Jellies And Gummies Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 32.41 Billion |

| Market Size (2031) | USD 43.05 Billion |

| Growth Rate (2026 - 2031) | 5.84% CAGR |

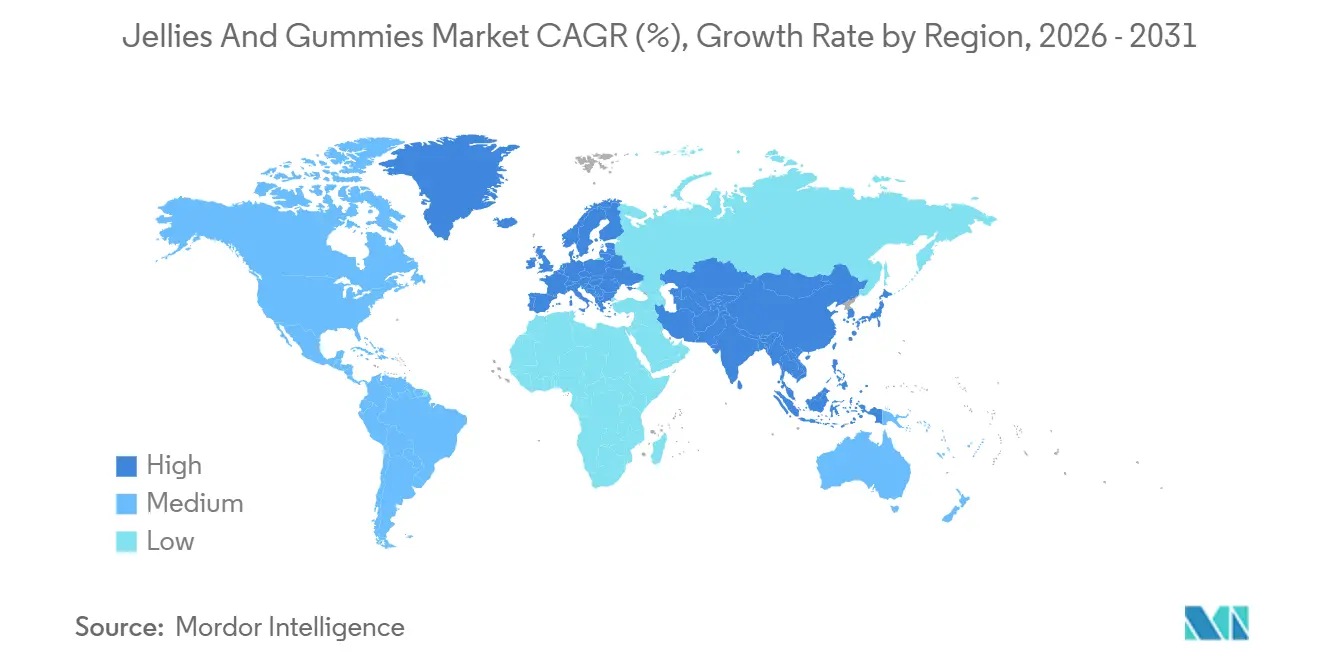

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

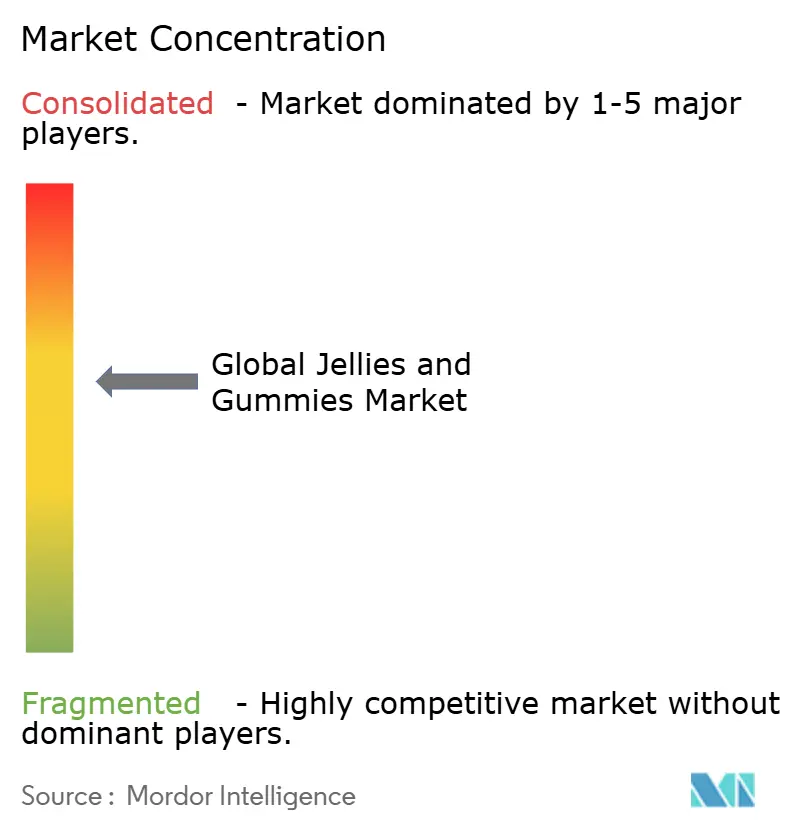

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Jellies And Gummies Market Analysis by Mordor Intelligence

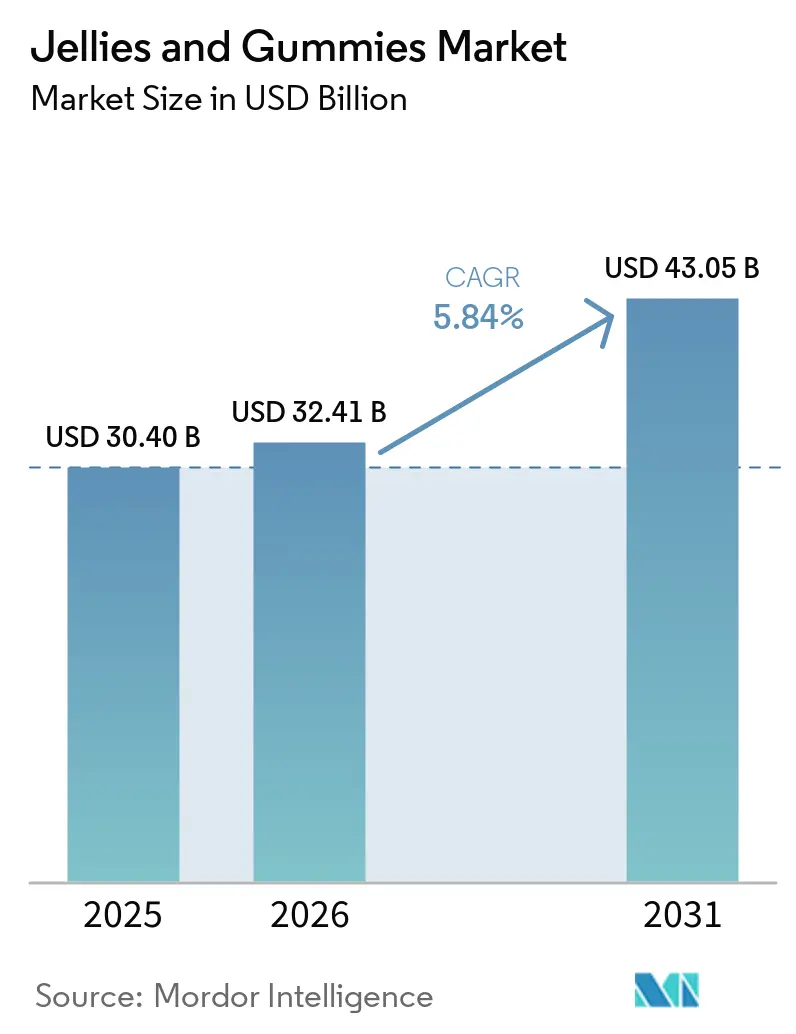

The jellies and gummies market size is expected to grow from USD 30.40 billion in 2025 to USD 32.41 billion in 2026 and is forecast to reach USD 43.05 billion by 2031 at a 5.84% CAGR over 2026-2031. The jellies and gummies market is driven by product innovation, changing consumer preferences, and expanding application areas. A key factor is the increasing demand for functional confectionery, with manufacturers fortifying gummies with vitamins, minerals, collagen, and probiotics to attract health-conscious consumers seeking convenient supplementation options. The rising popularity of plant-based and clean-label products has also led to the adoption of pectin and other non-gelatin ingredients, appealing to vegan and vegetarian consumers. Innovations in flavor and texture, such as exotic fruit blends, sour profiles, and multi-layered formats, are enhancing consumer engagement, particularly among younger demographics. Premiumization trends are further shaping the market, with brands offering organic, low-sugar, and artisanal options to meet evolving taste and wellness preferences. Additionally, the growth of e-commerce and direct-to-consumer channels has improved product accessibility and allowed niche brands to scale rapidly. The increasing use of gummies in pharmaceuticals and nutraceuticals has expanded their appeal beyond traditional confectionery, supporting sustained market growth.

Key Report Takeaways

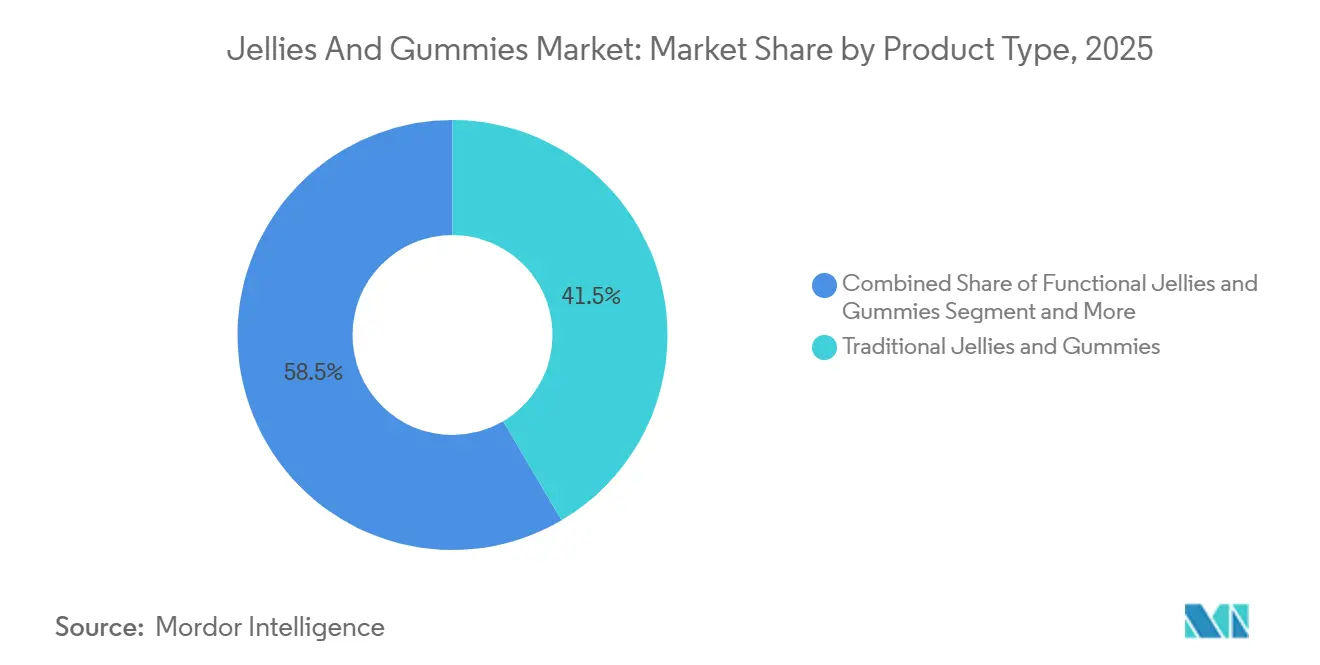

- Traditional jellies and gummies led with 41.53% of the 2025 jellies and gummies market share and are projected to trail functional variants that post a 6.27% CAGR through 2031.

- Gelatin-based formats commanded 43.86% of the 2025 value pool, whereas pectin/plant-based sources are set to expand at a 6.36% CAGR through 2031.

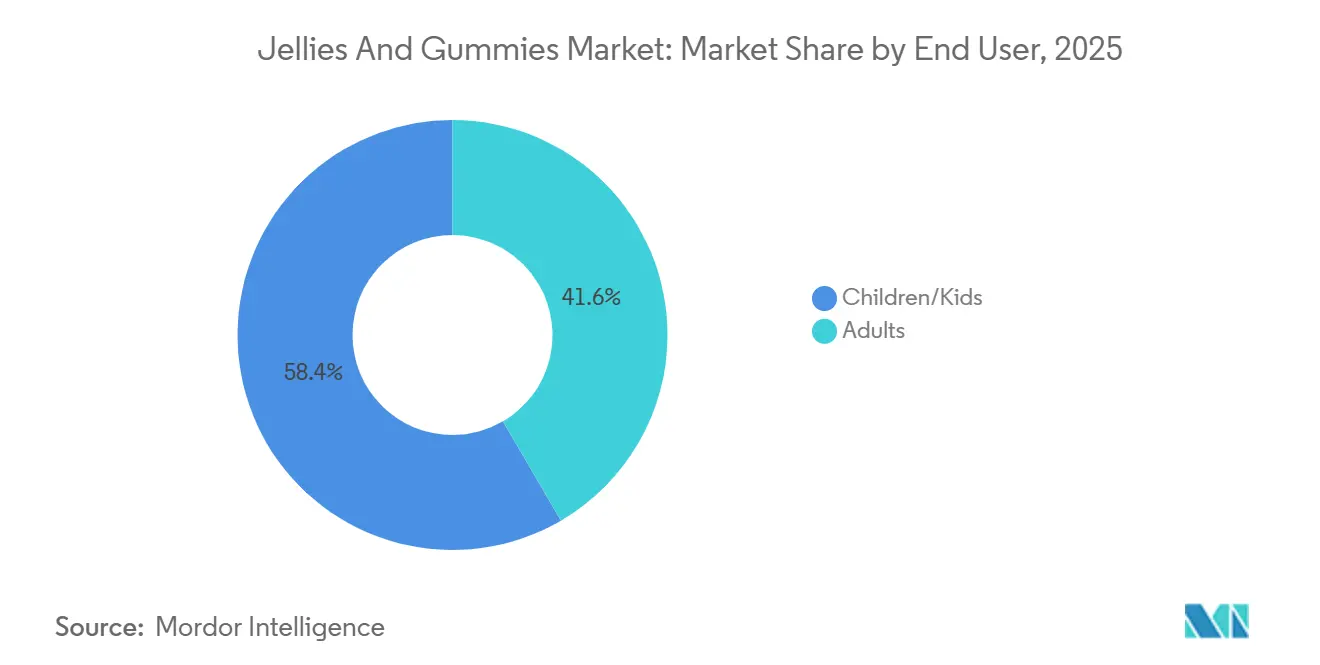

- Children accounted for 58.41% of 2025 consumption; however, the adult segment is forecast to advance at a 6.01% CAGR.

- Supermarkets/hypermarkets held a 37.30% channel share in 2025; online retail is the fastest riser with a 7.18% CAGR.

- Regionally, North America dominated at 41.11% in 2025, while Asia-Pacific delivers the quickest climb at 6.61% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Jellies And Gummies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for functional confectionery | +1.2% | Global, with concentration in North America, Western Europe, and urban Asia-Pacific | Medium term (2–4 years) |

| Innovation in flavors, shapes, and textures | +0.8% | Global, led by North America and Asia-Pacific novelty segments | Short term (≤ 2 years) |

| Expansion of plant-based and vegan product offerings | +1.0% | North America, Europe, Middle East (halal markets), India | Medium term (2–4 years) |

| Increasing demand for sugar-free and low-sugar alternatives | +0.9% | North America, Europe (United Kingdom HFSS compliance), Australia | Short term (≤ 2 years) |

| Growing popularity of personalized nutrition | +0.7% | North America, urban China, Japan, South Korea | Long term (≥ 4 years) |

| Strong influence of social media and digital marketing | +1.1% | Global, strongest in Gen Z and Millennial cohorts across all regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for functional confectionery

The increasing demand for functional confectionery is a significant driver of the global jellies and gummies market, as consumers seek products that combine indulgence with health benefits. Gummies have become a preferred format for delivering functional ingredients such as vitamins, minerals, probiotics, omega-3 fatty acids, and botanical extracts. They offer a more appealing and convenient alternative to traditional tablets and capsules. This trend is particularly prominent among younger consumers and working professionals who value ease of consumption and taste while maintaining a focus on wellness. In response, manufacturers are diversifying their product portfolios to include offerings targeted at immunity support, digestive health, beauty enhancement, and stress management. These products are often marketed with clean-label claims and reduced sugar content. The convergence of confectionery and nutraceuticals has further driven innovation in ingredient sourcing and formulation technologies. This enables brands to position gummies as both enjoyable treats and functional health supplements, thereby contributing significantly to market growth.

Innovation in flavors, shapes, and textures

Innovation in flavors, shapes, and textures is a key factor driving the global jellies and gummies market, enhancing consumer engagement and enabling product differentiation in a competitive environment. Manufacturers are expanding flavor offerings, ranging from traditional fruit options to exotic, sour, spicy, and hybrid combinations, to meet the changing taste preferences of various age groups and regions. Additionally, advancements in molding techniques have led to the creation of diverse shapes, including themed characters, filled centers, layered formats, and 3D designs, which are particularly appealing to children and impulse buyers. Texture innovations, such as dual-texture gummies, chewy-soft combinations, and aerated or foam-infused variants, further enhance the sensory experience and promote repeat purchases. These developments not only help brands differentiate themselves on retail shelves but also support premium positioning and seasonal or limited-edition product launches, contributing to increased consumption and sustained market growth.

Expansion of plant-based and vegan product offerings

The growth of plant-based and vegan product offerings is a significant factor driving the global jellies and gummies market. Changing dietary preferences and ethical considerations are encouraging consumers to choose gelatin-free alternatives. While traditional gummies use animal-derived gelatin, increasing awareness of veganism, sustainability, and religious dietary restrictions has led to the adoption of plant-based gelling agents such as pectin, agar-agar, and carrageenan. This shift allows manufacturers to reach a wider consumer base, including vegans, vegetarians, and flexitarians, while aligning with trends favoring clean-label and natural ingredients. In response, companies are introducing vegan-certified gummies that offer similar taste and texture to traditional products, often accompanied by organic, non-GMO, and allergen-free claims. This approach not only broadens product inclusivity but also supports premiumization and global market growth, positioning plant-based innovation as a key driver for the category.

Increasing demand for sugar-free and low-sugar alternatives

The growing demand for sugar-free and low-sugar alternatives is a significant driver of the global jellies and gummies market, as consumers increasingly focus on managing their sugar intake and its effects on health. Concerns about obesity, diabetes, and dental health have led to a preference for reduced-sugar confectionery options that offer indulgence with fewer calories. In response, manufacturers are reformulating products with alternative sweeteners such as stevia, erythritol, and maltitol to reduce sugar content while preserving taste. This trend is further bolstered by the rising popularity of functional and wellness-oriented snacks, where low-sugar positioning enhances product attractiveness. Moreover, regulatory pressures and sugar reduction initiatives in various countries are encouraging brands to innovate and expand their portfolios with healthier options, thereby broadening the consumer base and driving growth in the jellies and gummies market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations on sugar content and labeling | -0.6% | Global, most acute in United Kingdom, European Union, North America, Australia | Short term (≤ 2 years) |

| High competition from alternative supplement formats | -0.5% | Global, particularly North America and Europe where capsule infrastructure is mature | Medium term (2–4 years) |

| Product recalls and safety concerns | -0.4% | Global, with heightened scrutiny in North America and European Union post-incident | Short term (≤ 2 years) |

| Texture and taste limitations in sugar-free variants | -0.3% | Global, most pronounced in North America, Europe, and urban Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Stringent regulations on sugar content and labeling

Stringent regulations on sugar content and labeling present a significant restraint on the global jellies and gummies market by increasing compliance costs and limiting manufacturers' flexibility in product formulation. Regulatory authorities in key markets require transparent disclosure of nutritional information, particularly sugar levels, subjecting confectionery products to heightened scrutiny. For example, the European Commission's Regulation (EU) No 1169/2011 mandates that all pre-packaged foods display detailed nutrition declarations, including sugar content per 100g or 100ml[1]Source: European Commission, "Nutrition labelling," food.ec.europa.eu. This requirement limits the ability of brands to market high-sugar gummies as casual indulgences without clear disclosure. Similarly, the U.S. Food and Drug Administration requires labeling of “added sugars” with a recommended daily value of 50 grams based on a 2,000-calorie diet, increasing consumer awareness of sugar consumption[2]Source: U.S. Food and Drug Administration, "Added Sugars on the Nutrition Facts Label," fda.gov. Additionally, the UK Department of Health & Social Care has introduced restrictions on the promotion and placement of high fat, sugar, and salt (HFSS) products, including bans on multibuy offers and prominent in-store placements, which directly affect impulse purchases of confectionery items like gummies[3]Source: GOV.UK, "Restricting promotions of products high in fat, sugar or salt by location and by volume price: implementation guidance," gov.uk. These regulatory measures compel manufacturers to invest in reformulation and labeling compliance while also limiting marketing strategies, thereby constraining market growth and profitability.

High competition from alternative supplement formats

High competition from alternative supplement formats serves as a significant restraint on the global jellies and gummies market, particularly as the category expands into functional and nutraceutical applications. Traditional formats, including tablets, capsules, powders, and liquid shots, maintain dominance due to their superior ingredient stability, precise dosage control, longer shelf life, and often lower cost per serving. These formats are also favored by consumers seeking clinically effective or high-potency supplementation, where gummies may face challenges in delivering larger doses of active ingredients without affecting taste, texture, or sugar content. Additionally, advancements in delivery systems such as effervescent tablets, dissolvable strips, and ready-to-drink formulations provide convenient and fast-absorbing alternatives that appeal to health-conscious consumers. Consequently, while gummies attract users with their palatability and ease of consumption, the increasing availability and perceived efficacy of these alternative formats heighten competitive pressures, limiting the growth potential of gummies within the broader functional and dietary supplements market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Variants Outpace Legacy Formats

Traditional jellies and gummies accounted for a 41.53% market share in 2025, driven by their strong association with indulgence, nostalgia, and broad market appeal, solidifying their role in the global confectionery market. Their vibrant colors, playful shapes, and diverse flavors attract children and young consumers, while also appealing to adults seeking affordable treats and occasional indulgence. Ongoing innovation in taste profiles, spanning classic fruit flavors to sour, tangy, and exotic options, keeps the category dynamic and promotes repeat purchases. Seasonal launches, themed packaging, and collaborations with popular entertainment franchises further enhance visibility and encourage impulse buying. The widespread availability of these products across supermarkets, convenience stores, and online platforms, along with competitive pricing and bulk packaging formats, supports high-volume consumption and strengthens their position as a key segment within the jellies and gummies market.

Functional jellies and gummies are projected to grow at a CAGR of 6.27% through 2031, driven by the increasing integration of confectionery and wellness as consumers seek convenient and enjoyable ways to support their health. These products are emerging as alternatives to traditional supplement formats, offering benefits such as vitamins, minerals, probiotics, collagen, and herbal extracts in an easy-to-consume form. Growing awareness of preventive healthcare and demand for targeted solutions, including immunity support, digestive health, beauty enhancement, and stress relief, are boosting adoption across various age groups. Additionally, advancements in formulation technologies are enabling manufacturers to enhance ingredient stability, reduce sugar content, and incorporate plant-based or clean-label ingredients, improving product credibility. The combination of taste and functionality, supported by strong marketing emphasizing health benefits and lifestyle alignment, is driving the growth of functional jellies and gummies within the broader market.

By Ingredient Source: Plant-Based Alternatives Disrupt Gelatin Dominance

Gelatin-based formulations accounted for 43.86% of the market in 2025, driven by their superior texture, elasticity, and sensory appeal. Gelatin provides the distinctive chewy and bouncy consistency that consumers often associate with traditional gummies, making it a preferred choice for both confectionery and certain functional applications. Its ability to deliver a clear, glossy appearance and maintain a stable structure across various formulations ensures consistent product quality at scale. Furthermore, gelatin is cost-effective and widely available, enabling manufacturers to produce gummies at competitive prices while maintaining desirable mouthfeel and flavor release. The ingredient also offers formulation flexibility, allowing for the seamless incorporation of colors, flavors, and active ingredients, which supports product innovation and addresses mass-market demand.

Pectin/plant-based alternatives are growing at a 6.36% CAGR through 2031, driven by the increasing shift toward vegan, vegetarian, and clean-label consumption patterns as consumers avoid animal-derived ingredients. Pectin, typically sourced from fruits, aligns with natural and plant-based positioning, making it appealing to health-conscious and ethically driven consumers. These gummies also cater to religious dietary requirements and allergen-sensitive groups, broadening their global consumer base. Additionally, brands are utilizing pectin-based formulations to introduce organic, non-GMO, and low-sugar variants, often paired with fruit-based flavors that enhance the perception of naturalness. While the texture of pectin-based gummies differs slightly from gelatin, advancements in formulation technologies are improving chewiness and stability, enabling plant-based gummies to compete more effectively while supporting premiumization and differentiation in the market.

By End User: Adult Adoption Reshapes Consumption Patterns

The children/kids segment accounted for 58.41% of end-user demand in 2025, driven by their strong visual appeal, taste, and interactive consumption experience, which makes them highly attractive to younger audiences. Features such as bright colors, fun shapes like animals or cartoon characters, and a variety of fruity and tangy flavors enhance product excitement and encourage repeat consumption. Parents also play a significant role in this demand by purchasing gummies as occasional treats, rewards, or lunchbox additions, particularly when products are marketed with perceived benefits such as added vitamins or reduced sugar content. Seasonal packaging, collaborations with popular media characters, and small, convenient pack sizes further stimulate impulse buying and foster brand loyalty among children. Additionally, the ease of consumption compared to hard candies or chocolates makes gummies a preferred confectionery choice for kids, supporting sustained growth in this segment.

The adults segment is growing at a faster rate, with a 6.01% CAGR projected through 2031, driven by changing consumption patterns that combine indulgence with functionality and convenience. Adults are increasingly attracted to gummies not only as nostalgic treats but also as permissible indulgences that align with busy lifestyles. The rising demand for premium and artisanal variants featuring sophisticated flavors, organic ingredients, and low-sugar formulations caters to more refined taste preferences. Additionally, the expansion of functional gummies infused with vitamins, collagen, and other wellness ingredients appeals to health-conscious consumers seeking enjoyable alternatives to traditional supplements. Discreet, on-the-go consumption, appealing packaging, and positioning as both a treat and a lifestyle product further enhance their appeal among working professionals and older consumers, driving demand in the adult segment.

By Distribution Channel: E-Commerce Reshapes Retail Landscape

Supermarkets/hypermarkets accounted for a 37.30% distribution share in 2025, driven by factors such as high product visibility, extensive shelf space, and strong impulse purchasing behavior. These retail formats strategically position confectionery items near checkout counters, aisle ends, and promotional displays to encourage unplanned purchases. The availability of a wide assortment of brands, flavors, pack sizes, and price points in these stores allows consumers to easily compare options and select products that align with their preferences and budgets. In-store promotions, including discounts, bundle offers, and seasonal displays, further boost demand, particularly during festive periods and holidays. Additionally, the trust associated with established retail chains and the ability to physically inspect products enhance consumer confidence, contributing to consistent, high-volume sales of jellies and gummies through this channel.

Online retail stores are expanding at a 7.18% compound annual growth rate (CAGR) through 2031, driven by increasing digital adoption, convenience, and access to a broader product portfolio. E-commerce platforms provide consumers with the opportunity to explore a wide variety of domestic and international brands, including niche, premium, and functional gummy products that may not be readily available in physical stores. Features such as home delivery, subscription models for regular purchases, and personalized recommendations enhance the shopping experience and encourage repeat purchases. Online channels also offer detailed product information, reviews, and ingredient transparency, which are particularly valued by health-conscious consumers seeking functional or low-sugar options. Additionally, targeted digital marketing, influencer promotions, and exclusive online discounts significantly contribute to driving visibility and sales, making online retail an increasingly vital distribution channel for the jellies and gummies market.

Geography Analysis

North America accounted for a 41.11% market share in 2025, driven by strong demand for functional and fortified confectionery, supported by high consumer awareness of health and wellness. Gummies have gained popularity as a delivery format for supplements such as vitamins, collagen, and probiotics, offering a more enjoyable alternative to traditional pills. The region benefits from a well-established retail infrastructure and high e-commerce penetration, enhancing product accessibility and visibility. Continuous innovation in low-sugar, organic, and clean-label formulations aligns with growing concerns about sugar consumption. Additionally, premiumization trends and artisanal positioning appeal to adult consumers. Aggressive marketing, brand collaborations, and seasonal product launches further stimulate consumption across diverse age groups.

The Asia-Pacific market is expanding at a 6.61% CAGR through 2031, driven by rapid urbanization, rising disposable incomes, and evolving dietary habits. A large and youthful population base, particularly in countries like China and India, supports high demand for colorful, fun, and affordable confectionery products. Increasing health awareness is also encouraging the adoption of functional gummies, especially in urban centers where consumers are more receptive to nutraceutical innovations. The expansion of modern retail formats and the rapid growth of online shopping platforms have significantly improved product availability in both metropolitan and tier-2 cities. Additionally, local flavor adaptations and region-specific product innovations enable brands to cater to diverse taste preferences, further accelerating market growth.

In Europe, demand is driven by a strong preference for premium, organic, and plant-based gummies, alongside increasing regulatory focus on sugar reduction, which is encouraging reformulation and innovation. South America benefits from growing urban populations and expanding retail networks, where affordable confectionery products remain popular among price-sensitive consumers. In the Middle East and Africa, rising youth demographics, increasing westernization of diets, and expanding supermarket and convenience store channels are fueling demand. Across these regions, product diversification, including halal-certified and gelatin-free variants, along with improved distribution and marketing strategies, plays a crucial role in sustaining market expansion.

Competitive Landscape

The global jellies and gummies market exhibits a moderately fragmented competitive structure, where established multinational companies coexist with a growing number of niche and wellness-focused brands. Prominent confectionery companies, including Mars, Haribo, Ferrara Candy Company, Nestlé, and Perfetti Van Melle, maintain strong market positions through extensive product portfolios, brand recognition, and global distribution networks. These companies dominate traditional confectionery segments by leveraging economies of scale, efficient sourcing of key ingredients like gelatin, and widespread retail penetration. Their ability to innovate within established formats, introducing new flavors, packaging, and seasonal offerings, helps sustain consumer loyalty in mass-market segments.

Simultaneously, the market is experiencing the rapid growth of challenger brands such as SmartSweets, SmartyPants, and Goli Nutrition. These brands are reshaping the competitive landscape by focusing on health-conscious consumers. They differentiate themselves through clean-label formulations, reduced sugar content, plant-based ingredients, and strong digital-first branding strategies. By aligning with evolving regulatory requirements for sugar reduction and transparent labeling, these brands are capturing demand in functional and better-for-you segments. Their use of influencer marketing, direct-to-consumer channels, and social media engagement facilitates faster brand building and stronger connections with younger demographics, positioning them as agile competitors to traditional manufacturers.

Competition in the jellies and gummies market is further intensified by innovation and shifting consumer preferences. Advances in formulation technologies are enabling the development of new textures, delivery systems, and ingredient combinations, allowing both established players and emerging brands to diversify their product offerings. Additionally, the growing focus on personalization, ethical sourcing, and dietary inclusivity, such as vegan and halal compliance, is broadening the competitive scope beyond traditional factors like taste and price. As digital commerce evolves, brands that effectively integrate data-driven consumer insights with product development and distribution strategies are better positioned to capitalize on emerging opportunities. This dynamic environment underscores the increasingly innovation-driven nature of the competitive landscape.

Jellies And Gummies Industry Leaders

-

Mars, Incorporated

-

Ferrara Candy Co. Inc.

-

Haribo GmbH & Co. KG

-

Nestlé S.A.

-

Albanese Confectionery Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: GateDrop launched a new line of energy gummies, marking its strategic entry into the functional confectionery market. The product is positioned as a convenient and versatile alternative to traditional energy drinks.

- April 2026: TopGum Industries expanded its nutraceutical portfolio with the introduction of a women’s health-focused gummy line, addressing wellness needs related to PMS, menopause, prenatal care, and hormonal balance. The product line features science-based formulations, incorporating botanicals such as shatavari and Vitex, along with essential nutrients like magnesium, vitamin D, and vitamin B6, to provide targeted health benefits in a convenient gummy format. The company is also enhancing its clean-label approach by utilizing plant-based, pectin-derived formulations and reduced-sugar systems, enabling brands to deliver functional, evidence-based supplements that cater to the increasing demand for personalized and preventive healthcare solutions.

- February 2026: Sweet Venture Group launched a new gummy candy concept under the Gummi Popz™ brand, designed to offer a multi-sensory experience with layered flavors and popping textures. This initiative aims to attract younger, trend-conscious consumers by highlighting customization, shareability, and interactive eating experiences that extend beyond conventional confectionery formats.

Global Jellies And Gummies Market Report Scope

| Traditional Jellies and Gummies |

| Functional Jellies and Gummies |

| Sugar-Free/Low Sugar Jellies and Gummies |

| Other Product Types |

| Gelatin-Based |

| Pectin/Plant-Based (Vegan) |

| Other Hydrocolloids |

| Children/Kids |

| Adults |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Pharmacy/Drug Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Sweden | |

| Belgium | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Traditional Jellies and Gummies | |

| Functional Jellies and Gummies | ||

| Sugar-Free/Low Sugar Jellies and Gummies | ||

| Other Product Types | ||

| By Ingredient Source | Gelatin-Based | |

| Pectin/Plant-Based (Vegan) | ||

| Other Hydrocolloids | ||

| By End User | Children/Kids | |

| Adults | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Pharmacy/Drug Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global jellies and gummies market in 2026?

The jellies and gummies market size is USD 32.41 billion in 2026 and is expected to reach USD 43.05 billion by 2031.

Which region grows the fastest through 2031?

Asia-Pacific posts the quickest advance at a 6.61% CAGR, propelled by urbanization, halal-certified launches, and rising discretionary incomes.

What segment captures the largest 2025 share?

Traditional jellies and gummies lead with 41.53% of 2025 value.

What is the outlook for online retail?

Online sales rise at a 7.18% CAGR as TikTok Shop, brand websites, and subscription models cut shelf-space hurdles and lower customer acquisition costs.

Page last updated on: