Dry Shampoo Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

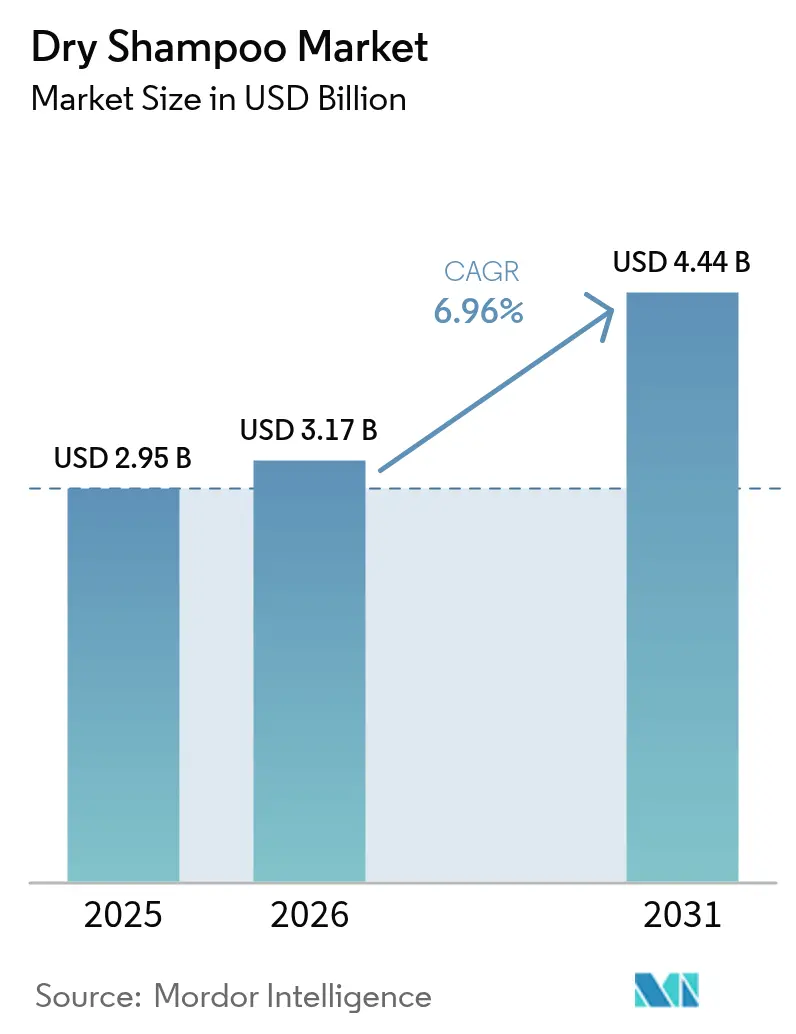

| Market Size (2026) | USD 3.17 Billion |

| Market Size (2031) | USD 4.44 Billion |

| Growth Rate (2026 - 2031) | 6.96% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

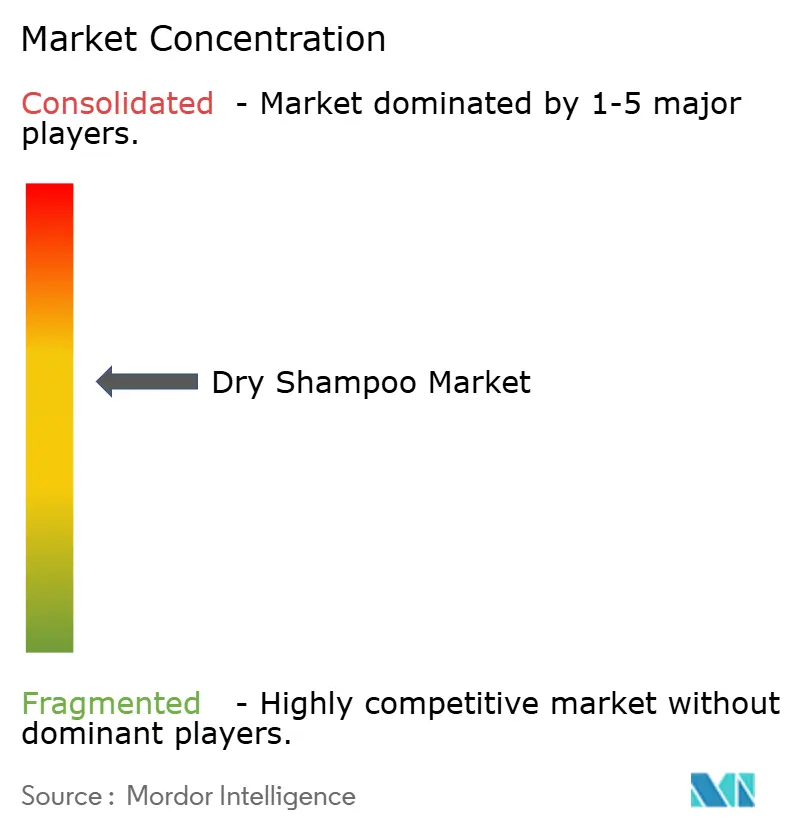

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dry Shampoo Market Analysis by Mordor Intelligence

The dry shampoo market size is expected to grow from USD 2.95 billion in 2025 to USD 3.17 billion in 2026 and is forecast to reach USD 4.44 billion by 2031 at a 6.96% CAGR over 2026-2031. Accelerated urban lifestyles, longer intervals between traditional shampoo washes, and widening digital access in emerging economies are lifting baseline demand. Powder and lotion-to-powder formats are gaining popularity as consumers seek propellant-free options that comply with evolving VOC limits in California and the European Union[1]Source: California Air Resources Board, “Consumer Products Program,” ww2.arb.ca.gov. Ingredient transparency requirements under EU Cosmetics Regulation 1223/2009 and the United States MoCRA are favoring incumbents that can shoulder testing and recall costs, yet the same rules are squeezing out counterfeit products and raising consumer trust in official channels. Simultaneously, biotechnology is reshaping product design, with peptide-based odor-neutralizing actives enabling low-residue performance in both salon and at-home routines.

Key Report Takeaways

- By product type, spray aerosols led with 65.62% of the dry shampoo market share in 2025, while powder formats are forecast to grow at a 7.80% CAGR through 2031.

- By nature, conventional formulations captured 76.74% revenue in 2025; organic variants are poised to expand at an 8.13% CAGR to 2031.

- By price range, mass-market SKUs accounted for 62.82% sales in 2025, yet premium offerings are projected to advance at a 7.78% CAGR over the same horizon.

- By distribution channel, supermarkets and hypermarkets accounted for 37.62% of sales in 2025, whereas online retail is expected to expand fastest at an 8.12% CAGR.

- By geography, Europe accounted for 35.43% of revenue in 2025, and Asia-Pacific is anticipated to register the highest regional growth at a 7.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dry Shampoo Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient hair-care routines | +1.2% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Increasing adoption among the female workforce | +0.9% | Global, strongest in North America, Western Europe, urban India, and China | Medium term (2-4 years) |

| E-commerce channel expansion across emerging markets | +1.5% | Asia-Pacific (Vietnam, Thailand, Indonesia), Latin America (Brazil, Argentina), Middle East | Medium term (2-4 years) |

| Travel-size SKUs are boosting impulse buys in airports and in-flight retail | +0.6% | Global travel hubs: North America, Europe, the Middle East (Dubai, Doha), Asia-Pacific (Singapore, Bangkok) | Short term (≤ 2 years) |

| Salon-led colour-preservation regimens between visits | +0.8% | North America, Europe, urban Asia-Pacific (Japan, South Korea, China) | Long term (≥ 4 years) |

| Sustainability push for waterless beauty product lines | +1.1% | Europe, North America, Australia/New Zealand; spillover to urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient hair-care routines

Time-pressed professionals are turning to dry shampoos, achieving oil absorption in under 2 minutes, as a replacement for traditional wash cycles. This shift is especially evident among Gen Z consumers, the fastest-growing demographic in the U.S. haircare market, where products from the shampoo family dominate. The move is not just about convenience: dry shampoos facilitate multi-day styling, minimizing heat-tool use and water waste. This trend aligns with the "skinification" of haircare, emphasizing scalp health and hair vitality with a dermatological approach. Brands are innovating, introducing features like sweat-activated fragrances. For instance, Batiste's March 2024 Touch-Activated Dry Shampoo releases its scent during physical activity, elevating dry shampoo from a mere stopgap to an essential accessory for an active lifestyle. The U.S. Bureau of Labor Statistics forecasts a 33% growth in personal care services employment from 2020 to 2030, outpacing total employment growth by five times[2]Source: Bureau of Labor Statistics, “Occupational Outlook Handbook: Barbers, Hairstylists, and Cosmetologists,” bls.gov. This underscores a robust demand for products that can replicate salon results at home. Given the interplay of time constraints, a focus on scalp health, and the desire for at-home styling, dry shampoo emerges not just as a fleeting trend but as a significant growth category in the market.

Increasing adoption among female workforce

In OECD economies, female labor force participation rates have stabilized above 67.1% in 2024. This trend has led to a rise in dual-income households, where the efficiency of grooming routines plays a crucial role in managing discretionary time. As urban working women shift towards 3-to-4-day hair wash cycles, they increasingly rely on dry shampoos for non-wash days. This practice is not just a personal choice; it's backed by professional hairstylists who advocate for less frequent washing to maintain natural scalp oils and the integrity of color-treated hair. Interestingly, men are now entering the grooming services market at an accelerating pace. The Bureau of Labor Statistics (BLS) highlights a notable trend: men are adopting personal care routines that were once predominantly female. This shift suggests that the market for dry shampoos could broaden, reaching beyond its traditional female audience. Brands are taking note. They're rolling out fragrance-free and residue-free formulations to cater to this evolving demographic. For instance, Redken's Invisible Dry Shampoo, enriched with Vitamin E and tailored for dark hair, is positioned for 1-to-2-day refresh cycles. Such products are particularly appealing in professional settings, where a subtle touch is essential.

E-commerce channel expansion across emerging markets

Online retail is projected to grow at an 8.12% CAGR through 2031, driven by the global rise of digital commerce in beauty. Vietnam leads Southeast Asia's online beauty sales, surpassing the combined revenues of Indonesia, Malaysia, Thailand, Singapore, and the Philippines. In India, omnichannel beauty retailers like Nykaa (187 stores, 74% online sales), Tira Beauty (triple-digit store expansion), and Sephora (26 stores, doubling in 3-4 years) are using augmented reality and influencer-led live commerce to attract first-time buyers. In Brazil, the world's third-largest haircare market, advertising spend rose from BRL 44.9 billion in 2022 to BRL 60.5 billion in 2024, with e-commerce enabling direct-to-consumer brands like Lola From Rio to bypass traditional retail. The closure of the de minimis customs exemption under MoCRA has reduced counterfeit inflows, with U.S. Customs reporting 31% of intercepted FY2023 counterfeits were beauty items. Legitimate brands are now investing in blockchain-verified supply chains and certified brand stores. Rising digital access in emerging markets and stricter anti-counterfeit measures in developed ones position e-commerce as both a growth driver and a quality-control battleground.

Sustainability push for waterless beauty product lines

Dry shampoos are advancing water conservation goals with biodegradable polymers, refillable packaging, and zero-waste delivery systems, appealing to eco-conscious consumers in Europe and North America. In 2021, the EU cosmetics sector invested EUR 2 billion in research and development, a 30% increase since 2013, driven by sustainability initiatives like microplastics restrictions under REACH and PCR content mandates, according to the European Commission. Redken, a L'Oréal brand, uses at least 96% recycled plastic in its color portfolio bottles and conducts biodegradability testing per OECD 301 standards. Green Seal's GS-50 certification bans aerosols, caps VOC content at 2-5%, and prohibits PFAS, parabens, and phthalates, enabling compliance for powder and lotion-to-powder dry shampoos. Unilever's 2024 acquisition of K18 underscores waterless innovation's value, with K18's AirWash dry shampoo using peptide-based OdorBind technology to neutralize odors and reduce allergens. Thailand, producing 85% of its cosmetics locally and expecting 10-13% annual export growth, is emerging as a hub for "T-Beauty" clean formulations, blending botanicals with wellness and supporting waterless dry shampoo manufacturing for ASEAN and Middle Eastern markets, per the International Trade Administration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aerosol propellant and talc-related health concerns | -0.9% | Global, with heightened regulatory scrutiny in the EU, California, and select U.S. states | Short term (≤ 2 years) |

| Counterfeit/low-quality products eroding brand trust | -0.7% | Global e-commerce channels, concentrated in the UK, EU, U.S., and cross-border shipments from China/Hong Kong | Medium term (2-4 years) |

| Starch-based feedstock price volatility in the supply chain | -0.5% | Global, with exposure to agricultural commodity markets in Thailand, Vietnam, and India (tapioca/rice starch) | Medium term (2-4 years) |

| VOC-emission caps limiting aerosol formulation in select U.S. states | -0.4% | California, select Northeast U.S. states; potential spillover to Canada and the EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aerosol propellant and talc-related health concerns

Formulators are abandoning legacy ingredients and delivery systems due to inhalation risks from aerosol delivery and talc contamination. This shift is compressing margins and extending the time-to-market for reformulated SKUs. In its 2024 opinion, the European Commission's Scientific Committee on Consumer Safety (SCCS) deemed titanium dioxide (TiO2) unsafe in hair aerosol sprays at the commonly used 25% concentration[3]Source: Scientific Committee on Consumer Safety, “Opinion on Titanium Dioxide (Nano),” ec.europa.eu. They set maximum safe levels at 1.4% for consumers and 1.11% for professional hairdressers, citing inhalation risks of carcinogenicity. Concurrently, the U.S. FDA, responding to asbestos contamination findings, has ramped up talc testing. With MoCRA mandating standardized testing methods for cosmetic-grade talc, the FDA's 2024 withdrawal of a proposed rule for further reconsideration has left manufacturers in a regulatory quandary. Addressing these dual health concerns, brands like Briogeo introduced the Style + Treat Dry Shampoo Puff in December 2024. This product is both talc-free and aerosol-free, utilizing a powder-puff applicator while ensuring oil-absorption efficacy. The International Agency for Research on Cancer (IARC) has identified talc, TiO2, and carbon black as inhalation carcinogens. This classification poses a regulatory challenge, especially for aerosol-format dry shampoos, pushing the market towards powder, paste, and lotion-to-powder alternatives.

Counterfeit/low-quality products eroding brand trust

Counterfeit dry shampoos sold through unregulated online marketplaces have introduced toxic contaminants into the supply chain, eroding consumer trust and forcing brands to invest in authentication technologies and legal measures. Testing by the UK Intellectual Property Office found contaminants like beryllium oxide, arsenic, lead, and mercury in counterfeit cosmetics, while consumer group Which? reported that 67% of cosmetics purchased online were likely counterfeit. The EUIPO estimates counterfeiting costs the EU cosmetics sector EUR 3 billion annually, or 4.8% of total sales, with 24% of UK women knowingly purchasing counterfeit products due to price sensitivity. Customs and Border Protection noted beauty and personal care items made up 31% of intercepted counterfeit goods in FY2023, prompting the FDA to close the de minimis customs exemption for shipments under USD 800 from China and Hong Kong. This policy will increase inspection rates and import costs but reduce counterfeit penetration. The FDA's MoCRA initiative expanded its database from 35,102 to 589,762 registered products, providing a compliance baseline for legitimate manufacturers, though enforcement remains uneven. Brands are partnering with certified e-commerce platforms and deploying QR-code traceability systems, which add 3-5% to landed costs but mitigate reputational damage from counterfeits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Aerosol Dominance Meets Powder Disruption

In 2025, spray aerosols held 65.62% of the market, reflecting consumer preference for even product distribution. However, powder formats are projected to grow at a 7.80% CAGR through 2031, driven by health and environmental concerns. Searches for non-aerosol dry shampoos rose 37.3% year-over-year, with tools like powder puffs and brushes gaining traction for portability and reduced inhalation risks. In January 2025, Kitsch launched a Pump-Powder Dry Shampoo free of talc and aerosols, while Ceremonia introduced a Dry Shampoo with Arrowroot and natural starch alternatives. R+Co Bleu’s Vapor Lotion to Powder Dry Shampoo combines cream precision with powder efficacy, addressing challenges of loose-powder formats. The "Other Product Type" segment, including foams and pastes, is niche but growing in salon channels where stylists prefer tactile control.

Regulatory changes are accelerating this shift. The SCCS capped titanium dioxide in aerosols at 1.4% for consumers and 1.11% for hairdressers due to carcinogenicity concerns. California and Northeast U.S. states enforce VOC limits below 10%, constraining propellant formulations. Procter & Gamble has patented low-VOC propellant blends to maintain spray performance while complying with regulations. Powder formats benefit from Green Seal GS-50 certification, which prohibits aerosols, caps VOCs at 2-5%, and bans PFAS and parabens, appealing to eco-conscious consumers. The format shift reflects segmentation: aerosols dominate mass retail and travel for convenience, while powders capture premium and clean-beauty niches where ingredient transparency commands higher prices.

By Nature: Conventional Formulations Under Organic Pressure

In 2025, conventional dry shampoos held 76.74% market share, driven by brands like Batiste, TRESemmé, and Pantene leveraging synthetic fragrances, silicone-based agents, and petroleum-derived propellants. However, organic dry shampoos are projected to grow at 8.13% CAGR through 2031, fueled by clean-beauty certifications and ingredient transparency. ECOCERT's COSMOS Organic standard mandates 99% natural-origin ingredients, 95% organic plant ingredients, and 20% organic product weight for leave-on cosmetics (10% for rinse-off), banning synthetic fragrances, parabens, and most silicones. EWG Verified certification prohibits aerosols, requires full fragrance disclosure, and mandates allergenicity testing, creating high compliance barriers for clean-beauty brands.

Consumer skepticism about premium efficacy drives organic growth, as many doubt premium products outperform mass alternatives. To justify price premiums, organic brands emphasize benefits like scalp health, reduced buildup, and allergen avoidance. Ceremonia's arrowroot-based dry shampoo targets Latinx consumers with plant-derived formulations, while K18, acquired by Unilever in Q1 2024, offers a biotech peptide platform that neutralizes odors. Thailand's "T-Beauty" movement, focusing on botanical ingredients and clean-label claims, positions the country as a manufacturing hub for organic dry shampoos targeting ASEAN and Middle Eastern markets, where halal certification aligns with cultural preferences. Conventional formulations will dominate the mass market due to affordability, but organic variants are carving a premium niche with 30-50% price premiums justified by ingredient provenance and certification rigor.

By Price Range: Mass Accessibility Versus Premium Differentiation

In 2025, mass-market dry shampoos accounted for 62.82% of the revenue, reflecting their affordability and the pricing power of multinational CPG brands distributing through supermarkets, hypermarkets, and drugstores. Premium dry shampoos are projected to grow at a 7.78% CAGR through 2031, driven by salon professionals, luxury beauty retailers like Sephora, Ulta, and Nykaa, and direct-to-consumer brands emphasizing scalp health, biotech actives, and sustainable packaging. Many consumers view haircare as affordable compared to other beauty segments, with travel-sized unit sales surging in 2025. Premium brands are leveraging smaller SKUs to lower entry barriers while maintaining per-ounce premiums.

India's luxury beauty market, where haircare comprises 10% of the segment, highlights premium opportunities. Retailers like Nykaa (187 stores by FY24, 74% online sales), Tira Beauty (expanding stores), and Sephora (doubling 26 stores in 3-4 years) are using augmented reality tools and in-store consultants to attract first-time premium haircare buyers. L'Oréal's acquisition of Color Wow in July 2025 underscores the value of salon-exclusive channels commanding 2-3x price premiums over mass alternatives. Mass brands are defending share by introducing "masstige" tiers with premium claims like biotin and keratin, sold at drugstores, and partnering with retailers like Target and Walmart to offer 20-30% discounts. Price segmentation focuses on usage occasions: mass SKUs for daily refresh, premium SKUs for color-treated hair or events, and travel minis for impulse purchases in airports and hotels.

By Distribution Channel: Omnichannel Convergence and E-Commerce Acceleration

In 2025, supermarkets and hypermarkets captured 37.62% of dry shampoo sales, leveraging high foot traffic, impulse-buy endcap placements, and promotions like buy-2-get-1-free. Online retail stores are projected to grow at an 8.12% CAGR through 2031, driven by marketplace expansions, social commerce (TikTok Shop, Instagram Shops), and subscription models ensuring repeat purchases. Singapore's beauty and personal care market, valued at USD 1,244 million in 2024 with 1% annual growth, highlights a digital-savvy population, with 97% of those aged 15+ as online consumers. E-commerce sales are expected to reach USD 14 billion by 2027, indicating strong growth potential in online channels, as noted by the International Trade Administration.

Health and beauty stores, along with specialty retailers like Ulta, Sephora, Watsons, and Sally Beauty, serve as key discovery hubs where consultants recommend products tailored to hair types. For example, Sally Beauty markets dry shampoo as a solution to "keep hair fresh between washes," grouping it with styling products to encourage basket expansion. Convenience stores and "Other Distribution Channels" (airport duty-free, hotel amenities, gyms) drive impulse purchases with travel-size SKUs. In 2025, U.S. travel boosted mini-size beauty sales, with airport retail and inflight catalogs offering high-margin channels where consumers pay 20-40% premiums for convenience. The closure of the de minimis customs exemption for China and Hong Kong shipments under MoCRA has reduced counterfeit inflows, prompting brands to prioritize certified marketplace stores like LazMall, Shopee Mall, and Nykaa Luxe, as noted by the U.S. Government Accountability Office. Omnichannel strategies, combining in-store discovery, online replenishment, and social commerce, are now essential. Brands are investing in CRM systems to send repurchase reminders and personalized messages, reducing repurchase cycles by up to 25%.

Geography Analysis

Europe accounted for 35.43% of the dry shampoo market share in 2025, driven by well-established grooming habits and strict recycling regulations that encourage the use of eco-friendly packaging. The European Union has implemented rules that promote the adoption of low-Volatile Organic Compounds (VOC) sprays and recyclable materials like aluminum cans, making these products more attractive to environmentally conscious consumers. Premium organic dry shampoos are becoming increasingly popular, as consumers in the region are willing to spend more on products that are both effective and sustainable. Retailers are dedicating more shelf space to these high-end options, reflecting the growing demand for eco-friendly and health-focused products in Europe.

The Asia-Pacific region is expected to grow at a CAGR of 7.88% through 2031, driven by rising disposable incomes, urbanization, and water scarcity issues in countries like India, China, and Southeast Asia. These challenges are encouraging the adoption of water-saving personal care products, including dry shampoos. In India, local brands are leveraging Ayurvedic formulations to attract consumers, while Korean companies are introducing innovative scalp-soothing powders designed for humid climates. The growing awareness of hygiene and convenience among urban populations is further boosting the demand for dry shampoos in this region, making it a key area for market growth. The increasing influence of social media and online platforms is helping to raise awareness about these products.

North America is experiencing steady growth in the dry shampoo market, supported by busy lifestyles and a strong salon culture that promotes the use of dry shampoos as part of hairstyling routines. Retailers are focusing on expanding their offerings of talc-free and clean-label products to cater to the growing demand for healthier and safer options. Meanwhile, South America and the Middle East and Africa are emerging as potential markets, with demand increasing due to the expansion of e-commerce platforms. These digital channels are improving product accessibility, while localized manufacturing efforts are helping to reduce costs, making dry shampoos more affordable for consumers in these regions.

Competitive Landscape

The competition in the dry shampoo market is moderately concentrated, with major global companies like L’Oréal SA, Procter & Gamble, Unilever plc, and Kao Corporation maintaining their leadership through their large-scale operations, strong research and development capabilities, and multichannel strategies. For instance, L’Oréal’s acquisition of Color Wow in 2025 highlights its focus on expanding into high-growth niches, such as texture-specific hair care solutions. These companies continue to strengthen their market positions by investing in innovative products and targeting emerging trends to meet evolving consumer demands.

Smaller direct-to-consumer (DTC) brands are gaining traction by targeting specific customer needs, such as products for curly hair, post-workout refreshers, or men’s grooming. These brands often use social media influencers to build trust and appeal to niche audiences. Many also emphasize sustainability by offering refillable packaging options and providing transparency through QR-code ingredient tracking. Platforms like TikTok are being used to educate consumers through tutorials, further enhancing brand visibility and trust. Innovations in aerosol formulations and packaging are also becoming critical as companies adapt to stricter regulations on volatile organic compounds (VOCs).

Companies are exploring new ways to expand their market reach, such as co-branding with airlines, fitness centers, and ride-sharing services to distribute dry shampoo samples in everyday settings. This strategy helps introduce the product to potential customers in high-use scenarios. On the technical front, advancements like starch-silica hybrids and encapsulated fragrance beads are being developed to improve product performance, offering a fresher feel without leaving residue. These innovations highlight the ongoing competition among brands to deliver superior quality and meet consumer expectations.

Dry Shampoo Industry Leaders

Unilever plc

Procter & Gamble

L'Oréal S.A.

Kao Corporation

Church & Dwight Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: K18 Biomimetic Hairscience launched AirWash, a dry shampoo specifically designed for individuals with active and busy lifestyles. The product introduction was backed by Olympic gymnast Simone Biles, adding credibility and appeal to the campaign.

- June 2025: L’Oréal finalized the acquisition of Color Wow, incorporating its specialized styling technology into L’Oréal’s premium dry shampoo portfolio. This strategic move aimed to strengthen L’Oréal’s position in the haircare market.

- January 2025: Kitsch launched a Pump-Powder Dry Shampoo that eliminates both talc and aerosol propellants, using a pump dispenser to address health concerns related to inhalation exposure and VOC emissions. The product targets clean-beauty consumers seeking non-aerosol alternatives and reflects the 37.3% year-over-year increase in searches for non-aerosol dry shampoos.

Global Dry Shampoo Market Report Scope

Dry shampoo is a hair care product designed to absorb excess oil, dirt, and sweat from your scalp and hair without using water. The dry shampoo market is segmented by product type, nature, price range, distribution channel, and geography. By product type, the market is segmented into spray, powder, and other product types. By Nature, the market is segmented into conventional and organic. By Price Range, the market is segmented into mass and Premium. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, health and beauty stores, online retail stores, and other distribution channels. By Geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. Market forecasts are provided in terms of value (USD) and volume (tons).

| Spray |

| Powder |

| Other Product Type |

| Conventional |

| Organic |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Spray | |

| Powder | ||

| Other Product Type | ||

| Nature | Conventional | |

| Organic | ||

| Price Range | Mass | |

| Premium | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the dry shampoo market be by 2031?

The dry shampoo market is forecast to reach USD 4.44 billion by 2031, expanding at a 6.96% CAGR from 2026.

Which product type leads sales today?

Spray aerosols currently hold 65.62% revenue share, although powder formats are the fastest-growing segment.

Why is Asia-Pacific the fastest-growing region?

Rising disposable incomes, mobile commerce adoption, and strong local manufacturing capacity in Southeast Asia and India are driving a projected regional CAGR of 7.88%.

What regulations affect aerosol dry shampoo?

California enforces sub-10% VOC limits, and the EU caps titanium dioxide content at 1.4% for consumer products, prompting reformulation of aerosol lines.

How are companies combating counterfeit products online?

Brands are implementing QR-code serialization, partnering with certified marketplace stores, and leveraging expanded FDA product-listing databases under MoCRA.

Is organic dry shampoo gaining traction?

Yes, organic variants are projected to grow at 8.13% CAGR as ECOCERT and EWG certifications help consumers identify talc-free, propellant-free options.

Page last updated on: