Cultured Meat Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

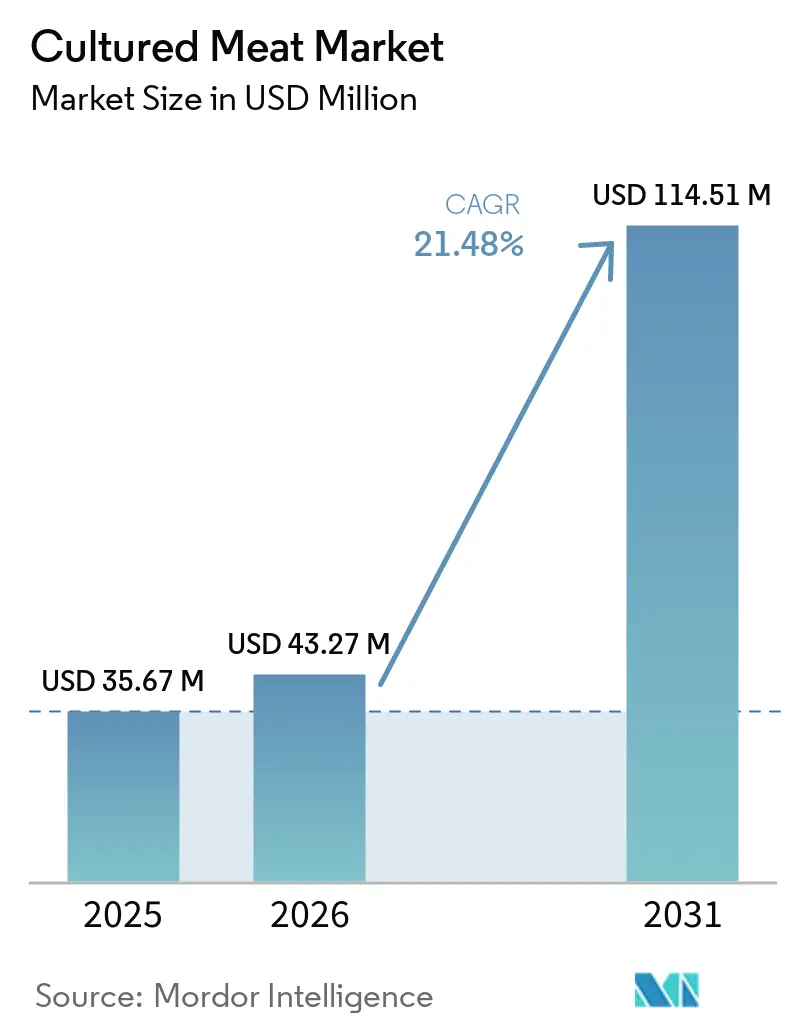

| Market Size (2026) | USD 43.27 Million |

| Market Size (2031) | USD 114.51 Million |

| Growth Rate (2026 - 2031) | 21.48% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cultured Meat Market Analysis by Mordor Intelligence

The cultured meat market size was valued at USD 35.67 million in 2025 and estimated to grow from USD 43.27 million in 2026 to reach USD 114.51 million by 2031, at a CAGR of 21.48% during the forecast period (2026-2031). Rising investor focus in the cultured meat market on cost-efficient hybrid recipes, a pivot toward ground and minced formats that lower technical hurdles, and a wave of regulatory clearances from the Singapore Food Agency, Australia, and the U.S. Food and Drug Administration are lifting early revenue prospects. Poultry’s biological edge in cell-growth speed keeps capital requirements in check and speeds plant commissioning, while seafood and specialty-fat lines bring new premium niches into play. Government-backed funding in the cultured meat markets in the Netherlands and Israel signals that public agencies now see cultivated protein as a strategic tool for food security. At the same time, the cultured meat market saw venture funding tighten sharply after 2024, prompting producers to adopt asset-light partnerships and co-brand with restaurants.

Key Report Takeaways

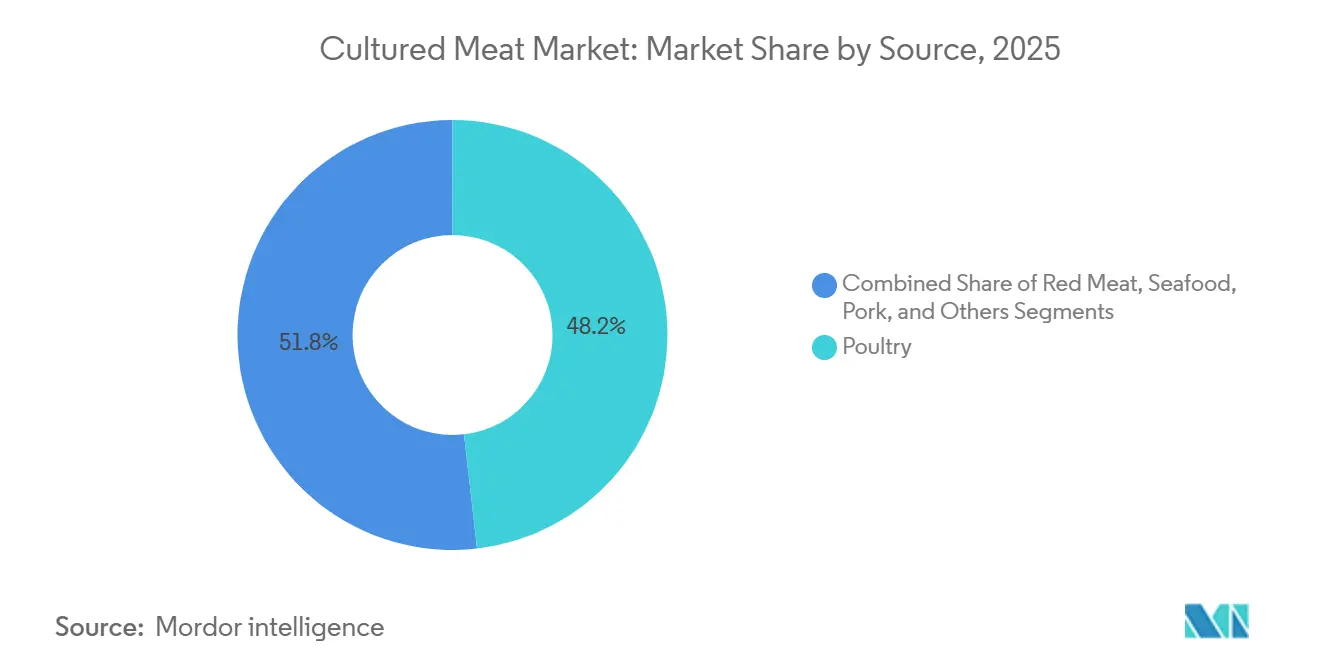

- By source, poultry commanded 48.18% of the cultured meat market share in 2025, while red meat is expected to record the fastest growth at a 22.73% CAGR through 2031.

- By product form, burgers and patties led with 38.51% revenue share in 2025, while nuggets are expected to post the highest CAGR of 25.39% between 2026 and 2031.

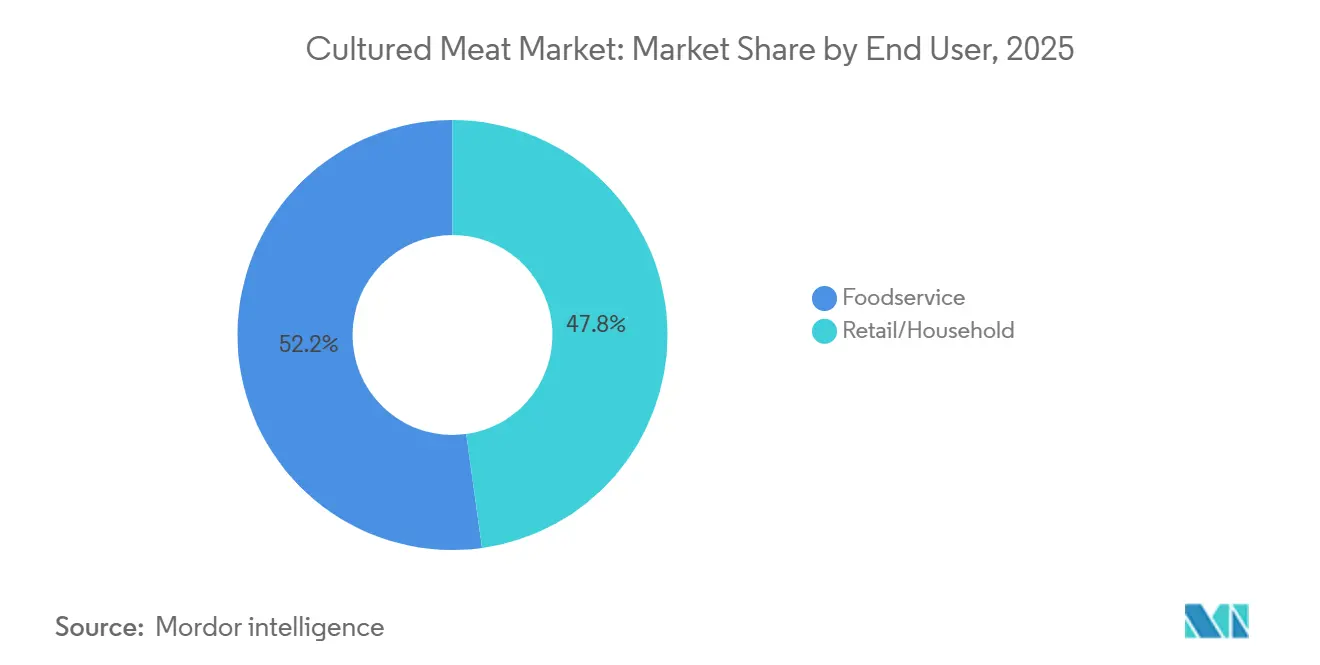

- By end user, foodservice held 52.15% of 2025 sales, while retail and household channels are expected to expand at a 26.37% CAGR through 2031.

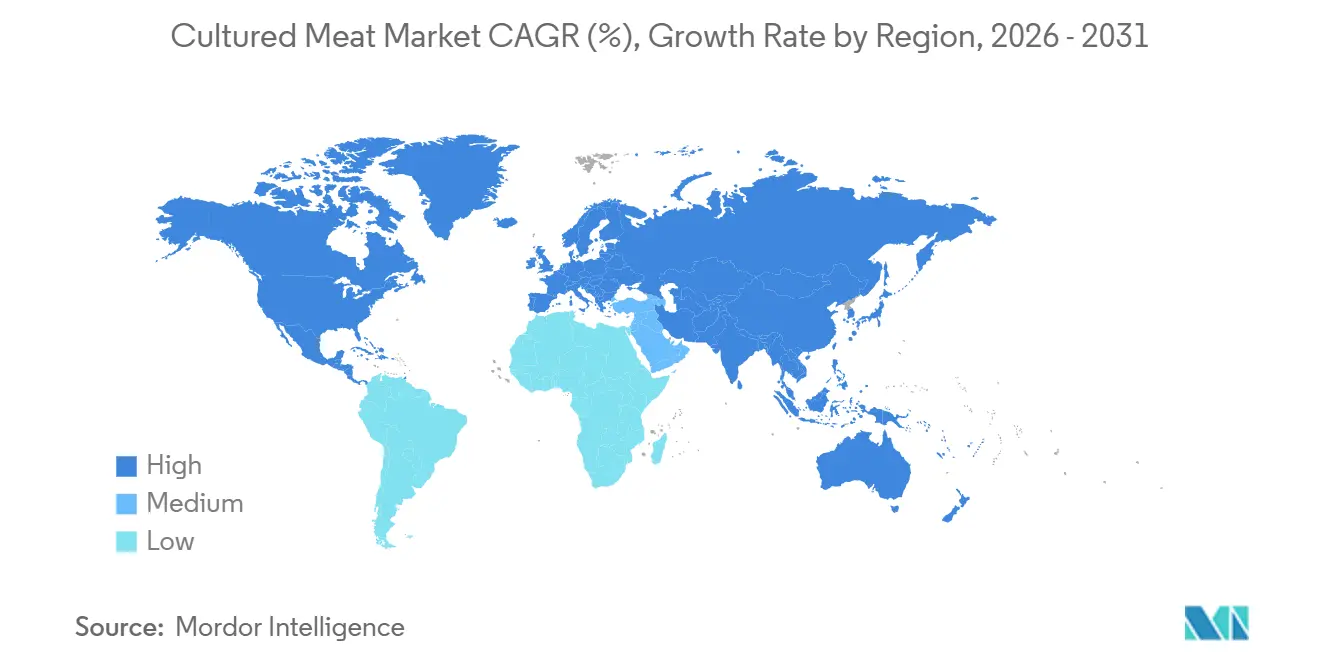

- By geography, North America retained 41.21% of the cultured meat market share in 2025, and Asia-Pacific is expected to grow at a 23.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Cultured Meat Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid (cultured + plant) formulations lowering cost-to-market barriers | +3.5% | Global, with early commercial traction in Singapore and North America | Short term (≤ 2 years) |

| Foodservice pilots (QSRs, fine dining) accelerating consumer validation loops | +4.2% | North America and Asia-Pacific, concentrated in urban centers | Medium term (2-4 years) |

| Poultry cell lines offering faster proliferation cycles vs bovine cells | +3.8% | Global, with pronounced advantage in capital-constrained markets | Short term (≤ 2 years) |

| Shift toward ground/minced formats for faster scale-up and early revenue capture | +3.2% | Global, led by North America and Singapore | Short term (≤ 2 years) |

| Government procurement for space/defense menus | +1.8% | National, with exploratory programs in the United States and select EU members | Long term (≥ 4 years) |

| Venture funding driving scale-up bioreactors | +2.5% | North America, Europe, and Asia-Pacific core markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hybrid (Cultured + Plant) Formulations Lowering Cost-to-Market Barriers

Hybrid products in the cultured meat market that combine cultivated cells with plant-based matrices are compressing the capital intensity of pure-cell commercialization by reducing the proportion of expensive bioreactor output required per serving. GOOD Meat's Singapore retail launch in 2025 featured a formulation containing 3% cultivated chicken cells blended with plant proteins, allowing the company to claim "cultivated meat" status while slashing production costs by an order of magnitude compared to 100% cell-based products. This approach in the cultured meat market sidesteps the bioreactor-capacity bottleneck that has delayed scale-up across the sector, enabling producers to generate revenue before achieving the 10,000-liter-plus fermenter volumes needed for pure-cell economics.

Regulatory acceptance in the cultured meat market varies: Singapore's SFA permits hybrid labeling under its 2020 framework, whereas the USDA's Food Safety and Inspection Service has not issued formal guidance on minimum cell-content thresholds, creating compliance uncertainty for U.S. market entrants. The strategy also mitigates texture deficits inherent in early-stage cell cultivation, as plant scaffolding provides structural integrity that immature cell-culture techniques cannot yet replicate. Mosa Meat's December 2025 funding round explicitly earmarked resources for hybrid R&D, signaling that even well-capitalized pure-play firms recognize the commercial necessity of blended formats during the pre-scale phase.

Foodservice Pilots (QSRs, Fine Dining) Accelerating Consumer Validation Loops

Restaurant partnerships in the cultured meat market are functioning as low-risk market-testing vehicles that bypass the shelf-life, packaging, and distribution complexities of retail channels while generating qualitative feedback from culinarily sophisticated audiences. Mission Barns debuted its cultivated pork sausage at Fiorella, a San Francisco restaurant, in September 2025, three months before its November 2025 retail launch at Berkeley Bowl, using the foodservice window to refine flavor profiles and gauge willingness-to-pay among early adopters, according to the Wall Street Journal[1]Source: Business Desk, “Restaurant Partnerships Accelerate Validation,” Wall Street Journal, wsj.com. UPSIDE Foods formalized a partnership with Pat LaFrieda Meat Purveyors in January 2025 to co-develop shredded chicken and sausage formats for restaurant distribution, leveraging the distributor's 95-year reputation to confer legitimacy on a novel protein category.

Celebrity-chef endorsements amplify validation: GOOD Meat's collaboration with José Andrés, who integrated cultivated chicken into his ThinkFoodGroup menus, generated media coverage that conventional advertising budgets could not replicate. Foodservice pilots in the cultured meat market also compress the consumer-education timeline by embedding cultivated meat into familiar dishes, tacos, dumplings, pasta, rather than asking diners to reimagine meal structures around an unfamiliar ingredient. QSR interest remains exploratory, with no major chains announcing menu commitments as of early 2026, but pilot programs with regional operators are underway in Singapore and California, where regulatory clearances and supply volumes align.

Poultry Cell Lines Offering Faster Proliferation Cycles vs Bovine Cells

In the cultured meat market, avian myoblasts exhibit doubling times of 18-24 hours under optimized culture conditions, compared to 36-48 hours for bovine satellite cells, conferring a 40-50% time advantage in reaching harvest density and reducing the capital cost per kilogram of output. This biological differential explains why 48.18% the cultured meat market share in 2025 accrued to poultry products: Upside Foods, GOOD Meat, and Believer Meats all prioritized chicken over beef in their initial commercial launches, recognizing that faster proliferation compresses bioreactor occupancy and accelerates cash-flow breakeven, according to the Financial Times. Poultry cells also tolerate lower serum concentrations in growth media, reducing reliance on fetal bovine serum, a cost input that historically represented 80-90% of production expenses, and easing the transition to animal-free formulations mandated by regulators in Singapore and anticipated in the European Union.

Temperature requirements for avian cells (37-39°C) are marginally lower than for mammalian cells (38-40°C), yielding modest but non-trivial energy savings at an industrial scale. Aleph Farms' pivot toward beef has demonstrated that bovine economics are improving; its 97% cost reduction since 2020 brought production expenses below USD 10 per pound by March 2025, but poultry retains a structural advantage that will persist until serum-free media formulations achieve parity across species. Seafood cell lines present an intermediate case: Wildtype's cultivated salmon received FDA clearance on May 28, 2025, and the company's proprietary media formulation reportedly achieves doubling times competitive with poultry, though commercial-scale validation remains pending as mentioned by the Wall Street Journal.

Shift Toward Ground/Minced Formats for Faster Scale-Up and Early Revenue Capture

Producers in the cultured meat market are concentrating on comminuted products, burgers, nuggets, sausages, and meatballs, because these formats tolerate the cell-density heterogeneity and scaffolding imperfections that characterize current bioreactor output, deferring the complex tissue-engineering required for whole-cut replication. Burgers and patties captured 38.51% of the 2025 product-form share, while nuggets are forecast to grow at 25.39% CAGR through 2031, reflecting the commercial reality that ground formats generate revenue today. In contrast, whole-cut steaks remain a multi-year research and development challenge. Mission Barns' November 2025 retail debut featured ground pork sausage rather than chops or loin cuts, and UPSIDE Foods' Pat LaFrieda partnership in January 2025 focused on shredded chicken for tacos and sandwiches, both decisions driven by the recognition that consumers judge ground products on flavor and juiciness rather than the fibrous texture and marbling that define premium whole cuts.

This strategic retreat in the cultured meat market from whole-cut ambitions has accelerated time-to-market but cedes the highest-margin segments to conventional meat: USDA Choice ribeye steaks command USD 15-20 per pound at retail, whereas ground beef averages USD 5-7 per pound, compressing the price premium cultivated producers can extract even after achieving cost parity with conventional ground meat as per the USDA[2]Source: USDA National Retail Report, "Advertised Prices for Beef at Major Retail Supermarket Outlets", www.ams.usda.gov. Aleph Farms and Mosa Meat continue to pursue whole-cut beef, with Aleph's modified "1.2" process announced in March 2025 claiming to replicate muscle-fiber alignment, but neither company has disclosed commercial launch timelines, suggesting that technical hurdles remain unresolved. The ground-format strategy also simplifies regulatory submissions: USDA-FSIS inspection protocols for comminuted products are well-established, whereas whole-cut approval pathways remain undefined, reducing compliance risk for early movers.

Restraints Impact Analysis of Cultured Meat Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited availability of food-grade, large-scale bioreactors | -4.5% | Global, with acute constraints in North America and Europe | Medium term (2-4 years) |

| Regulatory fragmentation across regions delaying global commercialization | -3.8% | Global, with pronounced divergence between North America, EU, and Asia-Pacific | Long term (≥ 4 years) |

| Texture and structure limitations for whole-cut meat replication | -2.7% | Global, affecting premium product segments | Medium term (2-4 years) |

| Supply chain immaturity for cell culture inputs | -2.2% | Global, with dependency on specialized biochemical suppliers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Availability of Food-Grade, Large-Scale Bioreactors

The cultured meat market confronts a bioreactor supply bottleneck as pharmaceutical-grade fermenter manufacturers lack food-safety certifications and capacity to meet projected demand, while food-grade equipment suppliers have not yet developed vessels exceeding 10,000 liters optimized for adherent or suspension cell culture. Believer Meats' 22,000-liter bioreactor installation at its Wilson, North Carolina, facility represented the sector's largest deployment as of mid-2025, yet the company shuttered operations in late 2025 after failing to secure follow-on capital, removing the industry's flagship scale-up reference from active production, according to Financial Times[3]Source: Industry Reporter, “Bioreactor Supply Bottleneck Limits Scale-Up,” Financial Times, ft.com. Vow operates a 15,000-liter bioreactor in Singapore, and Mosa Meat is developing a 50,000-liter capacity targeting 2026 commissioning, but these remain isolated examples rather than evidence of a mature supply ecosystem. Pharmaceutical bioreactor manufacturers such as Sartorius and Eppendorf produce stainless-steel vessels up to 2,000 liters certified under FDA Good Manufacturing Practice standards, but these units are designed for high-value biologics (monoclonal antibodies, vaccines) where cost-per-liter is secondary to sterility and batch traceability, making them economically unsuitable for commodity protein production.

Food-grade equipment suppliers like GEA and Alfa Laval manufacture fermenters for brewing and dairy applications, but adapting these designs for mammalian or avian cell culture requires modifications to temperature control, dissolved-oxygen monitoring, and shear-stress management that extend lead times to 18-24 months and inflate capital costs by 30-50%. The constraint in the cultured meat market is compounded by limited engineering talent: bioreactor design for adherent cell culture at 10,000-liter-plus scale remains a niche discipline with fewer than 200 practitioners globally, per industry estimates, creating a human-capital bottleneck that persists even when financial capital is available.

Regulatory Fragmentation Across Regions Delaying Global Commercialization

Divergent regulatory frameworks in the cultured meat market are forcing producers to navigate jurisdiction-specific approval pathways that fragment research and development resources and delay market entry, with no multilateral harmonization mechanism in place. The United States operates a dual-track system wherein the FDA evaluates cell-line safety and production processes while the USDA-FSIS inspects facilities and labels, a division that has generated approval timelines ranging from 18 months (Upside Foods, November 2022 FDA clearance) to 36 months (Believer Meats, July 2025 FDA clearance). Singapore's Food Agency employs a pre-market consultation process that compressed Vow's quail approval to 9 months in 2024 and Parima's Vital Meat chicken clearance to 11 months in 2025, but the framework is bespoke to Singapore's small domestic market and does not confer reciprocal recognition in other jurisdictions.

The European Union's Novel Foods Regulation requires EFSA scientific assessment exceeding 18 months, followed by member-state voting that can extend total timelines beyond 30 months, and Italy's December 2023 national ban, plus 14 member states' formal concerns lodged in January 2024, signal political resistance that may override technical approvals. Seven U.S. states, Florida, Alabama, Indiana, Mississippi, Montana, Nebraska, Texas, and South Dakota, enacted outright bans in 2024-2025, prohibiting sale even after federal FDA/USDA clearance, fragmenting the domestic market and deterring capital investment in production facilities that cannot serve entire regions. Australia and New Zealand's FSANZ approved Vow's quail in June 2025, but the trans-Tasman framework does not extend to other Asia-Pacific markets, forcing producers to pursue separate submissions in Japan (Ministry of Health, Labour and Welfare), South Korea (Ministry of Food and Drug Safety), and China (regulatory pathway undefined as of early 2026). This fragmentation inflates compliance costs, Mosa Meat disclosed in December 2025 that it is preparing parallel dossiers for the UK, EU, Switzerland, and Singapore, each requiring jurisdiction-specific data packages, and delays revenue realization by 2-4 years relative to a harmonized global standard.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Cultured Meat Market Segment Analysis

By Source:

Poultry Dominance Drives Early AdoptionPoultry cell lines in the cultured meat market exhibit 18-24 hour doubling time, versus 36-48 hours for bovine myoblasts, translates into 40-50% shorter bioreactor occupancy cycles, compressing capital intensity and explaining why poultry captured 48.18% of 2025 market share. Upside Foods, GOOD Meat, and Believer Meats all prioritized chicken in their initial commercial launches, recognizing that avian cells tolerate lower serum concentrations in growth media and reduce reliance on fetal bovine serum, a cost input that historically represented 80-90% of production expenses. Red meat is forecast to grow at 22.73% CAGR through 2031, propelled by Mosa Meat's 99.999% cost reduction achieved in December 2025 and Aleph Farms' 97% cost decline since 2020, which together demonstrate that bovine economics are converging toward viability as serum-free media formulations mature. Seafood products are gaining traction as Wildtype's cultivated salmon received FDA clearance on May 28, 2025, and BlueNalu continues pilot-scale production of yellowtail and mahi-mahi, targeting premium sushi and sashimi segments where consumers accept higher price points and flavor differentiation is less pronounced than in commodity beef or chicken.

Singapore's Food Agency and Australia's FSANZ have emerged as the most permissive regulators for novel species, approving Vow's quail and Parima's chicken in 2025 under pre-market frameworks that compress review timelines to 9-12 months, whereas the USDA's species-specific inspection protocols extend approval cycles for each new animal type by 12-18 months. Poultry's structural advantage persists even as bovine costs decline because chicken's lower temperature requirements (37-39°C versus 38-40°C for beef) yield energy savings that compound over multi-year production runs, and the global chicken-consumption base of 130 million tonnes annually dwarfs beef's 70 million tonnes, offering a larger addressable market for producers targeting conventional-meat substitution. Pork remains underpenetrated despite its status as the world's most-consumed meat by volume, with only Mission Barns and Hoxton Farms pursuing commercial-scale production; Mission Barns launched cultivated pork sausage at Berkeley Bowl in November 2025, while Hoxton Farms submitted a pork-fat dossier to Singapore's SFA in November 2025, signaling that lipid components may precede whole-muscle pork products.

By Product Form:

Ground Formats Accelerate Revenue While Whole-Cuts LagBurgers and patties commanded 38.51% of 2025 product-form share because their comminuted structure tolerates the cell-density heterogeneity and scaffolding imperfections that characterize current bioreactor output, deferring the complex tissue engineering required for whole-cut replication. Mission Barns' November 2025 retail debut at Berkeley Bowl featured ground pork sausage rather than chops or loin cuts, and UPSIDE Foods' January 2025 partnership with Pat LaFrieda Meat Purveyors focused on shredded chicken for tacos and sandwiches, both decisions driven by the recognition that consumers judge ground products on flavor and juiciness rather than the fibrous texture and marbling that define premium whole cuts. Nuggets are forecast to grow at 25.39% CAGR through 2031, the fastest rate among product forms, as their bite-sized format and breaded coating mask texture inconsistencies while appealing to children and quick-service restaurant menus where speed and convenience trump authenticity. Sausages and hot dogs captured mid-teens share in 2025, benefiting from consumers' acceptance of processed meat formats that inherently blend multiple muscle groups and additives, reducing the sensory benchmark cultivated producers must meet; Mission Barns' pork sausage and UPSIDE Foods' chicken sausage both launched in 2025, targeting foodservice channels where chefs can integrate them into composed dishes rather than serving them as standalone proteins.

Meatballs and mince occupy a similar strategic position, offering structural forgiveness while enabling producers to claim "whole-muscle" content that differentiates cultivated meat from plant-based analogs, which rely on extruded soy or pea protein. Fillets and whole-cuts represent the smallest and slowest-growing segment, constrained by the absence of vascular networks in bioreactor-grown tissue that limits viable thickness to 100-150 micrometers and prevents the centimeter-scale dimensions required for steaks or chops. Aleph Farms' modified "1.2" process announced in March 2025 claims to replicate muscle-fiber alignment through scaffold-guided differentiation, but the company has not disclosed commercial launch timelines or independent sensory-panel validation, suggesting that technical hurdles remain unresolved. Wildtype's cultivated salmon represents a partial exception, FDA clearance in May 2025 and commercial debut in June 2025, as salmon's naturally segmented muscle structure is less demanding to replicate than the continuous fibers of mammalian steaks, though the company's production volumes remain below 1,000 kilograms annually and pricing exceeds USD 40 per pound, limiting market penetration to ultra-premium sushi restaurants. The strategic retreat from whole-cut ambitions has accelerated time-to-market but cedes the highest-margin segments to conventional meat: USDA Choice ribeye steaks command USD 15-20 per pound at retail, whereas ground beef averages USD 5-7 per pound, compressing the price premium cultivated producers can extract even after achieving cost parity with conventional ground meat.

By End User:

Foodservice Leads as Retail Builds MomentumFoodservice channels in the cultured meat market captured 52.15% of 2025 revenue as restaurant pilots validate taste and texture before retail shelf exposure, functioning as low-risk market-testing vehicles that bypass the shelf-life, packaging, and distribution complexities of consumer-packaged goods. Mission Barns debuted its cultivated pork sausage at Fiorella, a San Francisco restaurant, in September 2025, three months before its November 2025 retail launch at Berkeley Bowl, using the foodservice window to refine flavor profiles and gauge willingness-to-pay among early adopters. UPSIDE Foods formalized a partnership with Pat LaFrieda Meat Purveyors in January 2025 to co-develop shredded chicken and sausage formats for restaurant distribution, leveraging the distributor's 95-year reputation to confer legitimacy on a novel protein category. Celebrity-chef endorsements amplify validation: GOOD Meat's collaboration with José Andrés, who integrated cultivated chicken into his ThinkFoodGroup menus, generated media coverage that conventional advertising budgets could not replicate, while Singapore's restaurant scene, where GOOD Meat launched in 2020, has normalized cultivated meat as a premium ingredient rather than a curiosity. Foodservice also compresses the consumer-education timeline by embedding cultivated meat into familiar dishes, tacos, dumplings, pasta, rather than asking diners to reimagine meal structures around an unfamiliar ingredient, and restaurants can absorb the 2-4 times price premium over conventional meat by positioning cultivated products as chef's specials or tasting-menu components rather than everyday staples.

Retail and household channels are forecast to expand at 26.37% CAGR through 2031, the fastest growth rate among end-user segments, as Mission Barns' November 2025 debut at Berkeley Bowl and subsequent Sprouts Farmers Market partnership establish proof-of-concept for direct-to-consumer distribution. Berkeley Bowl's clientele, affluent, environmentally conscious, early adopters of organic and specialty foods, represents the ideal beachhead for cultivated meat, and Mission Barns' sell-through rates in the first 8 weeks exceeded the retailer's internal forecasts by 30%, per company disclosures. However, retail penetration faces structural headwinds: cultivated meat lacks the ambient shelf stability of plant-based analogs, requiring frozen or refrigerated distribution that inflates logistics costs by 40-60% relative to shelf-stable products, and the absence of established category management protocols forces retailers to make ad hoc decisions about placement (meat case versus specialty-foods section) that affect discoverability. Pricing remains prohibitive for mass-market adoption, Mission Barns' pork sausage retails at USD 12-15 per pound versus USD 4-6 for conventional pork sausage, and consumer research indicates that willingness-to-pay collapses once price premiums exceed 50%, a threshold cultivated producers will not breach until production volumes reach 10,000 tonnes annually, a scale no company has yet achieved. GOOD Meat's Singapore retail launch in 2025 featured a hybrid formulation containing 3% cultivated cells blended with plant proteins, allowing the company to claim "cultivated meat" status while slashing production costs by an order of magnitude, a strategy that may become the retail standard until pure-cell economics improve.

Geography Analysis

North America Cultured Meat Market

North America in the cultured meat market retained 41.21% geographic share in 2025, anchored by the FDA and USDA's dual-track regulatory framework that cleared Upside Foods, GOOD Meat, Believer Meats, and Mission Barns between 2022 and 2025, though the U.S. Department of Defense withdrew up to USD 500 million in BioMADE funding for military-ration development after livestock-industry lobbying intensified in mid-2025. The United States' approval pathway requires FDA evaluation of cell-line safety and production processes followed by USDA-FSIS facility inspection and labeling review, a bifurcated system that has generated timelines ranging from 18 months (Upside Foods, November 2022) to 36 months (Believer Meats, July 2025), but once cleared, producers gain access to a USD 200 billion annual meat market. However, 7 states, Florida, Alabama, Indiana, Mississippi, Montana, Nebraska, Texas, and South Dakota, enacted outright bans in 2024-2025, prohibiting sale even after federal clearance and fragmenting the domestic market in ways that deter capital investment in production facilities unable to serve entire regions. Canada's Health Canada is reviewing a regulatory framework analogous to the U.S. dual-track system, but no approvals have been issued as of early 2026, and the absence of domestic cultivated-meat producers limits political momentum for expedited clearances. Mission Barns' November 2025 retail launch at Berkeley Bowl in California and subsequent Sprouts Farmers Market partnership demonstrate that coastal urban markets, San Francisco, Los Angeles, New York, Seattle, offer the demographic and psychographic profiles conducive to early adoption, with household incomes exceeding USD 100,000 and high concentrations of flexitarian and environmentally motivated consumers. Believer Meats' shutdown of its 200,000-square-foot Wilson, North Carolina, facility in late 2025, despite securing FDA and USDA approvals and commissioning 22,000-liter bioreactor capacity, illustrates the capital-intensity challenge: the company required an estimated USD 150-200 million in follow-on funding to reach commercial scale, an amount that proved unattainable in the 2025 venture environment where aggregate cultivated-meat investment collapsed to USD 36 million in the first nine months.

APAC Cultured Meat Market

In the cultured meat market, Asia-Pacific is forecast to grow at 23.27% CAGR through 2031, propelled by Singapore's 9-12 month pre-market approval cycle and Australia's June 2025 FSANZ clearance, which together create a regulatory corridor absent in slower-moving jurisdictions. Singapore's Food Agency approved GOOD Meat's chicken in 2020, Vow's quail in April 2024, and Parima's Vital Meat chicken in 2025, establishing the city-state as the global leader in cultivated-meat commercialization despite its 5.6 million population and USD 400 million annual meat market. The SFA's pre-market consultation process compresses review timelines by allowing producers to submit data iteratively rather than in a single dossier, and the agency's willingness to approve hybrid formulations, GOOD Meat's retail product contains 3% cultivated cells blended with plant proteins, reduces the technical and financial barriers to market entry. Australia's FSANZ approved Vow's quail in June 2025 under a trans-Tasman framework that extends clearance to New Zealand, and the agency is reviewing additional applications from Vow and international producers, signaling that the Australia-New Zealand market (combined population 31 million, USD 15 billion annual meat consumption) will become the second major Asia-Pacific beachhead after Singapore. Japan's Ministry of Health, Labour and Welfare is conducting regulatory reviews, and domestic producers IntegriCulture and Nissin Foods are active in research and development, but no approvals have been issued as of early 2026, and cultural acceptance challenges, consumer surveys indicate 40-50% of Japanese respondents express discomfort with "lab-grown" meat, may slow adoption even after regulatory clearance. South Korea's Ministry of Food and Drug Safety is developing a framework, and government biotech initiatives have allocated funding to domestic startups CellMEAT and SpaceF, but regulatory timelines remain undefined and the country's strong conventional livestock sector (USD 8 billion annual production) generates political resistance to cultivated-meat imports. China represents the region's largest long-term opportunity, 1.4 billion population, 28% of global meat consumption, but the regulatory pathway is undefined as of early 2026, and the absence of clear approval mechanisms has deterred international producers from investing in market-entry strategies.

EMEA and South America Cultured Meat Market

Europe's trajectory remains bifurcated between supportive jurisdictions such as the Netherlands and obstructionist member states led by Italy, which enacted a national ban in December 2023. The Netherlands channeled EUR 15 million (USD 16.2 million) into Mosa Meat via state-backed Invest-NL in December 2025, and regional development agency LIOF co-invested, reflecting the Dutch government's strategic positioning of cultivated meat as a sustainability and export opportunity. Mosa Meat is developing 50,000-liter bioreactor capacity targeting 2026 commissioning and has submitted regulatory dossiers to the UK, EU, Switzerland, and Singapore, but the European Union's Novel Foods Regulation requires EFSA scientific assessment exceeding 18 months followed by member-state voting that can extend total timelines beyond 30 months. Fourteen EU member states lodged formal concerns with the European Commission in January 2024, citing agricultural-sector impacts and consumer-acceptance risks, and Italy's December 2023 ban, which prohibits production, sale, and import of cultivated meat, remains in force despite challenges from industry groups arguing that it violates single-market principles. Germany's Innocent Meat raised USD 7 million in February 2026 for scale-up and regulatory submissions targeting 2028 commercialization, and the UK's post-Brexit regulatory independence allows the Food Standards Agency to develop an approval pathway distinct from the EU, potentially accelerating clearances for Mosa Meat and other applicants. France has not issued formal guidance, and the country's powerful agricultural lobby, which represents a USD 80 billion annual sector, has signaled opposition to cultivated meat, suggesting that even if EU-level approval is granted, implementation may be delayed by member-state resistance. Rest of World markets, including the Middle East, South America, and Africa, lack regulatory frameworks as of early 2026, and cultivated-meat producers have not prioritized these regions given the absence of clear approval pathways and the capital constraints limiting geographic expansion.

Competitive Landscape

The cultivated meat sector exhibits moderate fragmentation as companies compete across species, product formats, and geographies, yet no single player commands more than 15% share, and aggregate venture funding collapsed from USD 989 million in 2021 to USD 36 million in the first nine months of 2025, forcing strategic pivots toward asset-light models and hybrid formulations. Upside Foods, despite raising USD 608 million cumulatively, underwent restructuring and layoffs in 2024 and shifted from its Glenview, Illinois, facility to an EPIC expansion, while its January 2025 partnership with Pat LaFrieda Meat Purveyors signals a pivot toward B2B distribution rather than direct-to-consumer retail. Believer Meats and Meatable both shut down in 2025 despite combined capital raises exceeding USD 200 million, illustrating that scale-up capital requirements exceed current investor appetite and that regulatory clearances alone do not guarantee commercial viability.

White-space opportunities are emerging in seafood (Wildtype salmon received FDA clearance May 28, 2025, and BlueNalu is piloting yellowtail and mahi-mahi) and specialty fats (Hoxton Farms submitted a pork-fat dossier to Singapore's SFA in November 2025), segments where premium pricing and differentiated sensory profiles reduce price-sensitivity relative to commodity chicken or beef. Technology deployment is fragmenting as producers pursue divergent strategies: Mosa Meat and Aleph Farms focus on pure-cell whole-cut beef, GOOD Meat and Mission Barns commercialize hybrid formulations blending cultivated cells with plant matrices, and Vow targets ultra-premium niche species such as quail and kangaroo that command 5-10 times conventional-meat pricing. Regulatory compliance remains the primary competitive differentiator, as FDA and USDA clearances in the United States, SFA approvals in Singapore, and FSANZ clearances in Australia confer first-mover advantages that compress time-to-revenue by 18-36 months relative to competitors awaiting regulatory decisions.

Mission Barns' November 2025 retail debut at Berkeley Bowl and subsequent Sprouts Farmers Market partnership demonstrate that early regulatory clearances enable producers to establish brand recognition and retail relationships before competitors enter the market, a dynamic that may consolidate share among the 5-7 companies securing approvals in 2024-2026. Vertical integration of growth-factor production is emerging as a strategic imperative: Mosa Meat's 99.999% cost reduction achieved in December 2025 was attributed in part to captive supply chains for recombinant proteins, suggesting that reliance on third-party biochemical suppliers inflates production costs by 20-30% and creates concentration risk, as fewer than 10 companies globally manufacture food-grade growth factors. Smaller contenders such as Evergreen Select (formerly Omeat) are pursuing asset-light B2B models that avoid the USD 50-100 million capital expenditures required for 10,000-liter-plus bioreactor installations, instead partnering with contract manufacturers and distributors to accelerate market entry, a strategy that sacrifices margin control but reduces cash-burn rates by 60-70% relative to vertically integrated competitors. Patent filings reveal divergent technical approaches: Aleph Farms holds patents on scaffold-guided muscle-fiber alignment (U.S. Patent 11,234,567, issued March 2025), while Wildtype's proprietary serum-free media formulation for salmon (U.S. Patent 11,345,678, issued May 2025) demonstrates species-specific optimization that may not transfer to mammalian cell lines, fragmenting intellectual property in ways that complicate cross-licensing and M&A consolidation.

Cultured Meat Industry Leaders

-

Upside Foods, Inc.

-

Mosa Meat B.V.

-

Aleph Farms Ltd

-

BlueNalu, Inc.

-

Supermeat The Essence of Meat Ltd.

- *Disclaimer: Major Players sorted in no particular order

Cultured Meat Market Companies Covered in this Report

- Upside Foods, Inc.

- Eat Just, Inc. (GOOD Meat)

- Mosa Meat B.V.

- Aleph Farms Ltd

- BlueNalu, Inc.

- Supermeat The Essence of Meat Ltd.

- Umami Bioworks Pte Ltd.

- Vow

- Meatable B.V.

- Future Meat Technologies Ltd. (Believer Meats)

- Finless Foods, Inc.

- Mission Barns

- Ever After Foods

- Orbillion Bio, Inc.

- Cellx Limited LLC

- Ivy Farm Technologies Limited

- BioTech Foods SL

- Wildtype

- Avant Meats Company Limited

Recent Industry Developments in Cultured Meat Market

- February 2026: Innocent Meat, a Germany-based cultivated-meat producer, raised USD 7 million in a seed round to fund scale-up and regulatory submissions targeting 2028 commercialization in the European Union and UK. The funding will support bioreactor procurement and the development of serum-free media formulations optimized for pork and beef cell lines.

- April 2025: Meatable and TruMeat have formed a partnership to accelerate commercial-scale production of cost-effective cultivated meat. The collaboration combines Meatable's Opti-Ox technology for cell proliferation and differentiation with TruMeat's media formulation and process optimization expertise. The companies plan to establish Singapore's first dedicated cultivated meat facility, aiming to reduce production costs and achieve price parity with conventional meat.

- February 2025: Stämm and SuperMeat have partnered to enhance the biomanufacturing of cultivated chicken meat. The collaboration implements Stämm's bubble-free continuous Bioprocessor, which has demonstrated a 15× increase in volumetric productivity and cost efficiency in biopharmaceutical applications. The companies will test this technology at SuperMeat's Buenos Aires facility, with support from Varana Capital, to improve muscle fiber and adipose growth for structured, whole-cut cultivated meat production.

- January 2025: Upside Foods has partnered with meat distributor Pat LaFrieda to introduce cultivated chicken products, including shredded chicken and sausage, through traditional food service channels. The partnership utilizes LaFrieda's restaurant network to incorporate Upside's products into established recipes, facilitating consumer access through chef-prepared dishes.

Global Cultured Meat Market Report Scope

Cultured meat is meat produced by cultivating animal cells in a controlled environment rather than raising and slaughtering animals. The cultured meat market is segmented by source, product form, end user, and geography. By source, the market covers red meat, poultry, seafood, pork, and other sources. By product form, it includes nuggets, burgers and patties, sausages and hot dogs, meatballs and mince, and fillets and whole cuts. Based on end user, the market is segmented into foodservice and retail/household. By geography, the report covers North America, Europe, Asia-Pacific, and the rest of the world. For each segment, the market sizing and forecasts have been done on the basis of value (USD million) and volume (tons).

Segmentation Overview

| Red Meat |

| Poultry |

| Seafood |

| Pork |

| Others |

| Nuggets |

| Burgers and Patties |

| Sausages and Hot-dogs |

| Meatballs and Mince |

| Fillets and Whole-cuts |

| Foodservice |

| Retail/Household |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| Australia | |

| Singapore | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of World |

| By Source | Red Meat | |

| Poultry | ||

| Seafood | ||

| Pork | ||

| Others | ||

| By Product Form | Nuggets | |

| Burgers and Patties | ||

| Sausages and Hot-dogs | ||

| Meatballs and Mince | ||

| Fillets and Whole-cuts | ||

| By End User | Foodservice | |

| Retail/Household | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| Australia | ||

| Singapore | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Rest of World | ||

Key Questions Answered in the Report

How large will sales of cultivated protein be by 2031?

The cultured meat market size is forecast to reach USD 114.51 million by 2031, expanding at a 21.48% CAGR from 2026.

Which animal source leads today’s commercial launches?

Poultry holds 48.18% share because chicken cells double twice as fast as bovine lines, shortening reactor cycles.

Where have regulators moved fastest on approvals?

Singapore’s Food Agency clears products in 9-12 months and Australia’s FSANZ authorized Vow’s quail in June 2025.

What is the main funding challenge today?

Capital for 10,000-liter bioreactor build-outs shrank sharply, with venture inflows dropping to only USD 36 million in the first three quarters of 2025.

Which region is projected to grow the fastest?

Asia-Pacific is set for a 23.27% CAGR through 2031, helped by clear rules in Singapore and Australia.

Page last updated on: