Gum Arabic Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.01 Billion |

| Market Size (2031) | USD 1.42 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

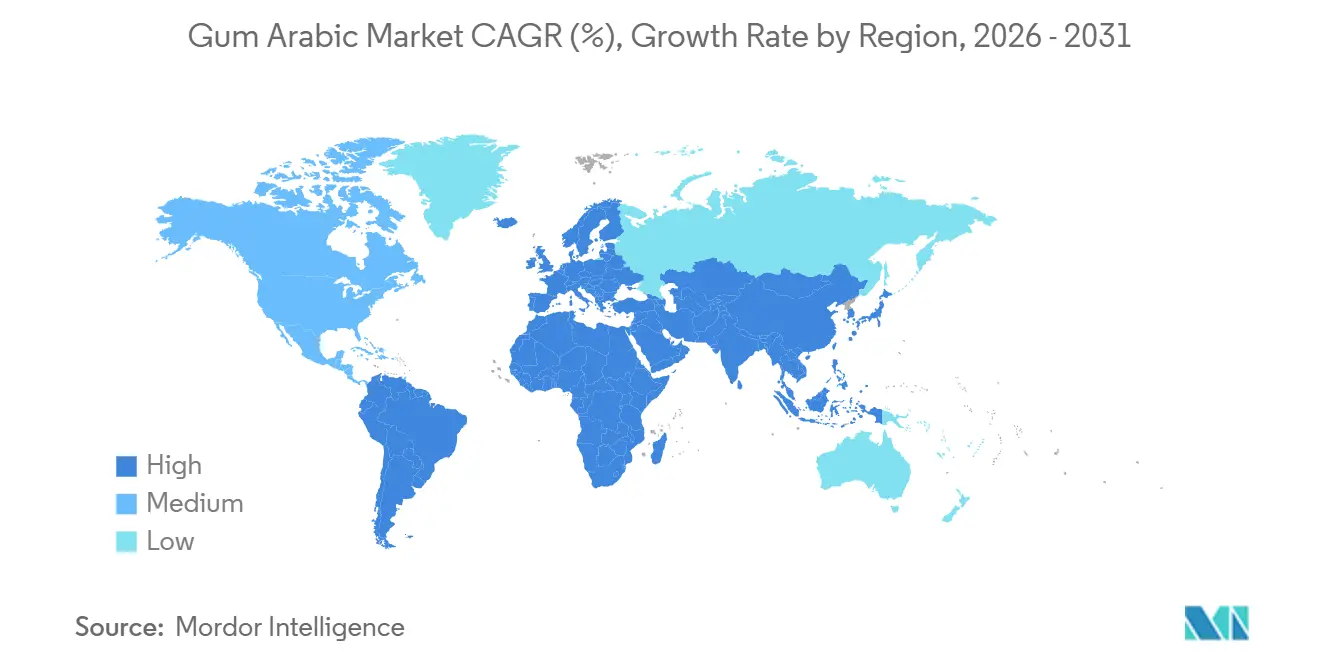

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gum Arabic Market Analysis by Mordor Intelligence

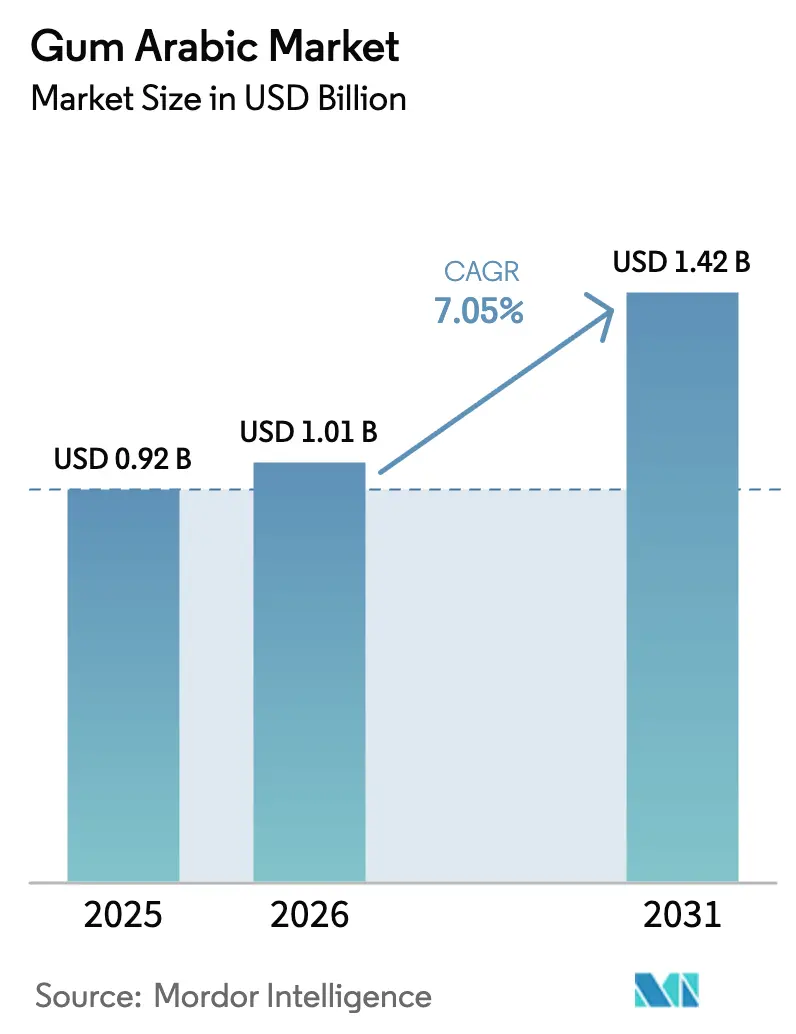

The Gum Arabic Market size was valued at USD 0.92 billion in 2025 and is estimated to grow from USD 1.01 billion in 2026 to reach USD 1.42 billion by 2031, at a CAGR of 7.05% during the forecast period (2026-2031). The steady demand for gum arabic is driven by its distinctive properties, as no synthetic alternative can replicate its low-viscosity emulsification, soluble-fiber functionality, and clean-label attributes. Beverage reformulations in North America and Europe, the adoption of microencapsulation in pharmaceuticals, and the premiumization of pet food ensure global demand remains strong despite supply disruptions tied to Sudan. While conflicts have redirected supply routes through Chad and South Sudan, smuggling and emergency logistics have prevented severe shortages. However, these disruptions have caused price increases, encouraging large processors to explore vertical integration. Margin stability is supported by pharmaceutical applications that can accommodate higher pricing and by multi-origin sourcing strategies that reduce geopolitical risks. As competition grows, suppliers are innovating by blending gum arabic with pectin or xanthan to meet the needs of price-sensitive customers without compromising cloud stability.

Key Report Takeaways

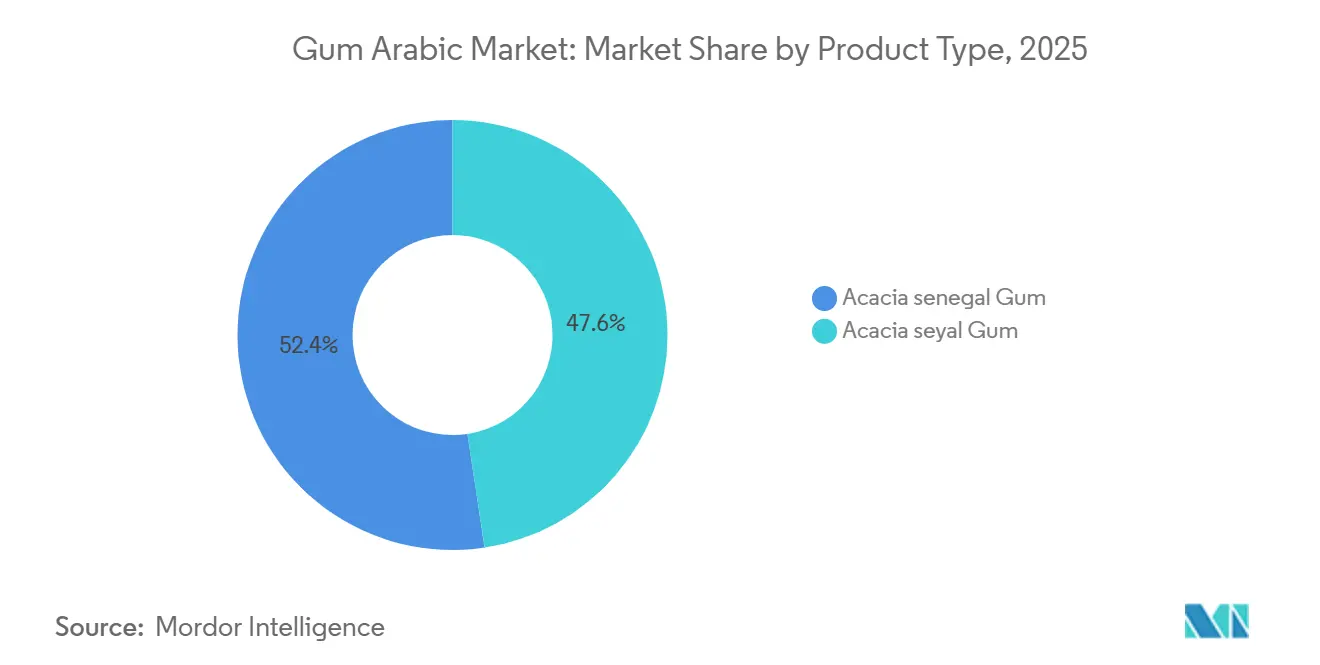

- By product type, Acacia senegal gum held 52.38% of the gum arabic market share in 2025. Acacia seyal gum is forecast to expand at a 9.32% CAGR through 2031.

- By grade, food-grade gum arabic held 58.45% of the gum arabic market share in 2025, while pharmaceutical-grade material is advancing at a 9.86% CAGR to 2031.

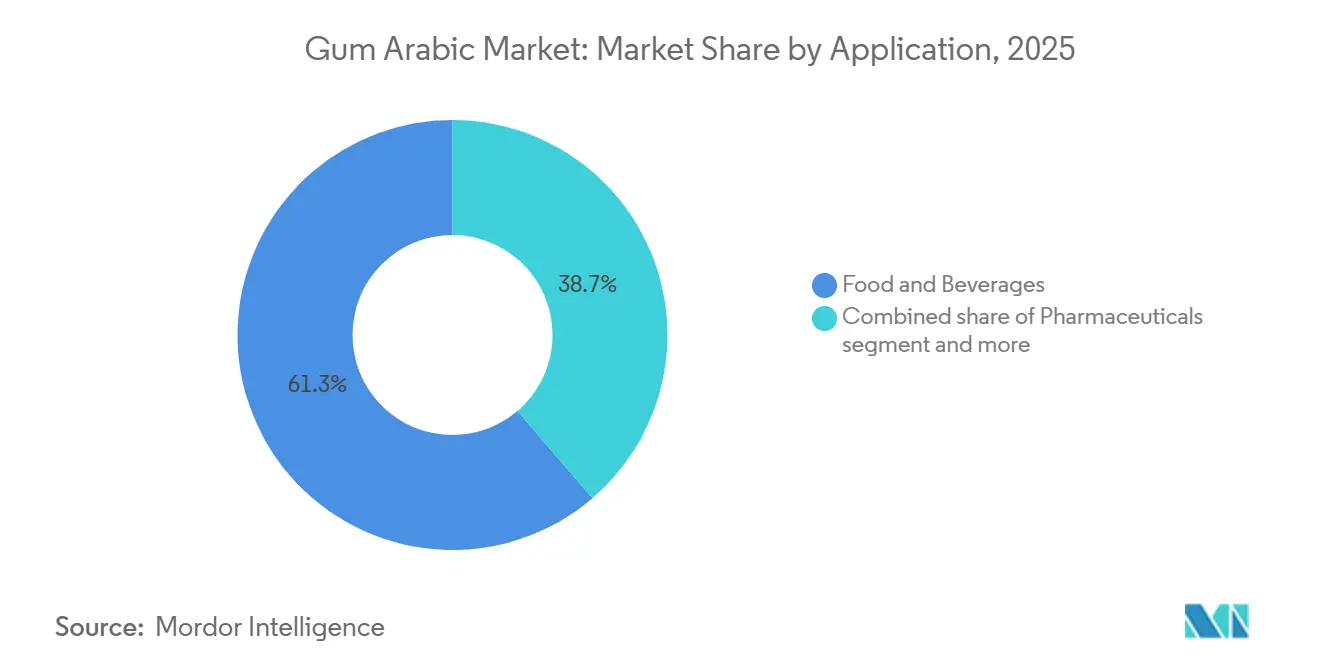

- By application, food and beverages held 61.28% of the gum arabic market share in 2025, while pharmaceuticals are projected to grow at a 9.02% CAGR to 2031.

- By geography, North America held 38.54% of the gum arabic market share in 2025, while the Middle East and Africa are set to expand at a 9.15% CAGR over 2027–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gum Arabic Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Natural and Plant-Based Ingredients | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing Consumption of Processed and Convenience Foods | +1.5% | Global, particularly Asia-Pacific and North America | Long term (≥ 4 years) |

| Inclination Towards Functional and Immune-Boosting Foods | +1.2% | North America, Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Use in Flavor and Oil Encapsulation in Pharma and Nutraceuticals | +1.0% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Multifunctionality of Gum Arabic and Diverse Applications | +0.9% | Global | Long term (≥ 4 years) |

| Expansion of Pet Food Sector Driving Demand for Safe Stabilizers | +0.7% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for natural and plant-based ingredients

As consumers increasingly shift towards clean-label products, food manufacturers are moving away from modified starches and synthetic emulsifiers, opting instead for plant-derived hydrocolloids. Reflecting the market's growth, organic food sales in the U.S. reached USD 65.4 billion in 2024, according to the Organic Trade Association[1]Source: Organic Trade Association, "U.S. Organic Industry Survey 2025", ota.com. This transition significantly benefits gum arabic, which holds a Generally Recognized as Safe (GRAS) status under FDA 21 CFR 184.1330. Importantly, gum arabic only requires labeling as "acacia gum" on ingredient panels, avoiding the need for E-number disclosure. In North America, beverage formulators are reformulating citrus soft drinks by replacing brominated vegetable oil with gum-arabic-based cloud emulsions. This change not only stabilizes flavor oils but also addresses consumer concerns about synthetic additives. This regulatory and consumer-driven trend is also accelerating in the European Union. Regulation (EC) No 1333/2008 permits gum arabic (E414) in most food categories under Good Manufacturing Practice, providing a compliance advantage over other hydrocolloids that face maximum-use-level restrictions. Studies confirming gum arabic's bifidogenic effects at a daily intake of 10 grams support its classification as a prebiotic fiber. This dual functionality, enhancing both texture and nutrition, enables it to achieve premium pricing in the growing functional-beverage market. Additionally, organic and fair-trade certifications are now critical for buyers in North America and Europe. Premium confectionery brands are increasingly incorporating Rainforest Alliance and Fair Trade USA audits into their procurement contracts, emphasizing the importance of these certifications.

Growing consumption of processed and convenience foods

Urbanization in Asia-Pacific and Latin America is expanding the market for shelf-stable bakery, dairy, and confectionery products. For example, the U.S. Census Bureau reported that the "bread and bakery product manufacturing" industry in the U.S. achieved revenues of USD 46.22 million in 2024[2]Source: U.S. Census Bureau, "Industry revenue of “bread and bakery product manufacturing", census.gov. These products rely on hydrocolloids to extend shelf life and maintain texture during distribution, with gum Arabic standing out due to its low viscosity at high concentrations, which allows stabilization without affecting mouthfeel. India's packaged-food sector, which is projected to grow at double-digit rates through 2025, is increasingly using gum arabic in dairy-based sweets and beverages to prevent syneresis and improve freeze-thaw stability, addressing the formulation challenges posed by guar gum's sensitivity to pH and temperature. In Southeast Asia, the ready-to-drink coffee and tea segment incorporates gum Arabic to stabilize milk proteins in acidic environments, a requirement that xanthan gum cannot meet without causing sedimentation. Confectionery manufacturers in the Middle East are utilizing gum arabic's film-forming properties to produce sugar-coated almonds and dragées that resist humidity, a critical feature in regions where relative humidity exceeds 70% for extended periods. In Africa, the growing convenience-food market is driving domestic consumption of gum-arabic-based products alongside increasing export volumes, creating a dual-market dynamic that supports price floors even during periods of softened global demand.

Inclination towards functional and immune-boosting foods

Gum arabic, valued for its soluble dietary fiber properties and prebiotic effects, is increasingly incorporated into functional foods and dietary supplements aimed at improving gut health and immune support. This trend has accelerated since the pandemic, as consumers seek ingredients with proven health benefits. Nutraceutical manufacturers utilize gum arabic as a carrier matrix for spray-dried probiotics. Its glass-transition temperature and moisture-barrier properties help protect live cultures during storage and enhance their viability in the gastrointestinal tract. The immune-modulating properties of gum arabic, linked to its arabinogalactan-protein structure, are being investigated in clinical trials for inflammatory bowel disease and metabolic syndrome. These studies could lead to health claims that support pharmaceutical-grade pricing in specialized nutrition markets. In North America, functional beverage brands are promoting gum-arabic-based drinks as "gut-health shots," a category priced 3 to 4 times higher than traditional soft drinks and capable of absorbing premium ingredient costs.

Use in flavor and oil encapsulation in pharma and nutraceuticals

Spray-drying with gum arabic as the wall material is widely regarded as the leading method for encapsulating volatile flavors and oxidation-prone oils. This is attributed to gum arabic's ability to maintain low viscosity at high solids content (up to 50% w/w), enabling effective atomization and rapid drying. Furthermore, its emulsification properties help form stable oil-in-water dispersions, preventing coalescence during processing. In the pharmaceutical industry, manufacturers are increasingly adopting gum-arabic-based microencapsulation. This approach effectively masks the bitter taste of active ingredients in pediatric formulations, improving patient compliance and reducing dependence on synthetic sweeteners. In North America, the omega-3 supplement market, valued at over USD 2 billion, utilizes gum arabic to encapsulate fish and algal oils. This process protects polyunsaturated fatty acids from oxidation and supports the development of powdered formats that can be incorporated into functional foods and beverages. Flavor houses are employing gum arabic to encapsulate citrus oils and spice extracts, producing free-flowing powders that simplify handling and enhance dosing accuracy in industrial bakery and snack applications. The nutraceutical industry's growing focus on vegan and allergen-free formulations is driving the adoption of gum arabic. As a plant-based alternative to gelatin and whey protein, gum arabic addresses dietary and ethical concerns prevalent among certain consumer groups.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy Reliance on Sudan and West Africa | -1.5% | Global, with acute impact on North America and Europe | Short term (≤ 2 years) |

| Presence of Lower-Cost Alternative Hydrocolloids | -1.0% | Global, particularly price-sensitive segments in Asia-Pacific | Medium term (2-4 years) |

| Inconsistent Product Quality Caused by Adulteration Practices | -0.8% | Global, with concentration in pharmaceutical-grade segments | Short term (≤ 2 years) |

| Regulatory Constraints and Compliance Challenges | -0.5% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heavy reliance on Sudan and West Africa

In 2024, Sudan's Acacia trees are expected to supply an overwhelming 80% of the global gum Arabic market, according to the European Union's delegation to Sudan[3]Source: Delegation of the European Union to the Republic of Sudan, "The EU supports the continuation of the production of gum Arabic" eeas.europa.eu. However, this heavy reliance creates a structural vulnerability, particularly amid Sudan's ongoing civil conflict. West African producers, including those in Chad, Nigeria, and Senegal, face significant limitations. They lack the capacity and quality consistency to quickly meet sudden demand surges. Additionally, their primary gum, derived from Acacia seyal (talha), commands lower prices and cannot fully replace the premium Senegal gum used in high-value applications such as beverage emulsions and pharmaceutical coatings. Climate change further exacerbates the situation, as erratic rainfall patterns in the Sahel region compress harvest periods and reduce per-tree yields, increasing supply risks even during stable periods. To mitigate these challenges, buyers are pursuing diversification strategies, such as investing in Australian Acacia plantations and researching enzymatically modified starches. However, these alternatives remain years away from achieving the scale needed to offset potential supply shortages from Sudan.

Presence of lower-cost alternative hydrocolloids

Xanthan gum, obtained through microbial fermentation of glucose, delivers excellent viscosity stability across a wide range of pH and temperatures. With a cost advantage of 20% to 30% compared to gum arabic, it is widely used in cost-sensitive applications such as salad dressings, sauces, and industrial bakery products, where thickening is prioritized over emulsification. Guar gum, extracted from legume seeds, provides similar thickening properties at a lower cost but lacks gum arabic's emulsification capabilities and exhibits poor stability in acidic conditions. This restricts its application in citrus beverages and dairy products. Modified starches, particularly those treated with octenyl succinic anhydride (OSA) to enhance emulsifying properties, are gaining popularity in beverage formulations as manufacturers aim to reduce ingredient costs. However, consumer concerns about chemically modified ingredients limit their adoption in premium and organic segments. Pectin, derived from citrus peel and apple pomace, competes with gum arabic in confectionery applications but requires specific pH and calcium conditions to gel, which reduces formulation flexibility. The availability of these alternatives imposes a pricing ceiling on gum arabic, especially in segments where functionality requirements are less stringent and buyers are willing to accept trade-offs in texture or stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Senegal Gum Anchors Premium Segments While Seyal Gum Captures Cost-Sensitive Growth

In 2025, Acacia senegal gum accounted for 52.38% of the gum arabic market share, attributed to its high arabinogalactan-protein content. Its low-viscosity emulsification effectively stabilizes beverage cloud systems at concentrations of 10% to 15% without creating a thick mouthfeel. Leading soft-drink manufacturers in North America and Europe prefer senegal gum for dispersing citrus oils in carbonated beverages, avoiding the sedimentation challenges associated with xanthan or guar alternatives. Pharmaceutical-grade senegal gum, which adheres to stringent USP and Ph. Eur. heavy-metal and microbial standards, commands a 30% to 40% premium over food-grade variants. This makes it the preferred excipient for sustained-release tablets and microencapsulation of active ingredients. The ongoing conflict in Sudan has constrained the supply of senegal gum and driven up prices, prompting buyers to explore Australian Acacia plantations. However, these plantations produce negligible commercial volumes, with production costs being 50% to 70% higher due to labor and land expenses.

Acacia seyal gum is projected to grow at a 9.32% CAGR through 2031, driven by its 20% to 30% cost advantage over senegal gum in applications where lower arabinogalactan-protein content and reduced emulsification are acceptable. Producers in West Africa, particularly Chad and Nigeria, are increasing seyal output to offset Sudanese supply shortages. Meanwhile, buyers in emerging markets are reformulating bakery stabilizers and dairy emulsions to utilize seyal's functional properties. Pet-food manufacturers, focusing on natural binding rather than emulsification, are accelerating the adoption of seyal gum, supporting demand and maintaining price stability. Additionally, blending strategies that combine senegal and seyal gums at intermediate price points are expanding seyal's market potential. This shift positions seyal gum beyond its traditional role as a low-cost alternative, strengthening the gum arabic market's ability to withstand disruptions from single-origin sources.

By Grade: Pharmaceutical Applications Command Premium Pricing and Faster Growth

In 2025, food-grade gum arabic captured 58.45% of the market share, highlighting its extensive application in confectionery glazing, beverage emulsification, bakery stabilization, and dairy products, all compliant with FDA GRAS and EU E414 standards. Beverages represent approximately 40% of food-grade gum arabic's consumption, where it stabilizes citrus oils in soft drinks, prevents ring formation in carbonated beverages, and creates cloud emulsions in ready-to-drink teas. Confectioners utilize food-grade gum arabic to prevent sugar crystallization in hard candies, regulate moisture in gummies, and add gloss to dragées and chocolate-coated nuts. They leverage its distinctive film-forming and low-hygroscopic properties, which alternative hydrocolloids cannot replicate. The bakery and dairy industries use food-grade gum arabic to extend shelf life and improve freeze-thaw stability in frozen desserts. However, price sensitivity continues to drive substitution pressure from modified starches and guar gum.

Pharmaceutical-grade gum arabic is expected to grow at a strong 9.86% CAGR through 2031, fueled by the expansion of generic drug production in India and China. In these markets, it serves as a tablet binder, coating agent, and controlled-release matrix, meeting USP and Ph. Eur. purity requirements. The microencapsulation of probiotics, omega-3 oils, and fat-soluble vitamins using pharmaceutical-grade gum arabic is experiencing double-digit growth. Nutraceutical brands, particularly those focusing on vegan and allergen-free products, increasingly prefer gum arabic as a natural alternative to gelatin and modified starches. Additionally, spray-drying with gum arabic as a protective wall material, which preserves volatile compounds and enhances bioavailability, has become a standard practice in the nutraceutical industry. This trend has established a structural demand for pharmaceutical-grade gum arabic, making it less vulnerable to price fluctuations compared to food-grade applications. Meanwhile, other grades, such as technical-grade gum arabic, are used in printing, lithography, and textile sizing. This segment remains stable but grows at a slower pace, often utilizing lower-purity siftings and dust, providing producers with a value-recovery mechanism.

By Application: Pharmaceuticals Outpace Traditional Food Uses as Microencapsulation Gains Traction

In 2025, the food and beverages sector accounted for 61.28% of the gum arabic market share. However, growth rates are decelerating as North American and European markets near saturation, with reformulation cycles now extending beyond the usual three to five years. Within this sector, the bakery and confectionery segments use gum arabic to prevent sugar crystallization, regulate moisture migration, and provide glazing. In dairy applications, it stabilizes proteins in acidic yogurt drinks and prevents syneresis in ice cream. The meat sector employs gum arabic as a binder in processed meats and as a coating for marinated products, although its usage volume is relatively small compared to beverages and confectionery. The beverages sub-segment, which includes soft drinks, energy drinks, and functional beverages, is the largest consumer of gum arabic. This demand is driven by its critical role in stabilizing citrus oils and forming cloud emulsions that resist sedimentation throughout the product's shelf life.

The pharmaceuticals segment is projected to grow at a 9.02% CAGR through 2031, increasing its market share. This growth is primarily driven by generic-drug manufacturers in India, China, and Southeast Asia, who are increasingly using gum arabic for tablet binding, film coating, and sustained-release formulations. These applications benefit from gum arabic's biocompatible excipients with low toxicity. Additionally, the microencapsulation of active pharmaceutical ingredients using spray-dried gum arabic enables taste-masked pediatric formulations and gastro-resistant delivery systems, improving patient compliance. Within the pharmaceutical sector, the nutraceutical sub-segment utilizes gum arabic to encapsulate probiotics, omega-3 oils, and botanical extracts. This not only creates easy-to-handle powdered formats but also enhances stability. Meanwhile, the animal feed and pet food sectors are experiencing mid-single-digit growth rates. This growth is driven by premium pet-food brands adopting gum arabic as a natural binder in wet-food formulations, influenced by the humanization of pet nutrition and consumer demand for clean-label ingredients. Lastly, while cosmetics and personal care applications represent a smaller volume, they remain stable and command premium pricing due to the high-purity material required for products such as pressed powders, peel-off masks, and hair-styling items.

Geography Analysis

In 2025, North America accounted for 38.54% of the gum arabic market, driven by beverage leaders such as The Coca-Cola Company and PepsiCo. These companies use gum arabic to stabilize flavor oils in citrus soft drinks and create cloud emulsions in ready-to-drink teas. The FDA's GRAS status and consumer preference for natural ingredients provide a strong foundation for demand. The United States leads North America's gum arabic consumption, sourcing primarily from Sudan and Chad, with smaller contributions from Nigeria and Senegal. While Canada and Mexico are smaller markets, they are experiencing growth in the natural and organic food sectors, where gum arabic's clean-label attributes resonate with consumer preferences. In North America's confectionery industry, gum arabic is used in sugar-coated almonds, gummies, and chocolate products. Additionally, the pharmaceutical and nutraceutical industries utilize it for microencapsulation and tablet-binding applications that require USP-grade purity.

The Middle East and Africa region is projected to grow at a 9.15% CAGR through 2031, benefiting from its proximity to gum-arabic-producing countries such as Sudan, Chad, Nigeria, and Senegal. This geographical advantage reduces logistics costs and allows for quicker responses to supply disruptions. Domestic consumption of gum-arabic-based confectioneries, beverages, and traditional foods in the Middle East is increasing alongside export volumes. This dual-market dynamic helps maintain price floors even during periods of global demand fluctuations. The UAE and Saudi Arabia are emerging as re-export hubs, importing raw gum arabic from Sudan and Chad, processing it into food-grade and pharmaceutical-grade materials, and exporting finished products to Europe and Asia. In South Africa, the food-processing industry is incorporating gum arabic into dairy products, beverages, and baked goods to meet urban consumers' demand for clean-label products. Nigeria and Egypt, both gum-arabic producers, are expanding domestic processing capabilities to capture value-addition margins that have historically benefited European and North American importers. Meanwhile, Turkey's confectionery and beverage industries are adopting gum arabic to comply with EU regulations on natural additives, positioning Turkish manufacturers to export to European markets.

In 2025, Europe held a significant share of the gum arabic market, supported by strict regulations under Regulation (EC) No 1333/2008, which favor natural additives over synthetic alternatives. This regulatory framework provides gum arabic (E414) with a competitive advantage in confectionery, beverages, and dairy applications. The United Kingdom, Germany, France, and Italy are the largest consumers in the region. Beverage manufacturers in these countries are reformulating citrus drinks to eliminate synthetic emulsifiers, while confectionery producers are using gum arabic for glazing and moisture control. Europe's organic and fair-trade segments are expanding rapidly, with buyers increasingly demanding traceability and sustainability certifications. Although these certifications increase costs, they enable premium pricing at retail. The Asia-Pacific region is experiencing above-average growth rates, driven by urbanization and rising incomes in China, India, and Southeast Asia. These trends are expanding the market for processed foods and beverages that rely on hydrocolloids for stabilization and extended shelf life. South America, led by Brazil, Argentina, and Colombia, represents a smaller but stable market. Gum arabic is used in confectionery, beverages, and dairy products in the region, but growth is limited by price sensitivity and competition from locally sourced guar gum and modified starches.

Competitive Landscape

The gum arabic market is moderately concentrated, with key players such as Nexira SAS, Agrigum International Ltd, Farbest-Tallman Foods Corporation, Kerry Group Plc, and Ingredion Incorporated (TIC Gums) controlling a significant portion of global trade. These companies rely on long-term sourcing agreements with Acacia-tapping cooperatives in Sudan, Chad, and Nigeria. In contrast, the rest of the market is fragmented, consisting of regional exporters and smallholder aggregators who often lack the resources to invest in traceability systems and quality-control infrastructure. High barriers to entry, including the need for multi-year supplier relationships in conflict-prone regions and the costs associated with ISO 9001 certifications and fair-trade audits, reduce competitive intensity. These challenges, combined with price volatility and geopolitical risks, discourage smaller entrants. Market strategies focus on vertical integration and geographic diversification. For example, Nexira has established its own sourcing network in Chad to mitigate supply disruptions in Sudan, while Ingredion blends gum arabic with pectin and xanthan to lower formulation costs for price-sensitive customers.

Opportunities are emerging in pharmaceutical-grade applications, where generic-drug manufacturers in India and China are seeking biocompatible excipients that comply with USP and Ph. Eur. specifications. Similarly, the premium pet food segment is experiencing growth, as natural binders command a 10% to 15% retail premium over synthetic alternatives. Australian Acacia plantations are also entering the market, piloting commercial-scale production of Acacia senegal gum to reduce dependence on Sudanese supplies. However, these efforts face hurdles, including lower yields compared to African standards and production costs that are 50% to 70% higher due to labor and land expenses.

Technology is becoming a key differentiator in the market. Leading suppliers are investing in spray-drying and microencapsulation technologies, enabling them to offer value-added products such as pre-dispersed gum-arabic powders and customized hydrocolloid blends. These innovations simplify formulations for food and pharmaceutical manufacturers. The rise in patent filings for modified gum-arabic derivatives, such as enzymatically treated gums with improved emulsification properties, highlights a shift toward proprietary ingredients. These products not only command premium pricing but also help suppliers avoid commoditization. Compliance with JECFA specifications and traceability standards is driving market consolidation. Larger suppliers, capable of absorbing the costs of third-party audits and blockchain-based supply-chain tracking, are gaining market share. Conversely, smaller exporters, who often lack the capital to invest in quality infrastructure, are being squeezed out.

Gum Arabic Industry Leaders

-

Nexira SAS

-

Ingredion Incorporated (TIC Gums)

-

Agrigum International Ltd

-

Farbest-Tallman Foods Corporation (Farbest Brands)

-

Kerry Group Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Ampak Co. Inc. has formed a strategic partnership with Agrigum International to expand the distribution of gum arabic across the United States. This collaboration combines Ampak’s extensive United States distribution network with Agrigum’s expertise in sustainably sourced, high-quality gum arabic and advanced formulation capabilities. The partnership aims to improve the availability of gum arabic for food, beverage, nutraceutical, and personal care manufacturers, while also driving innovation in applications and ensuring a more reliable, efficient supply chain.

- April 2024: Farbest Brands, in collaboration with Alland and Robert, has introduced Beyond Acacia, a next-generation gum acacia developed through an innovative process that yields high-density granules. This advanced form enhances dispersibility and solubility, including in cold processing conditions, while also minimizing foam and dust during production. These improvements reduce lump formation and the need for extensive blending, leading to more streamlined manufacturing and ultimately lowering energy consumption in the production of food products.

- February 2024: Alland and Robert expanded its production facility in Normandy, France, doubling its size and adding a fourth production line to increase acacia gum output by 50%, reaching approximately 30,000 metric tons annually. This EUR 11 million investment also aligns with the company’s sustainability strategy, aiming to cut greenhouse gas emissions per kilogram produced by 20% by 2025. Alongside the facility upgrade, Alland and Robert launched “Beyond Acacia,” a new high-density acacia gum granule developed over two years of research and development.

Global Gum Arabic Market Report Scope

Gum arabic is defined as an edible tree gum exudate from acacia senegal, recognized as a nondigestible polysaccharide that functions as dietary fiber. The gum arabic market is segmented by product type, grade, application, and geography. By product type, the market is segmented into acacia senegal gum and acacia seyal gum. By grade, the market is segmented into food grade, pharmaceutical grade, and others. By application, the market is segmented into food and beverages, animal feed and pet food, pharmaceuticals, cosmetics, and personal care. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD) and volume (Tons).

| Acacia senegal Gum |

| Acacia seyal Gum |

| Food Grade |

| Pharmaceutical Grade |

| Others |

| Food and Beverages | Bakery and Confectionery |

| Dairy and Dairy Products | |

| Meat Industry | |

| Beverages | |

| Others | |

| Animal Feed and Pet Food | |

| Pharmaceuticals | |

| Cosmetics and Personal Care |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Acacia senegal Gum | |

| Acacia seyal Gum | ||

| By Grade | Food Grade | |

| Pharmaceutical Grade | ||

| Others | ||

| By Application | Food and Beverages | Bakery and Confectionery |

| Dairy and Dairy Products | ||

| Meat Industry | ||

| Beverages | ||

| Others | ||

| Animal Feed and Pet Food | ||

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value by 2031?

The gum arabic market size is expected to reach USD 1.42 billion by 2031, growing at a 7.05% CAGR from 2027 to 2031.

Which product type holds the largest share?

Acacia senegal gum held 52.38% of market share in 2025, driven by its superior emulsification properties in premium beverage and confectionery applications.

Why is pharmaceutical-grade material growing faster?

Pharmaceutical-grade gum arabic is expanding at a 9.86% CAGR through 2031, fueled by generic-drug manufacturing in India and China and microencapsulation of probiotics and omega-3 oils.

What are the main supply risks?

Sudan's 70% to 80% share of global supply creates vulnerability, as ongoing conflict has disrupted logistics and lifted prices by approximately 30% year-on-year in 2024.

Page last updated on: