Hair Wigs And Extensions Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 11.83 Billion |

| Market Size (2030) | USD 21.22 Billion |

| Growth Rate (2025 - 2030) | 12.94% CAGR |

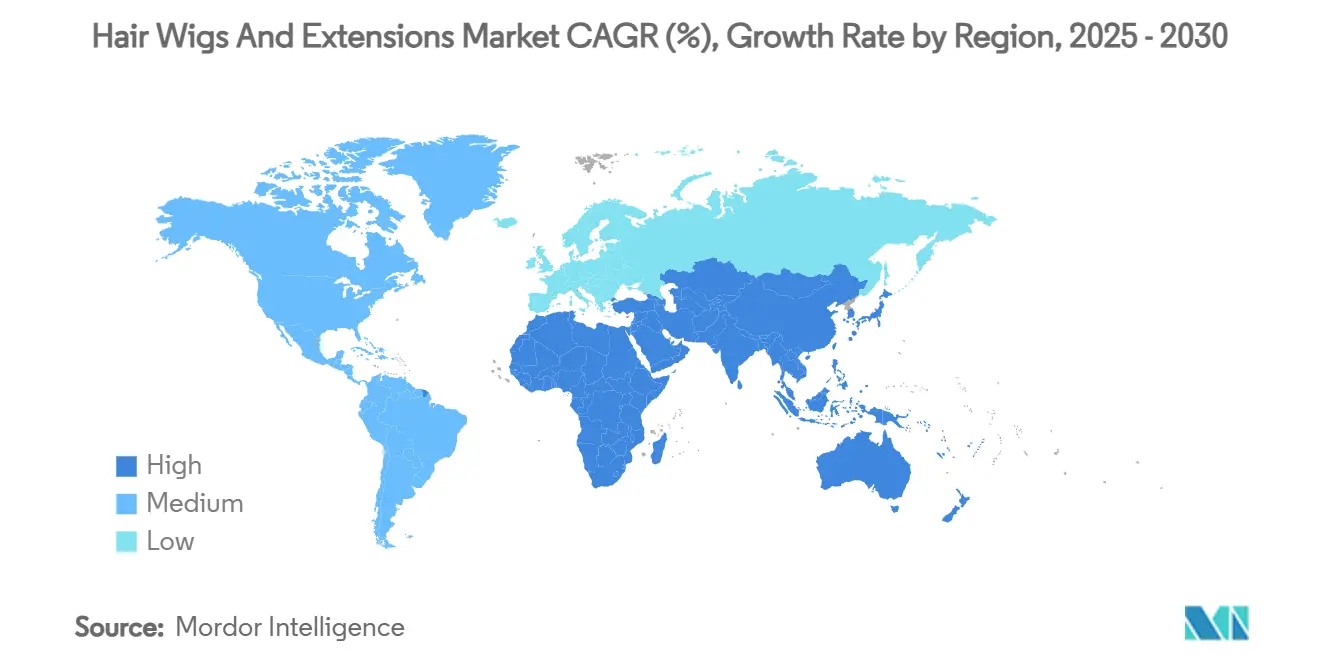

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

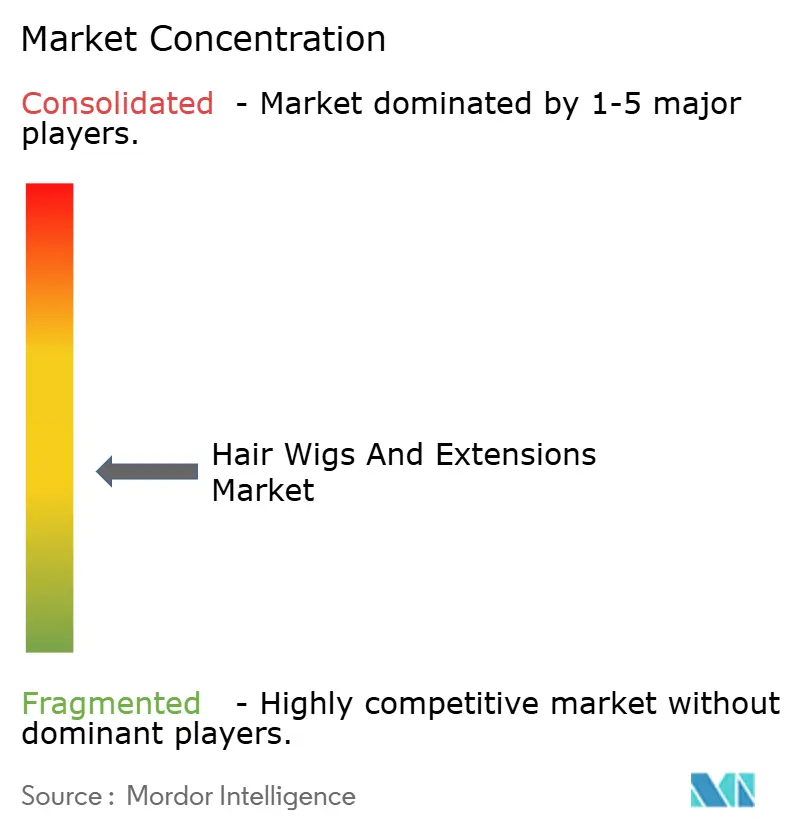

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hair Wigs And Extensions Market Analysis by Mordor Intelligence

The hair wigs and extensions market size is estimated to be USD 11.83 billion in 2025 and is forecast to reach USD 21.22 billion by 2030, reflecting a 12.94% CAGR. Growth is fueled by rising alopecia incidence, social acceptance of hair augmentation, progress in synthetic fiber engineering, and supportive regulatory clarity that recognizes wigs as medical aids in many jurisdictions. Demand also benefits from strong fashion cycles, celebrity influence, and e-commerce convenience, while producers face tariff shocks on Chinese hair imports that are pushing companies to diversify sourcing and accelerate synthetic innovation. Middle East and Africa is the fastest-growing region, yet North America retains the largest revenue contribution because of high disposable income and deep salon networks. Competitive intensity remains moderate: leading brands leverage omnichannel sales and vertical integration, but smaller niche players still secure share through direct-to-consumer strategies and ethical-sourcing narratives.

Key Report Takeaways

- By product type, hair extensions dominated the hair wigs and extensions market with a 64.06% share in 2024 and was expected to grow at a CAGR of 14.12% during 2025-2030..

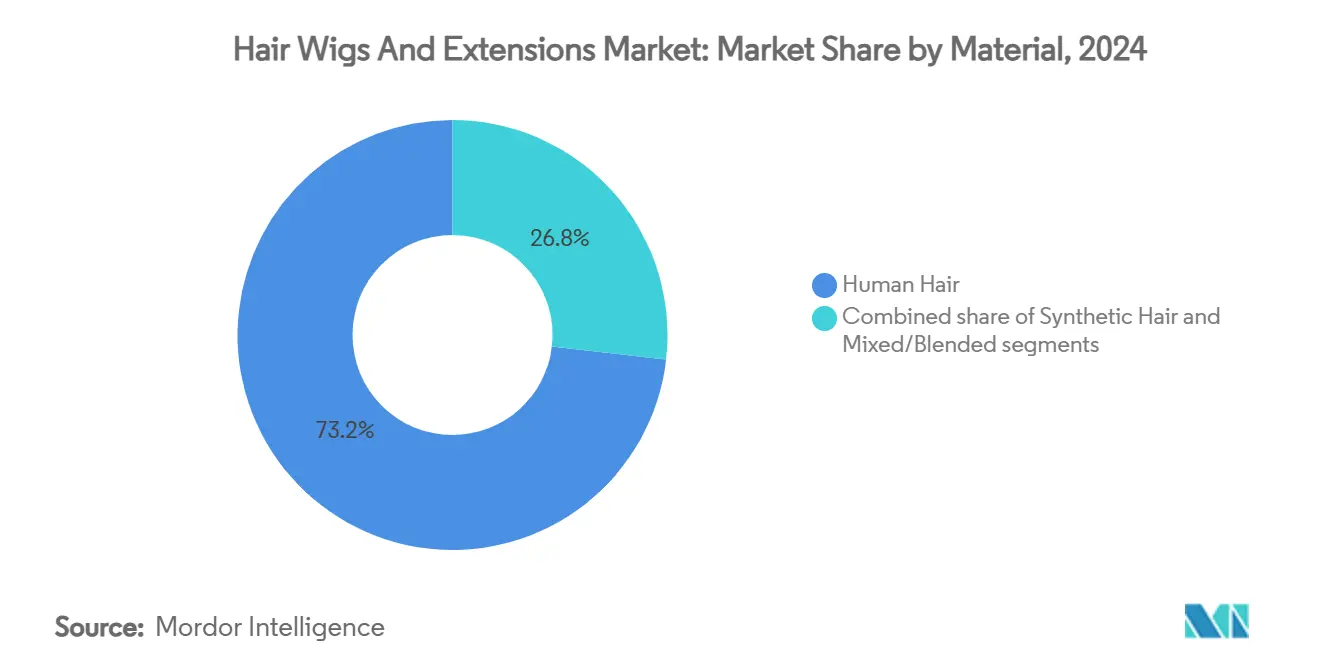

- By material, human hair commanded 73.18% share of the hair wigs and extensions market size in 2024, whereas synthetic hair posted the fastest 14.50% CAGR outlook to 2030.

- By end user, individual consumers generated 68.25% of 2024 revenues; commercial settings are projected to expand at 14.37% CAGR between 2025-2030.

- By gender, female customers captured 82.45% of market share in 2024, yet the male segment is forecast for a 14.83% CAGR through 2030.

- By distribution channel, offline stores controlled 55.75% of 2024 sales, even as online platforms are advancing at a 13.75% CAGR to 2030.

- By geography, North America accounted for 42.62% of 2024 revenue; Middle East and Africa is poised for the highest 13.55% CAGR over the forecast period.

Global Hair Wigs And Extensions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of alopecia and hair-loss disorders | +2.1% | Global, with concentration in North America and Europe | Long term (≥ 4 years) |

| Strong influence from fashion and beauty trends | +2.8% | Global, led by North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Advancements in product technology | +1.9% | Global, with research and development centers in North America and Europe | Long term (≥ 4 years) |

| High demand for personalized wigs and extensions | +1.7% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growing societal acceptance and normalization | +2.3% | Global, accelerating in Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Demand for ethically sourced, traceable human hair | +1.4% | North America and Europe, with supply chain impacts in Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising incidence of alopecia and hair-loss disorders

The increasing prevalence of alopecia and hair-loss conditions creates market opportunities, as more individuals seek solutions for hair loss management. For instance, in 2023, androgenetic alopecia constituted more than 95% of male hair loss cases. According to the American Hair Loss Association, approximately two-thirds of American men face significant hair loss by age 35, with 85% experiencing substantial thinning by age 50. Additionally, 25% of men affected by male pattern baldness begin losing hair before age 21 [1]Source: American Hair Loss Association, "Men’s Hair Loss", americanhairloss.org. This widespread occurrence creates sustained demand for hair replacement solutions across age groups. The market serves individuals affected by various forms of alopecia, including androgenetic, alopecia areata, and traction alopecia, which impact both men and women globally. Major market players like Aderans Co., Ltd., Rebecca Hair Products Co., Ltd., and HairUWear Inc. develop natural-looking and comfortable solutions for both cosmetic and medical purposes. These companies provide products for diverse consumer needs, including individuals undergoing chemotherapy, those with autoimmune conditions, and people experiencing stress-related hair loss. The market growth continues to strengthen through technological advancements, increased awareness, and broader social acceptance of hair replacement solutions.

Strong influence from fashion and beauty trends

The widespread adoption of social media platforms has reshaped consumer behavior in the hair accessories industry. Instagram, TikTok, and YouTube serve as primary channels where users, influencers, and celebrities share diverse hairstyles using wigs and extensions, creating widespread trends that reach global audiences rapidly. The market has evolved beyond its traditional focus on hair loss solutions to include fashion-oriented consumers seeking temporary style changes in length, volume, and color. For instance, companies like Luxy Hair, Mayvenn Inc., and Glam Seamless utilize social media marketing through tutorials and influencer collaborations to demonstrate the accessibility of their products. Additionally, technological advancements in "invisible" and seamless extension applications address consumer demands for natural-looking, flexible styling options. Celebrity appearances featuring hair extensions have normalized their use as fashion accessories, expanding the consumer base beyond medical necessity. Furthermore, the continuous circulation of beauty trends through social media maintains market momentum by generating consistent demand in the global hair wigs and extensions industry. This shift toward fashion-focused applications represents a significant factor in market growth, with implications extending through 2025 and beyond.

Advancements in product technology

Product technology advancements are improving the production and design of wigs and extensions through enhancements in natural appearance, comfort, and customization. The integration of ultra-thin wefts, undetectable lace fronts, and advanced color-matching technologies enables seamless blending with natural hair. AI-powered tools and 3D scalp mapping technology enhance personalization by providing tailored fittings and color recommendations, improving overall customer satisfaction. New materials and sterilization techniques have improved product durability and hygiene standards, while lightweight clip systems provide secure and comfortable daily wear. Companies such as Aderans Co., Ltd., HairUWear Inc., and Mayvenn Inc. implement these technologies to address various consumer needs, from medical hair loss solutions to fashion applications. The market has adopted augmented reality for virtual try-on services, improving the purchasing experience and reducing product returns. The incorporation of sustainable and ethically sourced hair materials meets the increasing consumer demand for environmental responsibility. These technological improvements increase product longevity and enhance user experience, supporting market growth through 2025 and beyond. The evolution of wigs and extensions from noticeable accessories to refined, natural-looking beauty products has increased their global acceptance.

High demand for personalized wigs and extensions

Increasing demand for personalized products that match specific hair characteristics and lifestyle requirements is driving growth in the hair wigs and extensions market. Companies such as Remi Cachet implement strict quality control measures, evaluating hair health and density to ensure product quality. The FDA's regulatory framework, which exempts wigs and hairbrushes from cosmetic product listing requirements, enables manufacturers to develop diverse, personalized offerings [2]Source: Food and Drug Administration (FDA), "Guidance for Industry: Registration and Listing of Cosmetic Product Facilities and Products", fda.gov. The personalization extends beyond aesthetic features like color, texture, and length to include various application methods such as clip-in, tape-in, and pre-bonded options, accommodating different user preferences and skill levels. Advanced technologies, including AI-based color matching, 3D scalp mapping, and virtual try-on capabilities, enhance the customization process and improve customer satisfaction. Companies including Remi Cachet, UniWigs Inc., and Parfait are implementing these technological solutions to provide customized wig options. The market's growth is supported by this personalization trend, along with fashion influences, medical hair loss requirements, and technological advancements. The focus on personalized wigs and extensions, offering natural appearance, comfort, and convenience, continues to drive market expansion with sustained growth expected through 2025 and beyond.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of premium human hair products | -1.8% | Global, most pronounced in price-sensitive markets | Short term (≤ 2 years) |

| Alternative medical hair-loss treatments (PRP, JAK inhibitors) | -1.2% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Regulatory scrutiny on forced-labor hair supply chains | -0.9% | Global, with enforcement focus in North America and Europe | Long term (≥ 4 years) |

| Limitation due to hygiene and maintenance challenges | -0.7% | Global, particularly in humid climates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost of premium human hair products

The high cost of premium human hair products constrains market penetration in price-sensitive market segments. Premium human hair wigs and extensions command substantial prices, ranging from hundreds to thousands of dollars based on quality, length, and processing techniques. Salons and retailers are adapting by exploring alternative suppliers in India and Vietnam and forming buying groups to reduce costs, though quality concerns persist compared to Chinese supply. As of April 2025, U.S. government tariffs on Chinese imports have increased to 125% on various products, including human hair wigs and extensions, affecting global pricing [3]Source: The Hair Society, "Navigating the Storm: Strategies for Hair Salons Facing Elevated Tariffs on Chinese Imports", thehairsociety.org . Also, the removal of the "de minimis" exemption means imports under USD 800 now face 90% tariffs plus fees, impacting small-scale purchases and individual consumers. This tariff escalation creates a market shift: premium segments maintain demand from consumers prioritizing quality and natural appearance, while cost pressures drive innovation in synthetic alternatives and segment the market toward affordable products. Companies like Aderans Co., Ltd., HairUWear Inc., and Mayvenn Inc. continue to lead in premium offerings. While synthetic alternatives grow as price-accessible options amid tariff pressures, the premium human hair market persists due to consumer preference for natural, high-quality appearances. The increasing cost environment, influenced by tariffs and supply chain changes, shapes market dynamics beyond 2025, making innovation and diversification essential strategies for industry participants.

Alternative medical hair-loss treatments (PRP, JAK inhibitors)

The hair wigs and extensions market sees medical treatments like platelet-rich plasma (PRP) therapy and Janus kinase (JAK) inhibitors emerging as alternatives to wigs and extensions, particularly for patients with treatable conditions like androgenetic alopecia (AGA). PRP therapy uses the body's growth factors to stimulate hair follicle activity, with studies showing increased hair density and thickness after several months of treatment. Research indicates improvements in hair count, density, and reduced shedding, particularly in patients receiving extended treatments with higher PRP volumes. JAK inhibitors demonstrate effectiveness in restoring hair growth for specific autoimmune-related hair loss cases. However, these medical therapies have limitations - they may not work for all hair loss types and require ongoing treatment with varying results. This makes wigs and extensions essential for immediate aesthetic solutions. Companies like Aderans Co., Ltd. and HairUWear Inc. provide temporary options for patients during treatment periods. Surgical hair transplants and topical treatments like minoxidil remain important components of medical hair loss treatments. The market accommodates both medical therapies and hair replacement products, with wigs and extensions meeting needs where medical solutions are inadequate or require extended treatment periods. This combination of medical treatments and hair accessories expands consumer options and continues to drive market growth through 2025 and beyond.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Human Hair Dominance Faces Synthetic Innovation

Human hair holds a 73.18% market share in 2024, primarily due to its styling versatility and natural appearance, which supports premium pricing despite supply chain challenges. Synthetic hair is experiencing the highest growth rate with a 14.50% CAGR (2025-2030), driven by technological advancements and cost advantages as human hair prices increase. Mixed/blended materials provide a balanced option, combining the quality of human hair with synthetic hair's durability and cost-effectiveness.

The European Union's approval of melanin-based black hair products marks a significant development in synthetic hair coloring, using 5,6-dihydroxyindole to produce natural-looking colors with reduced health risks. However, quality control issues remain in synthetic materials, as research indicates some products contain toxic contaminants exceeding safety thresholds. This situation presents opportunities for manufacturers who focus on clean production methods and safety certifications. The material market reflects increasing consumer emphasis on sustainability and ethical sourcing practices, with environmental impact and labor conditions influencing purchasing behavior.

By Product Type: Hair Extensions Drive Market Expansion

Hair extensions hold a dominant 64.06% market share in 2024 and are projected to grow at a 14.12% CAGR during 2025-2030, as consumers increasingly prefer enhancement solutions over full replacements. Full wigs and half wigs occupy distinct market segments, with full wigs primarily serving complete hair loss needs and half wigs offering targeted coverage and volume solutions. The extension segment's expansion is driven by multiple application methods, including clip-in, tape-in, sew-in/weave, and pre-bonded/micro-link options, catering to varying expertise levels and usage durations. Moreover, the Kevin Murphy Group's acquisition of Australian premium hair extensions company Showpony in April 2023 indicates a market trend toward consolidation focused on quality products with ethical sourcing practices.

Clip-in extensions show the highest growth among application methods, driven by their user-friendly nature and temporary application that appeals to new users and occasional wearers. Tape-in and pre-bonded extensions fulfill the semi-permanent segment, requiring professional installation while providing extended wear periods. The "others" category includes specialized techniques such as sew-in/weave and micro-link applications, which address specific hair types and cultural preferences, particularly in multicultural markets where traditional braiding and weaving methods combine with modern extension technologies.

By End User: Commercial Applications Accelerate

The market in 2024 is dominated by individual consumers, who represent 68.25% of the market share. This segment primarily uses these products for personal beauty enhancement and medical purposes, particularly for managing hair loss from conditions like alopecia or chemotherapy treatments. Individual consumers generate consistent demand for both human and synthetic hair products, using them for daily wear and style variations. Companies like Aderans Co., Ltd., HairUWear Inc., and Mayvenn Inc. serve this consumer base by offering customizable products that meet both cosmetic preferences and medical requirements.

The commercial segment is experiencing the fastest growth, with a projected CAGR of 14.37% from 2025 to 2030. This segment encompasses salons, entertainment industry users, and medical facilities that provide hair loss solutions. Commercial users leverage bulk purchasing advantages and professional application expertise to enhance product performance and client satisfaction. Salons and medical centers typically require high-quality products that offer durability and natural appearance. Companies such as Great Lengths S.p.A. and Platform Hair Extensions support these professional channels through educational programs and training initiatives to improve application techniques and product knowledge. This professional development strengthens the commercial market's growth and contributes to the industry's advancement through 2025 and beyond.

By Gender: Male Market Expansion Accelerates

Female consumers hold 82.45% market share in 2024, aligning with traditional beauty market dynamics and women's higher adoption rates of hair accessories. The male consumer segment shows the highest growth potential with a 14.83% CAGR (2025-2030), attributed to evolving male grooming preferences and increased incidence of male pattern baldness. Men's market growth stems from decreased stigma surrounding hair loss treatments and broader acceptance of cosmetic solutions. Product development in the male segment prioritizes natural-looking results and simple application methods, focusing on solutions that blend with existing hair.

The adoption of gender-neutral beauty standards has expanded the market for hair wigs and extensions beyond traditional female consumers. Media representation of male grooming has normalized the use of wigs and hairpieces among men. Medical conditions, including alopecia and chemotherapy-induced hair loss, continue to drive demand across all genders. In response to increasing inclusivity, manufacturers are developing products that accommodate various hair textures and styles to serve a diverse customer base.

By Distribution Channel: Digital Transformation Accelerates

Offline stores command a 55.75% market share in 2024. Physical retail channels, including specialty stores, salons, and hypermarkets, maintain their dominance by offering customers the ability to examine products firsthand and receive professional consultation. Companies like Great Lengths S.p.A., Evergreen Products Group, and HairUWear Inc. prioritize their offline presence to provide essential services such as texture assessment, color matching, and expert guidance, particularly for premium and medical-use products. These stores excel in delivering personalized fitting services and direct styling assistance, which strengthens customer satisfaction and retention.

Online stores are experiencing significant expansion, with a projected CAGR of 13.75% from 2025 to 2030. This growth stems from factors including accessibility, extensive product ranges, and competitive prices. Companies such as Luxy Hair, Mayvenn Inc., and Beautyforever Hair utilize e-commerce platforms to serve international markets with both human and synthetic hair products. The integration of augmented reality (AR) try-on features and detailed product photography helps address traditional online shopping limitations. Comprehensive return policies and thorough product information minimize purchase risks for consumers. The market demonstrates an increasing shift toward omnichannel retail, where digital and physical shopping experiences complement each other, supporting market expansion through 2030.

Geography Analysis

North America holds 42.62% market share in 2024, supported by high disposable incomes, advanced healthcare infrastructure addressing medical hair loss, and widespread acceptance of hair enhancement solutions. The United States market benefits from established distribution networks and clear FDA regulations, which enhance consumer trust in premium products. However, increased tariffs on Chinese hair imports, up to 125%, create cost pressures and affect market growth through higher product prices and supply chain complications. Besides, Canada and Mexico contribute to North American market expansion through cross-border trade and common beauty trends, despite varying regulatory requirements.

Europe maintains significant market presence through its beauty industries in Germany, the United Kingdom, Italy, and France, emphasizing premium products and ethical sourcing standards. The European Union's regulatory framework supports product safety and innovation, as demonstrated by the approval of melanin-based hair coloring technology. USDA regulations for hair and wool exports to the EU require specific treatments and documentation, favoring regional suppliers. European consumers prioritize sustainability and ethical sourcing in hair products. The Netherlands, Poland, and Belgium function as distribution centers for European markets, while Nordic countries show increased adoption of hair enhancement products.

The Middle East and Africa region exhibits the highest growth rate, with a projected 13.55% CAGR from 2025 to 2030, driven by young populations, urbanization, and increasing beauty awareness. South Africa, Saudi Arabia, and the United Arab Emirates support market growth through established beauty retail networks and affluent consumer bases. Cultural acceptance of hair coverings enhances market potential. Nigeria shows growth potential despite synthetic product quality concerns, increasing demand for premium products. Egypt, Morocco, and Turkey serve as manufacturing and distribution hubs, benefiting from proximity to European markets and competitive labor costs. Furthermore, the Asia-Pacific region contributes significantly through major exporters like India and Hong Kong, while Japan and South Korea demonstrate increasing demand due to fashion trends and medical hair loss awareness.

Competitive Landscape

The hair wigs and extensions industry maintains a moderately fragmented competitive landscape, where both established companies and new entrants pursue market expansion through distinct strategies. Major companies implement vertical integration to control supply chains and maintain quality standards, essential for customer trust and brand loyalty. Smaller companies focus on direct-to-consumer sales approaches, targeting specific customer segments with customized products. This market structure accommodates various business models operating successfully.

Companies exhibit varying levels of technology adoption, influencing their market position and product development. While some manufacturers invest in synthetic hair technology and digital marketing platforms to increase sales, others concentrate on premium human hair sourcing and traditional retail partnerships. The FDA's Modernization of Cosmetics Regulation Act of 2022 has introduced additional facility registration and product listing requirements, benefiting companies with established quality control and compliance systems.

Industry consolidation continues, as demonstrated by the Kevin Murphy Group's acquisition of Showpony in April 2024. Market opportunities exist in sustainable manufacturing, ethical sourcing transparency, and product customization using AI and augmented reality technologies. New companies disrupt traditional distribution through direct-to-consumer approaches and social media presence, while established firms expand their product lines and develop omnichannel strategies. In the Asia-Pacific region, Indian and Hong Kong-based companies increase their market presence through diversified sourcing and technological innovation. The market's competitive environment continues to evolve, influenced by technological advancement, regulatory requirements, and supply chain management, rewarding companies that demonstrate adaptability and strategic planning.

Hair Wigs And Extensions Industry Leaders

-

Aderans Co., Ltd.

-

Evergreen Products Group Ltd.

-

Great Lengths S.p.A.

-

Rebecca Hair Products Co., Ltd.

-

Artnature Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Bellami Hair launched its Textured Hair Collection to address an underserved segment in the beauty industry. The company developed three texture options: 3C Ringlet, 3A Spiral, and Blowout, which matched natural curl and coil patterns. The products were available in seven shades and three lengths, providing options for diverse hair tones and curl types.

- March 2025: Luvme Hair released the Luvme All-Day Comfort Wig, which featured a redesigned wig cap that improved fit and breathability. The wig incorporated three key design elements: a 3-Adjustment Clasp Design, a Zero-Gravity Wig Cap Design, and a C-Shape Ear-to-Ear Design. These features enhanced the wig's comfort and security during wear.

- November 2024: Bozoma Saint John, former chief marketing officer at Netflix, launched Eve By Boz, a wig and haircare company. The brand differentiated itself by offering multiple lace colors for wigs to match various skin tones. The 171-piece collection became available exclusively through the company's website.

Global Hair Wigs And Extensions Market Report Scope

| Wigs | Full Wigs |

| Half Wigs | |

| Hair Extensions | Clip-In |

| Tape-In | |

| Others (Sew-In/Weave, Pre-Bonded/Micro-Link, Pre-Bonded/Micro-Link) |

| Human Hair |

| Synthetic Hair |

| Mixed/Blended |

| Individual Consumers |

| Commercial Users |

| Male |

| Female |

| Offline Stores |

| Online Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Wigs | Full Wigs |

| Half Wigs | ||

| Hair Extensions | Clip-In | |

| Tape-In | ||

| Others (Sew-In/Weave, Pre-Bonded/Micro-Link, Pre-Bonded/Micro-Link) | ||

| By Material | Human Hair | |

| Synthetic Hair | ||

| Mixed/Blended | ||

| By End User | Individual Consumers | |

| Commercial Users | ||

| By Gender | Male | |

| Female | ||

| By Distribution Channel | Offline Stores | |

| Online Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the global hair wigs and extensions market be by 2030?

Forecasts indicate USD 21.22 billion by 2030, representing a 12.94% CAGR from 2025.

Which product segment is growing fastest to 2030?

Synthetic extensions are set for the highest 14.50% CAGR due to cost advantages and better realism.

What drives demand in Middle East and Africa?

Young demographics, rising urban income, and cultural events that favor elaborate hairstyles support a 13.55% CAGR outlook.

How are brands addressing sustainability concerns?

Initiatives include blockchain traceability, recycled fiber development, and carbon-neutral packaging programs.

Page last updated on: