Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.65 Billion |

| Market Size (2031) | USD 16.20 Billion |

| Growth Rate (2026 - 2031) | 8.76% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Face Mask Market Analysis by Mordor Intelligence

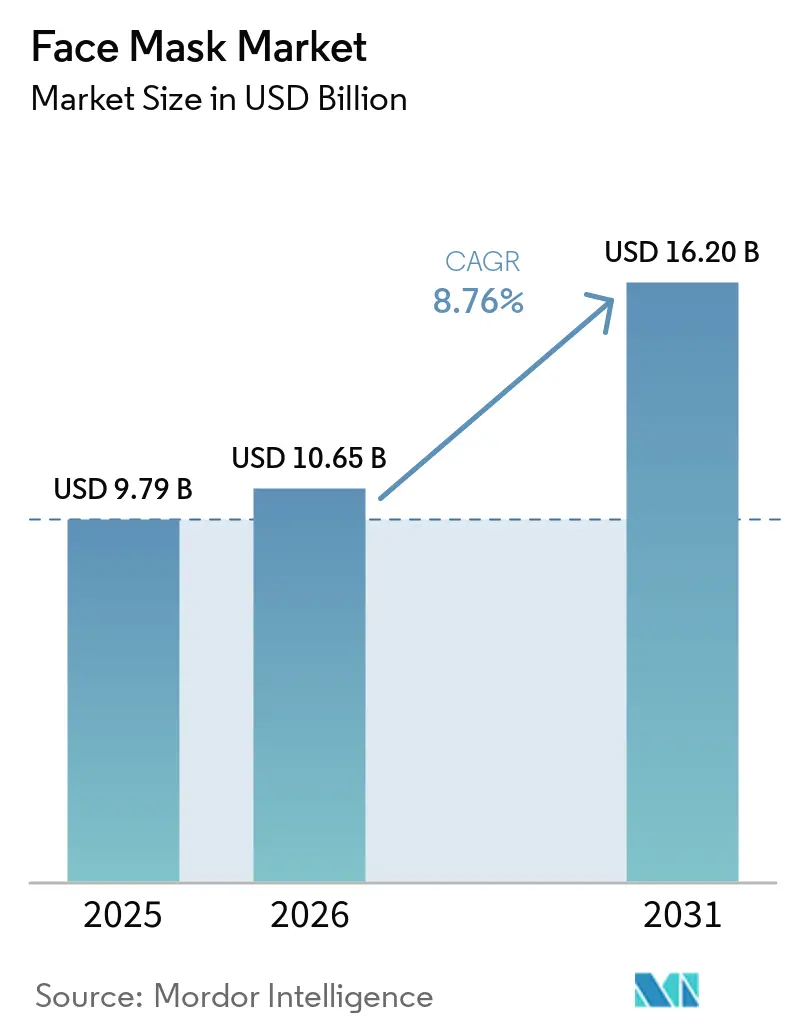

The face mask market size is expected to grow from USD 9.79 billion in 2025 to USD 10.65 billion in 2026 and is forecast to reach USD 16.20 billion by 2031 at a 8.76% CAGR over 2026-2031. The industry is witnessing a shift in product differentiation, moving from basic hydration to a focus on targeted actives, integration with devices, and innovative distribution channels. As consumers increasingly prioritize ingredient transparency and eco-friendly packaging, there's a noticeable shift towards premium, clean-label products. The rise of digital engagement, particularly through live-streaming commerce, has shortened the journey from product discovery to purchase, underscoring the need for real-time inventory management. As of 2026, competitive advantages hinge more on owning intellectual property, being prepared for regulatory challenges, and having a broad omnichannel presence, rather than just scale. Additionally, in response to growing sustainability concerns, manufacturers are innovating with biodegradable and eco-friendly mask formats, catering to the rising consumer demand for environmentally responsible products.

Key Report Takeaways

- By product type, cream and gel masks held 46.96% revenue share in 2025, while clay masks are expected to expand at a 9.80% CAGR through 2031.

- By ingredient, conventional formulations accounted for 69.74% of face mask market share in 2025, whereas natural and organic variants are forecast to grow at a 10.93% CAGR to 2031.

- By end user, women represented 58.82% of sales in 2025, yet the men’s segment is projected to post a 9.78% CAGR to 2031.

- By distribution channel, specialty stores captured 32.57% of sales in 2025, while online retail is on track for a 9.36% CAGR through 2031.

- By geography, Asia Pacific commanded 75.43% revenue share in 2025, and North America is expected to register the fastest regional CAGR at 9.56% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Face Mask Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological innovations in ingredients and functionality | +0.8% | Global, with a concentration in Japan, South Korea, and France | Medium term (2-4 years) |

| Increased air pollution and environmental concerns | +0.6% | Asia-Pacific core (China, India), spill-over to urban Middle East and Africa | Long term (≥ 4 years) |

| Rising consumer spending on skincare products | +0.5% | North America, Europe, and emerging Asia-Pacific markets | Short term (≤ 2 years) |

| Influence of social media and celebrity endorsements | +0.4% | Global, strongest in North America, Asia-Pacific youth demographics | Short term (≤ 2 years) |

| Increasing prevalence of skin issues | +0.3% | Global, elevated in urban centers with high pollution | Long term (≥ 4 years) |

| Demand for natural, organic, and clean facial care products | +0.7% | North America, Europe (EU Regulation 1223/2009 compliance) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological innovations in terms of ingredients and functionality

Ingredient science is evolving from mere hydration to proactive correction. Brands are now harnessing the power of peptides, growth factors, and encapsulated retinoids, ensuring they thrive even in challenging environments. L'Oréal, in July 2025, unveiled Melasyl, a product that curbs melanin production through a unique pathway, setting it apart from traditional tyrosinase blockers. This innovation not only offers a competitive edge but also comes with patent protection, bolstering L'Oréal's stance in the hyperpigmentation market. Shiseido, in November 2025, laid out its Action 2030 blueprint, dedicating a substantial JPY 100 billion (USD 670 million) towards medical dermatology. This investment encompasses cutting-edge solutions like LED-integrated masks, which merge light therapy with active topicals, and micro-needle patches designed for enhanced transdermal delivery. Estée Lauder, in 2025, rolled out its Advanced Night Repair PowerFoil Mask, leveraging a unique heat-generating foil to amplify the absorption of its signature Chronolux technology. Such groundbreaking advancements are not just elevating at-home skincare routines to professional standards but are also heightening consumer expectations and pushing up average selling prices. On the regulatory front, the Food and Drug Administration's Modernization of Cosmetics Regulation Act (MoCRA), finalized in December 2023, introduced new mandates like facility registration and adverse-event reporting. These regulations seem to tilt the playing field, benefiting established players with robust compliance infrastructures while posing challenges for smaller entrants.

Increased air pollution and environmental concerns

The demand for anti-pollution skincare has surged, driven by urban particulate exposure. Research in the Journal of Investigative Dermatology highlights that pollutants like PM2.5, PM10, and polycyclic aromatic hydrocarbons can cause oxidative stress, activate the aryl hydrocarbon receptor, and lead to the degradation of collagen and elastin fibers[1]Source: Journal of Investigative Dermatology, “Air Pollution and Skin Aging,” jidonline.org . In China and India, where air-quality issues are a constant concern, consumers are turning to masks enriched with antioxidants like niacinamide, resveratrol, and green-tea polyphenols. This preference is now making its way into cities across the Middle East and Africa, regions grappling with rising particulate levels due to swift industrialization. Brands are touting pollution-defense benefits, often referencing in-vitro assays that gauge the scavenging of reactive oxygen species. However, it's worth noting that regulatory bodies have yet to establish standardized testing protocols. Looking ahead, as climate change exacerbates wildfires and dust storms, what was once a niche anti-pollution formulation is poised to become a standard expectation in skincare.

Influence of social media and celebrity endorsements

By late 2025, TikTok's #skincare hashtag racked up a staggering 89.2 billion views, while #sheetmask garnered 1.2 billion. These figures underscore a viral demand cycle, elusive to traditional advertising. Per the Influencer Marketing Hub, influencer marketing boasts an impressive average return of USD 5.78 for every dollar spent, eclipsing both display and search advertising. Micro-influencers, with follower counts between 10,000 and 100,000, achieve engagement rates between 3% and 10%. This is three times higher than their celebrity counterparts, positioning them as cost-effective champions for budding brands. In 2024, China's live-streaming commerce saw hosts, in real-time, applying masks and offering fleeting discounts, turning viewers into buyers in mere minutes. Estée Lauder's 2025 collaboration with actress Nicole Richie for its Nutritious line highlights a trend: legacy brands merging celebrity allure with digital-savvy strategies. However, there's a looming challenge: as brands scramble for viral attention, organic reach diminishes and the costs of acquiring customers escalate.

Demand for natural, organic, and clean facial care products

Fragmenting the ingredient landscape, clean-beauty mandates are reshaping the beauty industry. The U.S. Department of Agriculture mandates that for a product to bear the "organic" label, it must contain at least 95% certified-organic content. For products labeled as "made with organic ingredients," the threshold is set at 70%. Meanwhile, the European COSMOS standard stipulates that leave-on products must have 95% of their ingredients derived from physically processed plants, with a minimum of 20% being organic by weight. Sephora's Clean program and Ulta's Conscious Beauty initiative have taken a bold step, excluding over 50 ingredients from their offerings. This list notably features parabens, phthalates, and preservatives that release formaldehyde. By doing so, these retail giants are effectively establishing private-sector standards that surpass even those set by the Food and Drug Administration. In 2024, products certified by Ecocert boasted an impressive average of 99% natural-origin ingredients. This statistic has sent ripples through the industry, compelling conventional formulators to either reformulate their products or face the risk of being delisted. The EU's Regulation 2021/850 has introduced further constraints, specifically targeting titanium dioxide in leave-on cosmetics and setting limits on salicylic acid concentrations. As a result, brands are now pivoting, opting for botanical alternatives like willow-bark extract and bakuchiol in place of synthetic actives. Such regulatory tightening appears to be a boon for vertically integrated players. These companies, with their control over raw-material sourcing, are better positioned to absorb the costs associated with organic certification.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over chemical ingredients | -0.4% | North America, Europe (heightened consumer scrutiny) | Medium term (2-4 years) |

| Alternative and traditional methods of skin routine practices | -0.3% | Asia-Pacific (gua sha, jade rolling), global DIY trends | Long term (≥ 4 years) |

| Skin sensitivity and allergic reactions | -0.2% | Global, elevated in populations with atopic dermatitis | Short term (≤ 2 years) |

| Supply chain and raw material constraints | -0.5% | Global, acute in hyaluronic acid, botanical extracts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health concerns over chemical ingredients

As consumers grow wary of synthetic preservatives and fragrances, formulation priorities are shifting. Clinical patch-testing data from the Journal of the American Academy of Dermatology reveal that fragrances in cosmetics cause contact dermatitis in 14% to 30% of cases, while preservatives like methylisothiazolinone and parabens account for another 10% to 15%[2]Source: Journal of the American Academy of Dermatology, “Contact Dermatitis Trends,” jaad.org. In 2024, the Food and Drug Administration's MedWatch logged thousands of complaints related to cosmetics, even though the agency only pre-approves color additives. In the U.S., "hypoallergenic" claims lack regulation, leading to a trust gap. Clean-beauty brands capitalize on this by highlighting excluded ingredients instead of making vague safety promises. While European Regulation 1223/2009 enforces safety assessments and restricts over 1,300 substances, U.S. oversight remains more lenient. This discrepancy pressures multinational brands to either harmonize their formulations or keep separate SKUs for different markets. Consequently, brands face margin compression as they invest in allergen testing, fragrance-free variants, and transparent labeling to sidestep regulatory scrutiny and consumer backlash.

Supply chain and raw material constraints

Hyaluronic acid, a key humectant in hydrating masks, is at risk due to concentrated supply. Most of its commercial production comes from bacterial fermentation facilities in China. Any disruption, be it regulatory, geopolitical, or environmental, can lead to a price spike of 20 to 30% within weeks. Botanical extracts like chamomile, calendula, and green tea face challenges from climate variability. Droughts in crucial growing regions diminish yields and inflate costs, pushing formulators to either find substitutes or accept reduced margins. The move towards sustainable sourcing intensifies these challenges. Achieving organic certification demands a three-year transition to pesticide-free land, and fair-trade premiums can inflate raw-material costs by an additional 10 to 15%[3]Source: United States Department of Agriculture, “Organic Certification Costs,” usda.gov . Restrictions on preservatives limit options. With parabens and formaldehyde-releasers losing favor, brands are pivoting to alternatives like phenoxyethanol, benzyl alcohol, and natural options such as radish-root ferment. However, these alternatives are less effective at lower concentrations and necessitate higher usage rates. Sustainability mandates in packaging, exemplified by the EU's Single-Use Plastics Directive, are steering brands towards recyclable or biodegradable materials. Yet, these eco-friendly options typically come at a premium of 15 to 25% over traditional films and might jeopardize barrier properties, which are crucial for protecting sensitive actives from oxidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Multi-Masking Fuels Clay Resurgence

Clay masks are projected to grow at a 9.80% CAGR through 2031, outpacing the overall market, even as cream and gel masks command a 46.96% share in 2025. This resurgence is largely attributed to the trend of multi-masking. In this practice, consumers apply various mask types to different facial zones, using clay on the T-zone to absorb sebum and a hydrating cream on the cheeks, to tackle mixed skin concerns in one session. Kaolin and bentonite clays, valued for their cation-exchange capacity, effectively bind impurities without compromising the skin's lipid barrier. Bubble clay masks, which produce an oxygen foam upon application, offer a unique sensory experience that boosts social media shares and encourages repeat purchases. While sheet masks dominate in the Asia Pacific, benefiting from biocellulose and hydrogel substrates that mold to facial contours and minimize essence evaporation, their growth is slowing due to rising sustainability concerns over single-use packaging. Peel-off masks, though catering to a niche audience seeking visible debris removal, come with dermatologist warnings about potential barrier integrity compromise from aggressive peeling. Cream and gel masks hold the largest market share, thanks to their versatility across all skin types, adaptable application times, and seamless integration into routines. Highlighting a shift towards hybrid formats, Shiseido's November 2025 strategy underscores a focus on LED-integrated masks and micro-needle patches, blending topical delivery with physical methods.

Substrate technology innovations are increasingly blurring the lines between product types. Estée Lauder's 2025 PowerFoil Mask, featuring a heat-generating metallic film, boosts penetration, effectively combining the ease of a sheet mask with the active-delivery prowess of a cream. Hydrogel masks, composed of 90 to 95 percent water or serum, are carving a niche in premium segments due to their drip-free adherence and cooling effect, which calms inflamed skin. Regulatory standards differ by mask type: while most jurisdictions classify leave-on masks under cosmetic regulations, those with prescription-strength actives, like tretinoin or concentrated acids, might be deemed over-the-counter drugs, necessitating pre-market approval. The Food and Drug Administration's MoCRA, finalized in December 2023, imposes facility registration and adverse-event reporting mandates on all cosmetic manufacturers, a move that escalates compliance costs, particularly for smaller brands.

By Ingredient: Clean Beauty Redefines Formulation Economics

Natural and organic masks are projected to grow at a 10.93% CAGR, nearly 50% faster than conventional counterparts, driven by clean-beauty mandates and shifting consumer expectations. Conventional formulations, holding a 69.74% market share in 2025 due to proven efficacy and cost advantages, face mounting regulatory challenges. The EU's Regulation 2021/850 restricts titanium dioxide in leave-on products and caps salicylic acid, prompting reformulation cycles that benefit brands with in-house research and development. COSMOS certification, requiring 95% physically processed plant ingredients and at least 20% organic content for leave-on products, is becoming the standard in European specialty retail. Sephora's Clean program excludes over 50 ingredients, including parabens, phthalates, and mineral oils, setting stricter private-sector benchmarks than Food and Drug Administration guidelines.

The shift to natural ingredients introduces supply-chain complexities. Organic certification requires a three-year pesticide-free land transition, while fair-trade premiums add 10-15% to raw-material costs. Botanical extracts like chamomile and calendula are vulnerable to climate variability; droughts in key regions can cut yields by 20-30%, forcing formulators to substitute or accept margin compression. Preservative restrictions add to the challenge: as parabens and formaldehyde-releasers fall out of favor, brands turn to alternatives like phenoxyethanol, benzyl alcohol, and radish-root ferment, which require higher usage rates for equivalent microbial protection. L'Oréal's 27% online sales penetration in 2023 highlights the channel's role in educating consumers and justifying premium pricing for clean formulations. While conventional masks retain cost advantages in mass channels, the margin gap is narrowing as scale economies emerge in organic agriculture and fermentation-derived actives.

By End User: Male Grooming Normalizes Facial Masking

From 2026 to 2031, men's facial mask adoption is projected to grow at a 9.78% CAGR, surpassing the women's segment, even though women commanded a 58.82% market share in 2025. The surge in men's skincare can be largely attributed to social media's influence. For instance, TikTok's #mensskincare hashtag garnered a whopping 203 million views by mid-2025, spotlighting male influencers showcasing comprehensive routines that encompass cleansing, toning, masking, and moisturizing. In response, brands are rolling out targeted products. Take Kenvue's Neutrogena, for example: their Hydro Boost+ Niacinamide Capsule Mask, launched in 2024, boasts unisex packaging and zeroes in on oil control and pore refinement, key concerns for male consumers. Similarly, Beiersdorf's Nivea Men Sensitive line broadened its offerings in 2025, introducing a clay mask tailored for thicker, oilier male skin.

While women continue to dominate the demographic landscape, thanks to established multi-step routines in the Asia-Pacific and increasing discretionary spending in North America and Europe, the gap is swiftly closing among younger generations. Notably, Gen Z men are reshaping the narrative, perceiving skincare as an act of self-care rather than mere vanity. This cultural evolution, intensified by the pandemic's Zoom fatigue and a newfound emphasis on appearance, is reshaping the industry's dynamics. Furthermore, the men's segment enjoys a unique advantage: a pronounced lower sensitivity to price. Many male consumers gravitate towards premium products as their initial foray, rather than gradually upgrading, leading to elevated average transaction values. Brands steering clear of overtly masculine branding, opting instead for a focus on efficacy, simplicity, and dermatologist endorsements, are reaping rewards from both genders. This trend underscores a significant shift towards gender-neutral positioning in the personal care realm.

By Distribution Channel: Live Streaming Reshapes Retail Economics

Online retail is set to outpace all distribution channels, boasting a projected CAGR of 9.36% through 2031. Meanwhile, specialty stores commanded a notable 32.57% market share in 2025. The surge in online sales can be attributed to the rise of social commerce, live streaming, and augmented-reality try-on tools. In China, beauty sales via live streaming have reached unprecedented heights. Hosts not only demonstrate real-time mask applications but also offer flash discounts, swiftly converting viewers into buyers. A testament to this trend, TikTok Shop's P.Louise raked in USD 2 million in just 12 hours during a live stream, and Made by Mitchell achieved the same feat within a week.

Specialty retailers like Sephora and Ulta dominate the market by curating product assortments, providing in-store consultations, and implementing loyalty programs that encourage repeat visits. As of 2023, Sephora boasts over 2,700 global stores, while Ulta Beauty operates 1,355 locations across the U.S. Both have seamlessly integrated buy-online-pick-up-in-store (BOPIS) services, merging digital ease with physical interaction. In a strategic move, Ulta partnered with Target in 2021, establishing shop-in-shops in 100 Target outlets, thereby penetrating suburban markets that lacked standalone beauty stores. While supermarkets and hypermarkets see a dip in market share, consumers are gravitating towards specialty and online channels, drawn by their wider assortments and tailored recommendations. Although other channels like direct-to-consumer websites and subscription boxes are on the rise, they remain scattered and fragmented. L'Oréal's 27% online penetration in 2023 underscores its commitment, fueled by investments in Beauty Tech, virtual try-ons, and influencer collaborations that boost traffic to both its own and retail partner platforms. This pivot towards online and specialty channels is tightening profit margins for mass retailers, compelling brands to reevaluate their trade spending and promotional strategies.

Geography Analysis

In 2025, Asia Pacific dominated the global face mask revenue, accounting for 75.43%. This stronghold is attributed to the region's multi-step skincare rituals, where masking is embraced as a routine, often weekly or even daily, rather than a mere occasional treat. South Korea's renowned 10-step regimen, encompassing double cleansing, toning, essence, serum, sheet mask, eye cream, moisturizer, and sunscreen, has gained worldwide traction, thanks to K-beauty brands and social media tutorials. Meanwhile, Japan prioritizes prevention over correction, fueling the demand for hydrating and anti-aging masks, often infused with sake, rice bran, and camellia oil. China's rich tradition in herbal medicine accentuates the value of ingredients like ginseng, pearl powder, and bird's nest. These not only command premium prices but also resonate deeply with consumers who appreciate their culturally rooted efficacy. In Q3 2024, Amorepacific boasted a revenue of KRW 1.4 trillion (USD 1.05 billion), with skincare products constituting over 60% of its sales. Shiseido, in its November 2025 strategy, acknowledged that while China accounts for 30% of its group revenue, the brand is diversifying into the U.S., Europe, India, and Africa to mitigate concentration risks. India's beauty market is on an upward trajectory, especially with the surge of online channels. Hindustan Unilever's strategic acquisition of Minimalist for INR 27.06 billion (USD 325 million) in 2025 underscores the multinational's recognition of India's burgeoning potential. Simultaneously, Marico's acquisition of Beardo, targeting the men's grooming segment, was valued at approximately INR 4 billion (USD 48 million).

North America is set to lead with a 9.56% CAGR through 2031, the fastest among all regions. This growth is fueled by the rising trend of clean beauty, the normalization of male grooming, and the expansion of specialty retail. Initiatives like Sephora's Clean program and Ulta's Conscious Beauty have raised ingredient standards, often surpassing Food and Drug Administration requirements, compelling brands to either reformulate or face delisting. The Food and Drug Administration's MoCRA, finalized in December 2023, introduced mandates like facility registration, product listing, and adverse-event reporting. While these measures elevate compliance costs, they also create entry barriers, favoring established industry players. L'Oréal's SAPMENA region, encompassing Sub-Saharan Africa, Pakistan, the Middle East, and North Africa, boasts over 43% of the global population under 25. With more than 50 million Beauty Tech interactions recorded, the region showcases significant untapped potential in digital commerce.

Europe's growth faces hurdles due to market saturation and intricate regulations. For instance, Regulation 1223/2009 restricts over 1,300 substances, while Regulation 2021/850 places further limitations on titanium dioxide and salicylic acid, necessitating constant reformulation. Although South America and the Middle East and Africa are smaller markets, urban centers within these regions present lucrative opportunities. Rising incomes and the allure of Western beauty ideals are driving up skincare expenditures. Brazil, with its vast population and rich beauty culture, stands out as a prime entry point for global brands. In contrast, countries within the Gulf Cooperation Council showcase impressive per-capita spending on luxury cosmetics.

Competitive Landscape

The face mask market is moderately fragmented. The top five players, L'Oréal, Estée Lauder, Unilever, Shiseido, and Amorepacific, command a significant share, but there's still ample space for regional specialists and direct-to-consumer newcomers. These incumbents vie for dominance through rapid innovation, robust regulatory compliance, and expansive omnichannel distribution. A case in point: L'Oréal's strategic EUR 1 billion (USD 1.08 billion) acquisition of Medik8 in June 2025 underscores its shift towards clinical-grade skincare and a direct-to-consumer approach, sidestepping traditional retail markups. Meanwhile, Shiseido's November 2025 "Action 2030" strategy, with a hefty allocation of over JPY 100 billion (USD 670 million) to medical dermatology, is pioneering at-home treatments like LED-integrated masks and micro-needle patches. Technology is carving out competitive advantages: L'Oréal's AI-driven Perso device crafts on-demand personalized skincare, and its 27% online sales penetration in 2023 is bolstered by investments in virtual try-ons and influencer collaborations. In India, as the beauty market is set to burgeon, local brands are being swiftly consolidated. Hindustan Unilever's acquisition of Minimalist for INR 27.06 billion (USD 325 million) and Marico's purchase of Beardo for around INR 4 billion (USD 48 million) highlight this aggressive land-grab in emerging markets.

White-space opportunities cluster in three areas: men's grooming, medical-grade at-home devices, and sustainable packaging. As male consumers increasingly embrace grooming products, brands that prioritize efficacy and simplicity over overtly masculine branding stand to gain. Medical-grade devices, merging LED therapy, micro-needling, or iontophoresis with topical masks, are straddling the line between cosmetics and medical devices. This regulatory gray area favors pioneers armed with clinical data and Food and Drug Administration approvals. While sustainable packaging poses a cost challenge, recyclable or biodegradable materials can be 15 to 25 percent pricier than standard films; brands cracking this code will resonate with eco-conscious consumers. This is especially true in Europe, where the Single-Use Plastics Directive enforces extended producer responsibility.

Smaller players like Herbivore Botanicals and Honasa Consumer (the parent of Mamaearth) are carving niches by championing clean formulations, transparent ingredient sourcing, and digital-first distribution. Regulatory compliance, often overlooked, acts as a formidable barrier. The Food and Drug Administration's MoCRA and EU Regulation 1223/2009 mandate rigorous standards, facility registration, safety assessments, and adverse-event reporting, necessitating dedicated compliance teams and raising entry barriers for undercapitalized startups.

Face Mask Industry Leaders

Shiseido Company Limited

Amorepacific Corporation

Unilever PLC

The Estée Lauder Companies Inc.

L’Oréal S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: BYOMA introduced the Bio-Collagen Radiance Facial Mask, its first-ever facial mask and a new high-performance treatment designed to deliver glass-like skin in just 20 minutes. Clinically proven to provide all-day hydration in one use, strengthen the skin barrier by up to 36%, and reduce the appearance of wrinkles, the mask offers visible results without the need to sleep in it.

- May 2025: Dr.Rashel introduced India's first vegan bio-collagen deep facial mask in its ProBoost skincare range. The mask contains plant-based ocean collagen and soya fiber, designed to repair skin, enhance elasticity, and minimize fine lines. The mask claims to contain no harmful chemicals and is cruelty-free, meeting the increasing consumer demand for clean and ethical beauty products in India.

- February 2025: Beauty by Bie introduced the DND Overnight Mask, developed through 27 trials over 21 months. The mask contains 3D Matrix Technology, prebiotics, probiotics, ceramides, and bakuchiol to repair and restore skin during sleep. The product claims to enhance the skin's microbiome, strengthen barrier function, and improve appearance overnight through a single application.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global cosmetic face mask market as leave-on skin care treatments such as clay, sheet, hydrogel, peel-off, and cream or gel masks that are purchased by retail or professional beauty outlets for home or in-spa application. The value represents manufacturer-level revenues expressed in constant 2024 US dollars.

Disposable medical masks, respirators (for example, N95), reusable cloth coverings, and any masks marketed strictly as personal protective equipment are outside this scope.

Segmentation Overview

- Product Type

- Clay Mask

- Peel-Off Mask

- Sheet Mask

- Cream Mask/Gel Mask

- Ingredient

- Conventional

- Natural and Organic

- End User

- Men

- Women

- Distribution Channel

- Supermarkets and Hypermarkets

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

- Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- New Zealand

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Peru

- Colombia

- Chile

- Rest of South America

- Middle East and Africa

- South Africa

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with contract manufacturers, ingredient suppliers, dermatologists, and category buyers across Asia-Pacific, North America, and Europe refined price bands, channel mark-ups, and regional usage frequency. Follow-up surveys with urban millennial consumers verified the shift toward natural and premium formats and helped benchmark average masks per capita.

Desk Research

We pulled baseline consumption using open trade codes for beauty preparations (HS 330499) from UN Comtrade, Eurostat COMEXT, and US ITC DataWeb, supplemented by national statistics from Korea Customs Service and Japan's Ministry of Economy, Trade and Industry. Consumer spend patterns were taken from household budget surveys issued by the US BLS, the Chinese National Bureau of Statistics, and Statistics Indonesia, while regulatory updates were monitored through FDA Cosmetics, the EU Cosing portal, and ASEAN Cosmetic Committee notes. Company revenue splits came from D&B Hoovers, and news flows were screened on Dow Jones Factiva. The sources listed here illustrate the range and are not exhaustive.

Market-Sizing & Forecasting

We first adopted a top-down model that reconstructs demand from retail sales of facial skin care, isolating the mask share through usage incidence and average selling price multipliers, which are then cross-checked with import-export volumes and contract packer capacity. Selected bottom-up roll-ups of listed brand revenues and sampled online unit sales validate and adjust totals once variances exceed five percent. Key variables feeding our model include female labor participation, social media beauty engagement, e-commerce penetration in personal care, inflation-adjusted disposable income, and Asia to rest of world export ratios. Five-year forecasts are produced with multivariate regression layered on scenario analysis around ingredient cost inflation and clean label adoption rates. Data gaps in smaller geographies are bridged by applying region-weighted per capita spend differentials that were agreed during expert calls.

Data Validation & Update Cycle

Outputs move through a two-step analyst peer review, anomaly checks against independent retail audit indicators, and variance reconciliation before sign-off. The study is refreshed every twelve months, with interim revisions triggered by material events such as regulatory bans or sharp currency shifts.

Why Mordor's Face Mask Baseline Earns Stakeholder Confidence

Published values often diverge because researchers select dissimilar mask types, base years, and pandemic adjustment rules. Below we benchmark our 2025 figure against external numbers to illustrate the main gap drivers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.88 B (2025) | Mordor Intelligence | - |

| USD 25.10 B (2022) | Global Consultancy A | Includes surgical, respirator, and cloth masks; uses pandemic-elevated year |

| USD 10.76 B (2022) | Trade Journal B | Focuses on protective face masks for healthcare and industry; different base year |

| USD 0.40 B (2025) | Industry Association C | Tracks only sheet masks; excludes clay, peel-off, and cream formats |

The comparison shows that high numbers arise when medical or fashion masks are folded in, while very low values reflect a single product slice. By selecting a clear cosmetic-only scope, employing a consistent currency and inflation baseline, and validating with both channel checks and trade data, Mordor Intelligence provides a balanced, reproducible starting point for strategic decisions.

Key Questions Answered in the Report

What is the current value of the global face mask market and its expected CAGR?

The face mask market size is expected to grow from USD 9.79 billion in 2025 to USD 10.65 billion in 2026 and is forecast to reach USD 16.20 billion by 2031 at a 8.76% CAGR over 2026-2031.

Which region generates the highest revenue in facial masks?

Asia Pacific accounts for 75.43% of global revenue, driven by multi-step skincare routines and high sheet-mask penetration.

Which product type is expanding faster than the overall market?

Clay masks are forecast to post a 2.80% CAGR through 2031, outperforming the total market.

What channel shows the strongest growth outlook?

Online retail is expected to achieve a 4.36% CAGR, boosted by live-streaming commerce and hybrid fulfillment models.

How are regulations influencing formulation strategies?

U.S. MoCRA and EU Regulation 2021/850 tighten ingredient and reporting requirements, favoring brands with robust compliance systems.

Which end-user segment offers the quickest incremental growth?

The men’s segment is projected to grow at a 3.78% CAGR as grooming norms evolve and gender-neutral packaging gains acceptance.

Page last updated on: