Algae Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.77 Billion |

| Market Size (2031) | USD 10.43 Billion |

| Growth Rate (2026 - 2031) | 9.04% CAGR |

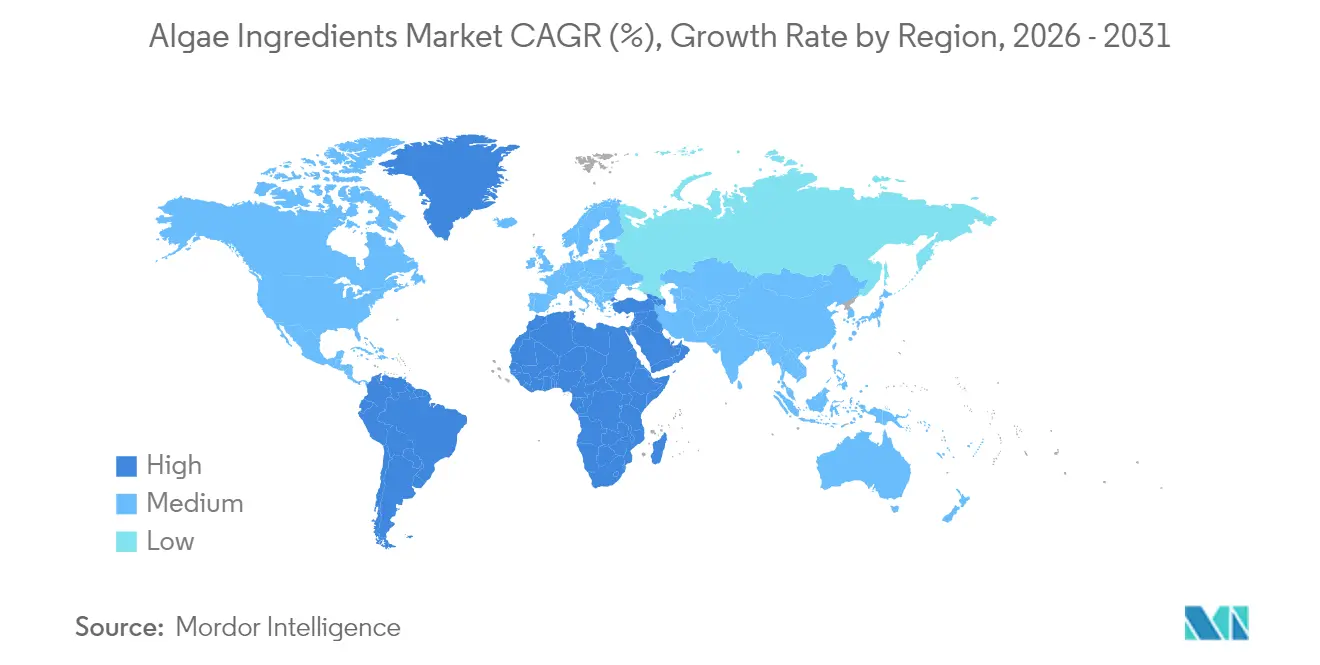

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Algae Ingredients Market Analysis by Mordor Intelligence

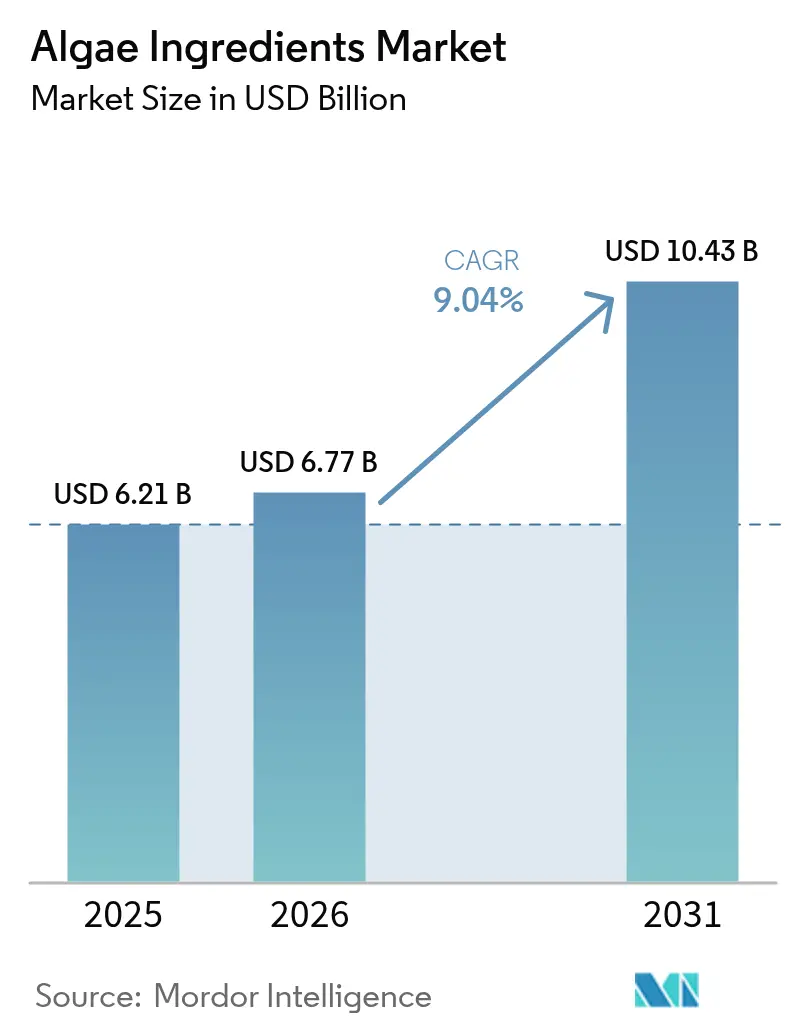

Algae ingredients market size in 2026 is estimated at USD 6.77 billion, growing from 2025 value of USD 6.21 billion with 2031 projections showing USD 10.43 billion, growing at 9.04% CAGR over 2026-2031. Manufacturers are adopting vertically integrated bioprocessing platforms to reduce production costs and ensure a contaminant-free supply. Food, beverage, and pharmaceutical companies value algae's clean-label properties and consistent nutrient content. The Asia-Pacific region maintains its market leadership due to established aquaculture infrastructure and efficient manufacturing capabilities. The Middle East and Africa region shows significant growth potential as investments in the blue economy increase. The market remains competitive as mid-sized companies establish niche positions through strain development, while large companies focus on omega-3 applications and form strategic partnerships to expand their market presence.

Key Report Takeaways

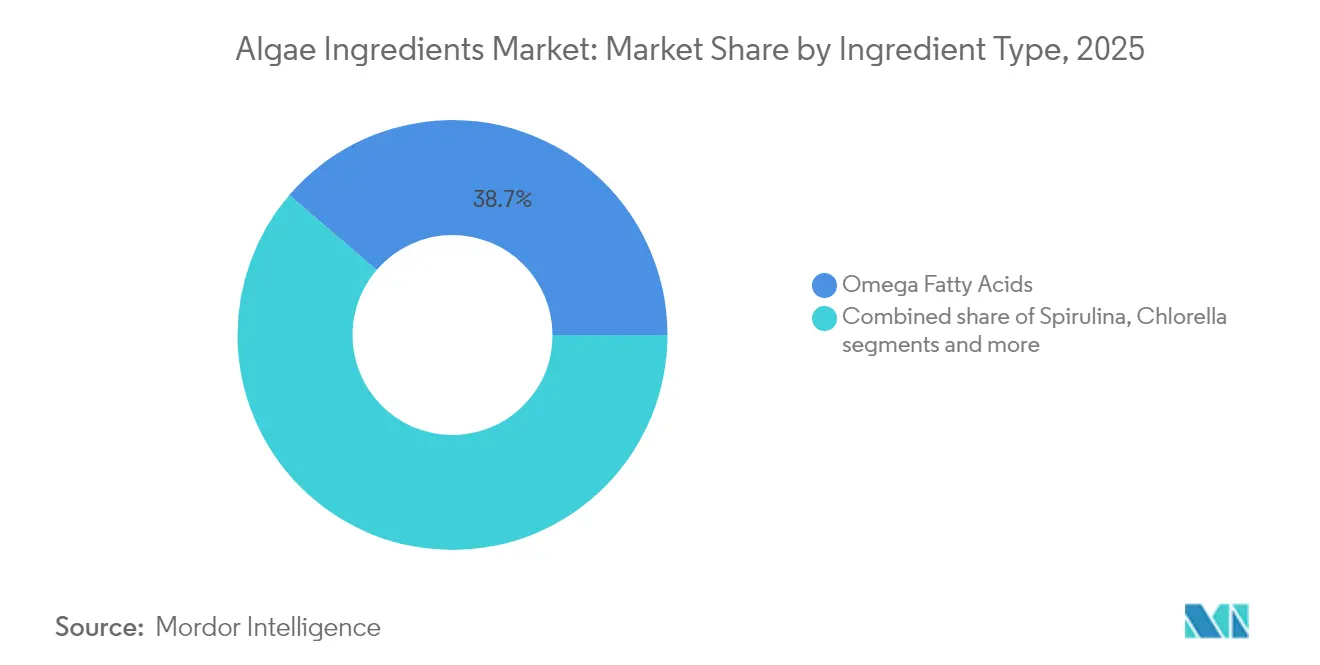

- By ingredient type, omega fatty acids held 38.72% of the algae ingredients market share in 2025 and are projected to advance at an 11.18% CAGR from 2026-2031.

- By source, brown algae commanded 56.82% revenue share of the algae ingredients market in 2025, whereas green algae are set to register the fastest growth at a 10.55% CAGR through 2031.

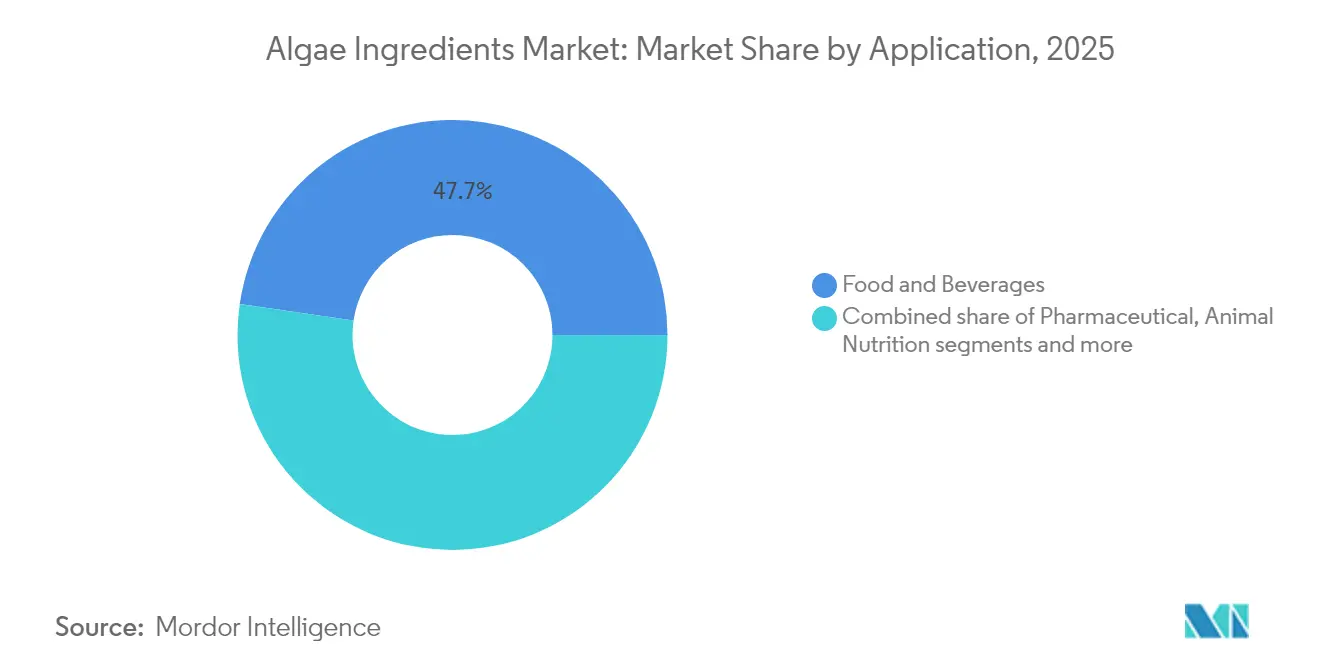

- By application, food and beverages contributed 47.69% of the global algae ingredients market size in 2025, but pharmaceutical uses are forecast to expand most rapidly at an 11.12% CAGR to 2031.

- By region, Asia-Pacific dominated with a 41.88% share of the algae ingredients market in 2025; Middle East and Africa is poised for the quickest growth at a 11.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Algae Ingredients Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nutritional Benefits of Algae-Derived Products | +1.8% | Global, with premium markets in North America and Europe | Medium term (2-4 years) |

| Biotechnology and Cultivation Advancements | +2.1% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Increase Use of Algae in Animal Nutrition | +1.5% | Global, concentrated in aquaculture regions | Short term (≤ 2 years) |

| Consumer Awareness About Health Benefits of Omega-3 | +1.2% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growing Demand from the Cosmetics Industry | +0.9% | Global, led by premium markets | Medium term (2-4 years) |

| Inclination Towards Natural Food Additives | +1.3% | Europe and North America, spreading globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Nutritional Benefits of Algae-Derived Products

Algae ingredients provide higher bioavailability and concentration of essential nutrients compared to conventional sources, making them effective alternatives in functional foods and dietary supplements. The enhanced nutrient absorption and concentrated delivery mechanisms make algae-based ingredients particularly valuable for manufacturers and consumers. The FDA's GRAS Notice 1185 for DHA-rich oil from Schizochytrium sp. validates its safety for infant formulas and general foods, allowing consumption of up to 1.5 grams of DHA per person daily [1]Source: U.S. Food and Drug Administration, “GRAS Notice No. 1185 for DHA-Rich Oil from Schizochytrium sp.,” www.fda.gov. This regulatory approval strengthens market confidence and expands application possibilities across various food categories. The nutritional benefits enable premium pricing and market differentiation, as demonstrated by DSM-Firmenich's life'sDHA® B54-0100, which contains 545 mg of pure DHA per gram, allowing for smaller capsules and efficient formulations. The high concentration of DHA in these products reduces manufacturing costs and improves product development flexibility for food and supplement manufacturers.

Biotechnology and Cultivation Advancements

Innovations in photobioreactors and genetic engineering are transforming algae production by improving productivity and enabling commercial viability. Advanced cultivation systems with automated monitoring and precise controls enhance biomass yields and product quality. In May 2025, BGG doubled astaxanthin production capacity in Yunnan Province, reducing carbon emissions through efficiency and renewable energy. The facility uses advanced photobioreactors, harvesting techniques, AI, and data analytics to optimize strain selection and growth conditions. BASF's research into micro-algae for bio-based chemicals highlights integrated biorefinery models, diversifying product streams like biofuels, nutritional supplements, and specialty chemicals.

Increase Use of Algae in Animal Nutrition

Marine microalgae have received FDA approval as a DHA source for adult dog food, while NOAA has greenlit taurine from marine red algae for carnivorous fish feed. These regulatory nods pave the way for wider use of algae ingredients in aquaculture, livestock, and pet food sectors. These ingredients not only boost animal performance but also meet pressing sustainability goals. With this regulatory backing, manufacturers are empowered to craft innovative feed solutions that balance nutrition with environmental responsibility. The USDA's Coast to Cow to Consumer project is exploring marine algae in boosting milk production and curbing greenhouse gas emissions. This suggests algae's potential extends beyond aquaculture, reaching into terrestrial livestock. Such research underscores the adaptability of algae-based ingredients in diverse animal feed markets, setting the stage for future growth and sustainable feed innovations.

Consumer Awareness About Health Benefits of Omega-3

Scientific evidence and regulatory validations have heightened consumer awareness of omega-3 benefits, particularly from sustainable algal sources that address marine contamination concerns. These sources offer a viable alternative to fish-based omega-3s, eliminating pollution and sustainability issues. Research confirms the bioavailability and effectiveness of algal omega-3s, appealing to health-conscious consumers. In 2024, Korea Eundan transitioned from fish oil to algal omega-3 products, aligning with industry trends toward plant-based and sustainable options. The FDA's review highlights the safety and efficacy of prescription algal omega-3s, strengthening their position in pharmaceutical and supplement markets and driving adoption by manufacturers and healthcare providers.

Restraints Impact Analysis of Algae Ingredients Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production and Processing Cost | -2.3% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Seasonal and Environmental Sensitivity | -1.1% | Regions dependent on outdoor cultivation | Medium term (2-4 years) |

| Lack of Standardization in Algae-Based Ingredients | -0.8% | Global, regulatory fragmentation | Short term (≤ 2 years) |

| Contamination Risk and Safety Concern | -1.2% | Global, heightened in developing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production and Processing Cost

Algae cultivation for high-value ingredients like omega-3 fatty acids, proteins, and pigments (astaxanthin and beta-carotene) requires controlled environments, such as photobioreactors or open ponds, which demand significant capital investment. Precise control of temperature, light, CO₂ levels, and nutrients, along with continuous monitoring to prevent contamination, increases production costs compared to traditional crops and synthetic alternatives. Post-cultivation, harvesting, drying, and compound extraction involve costly processes like bead milling, sonication, supercritical CO₂ extraction, and solvent-based techniques, requiring expensive solvents, high energy input, and specialized equipment. Purifying the final ingredient to food-grade or pharmaceutical-grade standards involves multiple energy-intensive steps, resulting in high unit costs.

Contamination Risk and Safety Concern

As climate change progresses, the CDC reports an increase in the frequency and severity of harmful algal blooms. These blooms, caused by cyanobacteria, release toxins like microcystins, anatoxins, and cylindrospermopsins, which can harm human and animal health by causing liver damage, neurological issues, and respiratory problems [2]Source: Centers for Disease Control and Prevention, “Harmful Algal Bloom (HAB) Associated Illness,” www.cdc.gov. The FDA addresses these risks by regularly testing blue-green algae dietary supplements for microcystin contamination. Products exceeding safety limits are promptly recalled, and public safety notifications are issued. This oversight necessitates stringent quality assurance across the supply chain, including advanced testing, detailed documentation, and preventive controls. Regular employee training, environmental monitoring, and third-party testing further enhance safety and compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Algae Ingredients Market Segment Analysis

By Ingredient Type:

Omega Fatty Acids Drive InnovationOmega Fatty Acids command a 38.72% market share in 2025 and exhibit an 11.18% CAGR through 2031. This growth stems from their established market position and improvements in algal-derived EPA and DHA formulations. The continuous research and development in extraction technologies have enhanced the quality and bioavailability of these fatty acids, making them more appealing to manufacturers. Carrageenan and Alginate serve distinct functions in food texturing and pharmaceutical applications, offering versatile solutions for product formulation and stability. Carotenoids gain traction in cosmetics and nutraceuticals through enhanced extraction techniques, with manufacturers focusing on improving yield and purity levels.

BGG expanded its facility to double the production of Certified Organic Haematococcus pluvialis astaxanthin, addressing rising demand for natural antioxidants. This reflects growing consumer preference for natural ingredients and sustainable production. FDA approvals for algae-based color additives boost growth by expanding applications in food, beverages, and dietary supplements. The market's demand for omega fatty acids remains strong, driven by documented health benefits and regulatory support. Clinical research on their cardiovascular and cognitive benefits further drives adoption. Additionally, beta-glucans from Euglena gracilis show potential in immune and metabolic health applications.

By Source:

Brown Algae Dominance ChallengedBrown Algae accounts for 56.82% of the market share in 2025, while Green Algae demonstrates a higher growth rate at 10.55% CAGR through 2031. The market distribution reflects the economic factors of cultivation methods and application effectiveness across industries. This distribution pattern indicates a significant shift in market dynamics, where traditional dominance meets emerging technological capabilities. The varying growth rates between species highlight the evolving nature of the seaweed industry and its adaptation to changing market demands.

Brown algae maintain their market leadership through established infrastructure and processing facilities, supported by robust supply chains. Green algae's growth trajectory is attributed to its adaptability to controlled cultivation environments and potential for genetic enhancement. The industry continues to prioritize environmental sustainability in seaweed farming operations, maintaining a balance between ecological preservation and production demands. The cultivation methods for both species differ significantly, with brown algae benefiting from traditional open-water farming techniques, while green algae excel in modern, controlled environments. These distinct characteristics influence their market positions and future growth potential in various applications across food, pharmaceutical, and industrial sectors.

By Application:

Pharmaceutical Growth AcceleratesFood and Beverages applications maintain a commanding 47.69% market share in 2025, reflecting the industry's strong presence in traditional food products and innovative formulations. The Pharmaceutical segment demonstrates robust growth potential with a projected 11.12% CAGR through 2031, driven by increasing therapeutic applications and regulatory approvals for medical nutrition products. This growth is exemplified by the European Commission's approval of Kemin Industries' BetaVia Pure, which secured a five-year exclusivity period for Euglena gracilis-derived postbiotics, marking a significant advancement in pharmaceutical applications.

GreenCoLab's product showcase at Vitafoods Europe 2024 includes a comprehensive range of algae-based products such as caviar alternatives, craft beer, and plant-based burgers. The company's product portfolio demonstrates the broad versatility of algae-based ingredients across multiple food applications, from premium luxury items to everyday consumer products. The successful integration of algae ingredients into diverse food categories indicates their potential to transform conventional food manufacturing processes while meeting consumer preferences for sustainable alternatives.

Geography Analysis

APAC Algae Ingredients Market

In 2025, Asia-Pacific holds a 41.88% market share, driven by its strong aquaculture sector, manufacturing capabilities, and established seaweed cultivation infrastructure. Growing consumer acceptance of algae-based products and China's demand for fishmeal alternatives, as noted in the FAO's 2024 fisheries report, further strengthens the region's position . The Asia-Pacific Aquaculture 2024 conference highlights algae's role in the blue economy. Integrated supply chains, government support, and advancements in cultivation technologies by Japan and Australia, along with India's spirulina trials targeting malnutrition, showcase the region's market leadership.

MEA Algae Ingredients Market

The Middle East and Africa region projects the highest growth rate at 11.65% CAGR through 2031. This growth stems from comprehensive sustainability programs and strategic blue economy investments, particularly Saudi Arabia's large-scale regenerative aquaculture initiatives. The African continent presents substantial opportunities in coastal cultivation and directly addresses regional food security needs. However, the market growth in these regions remains dependent on the development of essential infrastructure, including processing facilities, transportation networks, and storage capabilities.

North America and Europe Algae Ingredients Market

North America and Europe maintain strong market positions through their focus on premium applications and comprehensive regulatory frameworks. European regulations provide detailed guidelines for macroalgae products across multiple categories, including medicinal applications, food supplements, and agricultural fertilizers. The CEN/TC 454 standardization efforts enhance market access by implementing unified standards across member states. These regions establish global benchmarks for product safety and effectiveness through rigorous testing protocols and quality control measures, influencing international market practices and standards.

Regulatory Landscape

Regulation for algae ingredients is shaped by food-safety approvals, novel food pathways, and contaminant control across major markets. In the European Union, the novel food framework and EFSA assessments act as key gateways for new microalgae-derived ingredients. The European Commission authorized beta-glucan from Euglena gracilis as a novel food in April 2024 (Implementing Regulation (EU) 2024/1046), while EFSA issued a negative-type conclusion in April 2025 for dried biomass powder of Chlamydomonas reinhardtii THN 6 due to insufficient data. EFSA also concluded in December 2025 that algal meal from Haematococcus pluvialis containing astaxanthin is safe for certain new uses under specified conditions, and the European Commission updated specifications for astaxanthin-rich oleoresin from H. pluvialis in April 2024 (Implementing Regulation (EU) 2024/1026), underscoring the importance of specifications, intake limits, and compositional controls.

In the United States, algae ingredients commonly rely on GRAS determinations and ingredient-specific clearances, supported by the FDA GRAS Notice Inventory as a public reference point for evaluated substances (including algal-derived DHA oils). FDA oversight also extends to safety monitoring for contaminants, including testing focus areas for algae-based supplements where toxin contamination is a concern. A compliance inflection point is the FDA Human Foods Program 2026 priority deliverable to publish a proposed rule to require mandatory submission of GRAS notices for new substances claimed to be GRAS. If finalized, this would shift the current voluntary notification dynamic and raise the bar for dossier readiness, traceability, and safety substantiation for new algae-derived ingredients entering the US market.

Value Chain Analysis

The algae ingredients value chain spans strain or species selection (microalgae strains and macroalgae species), cultivation (open ponds, photobioreactors, or fermentation-based systems), harvesting and dewatering, drying or stabilization, and downstream extraction or purification (oils, pigments, hydrocolloids) to meet food, nutraceutical, feed, personal care, and pharmaceutical specifications. Manufacturers increasingly pursue vertically integrated bioprocessing to control contamination risk, standardize quality, and reduce unit costs, while buyers focus on consistent nutrient content, sensory performance, and documentation for regulatory and customer audits.

Processing and commercialization are closely tied to regulatory and application gatekeepers, with EFSA opinions and EU authorizations determining route-to-market timing for novel microalgae ingredients and colorants. Recent industry moves point to more proprietary fermentation and higher-value formulations influencing both upstream and downstream nodes. Fermentalg introduced a solvent-free fermentation omega-3 platform with a high-EPA algae oil (Omega Origins) in May 2026, while Checkerspot scaled fermentation-derived omega-7 POA oil to a higher concentration in April 2026 to address ingredient supply constraints. Consolidation is also reshaping supply reliability and portfolios, as seen in May 2026 when Euglena acquired Kobelco Eco-Solutions microalgae business assets, including cultivation assets for Euglena gracilis EOD-1, to tighten control over cultivation capacity, know-how, and branded supplement channels.

Competitive Landscape

The algae ingredients market maintains a moderate fragmentation, creating opportunities for strategic consolidation while fostering competition that drives innovation and pricing efficiency. Market leaders maintain their positions through vertical integration and technological capabilities, particularly in production optimization and quality control. DSM-Firmenich's strategic focus on algal omega-3 oils demonstrates the industry's shift toward high-value, sustainable ingredients, while other companies invest in specialized product development and market expansion initiatives.

Companies compete through biotechnology advancement, regulatory compliance, and supply chain integration, with significant investments in photobioreactor technologies and strain optimization to reduce costs. Advanced cultivation methods, including closed-system technologies and automated monitoring systems, enable improved yield and product consistency. The merger between Cellana and PhytoSmart reflects the industry's consolidation trend, combining cultivation expertise with market access capabilities to strengthen market presence and distribution networks. New opportunities emerge in applications such as precision fermentation for food ingredients, where developments in synthetic biology influence market dynamics.

The integration of artificial intelligence and machine learning in production processes further enhances operational efficiency. Companies with strong R&D capabilities and regulatory expertise gain competitive advantages, as shown by DSM-Firmenich's extensive patent portfolio in algal omega-3 production and bioprocessing technologies. Market participants also focus on developing sustainable production methods and establishing strategic partnerships across the value chain to secure raw material supply and enhance market reach.

Algae Ingredients Industry Leaders

DSM-Firmenich

Archer Daniels Midland Company

BASF SE

Cargill Inc.

Corbion N.V.

- *Disclaimer: Major Players sorted in no particular order

Algae Ingredients Market Companies Covered in this Report

- DSM-Firmenich AG

- Cargill Inc.

- Corbion N.V.

- BASF SE

- Archer Daniels Midland Company (ADM)

- Cyanotech Corporation

- Fuji Chemical Industries Co. Ltd.

- Aliga Microalgae A/S

- Allmicroalgae (Secil Group)

- DIC Corp.(Earthrise Nutritionals)

- Roquette Frères

- Dupont-IFF (Danisco)

- Evonik Industries AG

- Fermentalg SA

- Parry Nutraceuticals (Murugappa)

- Solabia Group

- Cellana Inc.

- Alltech Inc.

- Syngenta Group

- Qingdao Seawin Biotech

Market Opportunities and Future Outlook

Opportunities are expanding where regulatory clearances and targeted functionality open new formulation space beyond commodity algae biomass. In the EU, the April 2024 authorization of beta-glucan from Euglena gracilis as a novel food, with a five-year exclusivity period linked to Kemin Foods L.C. from April 30, 2024, shows how differentiated microalgae-derived actives can be monetized with robust dossiers. In the United States, the June 2025 FDA authorization of galdieria extract blue across multiple food categories strengthens the commercial case for microalgae-based color systems in beverages and desserts, supporting product developers looking for natural alternatives with more predictable supply than crop-based botanicals.

Capacity buildouts and technology choices also indicate where scaling activity is concentrating, especially in high-value pigments and omega lipids. In May 2026, the second phase of a spirulina cultivation project in Vietnam was scheduled to add 360 tonnes annually to reach 600 tonnes of capacity, pointing to continued upstream investment at commercial scale in Asia. In July 2026, Pinnacle Food Group Limited commenced construction of a commercial-scale microalgae-based astaxanthin facility in Canada, reinforcing a North American pathway for localized pigment supply. Alongside these buildouts, smart-farming upgrades for spirulina and modular production approaches are being used to improve consistency and reduce operational friction (energy, water handling, and quality variability), supporting adoption across food, nutraceutical, and animal nutrition applications where specification control and traceability drive supplier selection.

Recent Industry Developments in Algae Ingredients Market

- June 2026: Corbion published an updated life cycle assessment (LCA) for its algae-derived omega-3 DHA portfolio, reporting an 18-23% lower climate change impact versus its 2021 assessment. The update strengthens sustainability documentation that buyers use in ESG screening and tendering, and it supports algae-based DHA positioning against marine and alternative lipid sources.

- March 2025: DIC Corporation's US subsidiary Earthrise Nutritionals began operations at a new edible algae cultivation facility in California focused on spirulina, incorporating sustainable smart-farming practices. The added cultivation footprint improves supply assurance for spirulina-based ingredients and supports tighter process control for food-grade specifications.

- November 2024: Microphyt launched ZenGut, a microalgae ingredient positioned for mood and gut health applications, extracted from the Tetradesmus obliquus MI 175.B1a strain. The launch highlights continued product development in application-specific microalgae ingredients, reinforcing differentiation through strain selection and targeted health positioning.

Algae Ingredients Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the algae ingredients market covers ingredients made from microalgae and macroalgae that are processed and sold as inputs, such as powders, extracts, oils, pigments, and hydrocolloids, to manufacturers in food, nutraceutical, feed, personal care, and pharma.

Scope exclusions: We exclude finished consumer products, algae biofuels, fertilizer-grade biomass, and industrial algae chemicals that are not intended for human or animal consumption.

Segments Covered in This Report

- By Ingredient Type

- Spirulina

- Chlorella

- Omega Fatty Acids

- Carageenan

- Alginate

- Caretonoids

- Other Ingredient Type

- By Source

- Red Algae

- Green Algae

- Brown Algae

- By Application

- Food and Beverages

- Pharmaceutical

- Animal Nutrition

- Personal Care and Cosmetics

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- United Kingdom

- Germany

- Spain

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping what is being produced, traded, and regulated, then translating that into an ingredient demand pool that can be modeled. We refer to public sources such as FAO datasets, UN Comtrade trade statistics, USDA and EU agriculture and food publications, Codex Alimentarius and related national food-safety standards, and peer-reviewed journals on algal cultivation yields and extraction pathways.

To anchor the commercial side, we also review company annual reports, investor presentations, product specification sheets, association and conference publications, and credible press coverage of capacity additions and new applications. In addition, paid subscriptions we hold for company financial intelligence, patent databases, and shipment-level import and export data are used selectively to cross-check pricing ranges and trade flows when public series are incomplete. The sources listed here are illustrative only, and many other documents are reviewed to collect, validate, and clarify market assumptions.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions that matter most, especially what is counted as an ingredient sale versus internal use or a finished product. We speak with a mix of ingredient suppliers, processors, distributors, and downstream formulators, and we cover demand signals across APAC, EMEA, and the Americas so regional mix and pricing logic can be checked in a consistent way.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 12% | APAC: 49% |

| Mid tier: 48% | Functional/Unit leaders: 34% | EMEA: 33% |

| Smaller Players: 19% | Managers: 54% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand reconstruction, where end-use output indicators are converted into algae-ingredient consumption through penetration rates and dosage or inclusion assumptions, then valued using realistic transfer prices. The model is checked with selective bottom-up approximations, such as supplier revenue sampling, trade flow checks for key ingredient lines, and volume multiplied by average selling price for a few well-covered categories. This helps adjust totals when one signal looks overstated.

Inputs that typically move the number include cultivation and extraction capacity additions, yield and conversion factors from biomass to ingredient, price ranges by ingredient class, regional adoption in food and dietary supplements, and feed inclusion trends tied to aquaculture expansion. Where direct volume data is patchy, gaps are handled through proxy variables, for example import dependence, application mix shifts, and reported utilization ranges, and then re-tested through primary discussions.

For forecasting, scenario analysis is used so different adoption speeds and pricing paths translate into a realistic base case, followed by a light regression check on macro drivers such as income growth, supplement spend, and aquaculture output. Assumptions are kept simple and repeatable, and they are only moved when more than one signal supports the change.

Data Validation & Update Cycle

Outputs are validated by comparing final market totals with independent signals such as trade balances, known capacity announcements, and typical ingredient price bands, then reviewing any large variances at the region and application level. If a result looks inconsistent, the drivers are re-opened, the assumptions are rechecked, and the relevant experts are contacted again to confirm what changed.

Before sign-off, the model goes through a multi-step analyst review so arithmetic, unit conversions, and price application stay consistent across countries and years. Reports are refreshed annually, and interim updates are added when material events occur, such as major capacity ramp-ups, demand shocks, or regulatory changes. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Algae Ingredients Market Size Compared Against Other Published Estimates

Published market sizes for algae ingredients can look far apart because the underlying scope and pricing point are not always the same, even when the titles sound similar. Differences usually come from what gets counted as an ingredient sale, which algae sources are included, and how pricing and regional mix are treated in the base year.

Some estimates expand the universe by adding biofuel and bioenergy uses or by counting finished supplements and packaged foods that contain algae. In Mordor Intelligence, the value is kept at ingredient transfer price and it is limited to algae-derived powders, oils, hydrocolloids, pigments, and concentrates sold into food, nutraceutical, feed, personal care, and pharma, with downstream finished goods excluded.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.77 B (2026) | |

| Industry Publisher A | USD 4.59 B (2026) | Uses a broader definition of factory-gate revenues across algae-based ingredients, but the category mix and timing align to a different base year logic, which can compress the 2026 value versus an ingredient-only transfer-price build. |

| Industry Publisher B | USD 4.50 B (2025) | Uses a different starting year and a wider tent that can include additional production methods and adjacent applications, so the near-term value shifts depending on what is counted as an ingredient versus a downstream product or energy use. |

The table shows that year selection and what is treated as an ingredient sale are the two biggest reasons for the spread in reported values. By keeping scope tied to a clear ingredient demand pool and then cross-checking it with trade, capacity, and price signals, the model stays transparent and can be replicated and updated as the market evolves.

Key Questions Answered in the Report

What is the current algae ingredients market size?

The algae ingredients market is valued at USD 6.77 billion in 2026 and is forecast to reach USD 10.43 billion by 2031.

What is driving the rapid growth of the algae ingredients market?

Strong demand for sustainable omega-3 oils, advances in closed photobioreactor technology that lower costs, and a steady stream of regulatory approvals for food, feed, and pharmaceutical uses are the core drivers behind the projected 9.04% CAGR over 2026-2031.

Which region dominates current sales, and which is growing fastest?

Asia-Pacific leads with 41.88% of 2025 revenue owing to large-scale aquaculture and seaweed farming, while Middle East and Africa is forecast to record the fastest 11.65% CAGR through 2031

Why are omega fatty acids so important in the algae ingredients industry?

Omega fatty acids captured 38.72% of 2025 revenue and are growing at 11.18% CAGR because algal DHA and EPA deliver high bioavailability, vegan compatibility, and freedom from marine contaminants, making them popular in dietary supplements, infant formula, and aquafeed.

Page last updated on: