Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

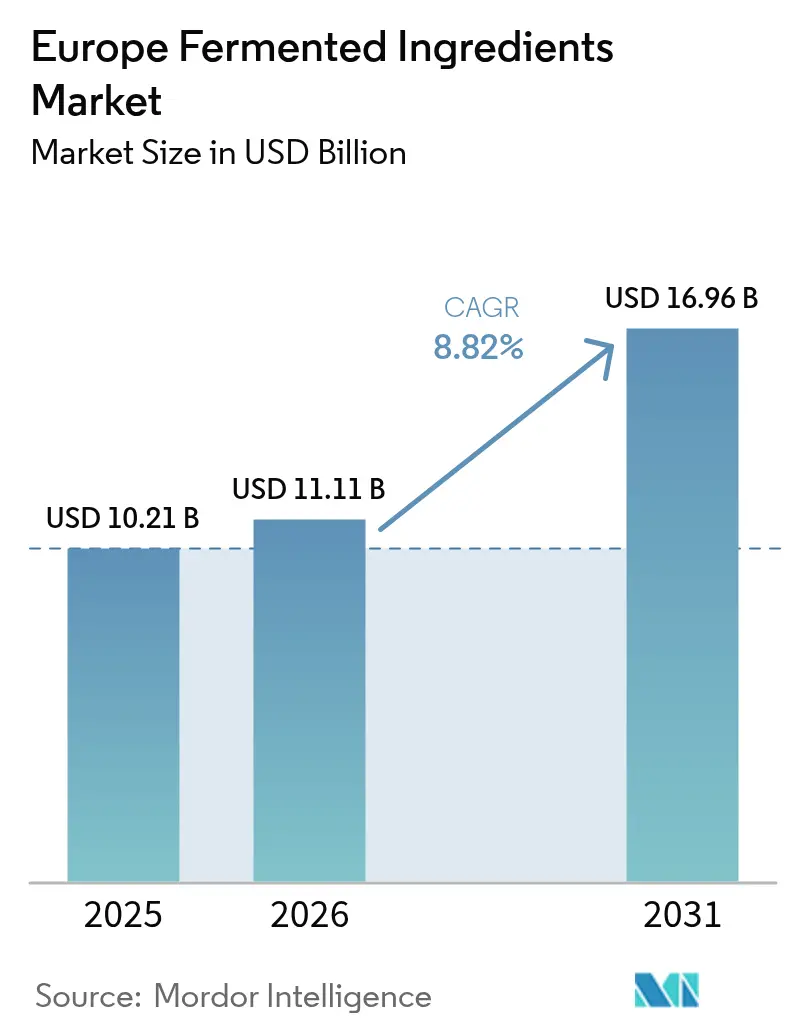

| Base Year Market Size (2025) | USD 10.21 Billion |

| Market Size (2026) | USD 11.11 Billion |

| Market Size (2031) | USD 16.96 Billion |

| Growth Rate (2026 - 2031) | 8.82% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Fermented Ingredients Market Analysis by Mordor Intelligence

The Europe Fermented ingredients market size is expected to grow from USD 10.21 billion in 2025 to USD 11.11 billion in 2026 and is forecast to reach USD 16.96 billion by 2031 at 8.82% CAGR over 2026-2031. This acceleration reflects a structural shift in how European manufacturers source functional molecules, driven by pharmaceutical demand for bio-based active pharmaceutical ingredients and consumer preference for recognizable ingredient labels. The European Commission's 2024 biotech and biomanufacturing strategy positions the region to capture a larger share of the global biotechnology market, where Europe currently holds a substantial share[1]Source: European Commission," biotech and biomanufacturing", research-and-innovation.ec.europa.eu. Structural demand for bio-based actives in pharmaceuticals, rising clean-label expectations in foods, and the European Commission’s biotech strategy collectively accelerate adoption across the Europe fermented ingredients market. German and Dutch fermentation hubs supply commodity amino acids and organic acids at scale, while France and Italy channel fresh investment into high-purity APIs and precision strains.

Key Report Takeaways

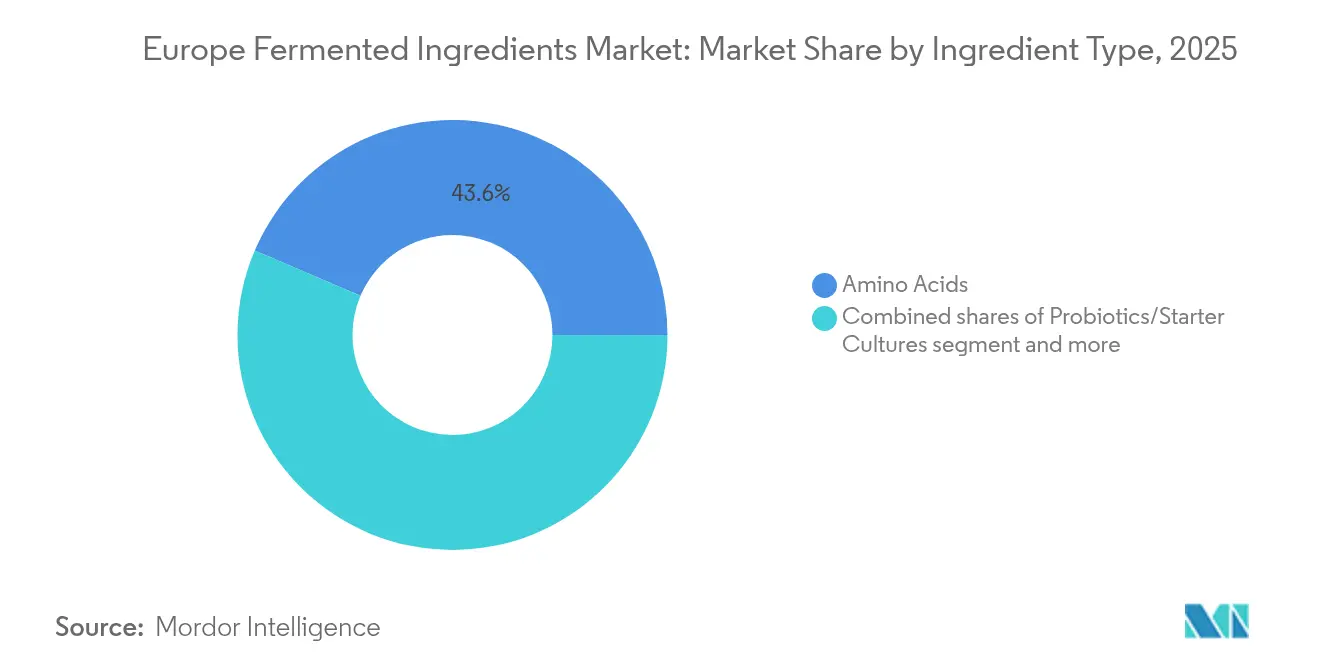

- By ingredient type, amino acids led with 43.58% of the Europe fermented ingredients market share in 2025, while probiotics and starter cultures are forecast to grow at a 8.99% CAGR through 2031.

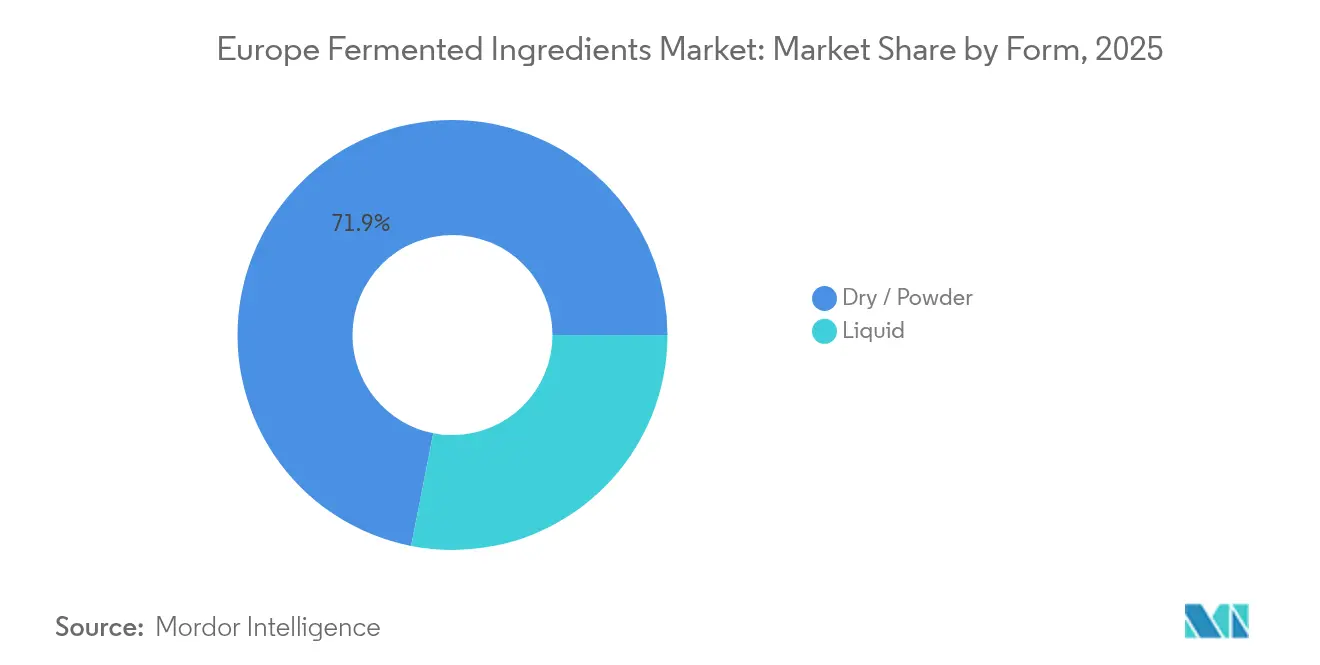

- By form, dry and powder formats accounted for 71.92% of the Europe fermented ingredients market size in 2025; liquid formats are projected to expand at a 9.31% CAGR to 2031.

- By application, food and beverages captured 45.12% of the Europe fermented ingredients market in 2025, whereas pharmaceuticals are set to advance at a 10.12% CAGR during the forecast period.

- By geography, Germany held 27.74% revenue share of the Europe fermented ingredients market in 2025, and France is anticipated to record the fastest growth at a 9.96% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Fermented Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing interest in functional foods with health benefits | +1.2% | Germany, France, the Netherlands, with spillover to Spain and Italy | Medium term (2-4 years) |

| Increasing use of fermented acids and enzymes in the food and beverages sector | +1.5% | Pan-European, concentrated in Germany, France, UK | Short term (≤ 2 years) |

| Clean-label requirement driving fermentation ingredient adoption | +1.3% | Germany, France, the Netherlands, the UK, Nordic countries | Medium term (2-4 years) |

| Growing pharmaceutical demand for bio-based fermentation APIs | +1.8% | Germany, France, Italy, the Netherlands | Long term (≥ 4 years) |

| Expanding incorporation of probiotics in personal care products | +0.8% | France, Germany, the UK, with emerging adoption in Spain | Medium term (2-4 years) |

| Improved shelf life using fermentation-derived preservatives | +0.7% | Pan-European, particularly in packaged food hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Pharmaceutical Demand for Bio-Based Fermentation APIs

Europe's drive to reshore pharmaceutical supply chains is redirecting capital toward fermentation-based active pharmaceutical ingredient production, a strategic response to the vulnerabilities exposed during COVID-19 when Asian API imports faltered. EUROAPI operates two large-scale fermentation sites in France and Italy with a combined capacity of nearly 6,000 cubic meters and full cGMP compliance, positioning the company to serve both innovator and generic drug manufacturers. Lonza's mammalian and microbial fermentation platforms in Switzerland and adjacent European facilities supply biologics and small-molecule APIs, leveraging decades of process development expertise. The European Medicines Agency's emphasis on supply security and the EU's pharmaceutical strategy, which targets 40% of critical API production within the bloc by 2030, are accelerating investments in fermentation infrastructure. Evonik's BioMilk platform, which uses yeast to biosynthesize tropane alkaloids traditionally extracted from plants, demonstrates how fermentation can de-risk supply chains dependent on agricultural inputs.

Clean-Label Requirement Driving Fermentation Ingredient Adoption

Consumer demand for ingredient transparency is compelling food manufacturers to replace synthetic additives with fermentation-derived alternatives that carry familiar names and natural origin claims. The European Food Safety Authority authorized buffered vinegar (E 267) in 2023 for use as a preservative in various food categories, validating fermentation-based preservation systems that extend shelf life without triggering clean-label concerns[2]Source: European Union, "European Food Safety Authority", efsa.europa.eu. Kerry Group's BioKerry platform integrates fermentation-derived enzymes, cultures, and flavor compounds to help customers reformulate products with shorter ingredient lists while maintaining sensory profiles. Corbion's lactic acid and lactates, produced via fermentation in the Netherlands, serve as multifunctional ingredients that acidify, preserve, and enhance texture without the stigma attached to chemical preservatives. Regulatory frameworks such as the EU's food enzyme regulation (EC) No 1332/2008 require rigorous safety assessments, yet once approved, fermentation enzymes like subtilisin and chymosin benefit from broad application permissions across dairy, baking, and beverage categories.

Increasing Use of Fermented Acids and Enzymes in Food and Beverages Sector

Fermented organic acids and industrial enzymes have become indispensable processing aids in European food and beverage manufacturing, enabling cost reduction, yield improvement, and novel product formats. Citric acid, produced via Aspergillus niger fermentation, functions as an acidulant and chelating agent in beverages, confectionery, and dairy, with Cargill and other producers operating large-scale facilities that convert molasses or glucose into multi-thousand-ton annual outputs. Enzymes such as amylases, proteases, and lipases accelerate starch conversion in brewing, protein hydrolysis in cheese making, and fat modification in bakery applications, reducing processing time and energy consumption. EFSA issued positive opinions in 2024 for glutaminase from Bacillus subtilis and bacillolysin from Bacillus amyloliquefaciens, expanding the toolkit available to food technologists. Novonesis, formed from the Novozymes-Chr. Hansen merger commands a leading position in food enzymes with a portfolio spanning dairy, baking, brewing, and protein processing, supported by EUR 3.6 billion in combined revenue and extensive application laboratories.

Growing Interest in Functional Foods with Health Benefits

European consumers increasingly prioritize foods that deliver tangible health benefits beyond basic nutrition, creating demand for fermentation ingredients that support gut health, immune function, and metabolic wellness. The DOMINO project, a multi-country research initiative involving 4,917 adults across 7 European nations, documented consumer perceptions of fermented foods and identified key drivers of acceptance, including perceived naturalness and digestive benefits. Probiotics such as Lactobacillus and Bifidobacterium strains are incorporated into yogurts, dietary supplements, and functional beverages, with DuPont's HOWARU range offering clinically documented strains for digestive and immune support. Prebiotics, which are often produced via enzymatic conversion of plant substrates, are gaining traction as formulators seek to substantiate health claims under EFSA's stringent evaluation framework. The European Food Safety Authority maintains a Qualified Presumption of Safety (QPS) list that streamlines approval for well-characterized microbial strains, reducing regulatory burden for probiotic developers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High specialized fermentation infrastructure costs hinder growth | -0.9% | Germany, France, the Netherlands, Italy | Long term (≥ 4 years) |

| Complex regulatory approval processes delay product launches | -0.8% | Pan-European, particularly affecting novel strains and applications | Medium term (2-4 years) |

| Competition from non-fermented functional ingredient alternatives | -0.5% | Germany, France, UK, Spain | Short term (≤ 2 years) |

| Fragmented starter culture supply chain complexity | -0.4% | Pan-European, with acute pressure in specialty dairy segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Specialized Fermentation Infrastructure Costs Hinder Growth

Capital requirements for fermentation facilities impose significant barriers to entry and constrain capacity expansion, particularly for smaller players lacking access to patient capital or established cash flows. Greenfield fermentation plants equipped with stainless-steel bioreactors, aseptic filling lines, and downstream purification systems, all meeting cGMP standards for pharmaceutical or food-grade production, typically require upfront investments exceeding USD 50 million, with lead times stretching 3 to 5 years from design to commissioning. Evonik's six European fermentation sites, collectively housing over 4,000 cubic meters of capacity, represent decades of accumulated investment and process optimization that few competitors can replicate. Energy costs for sterilization, agitation, and temperature control further burden operating economics, with European natural gas prices in 2024 remaining elevated relative to pre-2022 levels.

Complex Regulatory Approval Processes Delay Product Launches

Navigating the European Union's regulatory landscape for fermentation ingredients demands extensive dossier preparation, safety testing, and agency review, delaying commercialization and increasing development costs. The Novel Food Regulation (EU) 2015/2283 requires comprehensive safety assessments for ingredients derived from novel strains or processes, with EFSA review timelines often extending 18 to 24 months from submission to authorization. Food enzyme applications under Regulation (EC) No 1332/2008 similarly require detailed characterization of production organisms, enzyme purity, and intended use conditions, with EFSA issuing scientific opinions that can take 12 to 18 months. The Substances of Human Origin (SoHO) Regulation 2024/1938, which entered into force in 2024, introduces additional oversight for certain biological materials, potentially affecting fermentation-derived ingredients from human-associated microbiota. Divergent national interpretations of EU frameworks further complicate market entry, as member states retain discretion over certain implementation details.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Amino Acids Lead, Probiotics Accelerate

Amino Acids captured 43.58% of the europe fermented ingredients market in 2025, reflecting decades of entrenched demand from animal feed compounders and pharmaceutical synthesizers who rely on lysine, methionine, threonine, and tryptophan to optimize livestock growth and drug intermediates. Ajinomoto's EUR 150 million investment in Belgium during 2024 to expand specialty amino acid production underscores the strategic importance of this segment, as the company seeks to serve both nutrition and pharmaceutical customers with high-purity grades. Evonik's methionine production, a critical amino acid for poultry and swine diets, leverages fermentation and chemical synthesis routes to deliver consistent quality at scale. Probiotics and Starter Cultures, however, are forecast to grow fastest at 8.99% CAGR from 2026 to 2031, driven by expanding applications in functional foods, dietary supplements, and fermented dairy products. The January 2024 merger of Novozymes and Chr. Hansen into Novonesis consolidated two probiotic powerhouses, creating a platform with extensive strain libraries and application expertise across human and animal health.

Organic Acids, including citric, lactic, and acetic acids, serve as acidulants, preservatives, and pH regulators across food, beverage, and industrial applications, with Corbion's lactic acid production in the Netherlands exemplifying large-scale fermentation economics. Vitamins, particularly B-complex vitamins like riboflavin (B2), cobalamin (B12), and biotin, are produced via fermentation by DSM-Firmenich and BASF, leveraging microbial biosynthesis to achieve cost and sustainability advantages over chemical routes. Industrial Enzymes, proteases, amylases, lipases, cellulases, enable process intensification in baking, brewing, detergents, and biofuels, with Novonesis commanding a leading position through its combined enzyme portfolio. Polymers, such as polylactic acid (PLA) and polyhydroxyalkanoates (PHA), represent emerging segments where fermentation-derived monomers offer biodegradable alternatives to petrochemical plastics, though commercial scale remains limited. The Others category encompasses specialty molecules like biosurfactants, flavor compounds, and pigments, where fermentation enables access to complex structures difficult to synthesize chemically.

By Form: Dry Powder Dominates, Liquid Gains Traction

Dry and Powder forms held 71.92% of the European fermented ingredients market in 2025, a dominance rooted in superior shelf stability, reduced transportation costs, and ease of handling in downstream formulation processes. Spray drying, freeze drying, and drum drying technologies convert fermentation broths into free-flowing powders that retain enzymatic activity, probiotic viability, or chemical potency over extended storage periods, critical for global supply chains and just-in-time manufacturing. Lallemand's yeast and bacteria products, widely used in baking and brewing, are predominantly supplied in dry formats that tolerate ambient storage and simplify dosing. Kerry Group's enzyme and culture offerings similarly leverage dry formulations to serve diverse food manufacturers across Europe.

Liquid forms, however, are projected to expand at 9.31% CAGR from 2026 to 2031, driven by continuous fermentation systems that deliver fresh, high-titer broths directly to adjacent processing lines, eliminating drying costs and preserving heat-sensitive bioactives. Corbion's lactic acid is often supplied in liquid concentrate, enabling efficient integration into beverage and dairy production. Liquid probiotics and enzymes are gaining traction in applications where immediate activity is prioritized over long-term storage, such as on-site inoculation in cheese making or real-time enzyme addition in brewing. The shift toward liquid formats reflects broader trends in process integration and sustainability, as eliminating drying steps reduces energy consumption and carbon footprint, aligning with Europe's Green Deal objectives.

By Application: Food Dominates, Pharmaceuticals Surge

Food and Beverages applications commanded 45.12% of the European fermented ingredients market in 2025, reflecting the sector's massive consumption of organic acids, enzymes, probiotics, and vitamins across dairy, baking, brewing, confectionery, and beverage production. Enzymes such as amylases and proteases accelerate starch conversion and protein hydrolysis, reducing processing time and improving yield, while probiotics and starter cultures define product identity in yogurt, cheese, and fermented beverages. Organic acids like citric and lactic acid regulate pH, enhance flavor, and extend shelf life, with Corbion and Cargill operating large-scale production facilities. The European Food Safety Authority's 2024 opinions on glutaminase and bacillolysin expanded the enzyme toolkit available to food technologists, enabling novel applications in plant-based protein processing and flavor development. Pharmaceuticals, however, are forecast to grow fastest at 10.12% CAGR from 2026 to 2031, propelled by Europe's strategic push to reshore API production and reduce dependence on Asian suppliers.

Animal Feed applications consume large volumes of amino acids, lysine, methionine, threonine, and enzymes like phytase and xylanase to optimize livestock nutrition and reduce environmental impact through improved feed conversion ratios. Cosmetics and Personal Care represent a niche but growing segment, with probiotics and fermentation-derived bioactives incorporated into skincare formulations targeting microbiome balance and anti-aging benefits. S-Biomedic's LiveSkin Probiotic, approved for acne treatment in the EUR 4.4 billion European acne market, demonstrates the therapeutic potential of fermentation ingredients in dermatology. Other Applications encompass industrial chemicals, textiles, and specialty materials, where fermentation-derived molecules offer sustainability advantages over petrochemical routes.

Geography Analysis

Germany held 27.74% of the European fermented ingredients market in 2025, anchored by a robust biotechnology infrastructure, pharmaceutical manufacturing clusters, and established fermentation capacity across amino acids, enzymes, and vitamins. Evonik's six European sites, including multiple facilities in Germany, collectively house over 4,000 cubic meters of fermentation capacity and serve pharmaceutical, nutrition, and industrial customers. BASF's vitamin production, also concentrated in Germany, leverages fermentation for riboflavin and other B-complex vitamins, integrating with the company's broader chemical portfolio.

France is projected to grow fastest at 9.96% CAGR from 2026 to 2031, driven by government support for biotechnology innovation, precision fermentation ventures, and pharmaceutical API reshoring. Roquette, a French family-owned company with EUR 4.3 billion in revenue, operates fermentation capabilities for specialty ingredients and plant-based proteins. The Netherlands benefits from a concentrated biotech cluster, with Corbion's lactic acid production and DSM-Firmenich's vitamin and culture operations anchoring the sector. Wageningen University's fermentation research programs further strengthen the innovation ecosystem, supplying talent and technology to industry partners. Spain and Italy are emerging as attractive locations for fermentation investments, supported by competitive labor costs, renewable energy availability, and proximity to Mediterranean food and beverage markets. EUROAPI's Italian site complements its French operations, providing geographic redundancy and access to southern European customers. The United Kingdom, despite Brexit-related regulatory divergence, retains significant fermentation capacity in enzymes and specialty ingredients, with Tate & Lyle operating food ingredient facilities. Russia's fermentation sector remains constrained by geopolitical tensions and limited access to Western technology, though domestic producers continue to serve local food and pharmaceutical markets. The rest of Europe, encompassing Nordic countries, Eastern Europe, and smaller Western European nations, collectively contributes to regional capacity through specialized producers and contract fermentation operators, with regulatory harmonization under EU frameworks facilitating cross-border trade and investment.

Regulatory Landscape

Fermented ingredients placed on the EU market fall under General Food Law (Regulation (EC) No 178/2002), with the applicable pathway determined by the ingredient category and history of use. Food additives and their specifications are governed mainly by Regulation (EC) No 1333/2008, food enzymes by Regulation (EC) No 1332/2008, and ingredients that were not consumed significantly in the EU before 14 May 1997 are assessed under the Novel Food Regulation (EU) 2015/2283, with EFSA conducting the risk assessment.

Authorizations and updates to Union lists typically move through the Common Authorisation Procedure (Regulation (EC) No 1331/2008), which combines EFSA opinions with European Commission and Member State risk-management decisions. In January 2026, the European Commission adopted Commission Regulation (EU) 2026/196 amending specifications for several food additives (including xanthan gum, E 415, and locust bean gum, E 410) with transition periods ending on 18 August 2026, creating near-term compliance actions for ingredient suppliers and food manufacturers. EFSA also updated data-requirement guidance for food additive applications effective 20 July 2026, reinforcing expectations on dossier quality for companies seeking new approvals or changes to existing authorizations.

Value Chain Analysis

The value chain starts with feedstock sourcing (sugars, starches, cereals, and other carbohydrate streams) and utilities, then moves into strain development, upstream fermentation, downstream recovery (separation, purification, concentration), and finishing (spray drying or other drying for powders, blending, stabilization, and packaging). For pharmaceutical-grade fermentation outputs, cGMP production, quality control, and traceability requirements add more testing and documentation steps before release, whereas food-grade applications place more emphasis on consistency, labeling compliance, and application support for reformulation.

Distribution typically runs through direct sales to large food, beverage, and pharmaceutical manufacturers, specialized ingredient distributors, and application labs that support customer trials and scale-up. Industry bodies such as the European Fermentation Group (EFG, Cefic) point to the industrial footprint of fermentation in Europe (19 industrial plants across 11 countries and 7,065 direct jobs), alongside the importance of globally competitive access to key feedstocks, which remains a recurring cost and resilience pressure point. On the compliance side, labeling in the EU is governed by Regulation (EU) 1169/2011, while pre-market authorization may be required case-by-case under the Novel Food Regulation (EU) 2015/2283 when ingredients lack a qualifying history of safe use.

Competitive Landscape

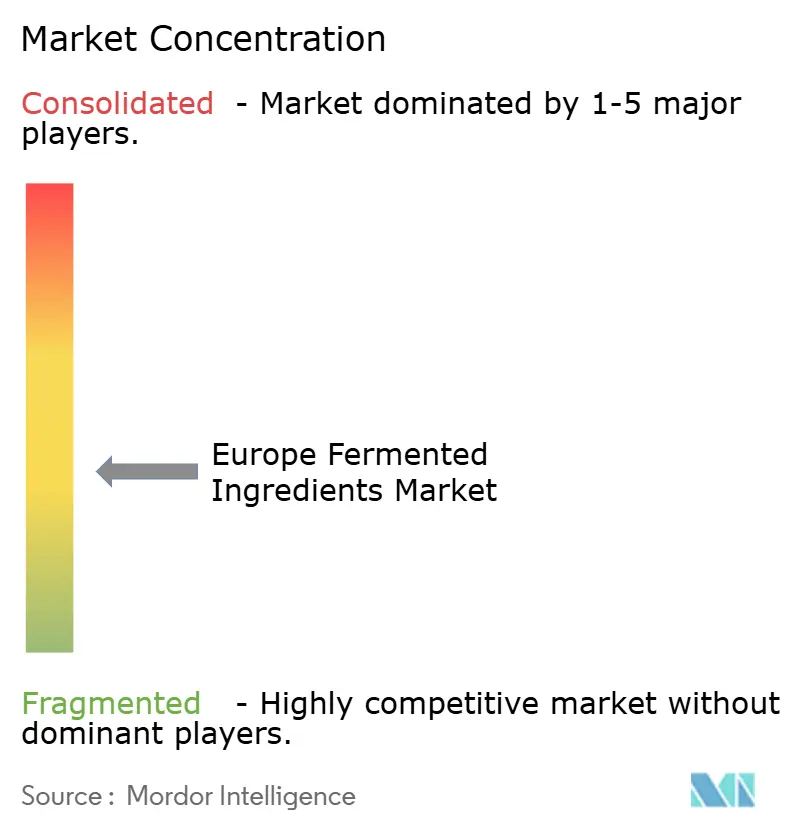

The European fermented ingredients market exhibits moderate fragmentation, reflecting a competitive landscape where multinational ingredient conglomerates, regional specialists, and contract fermentation operators coexist across diverse application niches. The January 2024 merger of Novozymes and Chr. Hansen into Novonesis, creating a EUR 3.6 billion revenue entity, exemplifies consolidation pressure as players seek scale in enzyme and probiotic portfolios to cross-sell into pharmaceutical, food, and animal nutrition channels. DSM-Firmenich, formed in May 2023 with combined revenue of EUR 12.6 billion, similarly leverages fermentation platforms spanning vitamins, cultures, and bioactives to serve multiple end markets and geographies.

Strategic moves center on vertical integration, with companies like Corbion and Evonik controlling fermentation capacity, downstream processing, and application development to capture margin across the value chain. Opportunities persist in precision fermentation for alternative proteins, where regulatory clarity around novel food approvals remains uneven across member states, and in biopolymer production, where commercial-scale economics have yet to be demonstrated. Smaller entrants and academic spin-outs target niche segments such as biosurfactants, specialty enzymes, and rare amino acids, leveraging strain engineering and process optimization to compete on performance rather than cost.

Technology adoption patterns reveal a bifurcation between commodity fermentation, where cost leadership and scale drive competitive advantage, and specialty fermentation, where intellectual property around strains, processes, and applications creates defensible positions. Evonik's BioMilk platform, which uses yeast to biosynthesize tropane alkaloids, demonstrates how fermentation can de-risk supply chains dependent on agricultural inputs and create proprietary positions through process patents. Ajinomoto's EUR 150 million investment in Belgium during 2024 to expand specialty amino acid capacity reflects a strategy of moving up the value curve toward pharmaceutical-grade molecules with higher margins and switching costs. Contract fermentation operators, such as Lonza's CDMO services, enable smaller pharmaceutical and biotech companies to access fermentation capacity without capital investment, creating a parallel competitive dynamic where flexibility and regulatory compliance substitute for scale.

Europe Fermented Ingredients Industry Leaders

-

Cargill, Incorporated

-

Döhler GmbH

-

DuPont

-

BASF SE

-

DSM‑Firmenich

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Commercial-scale buildout and conversion of existing sites is opening room for fermented and precision-fermented ingredients across foods, specialty proteins, and functional molecules, especially where manufacturers are looking for cleaner labels or more regionalized supply. In April 2026, FERM FOOD acquired Orkla's former site in Skovlund, Denmark, and positioned it to add up to 20,000 tonnes per year of solid-state fermentation capacity, indicating continued investment in European manufacturing footprints that can support food and ingredient customers with shorter lead times.

Novel Food progress and targeted funding are also shaping where adoption can accelerate once regulatory clearance and scale are in place. In June 2026, The Protein Brewery reported EU Novel Food approval for its mycelium-based Fermotein alongside an EUR 18 million Series B extension, showing how regulatory and financing steps can take novel fermentation-derived ingredients into broader commercial deployment after EFSA and EU processes. In June 2026, Solar Foods secured an EUR 77.8 million funding package under the EU IPCEI program for Factory 02 tied to large-scale Solein production, reinforcing how public funding programs can speed capacity build-out for new fermentation-based ingredient categories. These developments sit alongside ongoing demand in established Europe segments for fermented acids, enzymes, amino acids, and cultures used in reformulation, preservation, and functional positioning.

Recent Industry Developments

- June 2026: The Protein Brewery secured EU Novel Food approval for its mycelium-based Fermotein ingredient and closed an EUR 18 million Series B extension. The combination of regulatory clearance and fresh capital moves the company from development and trials into broader commercialization, raising competitive intensity in fermentation-derived alternative protein ingredients for European formulators.

- April 2026: FERM FOOD acquired Orkla's former site in Skovlund, Denmark, with the expansion positioned to add up to 20,000 tonnes per year of solid-state fermentation capacity (effective 1 April 2026). The site acquisition strengthens regional supply options for fermented ingredients and highlights the use of brownfield assets to accelerate capacity additions versus greenfield build timelines.

- February 2024: Superbrewed Food partnered with Doehler to bring its postbiotic protein to the food and beverage industry, building a route to European scale-up using an established ingredient manufacturer. The collaboration lowered commercialization friction by tying novel ingredient development to existing processing, formulation, and go-to-market capabilities within Europe.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers fermented ingredients sold into end use industries across Europe, where bacteria, yeasts, or molds are used to produce functional ingredients such as acids, amino acids, vitamins, enzymes, and culture based ingredients used in formulations.

Scope exclusions: This sizing excludes finished fermented foods and beverages sold at retail, and it counts only the ingredient value rather than the packaged end product value.

Segmentation Overview

-

By Ingredient Type

- Amino Acids

- Organic Acids

- Vitamins

- Industrial Enzymes

- Probiotics / Starter Cultures

- Polymers

- Antibiotics

- Others

-

By Form

- Liquid

- Dry / Powder

-

By Application

- Food and Beverages

- Pharmaceuticals

- Animal Feed

- Cosmetics and Personal Care

- Biofuel

- Other Applications

-

By Geography

- United Kingdom

- Germany

- France

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a fact base on fermentation related output and demand signals in Europe, and then mapping where those signals flow into ingredient consumption. We mainly used public sources such as Eurostat for production and trade series, FAOSTAT for agriculture inputs that link to feed and food processing, and EFSA publications for safety opinions that influence permitted uses.

To keep the model anchored, we also reviewed sources such as the European Commission food and bioeconomy updates, national statistical offices in major European economies, and peer reviewed journals covering industrial biotechnology and fermentation yields. Company annual reports, investor decks, and press releases were used to validate capacity additions, product focus, and pricing commentary. For stitching company level context into the market model, our analysts also referenced paid subscriptions focused on company financials, patent landscapes, and shipment level trade statistics. These sources are indicative and not exhaustive, and many other public documents and references were checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on checking what is actually sold as a fermented ingredient in Europe and how pricing moves by form and application. We spoke with a mix of ingredient manufacturers, distributors, and downstream formulators across APAC, EMEA, and the Americas to validate demand drivers, typical contract structures, and the realism of volume and ASP assumptions used in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | |

| Mid tier: 46% | Functional/Unit leaders: 31% | |

| Smaller Players: 18% | Managers: 57% |

Market-Sizing & Forecasting

Our sizing starts from a top-down build where European demand pools are reconstructed using a mix of food and feed output indicators, fermentation intensive application shares, and trade flows for relevant ingredient families, which is then converted into value through observed pricing bands. The totals are then cross checked with selective bottom-up approximations, such as rolling up a sample of supplier revenues by fermented ingredient lines, distributor channel checks, and volume times ASP sanity checks for a few high weight categories.

Key inputs used in the model include reported output of processed foods and animal feed, application penetration of culture based ingredients and industrial enzymes, import export movement for organic acids and similar intermediates, observed form mix shifts between liquid and dry, and capacity utilization direction from producer commentary. Pricing is treated carefully because ASPs can move with energy costs, sugar and starch inputs, and contract timing, so we use a blended ASP approach that is refreshed by year and tested against interview feedback.

For forecasting, scenario analysis is used around a central case, where growth drivers like clean label reformulation, probiotics and culture adoption, and bio based ingredient substitution are stress tested against downside cases like slower industrial activity or input cost spikes. Where bottom-up coverage is incomplete, gaps are handled through share based extrapolation using application weights and country level consumption indicators, and then rechecked for plausibility against trade and production signals.

Data Validation & Update Cycle

Model outputs are validated through multiple checks so obvious overcounts and undercounts are caught early, and the math stays tied to real world signals. We compare the final market totals against independent indicators such as country level production trends, trade balances for relevant ingredient families, and the implied per unit ingredient intensity in key end uses.

Variance checks are run by country, by ingredient family, and by application so unusual swings are flagged and reviewed before sign off. If a major capacity change, regulation shift, or sustained pricing movement is identified, assumptions are rechecked and experts may be recontacted to confirm direction and timing. The report is refreshed annually, and before delivery a final analyst pass is done so clients receive the most current view based on the latest available data.

Mordor Intelligence's Europe Fermented Ingredient Market Size Compared With Other Published Estimates

Different published market values for Europe fermented ingredients can vary even when the same words are used, because the scope boundary is often interpreted differently and the pricing year can shift the result. Gaps also come from whether the estimate counts only ingredient sales or mixes in some finished product value, and whether trade and production signals are used as hard constraints.

A practical driver of spread is the refresh cadence and currency timing used for annual pricing, especially when input costs move and contracts reset at different points in the year. In this study, the ASP blend and FX conversion are refreshed on a current year calendar basis and revalidated against producer and buyer checks, which helps explain why the USD 10.21 B (2025) number can differ from figures shown elsewhere, a choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.21 B (2025) | |

| Industry Publisher A | USD 8.15 B (2024) | Uses an earlier pricing year and may apply broader process based groupings that can miss Europe specific form mix and application intensity shifts, leading to lower value when ASPs rise. |

| Consultancy B | USD 15.76 B (2025) | Likely applies a wider inclusion set across adjacent fermented inputs and uses a longer horizon projection structure, which can lift the 2025 value if category boundaries and average pricing assumptions are expanded. |

The table shows that timing and scope choices can move the headline number materially, even before any forecasting differences are considered. By keeping the ingredient only boundary clear, updating ASP and FX assumptions on a consistent calendar basis, and running trade and demand signal checks, the estimate remains traceable to inputs that can be reviewed and repeated.

Key Questions Answered in the Report

How large is the Europe fermented ingredients market in 2026?

The Europe fermented ingredients market size stands at USD 11.11 billion in 2026.

What CAGR is expected for fermented ingredients in Europe through 2031?

Revenue is forecast to rise at an 8.82% CAGR, reaching USD 16.96 billion by 2031.

Which ingredient type leads revenue today?

Amino acids command 43.58% of revenue, reflecting entrenched demand in feed and pharma.

Page last updated on: