Organic Shampoo Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

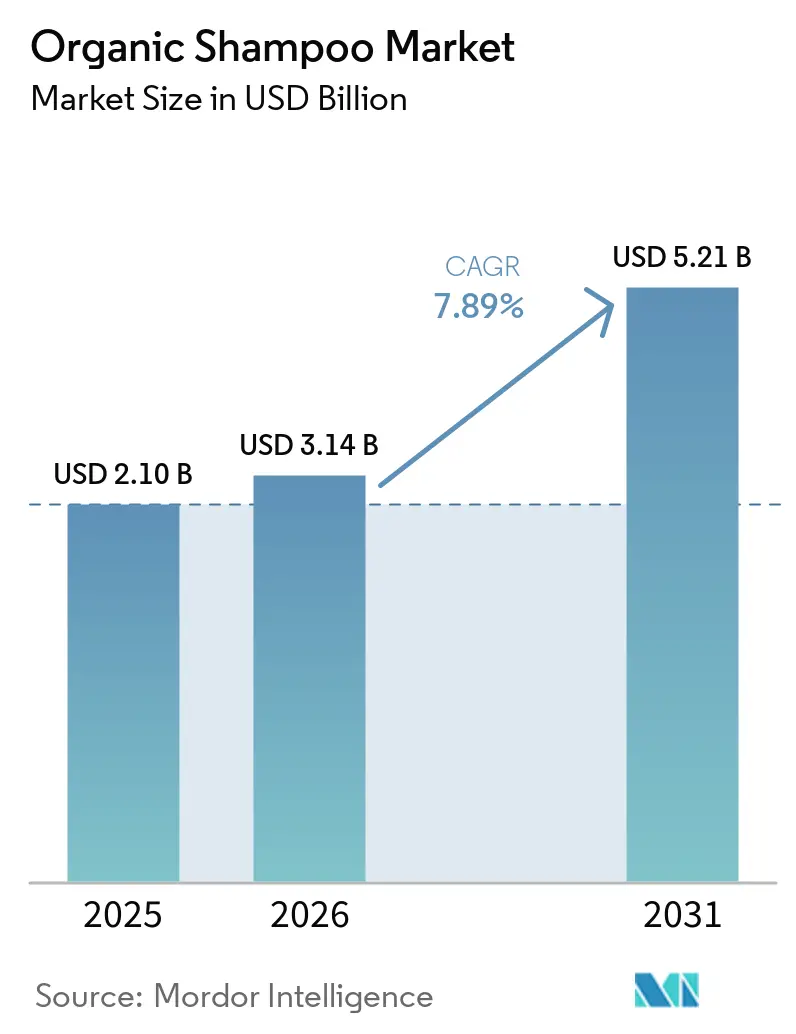

| Market Size (2026) | USD 3.14 Billion |

| Market Size (2031) | USD 5.21 Billion |

| Growth Rate (2026 - 2031) | 7.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Shampoo Market Analysis by Mordor Intelligence

The organic shampoo market size is projected to expand from USD 2.10 billion in 2025 and USD 3.14 billion in 2026 to USD 5.21 billion by 2031, registering a CAGR of 7.89% between 2026 and 2031. Consumer trade-offs have shifted from mere “natural” claims to clinically backed scalp-health benefits as regulatory scrutiny tightens ingredient disclosures in major economies. Retail margins continue to recalibrate because direct-to-consumer (DTC) channels and the collapse of the U.S. de minimis loophole are squeezing informal imports and boosting certified domestic volumes. Price bifurcation is widening: mass lines retain volume leadership, yet premium COSMOS- or USDA-certified SKUs are outpacing them as affluent households treat hair care as a wellness expenditure. Format choices are evolving too; liquid products still dominate, but dry and solid variants are gaining legitimacy amid water-saving lifestyles. Strategic opportunities, therefore, favor brands that marry therapeutic positioning with refillable or waterless delivery systems, while also maintaining digital intimacy with consumers.

Key Report Takeaways

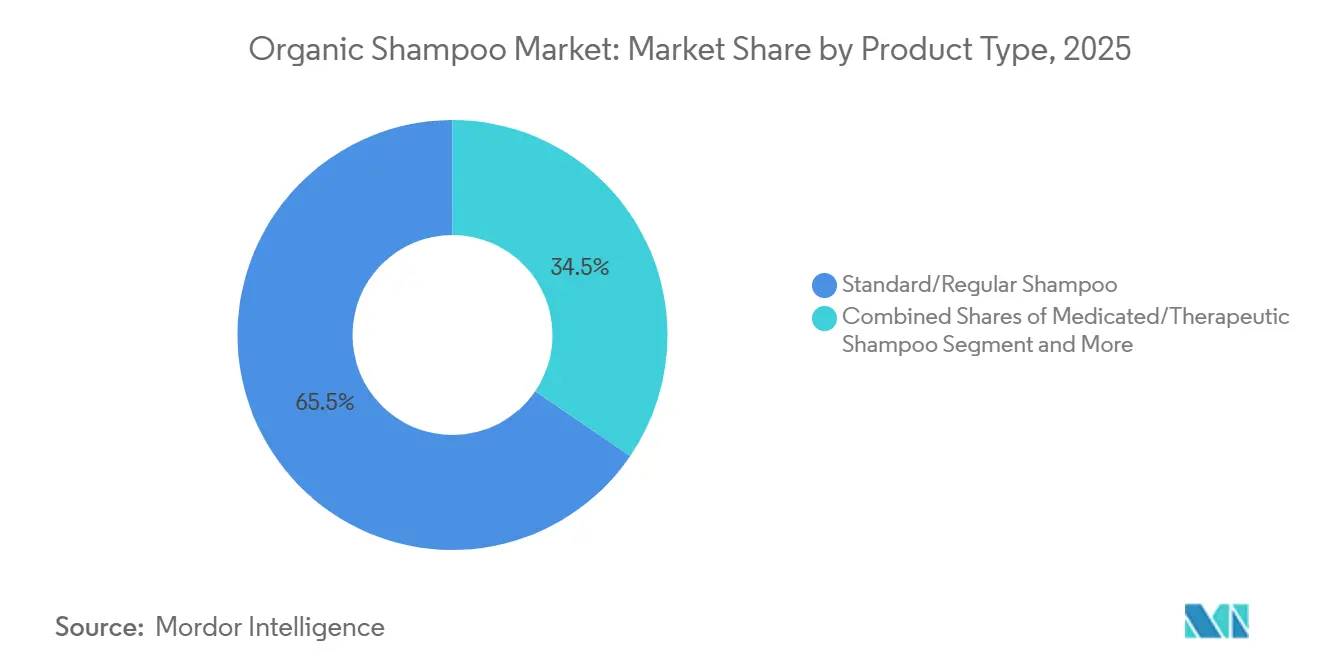

- By product type, Standard/regular formulations captured 65.48% of 2025 revenue, whereas medicated lines are the fastest climbers, advancing at a 9.65% CAGR through 2031.

- By form, Liquid offerings held 80.22% of 2025 volume, yet dry formats are expanding at a 9.62% CAGR.

- By price point, the mass tier accounted for 68.23% of 2025 sales, yet premium offerings are projected to rise at a 9.13% CAGR.

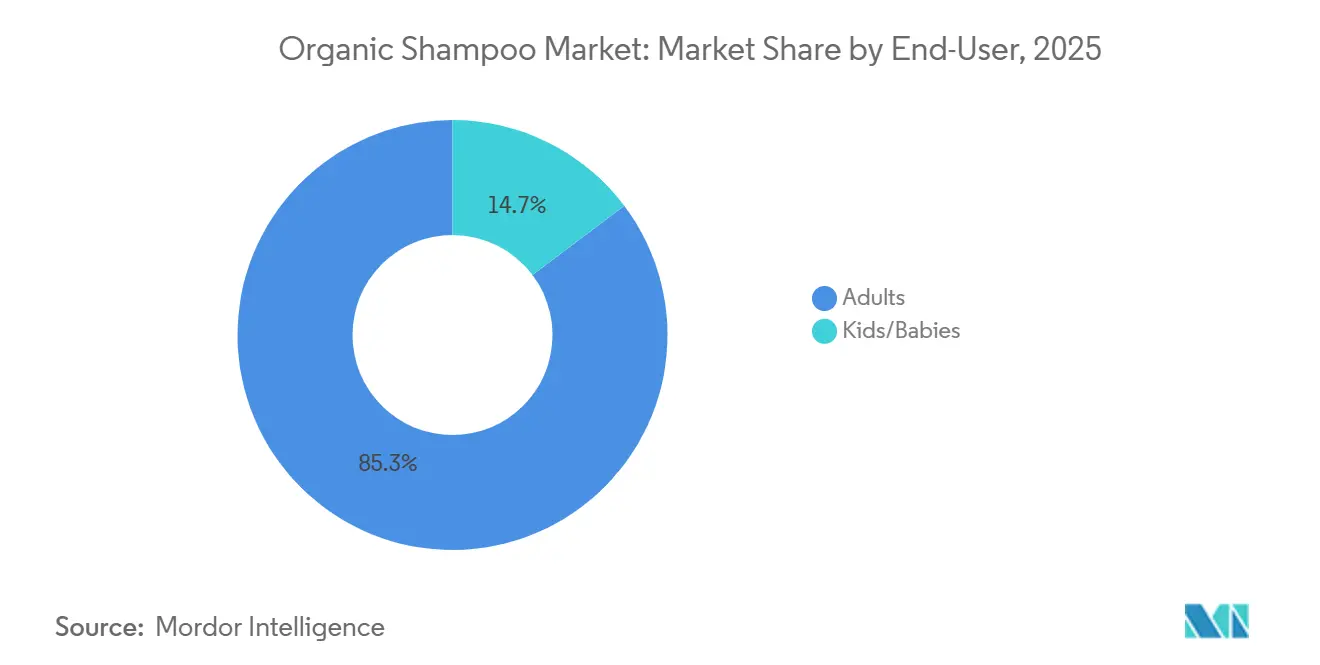

- By end-user, adults dominated with 85.26% share in 2025, while the kids/babies segment is slated for a 8.76% CAGR to 2031.

- By distribution channel, Beauty and health stores led 2025 distribution with 43.28% share, but online retail is set to be the structural winner, growing at a 9.11% CAGR.

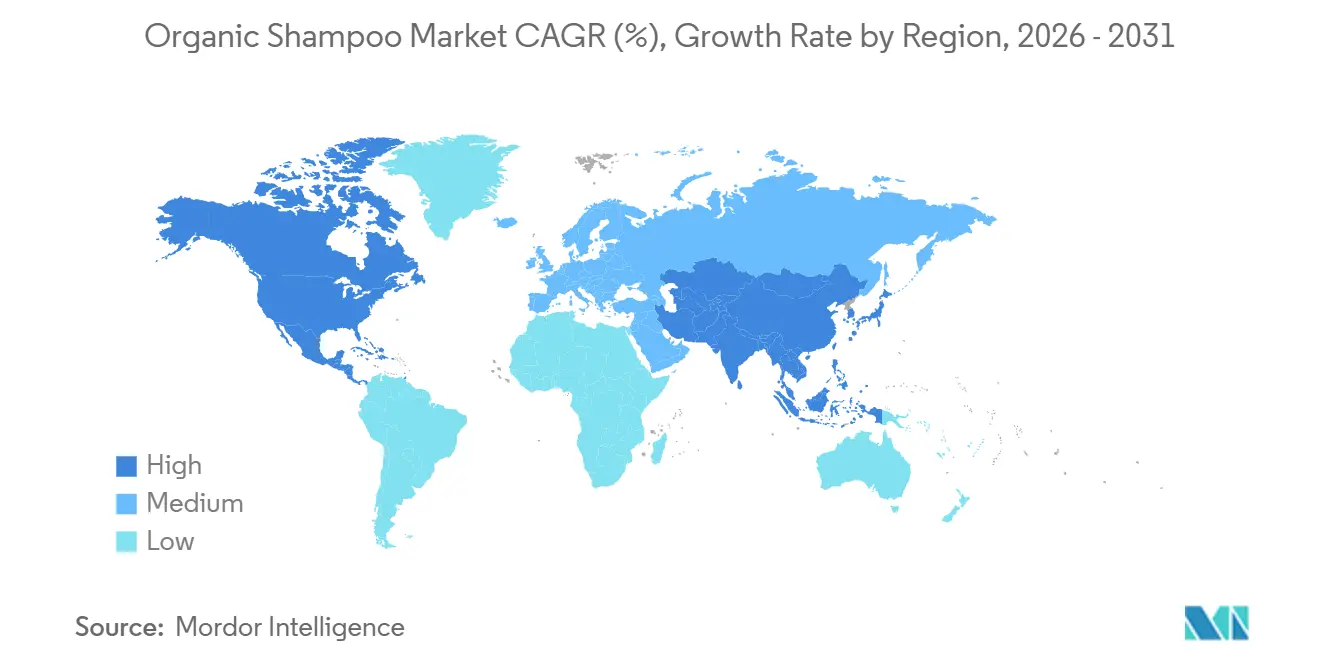

- By geography, North America posted 38.27% of 2025 revenue, while Asia Pacific is forecast to record the quickest regional expansion, rising at an 8.12% CAGR

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Shampoo Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean Beauty Trend Driving Consumer Preference | +1.8% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Rising Demand for Product Personalization | +1.3% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Strong Influence of Social Media Platforms | +1.5% | Global, particularly Asia-Pacific and North America | Short term (≤ 2 years) |

| Growing Focus on Sustainable Packaging Solutions | +1.2% | Europe core, spill-over to North America and APAC | Long term (≥ 4 years) |

| Continuous Innovation in Product Formulations | +1.4% | Global, with R&D concentrated in North America and Europe | Medium term (2-4 years) |

| Expansion of Product Availability and Retail Networks | +0.9% | Asia-Pacific, South America, MEA emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Clean Beauty Trend Driving Consumer Preference

Regulatory momentum is accelerating clean-beauty adoption beyond consumer sentiment alone. The FDA's MoCRA framework, which took effect in December 2022 and expanded through 2024-2026, now requires cosmetic manufacturers to register facilities, report adverse events, and disclose fragrance allergens, a departure from the previous voluntary regime[1]Source: U.S. Food & Drug Administration, “Modernization of Cosmetics Regulation Act,” fda.gov. This shift compels brands to reformulate away from synthetic preservatives and undisclosed fragrance compounds, narrowing the performance gap between organic and conventional shampoos. In parallel, the USDA's Organic Certification Cost Share Program reimburses 75% of certification expenses up to USD 750 annually, lowering the barrier for small-batch producers to enter the certified-organic tier. Social-media platforms amplify ingredient scrutiny; a 2024 study of Indian consumers found that 68% research product formulations on Instagram and TikTok before purchase, and 54% actively avoid sulfates and parabens based on influencer recommendations. Europe's COSMOS standard, which mandates that 95% of plant-derived ingredients be organic, is increasingly referenced by North American retailers as a de facto quality benchmark, even in markets without formal COSMOS recognition. This cross-border regulatory convergence is raising the floor for what qualifies as "clean," forcing laggard brands to either invest in reformulation or cede shelf space to certified competitors.

Rising Demand for Product Personalization

Personalization in hair care has moved from marketing rhetoric to operational reality, driven by advances in AI-driven diagnostic tools and modular formulation platforms. Several brands now offer at-home scalp-analysis kits that measure pH, sebum levels, and microbiome composition, then algorithmically recommend ingredient blends tailored to individual profiles. This shift is economically viable because contract manufacturers have adopted flexible batch sizes, and minimum order quantities have fallen from 10,000 units in 2020 to 1,000 units in 2025, enabling brands to offer dozens of SKU variants without prohibitive inventory risk. The organic segment benefits disproportionately because natural ingredient libraries (e.g., Ayurvedic herbs, cold-pressed oils, botanical extracts) lend themselves to modular mixing. In contrast, synthetic formulations often require fixed ratios to maintain stability. Direct-to-consumer subscription models further monetize personalization: median gross margins for beauty DTC brands reached 69% in 2025, compared to 45% for wholesale channels, because subscribers tolerate higher unit prices in exchange for curated experiences. Regulatory frameworks such as the EU's GDPR and California's CCPA impose data-handling obligations on brands that collect biometric or health-related information, but compliance costs are offset by the customer lifetime value uplift, personalized hair-care subscriptions exhibit 30% lower churn than generic offerings.

Strong Influence of Social Media Platforms

Social media has evolved from a discovery channel into a transaction layer, with platforms embedding native checkout flows that collapse the path from content to purchase. TikTok Shop, launched in the United States in 2023 and expanded globally through 2024-2025, enables creators to tag products directly in videos, and organic hair-care brands report conversion rates 2-3 times higher than traditional e-commerce. Instagram's algorithm prioritizes video content with high engagement, rewarding brands that invest in user-generated content campaigns; a 2024 analysis found that posts featuring customer testimonials generate 4.2 times more engagement than brand-produced content. Micro-influencers (10,000-100,000 followers) command lower sponsorship fees than macro-influencers yet deliver comparable conversion rates in niche categories such as organic personal care, making them cost-effective proxies for traditional advertising. Regulatory scrutiny is intensifying: the Federal Trade Commission updated its endorsement guidelines in 2024 to require explicit disclosure of material connections between brands and influencers, and non-compliance can trigger fines up to USD 50,000 per violation[2]Source: Federal Trade Commission. "Updated Endorsement and Testimonial Guidelines." ftc.gov.. Despite these guardrails, social platforms remain the primary discovery mechanism for consumers under 35, and brands that fail to maintain an active presence risk invisibility in a category where purchase decisions are increasingly driven by peer validation rather than retailer recommendations.

Expansion of Product Availability and Retail Networks

Retail expansion in emerging markets is outpacing infrastructure development, creating both opportunity and friction. In India, organized retail (supermarkets, hypermarkets, specialty chains) accounts for only 12% of total retail sales, yet e-commerce penetration in beauty and personal care reached 18% in 2025, leapfrogging the traditional brick-and-mortar buildout. This dynamic favors organic hair-care brands that can partner with e-commerce platforms (Amazon, Flipkart, Nykaa) to reach tier-2 and tier-3 cities without investing in physical distribution networks. In China, the cross-border e-commerce channel, enabled by free-trade zones in Shanghai, Hangzhou, and Guangzhou, allows foreign brands to sell directly to consumers without formal import licenses, bypassing the 18-24 month registration process required for conventional retail. However, this channel is under regulatory review; the General Administration of Customs announced in 2024 that it would tighten product-safety inspections for cross-border shipments, potentially slowing the entry of smaller organic brands. In Latin America, beauty and health stores (e.g., Drogasil in Brazil, Farmacity in Argentina) are expanding their organic SKU assortments in response to consumer demand, but import tariffs on finished goods remain high (15-35% depending on country), incentivizing local contract manufacturing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Presence of Counterfeit and Substandard Products | -0.7% | Global, with concentration in Asia-Pacific and MEA | Short term (≤ 2 years) |

| Intense Competition from Synthetic Shampoo Alternatives | -0.9% | Global, particularly mass-market segments | Medium term (2-4 years) |

| Complexities in Certification and Compliance Processes | -0.6% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| High Cost Associated with Products | -0.8% | Emerging markets in Asia-Pacific, South America, MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Presence of Counterfeit and Substandard Products

Counterfeit organic shampoos undermine brand equity and consumer trust, with enforcement data revealing the scale of the problem. U.S. Customs and Border Protection reported in 2024 that 31% of all intercepted counterfeit goods fell into the health and beauty category, and the agency seized over USD 50 million worth of fake personal-care products in fiscal year 2024 alone[3]Source: U.S. Customs & Border Protection, “Enforcement Statistics,” cbp.gov. The closure of the de minimis loophole in April 2025, which previously exempted shipments under USD 800 from formal entry procedures, has reduced the volume of uncertified products entering the United States, but counterfeiters have adapted by mislabeling shipments or routing goods through third countries. The FDA's cosmetic product listing database, launched in 2024 under MoCRA, is intended to improve traceability, but compliance remains voluntary until 2026, leaving a gap that counterfeiters exploit FDA Cosmetic Product Listing. In Asia-Pacific markets, enforcement is weaker; a 2025 study of e-commerce platforms in India and Indonesia found that 22% of "organic" shampoo listings lacked verifiable certification, and 14% contained prohibited ingredients such as formaldehyde-releasing preservatives

Intense Competition from Synthetic Shampoo Alternatives

Synthetic shampoos retain cost and performance advantages that organic formulations struggle to match at mass-market price points. Conventional surfactants such as sodium lauryl sulfate (SLS) deliver superior lather and cleansing efficiency at one-tenth the cost of plant-derived alternatives like coco-glucoside or decyl glucoside, enabling synthetic brands to undercut organic competitors by 30-50% on shelf price. Silicones (e.g., dimethicone, cyclomethicone) provide instant smoothness and shine that organic oils cannot replicate without multiple rinses, a performance gap that matters to consumers prioritizing convenience over ingredient purity. Large CPG companies (Procter & Gamble, Unilever, L'Oréal) leverage economies of scale to invest in marketing budgets that dwarf those of organic specialists; P&G's Pantene brand alone spent an estimated USD 200 million on global advertising in 2025, creating top-of-mind awareness that organic brands cannot match.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Therapeutic Variants Outpace Core Offerings

Standard shampoos accounted for 65.48% of the 2025 market volume, reflecting their broad appeal and strong distribution networks. Medicated formulations, however, are growing rapidly at a 9.65% CAGR through 2031, the fastest among product types. This shift highlights changing consumer priorities, with hair care increasingly linked to scalp health rather than aesthetics. Anti-dandruff and scalp-repair shampoos address specific issues like flaking and irritation but lack the clinical branding of medicated products. The "Others" category, including color-safe, volumizing, and curl-defining products, serves niche needs but trails therapeutic lines in growth. Medicated shampoos benefit from the integration of dermatology and cosmetics, with ingredients like ketoconazole, zinc pyrithione, and salicylic acid, once prescription-only, now featured in over-the-counter organic formulations combining efficacy with clean-label appeal.

The microbiome revolution is reshaping therapeutic branding. A 2024 study linked bacterial imbalances to seborrheic dermatitis and androgenetic alopecia, prompting brands to include prebiotics and postbiotics to balance scalp flora while protecting the skin barrier. This scientific approach differentiates medicated organics from generic "natural" claims, appealing to consumers seeking proven results. Regulatory frameworks also support therapeutic innovation. The FDA's monograph system allows certain active ingredients, such as coal tar and selenium sulfide, to be marketed without pre-market approval, expediting the launch of medicated organics. Standard shampoos, in contrast, compete on price and brand familiarity, limiting differentiation. Anti-dandruff products face commoditization as ingredients like zinc pyrithione and piroctone olamine become widespread, while the "Others" category remains fragmented into small micro-segments, each too minor to justify significant R&D investment.

By Form: Dry Formats Gain Traction Amid Waterless Trends

In 2025, liquid shampoos accounted for 80.22% of the market, driven by established consumer habits and manufacturing systems. However, dry formats are growing at a 9.62% CAGR through 2031 as waterless routines gain popularity. Dry shampoos, available as powders or aerosols, absorb sebum without rinsing, appealing to busy consumers and travelers. Solid shampoo bars eliminate plastic packaging and reduce shipping weight by 80%, aligning with sustainability goals. Liquid formats still perform better, rinsing cleanly, distributing evenly, and supporting a wider range of active ingredients like botanical extracts and essential oils. However, advancements in microencapsulation are helping stabilize volatile compounds in powder form, narrowing the gap.

Dry formats offer significant environmental benefits. A 250ml liquid shampoo bottle weighs about 300 grams (including water and packaging), while a 60-gram solid bar provides equivalent washes, cutting transport emissions by 75% and eliminating single-use plastics. The EU's 2024 revision of the Packaging and Packaging Waste Directive encourages brands to adopt concentrated or solid formats by imposing fees on plastic containers. Consumer acceptance is growing: a 2025 survey showed 42% of European consumers had tried solid shampoo bars, up from 28% in 2023, with 68% reporting positive experiences. Dry shampoos face challenges like residue buildup and scalp irritation from overuse, but brands are addressing these with finer particles and oil-absorbing clays like kaolin and bentonite. Liquid formats will dominate in the short term, but dry variants are gaining momentum as sustainability pressures grow and formulation challenges are resolved.

By Price Point: Premium Tier Expands Despite Economic Headwinds

In 2025, mass-market offerings accounted for 68.23% of revenue, driven by price-sensitive households and extensive retail distribution. Meanwhile, premium products are growing at a 9.13% CAGR through 2031, reflecting a divide in consumer spending. Premium organic shampoos, priced at USD 15-30 per bottle, justify their cost with certifications (USDA Organic, COSMOS), exotic ingredients like argan oil, and brand narratives emphasizing artisanal production or social impact. Mass-market organic shampoos, priced at USD 6-12, prioritize affordability by relying on "natural" claims over full organic certification. The premium segment's growth highlights a broader trend: affluent consumers increasingly spend on perceived healthier or sustainable products, despite inflation affecting other categories.

Direct-to-consumer (DTC) channels drive premium growth by retaining margins typically lost to retailers. In 2025, beauty DTC brands reported median gross margins of 69%, compared to 45% for wholesale, enabling greater investment in customer acquisition while remaining profitable. Subscription models enhance premium positioning, as consumers paying for recurring shipments accept higher prices for convenience and personalization. Subscription beauty products also see churn rates 30% lower than one-time purchases. Mass-market brands, in contrast, rely on shelf visibility and promotions, limiting margin growth. Private-label organics, priced between mass and premium, are emerging but lack the brand equity and storytelling that drive premium loyalty. While the mass segment will lead in volume, the premium tier's faster growth signals a clear split in the organic category's value propositions.

By End-User: Kids/Babies Segment Accelerates on Safety Focus

In 2025, adults represented 85.26% of the end-user volume due to their larger population and higher per-capita consumption. However, the kids/babies segment is set to grow at an 8.76% CAGR through 2031, driven by rising parental safety concerns. Parents increasingly prefer fragrance-free, pH-neutral formulations to minimize irritation risks. A 2024 UK study found 72% of parents actively seek products labeled "hypoallergenic" or "dermatologist-tested" for their children. Organic certification is often seen as a safety indicator, though USDA and COSMOS standards do not specifically address allergenicity or toxicology. Regulatory support also aids this segment: the EU's Cosmetics Regulation (EC) No 1223/2009 limits certain preservatives and fragrances in products for children under 3, favoring organic formulations over conventional ones.

Parents view hair care for children as a health necessity, reducing price sensitivity in the kids/babies segment. A 2025 survey showed 64% of UK parents are willing to pay a 20-30% premium for organic baby shampoos, compared to 38% for adult products. This willingness supports higher margins despite lower unit sales. In contrast, the adult segment is commoditized in the mass tier and fragmented in the premium tier, with numerous SKUs competing for shelf space. Demographic trends favor the kids/babies segment: while birth rates in developed markets decline, per-child spending rises as parents focus resources on fewer children. In emerging markets, growing middle-class incomes and urbanization are boosting demand for premium baby-care products, including organic shampoos. Although adults will remain the volume leader, the kids/babies segment's faster growth and higher margins offer brands a strong differentiation opportunity.

By Distribution Channel: Online Retail Reshapes Margin Structures

In 2025, beauty and health stores held a 43.28% distribution share due to curated selections and in-store expertise. However, online retail channels are growing at a 9.11% CAGR through 2031, driven by e-commerce economics and consumer convenience. Platforms like Amazon, niche beauty websites, and brand-owned DTC stores remove geographic barriers and enable niche SKUs, products unsuitable for physical shelves, to reach targeted audiences. Supermarkets and hypermarkets focus on mass-market brands, while convenience stores cater to impulse buys. These outlets lack the assortment depth and educational content that drive organic sales. Beauty and health stores balance curated selections and staff insights, but face margin pressures from online competitors bypassing retail mark-ups.

E-commerce is transforming customer acquisition and retention. Online beauty brands spend USD 30-50 per customer on digital ads via platforms like Facebook and Google, recovering costs through higher lifetime value: repeat buyers generate 3-4 times the margin of one-time customers, and subscription models ensure recurring revenue. Physical retailers rely on foot traffic and discounts, which compress margins. The pandemic accelerated e-commerce, with online beauty sales rising 40% in 2020-2021. While growth has normalized, online penetration remains at 18-22% in major markets. Omnichannel strategies are gaining traction, using physical stores for brand visibility and product discovery while driving online transactions for better margins. Beauty and health stores will retain near-term share due to expertise and curated offerings, but online channels are set to dominate as logistics improve and consumers grow more comfortable with digital beauty purchases.

Geography Analysis

In 2025, North America is expected to contribute 38.27% of global revenue, maintaining its position as the leader in per-capita certified spending. MoCRA's stricter regulations favor brands with established traceability systems, while USDA cost-share grants make it easier for independent players to enter the market. The de minimis closure in 2025 reduced uncertified imports, driving demand toward domestic producers and supporting premium price floors.

Asia-Pacific is projected to record the fastest growth, with an estimated 8.12% CAGR through 2031. Enhanced verifications by CNCA strengthen the authenticity of "organic" claims. Furthermore, products combining Ayurvedic or traditional Chinese botanicals with modern science are resonating with urban consumers seeking aspirational options. While cross-border e-commerce free-trade zones reduce time-to-shelf, new customs checks impose stricter safety documentation requirements.

Europe, supported by COSMOS and the EU Cosmetics Regulation, continues to set the standard for quality. Sustainability measures, particularly the Packaging Directive, are driving the adoption of refill pouches, positioning Europe as a hub for circular models now spreading globally. Midsona's milestone of achieving 65% recycled plastic highlights corporate alignment with these sustainability objectives. Although South America and the MEA regions lag in overall volume, they offer long-term growth potential as tariff and currency challenges diminish and the popularity of halal-plus-organic labels increases.

Competitive Landscape

In the organic shampoo market, a concentration score of 5 signifies a balanced coexistence between large conglomerates and agile indie brands. L’Occitane, capitalizing on its scale, has relaunched refill programs that successfully reduce plastic usage by 70%, thereby strengthening its premium positioning in the market. Midsona's acquisition of Risenta in 2026 not only consolidates its presence in Nordic retail spaces but also unlocks synergies valued at SEK 20 million. On the other hand, Hain Celestial's ongoing strategic review underscores the risks associated with insufficient investment in innovation, particularly as the company faces declining revenues in the personal-care segment.

Indie brands such as Juicy Chemistry and Acure are effectively utilizing direct-to-consumer (DTC) platforms, AI-powered personalization tools, and micro-influencer networks to outperform traditional marketing cycles. The adoption of advanced technologies is becoming a critical differentiator in the market. For instance, blockchain-based provenance tags enhance product authenticity and deter counterfeit activities, while AI-driven batching processes significantly reduce the time required to bring products from concept to retail shelves. Additionally, niche segments such as therapeutic shampoos, waterless formulations, and products designed for children and babies offer substantial growth potential. These opportunities are particularly pronounced in the fast-growing markets of APAC and Latin America, where category penetration remains relatively low, presenting untapped demand.

Regulatory compliance is increasingly acting as a competitive differentiator. Companies with expertise in adhering to USDA, COSMOS, CNCA, and MoCRA standards are better positioned to scale their operations across borders efficiently. Conversely, businesses that lag in compliance face heightened risks of delisting, especially as retailer audits become more rigorous. As a result, strategic mergers and acquisitions (M&A) are not only targeting brand portfolios but are also focusing on acquiring compliance infrastructures and formulation intellectual property. These assets enable companies to expedite multi-market regulatory approvals, providing a significant competitive edge in the global market.

Organic Shampoo Industry Leaders

-

The Hain Celestial Group, Inc.

-

Dr. Organic Ltd.

-

John Masters Organics

-

Neal’s Yard (Natural Remedies) Limited

-

L'Occitane Groupe S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: AVEDA, a purpose-driven pioneer of plant-powered, high-performance beauty that offers organic shampoo, announced its debut in the Amazon.ca Premium Beauty store, bringing its assortment of vegan hair, skin, body, and lifestyle products to consumers across the country. AVEDA's Amazon.ca Premium Beauty storefront featured an immersive Hair Care Guide – an educational experience page created in partnership with salon professionals from the AVEDA network. This guide included videos, product highlights, and storytelling to help consumers recreate their salon style at home.

- February 2025: Puddles introduced an organic skincare and haircare range for teenagers, expanding its COSMOS‑certified children’s portfolio. The range featured pH‑balanced, toxin‑free products made with ingredients like willow bark, basil, cica, turmeric, organic Parijat essential oil, and coconut cleansers. The products include shampoo.

- July 2024: An organic and vegan Australian brand launched 100 per cent natural shampoo and conditioner. With a commitment to ingredient transparency and customer wellbeing, the new products aimed to rival some of the best synthetic brands found in top-tier salons, while harnessing the power of natural, ethically sourced ingredients.

Global Organic Shampoo Market Report Scope

| Standard/Regular Shampoo |

| Anti-Dandruff/Scalp Repair Shampoo |

| Medicated/Therapeutic Shampoo |

| Others |

| Liquid |

| Dry |

| Mass |

| Premium |

| Adults |

| Kids/Babies |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Beauty And Health Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Standard/Regular Shampoo | |

| Anti-Dandruff/Scalp Repair Shampoo | ||

| Medicated/Therapeutic Shampoo | ||

| Others | ||

| By Form | Liquid | |

| Dry | ||

| By Price Point | Mass | |

| Premium | ||

| By End-User | Adults | |

| Kids/Babies | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Beauty And Health Stores | ||

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the organic shampoo market be by 2031?

The organic shampoo market size is projected to reach USD 5.21 billion by 2031, expanding at a 7.89% CAGR from 2026 to 2031

Which product type is growing fastest?

Medicated and therapeutic variants are the quickest risers, advancing at a 9.65% CAGR through 2031.

How is online retail affecting category margins?

Online channels grow at a 9.11% CAGR and deliver median gross margins of 69% because DTC models bypass retailer mark-ups, improving profitability.

Why are premium prices sustainable despite inflation?

Certified COSMOS or USDA labels, refillable packaging, and subscription convenience, sustaining premium tier growth at 9.13% CAGR

Page last updated on: