Cheese Ingredients Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

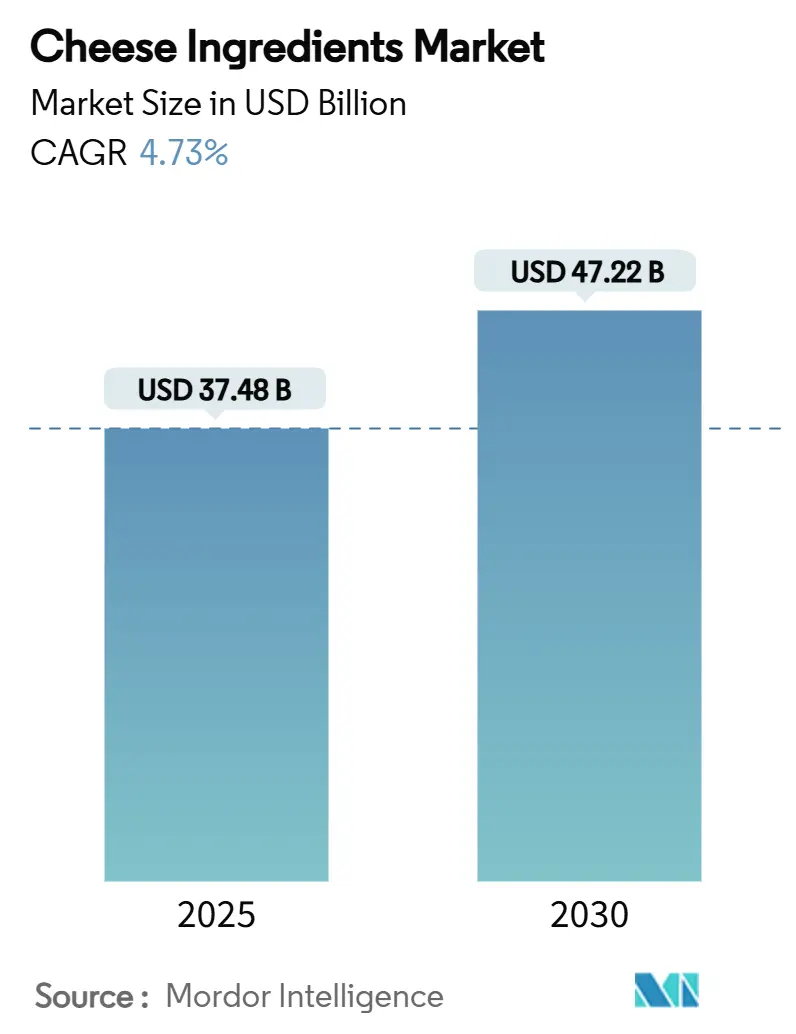

| Market Size (2025) | USD 37.48 Billion |

| Market Size (2030) | USD 47.22 Billion |

| Growth Rate (2025 - 2030) | 4.73% CAGR |

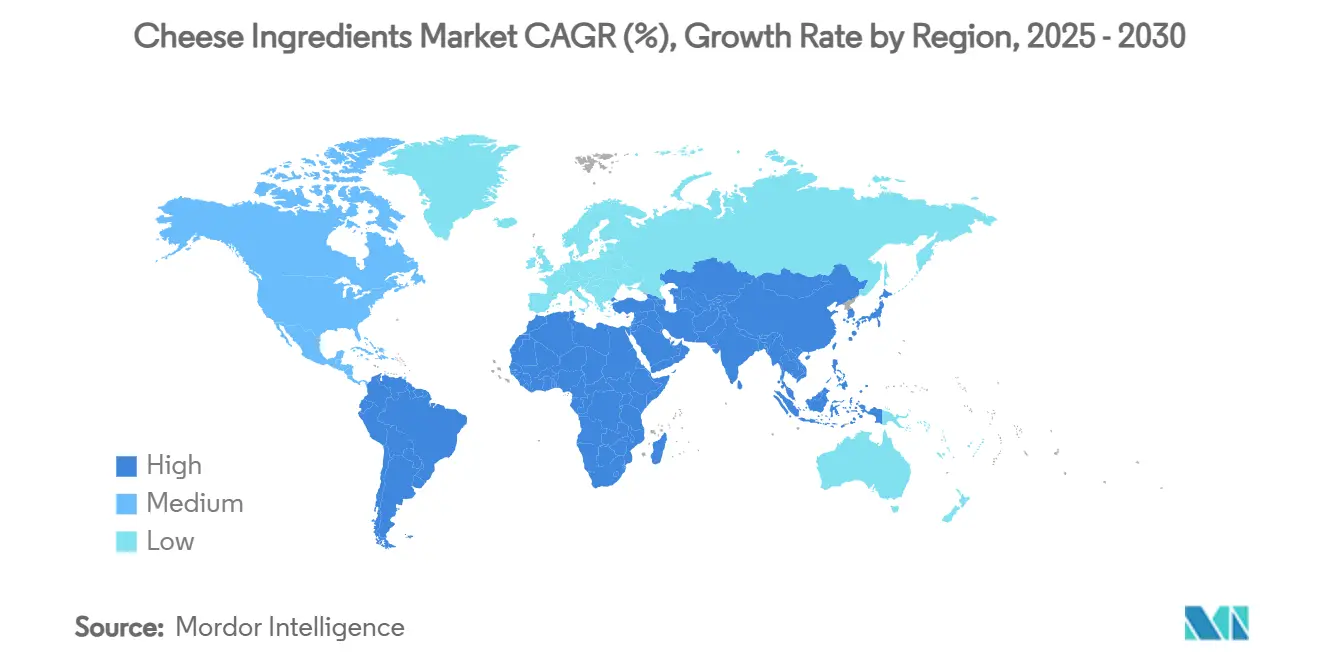

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

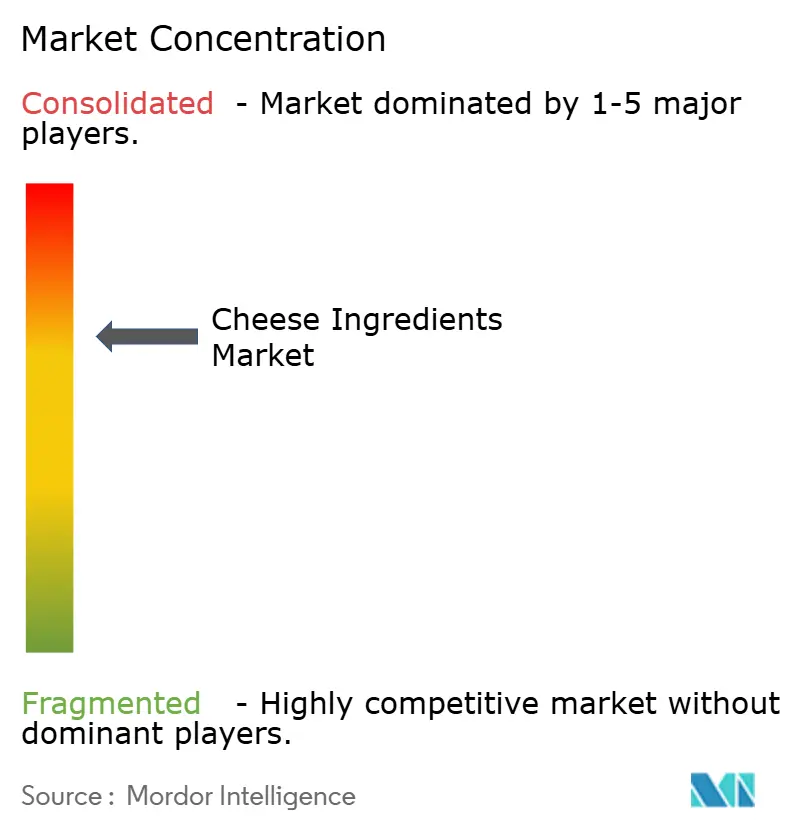

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cheese Ingredients Market Analysis by Mordor Intelligence

The cheese ingredients market size reached USD 37.48 billion in 2025 and is projected to rise to USD 47.22 billion by 2030, advancing at a 4.73% CAGR. This market size expansion reflects the ingredient sector’s resilience as cheese remains a staple in packaged foods, food-service menus, and emerging hybrid formulations. European leadership, ongoing investments in precision fermentation, and the rapid uptake of plant-based compositions all underpin sustained demand. Ingredient suppliers benefit from regulatory flexibility in North America[1]Food and Drug Administration. "Cheese Products Deviating From Standard of Identity; Temporary Permit for Market Testing." 2025, www.federalregister.gov, premiumization trends in Europe, and soaring protein needs across Asia-Pacific. Competitive strategies now emphasize clean-label reformulation, strategic partnerships with biotech start-ups, and vertical integration that protects raw-material access and quality.

Key Report Takeaways

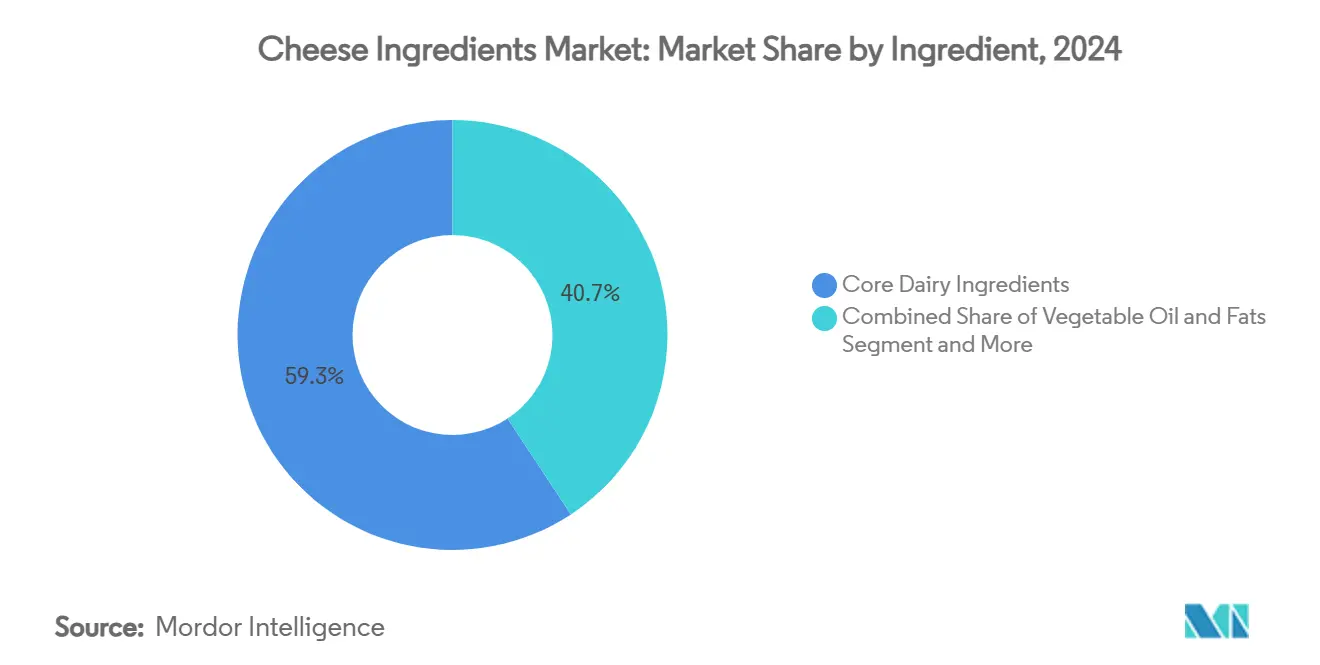

- By ingredient type, core dairy inputs captured 59.28% of the cheese ingredients market share in 2024, while specialty cultures and molds are expected to grow at an 8.47% CAGR to 2030.

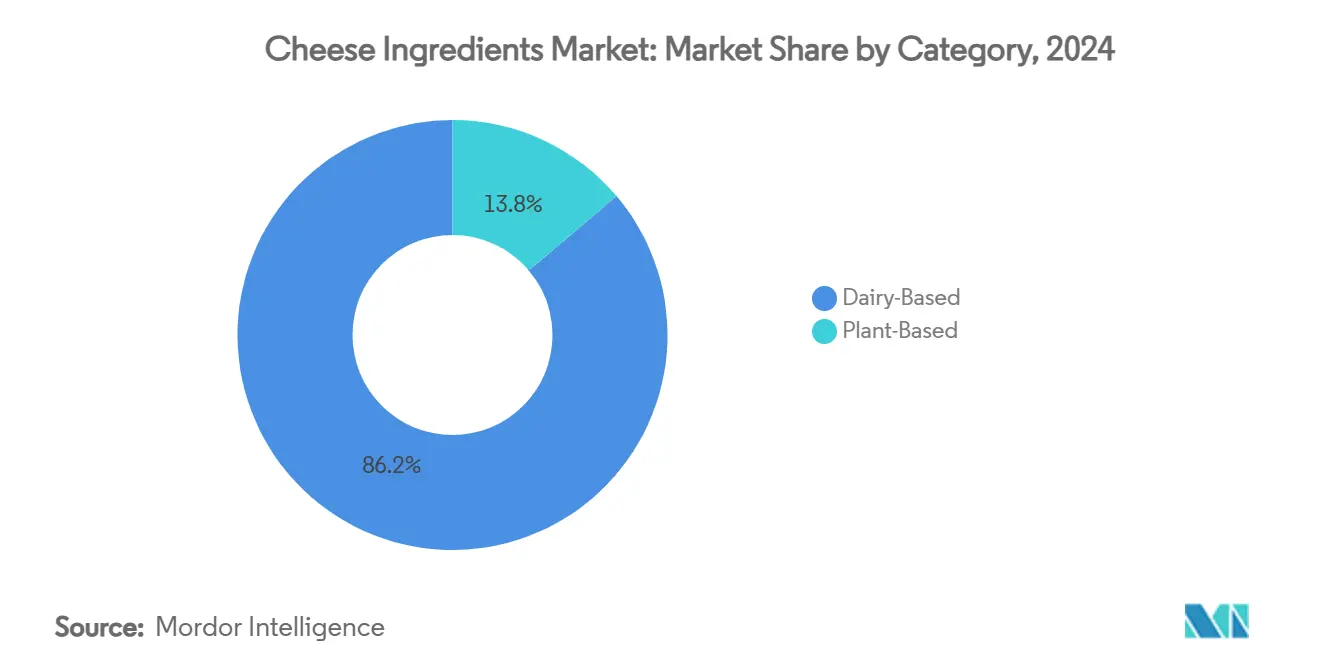

- By category, dairy-based ingredients accounted for 86.18% of the cheese ingredients market size in 2024; plant-based alternatives are advancing at a 10.18% CAGR between 2025 and 2030.

- By geography, Europe led with 30.28% of the cheese ingredients market share in 2024, whereas Asia-Pacific is forecast to expand at an 8.19% CAGR through 2030.

Global Cheese Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for plant-based and clean label products | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Technological advances in precision fermentation | +0.8% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Growing health consciousness and protein demand | +1.0% | Global, particularly strong in APAC | Short term (≤ 2 years) |

| Regulatory support for ingredient innovation | +0.5% | North America & Europe | Medium term (2-4 years) |

| Increasing cheese consumption in emerging markets | +0.9% | APAC, Latin America, MEA | Medium term (2-4 years) |

| Innovation in specialty cultures and functional ingredients | +0.6% | Global, led by Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Plant-Based and Clean Label Products

As consumers increasingly prefer products with recognizable, natural ingredients, cheese manufacturers are reformulating their offerings to include clean-label alternatives. Health Canada's endorsement of cellulose and microcrystalline cellulose as anticaking agents in plant-based cheese underscores a regulatory nod to the market's demand for natural additives. In 2024, plant-based cheese alternatives saw notable sales surges, signaling a shift towards mainstream acceptance, transcending traditional vegan circles. Research from the University of Göttingen highlighted that when German consumers are educated about the environmental perks[2]University of Göttingen. "Cheese of the future: Consumers open to animal-free alternatives." ScienceDaily, 2025, www.sciencedaily.com, they're more receptive to precision-fermented cheese alternatives, pointing to the potential of targeted educational campaigns. This movement isn't limited to direct consumption; food manufacturers are actively pursuing plant-based ingredients that not only uphold functional properties but also align with sustainability goals.

Technological Advances in Precision Fermentation

Precision fermentation technology is revolutionizing the production of dairy-identical proteins, eliminating the need for animal agriculture and disrupting conventional ingredient supply chains. For instance, DairyX has harnessed precision fermentation to produce casein micelles, crafting proteins that not only self-assemble but also mimic traditional dairy functions[3]Food Manufacturing staff. "DairyX Crafts Cow-Free, High-Protein Cheese." Food Manufacturing, 2024, www.foodmanufacturing.com, all while minimizing environmental harm. Furthermore, Standing Ovation's collaboration with Tetra Pak to boost the industrial production of alternative caseins underscores the technology's commercial promise and its potential for widespread acceptance. Tackling cost parity hurdles, precision fermentation proteins are nearing price competitiveness with their traditional dairy counterparts, positioning them as feasible alternatives for large-scale food production. Additionally, with several firms seeking GRAS determinations from the FDA, regulatory approvals are fast-tracking market entry, signaling imminent commercial availability.

Growing Health Consciousness and Protein Demand

As global protein consumption surges, especially in Asia-Pacific markets, there's a heightened demand for high-protein cheese ingredients, prized for their muscle health benefits and ability to promote satiety. The California Milk Advisory Board highlights a notable uptick in Asia's appetite for protein-rich dairy. Asian consumers are increasingly weaving cheese into their traditional diets, enhancing nutritional value. In the U.S., exports of higher-protein whey products are outpacing their lower-protein counterparts. This trend underscores manufacturers' pivot towards premium, nutritionally dense ingredients that yield better margins. Cottage cheese, with its high protein content and adaptability in both sweet and savory dishes, saw a robust 15% growth in 2025. This momentum isn't just limited to cottage cheese; food manufacturers are actively seeking protein-enriched cheese components, targeting categories like sports nutrition, functional foods, and healthy snacking.

Regulatory Support for Ingredient Innovation

Government agencies are increasingly adopting flexible regulatory frameworks, paving the way for the testing and commercialization of innovative cheese ingredients. A case in point is the FDA's recent extension of temporary permits to Bongards' Creameries, allowing them to market-test cheese products using extra virgin olive oil as an anti-sticking agent. This move underscores the regulatory body's openness to ingredient innovation. Meanwhile, Japan's Consumer Affairs Agency has rolled out new governance rules mandating comprehensive documentation for non-milk ingredients. These rules, especially the specific safety requirements for probiotic ingredients, delineate a clear path for approving innovative ingredients. In another significant move, the FDA has proposed revoking 18 identity standards for dairy products. This step is aimed at trimming redundant regulatory requirements, which could, in turn, hasten innovation in cheese ingredient formulations. Collectively, these regulatory shifts create a conducive environment for ingredient suppliers, empowering them to introduce novel solutions that cater to the ever-evolving demands of consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain disruptions and raw material cost volatility | -0.9% | Global, particularly affecting Europe & North America | Short term (≤ 2 years) |

| Complex food safety and quality standards | -0.2% | Global, particularly stringent in developed markets | Short term (2 years) |

| Environmental concerns and sustainability pressures | -0.3% | Global, strongest in Europe | Long term (≥ 4 years) |

| Competition from alternative protein sources | -0.5% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Disruptions and Raw Material Cost Volatility

Global dairy markets grapple with ongoing supply chain challenges. These challenges stem from disease outbreaks, climate impacts, and geopolitical tensions, leading to volatile ingredient costs and constraints on availability. The dairy sector feels the pinch from the Highly Pathogenic Avian Influenza, which not only hampers milk production but also tightens heifer supplies. This creates upstream challenges for cheese ingredient manufacturers. In 2025, European cheese prices saw a year-over-year surge of 10-12%. These price hikes are a direct consequence of reduced milk production, driven by profitability concerns and disease-related setbacks. Climate change casts a shadow over cheese production, with altered precipitation patterns, temperature swings, and extreme weather events jeopardizing both the supply and quality of milk. Such disruptions compel manufacturers to hold larger inventory levels, broaden their supplier bases, and craft contingency sourcing strategies, all of which amplify operational complexity and costs.

Environmental Concerns and Sustainability Pressures

Growing environmental awareness and regulatory pressure create challenges for traditional dairy ingredient suppliers while creating opportunities for sustainable alternatives. The dairy industry faces scrutiny over greenhouse gas emissions, water usage, and land use impacts, with livestock agriculture contributing 14.5% of global emissions. Companies like Savor develop lab-made alternatives with significantly lower carbon footprints (less than 0.8g CO2 equivalent per calorie) compared to traditional dairy products (approximately 2.4g CO2 equivalent per calorie), creating competitive pressure for conventional suppliers. Sustainability reporting requirements and corporate environmental commitments force ingredient suppliers to invest in cleaner production technologies, renewable energy, and waste reduction initiatives that increase operational costs. Consumer demand for sustainable packaging and reduced environmental impact creates additional compliance requirements and reformulation challenges for ingredient suppliers serving environmentally conscious markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient: Core Dairy Ingredients Dominate Amid Specialty Innovation

In 2024, core dairy ingredients secured a dominant 59.28% share of the market, underscoring their pivotal role in traditional cheese production and the robustness of the existing supply chain. Essential components like milk, cream, milk powder, and whey are favored for their functional properties, nutritional benefits, and cost efficiency in large-scale manufacturing. This segment is reaping the rewards of technological advancements in membrane processing. Techniques such as ultrafiltration and microfiltration are standardizing protein and fat content, leading to improved cheese yield and consistency. Yet, challenges loom: supply chain disruptions from disease outbreaks and climate events introduce volatility in the availability and pricing of raw materials. In response, manufacturers are pivoting towards more resilient sourcing strategies.

Specialty cultures and molds are emerging as the fastest-growing ingredient segment, boasting an impressive 8.47% CAGR from 2025 to 2030. This surge is largely fueled by consumers' growing appetite for complex flavors, artisanal products, and added functional benefits. In cheese production, the use of protective cultures not only bolsters bio-preservation but also offers clean-label alternatives to synthetic preservatives. Furthermore, breakthroughs in genomics and proteomics are paving the way for adjunct microorganisms that not only elevate flavor profiles but also hasten ripening. This innovation empowers manufacturers to roll out distinct products in shorter timeframes. While coagulating agents like rennet and citric acid enjoy consistent demand, texture modifiers such as emulsifying salts, starch, and hydrocolloids are witnessing a surge, especially in processed cheese and plant-based alternatives that seek functional ingredient solutions.

By Category: Plant-Based Surge Challenges Dairy Dominance

In 2024, the dairy-based category commands a dominant 86.18% market share, bolstered by entrenched consumer preferences, enhanced functional attributes, and a vast distribution network spanning both foodservice and retail channels. Traditional dairy ingredients, having undergone decades of refinement in cheese manufacturing, enjoy regulatory endorsements and optimized cost structures, granting them a competitive edge over alternatives. Demonstrating unwavering confidence in the long-term demand for dairy, major dairy corporations have poured over USD 8 billion into processing infrastructure expansions, predominantly in the US. Riding the wave of the protein trend, dairy-derived ingredients, especially high-protein whey, not only fetch premium prices but also play a pivotal role in stabilizing milk prices.

Plant-based cheese ingredients are on an upward trajectory, projected to grow at a 10.18% CAGR from 2025 to 2030. This surge is driven by a growing consumer appetite for sustainable and ethical alternatives that closely mimic the functionality of traditional cheese. Innovatively, companies like NewMoo are harnessing plant molecular farming techniques, cultivating casein proteins in soy plants. This breakthrough yields a liquid casein that not only mirrors the properties of dairy milk but also integrates effortlessly into current manufacturing workflows. Meanwhile, the vegan cheese sector is witnessing advancements, with innovations in legume-based proteins and cutting-edge fermentation techniques enhancing both texture and flavor. Furthermore, hybrid cheese formulations, which blend both dairy and plant-based components, strike a balance. They preserve familiar taste profiles while addressing pressing sustainability concerns, thus unveiling fresh market avenues for ingredient suppliers catering to both traditional and alternative cheese producers.

Geography Analysis

Europe retained 30.28% of global revenue in 2024, propelled by centuries-old cheese craftsmanship, extensive PDO frameworks, and high per-capita consumption. Producers emphasize value-added aging techniques and natural preservation, prompting strong uptake of specialty cultures. Milk production is forecast to decline marginally while cheese output inches higher through 2030, reflecting efficiency gains and skilled allocation of milk solids toward higher-margin formats. The forthcoming ban on artificial smoke flavorings compels suppliers to develop natural extracts, potentially shifting portions of the cheese ingredients market toward botanical smoke solutions.

Asia-Pacific posts the fastest regional growth at 8.19% CAGR as rising incomes and westernized diets boost cheese inclusion in snacks, bakery, and quick-service menus. Single-serve cream cheese and flavored processed slices sell strongly in Japan, South Korea, and urban China, aided by smaller pack sizes that align with modest household dairy consumption. Stricter Japanese documentation rules for non-milk inputs raise barriers yet equally reward suppliers able to certify probiotic cultures and novel binders at high safety standards. Growing demand across Southeast Asia for cheese-infused bakery toppings and instant noodles further expands the addressable market for specialty powders, flavor bases, and stabilized cheese sauces.

North America leverages robust precision-fermentation R&D, state-level incentives for dairy processors, and high consumer familiarity with both heritage and innovative cheese formats. New US facilities scheduled through 2025 will add 360 million lb of annual cheese capacity, enlarging opportunities for microbial cultures, enzymes, and functional dairy proteins. The FDA’s progressive stance on temporary permits encourages early market testing of novel additives, cementing the region as an origin point for ingredient innovation that later diffuses worldwide.

Competitive Landscape

Market concentration is moderate-to-high as multinationals leverage scale in procurement, processing, and distribution. Vertical integration remains common: large cooperatives source raw milk, fractionate proteins, and supply finished cheese, locking in internal demand for their ingredients. Strategic alliances with biotech firms, exemplified by Leprino Foods’ exclusive deal with Fooditive Group for animal-free caseins, illustrate incumbent efforts to secure future-proof portfolios.

Consolidation persists, with Lactalis and Bega bidding for Fonterra’s Oceania assets to expand ingredient footprints and export reach. Disruptors capitalize on precision-fermentation IP and flexible pilot plants to commercialize animal-free casein, whey, and fat analogues. DairyX’s stretchable casein micelles and Those Vegan Cowboys’ recombinant milk proteins showcase scalable alternatives that could erode dairy incumbents’ cost advantages once volume ramps.

Hybrid business models also emerge, whereby dairy giants license biotech formulations to hedge climate and regulatory risks while safeguarding consumer trust. Competitive differentiation therefore hinges on advanced fermentation know-how, clean-label positioning, and reliable raw-material networks rather than solely on traditional cost leadership.

Cheese Ingredients Industry Leaders

-

Arla Foods

-

Novonesis Group

-

Lallemand Inc.

-

DSM-Firmenich

-

International Flavors & Fragrances Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Standing Ovation partnered with Tetra Pak to boost industrial production of alternative caseins via precision fermentation, marking major scaling initiative for animal-free dairy proteins

- January 2025: Lactalis invested in Tulare, California facility to significantly increase Président Feta cheese production with new 38,000 square foot manufacturing line, creating 120 jobs and enhancing specialty cheese capacity

- August 2024: Grande Cheese Company embarked on major expansion at Chilton facility with 60,000 square foot addition focusing on mozzarella production, expected completion by mid-2026

Global Cheese Ingredients Market Report Scope

| Core Dairy Ingredients | Milk |

| Cream | |

| Milk Powder | |

| Whey | |

| Coagulating Agents | Rennet |

| Citric/Lactic acid | |

| Texture Modifiers/Stabilizers | Emulsifying Salts |

| Starch | |

| Gums | |

| Hydrocolloids | |

| Flavoring Agents | Salt |

| Smoke Flavor | |

| Herbs and Spices | |

| Yeast Extracts | |

| Natural Cheese Flavor | |

| Additives and Colorants | |

| Speciality Cultures/Molds | |

| Vegetable Oils and Fats | |

| Vegan cheese ingredients |

| Dairy-based |

| Plant-Based |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Russia | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Iran | |

| Turkey | |

| Rest of Middle East and Africa |

| Ingredient | Core Dairy Ingredients | Milk |

| Cream | ||

| Milk Powder | ||

| Whey | ||

| Coagulating Agents | Rennet | |

| Citric/Lactic acid | ||

| Texture Modifiers/Stabilizers | Emulsifying Salts | |

| Starch | ||

| Gums | ||

| Hydrocolloids | ||

| Flavoring Agents | Salt | |

| Smoke Flavor | ||

| Herbs and Spices | ||

| Yeast Extracts | ||

| Natural Cheese Flavor | ||

| Additives and Colorants | ||

| Speciality Cultures/Molds | ||

| Vegetable Oils and Fats | ||

| Vegan cheese ingredients | ||

| By Category | Dairy-based | |

| Plant-Based | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Iran | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What CAGR is forecast for the cheese ingredients market between 2025 and 2030?

The sector is projected to grow at 4.73% annually, lifting revenue from USD 37.48 billion in 2025 to USD 47.22 billion by 2030.

Which region will add value fastest over the next five years?

Asia-Pacific is set to expand at an 8.19% CAGR, propelled by higher protein intake and westernized eating patterns.

Why are specialty cultures gaining traction in cheese formulations?

They deliver complex flavors and bio-protection that replace synthetic preservatives, underpinning an 8.47% CAGR for the segment.

How quickly are plant-based cheese ingredients advancing?

Plant-based alternatives are rising at a 10.18% CAGR as consumers seek sustainable options without sacrificing taste or texture.

What role does precision fermentation play in future ingredient supply?

It enables animal-free casein and whey production, securing functional parity with dairy while reducing environmental impacts.

Page last updated on: