Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

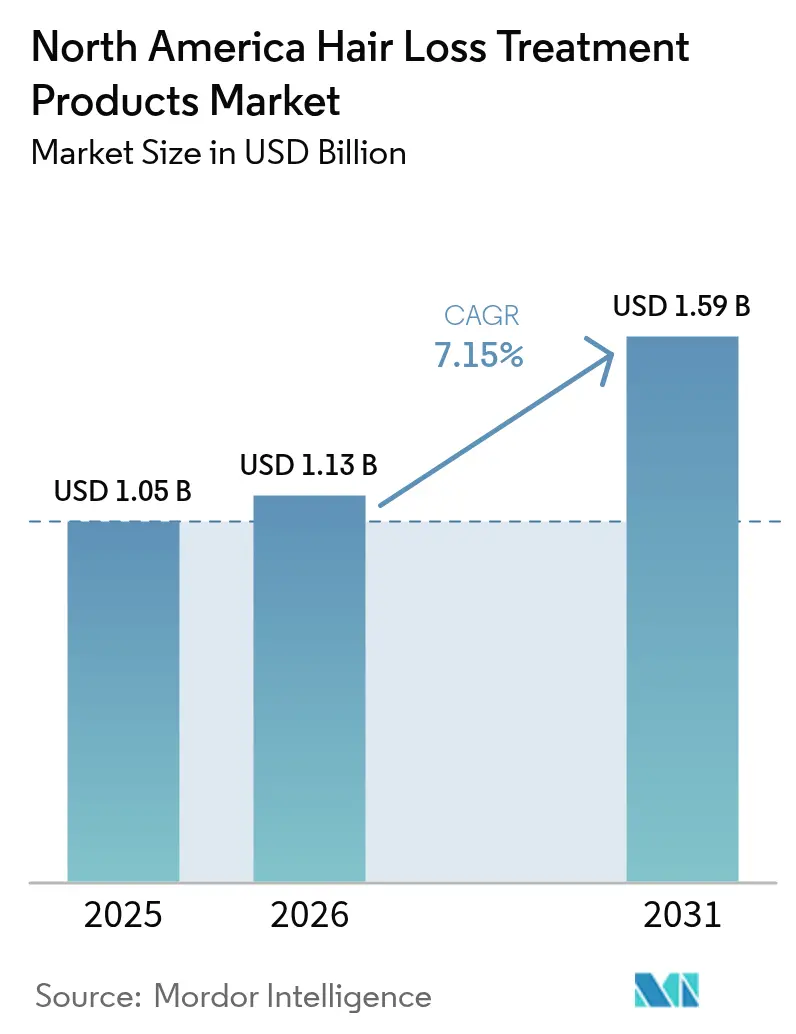

| Base Year Market Size (2025) | USD 1.05 Billion |

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 1.59 Billion |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Hair Loss Treatment Products Market Analysis by Mordor Intelligence

The North America hair loss treatment products market size was valued at USD 1.05 billion in 2025 and estimated to grow from USD 1.13 billion in 2026 to reach USD 1.59 billion by 2031, at a CAGR of 7.15% during the forecast period (2026-2031). This growth is attributed to an expanding consumer base, advancements in therapeutic options, and diverse retail strategies. In the U.S. and Canada, an aging population is increasing the prevalence of androgenetic alopecia. Rising aesthetic awareness and body image concerns, particularly among individuals aged 25 to 45 and influenced by social media, have driven more consumers to seek hair loss solutions to enhance confidence and appearance. A growing demand for natural, organic, and sustainable hair care products is encouraging manufacturers to focus on plant-based and chemical-free treatments. Regulatory approvals of innovative actives such as deuruxolitinib and baricitinib highlight a maturing scientific pipeline, motivating both physicians and consumers to adopt prescription-grade solutions. Telemedicine and direct-to-consumer (DTC) models are simplifying treatment pathways, enabling faster prescription access and fostering brand experimentation. With the FDA and COFEPRIS intensifying counterfeit surveillance and consumers favoring evidence-backed ingredients, established brands with robust quality controls continue to gain a competitive edge.

Key Report Takeaways

- By gender, female buyers represented 72.20% of the North American hair loss treatment products market share in 2025; the male segment is forecast to post the strongest 7.98% CAGR to 2031.

- By product type, shampoos and conditioners captured 82.62% revenue share in 2025, while serums are expected to advance at a 7.44% CAGR through 2031.

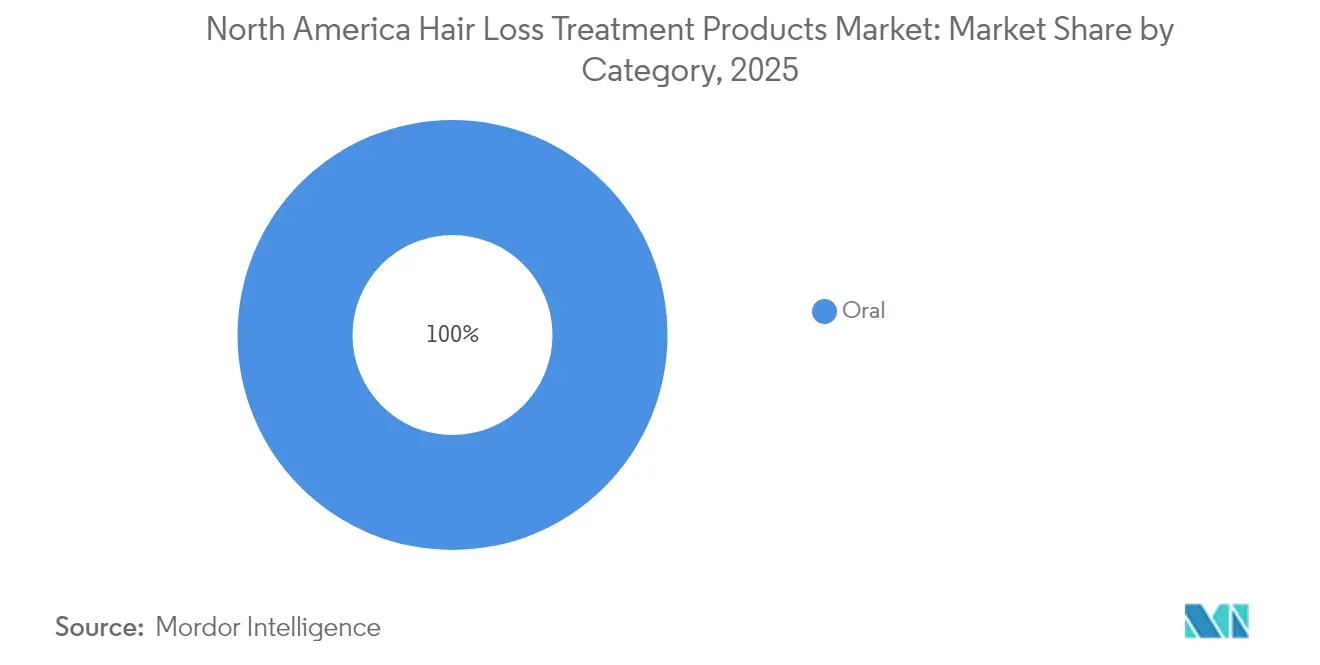

- By category, topical formulations accounted for 90.85% of the North America hair loss treatment products market size in 2025, whereas oral treatments will expand at a 7.85% CAGR up to 2031.

- By distribution channel, health and beauty stores controlled a 47.10% share in 2025; online retail is projected to deliver the fastest 7.76% CAGR between 2026-2031.

- By geography, the United States retained a 69.65% share of the North America hair loss treatment products market size in 2025; Mexico is poised for a 7.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Hair Loss Treatment Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging demographics and androgenetic alopecia prevalence | +1.8% | United States, Canada | Long term (≥ 4 years) |

| Growing aesthetic consciousness and social media influence | +1.5% | United States urban markets | Short term (≤ 2 years) |

| Increasing prevalence of hair loss and baldness | +1.2% | United States, Canada, Mexico | Medium term (2-4 years) |

| Expansion of at-home treatment options | +1.0% | United States, Canada, Mexico | Medium term (2-4 years) |

| Demand for natural, organic and sustainable products | +0.9% | Premium segments in United States, Canada | Short term (≤ 2 years) |

| Technological advancements in therapies | +0.8% | United States lead, Canada follow | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging demographics and androgenetic alopecia prevalence drive market foundation

North America's demographic shifts are creating a sustained demand for hair loss treatments as cases of androgenetic alopecia continue to rise. According to the National Alopecia Areata Foundation, approximately 700,000 individuals in the U.S. are affected by some form of alopecia areata[1]Source: National Alopecia Areata Foundation, "Alopecia Areata", www.naaf.org. The aging population, particularly the large Baby Boomer demographic, is driving increased treatment adoption. The rise in diagnosed cases and growing awareness of available treatments are fostering innovation and market growth for hair loss solutions. The U.S. Census Bureau reports that the population aged 65 and older in the U.S. grew by 3.1% in 2025, reaching 61.2 million[2]Source: US Census Bureau, "Older Population and Aging", www.census.gov. Since the prevalence of androgenetic alopecia increases with age, this demographic trend ensures consistent market growth, largely unaffected by economic fluctuations. Hair loss, as a progressive condition, requires long-term treatment adherence. In Mexico, the expansion of healthcare infrastructure, supported by COFEPRIS's regulatory modernization, is improving access to both prescription and over-the-counter treatments, particularly for aging populations that previously lacked specialized dermatological care.

Social media amplifies treatment adoption among younger demographics

Social media platforms such as Instagram, TikTok, YouTube, and Facebook are filled with personal stories and testimonials about hair loss and treatment experiences. These narratives strongly connect with younger audiences, motivating them to try advertised products and therapies. Digital platforms, particularly TikTok, are transforming how individuals discover and adopt hair loss treatments, with TikTok emerging as the leading health and beauty e-retailer in the U.S. Influencers and celebrities sharing their hair care routines, transformations, or hair loss treatments create viral trends that increase awareness and normalize treatment adoption. Their endorsements significantly influence product preferences and purchasing decisions among younger consumers. Social media acts as a discovery platform where younger users regularly come across new products, treatment options, and promotional offers, expediting their consideration and purchase decisions. Internet and social media usage is widespread in the region, with 93% of the U.S. population using the internet in 2023, according to the World Bank[3]Source: World Bank, "Individuals using the Internet", www.worldbank.org. However, while social media helps popularize treatments, it also spreads unverified claims and misinformation. This dual effect can spark curiosity and experimentation but also cause confusion, highlighting the need for evidence-based marketing.

Technological innovation expands treatment efficacy and patient access

Innovative therapeutic mechanisms are significantly broadening the range of treatment options beyond the traditional use of minoxidil and finasteride. Among the promising developments in the pipeline is Pelage Pharmaceuticals' PP405. This topical small molecule, currently undergoing Phase 2a clinical trials, is designed to target dormant follicle stem cells. Its mechanism holds the potential to stimulate the growth of terminal hair, which is thicker and more robust, as opposed to the finer vellus hair. Additionally, platelet-rich plasma (PRP) therapy is gaining widespread clinical acceptance as an autologous growth factor treatment, leveraging the patient’s own platelets to promote hair regrowth. Low-level laser therapy (LLLT) devices are also gaining traction as non-invasive, user-friendly solutions for at-home treatment. Moreover, advancements in delivery systems, such as microneedles and nanoparticle formulations, are revolutionizing topical treatments. These cutting-edge methods enhance the penetration of active ingredients while minimizing systemic side effects, effectively addressing patient concerns associated with the risks of oral medications.

At-home treatment expansion democratizes access and reduces costs

Consumers now have the convenience of managing hair loss at home using a variety of products, including shampoos, conditioners, serums, oils, and oral supplements. These solutions eliminate the need for specialist consultations or clinical procedures, making them an accessible option. This ease of use has significantly broadened the appeal of such products, particularly among younger individuals and those who are mindful of their budgets. Consumers' increasing demand for convenient and private treatment options is driving the rapid growth of direct-to-consumer platforms and at-home medical solutions. In Canada, telemedicine platforms such as Felix, Jack Health, and PepHealth, along with emerging services like Choiz in Mexico, are effectively removing traditional barriers to prescription access while significantly reducing consultation costs. A study conducted by the University of Toronto highlights the pressing need for alternative access pathways, revealing that only 38% of Ontario dermatologists accept OHIP referrals for hair loss treatment. In March 2025, Skin + Me introduced Hair + Me, a service that provides personalized prescription formulations. These formulations combine pharmaceutical ingredients, including minoxidil, finasteride, and dutasteride, with botanical oils, demonstrating a seamless integration of pharmaceutical effectiveness and consumer-oriented convenience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and unregulated products | -1.2% | North America | Short term (≤ 2 years) |

| Limited healthcare infrastructure | -0.9% | Mexico, rural North America | Long term (≥ 4 years) |

| Consumer skepticism on long-term safety | -0.8% | Core markets | Medium term (2-4 years) |

| Lengthy approval processes | -0.6% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit product proliferation undermines consumer confidence

The FDA issued multiple warnings throughout 2024-2025 regarding unapproved hair loss products, including specific alerts about compounded topical finasteride formulations linked to adverse effects. Regulatory enforcement actions have significantly intensified as counterfeit products exploit consumer vulnerabilities, including desperation for effective treatments and restricted access to prescriptions. This issue is especially prevalent in online marketplaces, where verification mechanisms are often insufficient to ensure product authenticity. The widespread availability of unregulated formulations presents a dual threat, as these products not only risk being ineffective but may also pose serious safety concerns. Some of these formulations have been found to contain undisclosed pharmaceutical ingredients or harmful adulterants, further endangering consumers. In Mexico, COFEPRIS has enhanced its oversight of cosmetic establishments by enforcing stricter verification requirements under NOM-259 Good Manufacturing Practices, which became effective in July 2023. Additionally, COFEPRIS has introduced simplified procedures to facilitate the approval of legitimate health supplies. Consumer education campaigns continue to stress the importance of using FDA-approved treatments and consulting licensed healthcare providers. However, misinformation on social media remains a significant challenge, as it promotes unverified remedies and potentially hazardous DIY formulations, further complicating efforts to ensure consumer safety.

Healthcare infrastructure gaps limit treatment access

Patients often face delays in diagnosis and treatment initiation due to a shortage of dermatologists and hair loss specialists, particularly in rural or underserved areas. Access challenges in rural regions are worsened by geographic maldistribution. Additionally, managed care gatekeeping and prior authorization requirements further complicate access to prescription treatments. A study from the University of Toronto highlights systemic capacity limitations: only 38% of Ontario dermatologists accept public insurance referrals for hair loss, underscoring the hurdles many patients face in accessing specialized care. In Mexico, infrastructure challenges are even more pronounced. COFEPRIS, under the leadership of new commissioner Armida Zuñiga, is pushing for regulatory reforms in 2025 to tackle approval backlogs and streamline device registration. While the expansion of telemedicine offers some relief to these access constraints, the regulatory frameworks governing remote prescribing differ widely across jurisdictions. These disparities may leave complex cases, which necessitate in-person evaluations, inadequately addressed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shampoos Drive Volume While Serums Capture Innovation Premium

Shampoos and conditioners hold a dominant 82.62% share of the North American hair loss treatment market in 2025, highlighting consumers' preference for these well-known, daily-use products. These items benefit from extensive retail availability across supermarkets, pharmacies, and e-commerce platforms, enabling broad market penetration without requiring prescriptions or specialized consultations. On the other hand, serums are the fastest-growing segment, with a 7.44% CAGR projected through 2031. Their growth is driven by premium brand positioning and the inclusion of clinical-grade ingredients that support higher pricing. Furthermore, the growing "skinification" trend in hair care has raised consumer expectations for precise, effective formulations, presented in elegant packaging similar to facial serums.

At the same time, the "Others" category, which includes supplements, devices, and professional treatments, leverages innovations from adjacent markets such as nutraceuticals and medical devices. However, the regulatory environment varies significantly: shampoos are regulated as cosmetics, while serums containing pharmaceutical ingredients must follow drug approval processes. This regulatory complexity provides established players with expertise in compliance a competitive edge.

By Gender: Male Segment Acceleration Challenges Female Market Dominance

Female consumers hold a significant 72.20% market share in 2025, driven by increasing societal acceptance of hair care investments and a diverse range of products, from cosmetics to medical-grade treatments. Women's hair loss often appears as diffuse thinning rather than traditional pattern baldness, fueling demand for volumizing shampoos, scalp treatments, and hormonal therapies such as spironolactone and topical antiandrogens. Meanwhile, the male segment is growing rapidly, with an 7.98% CAGR projected through 2031, supported by decreasing stigmas and targeted marketing efforts addressing the psychological effects of androgenetic alopecia.

Rogaine's "National Hats Off Day" campaign exemplifies effective male consumer engagement. Additionally, ethnic differences in treatment perceptions highlight opportunities for market segmentation, indicating that culturally tailored strategies could accelerate adoption. Male-focused direct-to-consumer platforms like Hims and Roman have simplified prescription access through telemedicine. Moreover, the approval of JAK inhibitors introduces new options for severe cases that were previously limited to hair transplantation. The combination of social media influence, clinical advancements, and reduced access barriers positions the male segment for sustained growth, despite its smaller current market base.

By Category: Topical Dominance Faces Oral Treatment Renaissance

Topical treatments dominate the market with a significant 90.85% share in 2025, highlighting a strong consumer inclination toward localized application methods. This preference stems from the benefits of reduced systemic exposure and the convenience of over-the-counter availability. Among these, topical finasteride formulations are gaining increasing popularity as viable alternatives to oral administration. These formulations offer the advantage of minimizing sexual side effects while maintaining their effectiveness through targeted delivery directly to the scalp, addressing consumer concerns about safety and efficacy.

Oral treatments, which currently account for an 9.15% market share, are witnessing strong growth with a 7.85% CAGR projected through 2031. This growth is driven by clinical validation of low-dose oral minoxidil and regulatory approvals for innovative systemic mechanisms. The FDA's approval of deuruxolitinib (Leqselvi) for severe alopecia areata marks the first new oral hair loss treatment in decades, establishing JAK inhibition as a viable therapeutic approach. Originally developed for hypertension, oral minoxidil is increasingly being used off-label for androgenetic alopecia, supported by dermatology consensus guidelines and advancements in cardiovascular monitoring protocols. Telemedicine platforms are enhancing prescription accessibility and addressing monitoring needs, though boxed warnings for JAK inhibitors regarding risks of infection, cardiovascular issues, and malignancies necessitate careful patient selection and ongoing monitoring.

By Distribution Channel: Digital Transformation Accelerates Online Retail Growth

Health and beauty stores maintain a commanding 47.10% market share in 2025 by leveraging their specialized product knowledge, offering professional consultations, and positioning premium brands to secure high-value transactions. These stores play a crucial role in educating consumers about complex treatment options, providing opportunities for product trials, and effectively upselling complementary items such as scalp care products and styling aids, thereby enhancing the overall shopping experience.

Online retail stores are the fastest-growing distribution channel, with a robust 7.76% CAGR projected through 2031. This growth is fueled by the convenience of online shopping, the privacy it offers, and the increasing adoption of subscription-based models. TikTok Shop has emerged as a significant player, establishing itself as the largest health and beauty e-retailer in the United States. On the other hand, supermarkets and hypermarkets cater to the broader consumer base by offering competitive pricing and convenience, making them a preferred choice for mainstream purchases. Regulatory oversight by the FDA ensures product safety across all distribution channels, while the implementation of simplified procedures for health supplies by COFEPRIS facilitates the expansion of cross-border e-commerce into Mexico, further driving market growth.

Geography Analysis

The United States holds a commanding 69.65% share of the North American hair loss treatment market in 2025. This dominance is attributed to its advanced healthcare infrastructure, high levels of disposable income, and well-established regulatory frameworks that encourage the adoption of innovative treatments. The U.S. market benefits significantly from a robust network of dermatology professionals, although workforce shortages pose challenges to patient access. The FDA plays a pivotal role in shaping both domestic and global treatment standards. A recent example is the approval of deuruxolitinib for alopecia areata, which has set a new therapeutic benchmark worldwide. Additionally, the growing penetration of e-commerce in beauty and personal care sales is reshaping the market landscape. Platforms like Amazon and TikTok Shop are increasingly capturing market share by integrating subscription-based models and social commerce strategies, making treatments more accessible to consumers.

Canada represents a well-established and mature market, supported by universal healthcare coverage that facilitates access to prescriptions. However, variations in dermatology referral acceptance across provinces create disparities in access to specialized care. In January 2024, Health Canada approved baricitinib (Olumiant) for alopecia areata, expanding the range of available treatment options for patients. Telemedicine platforms, such as Felix and Jack Health, are addressing geographic challenges by providing remote access to healthcare services, particularly in rural areas. The Canadian market also reflects a growing emphasis on sustainability, with a strong preference for natural and organic formulations. This trend aligns with regulatory priorities that focus on ingredient transparency and environmentally friendly practices.

Mexico is emerging as the fastest-growing geography in the North American hair loss treatment market, with a projected compound annual growth rate (CAGR) of 7.44% through 2031. This growth is driven by an expanding middle-class population, ongoing improvements in healthcare infrastructure, and regulatory modernization initiatives led by COFEPRIS. Under the leadership of Commissioner Armida Zuñiga, who is set to implement reforms in 2025, COFEPRIS is introducing measures to simplify health supply procedures, reduce approval timelines through digitalization, and strengthen the framework for biologics manufacturing. Telemedicine platforms like Choiz are gaining traction by offering personalized hair loss treatments under COFEPRIS oversight. Additionally, the implementation of NOM-259 Good Manufacturing Practices for cosmetics in July 2023 has enhanced product quality standards. The market is further benefiting from the expansion of cross-border e-commerce, supported by harmonized regulatory approaches and increasing consumer acceptance of purchasing health products online.

Regulatory Landscape

In the United States, hair growth or hair loss prevention claims generally trigger drug classification, bringing FDA oversight through drug approval pathways or compliance with applicable OTC monographs, rather than cosmetic rules. Typical NDA review timelines run around 10-12 months. This distinction is material for formats such as shampoos, conditioners, serums, and foams where claim language, active selection, and labeling can shift a product into stricter FDA requirements.

Canada regulates non-cosmetic hair loss products either as Natural Health Products under the Natural Health Products Regulations or as non-prescription drugs under the Food and Drugs Regulations, with licensing overseen by Health Canada and the Natural and Non-prescription Health Products Directorate (NNHPD). NNHPD product licensing requires evidence submissions for safety, efficacy, and quality, influencing time-to-market and documentation burden for brands that want to sell across both the United States and Canada. Across the region, heightened scrutiny of unapproved or compounded hair loss formulations, including topical finasteride (which does not have FDA approval for hair loss), reinforces the importance of compliant actives, substantiated claims, and controlled manufacturing and distribution practices.

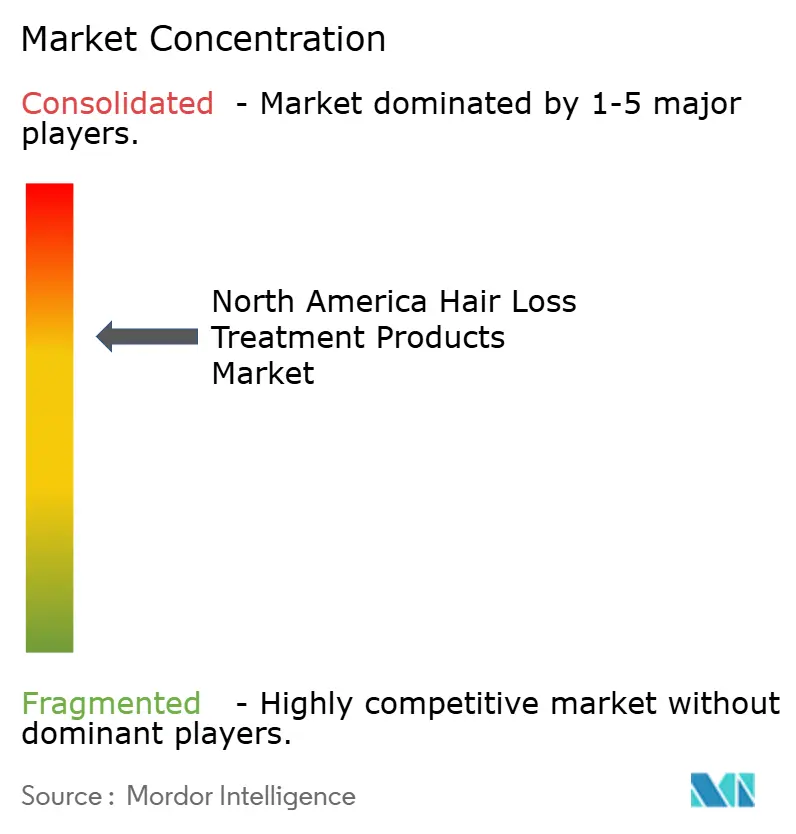

Competitive Landscape

The North American hair loss treatment market exhibits moderate concentration with established consumer goods companies leveraging brand recognition, distribution networks, and regulatory expertise to maintain market positions. Leading players like Procter and Gamble and L'Oréal have diversified their offerings, ranging from mass-market shampoos to prescription-grade treatments. They are also focusing on direct-to-consumer platforms and social media marketing to attract younger consumers. Companies are adopting an omnichannel distribution strategy, balancing traditional retail partnerships with the growing e-commerce and telemedicine channels, which provide higher margins and foster direct relationships with consumers.

Competition is intensifying as biotechnology firms introduce innovative approaches targeting follicle regeneration, immune modulation, and stem cell activation. Companies such as Pelage Pharmaceuticals, with its PP405, and established pharmaceutical firms developing JAK inhibitors, are emerging as competitors to traditional topical treatments. However, regulatory approval processes and stringent safety standards act as natural barriers to entry. Key players in the market include Procter and Gamble, L'Oréal, Unilever, Church and Dwight, and Kenvue. These companies, with extensive product portfolios in North America's developed regions, are significantly investing in research and development and marketing to enhance their market share. Additionally, they are focusing on online distribution channels to market and promote their products, aiming to expand their geographic presence and customer base. Digital and social media advertisements are being utilized to raise awareness about new product launches.

Technology adoption is driving differentiation, with companies investing in personalized formulations, AI-driven diagnostics, and advanced delivery systems such as microneedles and sustained-release formulations. The FDA's actions against counterfeit products create opportunities for legitimate manufacturers to highlight their safety, efficacy, and regulatory compliance. Meanwhile, COFEPRIS regulatory reforms in Mexico are enabling faster market entry for companies with proven safety profiles.

North America Hair Loss Treatment Products Industry Leaders

-

The Procter and Gamble Company

-

L'Oréal SA

-

Unilever Plc

-

Church and Dwight Co.

-

Kenvue

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A wave of regulatory-facing programs expands the range of options for dermatology-led brands and pharmacy channels across OTC, prescription, and specialist care. In April 2026, AbbVie submitted an application to the U.S. FDA seeking a new indication for upadacitinib (RINVOQ) in severe alopecia areata, building on Health Canada authorization of ritlecitinib, Litfulo, in late 2023. This momentum supports opportunities to develop clearer patient segmentation and treatment ladders that span OTC, prescription, and specialist care. A second area sits at the intersection of oral regimens, differentiated delivery, and telemedicine-enabled access. Veradermics reported positive topline results in April 2026 from its Phase 2/3 Study 302 for VDPHL01, an oral extended-release minoxidil formulation in male pattern hair loss, highlighting ongoing attempts to move beyond off-label oral minoxidil use. Regenerative and procedure-adjacent platforms also moved forward, with Xtresse receiving FDA IND acceptance in March 2026 for Xvie, an injectable extracellular vesicle therapy for androgenetic alopecia, signaling continued clinical investment that can expand the addressable market for physician-dispensed and hybrid at-home plus in-office models. Alongside these pathways, brand and channel strategies that emphasize compliant claims, counterfeit avoidance, and subscription replenishment for long-term regimens align with observed growth in online retail and DTC prescribing models across the United States and Canada, and with Mexico access initiatives under COFEPRIS modernization.

Recent Industry Developments

- July 2026: Hairmax announced its laser hair growth devices and hair wellness products became available through Ulta Beauty online. The move broadens mass-premium retail access for device-led hair restoration, supporting bundling with topical and supplement regimens and expanding visibility beyond clinic and direct channels.

- December 2025: The Procter and Gamble Company introduced Pantene Abundant and Strong, a three-step system including a daily scalp serum positioned around reducing hair shedding. It extends a leading mass brand deeper into scalp-first regimens, reinforcing competition in the high-volume shampoo and conditioner base while adding higher-margin treatment steps.

- October 2024: Organon completed the acquisition of Dermavant Sciences, adding the VTAMA (tapinarof) platform to its dermatology portfolio. The deal strengthens Organon in inflammatory dermatology, supporting adjacent scalp-condition management strategies that can influence consumer hair thinning routines and dermatologist prescribing pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from hair loss treatment products sold in North America, where the intent is to reduce hair fall or improve regrowth through topical or oral use across retail and professional channels.

Scope exclusions: We exclude surgical hair restoration procedures and standalone clinic service fees, and we only count product revenue where a saleable unit is purchased.

Segmentation Overview

-

By Product Type

- Shampoos and Conditioners

- Serums

- Others

-

By Gender

- Male

- Female

-

By Category

- Topical

- Oral

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Health and Beauty Stores

- Online Retail Stores

- Other Distribution Channel

-

By Geography

- United States

- Canada

- Mexico

- Rest of North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the market and to anchor assumptions that can be checked outside interviews. We referred to public sources such as the US Food and Drug Administration (drug and cosmetic rules), US International Trade Commission trade statistics, Statistics Canada tables, and the Mexican government statistics portal for macro indicators, along with association sites such as the American Academy of Dermatology for condition context.

In addition, we reviewed company filings, investor presentations, earnings call notes, and reputable press coverage to understand product launches, channel shifts, and pricing direction. Select paid subscriptions for company financials and patent databases were used only to speed up cross-checks on company exposure and innovation intensity. These desk sources are illustrative, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what gets counted as a hair loss treatment product in real buying behavior and how sales split across retail and online routes. We spoke with a mix of brand and channel participants, distributors, and dermatology aligned stakeholders across the United States, Canada, and Mexico, and then used their inputs to test adoption patterns, typical pricing moves, and how much volume sits in each product format.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | |

| Mid tier: 43% | Functional/Unit leaders: 37% | |

| Smaller Players: 21% | Managers: 50% |

Market-Sizing & Forecasting

The core sizing starts with a top-down build that reconstructs demand from North America level consumer spend signals and category mix, and then translates that into hair loss treatment product revenue by applying treatment adoption and channel weighting. To avoid overcounting, the model treats products as counted only when they are purchased as a distinct hair loss treatment item, not when they are general hair care with vague claims.

The totals are then stress-tested with selective bottom-up approximations, such as sampled price per unit times estimated units sold for key product formats, plus channel checks on online and pharmacy intensity, which are then used to adjust the final market numbers. Inputs used in the model include the share of shampoos and conditioners versus serums and other formats, topical versus oral mix, average selling price ranges by channel, online retail penetration, and observed regulatory positioning (cosmetic versus drug-like claims) that affects how products are marketed and sold. For forecasting, scenario analysis was used so that adoption, pricing progression, and channel shift assumptions could be moved within realistic bounds that interviewees considered plausible. Where bottom-up signals were incomplete, gaps were handled by using conservative ranges and then re-checking them against the total implied by the top-down demand pool.

Data Validation & Update Cycle

Validation is done through multiple passes that compare model outputs against independent signals, including channel growth cues, pricing movement, and product mix shifts seen in public disclosures. Outliers are flagged, investigated, and corrected through follow-up checks, and when needed we re-contact sources if a key assumption changes or a material event shifts market direction.

Before sign-off, the work is reviewed by another analyst to confirm calculations, unit consistency, and logic flow across North America geographies. The report is refreshed annually, and interim updates are made when major regulatory, channel, or demand changes occur. Right before delivery, a fresh review pass is completed so clients receive the latest updated view.

Mordor Intelligence's North America Hair Loss Treatment Products Market Size Compared With Other Published Estimates

Published market values for hair loss treatment products in North America often look far apart because each publisher draws the line around different product groups and selling points, and then uses different base years and growth assumptions.

Some estimates expand the scope into broader hair growth and restoration spending, which can pull in adjacent items and inflate the total. In Mordor Intelligence modeling, revenue is counted as product sales within shampoos and conditioners, serums, and other hair loss treatment products, and service-only clinic procedures are not added to the number, which is one practical reason the figures differ.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.05 B (2025) | |

| Regional Consultancy A | USD 5.50 B (2023) | Uses an earlier base year and a wider product framing that can mix general hair growth items with treatment products, and the scope signals are less clear on what is excluded from non-surgical care. |

| Industry Research Portal B | USD 2.75 B (2025) | Uses a broader hair loss and growth treatment definition that visibly includes categories like laser devices and supplements, which can lift totals compared with a product-only treatment count. |

The spread in the table is mostly explained by what gets included as a treatment purchase, plus base year choice and how devices and add-on categories are handled. By keeping the market tied to traceable product groups and then checking the outcome against channel and pricing realities, the resulting total stays easier to reproduce and interpret year to year.

Key Questions Answered in the Report

How large is the North America hair loss treatment products market in 2026?

The sector is valued at USD 1.13 billion in 2026 and is forecast to grow at a 7.15% CAGR to USD 1.59 billion by 2031.

Which product format records the highest sales volume?

Shampoos and conditioners dominate with 82.62% revenue share thanks to routine use and OTC availability.

Which therapeutic innovation has recently reshaped prescription options?

The United States Food and Drug Administration approval of the JAK inhibitor deuruxolitinib in 2024 introduced the first new oral therapy for severe alopecia areata in decades.

Why is Mexico the fastest-growing country segment?

Healthcare infrastructure upgrades, Comisión Federal para la Protección contra Riesgos Sanitarios (COFEPRIS) regulatory modernization and a rising middle class push Mexico toward a 7.44% CAGR through 2031.

Page last updated on: