Market Overview

| Study Period | 2021 - 2031 |

|---|---|

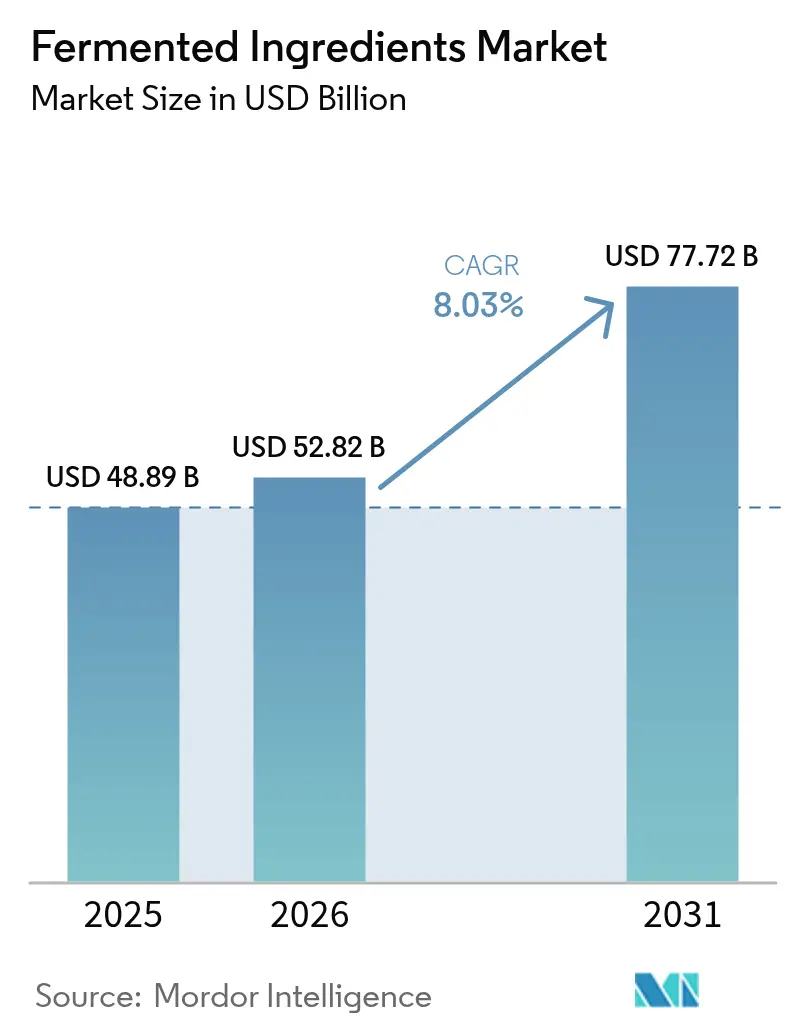

| Market Size (2026) | USD 52.82 Billion |

| Market Size (2031) | USD 77.72 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fermented Ingredients Market Analysis by Mordor Intelligence

The fermented ingredients market size was valued at USD 48.89 billion in 2025 and estimated to grow from USD 52.82 billion in 2026 to reach USD 77.72 billion by 2031, at a CAGR of 8.03% during the forecast period (2026-2031). This growth highlights a broader transition in the global food, beverage, nutraceutical, and pharmaceutical industries toward functional, natural, and bioactive ingredients that promote health, wellness, and preventive care. Increasing consumer awareness of the role of diet in managing chronic conditions, boosting immunity, and improving gut health has driven the adoption of fermented ingredients such as probiotics, postbiotics, amino acids, and enzymes. Additionally, advancements in fermentation technologies, including precision fermentation, microbial strain optimization, and enhanced bioprocessing methods, are enabling manufacturers to produce high-purity, sustainable, and specialty ingredients on a larger scale.

Key Report Takeaways

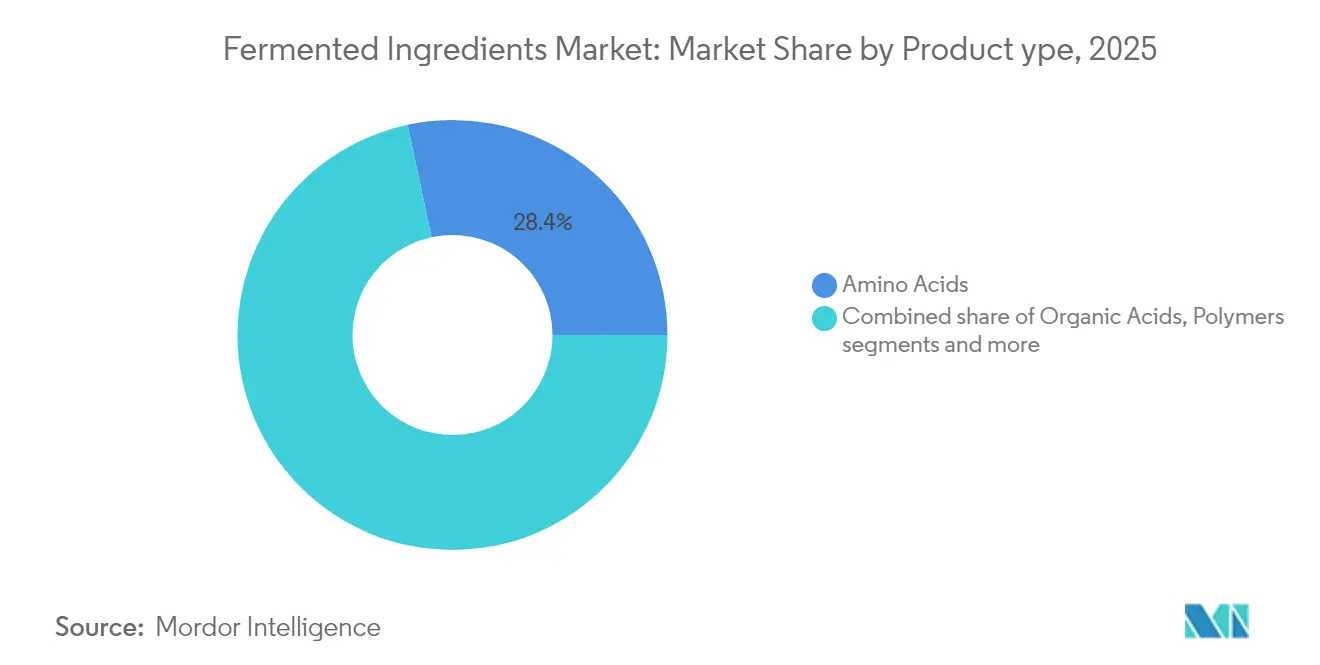

- By product type, amino acids led with 28.35% revenue share in 2025, while probiotics and postbiotics are advancing at a 8.82% CAGR to 2031.

- By form, dry formats accounted for 60.55% of the fermented ingredients market share in 2025; liquid formats are on track to expand at an 8.12% CAGR through 2031.

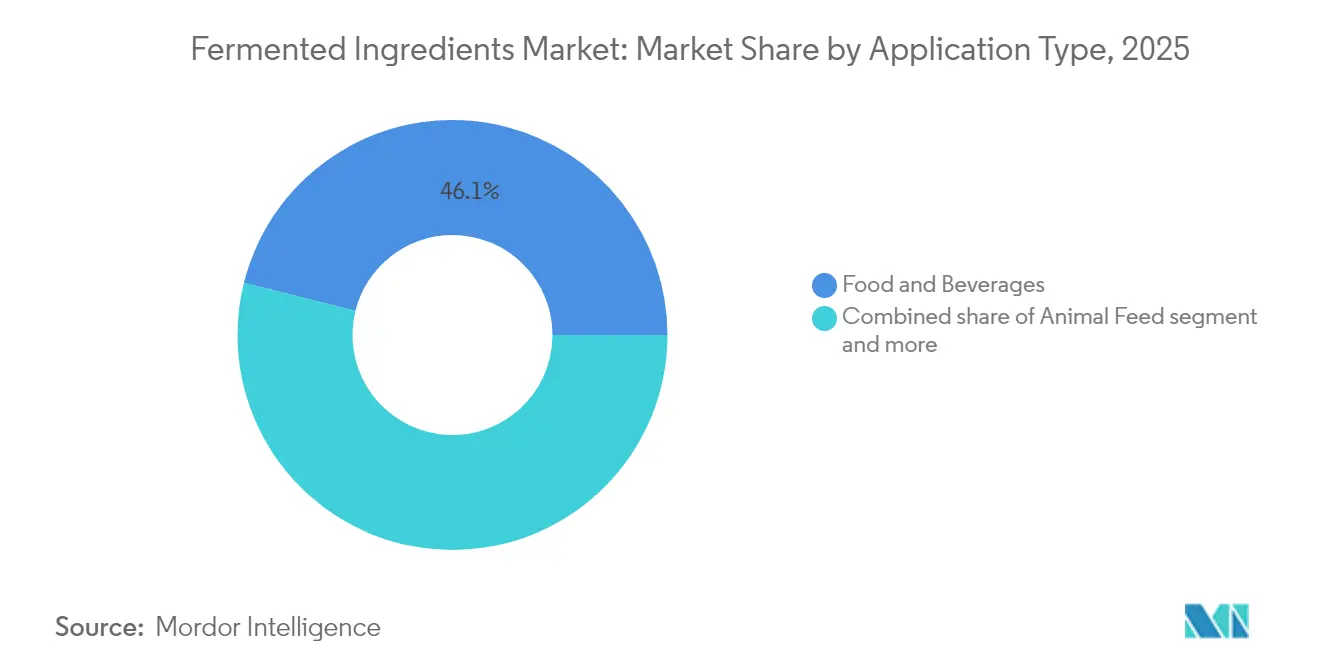

- By application, food and beverages held 46.10% of the fermented ingredients market size in 2025, and pharmaceuticals are set to post an 8.29% CAGR through 2031.

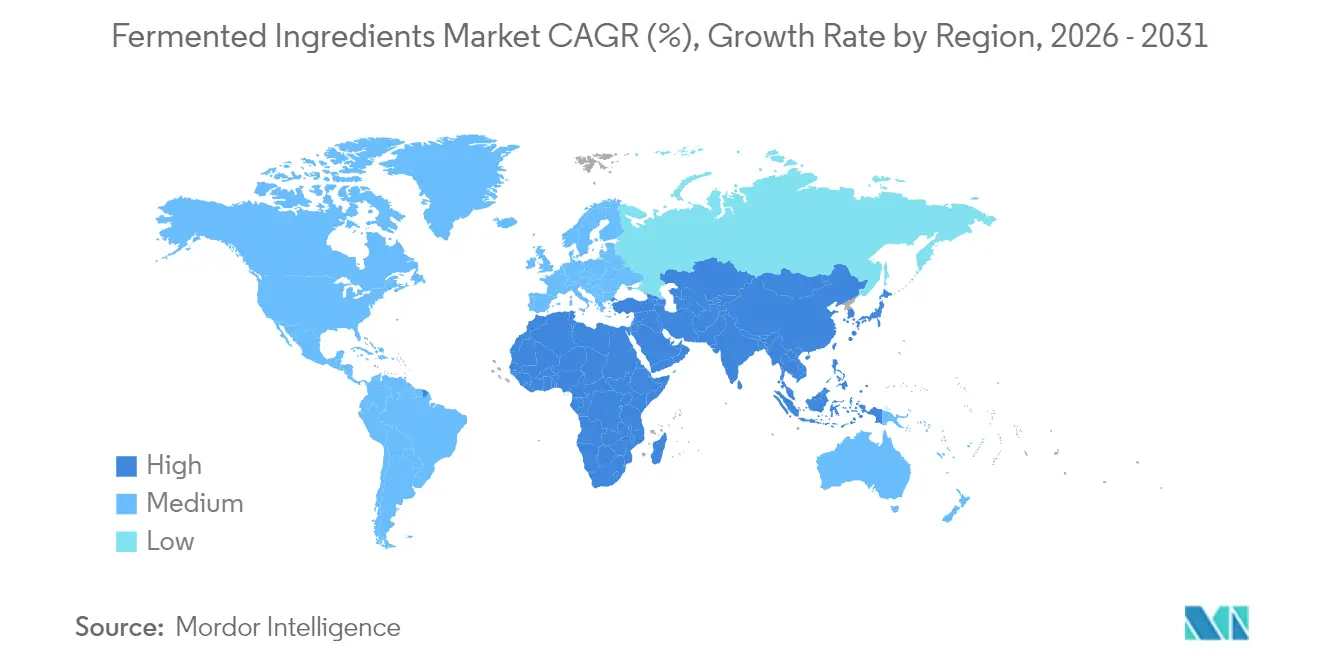

- By geography, Asia-Pacific captured a 34.20% share in 2025, and the region is forecast to grow at a 8.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fermented Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health and wellness awareness | +1.8% | Global, with strongest uptake in North America, Europe, and urban APAC | Medium term (2-4 years) |

| Expansion of plant-based diets | +1.5% | North America, Europe, and Asia-Pacific urban centers | Medium term (2-4 years) |

| Clean-label and natural product trends | +1.4% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Technological advancements in fermentation | +1.3% | Asia-Pacific core (China, India, Japan), North America | Long term (≥ 4 years) |

| Sustainability and eco-friendly production | +1.2% | Europe, North America, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Extended shelf life and natural preservation | +0.9% | Global, with emphasis in emerging markets (South America, Middle East and Africa) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising health and wellness awareness

Increasing health and wellness awareness is a key factor driving the growth of the fermented ingredients market. Consumers are increasingly seeking products that offer not only basic nutrition but also measurable health benefits. This trend has led to a significant rise in the adoption of fermented compounds, particularly probiotics and postbiotics, which are widely recognized for their benefits in supporting digestive health, immunity, and metabolic wellness. For example, Lactobacillus strains have been shown to reduce inflammatory markers in patients with metabolic syndrome, demonstrating their potential in managing chronic health conditions and improving overall well-being. The growing prevalence of lifestyle-related diseases further highlights the market potential. According to the International Diabetes Federation, approximately 11.1% of the global adult population had diabetes in 2024, with this figure projected to increase to 13% by 2050, underscoring the urgent need for preventive and functional nutrition solutions [1]Source: International Diabetes Federation, "Percentage of diabetics in the global adult population", idf.org. Consequently, consumers are increasingly turning to functional foods, beverages, supplements, and nutraceuticals enriched with fermented ingredients.

Expansion of plant‑based diets

The growth of plant-based diets is significantly influencing the market, as consumers globally adopt vegetarian, vegan, and flexitarian eating habits driven by health, ethical, and environmental considerations. Fermented ingredients are playing a crucial role in improving the nutritional value, flavor, and digestibility of plant-based foods and beverages, which often lack certain essential nutrients present in animal-derived products. Fermentation enhances protein quality, increases the bioavailability of micronutrients, and improves functional properties. Additionally, it contributes to the development of natural flavors, textures, and shelf stability, making plant-based products more appealing and nutritionally balanced. This trend is particularly evident in categories such as dairy alternatives, plant-based meat substitutes, fermented beverages, and protein-enriched snacks, where fermented ingredients offer both technological and health-related advantages. The global rise in plant-based eating, coupled with concerns about sustainability and animal welfare, has driven significant demand for fermentation technologies that produce bioactive compounds, clean-label functional ingredients, and nutrient-rich formulations.

Clean‑label and natural product trends

Clean-label and natural product trends are significantly contributing to the growth of the fermented ingredients market, as consumers increasingly prioritize transparency, minimal processing, and ingredients perceived as safe and wholesome. Fermented ingredients align with these preferences as they are produced through biological processes rather than chemical synthesis, offering both functional and nutritional benefits while supporting the demand for natural and minimally processed products. Consumer willingness to pay a premium for such products further strengthens this trend. For example, The Roundup Organization's 2025 report indicates that 55% of consumers are willing to spend more on eco-friendly brands, highlighting a broader preference for sustainable, natural, and clean-label products. Fermentation-based ingredients cater to this demand by enabling the production of high-quality bioactive compounds with reduced environmental impact, lower synthetic additive content, and enhanced functionality. Additionally, these ingredients play a crucial role in meeting the growing demand for innovative food and beverage formulations, offering manufacturers opportunities to differentiate their products in a competitive market.

Technological advancements in fermentation

Technological advancements in fermentation are driving the growth of the fermented ingredients market by enabling the large-scale production of high-purity, bioactive, and sustainable ingredients. Developments such as precision fermentation, microbial strain engineering, bioreactor optimization, and advanced downstream processing have allowed manufacturers to produce a wide range of fermented compounds, including amino acids, probiotics, postbiotics, organic acids, enzymes, and fermentation-derived omega-3 fatty acids, with improved stability, potency, and functionality. These advancements also support the production of bio-identical and animal-free ingredients, such as human milk oligosaccharides and collagen, addressing the increasing consumer demand for clean-label, plant-based, and ethically sourced products. By overcoming traditional production challenges, fermentation technologies enable the delivery of ingredients with consistent quality, targeted health benefits, and reduced dependence on synthetic or animal-derived sources, aligning with current dietary trends and regulatory standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs | -1.1% | Global, most acute in Europe and North America | Short term (≤ 2 years) |

| Regulatory challenges | -0.9% | Global, with highest friction in emerging markets (South America, MEA, parts of Asia-Pacific) | Medium term (2-4 years) |

| Supply chain vulnerabilities | -0.7% | Global, with critical bottlenecks in Asia-Pacific feedstock supply and European energy availability | Short term (≤ 2 years) |

| Limited awareness in emerging markets | -0.5% | South America, Middle East and Africa, tier-2 and tier-3 cities in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production costs

High production costs pose a significant challenge for the fermented ingredients market, particularly in price-sensitive regions and applications. The production of fermented ingredients such as amino acids, probiotics, postbiotics, vitamins, and specialty enzymes involves complex microbial fermentation processes, rigorous quality control measures, and advanced downstream processing. These requirements demand substantial capital investment and operational expenses. Furthermore, ensuring consistent product quality, stability, and potency across batches often requires specialized equipment, controlled environments, and skilled personnel, further increasing costs. As a result, fermented ingredients are often more expensive than conventional synthetic alternatives or non-fermented options, which can limit their use in low-margin applications such as mass-market processed foods and basic animal feed.

Regulatory challenges

Regulatory challenges significantly restrain the fermented ingredients market, as fermentation-derived compounds such as probiotics, postbiotics, amino acids, vitamins, and enzymes must adhere to complex, region-specific regulations. Key regulatory bodies and frameworks include the U.S. Food and Drug Administration (FDA), the European Food Safety Authority (EFSA) for novel food approvals, Health Canada for nutraceutical and functional food regulation, the Food Safety and Standards Authority of India (FSSAI) for functional foods, and the China National Center for Food Safety Risk Assessment (CFSA). These agencies enforce stringent guidelines regarding ingredient safety, labeling, permissible health claims, and clinical substantiation, which vary significantly across regions. Compliance often necessitates extensive safety testing, clinical trials, and detailed documentation, making the process time-consuming, costly, and particularly challenging for small or new market entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Amino Acids Anchor Volume, Probiotics Drive Innovation

The Amino Acids segment, accounting for 28.35% of the fermented ingredients market share in 2025, remains a significant contributor to the industry's growth. This is attributed to its broad applicability across various end-use sectors and its essential role in human and animal nutrition. Fermented amino acids, including lysine, glutamic acid, threonine, and tryptophan, are highly valued for their superior bioavailability and effectiveness compared to chemically synthesized alternatives. These attributes make them indispensable in food fortification, pharmaceuticals, and dietary supplements. Furthermore, increasing consumer awareness of protein-rich diets, sports nutrition, and the rising popularity of functional foods have significantly driven the demand for amino acids, particularly in developed markets.

The Probiotics and Postbiotics segment is the fastest-growing category in the fermented ingredients market, with a notable CAGR of 8.82% projected through 2031. This growth is primarily driven by increasing global awareness of gut health, immunity enhancement, and overall wellness. Rising consumer demand for natural and clean-label products has further supported the adoption of probiotics and postbiotics, as many consumers now favor preventive and holistic health approaches over synthetic alternatives. Additionally, the growing prevalence of gastrointestinal disorders worldwide has intensified this trend. For example, data from the National Institute of Statistics (ISTAT) indicates that approximately 1.15 million individuals of all ages in Italy were affected by peptic ulcer disease in 2023, underscoring a significant target population that could benefit from probiotic supplementation to improve digestive health and reduce complications .

By Form: Dry Dominates Logistics, Liquid Gains in Beverages

The dry fermented ingredients segment is projected to account for 60.55% of the market share in 2025, underscoring its leading position in the fermented ingredients market. This dominance is attributed to the stability, ease of handling, and extended shelf life provided by dry forms, which make them well-suited for large-scale industrial applications. Typically available in powder or granular form, dry ingredients enable manufacturers to precisely dose, blend, and incorporate them into various formulations without compromising quality or effectiveness. Moreover, the versatility of dry forms allows them to be used across a wide range of industries, including food and beverages, pharmaceuticals, and animal feed, further solidifying their market presence. Furthermore, dry forms are particularly beneficial in regions with limited cold-chain infrastructure, as they minimize reliance on refrigeration compared to liquid alternatives, thereby supporting distribution in emerging markets.

The Liquid Form segment of fermented ingredients is experiencing significant growth, with a CAGR of 8.12% projected through 2031. This growth is driven by the increasing demand for ready-to-use, functional, and specialty formulations across various applications, including food, beverage, pharmaceutical, and cosmetics. Liquid fermented ingredients, including liquid probiotics, organic acids, enzymes, and liquid vitamins, provide benefits such as immediate solubility, uniform mixing, and faster bioavailability. These attributes make them well-suited for use in beverages, syrups, sauces, dairy drinks, and clinical nutrition products. Furthermore, the segment's expansion is bolstered by the increasing consumer preference for health-focused products and the growing awareness of the benefits of fermented ingredients. The rising popularity of functional beverages and nutraceutical drinks further supports this growth, as liquid probiotics and postbiotics are increasingly favored for their convenience and effectiveness in delivering live microorganisms.

By Application: Food Leads Volume, Pharma Accelerates Growth

The Food and Beverages segment accounted for 46.10% of the application share in 2025, establishing itself as the largest end-use category in the fermented ingredients market. This significant market share is attributed to increasing consumer demand for functional and natural food products, along with a growing preference for flavors, preservatives, and nutritional enhancers produced through fermentation processes. Fermented ingredients are extensively utilized in bakery, dairy, beverages, meat, and fish products to enhance taste, texture, shelf life, nutritional value, and digestibility. The segment's growth is further supported by the global shift toward health and wellness-oriented diets, including protein-enriched foods, gut-friendly products, and fortified beverages, which capitalize on the functional advantages of fermented ingredients to align with changing consumer preferences.

The pharmaceutical segment of the fermented ingredients market is growing at a CAGR of 8.29% through 2031, driven by increasing demand for therapeutic, preventive, and functional healthcare solutions. Fermented ingredients are essential in the production of nutraceuticals, dietary supplements, clinical nutrition products, and biopharmaceuticals, making them a key component in modern medicine and wellness applications. Advances in precision fermentation, microbial strain optimization, and bioprocess engineering have improved production efficiency, stability, and bioavailability of pharmaceutical-grade fermented ingredients. These developments enable pharmaceutical companies to create high-potency formulations that provide specific health benefits, such as immune modulation, anti-inflammatory effects, and enhanced nutrient absorption, while adhering to safety and regulatory standards.

Geography Analysis

Asia-Pacific accounted for 34.20% of the fermented ingredients market share in 2025 and is projected to grow at a CAGR of 8.88% through 2031, making it the fastest-growing region globally. This growth is primarily driven by China's dominance in amino acid production and exports, which supports both domestic consumption and global supply chains. For example, data from the Observatory of Economic Complexity (OEC) indicates that China exported USD 1.5 billion worth of amino acids in 2024, highlighting its pivotal role in the global market . India is also emerging as a significant contributor, with its fermentation industry expanding rapidly due to government support, increased investment in biotechnology, and growing demand for functional foods, nutraceuticals, and animal feed. Factors such as a large population, rising health awareness, increasing disposable incomes, and expanding industrial capabilities position the Asia-Pacific as a key growth driver in the fermented ingredients market.

North America and Europe represent mature markets for fermented ingredients, characterized by slower volume growth but higher value generation. These regions benefit from trends such as premiumization, advanced Research and Development (R&D) capabilities, and regulatory-driven product reformulation. Manufacturers in these markets focus on developing clean-label, functional, and high-potency products to meet the growing consumer demand for health, wellness, and preventive nutrition. Europe, in particular, has seen strong adoption of probiotics, postbiotics, and organic acids in both food and pharmaceutical applications. Meanwhile, North America emphasizes innovation in functional beverages, nutraceuticals, and clinical nutrition products. The focus in these regions is on value creation, formulation advancements, and adherence to stringent regulatory standards, ensuring sustained profitability despite slower growth rates.

South America and the Middle East, and Africa present emerging opportunities for the fermented ingredients market, driven by increasing awareness of nutrition, food fortification initiatives, and the growth of functional food sectors. However, these regions face challenges such as infrastructure limitations, fragmented supply chains, and regulatory inconsistencies, which can hinder large-scale adoption. In South America, gradual adoption is observed in animal feed, dairy, and processed foods, while the Middle East and Africa show potential in functional foods, dairy products, and pharmaceuticals, particularly as urbanization and disposable incomes rise. Companies entering these markets must address logistical, regulatory, and educational challenges, but the untapped potential offers significant long-term growth opportunities as these regions continue to develop their food and health industries.

Regulatory Landscape

Fermented ingredients, including probiotics, postbiotics, amino acids, vitamins, and enzymes, typically move through established food additive, novel food, and supplement pathways rather than a single dedicated global framework specific to precision fermentation-derived ingredients. In the United States, the US Food and Drug Administration (FDA) oversees food additives and GRAS determinations under the Federal Food, Drug, and Cosmetic Act, and companies commonly use the GRAS notice process for microorganism-derived ingredients. In March 2026, the FDA issued a no-questions response related to the GRAS status of a Saccharomyces cerevisiae strain (BY-1532) for use as a secondary direct food additive.

In Europe, the European Food Safety Authority (EFSA) supports safety assessment for novel foods under Regulation (EU) 2015/2283, and microbial strain and genomics requirements have become more explicit through EFSA guidance for ingredients produced via microbial fermentation. EFSA also maintains the Qualified Presumption of Safety (QPS) approach for microorganisms used in the food chain and published an updated QPS list in January 2026 covering a large set of microorganism notifications, which can streamline premarket safety substantiation for qualifying strains. Industry bodies such as EuropaBio and other associations continue to advocate for clearer classification and streamlined authorization routes for food cultures and fermentation-derived ingredients to reduce time-to-market friction in the EU.

Value Chain Analysis

The fermented ingredients value chain starts with upstream biological and material inputs, including microbial strain development (culture collections, strain engineering, and validation), fermentation media and feedstocks (sugars, nitrogen sources, and micronutrients), and process aids. Manufacturing then includes upstream fermentation in industrial bioreactors, followed by downstream separation, purification, concentration, stabilization, and formulation into dry or liquid formats. The value chain also spans equipment and technology providers (bioreactors, filtration and chromatography systems, and analytics), CDMOs that offer fermentation and GMP infrastructure, and ingredient houses that blend, standardize, and tailor fermented actives for applications across food and beverages, pharmaceuticals, personal care, and animal nutrition.

Midstream constraints are largely tied to scale and compliance, especially access to large-scale fermentation capacity and long lead times for major fermentation and purification equipment, which can slow commercialization for higher-purity, application-specific ingredients. Companies increasingly use partnerships to address these gaps, including Wacker Chemie AG and BENEO (February 2025) collaborating to produce the human milk oligosaccharide 2-Fucosyllactose in Europe using precision fermentation, and ADM with Asahi Group Foods (February 2025) signing an exclusive international distribution agreement for Lactobacillus gasseri CP2305 (a postbiotic). Downstream, distribution runs through global ingredient channels and application formulators (dairy, bakery, beverages, clinical nutrition, and supplements), while cold-chain and shelf-life requirements influence logistics decisions, particularly for live-culture products versus stabilized postbiotics and enzymes.

Competitive Landscape

The fermented ingredients market demonstrates moderate concentration, featuring a combination of large multinational corporations and smaller, innovative companies. Established firms such as BASF SE, Archer-Daniels-Midland Company, Ajinomoto Co. Inc., and Cargill, Incorporated leverage their extensive customer relationships, global distribution networks, and brand recognition to maintain a competitive position. These companies often cross-sell fermented ingredients alongside their synthetic and conventional product portfolios, enhancing customer retention and capturing additional value across applications such as food, beverages, pharmaceuticals, and animal feed. Their scale enables significant investment in Research and Development (R&D), fostering advancements in fermentation technologies, process optimization, and product diversification.

The market is increasingly emphasizing fermentation-derived specialty ingredients, such as omega-3 fatty acids. These products address sustainability concerns associated with fish oil sourcing, making them appealing to environmentally conscious consumers and investors. Both established ingredient suppliers and venture-backed startups are investing in fermentation-based omega-3 solutions to meet the growing global demand for plant-based, sustainable, and high-purity bioactives. This shift highlights the expansion of fermentation technology beyond traditional amino acids and enzymes into high-value nutritional compounds that align with evolving health, sustainability, and regulatory trends.

Emerging disruptors are transforming the competitive landscape by utilizing precision fermentation to produce high-value molecules. These innovations cater to the increasing demand for clean-label, animal-free, and bio-equivalent ingredients, which are essential in functional foods, infant nutrition, nutraceuticals, and personal care products. By eliminating animal-derived inputs, these advancements not only align with consumer preferences but also enable new applications previously limited by ethical or regulatory constraints. Together, established players and agile, innovation-driven startups are fostering a dynamic competitive environment characterized by technological differentiation, strategic partnerships, and rapid product development.

Fermented Ingredients Industry Leaders

-

Ajinomoto Co. Inc.

-

Archer-Daniels-Midland Company

-

Associated British Foods PLC

-

BASF SE

-

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Industrial scale-up and capacity availability are a clear whitespace for fermented ingredients beyond traditional amino acids and enzymes, particularly for higher-value proteins and specialized bioactives that need robust downstream purification. Recent investments and site actions provide concrete signals for where capacity is being added: FERM FOOD (March 2026) acquired a former Orkla site in Skovlund, Denmark, targeting up to 20,000 tonnes per year of fermented plant-based ingredients, while Kerry (April 2026) opened an expanded biotechnology manufacturing hub in Carrigaline, Ireland to scale lactase enzyme production for global dairy processing. Equipment innovation is also supporting scale economics, including Tetra Pak launching its Bioreactor RF in July 2026, designed to support industrial fermentation from 10 to 50,000 liters and reduce operational costs.

Opportunities are widening around animal-free equivalents and functional performance that fits clean-label and nutrition priorities, including precision-fermented dairy proteins and lactoferrin for infant and mainstream nutrition. In 2026, partnerships and funding moves highlighted this direction, including Nestle partnering with Helaina to scale Effera (bioidentical human lactoferrin) and TurtleTree partnering with Novonesis to scale and commercialize precision-fermented lactoferrin for infant nutrition. At the same time, Europe is tightening and clarifying regulatory expectations for microorganism characterization and risk assessment, alongside ongoing industry engagement on the EU food and feed safety simplification agenda, which can favor companies that already have strong dossiers, validated strains, and traceable production systems to shorten approval cycles and expand geographic access.

Recent Industry Developments

- July 2026: Archer-Daniels-Midland Company (ADM) partnered with The Every Company to produce animal-free egg protein at ADM's facility in Clinton, Iowa using precision fermentation. The collaboration links a large-scale ingredients manufacturer to a defined production site, helping convert precision-fermented proteins from pilot activity into repeatable supply for food formulators.

- November 2025: BASF SE introduced an Isobionics natural lime flavor ingredient produced using fermentation technology, positioned around high purity. This broadened fermentation's role in flavor and fragrance ingredients, supporting premiumization and clean-label reformulation needs across beverages and packaged foods.

- September 2024: Nosh.bio and Zur Muehlen Group entered a commercial partnership to launch Koji Chunks as a single-ingredient meat analog. The collaboration connected a fermentation-derived ingredient platform with an established meat processor, supporting faster adoption pathways for fermented proteins in alternative protein formulations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the fermented ingredients market covers ingredients that are manufactured using controlled fermentation (microbial growth and enzyme action) and then sold for use in food and beverages, animal feed, pharmaceuticals, and industrial applications.

Scope exclusions: Finished consumer foods and drinks where fermentation is part of the final product, plus fermentation equipment and engineering services, are not counted.

Segmentation Overview

-

By Product Type

- Amino Acids

- Organic Acids

- Polymers

- Vitamins

- Industrial Enzymes

- Antibiotics

- Probiotics and Post-biotics

- Others

-

By Form

- Dry

- Liquid

-

By Application

-

Food and Beverages

- Dairy

- Bakery and Confectionery

- Beverages

- Meat and Fish Products

- Others

- Animal Feed

- Pharmaceutical

- Personal Care and Cosmetics

- Other Applications

-

Food and Beverages

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand and supply context where fermented based ingredients are used, then narrowing it to tradable ingredient outputs by end use. We lean on public statistics and standards to keep definitions consistent, using sources such as USDA and other national agriculture agencies for crop and feed baselines, FAOSTAT for agriculture production signals, UN Comtrade for trade flow direction checks, and the US FDA and the European Commission for regulatory and allowed use cues.

We also review company annual reports, investor presentations, and technical notes published by ingredient associations and universities, since they help validate product usage logic (for example, where enzymes are used as processing aids versus label declared additives). Patent databases and an import export shipment level database are used selectively to sense where capacity additions, new strains, or application shifts are happening, and then to pressure test timing. This list is not exhaustive, and many other public sources were also consulted to collect, cross check, and clarify inputs.

Primary Interviews and Surveys

Primary work focuses on confirming what is actually sold as a fermented ingredient and how volumes and pricing behave by application and region. We speak with ingredient producers, distributors, and end use formulators, and then recheck assumptions across APAC, EMEA, and the Americas so one region does not over influence the final number. When inputs disagree, follow up questions are asked to pin down practical drivers behind differences in reported demand and price realization.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | APAC: 40% |

| Mid tier: 49% | Functional/Unit leaders: 40% | EMEA: 34% |

| Smaller Players: 22% | Managers: 46% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where agriculture and processed food output, animal protein production, and industrial fermentation adoption indicators are used to reconstruct a realistic demand pool for fermented ingredient inputs. Those totals are then corroborated with selective bottom-up approximations, such as sampled supplier revenue signals, channel feedback on movement, and price per kg ranges applied to typical consumption volumes, which helps adjust for overcounting or missed pockets.

Key model inputs include application level penetration of fermentation derived ingredients, production volumes in feed and food processing, trade direction changes for amino acids and organic acids, the mix shift between dry and liquid forms, and observed pricing movement tied to sugar or feedstock cost and energy intensity. Forecasts are produced using scenario analysis supported by trend lines in these variables, and then sanity checked with expert views on capacity utilization and new application rollout speed. Where bottom-up checks are thin for a country or niche ingredient, we fill gaps through regional analogs and then apply conservative ranges until they are validated again in follow up calls.

Data Validation & Update Cycle

Outputs are checked in several passes so the number makes sense from more than one angle. We compare the model results with independent signals like regional trade growth, major capacity announcements, and application demand shifts, and then investigate any sharp swings in implied pricing or volume before sign off.

A second analyst review is used to recheck formulas, unit conversions, and assumption logic, followed by targeted re contacts when there is a large variance versus interview feedback. Reports are refreshed annually, and interim updates are made when material events occur, such as large plant start ups, regulation changes, or feedstock shocks. Before delivery, a final review pass is completed so the latest public updates are reflected.

Mordor Intelligence's Fermented Ingredients Market Size Compared With Other Published Estimates

Published market values for fermented ingredients often do not match because each study draws the line differently on what counts as an ingredient versus a finished fermented product, and because base years, currency timing, and pricing build ups are handled in different ways.

Some published figures fold in broader fermentation related categories and may also apply aggressive price expansion across the forecast window, which can lift the starting value quickly. In Mordor Intelligence, the number is anchored to ingredient outputs used in food and beverages, animal feed, pharmaceutical, and industrial applications, and it stays aligned to product type coverage (including antibiotics) plus repeat checks on form mix and region level demand signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 52.82 B (2026) | |

| Industry Publisher A | USD 44.02 B (2025) | Uses a different base year and a narrower basket in parts of the narrative, with limited clarity on whether items like antibiotics and certain industrial use cases are treated inside the core ingredient pool. |

| Industry Publisher B | USD 31.50 B (2025) | Takes a tighter view that explicitly avoids counting finished fermented foods and beverages, and it also appears to emphasize ingredient categories like cultures and dairy related ingredients, which can shift totals versus a broader type set. |

The spread in published values is mainly explained by scope choices and base year timing, and then amplified by how pricing and mix shifts are projected. By keeping the inputs tied to observable application demand, trade direction checks, and realistic price ranges, our estimate stays traceable to repeatable steps that a reader can follow and challenge.

Key Questions Answered in the Report

How large is the fermented ingredients market in 2026?

The market is valued at USD 52.82 billion in 2026 and is projected to reach USD 77.72 billion by 2031.

Which product category holds the largest share?

Amino acids lead with 28.35% of 2025 revenue due to heavy demand in animal feed.

Which region is growing fastest?

Asia-Pacific, expanding at a 8.88% CAGR through 2031, driven by capacity additions in China and India.

Why are liquid formats gaining popularity?

Beverage and dairy processors prefer liquid ingredients for direct blending, which reduces processing steps and maintains higher probiotic viability.

Page last updated on: