at a CAGR of 2.30% during the forecast period (2026-2031). Driven by its rich nutritional profile, particularly its high protein content and essential vitamins, pork has become the preferred choice for fitness enthusiasts and athletes focused on muscle development. The rising trend of dining out and increased on-the-go food consumption has further boosted demand in restaurants, food service establishments, and franchise outlets. Additionally, a surge in tourism across Europe, Asia-Pacific, and North America has positively influenced market growth. Fresh and chilled pork products lead the market, while frozen variants show strong growth potential. Although conventional pork dominates, organic offerings are steadily gaining traction. While off-trade channels are the primary revenue contributors, on-trade sales are set to expand rapidly. Among pork cuts, ham reigns as the most consumed, with ribs carving out a niche growth area. Asia Pacific stands as the dominant market, but South America is poised for the fastest growth rate. Yet, the market faces challenges from the rising popularity of plant-based alternatives and religious dietary restrictions in various regions. Despite these hurdles, the pork meat market is projected to sustain its growth, bolstered by pork's established role in global protein consumption and ongoing product innovations.

Key Report Takeaways

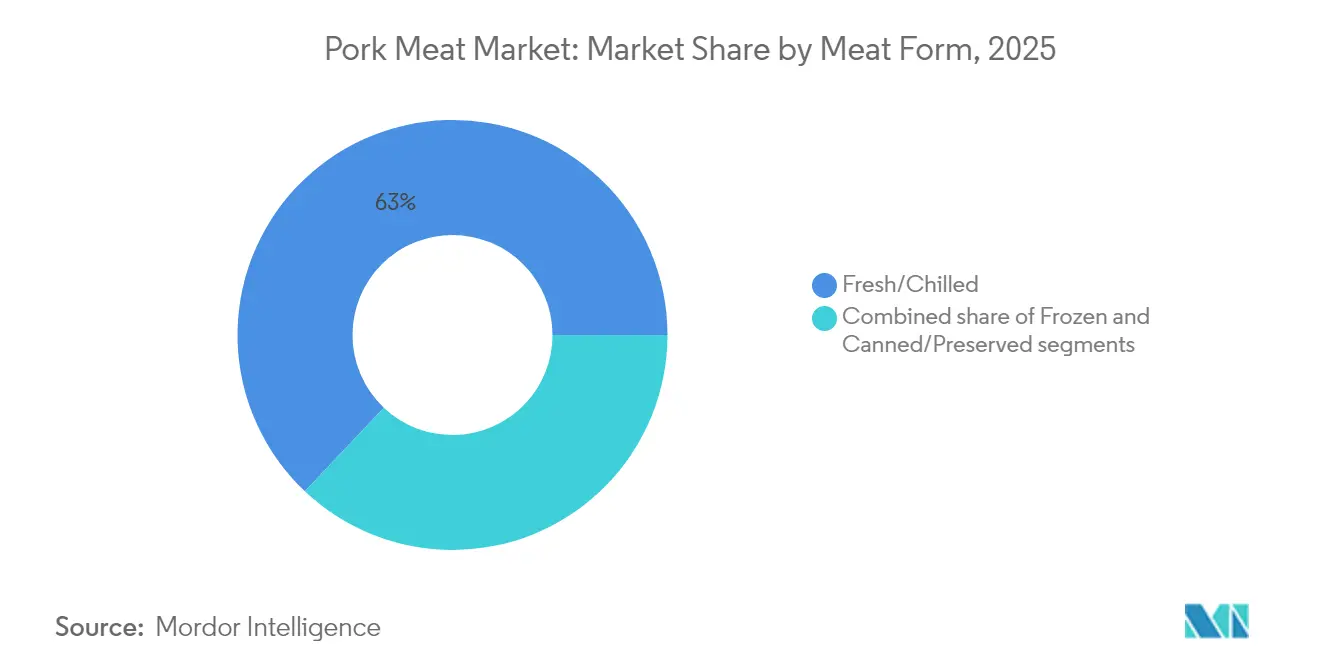

- By meat form, fresh/chilled products held 62.95% of the pork meat market share in 2025; frozen pork is forecast to expand at a 6.55% CAGR to 2031.

- By nature, the conventional segment accounted for 80.62% of the pork meat market size in 2025, whereas organic pork is projected to post a 7.09% CAGR through 2031.

- By distribution channel, off-trade sales commanded 73.55% revenue in 2025, while on-trade outlets are expected to grow at a 12.10% CAGR during 2026-2031.

- By cut type, ham dominated with 39.62% share of the pork meat market size in 2025; ribs are on track for a 4.34% CAGR over the same period.

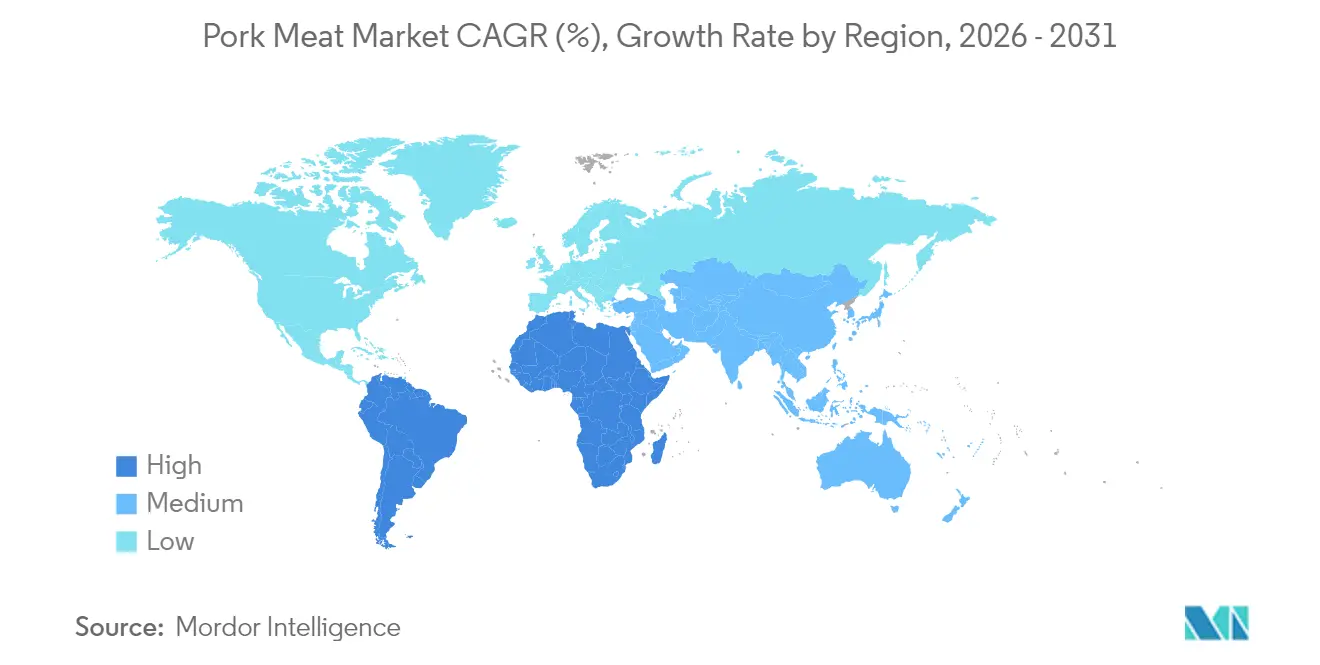

- By geography, Asia-Pacific generated 57.54% of global revenue in 2025, and South America is projected to be the fastest-growing region at a 15.05% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Pork Meat Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for protein-rich diets drives market growth | +0.8% | Global, especially developing markets | Medium term (2-4 years) |

| Expansion of cold chain infrastructure facilitates wider distribution and freshness | +0.6% | Asia-Pacific, Latin America, Middle East and Africa | Long term (≥ 4 years) |

| Growth in the foodservice and hospitality industry (on-trade) supports market demand | +0.4% | North America, Europe, Urban Asia | Short term (≤ 2 years) |

| Increasing demand for processed and convenient pork products boosts sales | +0.5% | Global, particularly developed markets | Medium term (2-4 years) |

| Advances in livestock farming and breeding techniques enhance production efficiency | +0.3% | Technology-adopting regions | Long term (≥ 4 years) |

| Increasing adoption of western dietary habits in developing countries contributes to higher pork consumption | +0.4% | Developing Asia, Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Preference for Protein-rich Diets Drives Market Growth

The increasing consumer awareness about protein-rich diets is driving the growth of the global pork meat market. Pork meat, being rich in high-quality protein, B-complex vitamins, and essential minerals such as zinc and iron, aligns with the growing consumer focus on nutritional value. Health-conscious consumers actively seek high-protein food options, recognizing proteins' role in muscle development, weight management, and overall health. The rising fitness culture and adoption of dietary patterns like keto and paleo diets have further increased the demand for protein-rich meat products. The availability of portion-controlled frozen pork products helps consumers manage their protein consumption while offering longer shelf life compared to fresh alternatives. According to the Food and Agriculture Organization (FAO), the global undernourishment rate was 9.1% in 2023, indicating the potential for pork meat to serve as an affordable protein source to improve dietary nutrition[1]Source: Food and Agriculture Organization, “The State of Food Security and Nutrition in the World 2024,” fao.org. These factors collectively contribute to the sustained demand for pork meat products in the global market.

Expansion of Cold Chain Infrastructure Facilitates Wider Distribution and Freshness

The expansion of cold chain infrastructure is significantly driving the global pork meat market by enabling efficient transportation and storage of pork products across longer distances while maintaining product quality. Modern cold chain facilities incorporate technologies like IoT sensors and automated temperature monitoring systems to ensure consistent temperature control during storage and transportation. According to the UN Environment Programme, developing countries experience approximately 40% of food loss during production to retail due to incomplete cold chains, highlighting the importance of robust cold chain networks [2]Source: United Nations Environment Programme, “Reducing Food Loss through Cold Chain Development,” ozone.unep.org. Recent innovations in temperature management, on raising frozen meat storage temperatures from -18°C to -12°C, demonstrate potential for reducing carbon emissions and energy costs while maintaining product quality according to the Australian Meat Processor Corporation [3]Source: Australian Meat Processor Corporation, “Energy-Efficient Frozen Meat Storage Report,” ampc.com.au . The development of temperature-controlled warehouses, refrigerated trucks, and advanced packaging solutions helps preserve the freshness and safety of pork meat throughout the supply chain, reduces food waste by extending shelf life, and enables retailers and distributors to maintain larger inventories to respond effectively to market demand fluctuations.

Growth in the Foodservice and Hospitality Industry (On-Trade) Supports Market Demand.

Emerging markets are witnessing a surge in demand for pork meat, fuelled by the global foodservice industry's recovery and expansion. Factors such as rapid urbanization, evolving consumer preferences, and increasing disposable incomes are reshaping consumption patterns. Moreover, the rise of quick-service restaurants in developing regions is propelling market growth. Foodservice operators are turning to pork meat not only for its cost-effectiveness and consistency in food preparation but also to cater to diverse consumer tastes. While recent food inflation has nudged some consumers towards home cooking, boosting retail meat sales, the foodservice sector continues its steady consumption of pork. This trend is bolstered by institutional buyers and restaurant chains that value pork's versatility and cost-efficiency. Pork-based dishes enjoy widespread popularity in fast-casual and street food settings, particularly in Asia and Latin America. Furthermore, innovations in menu design and the incorporation of region-specific flavors have enhanced pork's allure, even in markets that are competitive or culturally discerning.

Increasing Demand for Processed and Convenient Pork Products Boosts Sales

The rising demand for processed and convenient pork products, driven by changing consumer lifestyles, urbanization, and increasing disposable income, has significantly influenced the global pork meat market. Consumers, particularly in dual-income households with busy schedules, are increasingly seeking ready-to-cook and ready-to-eat pork products that offer convenience and reduced preparation time. The expansion of modern retail formats, improved cold chain infrastructure, and growth in the food service industry, especially quick-service restaurants and casual dining establishments, have enhanced the availability and accessibility of processed pork products. Manufacturers have responded by introducing convenient packaging solutions and new product variants. For example, in November 2024, North Country Smokehouse introduced Organic Ground Pork, their first fresh product, in 1 lb packages. According to The Observatory of Economic Complexity, the global trade of pig meat reached USD 36.5 billion in 2023, marking a 5.11% increase from USD 34.7 billion in 2022, with an annualized growth rate of 4.76% over the past five years[4]Source: The Observatory of Economic Complexity, “Pig Meat,” oec.world . These trends indicate a robust and growing market for pork products, with continued expansion expected in the coming years.

Restraints Impact Analysis of Pork Meat Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental and animal welfare issues raise regulatory and consumer challenges | –0.7% | Europe, North America, Global | Long term (≥ 4 years) |

| Competition from alternative proteins such as plant-based and poultry products restrains growth | –0.5% | Developed markets, urban centers | Medium term (2-4 years) |

| Volatility in feed prices increases production costs and affects profitability | –0.4% | Grain-importing regions | Short term (≤ 2 years) |

| Religious and cultural restrictions in various regions limit pork consumption and market growth | –0.3% | Middle East, South Asia, Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental and Animal Welfare Issues Raise Regulatory and Consumer Challenges

The pork meat market faces significant constraints due to growing environmental and animal welfare concerns. Stringent regulations regarding livestock farming practices, waste management, and animal housing conditions increase operational costs for producers. Consumer awareness about sustainable farming practices and animal welfare has led to increased demand for ethically sourced pork products, requiring producers to implement costly certification programs. Additionally, environmental regulations targeting greenhouse gas emissions from pig farms and waste management systems create compliance challenges for farmers. The industry also faces pressure to reduce its water consumption and implement proper manure management systems, which requires substantial capital investment. These environmental and welfare requirements, combined with varying regional regulations, create operational complexities and impact profit margins across the global pork supply chain.

Competition from Alternative Proteins such as Plant-based and Poultry Products Restrains Growth

The increasing consumer shift toward alternative protein sources poses a significant restraint to the pork meat market growth. Plant-based meat substitutes, lab-grown meat, and other protein alternatives are gaining popularity among health-conscious consumers and those concerned about environmental sustainability. Major food companies are investing heavily in developing plant-based pork alternatives, offering products that closely mimic the taste and texture of traditional pork meat. The growing availability of these alternatives in retail stores and restaurants, combined with increasing consumer awareness about health benefits and environmental impact, affects traditional pork meat consumption. Additionally, cultural and religious dietary restrictions in various regions continue to limit pork consumption, further contributing to market restraints. The competitive pricing of some alternative protein sources also influences consumer purchasing decisions, particularly in price-sensitive markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Pork Meat Market Segment Analysis

By Meat Form:

Fresh Dominance Amid Frozen InnovationFresh/chilled pork dominates the market with a 62.95% share in 2025, as consumers consistently choose these products for their perceived superior quality and versatility in cooking applications. This segment maintains its market leadership position through established distribution networks and strong consumer trust in traditional meat purchasing habits. The preference for fresh pork is particularly evident in Asian markets, where daily shopping for fresh meat remains a cultural norm. Additionally, retail chains and butcher shops continue to expand their fresh pork offerings, supported by improvements in cold chain logistics and storage facilities.

The frozen pork segment exhibits significant growth potential with a projected CAGR of 6.55% during 2026-2031, supported by advancing preservation technologies and increasing consumer demand for convenient meal solutions. While canned and preserved pork products occupy a smaller market share, they maintain steady demand through emergency preparedness markets and regions where cold chain infrastructure remains limited. The frozen segment benefits from extended shelf life and bulk purchasing options, making it attractive to food service operators and cost-conscious consumers. Modern quick-freezing techniques have also improved the quality perception of frozen pork, contributing to its growing acceptance in both developed and emerging markets.

By Nature:

Conventional Stability Versus Organic AccelerationThe conventional segment commands a dominant 80.62% market share in 2025, supported by well-established supply chains and cost advantages that resonate with price-sensitive consumers. This segment benefits from economies of scale, standardized production processes, and widespread distribution networks that enable competitive pricing and consistent availability across global markets. The conventional pork industry's robust infrastructure and efficient production methods continue to meet the high-volume demands of processors and retailers. Additionally, established quality control measures and regulatory compliance frameworks ensure consistent product quality while maintaining cost-effectiveness.

While conventional pork maintains its market leadership, the organic segment is experiencing rapid growth with a projected CAGR of 7.09% during 2026-2031. This growth is primarily fueled by increasing health consciousness among consumers and their willingness to pay premium prices for organic pork products. However, the acceptance of premium-priced organic and traceable pork products shows notable regional variations, reflecting differences in consumer preferences and purchasing power across markets. The organic pork segment is also benefiting from increasing transparency in production methods and stricter certification standards. Furthermore, growing awareness about animal welfare and environmental sustainability is strengthening consumer trust in organic pork products.

By Cut Type:

Ham Leadership With Ribs MomentumHam dominates the global pork meat market with a 39.62% share in 2025, owing to its versatility in fresh consumption and processed applications across various culinary traditions worldwide. The adaptability of ham in different cooking methods, preservation techniques, and its widespread acceptance in both traditional and modern cuisines reinforces its position as the preferred pork cut in the market. The consistent demand for ham products in retail channels and food service establishments contributes to its market dominance. Additionally, the growing popularity of convenience foods and ready-to-eat meat products further strengthens ham's market position.

Ribs exhibit the highest growth potential with a projected CAGR of 4.34% during 2026-2031, driven by the expanding barbecue culture and premium dining trends that position them as experiential food products. Other pork cuts, including shoulders, loins, and specialty products, cater to specific market segments, with their growth trajectories influenced by regional consumption patterns and advancements in meat processing technologies. The increasing consumer preference for authentic dining experiences and specialty meat cuts supports the growth of the ribs segment. Furthermore, the rise of social media food culture and outdoor dining trends continues to boost the demand for premium pork cuts, particularly ribs.

By Distribution Channel:

Off-Trade Dominance Challenged By On-Trade RecoveryOff-trade channels dominate the global pork meat market with a 73.55% share in 2025, as consumers increasingly prefer home cooking and bulk purchasing during economic uncertainty. Retail innovation has adapted to this trend, with supermarkets strategically showcasing pork products as budget-friendly alternatives to beef for holiday meals, while also offering convenience-oriented cuts and meal kits to meet consumer demands for easy preparation. The growth in off-trade sales is particularly notable in regions with strong retail infrastructure and digital commerce capabilities. Additionally, private label offerings and value-added pork products have gained traction in retail channels, providing consumers with diverse options at competitive price points.

On-trade channels are projected to grow at a 12.10% CAGR from 2026 to 2031, driven by the recovery of the foodservice industry and changing dining preferences that emphasize experiential consumption. This growth is further supported by the revival of tourism and ongoing urbanization, which has led to increased restaurant dining frequency among younger demographics, contributing to the expansion of pork consumption through foodservice establishments. Quick-service restaurants and casual dining venues have expanded their pork-based menu offerings to capitalize on this trend. Furthermore, the rise of food delivery services and ghost kitchens has created additional growth opportunities for pork consumption in the on-trade segment.

Geography Analysis

APAC Pork Meat Market

In 2025, Asia-Pacific commands a dominant 57.54% share of the market, but growth patterns tell a nuanced story. While China's mature market edges toward saturation, Southeast Asian nations are experiencing a surge in demand, driven by a shift from plant-based to animal proteins. Notably, many countries still see per capita pork consumption lagging behind dietary recommendations, hinting at potential growth. This demand is bolstered by urbanization, rising incomes, and the increasing footprint of modern food retail and services.

Brazil Pork Meat Market

South America emerges as the global pork market's fastest-growing contender, eyeing a robust 15.05% CAGR from 2026 to 2031. Brazil stands at the forefront, enhancing production efficiency and diversifying its export markets. Bolstered by government policies promoting agricultural growth and modern farming, Brazil's competitiveness is further amplified by advancements in processing infrastructure and cold chain capabilities, ensuring exports meet global quality standards.

North America and Europe Pork Meat Market

North America and Europe, both seasoned players in the pork market, chart a course of steady, moderate growth. These regions are pivoting towards value-added products and sustainability to sharpen their competitive edge. They navigate rising regulatory challenges and competition from alternative proteins, all while aligning with shifting consumer tastes. A commitment to animal welfare and environmental sustainability is evident, with both regions adopting cutting-edge technologies for waste management and carbon footprint reduction. Additionally, they're at the helm of crafting innovative packaging and convenience products, resonating with the evolving lifestyles and preferences of consumers.

Regulatory Landscape

Regulation in the global pork meat market is shaped primarily by sanitary and phytosanitary (SPS) rules, public health certification, and facility eligibility systems that govern market access for fresh/chilled and processed pork. In the United States, USDA Food Safety and Inspection Service (FSIS) import procedures require that exporting countries run systems deemed equivalent to US standards, and that foreign plants be listed as eligible establishments under their national central competent authority. As a result, maintaining listing and certification status remains a practical gating factor for trade flows.

Trade policy volatility has also become more material for pork, as WTO trade monitoring has highlighted a sharp rise in trade value affected by new tariff measures in recent reporting cycles. In Europe, the European Commission continues to refine health certification and import-related requirements, including a June 2026 Implementing Decision (EU) 2026/1375 that updates public health certification elements for certain fresh porcine meat imports from Canada. The latest changes reinforce the operational weight of documentation, attestations, and equivalence alignment alongside core food safety controls.

Competitive Landscape

The global pork meat market demonstrates a moderate fragmented market, with major players like JBS SA, Tyson Foods Inc., WH Group Ltd, and Danish Crown A/S holding significant market share. The industry faces increasing consolidation pressures due to regulatory compliance costs and operational efficiency demands, while major processors navigate unprecedented legal challenges. Regional players maintain a strong local presence through established distribution networks and consumer relationships. Vertical integration strategies further influence the market dynamics, as companies seek to control costs and ensure supply chain stability.

Companies across the value chain are accelerating technology adoption through investments in precision livestock farming, automated processing systems, and biosecurity enhancements. These investments aim to improve productivity and ensure regulatory compliance, although smaller operators face implementation challenges due to cost barriers. Market players are also expanding their presence through product innovation, as demonstrated by Prairie Fresh's launched of Hatch Chile Pork Tenderloin in August 2024. The integration of blockchain technology for supply chain transparency and artificial intelligence for quality control represents emerging trends in the industry.

The market presents growth opportunities in premium processed products, organic segments, and emerging market penetration. However, the rise of alternative proteins necessitates defensive positioning strategies for traditional processors to maintain market share. Market participants are focusing on sustainability initiatives and animal welfare certifications to meet evolving consumer preferences. The development of value-added products and convenience-oriented offerings continues to drive product differentiation strategies in mature markets.

Pork Meat Industry Leaders

JBS S.A

WH Group Ltd

Tyson Foods Inc

Danish Crown A/S

Tönnies Holding GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Pork Meat Market Companies Covered in this Report

- JBS SA

- Tyson Foods Inc

- Vion Food Group

- Cooperl Arc Atlantique

- Hormel Foods Corporation

- Danish Crown A/S

- Charoen Pokphand Group

- Premium Food Group

- WH Group Ltd.

- BRF S.A.

- Yurun Holding Group

- Seaboard Corporation

- NH Foods Ltd.

- Frimesa Cooperativa Central

- Grupo Vall Companys

- Marfrig Global Foods Brazil

- Tönnies Holding GmbH & Co. KG

- Arthur's Food Company Pvt. Ltd.,

- Dawn Meats Group

- The Campofrío Food Group S.A.U

Market Opportunities and Future Outlook

Investment and capacity renewal in pork processing and value-added production remains a visible opportunity area, especially where aging assets and labor constraints push processors toward automation-ready, higher-throughput plants. In February 2026, Smithfield Foods announced plans for a USD 1.3 billion, 1.1 million sq ft packaged meat and fresh pork processing facility in Sioux Falls, South Dakota, intended to replace an existing legacy plant. The announcement reinforces the modernization and packaged formats whitespace that support retail and foodservice demand.

Value-added conversion and regional capacity rebalancing also stand out as active themes. JBS USA advanced its USD 135 million sausage facility project in Perry, Iowa during 2026, reflecting processor focus on downstream products such as sausage that can improve mix and reduce exposure to commodity cut volatility. In South America, Aurora Coop inaugurated an expansion in Sao Gabriel do Oeste, Mato Grosso do Sul in July 2026, lifting slaughter capacity by 60% to 5,000 pigs per day and adding flexibility for both domestic supply and export programs. On the farm and supply side, industry-led sustainability and health initiatives create adjacent opportunities for traceability, measurement, and productivity tools, supported by National Pork Board research funding of over USD 2.8 million allocated in 2025, alongside wider adoption of data-driven production practices tied to environmental and animal welfare expectations.

Recent Industry Developments in Pork Meat Market

- July 2026: Aurora Coop inaugurated an expansion at its Sao Gabriel do Oeste pork facility in Mato Grosso do Sul, Brazil, raising slaughter capacity by 60% to 5,000 pigs per day. The added throughput strengthens regional supply availability for processors and retailers and supports export flexibility from a major producing geography.

- April 2026: JBS USA progressed construction of its Perry, Iowa sausage production facility into the structural steel phase as part of its USD 135 million investment program. The project highlights continued emphasis on value-added pork processing capacity that feeds both retail packaged demand and foodservice formats.

- November 2024: North Country Smokehouse launched Organic Ground Pork in 1 lb packs, marking its first fresh product offering. The move broadens organic pork availability in convenient formats and supports premiumization and differentiated retail assortment beyond conventional cuts.

Pork Meat Market Report Scope and Research Methodology

Market Definition and Coverage

This market measures the value of pork meat sold globally, covering fresh, chilled, frozen, and preserved pork from commercially raised pigs, counted at processor-level prices across retail and food-service channels.

Scope exclusions: Edible by-products and derivative ingredients (such as lard-based shortenings, heparin, gelatin, collagen) are excluded because they follow different value chains and pricing.

Segments Covered in This Report

- By Meat Form

- Fresh/Chilled

- Frozen

- Canned/Preserved

- By Nature

- Conventional

- Organic

- By Cut Type

- Ham

- Ribs

- Others

- By Distribution Channel

- Off-Trade

- Supermarkets/Hypermarkets

- Convinience Stores

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

- On-Trade

- Off-Trade

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- South Africa

- Nigeria

- Egypt

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with mapping supply and demand signals that can be checked in public data. We typically use sources such as FAOSTAT, OECD-FAO outlook tables, UN Comtrade trade flows, and USDA livestock and meat trade publications to understand production levels, trade direction, and price context.

We then support those signals with updates from government agriculture ministries, food safety and animal health bodies (for disease and movement restrictions), and trade association reporting. Where capacity and portfolio cues are needed, we also review company filings and investor materials. When a specific financial split is required, we use paid subscriptions for company financials and news intelligence, patent search, and shipment-level import and export checks, but mainly to validate assumptions rather than replace public statistics. The sources listed here are illustrative, and the study also uses additional references to collect, cross-check, and clarify inputs.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk model with people who manage day-to-day operations in the pork value chain, including processors, distributors, retail category teams, and food-service procurement roles. We also speak with industry experts across APAC, EMEA, and the Americas so regional differences in cut preferences, pricing, and channel mix are captured, and then key assumptions are rechecked if responses show wide variance.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | APAC: 46% |

| Mid tier: 46% | Functional/Unit leaders: 37% | EMEA: 35% |

| Smaller Players: 15% | Managers: 49% | Americas: 19% |

Market-Sizing & Forecasting

Sizing is built using a top-down model where production and trade data reconstruct the available pork meat supply by region, which is then aligned to consumption signals and channel splits. The value layer is added by applying region-specific price ladders at the processor level, with adjustments for product form mixes (fresh and chilled, frozen, preserved) so the final total stays consistent with how pork is priced and sold in practice.

To keep the model realistic, we track and update a set of market fingerprints each cycle, including slaughter and production volumes, import and export movements, hot carcass weight trends, channel mix between retail and food service, and price direction seen in public agriculture price series and trade unit values. Bottom-up approximations are used as a check, mainly through sampled ASP times volume logic for key regions and cut baskets, followed by channel checks with distributors and buyers. Any gaps are then corrected using conservative ranges rather than hard fills.

Forecasts are produced using scenario analysis anchored to expected changes in production capacity, animal disease disruption risk, feed-cost direction, and recovery timing in major producing countries. The scenarios are narrowed using consensus from interviews, so the final forecast reflects a practical base case rather than an overly optimistic rebound path.

Data Validation & Update Cycle

Validation happens in layers, starting with internal checks that compare model outputs against independent signals such as regional production totals, trade balances, and plausible price bands. Outliers are reviewed, and if a jump cannot be explained by a visible driver, such as a disease-related supply shock or a documented price swing, the assumptions are revisited and selective respondents are re-contacted.

Before sign-off, the numbers go through multi-step analyst reviews that focus on year-to-year continuity, currency conversion timing, and whether channel mixes look sensible for each region. Reports are refreshed annually, and interim updates are done when major events materially change supply, trade, or pricing, followed by a final pre-delivery pass so the latest view is reflected.

Mordor Intelligence's Global Pork Meat Market Size Compared With Other Published Estimates

Published market sizes for pork meat do not always align because the scope and pricing point can shift between studies, and small differences compound at a global level. The gaps usually come from what is counted as pork meat, whether values are taken at farmgate or processor level, how preserved formats are handled, and how currency and inflation are treated for the base year.

Edible pork by-products and derivative ingredients sit outside Mordor Intelligence's scope, which improves comparability against estimates that roll lard-based outputs and collagen-type products into a single pork value pool. Another frequent gap comes from studies that rely on a single average price across regions or that use faster price escalation, while our model uses region-linked price ladders and checks totals against production and trade signals before finalizing the base year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 406.76 B (2025) | |

| Global Consultancy A | USD 298.55 B (2025) | Often narrower inclusion of preserved formats and a heavier focus on fresh and frozen cuts only, combined with a simplified global average price that can understate high-price markets. |

| Industry Publisher B | USD 326.40 B (2025) | May mix farmgate and first-sale values across countries and apply broad CAGR-based progression, which can miss region-level price ladders and channel differences between retail and food service. |

Taken together, the spread is largely explained by what gets counted as pork meat and where in the value chain pricing is captured, followed by how base-year currency and price movement are applied. Using clear inclusions, region-sensitive pricing, and practical cross-checks against production and trade, the final number remains traceable to inputs that can be revisited and repeated each update cycle.

Key Questions Answered in the Report

What is the current size of the pork meat market?

The pork meat market is valued at USD 416.12 billion in 2026 and is forecast to reach USD 466.13 billion by 2031.

Which region holds the largest share of global pork consumption?

Asia-Pacific leads with 57.54% of global revenue, driven by long-standing culinary traditions and rising incomes.

Which pork segment is growing the fastest?

Organic pork is projected to expand at a 7.09% CAGR between 2026 and 2031 as health and sustainability concerns rise.

How fast is the frozen pork segment expanding?

Frozen pork is forecast to grow at a 6.55% CAGR through 2031, supported by convenience trends and better freezer technology.

Page last updated on: