Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

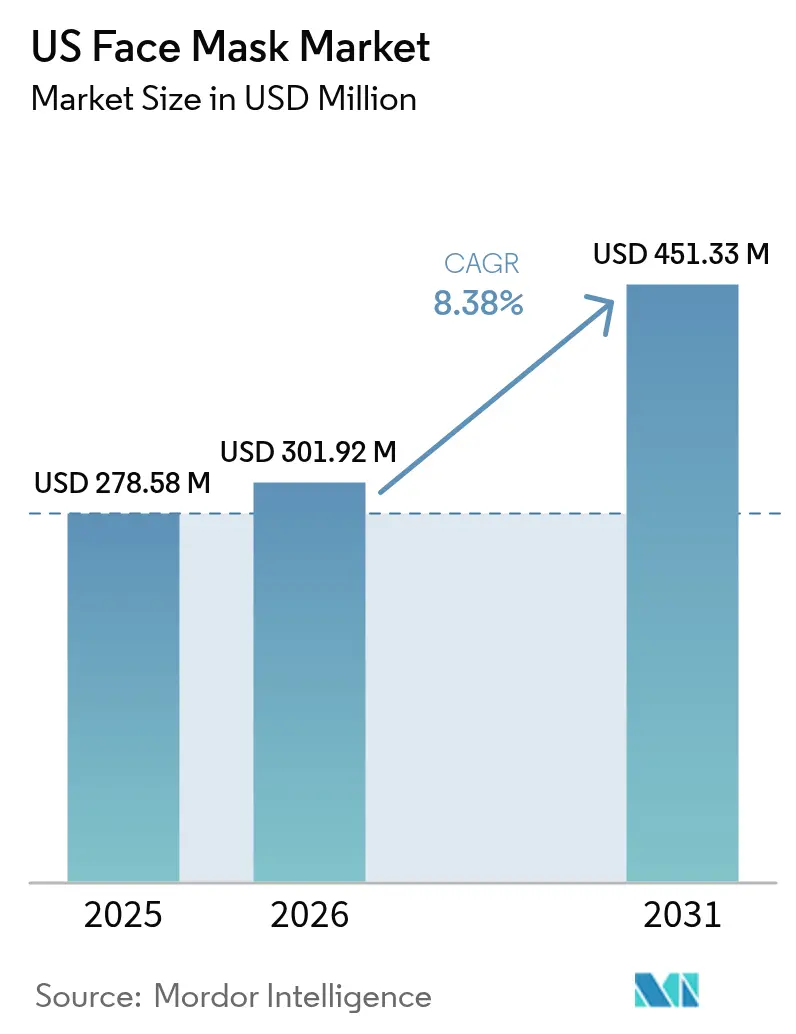

| Base Year Market Size (2025) | USD 278.58 Million |

| Market Size (2026) | USD 301.92 Million |

| Market Size (2031) | USD 451.33 Million |

| Growth Rate (2026 - 2031) | 8.38% CAGR |

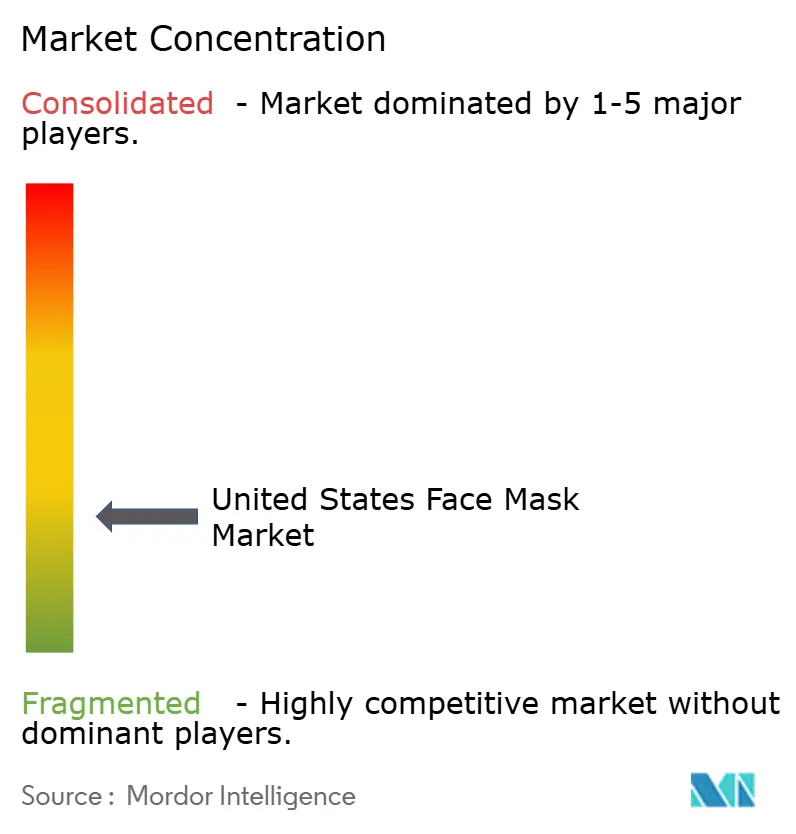

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Face Mask Market Analysis by Mordor Intelligence

The US face mask market size is expected to grow from USD 278.58 million in 2025 to USD 301.92 million in 2026 and is forecast to reach USD 451.33 million by 2031 at 8.38% CAGR over 2026-2031. The market expansion is driven by increased retail availability of diverse face mask products and the growing influence of Asian skincare culture in the United States. Social media platforms have emerged as effective marketing channels for face mask manufacturers, enhancing product visibility and consumer engagement. Consumer behavior analysis indicates that users who have incorporated face masks into their skincare routines during recent years intend to maintain these practices, suggesting a sustainable demand pattern. This market evolution reflects the convergence of technological advancement and environmental awareness in product development and distribution strategies. With increasing consumer awareness about skincare benefits and the continuous innovation in product formulations, the US face mask market is positioned for sustained growth in the coming years.

Key Report Takeaways

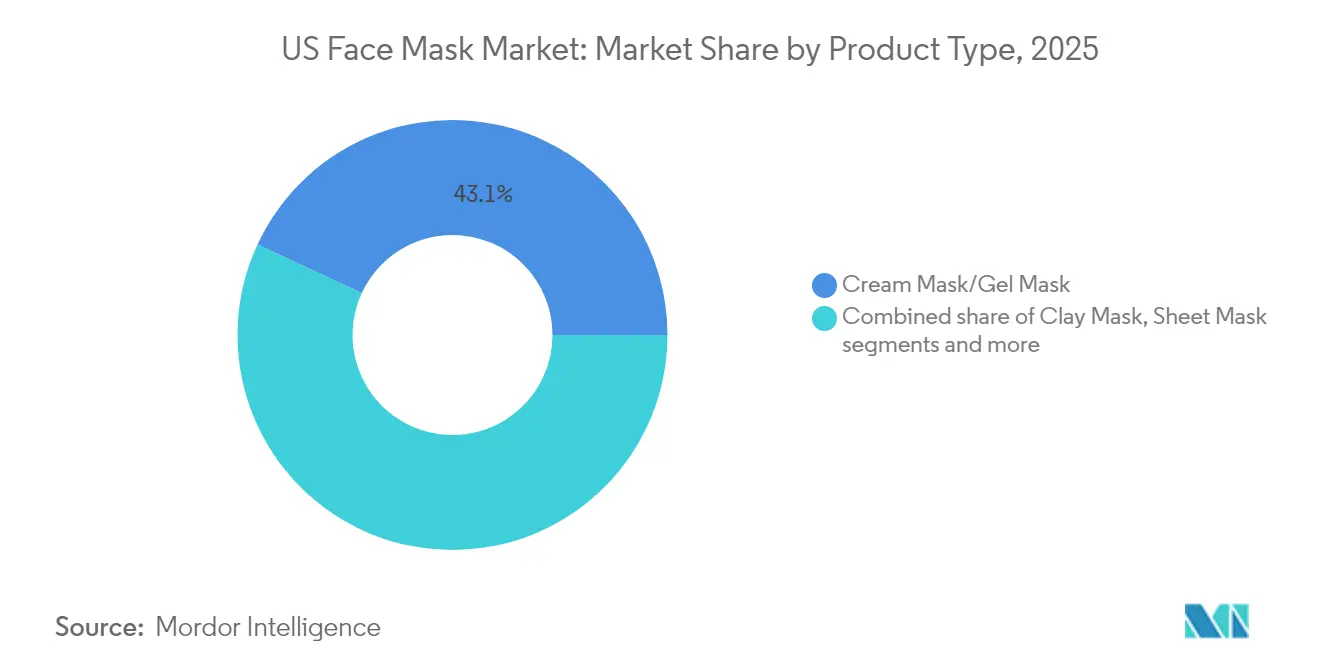

- By product type, cream/gel masks led with 43.08% of the US face mask market share in 2025, whereas clay masks are on track to expand at an 8.69% CAGR through 2031.

- By end user, women retained 57.32% of the market size in 2025, yet men are forecast to grow at a 9.11% CAGR on rising grooming adoption.

- By ingredient, conventional formulations commanded 67.21% of the US face mask market size in 2025; natural and organic variants record the fastest 9.47% CAGR through 2031.

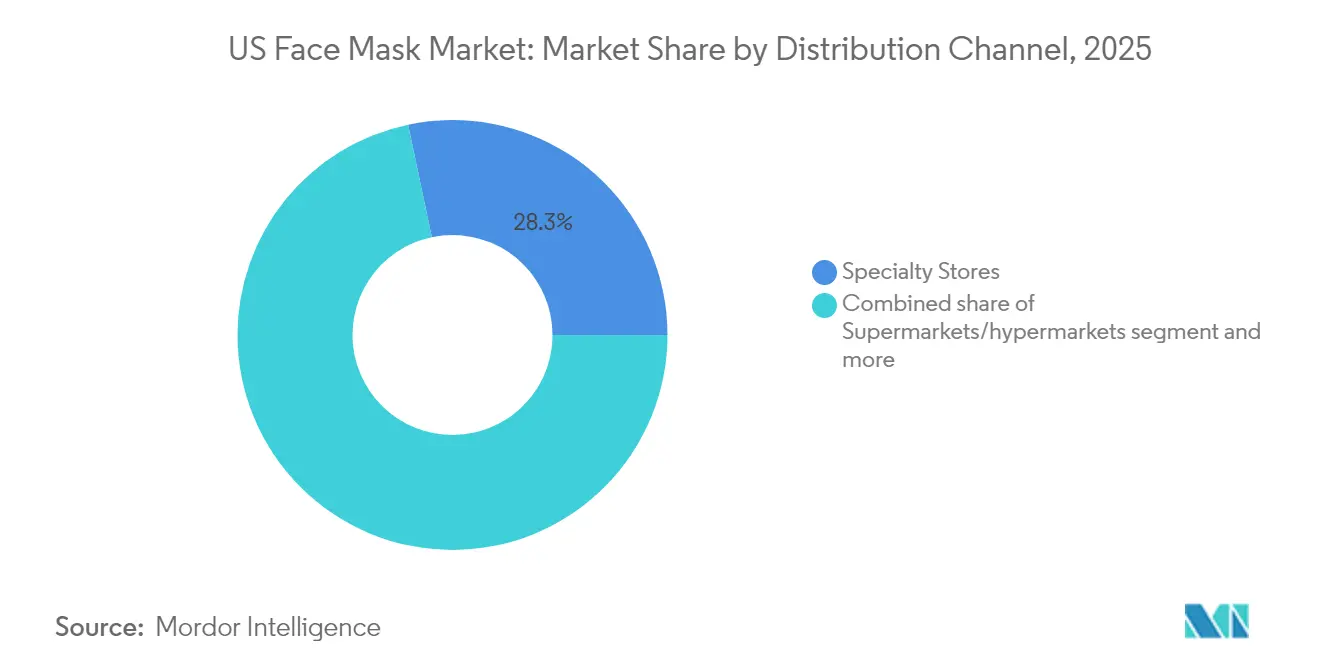

- By distribution channel, specialty stores captured 28.31% of the market share in 2025, while online retail is advancing at a 9.72% CAGR to 2031.

- By region, the South held 37.22% revenue share in 2025, whereas the Northeast is projected to log a 10.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Face Mask Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological innovations in ingredient and functionality | +2.1% | Global, with concentration in urban centers | Medium term (2-4 years) |

| Increased air pollution and environmental concerns | +1.8% | Northeast, West Coast metropolitan areas | Long term (≥ 4 years) |

| Rising consumer spending on skincare products | +1.5% | South, West regions with higher disposable income | Short term (≤ 2 years) |

| Influence of social media and celebrity endorsements | +1.3% | National, with early gains in the Northeast and West | Short term (≤ 2 years) |

| Surge in men’s skincare adoption | +1.0% | National, accelerated in urban markets | Medium term (2-4 years) |

| Demand for natural, organic, and clean facial care | +0.8% | Northeast, West Coast, educated demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Technological Innovations in Terms of Ingredient and Functionality

Technological advancements in ingredient formulations and functionality drive the US face mask market growth. Manufacturers incorporate innovative ingredients such as hyaluronic acid, peptides, and natural botanicals while developing smart masks with targeted delivery systems. The integration of biotechnology enables masks with enhanced penetration capabilities and time-release properties. Additionally, personalized face masks utilizing artificial intelligence and skin diagnostic tools allow consumers to address specific skincare concerns effectively. For instance, in December 2024, CosRx launched two new face masks - the Advanced Snail Mucin Glass Glow Hydrogel Mask and Peptide Collagen Hydrogel Eye Patch for Youthful Glow, demonstrating the market's continuous innovation in ingredient formulations.

Increased Air Pollution and Environmental Concerns

Environmental degradation in the United States has transformed face masks from luxury beauty products into essential preventive healthcare tools. The increasing air pollution levels in major US cities, combined with environmental challenges such as wildfires and dust storms, have prompted residents to use face masks during outdoor activities and daily commutes. This shift in consumer behavior stems from growing awareness of airborne pollutants and their health impacts, effectively expanding the addressable market beyond traditional cosmetics consumers. According to the American Lung Association's State of the Air 2025 report, 156.1 million Americans, 46% of the population, live in areas with failing grades for unhealthy levels of ozone or particle pollution [1]Source: American Lung Association, “State of the Air 2025 Key Findings,” lung.org. These environmental factors continue to drive the growth of the US face mask market as consumers prioritize skin health and protection against air pollution.

Rising Consumer Spending on Skincare Products

Consumer spending on skincare and facial care products in the United States has increased significantly, driven by continuous product innovation and new launches in the market. The broader beauty industry's resilience during economic uncertainty and consumers' prioritization of self-care investments have contributed to increased discretionary spending on skincare products. American consumers demonstrate growing consciousness about skin health and show a willingness to invest in premium skincare solutions, including face masks. According to Advanced Dermatology's 2024 survey, Americans spend an average of USD 897 per year on their appearance [2]Source: Advanced Dermatology, “America’s Beauty Budgets,” advdermatology.com. The rise in disposable income, combined with the growing influence of social media and beauty influencers, has encouraged consumers to experiment with various face mask products, although economic headwinds may influence value-conscious purchasing decisions in the near term.

Surge in Men's Skincare Adoption

Male consumers in the United States are driving significant growth in the face mask market through increased adoption of skincare products. The normalization of male grooming practices beyond basic cleansing and moisturizing, coupled with reduced social stigma around appearance-focused self-care, has expanded the market potential. According to Advanced Dermatology's 2024 survey, American men spend an average of USD 728 per year on their appearance. This trend is further supported by many brands introducing male-specific face mask products and implementing targeted marketing campaigns. The combination of growing skincare awareness among men, particularly in urban areas, and rising disposable income continues to drive the expansion of the face mask market in the United States.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over chemical ingredients | -1.2% | National, concentrated in educated demographics | Medium term (2-4 years) |

| Alternative and traditional skincare methods | -0.8% | Rural areas, older demographics | Long term (≥ 4 years) |

| Skin sensitivity and allergic reactions | -0.6% | National, particularly sensitive skin populations | Short term (≤ 2 years) |

| Supply chain and raw material constraints | -0.5% | Global impact, regional manufacturing dependencies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Over Chemical Ingredients

Consumer awareness regarding potentially harmful chemicals in face masks, such as synthetic fragrances, parabens, and artificial dyes, has become a significant market restraint. The presence of chemical preservatives, phthalates, formaldehyde-releasing preservatives, and synthetic colors has raised concerns among regulatory bodies and consumer advocacy groups due to their association with skin irritation and allergic reactions. This heightened awareness, coupled with the implementation of the Modernization of Cosmetics Regulation Act (MoCRA), which expanded FDA authority over cosmetics safety and labeling requirements, has created regulatory challenges for manufacturers [3]Source: US Food and Drug Administration, “Small Businesses & Homemade Cosmetics,” fda.gov . The shift in consumer preference towards clean beauty and natural ingredients has compelled manufacturers to reformulate their products, resulting in higher production costs and potentially lower profit margins.

Alternative and Traditional Skincare Methods

The prevalence of traditional and alternative skincare methods presents a significant restraint to the United States face mask market. Many consumers opt for natural remedies, including homemade masks using ingredients like honey, turmeric, and yogurt, which they perceive as cost-effective and chemical-free alternatives. Traditional skincare practices passed down through generations, combined with the growing DIY beauty trend and professional spa treatments offering personalized solutions, influence consumers to create their own face mask formulations. This trend strengthens during economic uncertainty when consumers actively seek cost-effective alternatives to commercial products. The increasing consumer awareness about natural ingredients and the availability of these alternatives may impact the market growth of commercial face mask products, particularly in the premium segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Clay Masks Drive Innovation Despite Cream Dominance

The face mask market demonstrates distinct segment dynamics, with cream and gel masks commanding a dominant 43.08% share in 2025, primarily due to their universal appeal in providing hydration and nourishment across diverse skin types. While these traditional formats maintain their leadership position, clay masks are emerging as the fastest-growing segment with an 8.69% CAGR through 2031, driven by increasing urban pollution concerns and consumer demand for deep-cleansing solutions. Sheet masks and peel-off variants occupy specific market niches, with the former facing environmental scrutiny despite social media popularity, and the latter serving consumers seeking visible transformation effects.

The market evolution reflects a shift from basic moisturizing treatments toward targeted solutions addressing specific skin concerns. Clay masks leverage their natural positioning to align with clean beauty preferences, while cream and gel formats are adapting through sustainable packaging initiatives and cleaner formulations to maintain their market dominance. This adaptation indicates the industry's response to changing consumer preferences and environmental considerations.

By End User: Men's Adoption Accelerates Gender Convergence

The gender segmentation reveals a significant transformation in skincare consumption patterns. While women maintain a dominant 57.32% market share in 2025, men's adoption is growing rapidly at a 9.11% CAGR through 2031, approaching overall market growth rates. This convergence reflects the normalization of male grooming practices beyond traditional boundaries, driven by social media influence, celebrity endorsements, and evolving masculine identity concepts that embrace self-care and appearance maintenance.

The male segment shows strong growth particularly in urban markets, where professional environments and cultural attitudes support expanded grooming routines, especially in the Northeast and West Coast regions with higher education levels and disposable incomes. Male consumers demonstrate distinct preferences from traditional female-focused products, necessitating targeted formulations that address specific skin concerns including larger pores, increased oil production, and coarser skin texture.

By Ingredient: Natural Formulations Gain Momentum

Conventional ingredients maintain a commanding 67.21% market share in 2025, while natural and organic formulations grow at 9.47% CAGR through 2031, driven by Millennials and Generation Z's preference for products emphasizing safety, ethicality, and sustainability. This shift toward cleaner beauty solutions and ingredient transparency presents both opportunities and challenges for manufacturers.

Natural formulations face technical hurdles in ingredient stability, preservation, and efficacy, requiring advanced expertise and higher development costs. This has led to the emergence of hybrid approaches that strategically combine natural actives with proven synthetic ingredients to balance performance requirements with clean beauty positioning.

By Distribution Channel: Digital Commerce Reshapes Retail

Specialty stores dominate the face mask distribution landscape with a 28.31% market share in 2025, leveraging their ability to provide expert consultation and product trial opportunities for premium purchases. While supermarkets/hypermarkets cater to price-conscious consumers seeking convenience, online retail exhibits the strongest growth trajectory at 9.72% CAGR through 2031, driven by increasing e-commerce adoption.

The ongoing digital transformation enables direct-to-consumer strategies that enhance profit margins while offering detailed product information and customer reviews as alternatives to in-store consultation. This shift has prompted the emergence of diverse distribution channels, including subscription services and social commerce platforms, necessitating omnichannel strategies that seamlessly integrate online and offline touchpoints to optimize market reach and maintain a consistent brand experience.

Geography Analysis

The South region dominates the US face mask market with a 37.22% share in 2025, supported by higher disposable incomes and cultural emphasis on appearance maintenance. The region's leadership stems from established beauty retail infrastructure, warm climate conditions, and cultural attitudes that normalize premium beauty product consumption. Major metropolitan areas like Atlanta, Miami, and Dallas function as beauty trend incubators and distribution hubs. However, the region's growth rate lags behind the national average, indicating market maturity and potential saturation.

The Northeast region exhibits the highest growth trajectory with a 10.12% CAGR through 2031, driven by urban density, higher education levels, and environmental consciousness. Key metropolitan areas, including New York, Boston, and Philadelphia, concentrate affluent consumers who demonstrate sophisticated beauty preferences and a willingness to invest in premium formulations. This growth outpaces the national average, reflecting the region's strong adoption of pollution protection skincare and clean beauty products.

The West and Midwest regions display distinct market characteristics that shape their moderate growth patterns. The West Coast, particularly California and Washington state, influences national product development through its focus on clean beauty and sustainability trends. In contrast, Midwest consumers emphasize practical benefits and value-oriented purchasing over premium positioning. These regional variations necessitate market-specific strategies that align with local economic conditions and cultural attitudes toward beauty investments.

Competitive Landscape

The US face mask market demonstrates significant fragmentation, creating opportunities for both established beauty conglomerates and emerging direct-to-consumer brands. This fragmentation stems from diverse consumer preferences across product types, price points, and ingredient philosophies, preventing any single player from achieving dominant market control. While established companies like L'Oréal, Unilever, and Estée Lauder maintain their market presence through extensive distribution networks and research capabilities, emerging brands successfully compete by utilizing digital commerce channels and clean beauty positioning.

Companies in the face mask market are increasing their investments in technology-driven innovation, sustainability initiatives, and direct-to-consumer capabilities. These strategies help bypass traditional retail intermediaries while improving profit margins and customer relationships. The market also witnesses strategic acquisitions aimed at accessing emerging technologies, expanding product portfolios, and incorporating digital-native brands that appeal to younger demographics through strong social media presence.

The face mask market presents significant growth potential in specialized segments, particularly in men's skincare, pollution protection formulations, and biodegradable packaging solutions. These opportunities address evolving consumer needs and environmental concerns while maintaining product efficacy and convenience.

US Face Mask Industry Leaders

L'Oréal SA

Procter & Gamble Company

The Estée Lauder Companies Inc.

Unilever Plc

Kenvue Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Pat McGrath Labs launched the Skin Fetish: Glass 001 Artistry Mask, a luxury peel-off mask designed to deliver a high-gloss “glass skin” effect. The formulation includes glycerin, rose water, and allantoin, and is marketed for its one-step luminous finish with runway appeal.

- September 2024: Naturium launched the AHA Exfoliating Mask 10%, a 5-minute resurfacing clay mask formulated with 5% glycolic acid, 5% lactic acid, and rice powder, positioned for quick texture refinement and pore minimization.

- April 2024: APRILSKIN launched the Carrotene IPMP Quick Dry Pore Tightening Clay Mask, positioning the SKU for rapid pore-refining benefits.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study classifies the United States face mask market as retail sales of cosmetic leave-on and wash-off masks, clay, sheet, peel-off, gel, and cream formats, formulated to cleanse, moisturize, or treat facial skin. According to Mordor Intelligence, the market stood at USD 278.58 million in 2025 and is projected to reach USD 418.58 million by 2030.

Scope exclusion: single-use surgical respirators, industrial dust masks, and other PPE coverings are not included in this valuation.

Segmentation Overview

- By Product Type

- Clay Mask

- Peel-Off Mask

- Sheet Mask

- Cream Mask/Gel Mask

- By End User

- Men

- Women

- By Ingredient

- Natural and Organic

- Conventional

- By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

- By Region

- Northeast

- Midwest

- South

- West

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with dermatologists, contract manufacturers, specialty retail buyers, and emerging indie brands in all four US census regions. Insights on average selling prices, actives driving sell-outs, and holiday promotion lifts were used to fine-tune desk estimates and stress-test assumptions.

Desk Research

We drew on open datasets from the US Census Bureau's Monthly Retail Trade Survey, Bureau of Economic Analysis personal-care expenditure tables, and the American Academy of Dermatology's consumer skincare polls. Trade updates from the Personal Care Products Council, ingredient patent filings mined via Questel, and import statistics from USITC DataWeb fleshed out demand drivers. Paid repositories, D&B Hoovers for brand revenue splits and Dow Jones Factiva for launch timelines, complemented these public sources. The sources listed are illustrative; many additional references informed data collection and validation.

Market-Sizing & Forecasting

A top-down demand pool, built from skincare spend per household and face mask penetration, was corroborated through selective bottom-up checks, sampled store sell-out data and disclosed brand revenues. Variables such as average unit price, online channel share, number of beauty box subscribers, disposable personal income, MoCRA-linked compliance costs, and TikTok search volumes feed the model. Multivariate regression, augmented by scenario analysis, extends these inputs to 2030; gaps in bottom-up rolls are bridged with regional ASP proxies and channel mix weights.

Data Validation & Update Cycle

Outputs undergo anomaly screens against Nielsen scan data and Statista trends before a senior reviewer signs off. Reports refresh yearly, with interim updates triggered by major recalls, regulatory shifts, or significant M&A events.

Why Mordor's United States Face Mask Baseline Commands Reliability

Published figures differ because publishers set distinct boundaries, price ladders, and refresh cadences.

Key gap drivers include inclusion of PPE respirators, shipment value counting instead of retail sell-through, and pandemic-era spikes some studies still anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 278.58 m (2025) | Mordor Intelligence | - |

| USD 396.65 m (2024) | Regional Consultancy A | Includes N95 and surgical masks alongside beauty masks |

| USD 1.50 bn (2025) | Global Consultancy B | Uses factory gate shipments and bundles nose strips and exfoliating patches |

| USD 10.50 bn (2024) | Industry Association C | Aggregates all protective face coverings supplied to healthcare, inflating the base year |

The comparison confirms that, by isolating cosmetic-only products, applying retail ASPs, and refreshing annually, Mordor Intelligence supplies a transparent, balanced baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the US face mask market?

The market stands at USD 301.92 million in 2026 and is forecast to climb to USD 451.33 million by 2031.

Why are clay masks growing faster than other segments?

Consumer concern about urban pollution drives demand for deep-cleansing clays, delivering an 8.69% CAGR through 2031.

Which distribution channel shows the highest growth?

Online retail is advancing at 9.72% CAGR, benefiting from live-stream shopping and direct-to-consumer models.

What are the key restraints hindering market expansion?

Ingredient safety concerns, DIY and other alternatives, sensitivity reactions, and supply chain disruptions collectively trim projected CAGR.

Page last updated on: