Meat Processing Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.90 Billion |

| Market Size (2031) | USD 12.60 Billion |

| Growth Rate (2026 - 2031) | 4.94% CAGR |

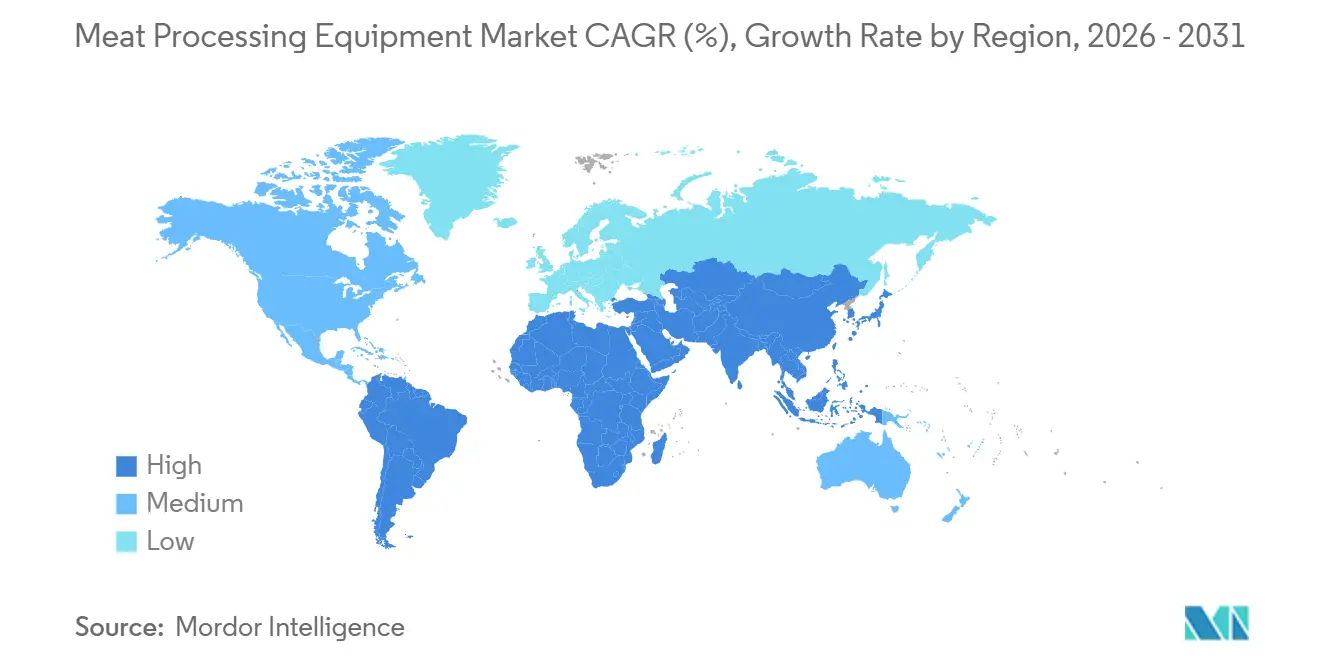

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Meat Processing Equipment Market Analysis by Mordor Intelligence

The meat processing equipment market size is expected to increase from USD 9.62 billion in 2025 to USD 9.90 billion in 2026 and reach USD 12.60 billion by 2031, growing at a CAGR of 4.94% over 2026-2031. This growth is largely fueled by shifting consumer demands, heightened food safety regulations, and an industry-wide push towards automation. Leading the charge is the Asia-Pacific region, bolstered by swift industrialization and supportive government initiatives, including India's substantial INR 15,000 crore (USD 1,550 million) investment in meat processing infrastructure. Currently, grinding and mixing equipment dominate usage, but there's a notable surge in the adoption of cutting and slicing tools. While pork continues to be the predominant meat processed, there's a rising inclination towards poultry equipment, aligning with the growing appetite for leaner proteins. Industrial processors, in their quest for efficiency and consistency, are at the forefront of equipment investments. The market landscape is also witnessing a wave of consolidation, highlighted by JBT Corporation's landmark USD 3.9 billion acquisition of Marel in 2025, birthing the JBT Marel Corporation, a move aimed at amplifying advanced automation capabilities. Furthermore, a burgeoning consumer preference for ready-to-cook and packaged meat is amplifying the demand for advanced processing systems.

Key Report Takeaways

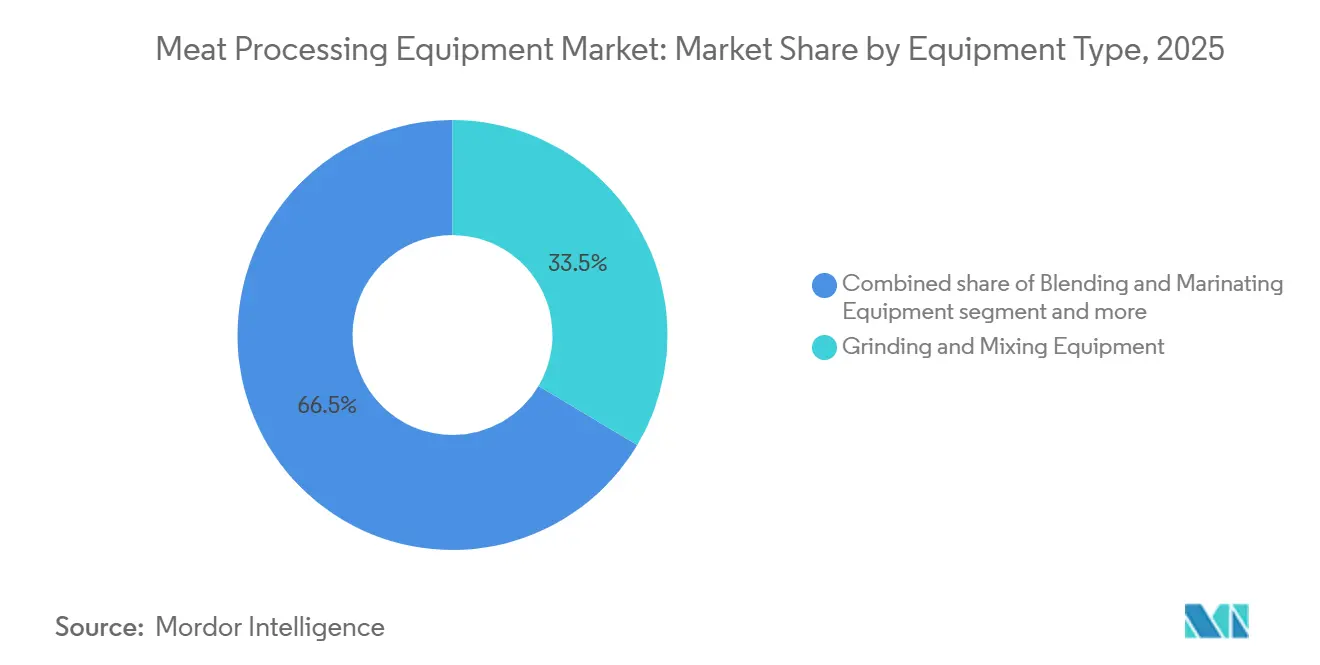

- By equipment type, grinding and mixing led with 33.54% of 2025 revenue, while cutting and slicing lines are projected to post the fastest 5.08% CAGR through 2031.

- By meat type, pork equipment held 38.69% of the 2025 meat processing equipment market share, yet poultry is forecasted to expand at a 5.67% CAGR through 2031.

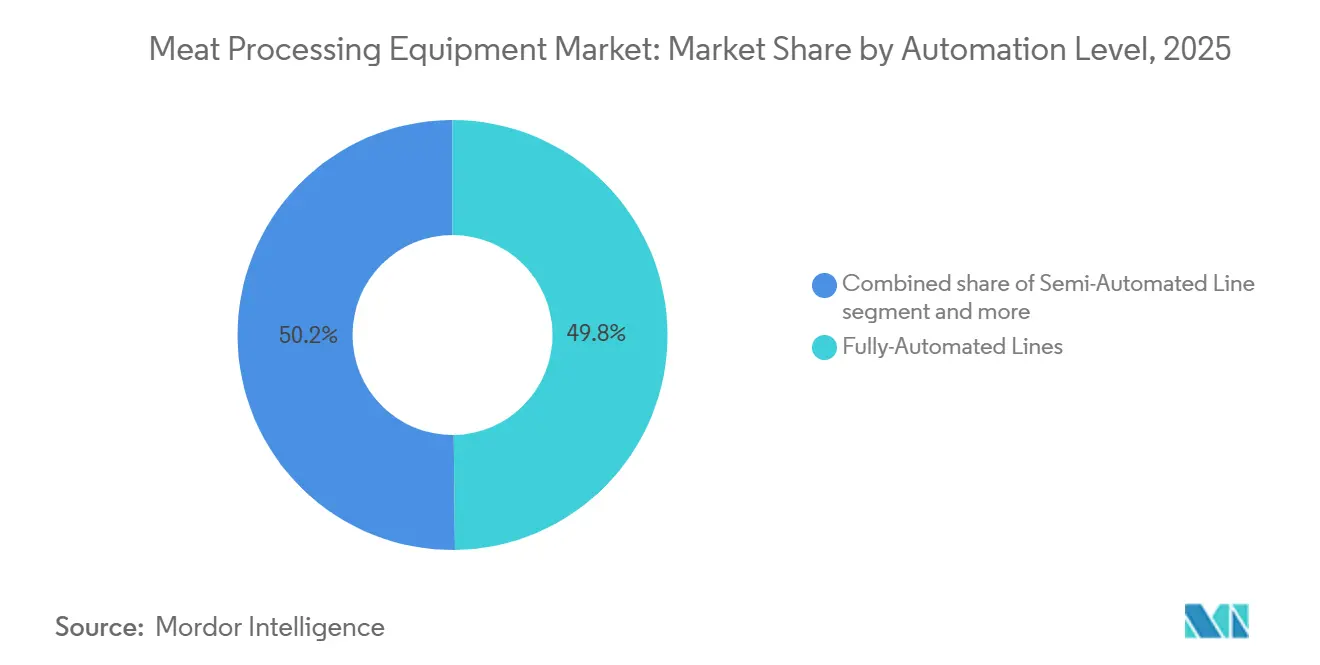

- By automation level, fully automated lines captured 49.81% of 2025 installations, and this segment is expected to advance at a 6.29% CAGR through 2031.

- By end user, industrial integrators represented 48.72% of 2025 demand, while this sector is anticipated to grow at a 5.81% CAGR through 2031.

- By geography, Asia-Pacific commanded 39.40% of 2025 revenue, and the region is predicted to grow at a 6.02% CAGR through 2031, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Meat Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor-scarce facilities turn to automation | +1.2% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Rising global meat consumption in emerging Asia | +1.0% | Asia-Pacific core (China, India, Southeast Asia), spill-over to the Middle East | Long term (≥ 4 years) |

| Stricter food-safety regulations drive equipment upgrades | +0.8% | Global, with early enforcement in North America and Europe | Short term (≤ 2 years) |

| Shift to ready-to-eat and value-added meat products | +0.7% | North America, Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| AI-enabled predictive-maintenance modules reduce downtime | +0.5% | Global, led by large integrators in North America, Europe, and Brazil | Medium term (2-4 years) |

| Decarbonization pressures are driving the CO₂-efficient thermal systems market | +0.4% | Europe (Carbon Border Adjustment Mechanism), Australia, select North American states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor-Scarce Facilities Turn to Automation

In North America and Europe, chronic workforce shortages are hastening the shift from manual tasks like deboning, trimming, and portioning to robotic cells and vision-guided cutting systems. In 2024, Delmarva Poultry Industry revealed that its member processors invested over USD 50 million in automation projects[1]Source: Delmarva Chicken Association, “Automation Investments in Delmarva Poultry Plants,” delmarvachicken.com. This move comes in response to the challenge of filling 1,000 open positions in the region, with a goal of achieving a 20% reduction in labor dependency by 2027. While poultry leads the charge, the trend is evident in beef and pork plants too. These facilities are now employing collaborative robots for repetitive tasks, such as belly scoring and primal separation, leading to improved yield consistency and fewer musculoskeletal injuries. Furthermore, automation allows processors to sustain line speeds even during seasonal labor shortages. This capability is crucial, especially when there's consistent year-round consumer demand for portion-controlled products. The momentum is building: as equipment OEMs enhance machine-learning algorithms for tasks like carcass grading and defect detection, the shortened return-on-investment timelines are enticing mid-tier processors to join the automation movement, standing shoulder to shoulder with larger integrators.

Rising Global Meat Consumption in Emerging Asia

Since 1990, meat consumption in Asia has surged, now averaging about 98 pounds per person annually. However, this figure still lags behind North American and European levels, indicating significant growth potential. In 2026, China's per-capita beef consumption dipped by 5% as consumers, facing economic challenges, gravitated towards more affordable pork and poultry. This shift not only boosted activity at poultry and pork processing plants but also heightened the demand for advanced equipment like high-speed evisceration lines, automated cut-up systems, and inline weighing tools. India's poultry industry is witnessing rapid growth, buoyed by increasing incomes and urban migration. Meanwhile, countries in Southeast Asia, including Thailand, Indonesia, and Vietnam, are modernizing their older slaughter facilities. This upgrade aims to align with export certification standards set by Japan, the Middle East, and the European Union. Such regional advancements are advantageous for equipment suppliers offering comprehensive solutions, including integrated cold-chain logistics, traceability software, and halal-compliant processing. As a result, the Asia-Pacific region is on track to be the fastest-growing area, boasting a projected CAGR of 6.02% through 2031.

Stricter Food-Safety Regulations Drive Equipment Upgrades

Regulatory agencies are tightening pathogen-control requirements, pushing processors to invest in equipment that mitigates contamination risks and bolsters traceability. In December 2024, the USDA Food Safety and Inspection Service rolled out updated measures for controlling Listeria monocytogenes. These measures, aimed at ready-to-eat meat facilities, often require the installation of enclosed cutting rooms equipped with positive-pressure ventilation and automated sanitation systems[2]Source: USDA Food Safety and Inspection Service, “New Listeria Control Measures,” fsis.usda.gov. In January 2025, FSIS unveiled a line-speed study, highlighting that plants utilizing vision-based inspections and automated trimming can safely boost their throughput without jeopardizing food safety. This effectively rewards their capital investments with heightened capacity. Meanwhile, the European Union is set to revise hygiene regulations, likely imposing stricter limits on retained water in poultry. This move is anticipated to spur demand for advanced chilling and air-drying equipment that not only meets the new thresholds but also maintains yield. Additionally, adherence to ISO 22000 and HACCP certifications is motivating processors to upgrade from aging equipment to modern lines. These new systems, boasting features like built-in data logging and real-time alerts, significantly diminish the chances of expensive recalls and export halts.

AI-Enabled Predictive-Maintenance Modules Reduce Downtime

Large processors are increasingly adopting AI-driven predictive maintenance, moving beyond pilot projects. They understand the stakes: unplanned downtimes can lead to losses of tens of thousands of dollars per hour, impacting both throughput and inventory. Marel's Innova software, a dominant player in the field, is already making waves. Installed in over 6,000 facilities worldwide, it oversees 30% of global poultry processing. Leveraging sensor data and machine-learning, Innova predicts issues like bearing failures and hydraulic leaks days in advance, preventing costly line stoppages. A 2024 study in Nature highlighted the prowess of AI in Chinese pork plants. With AI-driven vision systems, these plants slashed defect rates by 18% and enhanced carcass grading. This precision allowed them to optimize cut allocations and secure premium prices for export-grade primals. Equipment OEMs are not lagging. They're integrating IoT modules and edge-computing gateways into their new installations. This integration facilitates real-time monitoring of motor vibrations, temperatures, and energy consumption. The insights gathered are channeled into cloud-based analytics. These platforms don't just analyze; they recommend maintenance schedules, spare parts orders, and process tweaks. The result? A shift from reactive service calls to proactive, scheduled interventions, minimizing disruptions and prolonging asset life.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Outlay and Lengthy ROI | -0.6% | Global, acute for small and mid-tier processors | Short term (≤ 2 years) |

| Volatile Livestock Supply and Disease Outbreaks | -0.5% | Global, with acute episodes in North America (HPAI), Asia (ASF) | Short term (≤ 2 years) |

| Trade-Policy Uncertainty on Meat Exports | -0.4% | Export-oriented regions: Brazil, Australia, the EU, select U.S. states | Medium term (2-4 years) |

| Limited Skilled Operators for Smart Machinery | -0.3% | North America, Europe, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Outlay and Lengthy ROI

Investing in advanced processing equipment demands a hefty upfront cost, often deterring smaller and mid-tier processors who operate on tight margins. For instance, installing a spray chiller at a beef plant comes with a USD 2 million price tag, yet it can yield an impressive USD 5 million annually by enhancing yield and minimizing shrinkage. On the other hand, a thermal-management system, costing USD 5 million, promises annual energy savings of USD 2.2 million, translating to a payback period of just 2.3 years, as reported by the Wiley Online Library. Yet, processors lacking access to affordable financing or grappling with uncertain demand often sideline such ambitious projects. Instead, they lean towards incremental upgrades, prolonging the lifespan of their existing equipment. Highlighting the financial intricacies, the Utah State University Meat Processing Center crafted a financial-analysis tool tailored for smaller plants, specifically those processing under 750 heads annually. Their findings underscore the sensitivity of 20-year net-present-value calculations to variables like throughput growth, labor-cost inflation, and equipment residual value. This capital-intensive landscape has led to a divided market: while large integrators, buoyed by robust balance sheets and private-equity support, chase aggressive automation strategies, smaller operators find it challenging to justify investments that risk obsolescence before achieving break-even.

Volatile Livestock Supply and Disease Outbreaks

Processors are idling capacity and postponing equipment orders due to disruptions in livestock availability caused by African swine fever (ASF) and highly pathogenic avian influenza (HPAI). Over the last four years, ASF has led to the loss of 2.4 million pigs worldwide. In a bid to contain the disease, China has cut its sow herd by about 1 million head, which is roughly 2.5% of the national total. A study from Frontiers in Veterinary Science highlighted the potential fallout: a significant ASF outbreak in the U.S. could lead to welfare losses between USD 10.9 billion and USD 11.4 billion. Such a scenario would ripple through the equipment supply chain, causing processors to delay expansion projects and original equipment manufacturers (OEMs) to face order cancellations. In December 2025, HPAI outbreaks led to the culling of 6.4 million poultry worldwide, with the World Organization for Animal Health reporting 169 commercial outbreaks and 608 detections in wild birds[3]Source: World Organisation for Animal Health, “ASF & HPAI Situation Update,” woah.org. Brazil's first commercial case of HPAI in May 2025 prompted immediate trade bans from major export markets, highlighting the delicate nature of supply chains that influence equipment investment decisions, as noted by the USDA Foreign Agricultural Service. These disease outbreaks introduce volatility in capacity-utilization rates, complicating order forecasts for equipment suppliers and hindering processors' commitments to long-term capital plans.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Grinding Dominance Meets Cutting Innovation

In 2025, grinding and mixing equipment claimed a dominant 33.54% market share, underscoring its crucial role in processed meat production. These systems play a vital role in producing global staples such as sausages, patties, and ground meats. Their versatility across different meat types and scalability make them indispensable for both large processors and smaller niche players. Noteworthy innovations, like Air Products’ LIN-IS liquid nitrogen injection system, highlight strides in grinding efficiency and hygiene, ensuring optimal low temperatures during the mixing and grinding processes.

On the other hand, cutting and slicing equipment is emerging as the fastest-growing segment, with a projected CAGR of 5.08% extending to 2031. The increasing demand for portion-controlled and value-added meat products fuels this surge. The industry is leaning towards precision cutting technologies to ensure uniformity, reduce waste, and meet retail presentation standards. For example, Marel’s AI-driven cutting systems harness vision and machine learning to enhance speed and accuracy. Meanwhile, blending and marinating machines are in demand due to the booming ready-to-cook segment, while tenderizing, massaging, smoking, and curing systems cater to premium and regional product niches.

By Meat Type: Pork Leadership Challenged by Poultry Surge

In 2025, pork processing equipment secured a commanding 38.69% market share, reinforcing pork's position as the globe's most consumed meat. The diverse range of pork products, from fresh cuts to bacon and sausages, demands specialized equipment, cementing its role in both industrial and regional processing facilities. However, this dominance grapples with challenges posed by shifting consumption trends favoring leaner proteins and sustainability.

Poultry processing equipment is rapidly gaining traction, with forecasts suggesting a 5.67% CAGR through 2031. This surge is driven by rising health awareness, lower production costs, and poultry's reduced environmental impact. Innovations, such as BAADER’s ProFlex cut-up solution, boasting the ability to process 7,500 birds per hour with anatomical precision, underscore the segment's rapid evolution. While beef processing equipment sees consistent demand in developed markets, emerging markets are displaying a growing appetite. Mutton processing, albeit niche, holds profound cultural significance in areas like South Asia and the Middle East. The distinct processing needs of each meat type are propelling both equipment innovation and market growth.

By Automation Level: Full Automation Drives Industry Transformation

In 2025, fully-automated lines capture a 49.81% market share and are rapidly gaining ground, with a projected CAGR of 6.29% through 2031. This trajectory signals a major shift in meat processing. Faced with ongoing labor shortages and a steadfast demand for uniformity, processors are leaning more towards technologies that minimize manual tasks. Take, for instance, Meyn’s Rapid Plus M4.2 breast deboner, which can save up to 34 full-time equivalents in a single shift. These innovations not only boost productivity but also reduce reliance on human labor.

Semi-automated systems are essential for mid-sized processors, striking a balance between automation and flexibility. They enable human oversight for complex tasks while optimizing repetitive ones, making them ideal for diverse product lines. Although the prevalence of manual and hand-guided systems is waning, they still serve craft, specialty, and low-volume operations where full automation isn't economically viable. As automation technology becomes more accessible and cost-effective, even those historically dependent on manual methods are exploring hybrid systems.

By End User: Industrial Scale Drives Market Leadership

In 2025, the industrial segment captures 48.72% of the market share and is projected to grow at a 5.81% CAGR through 2031. This growth underscores the dominance of large-scale facilities that serve both national and global supply chains. These facilities prioritize high-throughput, precision, and automation, aiming to reduce labor reliance and ensure consistent quality. Equipment in this sector must adeptly handle various proteins and product formats, emphasizing rapid changeover capabilities. A testament to this trend is JBS’s USD 200 million investment in its Italian meat plant, which boasts auto-guided vehicles and fully automated production lines.

Craft butcheries, traditionally grounded in craftsmanship and local sourcing, now grapple with intensifying competition and evolving retail landscapes. They lean towards user-friendly, adaptable equipment rather than heavy-duty industrial systems. An example is Ross Industries’ AMS 400 Membrane Skinner, designed specifically for medium and craft processors. The HoReCa (Hotels, Restaurants, and Catering) sector seeks compact, multifunctional equipment, ideal for limited spaces and dynamic menu adjustments. While this segment operates on a smaller scale, it drives a significant demand for versatile and efficient equipment design, particularly in urban and upscale dining establishments.

Geography Analysis

In 2025, Asia-Pacific dominates the market with a 39.40% share and leads in growth, boasting a 6.02% CAGR projected through 2031. This highlights the region's pivotal role in the global meat processing equipment arena. Countries like China and India are modernizing their meat processing infrastructure, driven by rapid urbanization, surging protein demand, and significant government investments. China is pushing for automation in beef processing, championing intelligent farming initiatives. Meanwhile, India's INR 15,000 crore (USD 1,550 million) infrastructure fund is focused on facility development, aiming to uplift its currently modest meat processing rates.

North America and Europe, though not the quickest to grow, play a crucial role in the market. Their emphasis on food safety, regulatory adherence, and technological advancements keeps them at the forefront. Demand for automation and equipment upgrades is steady in these regions. Compliance mandates, such as the U.S. FSMA 204 traceability requirements, are compelling processors to update their legacy systems. While market saturation poses challenges for rapid growth, there's a notable investment trend towards premium, high-efficiency systems, especially from industrial processors aiming for better yields and reduced labor.

South America and the Middle East and Africa are witnessing gradual growth, fueled by rising domestic meat consumption and slight enhancements in processing capacity. Yet, challenges like currency fluctuations, import tariffs, and restricted capital access often stall equipment upgrades. In Brazil and Gulf nations, meat production driven by exports and food security initiatives bolsters market growth.

Competitive Landscape

The meat processing equipment market is moderately consolidated, and companies are honing their strategies, emphasizing value differentiation. Industry leaders are rolling out bespoke solutions tailored to the unique demands of processors. For instance, they offer high-throughput systems for industrial clients and adaptable machinery for mid-sized operations. While Meyn and BAADER spotlight their prowess in poultry processing automation, Frontmatec touts its expertise in hygienic designs and custom-built lines. To bolster visibility and engagement, companies are turning to digital campaigns, virtual equipment showcases, and active participation in global trade fairs.

In this industry, technology adoption stands as the bedrock of competitive advantage. Companies are channeling their efforts into innovations that enhance efficiency, curtail waste, and bolster traceability. A case in point: Marel’s collaboration with E+V Technology has fortified its vision systems, ensuring precise portioning and inspection. Leading manufacturers now prominently feature robotics, AI-driven sorting, automated deboning, and predictive maintenance software in their offerings.

In a bid to cement their market dominance, companies are increasingly turning to mergers, acquisitions, and strategic expansions. A standout move was JBT Corporation’s USD 3.9 billion takeover of Marel in January 2025, birthing the industry behemoth, JBT Marel Corporation. This acquisition underscores a prevailing trend of consolidation, with firms seeking to meld technical strengths and broaden their global reach. In a parallel move, Fortifi bolstered its automation prowess by bringing LIMA and MHM Automation into its fold, allowing it to straddle diverse protein sectors.

Meat Processing Equipment Industry Leaders

Marel hf.

GEA Group AG

JBT Corporation

Illinois Tool Works Inc.

The Middleby Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Brazil's Frigol announced agreements with DistriBoi and RioBeef to increase annual cattle slaughter capacity from approximately 650,000 head in 2025 to more than 1,000,000 head in 2026, a 60% expansion, with two plants approved for exports to China and one enabling U.S. market access, financed partly by a BRL 250 million agribusiness receivables certificate.

- March 2026: JBS announced capital expenditures of USD 2.4 billion for 2026, with approximately USD 1.4 billion allocated to expansion projects, including Pilgrim's Pride plants in the United States, pork facilities in Iowa, beef facilities in Cactus, Texas, a new plant in Paraguay, and an integrated poultry, beef, and lamb processing project in Oman.

- February 2026: Smithfield Foods announced plans to build a new USD 1.3 billion packaged-meat and fresh-pork processing facility in Sioux Falls, South Dakota, described as "the most modern of its kind in the U.S.," featuring advanced automation technology, with site work slated to begin spring 2026, initial groundbreaking anticipated H1 2027, and production expected by the end of 2028.

Global Meat Processing Equipment Market Report Scope

Meat processing equipment refers to specialized industrial or commercial machinery designed to handle, transform, and prepare raw meat into consumable products through cutting, grinding, mixing, blending, and other structural modifications. The global meat processing equipment market is segmented by equipment type, meat type, automation level, end user, and geography. By Equipment type, the market is segmented into cutting and slicing equipment, grinding and mixing equipment, blending and marinating equipment, tenderizing and massaging equipment, smoking and curing chambers, and others. By Meat Type, the market is segmented into pork, beef, poultry, and mutton. By automation level, the market is segmented into fully-automated lines, semi-automated lines, and manual/hand-guided equipment. By end user, the market is segmented into industrial, butcheries, and HoReCa. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Cutting and Slicing Equipment |

| Grinding and Mixing Equipment |

| Blending and Marinating Equipment |

| Tenderizing and Massaging Equipment |

| Smoking and Curing Chambers |

| Others |

| Pork |

| Beef |

| Poultry |

| Mutton |

| Fully-Automated Lines |

| Semi-Automated Lines |

| Manual/Hand-Guided Equipment |

| Industrial |

| Butcheries |

| HoReCa |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Equipment Type | Cutting and Slicing Equipment | |

| Grinding and Mixing Equipment | ||

| Blending and Marinating Equipment | ||

| Tenderizing and Massaging Equipment | ||

| Smoking and Curing Chambers | ||

| Others | ||

| Meat Type | Pork | |

| Beef | ||

| Poultry | ||

| Mutton | ||

| Automation Level | Fully-Automated Lines | |

| Semi-Automated Lines | ||

| Manual/Hand-Guided Equipment | ||

| End User | Industrial | |

| Butcheries | ||

| HoReCa | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the meat processing equipment market, and where is it headed?

The segment was valued at USD 9.90 billion in 2026 and is forecast to reach USD 12.60 billion by 2031, reflecting a 4.94% CAGR over 2026-2031.

Which geography is expanding the fastest for equipment suppliers?

Asia-Pacific leads global growth with a projected 6.02% CAGR through 2031, driven by plant upgrades in China, India, and Southeast Asia.

Why are processors accelerating automation projects right now?

Tight labor markets in North America and Europe, coupled with falling robot prices and stronger ROI models, make fully automated lines attractive for yield, safety, and uptime gains.

How are new food-safety rules influencing capital spending?

Stricter pathogen-control standards in the United States and the European Union are pushing plants to install enclosed, clean-in-place equipment that supports higher line speeds while meeting audit requirements.

Page last updated on: