Hair Mask Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

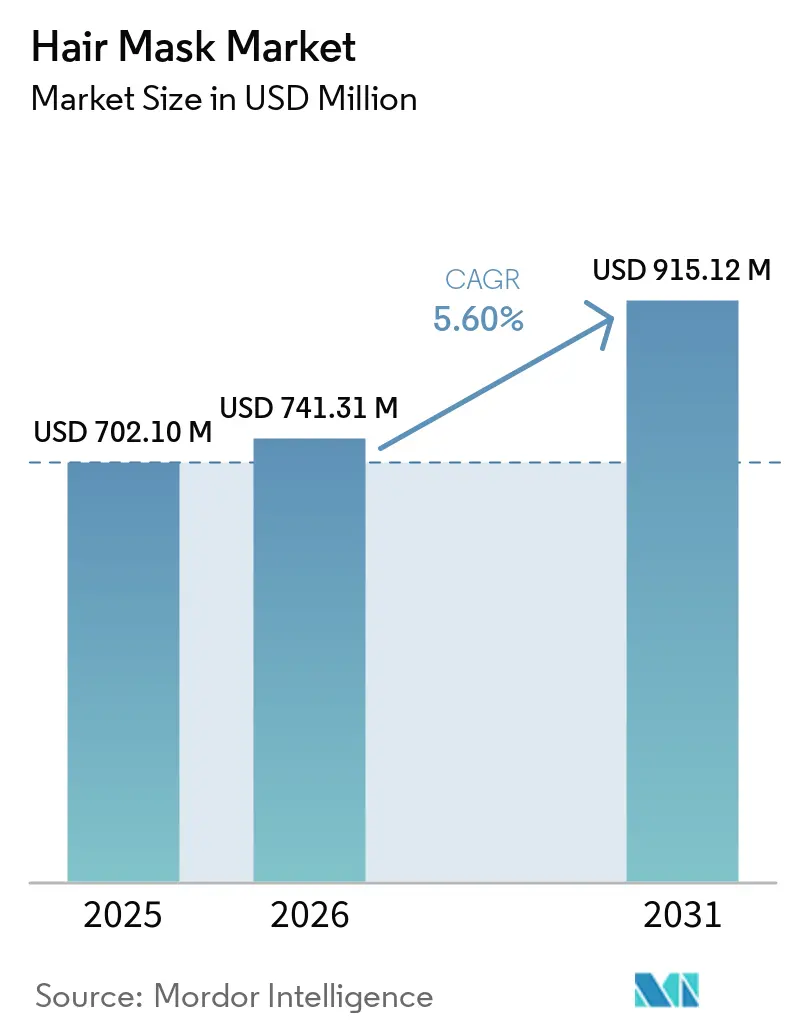

| Market Size (2026) | USD 741.31 Million |

| Market Size (2031) | USD 915.12 Million |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

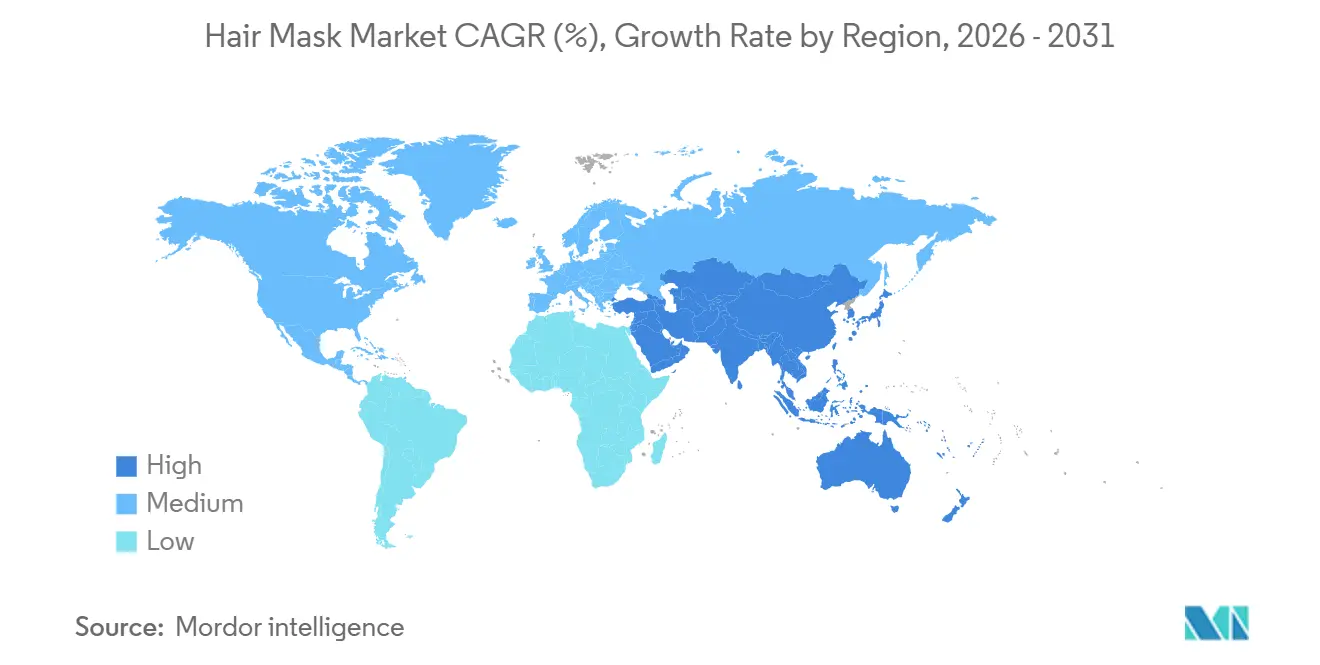

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

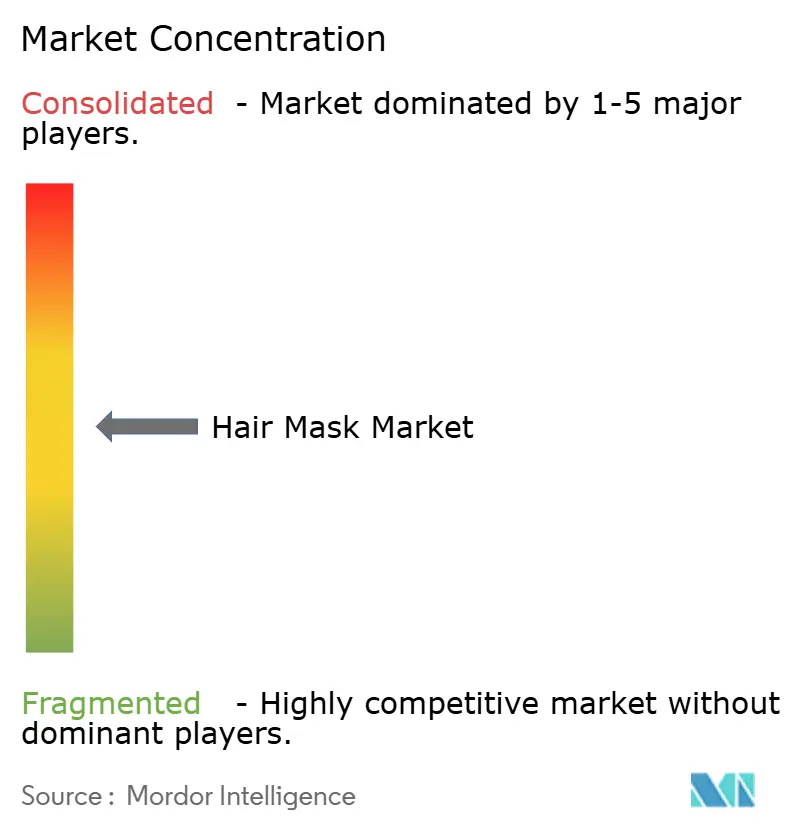

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hair Mask Market Analysis by Mordor Intelligence

The global Hair Mask market is projected to expand from USD 702.1 million in 2025 to USD 741.31 million in 2026, reaching approximately USD 915.12 million by 2031, reflecting a CAGR of 5.6% over 2026–2031. This growth trajectory is underpinned by shifting consumer behavior, regulatory changes, and the accelerating influence of digital commerce. The sector is increasingly defined by the integration of reparative treatments into weekly at-home routines, effectively blurring the boundary between professional salon services and everyday maintenance. Bans and restrictions on silicones and microplastics are shortening product reformulation cycles, compelling companies to adopt agile R&D models [1]European Commission, “Commission Regulation (EU) 2023/2055 on Microplastics,” europa.ec. In this environment, brands that quickly pivot toward peptide-rich formulations and plant-based actives are gaining a competitive edge, capturing consumer trust and loyalty ahead of slower-moving incumbents.

Key Report Takeaways

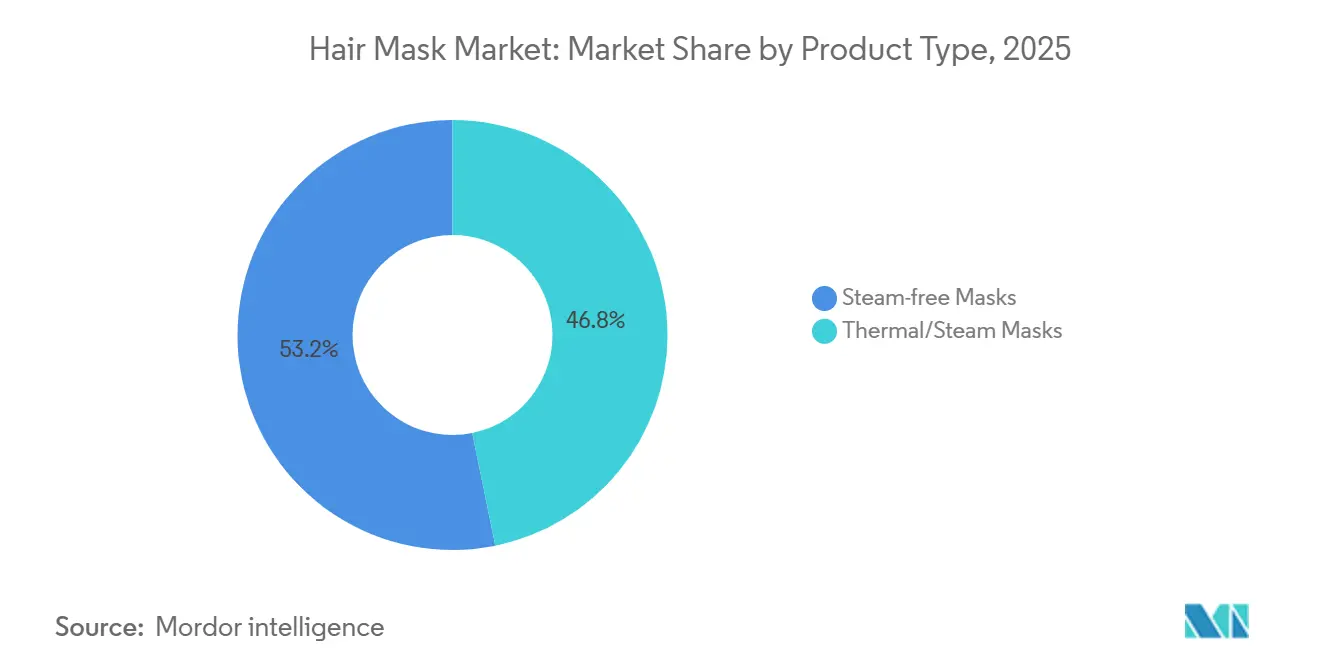

- By product type, steam-free masks led with 53.18% revenue share in 2025; thermal steam masks are forecast to expand at a 6.40% CAGR through 2031.

- By packaging type, pouches accounted for 50.12% of the Hair Mask market share in 2025, whereas jars are projected to register a 5.85% CAGR between 2026 and 2031.

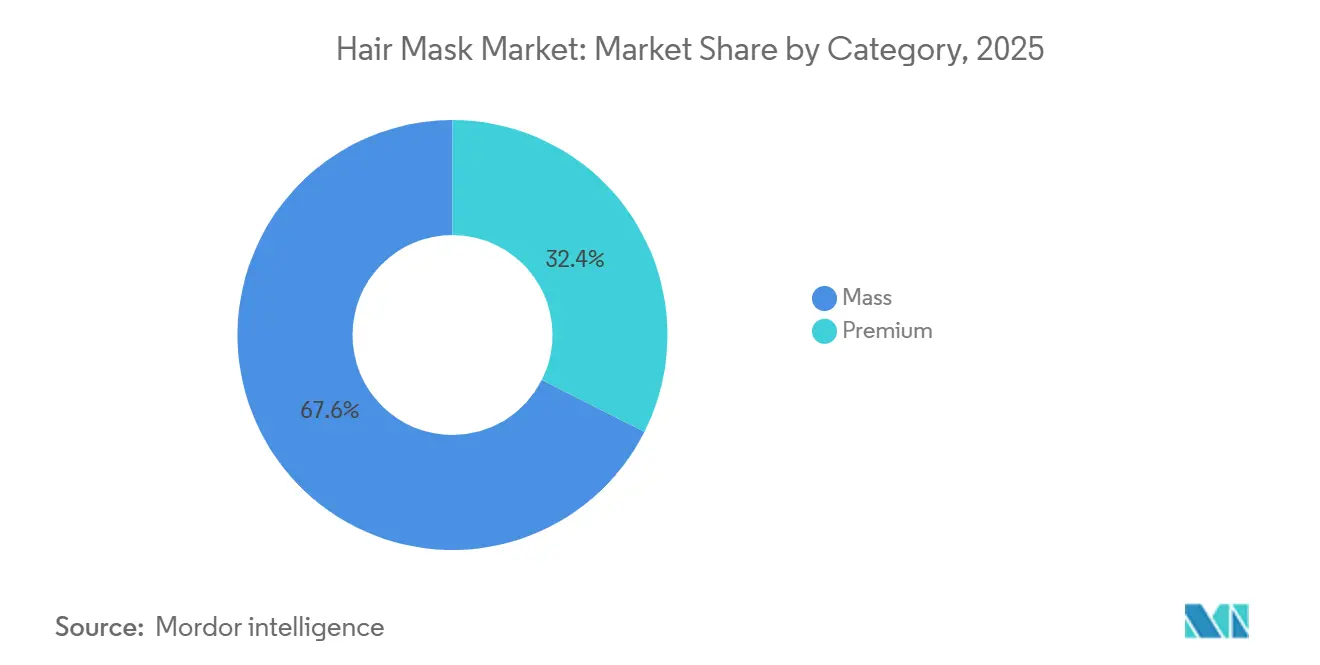

- By category, the mass segment accounted for 67.58% of the Hair Mask market size in 2025, while premium masks are expected to grow at a 6.25% CAGR through 2031.

- By distribution channel, health and beauty stores captured 38.30% share of the Hair Mask market in 2025; online retail is advancing at a 6.10% CAGR over the forecast horizon.

- By geography, Europe commanded 35.10% of 2025 global revenue, whereas Asia-Pacific is the fastest-growing region at a 5.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hair Mask Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for advanced post-damage hair repair solutions | +1.2% | North America, Europe (global spill-over) | Medium term (2-4 years) |

| Ingredient-led skinification trend shaping premium hair mask adoption | +1.5% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Rapid expansion of e-commerce and direct-to-consumer channels | +1.3% | Global; strongest in China and India | Short term (≤ 2 years) |

| Rising disposable incomes in emerging markets driving salon-grade product uptake | +0.9% | Asia-Pacific core, Latin America, MENA | Long term (≥ 4 years) |

| Increasing adoption of structured hair-cycling care routines | +0.6% | North America and Europe, expansion to Asia-Pacific | Short term (≤ 2 years) |

| Advancements in time-release and encapsulation technologies | +0.7% | Global R&D hubs in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Advanced Post-Damage Hair Repair Solutions

Rising incidence of hair damage from coloring, bleaching, and heat styling has made breakage the leading concern for approximately 36–37% of consumers in the U.S. and U.K., according to a May 2025 survey. Similarly, conversations around hair loss, particularly among Generation Z, have surged across social platforms, signaling a shift in concern beyond traditional aging demographics. This heightened awareness is reshaping consumer priorities, with repair-focused solutions increasingly favored over preventive care. In response, demand is accelerating for high-performance hair masks formulated with proteins, ceramides, and bond-building actives that penetrate the cortex rather than merely coating the cuticle. This behavioral shift has been amplified by dermatologists and influencers who frame intensive repair as a non-negotiable step in hair care routines. As a result, purchase frequency is rising, the addressable consumer base is expanding, and expectations for efficacy are increasing.

Ingredient-Led Skinification Trend Shaping Premium Hair Mask Adoption

The convergence of skincare and hair care continues to redefine the hair mask category, with consumers increasingly applying skincare-level standards to hair treatments. Ingredients such as peptides, niacinamide, and hyaluronic acid have transitioned from facial serums into hair formulations, enabling brands to substantiate performance claims with clinical and lab-backed data. Scientific validation, such as findings confirming peptide-keratin interactions that restore mechanical strength, is reinforcing the efficacy narrative and supporting premium pricing, with some masks reaching USD 50 for 50 ml formats. Peptide-based and bioactive formulations are emerging as key growth drivers, targeting structural repair, scalp health, and overall hair resilience at a molecular level. This shift is evident across both prestige and mass segments: premium launches like Kérastase’s Symbiose range incorporate microbiome-balancing prebiotics, while mass-market players such as Dove’s Damage Therapy line leverage bio-protein technology to broaden access to high-performance actives.

Rapid Expansion of E-Commerce and Direct-to-Consumer Channels

The rapid expansion of digital commerce is reshaping distribution dynamics in the hair care market, with online channels outpacing traditional retail. Brands are utilizing personalized product discovery tools, delivering educational content, and offering subscription models to drive higher usage frequency and strengthen brand loyalty. The adoption of direct-to-consumer models enables brands to achieve higher profit margins while fostering direct consumer relationships. In Q1 2025, e-commerce sales made up 16.2% of total sales in the U.S., signaling a clear shift towards online shopping, as reported by the U.S. Census Bureau[2]European Commission, “Commission Regulation (EU) 2023/2055 on Microplastics,” europa.ec. This approach is especially critical for premium-positioned products, where higher price points necessitate deeper consumer education and engagement. The continued expansion of digital channels is lowering traditional entry barriers, enabling niche and emerging brands to compete more effectively with established players. By leveraging data-driven targeting, personalized marketing, and differentiated customer experiences, these brands are accelerating market penetration and contributing to a more democratized and dynamic competitive landscape.

Rising Disposable Incomes in Emerging Markets Driving Salon-Grade Product Uptake

In emerging markets, particularly across Asia-Pacific and the Middle East, rising income levels are reshaping consumption patterns in the hair care category. Markets such as India are witnessing a steady rise in per-capita beauty expenditure, while mature economies like Japan already demonstrate strong premiumization, with high-end hair care accounting for a significant share of total category value. Similarly, middle-income consumers in the Gulf and Southeast Asia are adopting salon-grade products as accessible luxuries, reflecting a broader shift toward value-added, efficacy-driven solutions. This evolution is being reinforced by growing awareness of advanced hair care routines, increased exposure to global beauty standards, and the accessibility of premium products through digital channels. As a result, demand for high-performance hair masks is experiencing sustained growth, signaling a structural transition toward premium, treatment-oriented consumption across emerging markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of substitute products (conditioners and leave-ins) | -0.8% | Global, strongest in price-sensitive tiers | Short term (≤ 2 years) |

| High price sensitivity in mass-market segments | -0.9% | Emerging markets, low-income cohorts | Medium term (2-4 years) |

| Regulatory pressure on silicones and microplastic-based formulations | -0.6% | Europe highest, North America fragmented, Asia-Pacific emerging | Long term (≥ 4 years) |

| Supply chain volatility for premium natural oil ingredients | -0.5% | Morocco, Southeast Asia, Latin America sourcing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Substitute Products (Conditioners and Leave-Ins)

As product functionalities converge, hair masks face increasing substitution pressure from rinse-out conditioners and leave-in serums that deliver similar moisturizing and repair benefits at lower price points and with greater convenience. The emergence of hybrid formats that combine the benefits of masks and conditioners into quick-use solutions is blurring category boundaries. These multi-functional products appeal to time-constrained and value-conscious consumers, particularly in the mass market, reducing the need for multi-step routines. This dynamic is forcing dedicated mask brands to clearly articulate and demonstrate differentiated value, such as deeper repair, longer-lasting results, or advanced ingredient delivery systems. Without a compelling efficacy narrative, pure-play mask products risk losing shelf space in increasingly rationalized retail assortments

High Price Sensitivity in Mass-Market Segments

Macroeconomic pressures, including inflation and currency volatility, are amplifying price sensitivity among value-driven consumers, who account for nearly two-thirds of hair mask revenue but are expanding at a slower pace than the overall market. This dynamic is constraining the effectiveness of premium pricing strategies, particularly in mass segments where affordability remains a key purchase driver. In response, brands are increasingly adopting “masstige” positioning, offering performance-oriented formulations at more accessible price points to retain volume. However, heightened promotional activity from retailers is compressing margins, limiting profitability, and reducing the capacity for sustained investment in innovation and brand building. Brands that fail to clearly communicate differentiated performance or sustainability credentials risk rapid commoditization in an increasingly crowded marketplace. Structural challenges also persist in certain regions; for instance, relatively low digital penetration in markets such as Brazil restricts the scalability of higher-margin direct-to-consumer models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Thermal Masks Gain Traction as At-Home Salon Experiences Intensify

Steam-free masks continue to dominate the category, accounting for 53.18% of total revenue in 2025, driven by strong consumer preference for convenient, no-heat application formats that integrate into everyday routines. Their accessibility, ease of use, and compatibility with time-constrained lifestyles make them particularly attractive in the mass market. However, as private-label players increasingly replicate core formulations, steam-free variants face rising commoditization risk, intensifying price competition and limiting differentiation.

In contrast, thermal or steam-activated masks are emerging as the fastest-growing segment, projected to expand at a 6.4% CAGR through 2031, outpacing the broader market. Growth is fueled by sustained consumer demand for salon-quality results at home, a behavior that accelerated during the pandemic and has since become entrenched. Innovations such as self-heating sachets and USB-powered caps are enhancing convenience, while advancements like graphene film heating technology, capable of reaching optimal temperatures in under 90 seconds, are addressing historical barriers related to safety and usability. Brands are further strengthening adoption by bundling masks with affordable heating accessories, encouraging system-based purchases and fostering customer loyalty.

By Packaging Type: Jars Capture Premiumization and Refill Momentum

Pouch packaging continues to dominate the hair mask market, accounting for 50.12% of the total share in 2025, driven by its cost efficiency, portability, and suitability for single-use applications. This format aligns well with mass-market demand for convenience and affordability, particularly among on-the-go consumers. However, despite ongoing innovation such as mono-material designs aimed at improving recyclability, the environmental impact of flexible plastics remains a concern due to low recycling rates and potential regulatory restrictions on laminates, which could increase future costs.

In contrast, jar packaging is emerging as the fastest-growing segment, projected to expand at a CAGR of 5.85% through 2031. Growth is being driven by rising sustainability expectations and evolving regulatory frameworks, including Extended Producer Responsibility (EPR) policies in Europe. Refillable glass and aluminum jar systems can reduce packaging waste by up to 80%, strengthening their appeal among environmentally conscious consumers and supporting premium brand positioning. Meanwhile, tubes occupy a middle ground but lack strong differentiation, offering neither the sustainability advantages of jars nor the convenience of pouches. As a result, retailers are increasingly prioritizing shelf space for high-performing jar-based products in premium segments.

By Category: Premium Segment Outpaces Mass as Efficacy Narratives Resonate

The mass segment continues to dominate the hair mask market, accounting for 67.58% of total value in 2025, reflecting strong demand for affordable and accessible solutions. This segment caters to a broad consumer base prioritizing value, but it faces ongoing pressure from rising input costs and increasing expectations for high-performance, clean formulations at competitive price points. As a result, many mass brands are adopting “dupe” and masstige strategies, replicating premium benefits while maintaining affordability, to protect market share, albeit at the expense of margin expansion.

The premium segment is gaining momentum and is projected to grow at a CAGR of 6.25% through 2031, outpacing the overall market. This growth is driven by sustained trade-up behavior among affluent consumers, who have continued to increase beauty spending despite inflationary pressures. Prestige hair masks, often priced above USD 20 for a 200 ml format, leverage clinical validation, dermatologist endorsements, and sustainable packaging to justify price premiums exceeding 300% over mass alternatives. A key driver of this segment is rising consumer scrutiny of ingredient transparency, with buyers increasingly evaluating INCI lists and favoring scientifically backed formulations. Social media and expert-led education are further reinforcing the value proposition of premium products, enhancing willingness to pay for efficacy and safety.

By Distribution Channel: Online Retail Surges as Social Commerce Collapses Purchase Funnels

Health and beauty stores remain the leading distribution channel, accounting for 38.30% of market share in 2025, driven by their ability to provide expert guidance, personalized recommendations, and in-store sampling. These outlets play a critical role in educating consumers and building purchase confidence, particularly for products like hair masks that often require an explanation of benefits and usage. Their high-touch experience continues to resonate with shoppers seeking informed, assurance-driven purchasing decisions.

However, e-commerce is the fastest-growing channel, projected to expand at a CAGR of 6.1% through 2031. Growth is fueled by the scale and convenience of platforms such as Amazon, alongside the rapid rise of social commerce channels like TikTok Shop, where short-form content compresses discovery, evaluation, and purchase into a seamless journey. This environment enables indie brands to compete effectively with established players by leveraging algorithm-driven visibility and targeted engagement strategies. Supermarkets and hypermarkets, while offering convenience, are constrained by limited assortments, prompting consumers seeking specialized or high-performance masks to shift toward online platforms with broader selections.

Geography Analysis

Europe remains the largest regional market, accounting for 35.10% of global share in 2025, supported by strong consumption in countries such as Germany, France, and the United Kingdom. The region benefits from a well-established salon culture and mature premium retail channels, reinforcing demand for high-quality hair treatments. At the same time, stringent regulatory frameworks, including restrictions on microplastics and cyclic silicones, are accelerating product reformulation cycles. While these regulations increase compliance costs, they also create a competitive advantage for brands that can position themselves as leaders in sustainable and “clean” formulations. With GDP growth hovering around 2%, the market is relatively mature, and competition is increasingly centered on capturing wallet share rather than expanding the consumer base.

Asia-Pacific is the fastest-growing region, projected to register a CAGR of 5.9% through 2031, driven by rising incomes, rapid urbanization, and strong digital adoption. China stands out as a digital-first market, where online channels dominate hair-care sales, making e-commerce the primary route to market. India, while still at an earlier stage in per-capita beauty spending, is experiencing rapid growth, expanding the addressable premium segment.

North America continues to represent a high-value but slower-growth market, with overall hair-care growth remaining modest. However, the region's regulatory landscape, highlighted by the December 2023 rollout of the Modernization of Cosmetics Regulation Act (MoCRA), poses compliance challenges[3]Source: U.S Food and Drug Administration, "Modernization of Cosmetics Regulation Act of 2022 (MoCRA)", www.fda.gov. Canada, with its emphasis on natural products and bilingual labeling requirements, presents niche opportunities for eco-certified and clean-label brands.

Latin America is expected to grow at a moderate pace, supported primarily by Brazil, though relatively low e-commerce penetration limits the scalability of direct-to-consumer strategies. In contrast, the Middle East and Africa region is expanding steadily, driven by urbanization, rising incomes, and an expanding middle class. However, operational challenges such as high logistics costs and import duties continue to constrain margins.

Competitive Landscape

The hair mask market demonstrates moderate concentration, with competition intensifying as leading players gradually lose share to emerging brands and private-label offerings. While global incumbents such as Procter & Gamble, Unilever, and L’Oréal continue to benefit from scale, brand equity, and distribution strength, their dominance is being challenged by more agile competitors offering differentiated, science-led formulations.

Strategic acquisitions remain central to competitive positioning, with established companies investing in high-growth segments such as bond-repair, clean beauty, and textured hair to strengthen portfolios and maintain relevance. These moves reflect a broader shift toward technology-driven and inclusive product innovation.

Independent brands are gaining traction through digital-first models, influencer-led engagement, and rapid product development cycles. Private-label players are also expanding, leveraging price competitiveness and improving product quality to capture value-conscious consumers. Advancements in formulation technologies and supply chain transparency are lowering barriers to entry, enabling smaller players to compete more effectively. As a result, the market is becoming increasingly dynamic, with success dependent on innovation speed, product efficacy, and the ability to build strong, trust-based consumer relationships.

Hair Mask Industry Leaders

-

L’Oréal SA

-

Unilever PLC

-

Procter & Gamble Co

-

Henkel AG & Co. KGaA

-

Kao Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Innovative Beauty Group (IBG) launched its first fully owned hair and scalp care brand, Liva, marking a strategic shift toward building proprietary brands. Developed through its internal incubator, IBG Lab, the range debuted across more than 700 Walmart stores and online, leveraging IBG’s end-to-end capabilities in formulation, branding, and go-to-market execution to establish a scalable, consumer-centric offering.

- August 2025: Moroccanoil expanded its U.S. retail footprint through a nationwide launch in Ulta Beauty, introducing its full portfolio of haircare, body care, and fragrance products across approximately 800 stores and online, significantly broadening consumer access beyond its traditional salon-based distribution.

- May 2025: Hindustan Unilever Limited (HUL) made its debut in India's burgeoning prestige and professional beauty market with the launch of Nexxus, including a hair mask. HUL's introduction of Nexxus underscores its strategic shift towards premium brands, resonating with the desires of contemporary Indian consumers who prioritize both luxury and technical performance.

- March 2025: K18 Biomimetic Hairscience made a pivotal strategic move by partnering with CosmoProf, North America's largest professional beauty distributor, marking a significant milestone in the biotech hair care brand's professional-first growth strategy. The launch unfolded in two carefully orchestrated phases: online availability through the CosmoProf app and website on March 21, 2025, followed by nationwide in-store distribution across all U.S. and Canadian locations starting April 1, 2025

Global Hair Mask Market Report Scope

A hair mask is a deep-conditioning treatment formulated to deliver intensive nourishment, repair, and hydration to the hair and scalp. The hair mask market is analyzed across multiple dimensions, including product type, packaging type, distribution channels, and geography. By product type, the market is segmented into steam-free and thermal/steam-activated masks. Packaging type is categorized into pouches, jars, and tubes. Distribution channels comprise health and beauty stores, supermarkets/hypermarkets, online platforms, and others. Geographically, the study covers key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. For each segment, market sizing and forecasts are provided in terms of value (USD million).

| Steam Free Masks |

| Thermal/Steam Masks |

| Pouch |

| Jar |

| Tubes |

| Mass |

| Premium |

| Health and Beauty Stores |

| Online Retail Stores |

| Supermarkets/Hypermarkets |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Type | Steam Free Masks | |

| Thermal/Steam Masks | ||

| By Packaging Type | Pouch | |

| Jar | ||

| Tubes | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Health and Beauty Stores | |

| Online Retail Stores | ||

| Supermarkets/Hypermarkets | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Hair Mask market size and its expected growth?

The Hair Mask market size reached USD 702.1 million in 2026 and is forecast to hit USD 915.12 million by 2031, growing at a 5.60% CAGR.

Which product type leads the market today?

Steam-free masks dominate with 53.18% Hair Mask market share in 2025, reflecting consumer preference for quick, no-heat routines.

Why are thermal steam masks gaining traction?

Thermal steam masks open the cuticle to boost active penetration, helping the segment achieve the fastest forecast CAGR of 6.40% through 2031.

How are online channels shaping sales?

E-commerce is projected to grow at 5.90% CAGR, driven by personalized quizzes and influencer-led education.

Page last updated on: