Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 37.26 Billion |

| Market Size (2031) | USD 47.03 Billion |

| Growth Rate (2026 - 2031) | 4.77% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

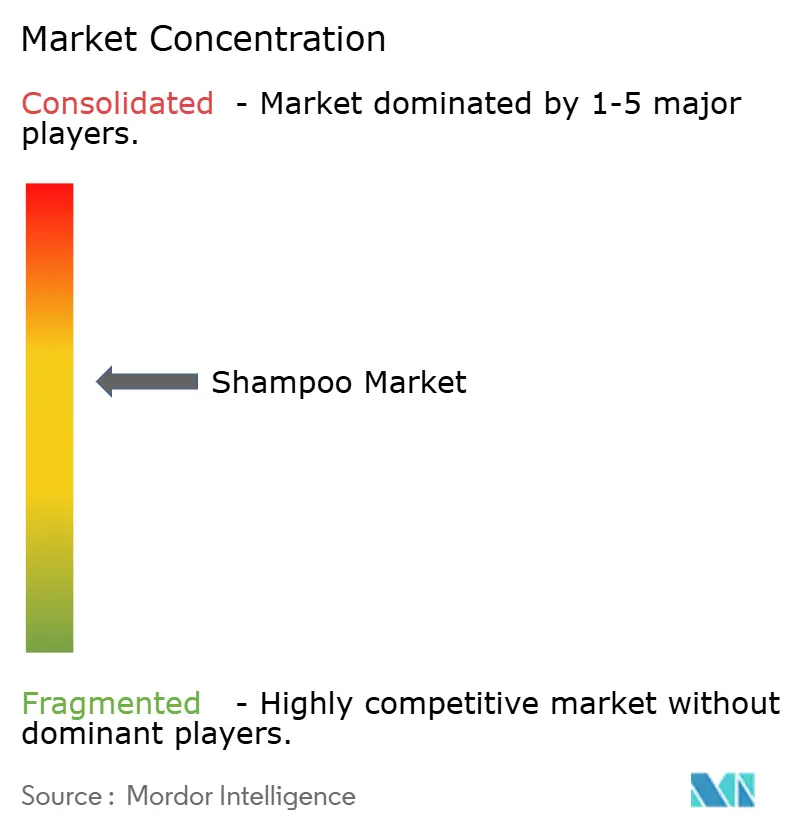

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Shampoo Market Analysis by Mordor Intelligence

The global shampoo market size was valued at USD 35.6 billion in 2025 and estimated to grow from USD 37.26 billion in 2026 to reach USD 47.03 billion by 2031, at a CAGR of 4.77% during the forecast period (2026-2031). The global hair shampoo market is on a steady rise, driven by changing consumer behaviors in retail. Today's shoppers prioritize ingredient transparency, wellness benefits, and ethical sourcing. This shift has bolstered the popularity of natural and organic shampoos, with brands like Garnier Whole Blends and Herbal Essences Bio: Renew leading the charge. The trend of premiumization is evident, as consumers opt for higher-end products like Kérastase Nutritive and Olaplex Bond Maintenance, signaling their readiness to invest in home-use solutions that deliver visible results. While mass-market giants like Head & Shoulders and Dove maintain their shelf dominance, younger consumers are turning to direct-to-consumer and niche brands. Personalized offerings, such as those from Function of Beauty and Prose, let buyers tailor formulations to their unique hair types and lifestyles. The online marketplace is further propelling this trend, granting consumers easy access to emerging brands and customized solutions. The Asia-Pacific region is at the forefront of this global growth, buoyed by rising incomes and a surge in digital commerce, leading to frequent product trials and brand-switching. Meanwhile, North America and Europe are leaning towards eco-conscious packaging and variants that are sulfate-free and vegan. In essence, the demand for shampoos is evolving, emphasizing premium efficacy, personalization, and sustainability, with consumers redefining value beyond mere pricing.

Key Report Takeaways

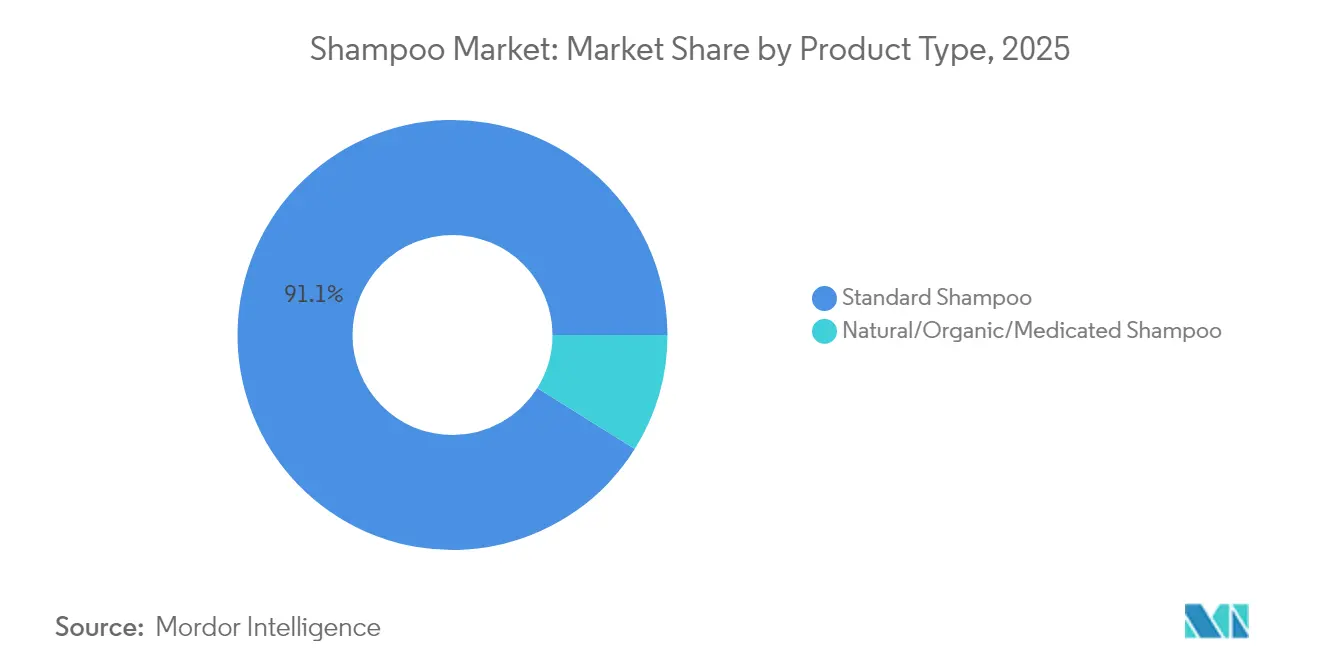

- By product type, standard shampoos commanded 91.10% of the shampoo market share in 2025, while natural, organic, and medicated variants are advancing at a 6.92% CAGR to 2031.

- By hair concern, specific-purpose formulations commanded 55.10% of the shampoo market revenue in 2025 and are advancing at a 4.83% CAGR through 2031.

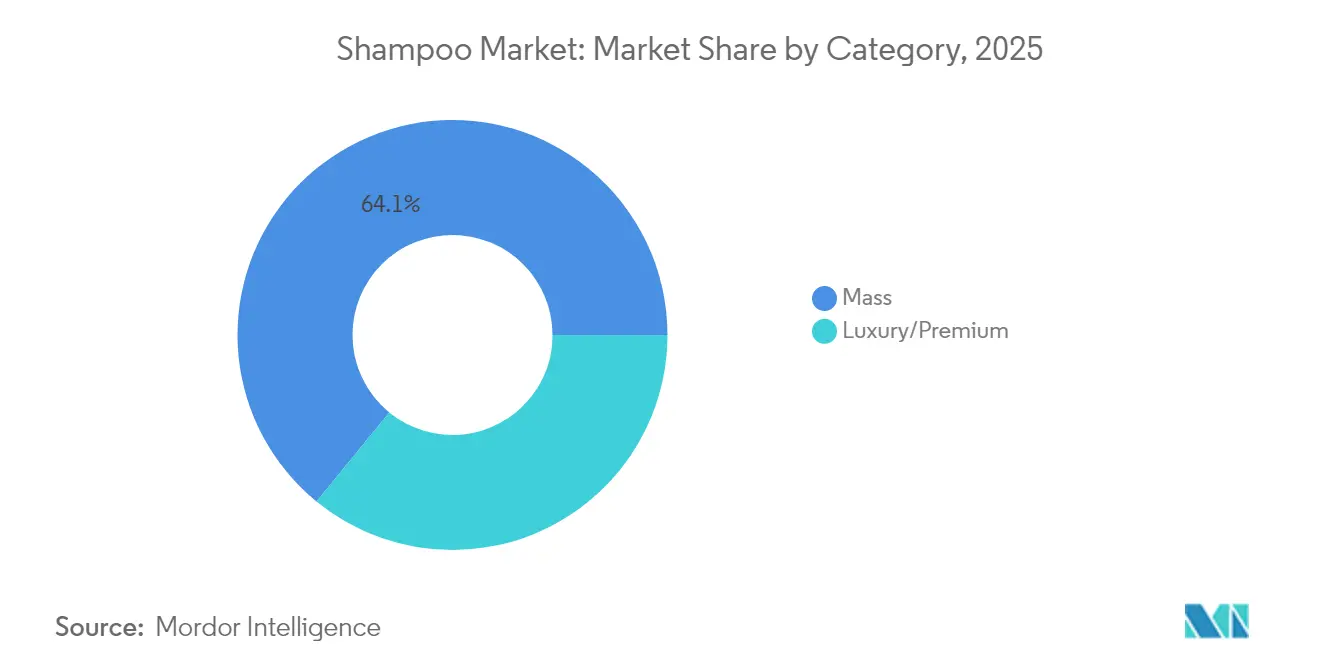

- By category, the mass segment commanded 64.10% of the shampoo market share in 2025, while the premium/luxury segment is advancing at a 4.93% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets commanded 35.20% of the shampoo market share in 2025, while online retail is advancing at a 6.38% CAGR through 2031.

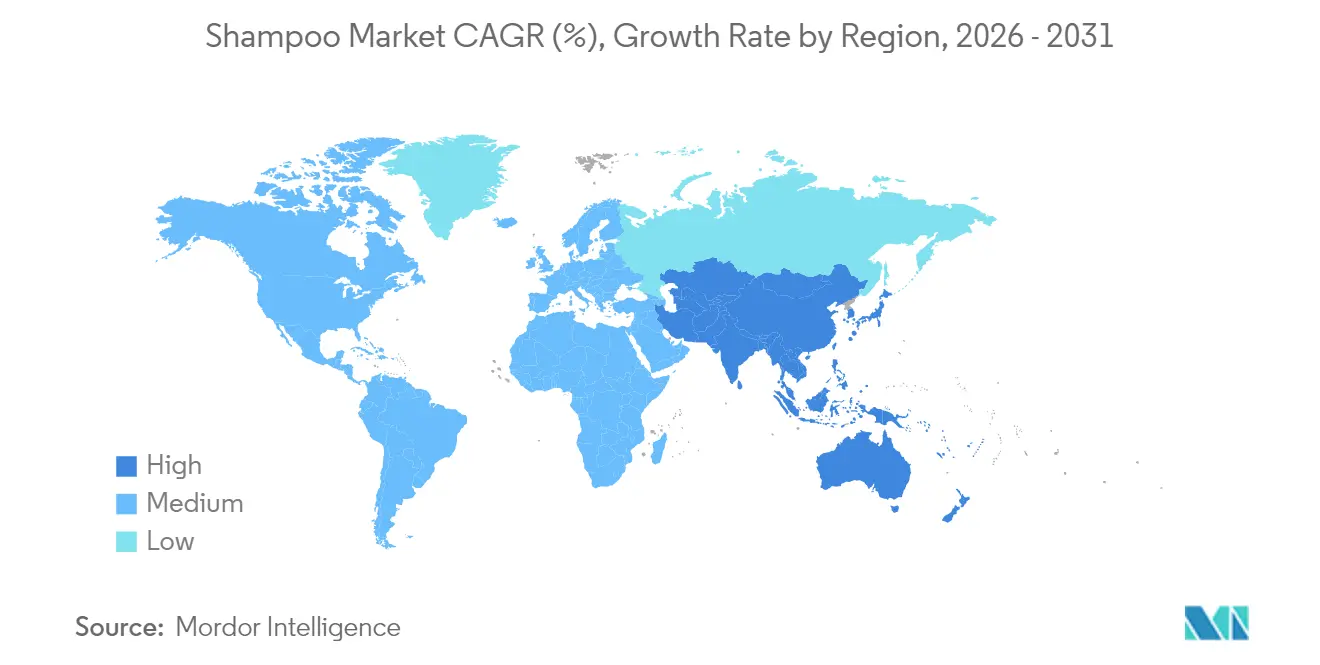

- By geography, Asia-Pacific commanded 47.10% of the shampoo market share in 2025 and is advancing at a 5.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Shampoo Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for organic and herbal shampoos | +1.2% | North America, Europe, Asia- Pacific | Medium term (2-4 years) |

| Social-media and digital-marketing influence | +0.8% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Rising demand in men’s segment | +0.6% | Asia-Pacific, Global | Medium term (2-4 years) |

| Adoption of multifunctional, active-rich formulas | +0.9% | Global premium tiers | Long term (≥ 4 years) |

| Sustainability and eco-friendly packaging | +0.7% | Europe, North America | Long term (≥ 4 years) |

| AI-based personalization and customization | +0.5% | North America, Asia- Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing preference for organic and herbal shampoos

As consumers increasingly seek gentler, cleaner alternatives that resonate with their wellness values, the retail haircare market witnesses a surge in demand for organic and herbal shampoos. A March 2025 study by NSF revealed that 74% of consumers now prioritize organic ingredients in personal care, underscoring a significant pivot towards clean beauty [1]Source: NSF International, “Global Consumer Insights on Organic Personal Care,” nsf.org. This shift is spurring product innovations, exemplified by Herbal Essences’ “Pure Plants” range, crafted with aloe and camellia oil, and designed for eco-conscious consumers with its transparent ingredient list and sustainable packaging. In India, brands like Forest Essentials, Lotus Herbals, Biotique, Pilgrim, Jovees, and Khadi Natural are spearheading the growth of retail herbal shampoos. These brands are infusing botanicals such as shikakai, amla, neem, hibiscus, and bhringraj into their offerings. Marketed to address issues like dandruff, hair fall, and scalp health, these shampoos leverage digital-first campaigns, influencer collaborations, and platforms like Nykaa to connect with a younger, ingredient-savvy audience. In 2024, Beyoncé’s Cécred line debuted, spotlighting bioactive natural ingredients like fermented rice water, showcasing the swift consumer embrace of plant-powered claims. Ultimately, as shoppers emphasize authenticity, efficacy, and sustainability, organic and herbal shampoos are evolving from niche options to pivotal players in the global retail shampoo market.

Influence of social media and digital marketing

Social media and digital marketing are reshaping consumer engagement and purchasing decisions in the shampoo market, with online influence emerging as a pivotal driver of retail growth. A 2024 survey from the University of Portsmouth revealed that 60% of consumers place their trust in influencer recommendations [2]Source: University of Portsmouth, “Influencer Impact on Consumer Skincare Choices,” port.ac.uk. Furthermore, nearly half of all purchase decisions are swayed by these endorsements, highlighting the significant impact of digital voices on consumer behavior. Celebrity-led product launches underscore this trend: Beyoncé’s Cécred line swiftly gained traction on TikTok and Instagram, while Blake Lively’s beauty brand debut in 2024 showcased the power of cultural icons in generating immediate awareness and driving retail demand. Established brands are also capitalizing on this trend. Olaplex remains at the forefront of digital haircare discussions, due to influencer-led tutorials. In India, brands like Biotique and Pilgrim are leveraging Instagram Reels and micro-influencers to promote natural shampoos, addressing local concerns such as dandruff and hair fall. Retail platforms are not to be outdone; Nykaa, with its ambassadors Sharvari and Rasha Thadani, has transformed its shampoo and haircare portfolio into a leading sales category, owing to aspirational campaigns that seamlessly merge beauty with lifestyle. These concerted efforts underscore the evolution of shampoo purchases: once a routine necessity, it's now a lifestyle choice, driven by social media engagement, peer validation, and celebrity endorsement. This shift is not only accelerating the adoption of premium products but also expanding the reach of both established and emerging retail brands.

Increasing demand for men's segment shampoos

As men increasingly embrace grooming as a vital aspect of self-care, men's shampoo is witnessing a surge in popularity, driving retail growth. A significant catalyst for this trend is the rising concern over hair loss. Medihair reports that over 65% of American men will experience varying degrees of hair loss by age thirty-five. By age 50, around 85% will exhibit signs of thinning, and nearly a quarter will start losing hair before turning 21 [3]Source: Medihair, “Hair Loss Statistics 2025,”medihair.com. This widespread concern is fueling the demand for retail solutions tailored to men's specific needs. In 2025, Phyto introduced its Anti-Itch Shampoo, crafted for sensitive male scalps, underscoring the industry's pivot towards gender-specific products. Retail giants are expanding their men's product lines, with offerings like Head & Shoulders' Men Ultra, boasting anti-dandruff and deep-cleaning features, and Beardo's Onion Shampoo, which not only addresses hair fall but also resonates with the growing preference for natural ingredients. Premium brands, such as American Crew, are amplifying their shampoo presence in modern trade outlets, catering to urban professionals desiring salon-quality results at home. In India, grooming-centric firms like Man Matters are expanding their men's shampoo selections across both e-commerce and brick-and-mortar stores, integrating them into comprehensive wellness routines. These developments underscore a significant shift: men are moving away from generic or family-oriented products, actively pursuing shampoos that resonate with their lifestyle and identity. This shift is not only expanding both the functional and premium segments but also propelling the overall growth of the shampoo market.

Rise of multifunctional shampoos with innovative active ingredients

As consumers increasingly prioritize efficient, purpose-driven products, multifunctional shampoos are stepping up to the plate, seamlessly blending cleansing, treatment, and styling benefits. Brands are crafting intelligent formulations that pack multiple advantages into a single application. Take Nutrafol’s Men’s Active Cleanse (2024), for example: it not only combines shampoo and conditioner but also champions scalp microbiome health with its gentle, biosurfactant-based cleansing. This appeals directly to men who value both effectiveness and simplicity. Viemaa’s 2025 BOND SHAMPOO takes it a notch higher, incorporating Biomimetic Cuticle Technology and hydrolyzed pea protein. This duo cleanses, fortifies, detangles, and revives damaged hair, catering to the dual demand for repair and convenience. Clean-hair pioneer Evolvh introduced its Better Roots Growth Shampoo (late 2024), harnessing biomimetic peptides and prickly pear elixir. This formulation not only bolsters scalp health and strengthens follicles but also ensures hydration, underscoring the consumer's desire for multifunctional performance. Verb’s Dandruff Shampoo (2024) masterfully combines high-concentration salicylic acid with the calming properties of clary sage and zinc PCA. This blend not only tackles dandruff head-on but also nourishes the scalp, addressing multifaceted concerns in one go.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory challenges | -0.9% | North America, Europe | Medium term (2-4 years) |

| High competition and market saturation | -1.1% | Global mature markets | Short term (≤ 2 years) |

| Supply-chain disruptions | -0.7% | Global | Short term (≤ 2 years) |

| Counterfeit shampoos | -0.6% | Emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High competition and market saturation

Oversaturation is posing significant challenges to the global shampoo market, as an influx of competing products across all segments makes it hard for brands to distinguish themselves. Mass-market players, like Tresemmé with its Pro Pure collection and Sunsilk's new herbal infusions, are consistently broadening their offerings. Concurrently, natural-centric brands such as Lotus Herbals and Pilgrim are introducing overlapping variants, emphasizing botanicals like aloe, hibiscus, and onion extract. Premium brands, including Aveda and Redken, are expanding their retail footprint with treatment-focused shampoos, merging the realms of salon-quality and mass-market products. Celebrity-backed launches, from Jisoo’s beauty line in Korea to Beyoncé’s Cécred, have heightened competition, shifting consumer focus from brand loyalty to novelty. E-commerce giants like Amazon and Nykaa showcase numerous similar dandruff and hair-fall shampoos, pushing brands to resort to heavy discounts for visibility. This plethora of options is muddying consumer choices, diluting long-term loyalty, and compelling both established and new brands to invest heavily in marketing for relevance. Retailers, with limited shelf space, are curtailing product duplication by streamlining their assortments, often at the expense of smaller brands. Consequently, the market is becoming increasingly crowded, making differentiation a challenge, squeezing profitability, and stunting overall growth, even with a steady stream of new product launches.

Availability of counterfeit shampoos

Counterfeit shampoos are shaking consumer confidence and stunting legitimate growth in the global haircare market. For example, an incident in April 2025: Surat authorities intercepted counterfeit "Head & Shoulders" shampoo bottles, valued at over INR16 lakh, intended for online and wholesale sales. This incident underscores the alarming infiltration of counterfeit products into mainstream distribution channels. Further raids in the same area revealed misleadingly labeled adulterated shampoos, amplifying the confusion these illicit products create at retail outlets. When consumers inadvertently buy these subpar imitations and face disappointing results or even adverse reactions, their trust in both the brand and the broader category wanes. This erosion of trust makes consumers wary of trying new products or splurging on premium ones. In light of these challenges, brands and retailers are compelled to invest heavily in anti-counterfeit packaging, authentication systems, and consumer education. While these measures are essential, they also inflate operational costs and squeeze profit margins. Retailers, aiming to mitigate risks, might even choose to delist lesser-known or niche products, curtailing shelf space for potential innovations. The pervasive issue of counterfeit products not only sows doubt in purchase decisions but also escalates brand protection expenditures. This dynamic curtails the market's capacity to introduce new products or premium offerings, stunting sustainable growth in the shampoo sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Standard Dominance Amid Natural Acceleration

Standard shampoos, with a commanding 91.10% share, dominate the global hair shampoo market, due to their widespread consumer familiarity and established distribution networks. Brands such as Head & Shoulders, Dove, and Pantene leverage strong brand recognition and consistent product performance to maintain their leadership on retail shelves worldwide. These brands, benefiting from economies of scale, enjoy extensive availability across supermarkets, hypermarkets, and e-commerce platforms, making them the go-to choice for consumers seeking reliable, everyday hair care solutions.

Natural, organic, and medicated shampoos are emerging as the fastest-growing segment, with a notable growth rate of approximately 6.92% CAGR. This surge reflects a shift in consumer preferences towards ingredient transparency, wellness-focused formulations, and pronounced hair health benefits. Brands like Sienna Naturals, Prose, Ceremonia, Ursa Major, and Attitude are carving a niche by offering botanical, organic, and sustainably sourced ingredients, appealing to eco-conscious and ingredient-savvy consumers. Furthermore, medicated variants, such as targeted dandruff or hair-fall solutions, are witnessing heightened acceptance, bolstered by mainstream distribution through retail and e-commerce channels. This accessibility not only diminishes the premium barrier but also propels the overall market expansion in the natural and organic segment.

By Hair Concern: Specific Purpose Solutions Drive Growth

In 2025, specific-purpose shampoos seized a commanding 55.10% share of the global hair shampoo market, projected to grow at a steady 4.83% CAGR through 2031. This trend underscores a growing consumer preference for products tailored to individual hair concerns. Leading the retail channels, anti-dandruff and scalp-health products, such as Head & Shoulders Clinical Strength and Neutrogena T/Gel, boast clinically validated efficacy. Meanwhile, volumizing and thickening shampoos, like Living Proof Full Shampoo and Olaplex Volume Shampoo, focus on enhancing root-level hair density and manageability. Strengthening and repair-centric products, such as Prose Repair Shampoo and Ceremonia Hair Repair, cater to consumers prioritizing preventive haircare. Furthermore, natural and plant-based alternatives, including Sienna Naturals Anti-Dandruff and Ursa Major Fortifying Shampoo, are carving a niche by merging performance with eco-friendly formulations.

General and multi-purpose shampoos, designed for family convenience, continue to thrive due to their everyday usability and widespread retail presence. Brands like Dove Daily Moisture and Pantene Daily Care cater to consumers desiring dependable, all-in-one solutions, even without specialized claims. While these familiar products enjoy broad accessibility, they're increasingly challenged by specific-purpose variants that, despite their premium pricing, entice consumers to seek targeted solutions for issues like dandruff, hair fall, and repair. Additionally, as consumer awareness evolves, emerging concerns such as pollution protection and blue-light defense are being addressed by brands like Attitude Protect & Repair Shampoo, gradually broadening the spectrum of multi-purpose offerings.

By Category: Mass Segment Stability Amid Luxury Acceleration

In 2025, the mass category commands the global hair shampoo market with a dominant 64.10% share, underscoring its widespread consumer appeal and solid retail foothold. Leading brands like Head & Shoulders, Dove, Pantene, and Sunsilk are making waves in supermarkets, hypermarkets, and e-commerce. Their success hinges on operational efficiency, clear value communication, and formulations catering to families. To bolster their market share, mass brands are rolling out merchandising innovations, loyalty programs, and expanding private labels, ensuring their products remain both accessible and trustworthy for daily haircare.

On the other hand, the luxury/premium segment is on an upward trajectory, boasting a growth rate of about 4.93% CAGR projected through 2031. This surge is driven by consumers' growing preference for high-performance, ingredient-centric formulations that promise visible results and enhanced hair health. Brands such as Kérastase, Olaplex, Oribe, and Living Proof are tapping into this trend, utilizing advanced active ingredients, unique packaging experiences, and endorsements from celebrities to captivate a younger, affluent audience. The online realm is pivotal, with social media initiatives and collaborations with influencers significantly boosting brand visibility and encouraging trials.

By Distribution Channel: Digital Transformation Accelerates

Supermarkets and hypermarkets command a dominant 35.20% share of the global hair shampoo market, capitalizing on consumer convenience, habitual purchases, and spur-of-the-moment buying. Leading brands such as Head & Shoulders, Dove, and Pantene maintain their retail prominence, due to their established visibility and strong ties with retailers. These retail channels enjoy advantages like geographic accessibility, promotional bundling, and seamless integration with digital discovery tools, ensuring they consistently reach a broad consumer base.

Online retail emerges as the fastest-growing channel, boasting a 6.38% CAGR, as the digital realm reshapes haircare shopping habits. Prestige and premium brands, including Olaplex, Living Proof, and Kérastase, are witnessing a surge in online sales, bolstered by platforms like TikTok Shop that facilitate direct engagement between creators and consumers. Specialty beauty retailers and direct-to-consumer brands, such as Prose and Sienna Naturals, stand out by offering personalized services and exclusive products. This shifting landscape is altering competitive dynamics, with digitally adept brands harnessing online marketing, while traditional retailers pivot to omnichannel strategies, striving for visibility and growth in both mainstream and niche markets.

Geography Analysis

Asia-Pacific dominates the global hair shampoo market, commanding a 47.10% share and expanding at a 5.52% CAGR. A robust retail infrastructure, heightened consumer demand, and a swift embrace of premium and specialty products fuel this growth. Countries such as China and India underscore this regional supremacy. With vast supermarket chains, contemporary trade formats, and a booming e-commerce landscape, brands are effectively reaching diverse consumer segments. In India, brands like Sunsilk, Dove, and Patanjali adeptly navigate both offline and online avenues to serve both mainstream and niche audiences. Meanwhile, in China, luxury haircare brands like L’Oréal Professionnel and Kérastase are gaining momentum, due to digital campaigns aimed at the younger, tech-savvy demographic.

North America and Europe are witnessing growth, driven by innovation, a push for premium products, and shifting consumer preferences. In North America, regulatory shifts, exemplified by initiatives like MoCRA, are steering the market. These changes favor established manufacturers with the resources for product development, especially as consumers demand transparency, sustainability, and high-performance formulations. This trend has amplified the appetite for luxury and specialized shampoos. Meanwhile, Europe's growth is underpinned by stringent regulations, a commitment to sustainability, and a heightened consumer focus on ethical sourcing. This environment has allowed premium and artisanal brands to flourish, especially through specialty beauty retailers and online platforms.

South America and the Middle East and Africa are witnessing gradual growth, influenced by local regulations and emerging retail landscapes. In Brazil, while economic improvements and heightened brand awareness present opportunities for both global and local players, challenges loom in the form of political instability, currency volatility, and counterfeit products. These regions are leaning heavily on modern retail growth and e-commerce, though traditional channels still play a pivotal role in rural and price-sensitive markets, leading to more tempered growth compared to their more established counterparts.

Competitive Landscape

Global players in the hair shampoo market are moderately consolidated, are honing their marketing strategies to resonate with a wide array of consumers. Major brands, including Procter & Gamble, Unilever, and L'Oréal, are harnessing the power of influencer partnerships, social media outreach, and celebrity endorsements, particularly targeting the engagement of Gen Z and millennial demographics. Meanwhile, brands rooted in the digital realm, like Prose and Sienna Naturals, are fostering brand loyalty through tailored messaging and community-centric content. Premium brands such as Kérastase and Olaplex are drawing in aspirational consumers by spotlighting their product heritage, luxury branding, and immersive marketing experiences. To boost shelf visibility and encourage consumer trials, brands are increasingly turning to strategies like hero-product promotions, seasonal launches, and curated bundles.

Embracing technology is becoming a pivotal factor in distinguishing market players. Brands are channeling investments into AI-driven platforms that curate haircare routines tailored to individual profiles and concerns. Furthermore, digital commerce enhancements are streamlining online product discovery, checkout processes, and customer retention efforts. Brands such as Living Proof and Prose are leveraging sophisticated analytics to gauge influencer returns, monitor social commerce metrics, and refine their digital advertising strategies. Highlighting the significance of intellectual property in this competitive landscape, innovations like Kao Corporation’s patented foam-type hair color formulations underscore its role as a shield for market differentiation.

Strategic alliances, mergers, and geographical expansions increasingly influence market dynamics. Henkel's strategic moves, including the acquisition of Vidal Sassoon's Greater China operations and Shiseido's Asia-Pacific professional hair division, underscore a trend towards consolidation for enhanced operational efficiency and deeper market penetration. Unilever's takeover of the eco-conscious brand Wild, known for its refillable products, signals a commitment to circular economy principles and sustainability. While emerging brands forge alliances with Asian ingredient suppliers for innovative and cost-effective formulations, established entities are bolstering their defenses by investing in regulatory compliance and quality assurance systems.

Shampoo Industry Leaders

Unilever PLC

The Procter & Gamble Company

Henkel AG & Co. KGaA

Kao Corporation

L'Oréal S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Meera launched Rice Kanji Shampoo, tapping into heritage rice-water rituals via CavinKare’s flagship brand.

- November 2024: CeraVe introduced Anti-Dandruff and Gentle Hydrating ranges using 1% pyrithione zinc plus the brand’s signature ceramides.

- July 2024: Aeterna debuted its made-in-Italy natural haircare line online and at Spacagna Italian Hair Design in Miami.

Global Shampoo Market Report Scope

Shampoo is a hair care product, typically in the form of a viscous liquid, that is used for cleaning hair. Less commonly, shampoo is available in solid bar format. The shampoo is used by applying it to wet hair, massaging the product into the scalp, and then rinsing it out.

The shampoo market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into 2-in-1 shampoo, anti-dandruff shampoo, kids shampoo, medicated shampoo, standard shampoo, and other product types. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, drug stores and pharmacies, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Standard Shampoo |

| Natural/Organic/Medicated Shampoo |

By HairConcern

| General/Multi-purpose | |

| Specific Purpose | Anti-Dandruff and Scalp Health |

| Volumizing and Thickening | |

| Strengthening and Repair | |

| Hair Regrowth and Hair Repair | |

| Others |

By Category

| Mass |

| Luxury/Premium |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Standard Shampoo | |

| Natural/Organic/Medicated Shampoo | ||

| By HairConcern | General/Multi-purpose | |

| Specific Purpose | Anti-Dandruff and Scalp Health | |

| Volumizing and Thickening | ||

| Strengthening and Repair | ||

| Hair Regrowth and Hair Repair | ||

| Others | ||

| By Category | Mass | |

| Luxury/Premium | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What was the shampoo market size leader by geography in 2025?

Asia-Pacific led with 47.10% share, driven by higher disposable income and strong digital-commerce adoption.

Which product-type segment is growing fastest through 2031?

Natural, organic, and medicated shampoos are projected to register the quickest expansion at a 6.92% CAGR.

How are distribution channels shifting for shampoo purchases?

Online retail is growing at a 6.38% CAGR as social commerce and direct-to-consumer models gain traction, while supermarkets and hypermarkets remain the largest channel with a 35.20% share in 2025.

Why are specific-purpose shampoos gaining ground?

Consumers increasingly seek targeted benefits-such as anti-dandruff or damage repair-resulting in a 55.10% share and a 4.83% CAGR outlook for this segment.

Page last updated on: