Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.84 Billion |

| Market Size (2026) | USD 0.9 Billion |

| Market Size (2031) | USD 1.23 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Hair Loss Treatment Products Market Analysis by Mordor Intelligence

The Europe hair loss treatment products market size was valued at USD 0.84 billion in 2025 and estimated to grow from USD 0.9 billion in 2026 to reach USD 1.23 billion by 2031, at a CAGR of 6.62% during the forecast period (2026-2031). The growing demand for effective solutions to combat hair loss, coupled with the rising adoption of natural and organic products, is significantly influencing market dynamics. The aging population across Europe is a key driver, as hair loss is a common concern among older demographics. Additionally, younger consumers are increasingly seeking preventive measures and treatments, further fueling market growth. The availability of over-the-counter (OTC) products, including shampoos, serums, and supplements, has made hair loss treatments more accessible to a broader audience. Social media platforms and digital marketing campaigns are playing a pivotal role in raising awareness and promoting various hair loss treatment products, thereby boosting consumer engagement. Technological advancements in the formulation of hair loss treatments, such as the incorporation of active ingredients like minoxidil and finasteride, are enhancing product efficacy and driving consumer trust. Furthermore, the market is witnessing a surge in demand for personalized solutions, with companies offering tailored products based on individual hair and scalp conditions. The competitive landscape is evolving rapidly, with key players focusing on innovation, mergers, acquisitions, and strategic partnerships to strengthen their foothold in the market. Companies are also investing in research and development to introduce advanced products that cater to diverse consumer needs.

Key Report Takeaways

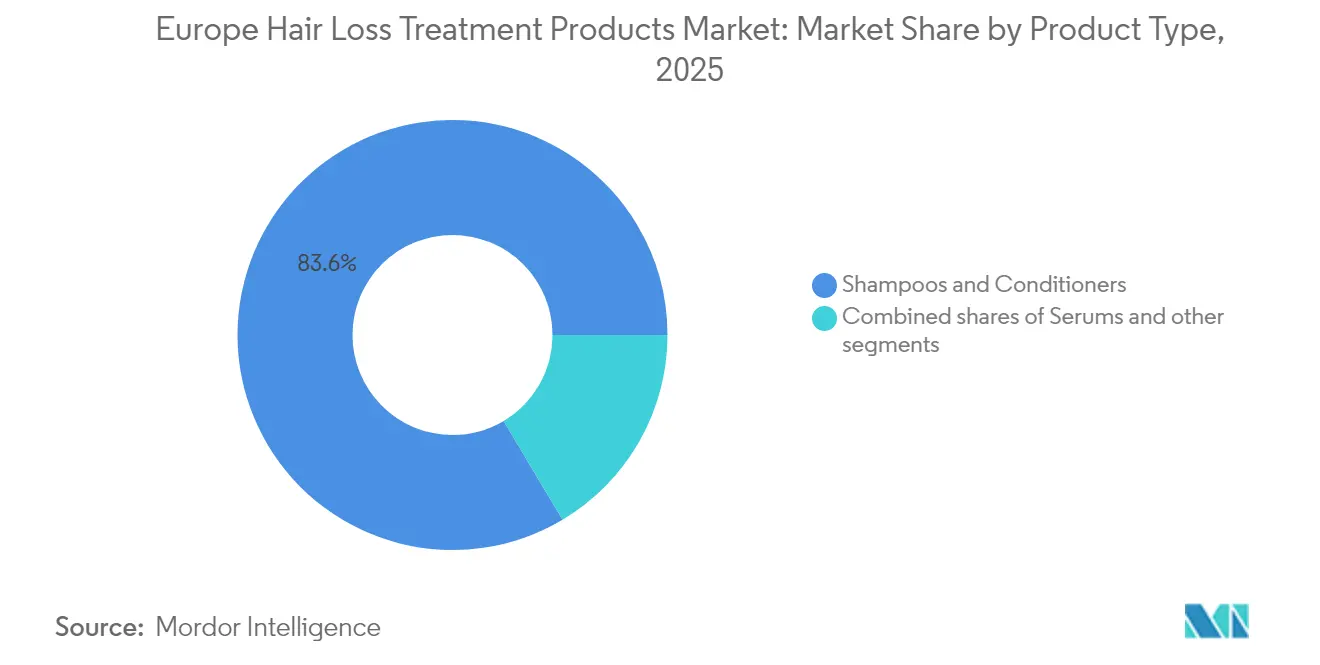

- By product type, shampoos and conditioners held 83.55% of the Europe hair loss treatment products market share in 2025, while serums are forecast to expand at a 6.92% CAGR through 2031.

- By gender, females accounted for 68.74% of 2025 revenue, whereas male demand is advancing at a 6.85% CAGR to 2031.

- By category, topical formats commanded 90.58% of the Europe hair loss treatment products market size in 2025 and oral products are set to grow at 7.12% CAGR over the forecast horizon.

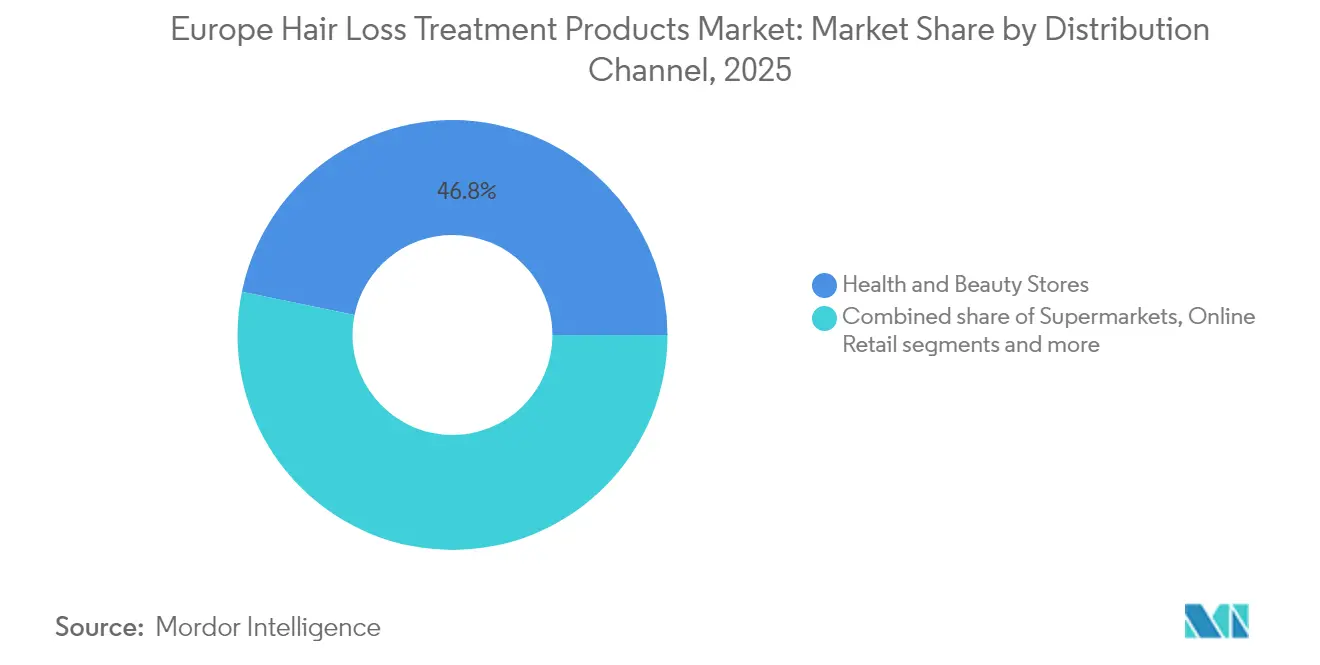

- By distribution channel, health and beauty stores led with 46.78% share in 2025; online retail stores deliver the fastest CAGR at 6.88% on the back of privacy-driven purchasing behavior.

- By geography, Germany secured 20.12% revenue share in 2025, while Spain is poised for the highest 7.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Hair Loss Treatment Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of male pattern baldness and increasing hair loss issues | +1.8% | Europe-wide, with highest impact in Spain, Germany, Czech Republic | Long term (≥ 4 years) |

| Growing awareness and concern about personal appearance and grooming | +1.5% | Western Europe core, expanding to Eastern Europe | Medium term (2-4 years) |

| Rising demand for natural and organic hair loss treatment products | +1.2% | Germany, Netherlands, Scandinavia with spillover to France, Italy | Medium term (2-4 years) |

| High incidence of age-related hair thinning due to an aging population | +1.0% | Netherlands, Germany, Italy with demographic transition | Long term (≥ 4 years) |

| Availability of advanced and innovative hair loss treatment solutions | +0.8% | Technology hubs: Germany, Netherlands, France | Short term (≤ 2 years) |

| Social media influence promoting awareness and acceptance of hair loss treatments | +0.7% | Spain, United Kingdom, France with high social media penetration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High prevalence of male pattern baldness and increasing hair loss issues

Male pattern hair loss (MPHL), also known as male androgenetic alopecia, is a highly heritable and age-dependent condition affecting a large proportion of men in Europe. According to a 2023 report by the National Institute of Health, hair loss in European men can begin as early as puberty, with a lifetime prevalence estimated to be approximately 80% [1]Source: National Center for Biotechnology Information, "Male-pattern hair loss: Comprehensive identification of the associated genes as a basis for understanding pathophysiology", pmc.ncbi.nlm.nih.gov. The condition is characterized by a progressive and distinct pattern of hair thinning and loss, typically starting with recession at the temples and thinning at the crown, eventually leading to baldness on the top of the scalp. This progressive hair loss has significant psychological and social effects, impacting self-esteem, confidence, and overall quality of life. The genetic basis of MPHL is strong, with androgen hormones playing a central role in follicular miniaturization and hair cycle disruption. Given its high prevalence and profound emotional impact, MPHL continues to be a key driver of demand for hair loss treatment products in Europe, encouraging innovation and the adoption of a range of therapeutic options.

Growing awareness and concern about personal appearance and grooming

Consumers in Europe are increasingly prioritizing convenience and protective benefits when purchasing wellness and beauty products. A 2023 survey conducted by Professional Beauty revealed that UK consumers, on average, spend GBP 4,600 annually on wellness-related products [2]Source: Professional Beauty, “Brits spend over £4.5K on self-care annually”, professionalbeauty.co.uk . . This substantial expenditure reflects a growing commitment to self-care and grooming, as consumers actively seek high-quality, effective, and convenient solutions to enhance their personal appearance and overall well-being. They are not only investing in products that deliver visible results but are also showing a preference for brands that align with their values, such as sustainability and ethical sourcing. The beauty and personal care sector continues to demonstrate robust growth and resilience, playing a significant role in strengthening the regional economy and driving advancements in treatments and product innovations. This ongoing trend highlights the market's shift towards premiumization, with consumers increasingly demanding scientifically advanced formulations that cater to their evolving needs and expectations.

Rising demand for natural and organic hair loss treatment products

There is a rising demand for natural and organic hair loss treatment products in Europe, driven by increasing consumer awareness of the potential harmful effects of chemicals in conventional formulations. Consumers are increasingly seeking products that offer effective results while aligning with their preferences for sustainable and clean-label ingredients. This trend is supported by a growing focus on health, safety, and environmental responsibility, encouraging manufacturers to innovate with plant-based, cruelty-free, and eco-friendly formulations. Additionally, leading players in the market are responding by expanding their portfolios to include natural and organic options, which cater to a broader demographic concerned with both aesthetics and wellness. This shift towards natural and organic products not only enhances consumer trust but also supports long-term market growth by addressing evolving ethical and regulatory standards in Europe.

High incidence of age-related hair thinning due to an aging population

The aging population is emerging as a critical factor influencing the Europe Hair Loss Treatment Products Market. With a growing number of individuals entering the 65-and-older age group, the prevalence of age-related hair thinning and hair loss is becoming increasingly common. This demographic shift is driven by rising life expectancy and persistently low birth rates, which are contributing to a steady expansion of the elderly population across the European Union. According to Eurostat, as of January 1, 2024, the EU's population was approximately 449.3 million, with over 21.6% falling into this age category [3]Source: Eurostat, "Population Structure and Ageing", ec.europa.eu. This trend is reshaping market demands, as older adults seek effective solutions tailored to their specific hair loss challenges. In response, manufacturers and marketers are focusing on developing innovative products that cater to the unique needs of this growing consumer segment, ensuring that the market evolves in alignment with the demographic changes occurring throughout Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of hair loss treatment products limiting consumer affordability | -1.5% | Eastern Europe, Southern Europe with lower disposable income | Medium term (2-4 years) |

| Side effects and allergies associated with certain chemical-based products | -1.2% | Europe-wide due to regulatory scrutiny, particularly Germany, France | Short term (≤ 2 years) |

| Availability of counterfeit and low-quality products in the market | -0.8% | Online channels across Europe, particularly affecting premium segments | Medium term (2-4 years) |

| Lack of consumer knowledge regarding hair loss causes and treatments | -0.5% | Rural areas and older demographics across Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost of hair loss treatment products limiting consumer affordability

The high cost of hair loss treatment products is a significant restraint on consumer affordability within the Europe Hair Loss Treatment Products Market. Premium products, including clinically approved topical treatments, oral medications, and advanced therapies such as platelet-rich plasma (PRP) and stem cell treatments, often carry price points that can be prohibitive for many consumers. For example, hair transplant procedures in Europe can range from approximately ERU 2,850 to EUR 12,000 depending on the clinic and treatment scope, while ongoing topical and oral treatments frequently require consistent investment over time. These costs, combined with limited insurance coverage for cosmetic treatments, restrict market accessibility, particularly among lower-income consumer segments. Additionally, the availability of alternative treatment methods such as surgery or laser therapy introduces competitive pressure, complicating purchasing decisions. Consequently, high pricing remains a considerable challenge that manufacturers and marketers must address to expand the user base and fully tap into the European market potential.

Side effects and allergies associated with certain chemical-based products

Side effects and allergic reactions associated with certain chemical-based hair loss treatment products pose a significant restraint for the Europe Hair Loss Treatment Products Market. Widely used medications such as finasteride, while effective, have been linked to serious adverse effects including sexual dysfunction, depression, and, in rare cases, suicidal thoughts. Topical treatments like minoxidil may cause scalp irritation, dryness, and allergic contact dermatitis in some users. These potential side effects raise concerns among consumers and healthcare providers, often limiting product adoption and long-term compliance. Moreover, increasing reports of adverse reactions have prompted stricter regulatory warnings and calls for improved safety monitoring. This risk profile encourages consumers to seek safer, natural alternatives, creating challenges for chemical-based treatments to maintain market share while driving the need for innovation focused on minimizing side effects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Serums Drive Innovation Despite Shampoo Dominance

Shampoos and conditioners held the dominant position in the Europe hair loss treatment products market in 2025, capturing a significant 83.55% share. Their strong presence is largely attributed to their established role as everyday essentials in personal grooming routines, offering convenience and familiarity to a wide base of consumers. These formats are perceived as easy-to-use, low-effort solutions that can be seamlessly integrated into existing hair care habits without requiring additional time or learning. This inherent accessibility continues to appeal to both new and existing consumers, reinforcing their popularity across diverse demographic segments. Moreover, shampoos and conditioners are widely available across retail channels, ranging from supermarkets to specialty stores, further supporting their leadership in this market. Their dominance also reflects consumer trust in tried-and-tested product forms, which are often the first line of defense when addressing hair loss concerns.

In contrast, serums represent the fastest-growing segment, projected to expand at a CAGR of 6.92% through 2031. Unlike traditional daily-use formats, serums are positioned as specialized treatments that deliver a higher concentration of active ingredients directly to the scalp or hair roots. This targeted approach resonates strongly with consumers seeking effective and visible solutions for hair thinning and loss, especially amid rising awareness of advanced treatment options. Their association with premiumization has further elevated the segment, as many serums are marketed with advanced formulations and clinically backed efficacy claims. Additionally, the growth of e-commerce and direct-to-consumer channels has made serums more accessible, enabling brands to highlight their value proposition to niche yet growing consumer groups. As personal care moves toward a focus on results-driven and customized solutions, serums are set to gain momentum as a preferred choice for consumers demanding more targeted outcomes.

By Gender: Male Acceleration Challenges Female Dominance

Female consumers commanded the largest share of the Europe hair loss treatment products market in 2025, accounting for 68.74% of the total. This dominance stems from the higher level of awareness among women regarding hair care and the greater emphasis placed on personal appearance and grooming. Women are more likely to seek proactive solutions to manage hair thinning or loss, making them the primary target group for a wide range of treatment products. Additionally, marketing strategies across brands often focus heavily on female consumers, reinforcing both visibility and adoption rates within this segment. The availability of diverse product formats, from shampoos and conditioners to advanced serums, further supports their engagement with the category. As a result, the female segment maintains its leading position, sustained by strong demand arising from lifestyle-driven concerns and ongoing self-care trends.

On the other hand, male consumers represent the fastest-growing segment, projected to expand at a CAGR of 6.85% between 2025 and 2031. This growth highlights a significant shift in treatment acceptance patterns among men, who are increasingly open to adopting preventive and corrective solutions for hair loss. Social changes and the reduced stigma around male grooming and self-care are key factors fueling this trend. Furthermore, the rising demand for targeted solutions, such as hair growth serums and scalp therapies designed specifically for men, has accelerated interest within this segment. The influence of digital platforms and direct-to-consumer marketing has also played a vital role in normalizing treatment options for male consumers, encouraging broader adoption. Consequently, the male demographic is evolving into a critical growth driver for the market, reshaping long-term demand dynamics within the hair loss treatment landscape.

By Category: Oral Treatments Gain Despite Topical Leadership

Topical treatments dominated the Europe hair loss treatment products market in 2025, securing a substantial 90.58% share. Their widespread adoption is primarily attributed to consumer preference for localized application methods, which are perceived as easier to use and more familiar compared to systemic alternatives. The direct application to the scalp provides a sense of targeted action, giving consumers confidence in the product’s effectiveness without the complexities associated with oral or prescription-based options. Perceived safety is another critical factor, as topical treatments are generally viewed as carrying fewer risks and side effects compared to systemic solutions. This perception has reinforced consumer trust, making them the first-line choice for individuals beginning hair loss treatments. In addition, the wide availability of topical products across retail, pharmacy, and online channels enhances accessibility, ensuring their continued dominance in the market landscape.

In contrast, oral treatments represent the fastest-growing category, projected to expand at a CAGR of 7.12% through 2031. Their rising appeal is connected to the increasing recognition of convenience, as oral formats require minimal time and effort compared to daily topical applications. Recent advancements in low-dose oral protocols have further strengthened confidence among consumers and healthcare providers by reducing potential side effect risks, which historically limited acceptance. This evolution is broadening the appeal of oral treatments beyond severe cases, fostering uptake among a wider consumer base seeking effective but manageable solutions. The growing endorsement of oral therapies in clinical recommendations and professional consultations is also bolstering credibility, driving stronger consideration rates. With greater innovation, rising consumer education, and expanding prescription accessibility, oral treatments are poised to reshape the competitive dynamic of the hair loss treatment products market over the coming years.

By Distribution Channel: Digital Transformation Accelerates

Health and beauty stores secured the largest share of the Europe hair loss treatment products market in 2025, accounting for 46.78% of the total. Their strong position is underpinned by advantages such as personalized consultations, where trained professionals can guide consumers toward the most suitable products. These outlets also provide opportunities for product sampling and trials, enabling consumers to experience formulations firsthand before committing to a purchase. Such experiential benefits foster greater trust and confidence in product efficacy, reinforcing loyalty to this distribution channel. The physical presence of health and beauty stores also allows brands to create an engaging retail environment, strengthening awareness and brand positioning. Combined with their ability to offer expert-driven recommendations, these stores continue to be the most influential and dependable sales avenue within the market.

In contrast, online retail stores represent the fastest-growing distribution channel, projected to register a notable 6.88% CAGR through 2031. The rapid expansion of e-commerce reflects the broader digital transformation of consumer buying behaviors, driven by convenience, accessibility, and the growing trust in online transactions. Online platforms provide a vast assortment of hair loss treatment products, empowering consumers to compare options, read reviews, and access professional endorsements at their convenience. In addition, subscription services and direct-to-consumer brands are gaining traction through online channels, offering cost savings and the ease of regular product delivery. Digital marketing strategies, including targeted advertising and social media campaigns, have further increased visibility and consumer engagement in this space. As shoppers continue to embrace digital purchasing habits and seek flexible access to specialized solutions, online retail stores are positioned to play a central role in shaping future market growth.

Geography Analysis

Germany emerged as the leading country in the Europe hair loss treatment products market in 2025, capturing 20.12% of the total revenue share. The country’s strong market presence is supported by high consumer awareness of hair health solutions, coupled with a well-established pharmaceutical and cosmetic industry that ensures the availability of advanced treatment options. German consumers are also highly receptive to preventive healthcare measures, driving consistent demand across both topical and oral formats. Furthermore, the country benefits from a dense network of pharmacies, health and beauty retailers, and specialized clinics, providing broad accessibility to professional consultations and products. Rising disposable incomes and lifestyle-driven grooming habits further reinforce Germany’s position as a key market driver. With continued emphasis on product innovation and clinically validated formulations, Germany is expected to maintain its leadership status in the regional landscape.

Spain, meanwhile, is projected to record the highest growth rate in the market, with a 7.05% CAGR anticipated through 2031. This expansion is fueled by growing consumer awareness of hair loss treatments, particularly among younger demographics who are increasingly adopting beauty and personal care regimens. Spanish consumers are showing greater willingness to experiment with premium and innovative solutions such as serums and oral supplements, reflecting shifting preferences toward targeted and convenient formats. The strong rise of e-commerce platforms and digital consultations in Spain has also expanded accessibility, making advanced solutions available to a wider segment of the population. Awareness campaigns and dermatologist-led endorsements are further building trust, accelerating adoption levels across both male and female consumers.

Beyond Germany and Spain, other European countries collectively represent a significant share of the hair loss treatment products market and contribute to the region’s overall growth. Markets such as France, the United Kingdom, and Italy continue to remain influential, each supported by strong beauty and personal care industries and high consumer spending on grooming products. Northern European countries, including Sweden and Denmark, are seeing emerging demand linked to lifestyle-driven health awareness and the rising adoption of premium solutions. Meanwhile, Eastern European markets are witnessing steady growth as increasing disposable incomes and expanding retail penetration enhance access to advanced treatments. These diverse country-level dynamics highlight the regional market’s complexity, where mature Western markets remain dominant while rapidly expanding southern and eastern markets contribute fresh growth momentum.

Competitive Landscape

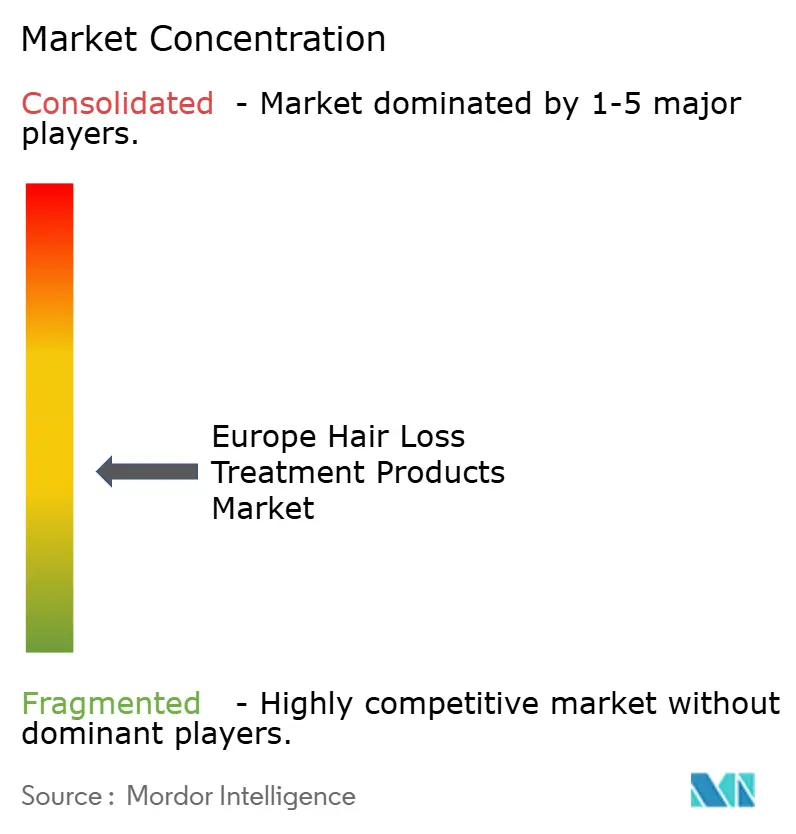

The European hair loss treatment products market demonstrates a moderately concentrated competitive landscape, with a score of 4 indicating balanced dynamics. This market features a mix of established pharmaceutical and consumer goods companies competing alongside emerging biotechnology firms and specialized device manufacturers. The competitive environment is shaped by the presence of key players who leverage their extensive resources and expertise to maintain their market positions while facing challenges from new entrants and evolving consumer preferences. Additionally, the market is influenced by increasing consumer awareness regarding hair loss treatments, which has led to a surge in demand for innovative and effective solutions.

Major players such as Procter & Gamble, L'Oréal, Henkel, and Unilever dominate the market by utilizing their expansive distribution networks and significant investments in research and development. These companies focus on developing innovative products and expanding their product portfolios to cater to a diverse consumer base. Their strong brand recognition and global presence provide them with a competitive edge, enabling them to capture a substantial share of the market. However, these established players must continuously adapt to changing regulatory frameworks and consumer demands to sustain their growth. Furthermore, partnerships and collaborations with dermatologists and trichologists are becoming a key strategy for these companies to enhance product credibility and reach.

Despite the dominance of these major companies, the market is witnessing increasing competition from smaller biotechnology firms and specialized device manufacturers. These emerging players are introducing advanced technologies and alternative treatment modalities, which are gaining traction among consumers seeking effective and non-invasive solutions. Additionally, regulatory scrutiny of traditional treatments is driving innovation, as companies strive to develop safer and more efficient products. The growing trend of e-commerce and direct-to-consumer sales channels is also enabling smaller players to compete more effectively by reaching a broader audience and reducing dependency on traditional retail networks. This dynamic environment fosters a competitive yet evolving market landscape in the European hair loss treatment products sector.

Europe Hair Loss Treatment Products Industry Leaders

-

Natura & Co.

-

Procter & Gamble Company

-

Henkel AG & Co., KGaA

-

Unilever PLC

-

L'Oréal SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Grabity, an anti-hair loss K-beauty brand crafted by top scientists from MIT and KAIST, made its European debut, underscoring a pivotal moment in its global growth journey. At FOIRE DE PARIS 2025, France's premier consumer goods expo, Grabity unveiled its offerings, including the Hair Lifting Shampoo and the newly introduced Hair Lifting Shot. These products emphasize a dual benefit: curbing hair loss while boosting volume. The brand's initial supply of 5,000 units flew off the shelves, testament to the overwhelming demand.

- February 2025: Mallia Therapeutics and Northway Biotech announced a strategic partnership to develop cGMP manufacturing processes for soluble CD83 protein as a topical treatment for androgenetic alopecia and alopecia areata, targeting hair follicle formation through novel immunomodulatory mechanisms.

- July 2024: Kintor Pharmaceutical, a clinical-stage biotechnology firm, has unveiled a topical solution targeting androgenetic alopecia (AGA) after securing the International Nomenclature Cosmetic Ingredient (INCI) approval for its proprietary KX-826. The newly launched cosmetic prominently features KX-826 as its primary component. "KX-826 gel serves as a precisely targeted topical androgen receptor antagonist.

Europe Hair Loss Treatment Products Market Report Scope

Hair-loss treatment products include all haircare products that claim to stop, control, or prevent hair loss.

The European hair loss treatment products market report analyses the recent trends, drivers, and challenges regarding the market. The market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into shampoo & conditioners, oils, serums, and other product types. By distribution channel, the market is segmented into supermarkets/hypermarkets, pharmacies, specialty stores, online retail stores, and other distribution channels. By geography, the market covers Germany, the United Kingdom, France, Spain, Italy, Russia, and other geographies. For each segment, the market sizing and forecasts have been done on the basis of value in USD million.

By Product Type

| Shampoos and Conditioners |

| Serums |

| Others |

By Gender

| Male |

| Female |

By Category

| Topical |

| Oral |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Shampoos and Conditioners |

| Serums | |

| Others | |

| By Gender | Male |

| Female | |

| By Category | Topical |

| Oral | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Health and Beauty Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe hair loss treatment products market?

The market is valued at USD 0.9 billion in 2026.

How fast is the market expected to grow?

It is projected to record a 6.62% CAGR, reaching USD 1.23 billion by 2031.

Which product type is expanding the quickest?

Serums lead growth with a 6.92% CAGR as consumers seek concentrated, leave-on solutions.

Why is Spain growing faster than other countries?

Spain combines the continent’s highest male baldness prevalence with rising per-capita beauty spending, driving a 7.05% CAGR.

How are online channels influencing sales?

E-commerce delivers discretion, subscription convenience and influencer discovery, growing at a 6.88% CAGR across the region.

Page last updated on: