Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| Market Size (2025) | USD 0.68 Billion |

| Market Size (2030) | USD 1.05 Billion |

| Growth Rate (2025 - 2030) | 9.01% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Hair Loss Treatment Products Market Analysis by Mordor Intelligence

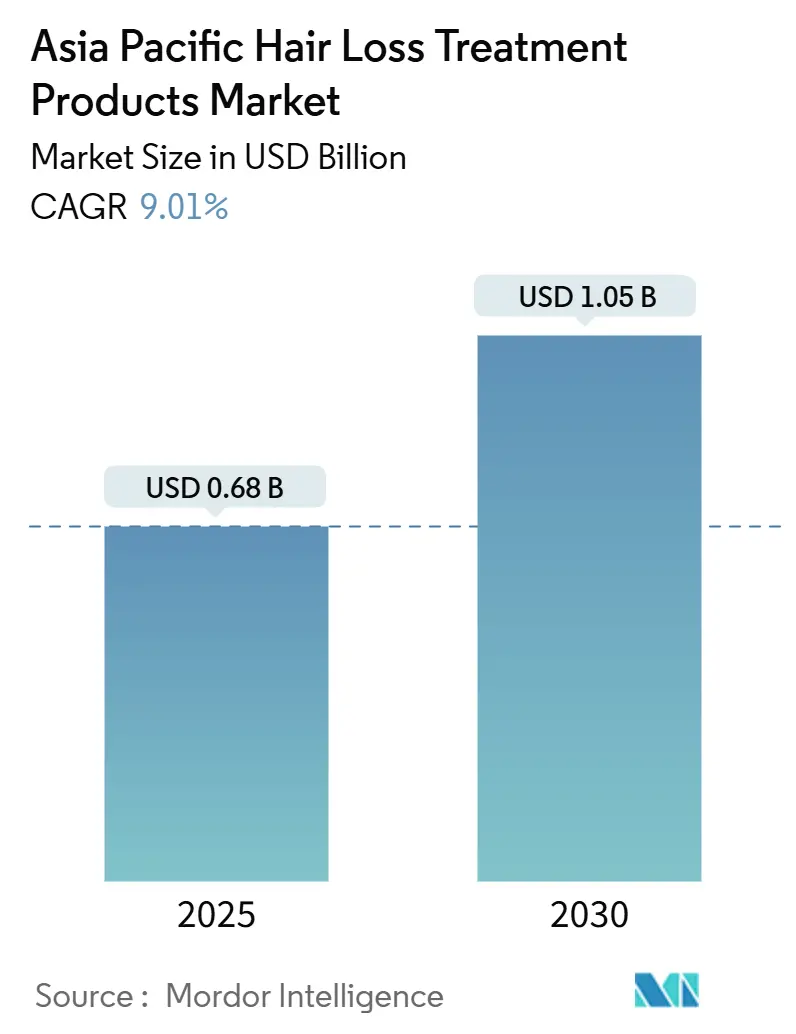

The Asia-Pacific hair loss treatment market size stands at USD 0.68 billion in 2025 and is forecast to reach USD 1.05 billion by 2030, registering a 9.01% CAGR over the period. Demand is pivoting from cosmetic cover-ups to clinically validated therapies that address androgenetic alopecia, telogen effluvium, and alopecia areata. Rising disposable incomes in emerging economies, strict action against counterfeit goods, and faster approval pathways for biologics and device-based interventions are reinforcing this shift. At the same time, livestream-centric e-commerce is accelerating trial and adoption, while premiumization allows brands to blend dermatology with beauty positioning.Despite regulatory crackdowns in Singapore, Thailand, South Korea, Malaysia, and Vietnam, counterfeit products continue to proliferate. Enforcement actions in these countries have successfully seized unregistered minoxidil and finasteride products. However, they have yet to eliminate parallel imports or the gray markets prevalent in e-commerce[1]Source: Health Sciences Authority, "HSA Seized Over 970,000 Units of Illegal Health Products and Removed More Than 7,000 Illegal Product Listings in 2024", hsa.gov.sg. Multinational FMCG companies, regional pharma leaders, and tech-driven start-ups are therefore engaged in a three-way race to capture clinical credibility, digital reach, and sophisticated formulations across the Asia-Pacific hair loss treatment market.

Key Report Takeaways

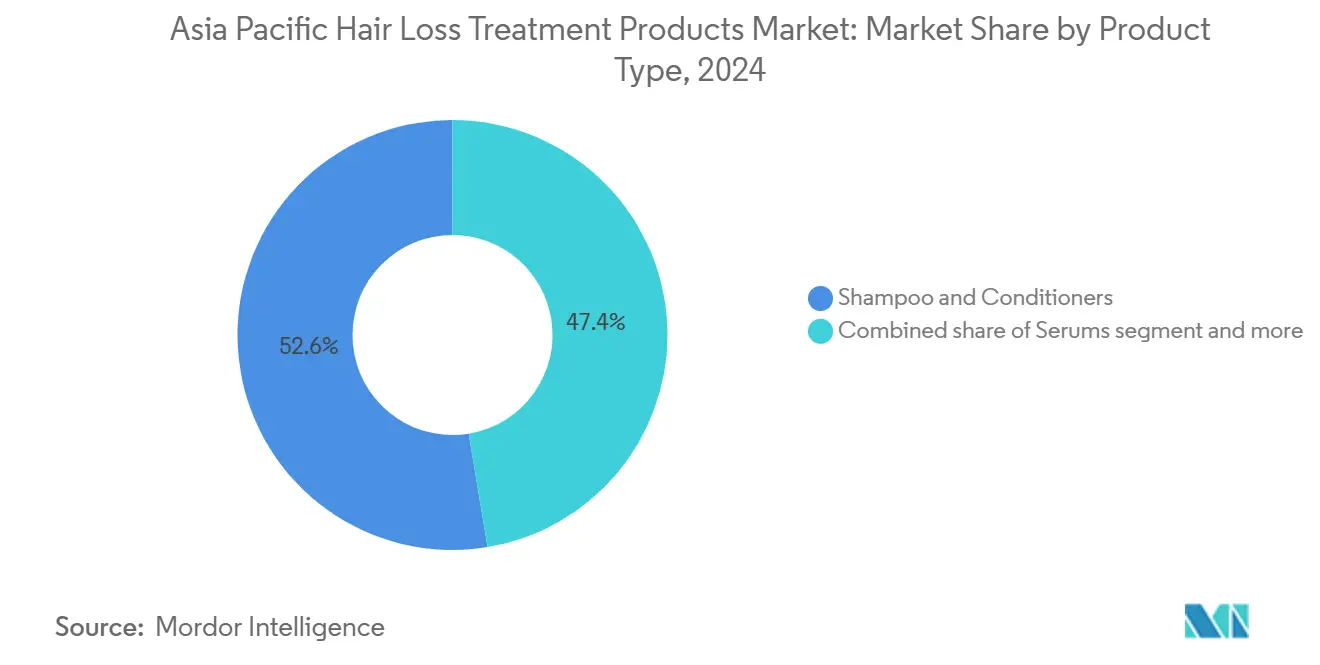

- Shampoos and conditioners led with 52.61% of the Asia-Pacific hair loss treatment market share in 2024; serums are set to advance at a 10.72% CAGR between 2025 and 2030.

- The male cohort accounted for 58.20% of 2024 revenue, while female demand is projected to grow at an 11.22% CAGR through 2030.

- Topical formulations controlled 94.32% of sales in 2024; oral supplements are forecast to expand at a 9.41% CAGR during 2025-2030.

- Health and beauty stores captured 47.12% of distribution in 2024; online retail is expected to post a 10.43% CAGR over the same period.

- China contributed 37.18% of 2024 regional revenue, whereas India is anticipated to deliver the fastest growth at a 10.91% CAGR to 2030.

Asia-Pacific Hair Loss Treatment Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of androgenetic alopecia | +2.0% | China, Japan, South Korea, Singapore | Long term (≥ 4 years) |

| Consumer affluence and rising beauty focus | +1.5% | India, Indonesia, Vietnam, Thailand, China tier-2/3 | Medium term (2-4 years) |

| E-commerce and social-commerce expansion | +2.2% | China, South Korea, India, Southeast Asia | Short term (≤ 2 years) |

| Tech-enabled therapies and personalization | +1.3% | Japan, South Korea, China, Australia | Medium term (2-4 years) |

| Influencer-led scalp-diagnostic apps fueling personalization | +0.8% | China, South Korea, urban India | Short term (≤ 2 years) |

| Regulatory crackdown on counterfeits boosting trust in premium brands | +0.7% | Singapore, Malaysia, Thailand, Vietnam, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of androgenetic alopecia

Clinical studies reveal a rising trend of androgen-linked hair loss among men and women in East and Southeast Asia. This condition, characterized by its chronic nature, often leads consumers to prioritize early medical interventions over temporary cosmetic solutions. The increasing awareness of long-term benefits and the availability of advanced treatments are driving this shift in consumer behavior. Thanks to Japan's expedited approach to regenerative medicine, Shiseido has successfully commercialized its autologous dermal sheath cup cell therapy. This development highlights how supportive policies can accelerate clinical adoption and innovation in the market. Meanwhile, regulators in other regions, like China's NMPA, are emphasizing the need for solid efficacy data in anti-hair-loss cosmetics, steering the market towards products grounded in evidence and scientific validation. Furthermore, gender-specific approvals, exemplified by India's inaugural authorization of minoxidil for female-pattern hair loss, not only highlight market segmentation but also pave the way for new revenue opportunities by addressing previously underserved demographics.

Consumer affluence and rising beauty focus

In India, Indonesia, and Vietnam, rising real disposable incomes are boosting spending on personal-care products. Urban millennials in these countries now view scalp health as integral to overall wellness, leading them to opt for premium shampoos enriched with peptides, collagen, and botanical extracts. This shift reflects a growing awareness of the benefits of high-quality ingredients in maintaining hair and scalp health. Similarly, consumers in tier-2 and tier-3 cities of China are moving away from traditional brick-and-mortar deals, gravitating instead towards mid-priced dermo-cosmetics that deliver on their promises of measurable results. These products often address specific concerns such as hair thinning, dandruff, and scalp sensitivity, making them increasingly popular. Promotional campaigns are now openly discussing topics like postpartum hair loss and hormonal changes, effectively expanding their reach to a broader female audience by normalizing these conversations and offering targeted solutions. Collectively, these shifts are driving consistent growth, both in volume and value, in the Asia-Pacific hair loss treatment market.

E-commerce and social-commerce expansion

Online sales dominate the hair care segment, and social media platforms are driving this trend. Platforms like Douyin, Xiaohongshu, and TikTok Shop are revolutionizing the shopping experience, merging livestream education, instant checkout, and algorithmic discovery. This innovation condenses the traditional journey from awareness to purchase into mere minutes. Start-ups, often without shelf access, are gaining traction through influencer-led flash promotions. Meanwhile, established multinationals are leveraging these same channels to counteract sluggish offline sales. The surge in Southeast Asian imports of Chinese cosmetics highlights a logistics evolution, seamlessly connecting factories to consumers. As a result, short-form videos have emerged as a pivotal growth catalyst for the hair loss treatment market in the Asia-Pacific region.

Tech-enabled therapies and personalization

Low-level laser helmets, exosome-enriched serums, and AI-driven scalp analysis apps are reshaping treatment paradigms by offering innovative and personalized solutions for hair loss. FDA-cleared laser devices achieve density gains in just 16 weeks, leading affluent users to complement or even substitute pharmacotherapy, as these devices provide a non-invasive and convenient alternative. Japan and South Korea, at the forefront of device and biomaterial patent filings, are establishing themselves as technology exporters to their neighboring markets, leveraging their advanced research and development capabilities. Diagnostic software measures sebum levels, inflammation, and follicle density with high precision, enabling clinicians and retailers to recommend tailored regimens that command premium pricing. These advancements not only enhance perceived efficacy but also bolster brand loyalty, driving the premiumization trend in the Asia-Pacific hair loss treatment market, where consumers increasingly seek effective and high-quality solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced and prescription treatments | -0.9% | Japan, South Korea, Australia, urban China | Medium term (2-4 years) |

| Side-effects and variable efficacy of key actives | -0.6% | Global, with heightened concern in Japan, South Korea | Long term (≥ 4 years) |

| Proliferation of counterfeit/unregistered products | -0.8% | India, Southeast Asia (Vietnam, Thailand, Indonesia), China tier-2/3 cities | Short term (≤ 2 years) |

| Platform takedown policies causing supply volatility for niche brands | -0.5% | China, South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost of advanced and prescription care

High prices, often reaching several thousand U.S. dollars, limit autologous cell therapies to affluent urban consumers, restricting accessibility for a broader demographic. In South Korea, FUE transplant packages range from USD 3,000 to 15,000, posing a significant financial hurdle for middle-income individuals, even in medical-tourism hotspots known for their price sensitivity. While newly approved biologics like JAK inhibitors offer enhanced efficacy and represent a breakthrough in treatment options, their premium pricing remains a challenge unless insurers broaden their reimbursement policies to make these therapies more accessible. Platelet-rich plasma treatments, necessitating multiple sessions over time, lead to escalating out-of-pocket costs for patients, particularly in markets with limited or no aesthetic coverage. This growing disparity between affordable generics and high-margin clinical solutions is slowing the overall uptake of hair loss treatments in the Asia-Pacific region, highlighting the need for more cost-effective and inclusive solutions.

Counterfeit and unregistered formulations

Regulators in Singapore, Thailand, and Vietnam have ramped up efforts against illicit minoxidil and finasteride, conducting intensified raids to curb the distribution of these unauthorized products. However, parallel imports and gray-market e-commerce channels continue to thrive, undermining regulatory efforts. A 2024 ban in India on 156 fixed-drug combinations not only disrupted supply chains but also inadvertently prompted online sellers to repackage these banned formulas under new labels, creating additional challenges for enforcement agencies[2]Source: Ministry of Health and Family Welfare, "156 FDCs banned with immediate effect, declared irrational", mohfw.gov.in. Meanwhile, China's draft efficacy guidelines are inflating compliance costs, forcing some undercapitalized brands to either cut corners in production or withdraw from the market entirely. As consumers grapple with inconsistent product quality, their trust in available treatments erodes, often delaying the start of therapy and impacting overall market growth. This ongoing battle with counterfeiting not only undermines brand equity but also stifles the potential for premium trading-up in the Asia-Pacific hair loss treatment market, limiting opportunities for higher-value product segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Daily-Use Shampoos Dominate, Serums Gain Clinical Momentum

In 2024, shampoos and conditioners dominated the Asia-Pacific hair loss treatment market, accounting for 52.61% of the revenue. Their success stemmed from being daily staples, priced affordably under USD 5, and widely available in mass channels. Formulations designed for daily use are now integrating actives like keratin and hyaluronic acid, promoting scalp and fiber health without altering consumer habits. However, the rinse-off nature of these products limits the duration of active ingredient penetration, especially when compared to leave-on alternatives. Supermarkets and drugstores anchor this mass segment, with anti-hair-fall shampoos serving as accessible entry points for price-sensitive consumers. In response, multinationals are leveraging these high-volume formats as gateways, gradually steering users towards more specialized and higher-value solutions. While device-based options, such as laser helmets priced between USD 200 and USD 800, remain niche in volume, they bolster the perception of hair loss as a condition deserving intensive, multi-step management.

Serums are emerging as the fastest-growing segment, boasting a projected CAGR of 10.72%. Consumers are increasingly transitioning from standard shampoos to these leave-on solutions, drawn by promises of stronger, clinically-backed results. The prolonged contact of serums with the scalp boosts the effectiveness of actives like minoxidil, peptides, and cutting-edge exosome-based technologies. Typically priced between USD 30 and USD 100, serums occupy a premium market space. Products like V Medical Aesthetics’ exosome serum and Taiwanese offerings featuring banana-flower-derived DHT blockers highlight the trend of biotech innovations enhancing both performance and pricing in this segment[3]Source: TCI Co., LTD, "2023 Annual Report", tci-bio.com. Looking ahead five years, the trend of premiumization, coupled with major brands like Unilever acquiring science-driven indie labels, is set to amplify the serum's share in the Asia-Pacific hair loss treatment market, even as shampoos and conditioners maintain their lead in unit sales.

By Gender: Male Leadership Narrows Amid Rapid Female Upswing

In 2024, male consumers dominated the Asia-Pacific hair loss treatment market, accounting for 58.20% of the revenue. This trend is largely attributed to the widespread occurrence of androgenetic alopecia among men and the established treatment protocols that prominently feature minoxidil and finasteride. The male segment's dominance underscores a deep-rooted familiarity with these treatments, particularly those that are fast-acting and discreetly tailored to male preferences. On the other hand, the female segment is poised for rapid growth, projected at an 11.22% CAGR. This surge is bolstered by heightened awareness of issues like postpartum hair loss and hormonal imbalances. Furthermore, regulatory advancements, such as India's endorsement of minoxidil for female pattern hair loss and the proliferation of clinic services in nations like South Korea, are accelerating the adoption of gender-specific treatments.

Women are increasingly drawn to holistic treatment methods, blending traditional Chinese herbal remedies with contemporary light-based therapies, aligning with their wellness-centric approach. Social media platforms are pivotal in destigmatizing hair loss treatments, highlighting genuine transformations and heartfelt testimonials, and promoting timely interventions for all genders. Brands are adeptly tailoring their messaging and packaging: men's products spotlight fast-drying, discreet lotions, while women's offerings highlight botanical ingredients and wellness advantages. Given these dynamics, the Asia-Pacific hair loss treatment market is on track to witness a more equitable gender representation in the years ahead.

By Category: Topicals Rule, Oral Nutraceuticals Climb

In 2024, topical formulations led the Asia-Pacific hair loss treatment market, accounting for 94.32% of total expenditures. This dominance is largely attributed to the over-the-counter availability of minoxidil and its extensive clinical validation over the years. While consumers trust these proven active ingredients, challenges such as the need for twice-daily applications and potential scalp irritation can hinder consistent use. Topical products, ranging from shampoos and serums to lotions and foams, are readily available at both mass and premium price points in pharmacies and supermarkets. Established brands are reformulating these products with advanced delivery systems to reduce side effects and fend off competition from emerging alternatives. Additionally, topicals enjoy regulatory advantages, facing fewer hurdles than systemic or invasive treatments, further cementing their market position.

Oral nutraceuticals are the market's fastest-growing segment, projected to grow at a 9.41% CAGR. These products offer a convenient systemic alternative, avoiding the irritations and application challenges of topicals. Ingredients like biotin, saw palmetto, and marine collagen are popular, touted for their holistic benefits and facing lighter regulatory scrutiny in the supplement realm. Innovations, such as probiotic ferments and banana-stamen extracts from Taiwan, showcase the industry's push for diversification and differentiation from traditional topicals. Furthermore, emerging research on oxytocin-receptor agonists and cell-based therapies, highlighted in recent journals, sets higher efficacy standards and compels all market segments to adapt. Ultimately, the interplay of convenience, safety perceptions, and innovation will shape the trajectory of oral options in the Asia-Pacific hair loss treatment landscape.

By Distribution Channel: Digital Acceleration Challenges Storefront Dominance

In 2024, health and beauty chains seized 47.12% of the Asia-Pacific hair loss treatment market, thanks to curated product selections and in-store consultations that foster consumer trust. These chains adeptly steer customers towards both mass-market shampoos and premium serums, providing tailored advice that outshines the offerings of traditional supermarkets. Their ability to offer personalized recommendations, coupled with a wide range of specialized products, positions them as a preferred choice for consumers seeking effective solutions. While supermarkets play a role in selling budget-friendly, impulse items like anti-hair-fall shampoos, health and beauty outlets excel in higher-margin products, thanks to their knowledgeable staff and promotional bundles. The segment's strength is bolstered by its physical presence, allowing for product trials and immediate satisfaction, especially as demand for visible results surges. Additionally, the in-store experience often includes consultations with trained professionals, further enhancing consumer confidence and driving repeat purchases.

Online retail is the channel to watch, boasting the fastest growth rate, with projections of a 10.43% CAGR. This surge is fueled by smooth single-screen experiences, highlighted by livestream flash sales and smart algorithm recommendations. Platforms such as Douyin and Xiaohongshu play a pivotal role, swiftly converting casual interest into immediate purchases, thereby diminishing the shelf space advantages once held by traditional retailers. These platforms leverage advanced technologies to create engaging shopping experiences, such as interactive product demonstrations and real-time customer interactions, which significantly boost conversion rates. To counter potential pitfalls, like account suspensions due to unverified claims, brands are adopting omnichannel strategies. These strategies seamlessly blend digital initiatives with support from clinics and pharmacies, ensuring a balanced approach to market penetration. As digital policies evolve and fulfillment methods innovate, they will play a crucial role in determining the channel mix and shaping the future trajectories of the Asia-Pacific hair loss treatment market.

Geography Analysis

In 2024, China accounted for 37.18% of the regional revenue, driven by trends like premiumization, "skinification," and the rise of advanced livestream commerce. Sales of high-end shampoos, priced at CNY 120 and above, saw a remarkable 114% year-over-year surge. Highlighting China's pivotal role as a hub for both innovation and consumption, Henkel inaugurated a new research and development center in Shanghai. Meanwhile, newly drafted NMPA guidelines, which mandate clinical substantiation, are set to elevate compliance hurdles. This shift is likely to benefit resource-rich multinationals and disciplined domestic leaders. With hair transplant surgeries exceeding half a million annually, there's a clear demand for both surgical and regenerative solutions, bolstering the Asia-Pacific hair loss treatment market across various price tiers.

India is on track to achieve the fastest growth rate, projected at a 10.91% CAGR through 2030. This momentum is fueled by pharmaceutical innovations and the widespread adoption of digital payments in tier-2 and tier-3 cities. Dr. Reddy's recent launch of a female-pattern minoxidil underscores a regulatory shift towards gender-specific treatments. Simultaneously, Sun Pharma's FDA clearance for deuruxolitinib suggests an impending wave of biologic products. While recent bans on fixed drugs caused supply disruptions, they simultaneously created opportunities for compliant brands, leading to a surge in new product introductions. With the added boost of Production Linked Incentive schemes for bulk drugs, India is carving out a dual identity: a burgeoning growth engine and a pivotal export hub in the Asia-Pacific hair loss treatment landscape.

Japan, South Korea, and Australia stand as the mature triad in the region. Here, devices, regenerative medicine, and high-science topicals command premium prices. Shiseido's launch of a cell-based therapy in Tokyo, combined with South Korea's dominance in natural-ingredient and biomaterial patents, underscores the region's innovative prowess. Southeast Asia, which imported nearly USD 490 million worth of Chinese cosmetics last year, showcases a blend of aspiration and cost-sensitivity. Investments in follicle stem-cell banks in Thailand, alongside Vietnam's crackdown on counterfeit products, highlight the sub-region's swift transition from basic shampoos to sophisticated clinical offerings. These collective dynamics not only deepen market penetration but also enhance value creation in the Asia-Pacific hair loss treatment arena.

Competitive Landscape

In the Asia-Pacific hair loss treatment market, a moderate concentration is evident. Rinse-off basics see dominance from FMCG giants like L’Oréal, Unilever, and Procter & Gamble, leveraging their scale and marketing prowess. Meanwhile, pharmaceutical stalwarts such as Sun Pharma, Cipla, and Dr. Reddy’s navigate prescription corridors, championing treatments like minoxidil, finasteride, and the emerging JAK inhibitors. On the other hand, niche disruptors, including Nutrafol, Capillus, and Viviscal are making waves by adopting direct-to-consumer models and forging influencer partnerships, thereby appealing to affluent early adopters and broadening the market's addressable base.

South Korea, accounting for 42.9% of global patent filings in hair-loss cosmetics, empowers its formulators to license active ingredients to manufacturers in China and Southeast Asia. This strategy effectively exports technology with minimal marketing expenditure. Corporate maneuvers spotlight mergers and acquisitions: Unilever's acquisitions of K18 and Minimalist enhance its peptide and clinical offerings, while Shiseido's stake in Kobe’s cell-processing facility underscores its quest for supply chain independence. With regulators tightening the reins on efficacy claims, the ability of corporations to present robust clinical dossiers could delineate the industry's frontrunners from its laggards.

Opportunities abound in mid-priced device therapies, AI-driven scalp diagnostics, and nutraceuticals tailored for postpartum women. Brands that meld diagnostics with subscription-based treatment packages stand to secure consistent revenue streams and shield themselves from imitation threats. With the top five players commanding a combined market share of around 60%, there's a window for specialized challengers to carve out loyalty niches, doing so without inciting swift retaliation from established incumbents.

Asia-Pacific Hair Loss Treatment Products Industry Leaders

-

Loreal S.A.

-

Procter & Gamble Co

-

The Himalaya Drug Company

-

Johnson & Johnson Consumer Inc.

-

Henkel AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Ayunature Care, under the guidance of Ayurvedic physician Dr. Renuka Siddhpura, introduced a pioneering Five-Product Ayurvedic Hair Restoration System. This initiative aims to combat the escalating hair loss concerns of over 30 million Indians. Marketed as a holistic, chemical-free alternative to traditional treatments, the system not only seeks to rejuvenate confidence but also bolsters Ayunature's ambition to broaden its wellness centre footprint both in India and internationally.

- August 2025: Bare Anatomy, powered by Innovist, unveiled its EXPERT Anti-Hair Fall Shampoo. This clinically-backed formula promises to combat daily and seasonal hair fall, boasting up to 5X more effectiveness than standard shampoos.* The shampoo harnesses the power of Adenosine to curb hair fall and enhance thickness, while Procapil works to diminish thinning and fortify roots, promoting overall scalp health and hair density.

- August 2025: Hair ResQ bolstered its thinning-hair lineup with three innovative products. These additions are crafted to fortify, volumize, and safeguard delicate strands. The updated range features the Shine Boost Biotin Shampoo, designed to amplify shine and promote a fuller appearance. Additionally, there's a Thickening Treatment infused with advanced biotin for enhanced volume, and a specialized scalp solution aimed at invigorating roots and boosting hair density.

Asia-Pacific Hair Loss Treatment Products Market Report Scope

The Asia-Pacific Hair Loss Treatment Products market is segmented by distribution channel and geography. By distribution channel, the market is segmented into supermarkets and hypermarkets, convenience stores, department stores, pharmacies & drug stores, specialist retailers, online retail and others. Based on geography, the study provides an analysis of Asia Pacfic hair loss treatment market in China, India, Japan, Australia, and Rest of Asia Pacific.

By Type

| Shampoos and Conditioners |

| Serums |

| Others |

By Gender

| Male |

| Female |

By Category

| Topical |

| Oral |

By Distribution Channel

| Health and Beauty Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Distribution Channels |

Country

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| South Korea |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| By Type | Shampoos and Conditioners |

| Serums | |

| Others | |

| By Gender | Male |

| Female | |

| By Category | Topical |

| Oral | |

| By Distribution Channel | Health and Beauty Stores |

| Supermarkets/Hypermarkets | |

| Online Retail Stores | |

| Other Distribution Channels | |

| Country | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific hair loss treatment market in 2025?

It is valued at USD 0.68 billion and is projected to hit USD 1.05 billion by 2030.

What is the expected CAGR for hair-loss therapies in Asia-Pacific?

The market is forecast to register a 9.01% CAGR from 2025 to 2030.

Which product type currently leads sales?

Shampoos and conditioners hold 52.61% of 2024 revenue, reflecting daily-use convenience.

Which country is poised for the fastest growth through 2030?

India is expected to expand at a 10.91% CAGR owing to pharma innovation and e-commerce reach.

Page last updated on: