Sugar Alcohol Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

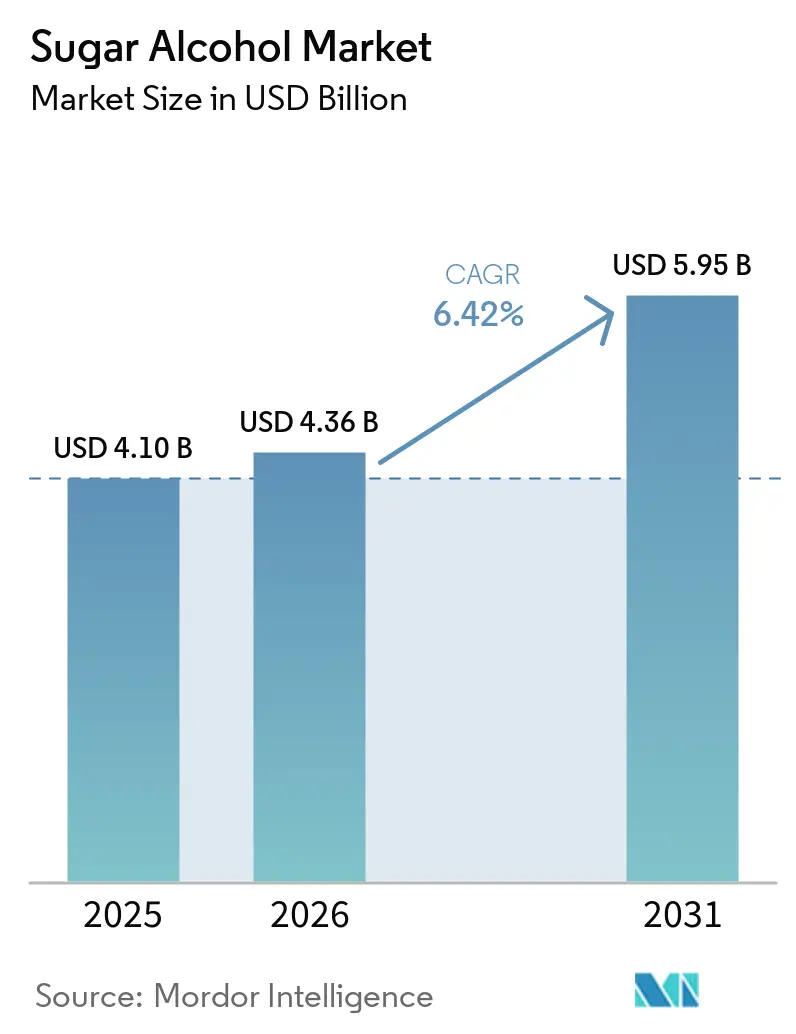

| Market Size (2026) | USD 4.36 Billion |

| Market Size (2031) | USD 5.95 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sugar Alcohol Market Analysis by Mordor Intelligence

The Sugar alcohols market size was valued at USD 4.10 billion in 2025 and estimated to grow from USD 4.36 billion in 2026 to reach USD 5.95 billion by 2031, at a CAGR of 6.42% during the forecast period 2026-2031. This growth is driven by the increasing use of polyols in food, pharmaceutical, and personal care industries as low-calorie bulking agents, non-cariogenic sweeteners, humectants, and excipients. Their multifunctionality gives sugar alcohols an advantage over high-intensity sweeteners, especially as sugar reduction remains a priority for public health bodies, regulators, and major retailers. Trade actions in Europe and the U.S. are also influencing sourcing strategies, boosting demand for traceable and fermentation-based supplies while reducing reliance on single-origin sources. The market is divided between higher-margin premium grades and price-sensitive commodity grades, creating competitive pressure on standard erythritol and sorbitol while supporting stronger pricing in pharmaceutical and specialty applications. Key opportunities lie in sugar-free foods, oral care, nutraceuticals, and excipient-grade ingredients, where health benefits, formulation functionality, and supply reliability align.

Key Report Takeaways

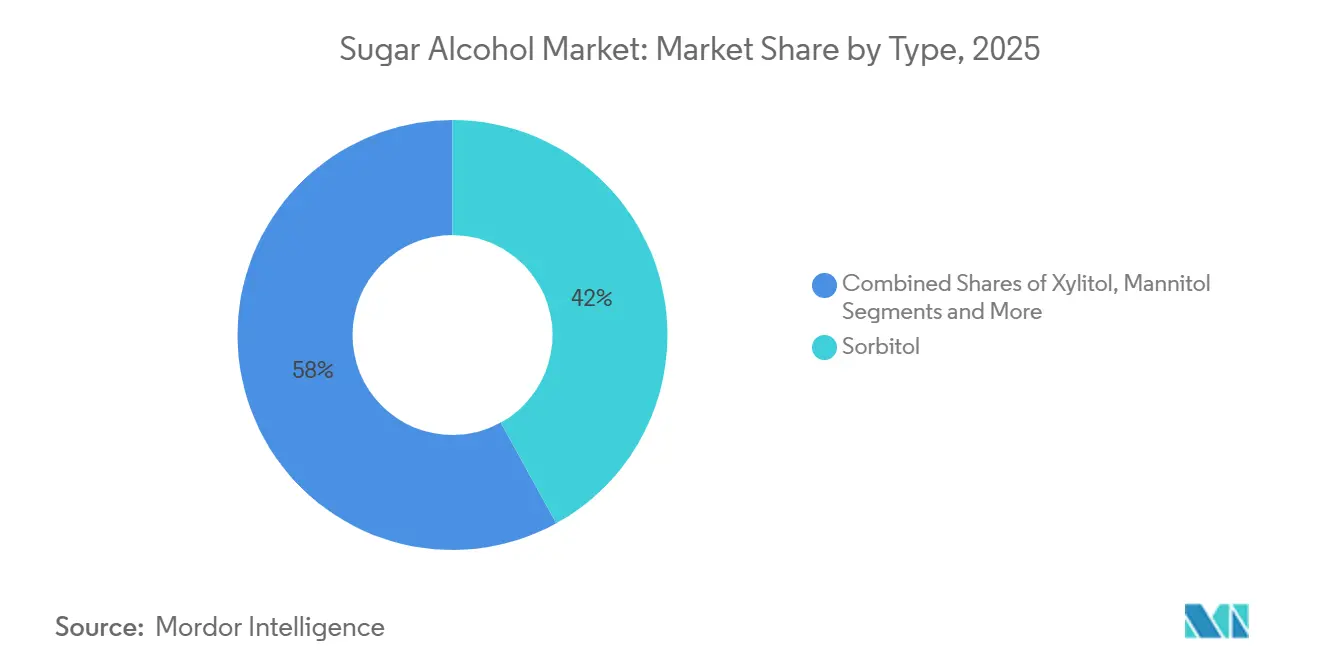

- By type, sorbitol held 41.98% of the sugar alcohols market in 2025, while erythritol is forecast to expand at 6.86% CAGR through 2031.

- By form, powder accounted for 72.76% of the sugar alcohols market in 2025, while liquid is projected to record the highest growth at 7.01% CAGR through 2031.

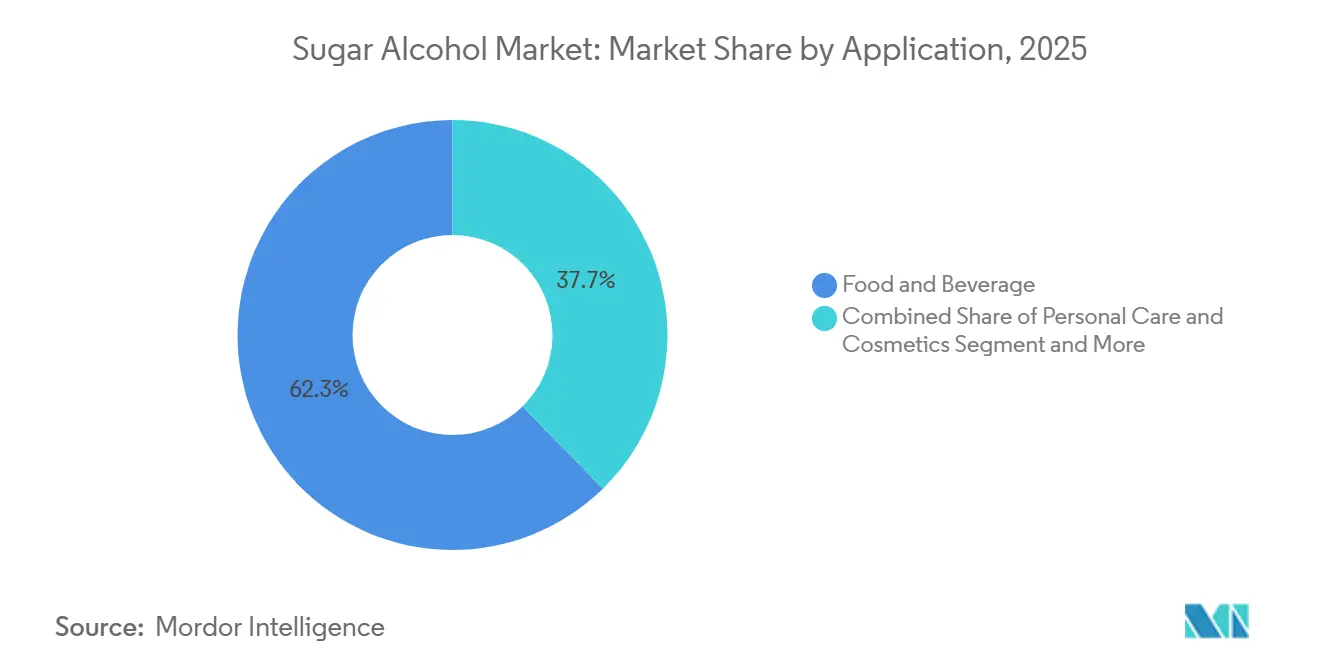

- By application, food and beverage captured 62.33% of the sugar alcohols market in 2025, while personal care and cosmetics are expected to advance at 7.91% CAGR through 2031.

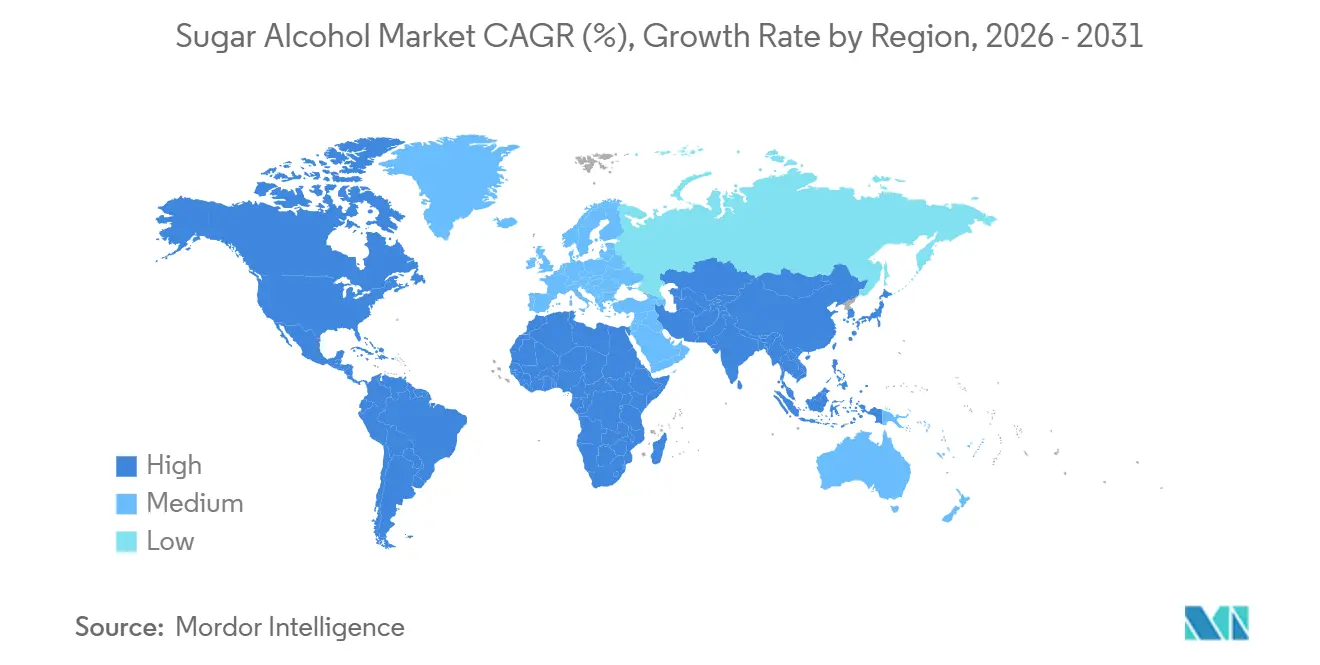

- By geography, Europe accounted for 44.87% of the sugar alcohols market in 2025, while North America is forecast to grow fastest at a 7.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sugar Alcohol Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | impact timeline |

|---|---|---|---|

| Consumer preference shifting toward low-calorie and sugar-free products | +1.8% | Global; strongest pull in Europe and North America | Short term (≤ 2 years) |

| Rising prevalence of diabetes and obesity fueling alternative sweetener demand | +1.5% | Global; accelerating in APAC and MEA | Medium term (2–4 years) |

| Growing consumer demand for clean-label, naturally sourced ingredients | +0.9% | North America & Europe; rapid uptake in APAC | Medium term (2–4 years) |

| Surge in demand for functional foods and beverages | +0.7% | Global; highest intensity in APAC and North America | Medium term (2–4 years) |

| Non-insulin-dependent sweetness gaining traction among consumers | +0.5% | Global; concentrated in diabetic nutrition applications | Long term (≥ 4 years) |

| Expansion of pharmaceutical applications | +0.4% | Global; North America and Europe leading | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer Preference Shifting Toward Low-Calorie and Sugar-Free Products

The reformulation of packaged food and beverage products is accelerating, driving growth in the sugar alcohols market. Polyols, a type of sugar alcohol, play a key role by providing bulk, texture, and process stability, features that high-intensity sweeteners alone cannot offer. In Germany, official data shows that 94.5% of sugar-free and reduced-sugar soft drinks use a combination of multiple sweeteners instead of relying on a single ingredient. This highlights the importance of polyols in blended sweetener systems[1]Source: Bundesinstitut für Risikobewertung, “Sweeteners in Food, Selected Questions and Answers”, bfr.bund.de. As a result, the sugar alcohols market is expanding, supported by new SKU launches, even though sweetness levels per serving are limited by tolerance thresholds and labeling requirements. Additionally, polyols are becoming more relevant in mainstream food categories as large brands aim to maintain the mouthfeel and structure of traditional sugar-based products. This trend is driving demand not only in the sugar-free category but also in reformulated products across biscuits, confectionery, beverages, and nutritional items. Suppliers capable of ensuring consistent functionality across various product textures and processing conditions are particularly well-positioned to benefit from this growing demand in the sugar alcohols market.

Rising Prevalence of Diabetes and Obesity Driving Demand for Alternative Sweeteners

Broader demand for sugar reduction tools, aimed at calorie control and glycemic management, is bolstering the sugar alcohols market. Polyols cater to this demand, enabling manufacturers to cut sugar without compromising on bulk, sweetness balance, moisture retention, or processing behavior in the final products. This versatility is crucial for food, oral care, and pharmaceutical producers, who seek practical substitutes over mere single-function sweeteners. Consequently, the sugar alcohols market is buoyed not only by public health pressures but also by both private label and branded manufacturers. These manufacturers are expanding their portfolios to include sugar-free and reduced-sugar options across various everyday consumption categories. Given that these health concerns resonate with both premium and mass-market channels, the demand for sugar alcohols is poised to remain robust. This widespread appeal broadens the customer base for products containing polyols. As a result, the sugar alcohols market is more closely aligned with enduring dietary shifts than fleeting consumer trends.

Consumer Demand for Clean-Label, Naturally Sourced Ingredients

As clean-label preferences gain traction, the sugar alcohols market is witnessing a pronounced shift towards fermentation-derived polyols, touted for their natural sourcing and traceable production. This trend has led to a commercial divide: fermentation-based erythritol is now favored over its hydrogenation-based counterparts, despite both offering similar technical performance. The pattern was further solidified by the January 2025 anti-dumping duties imposed on Chinese-origin erythritol in Europe, nudging buyers towards diversified sourcing and stringent origin documentation. In today's sugar alcohols market, transparency in supply isn't just a procurement asset; it's a marketing boon. This is particularly evident in sectors like confectionery, dairy alternatives, supplements, and premium beverages. Suppliers adept at documenting fermentation pathways, utilizing non-GMO inputs, and maintaining stable regional supply arrangements are reaping the rewards. Their ability to showcase these attributes not only bolsters their market position but also aligns with the discerning tastes of clean-label buyers, who prioritize sourcing quality alongside calorie reduction and flavor in their sugar alcohol choices.

Rising Demand for Functional Foods and Beverages Market

Polyols, once mainly valued for reducing sweetness, are now gaining importance in functional food and beverage formulations. Xylitol, well-known for its oral health benefits, provides a clear opportunity for formulators to develop products that combine great taste, dental health advantages, and lower sugar content. A peer-reviewed study published in 2025 highlighted that erythritol and xylitol, as membrane-active polyols, can reduce reactive oxygen species in mammalian cells. This finding opens up new possibilities for their use in functional nutrition. If future human studies confirm these effects in commercial nutrition products, the sugar alcohols market could see significant growth. Such evidence would give suppliers a strong, science-based advantage beyond just calorie reduction. Even now, manufacturers are actively testing formulations that use polyols to enhance taste, texture, and health benefits in a single product. This approach keeps the sugar alcohols market aligned with areas where consumer loyalty and pricing power are stronger compared to traditional sweetener applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasingly stringent labeling regulations | -0.4% | Europe, North America | Short term (≤ 2 years) |

| Challenges in sourcing raw materials | -0.4% | APAC feedstock chains and global supply networks | Short term (≤ 2 years) to Medium term (2-4 years) |

| Environmental concerns over synthetic production | -0.3% | Global, highest scrutiny in Europe and North America | Medium term (2-4 years) |

| Product adulteration and inconsistent quality | -0.2% | APAC-origin supply chains and global import markets | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Labeling Regulations Are Becoming More Stringent

Regulatory compliance plays a significant role in shaping the sugar alcohols market, requiring clear labeling of sweetener compositions and consumer warnings. In Europe, products containing more than 10% sugar alcohols must include a warning that excessive consumption may cause laxative effects. This regulation directly impacts serving size decisions for confectionery and snack products. While these rules do not reduce demand, they limit how much polyol content manufacturers can include in individual products. In 2025, in the United States, the FDA requires sugar alcohols to be listed on nutrition labels and included under total carbohydrates. This regulation increases scrutiny on zero-sugar claims and related health messaging[2]Source: Food and Drug Administration, “Food and Drug Administration Compliance Program Manual Program 7321.005, General Food Labeling Requirements”, fda.gov. Additionally, the market faces medium-term uncertainty as older additive frameworks are re-evaluated. Even when the authorized-use status remains unchanged, these reviews can alter compliance requirements. Therefore, maintaining regulatory readiness is a key competitive advantage for suppliers and brand owners operating across multiple regions in the sugar alcohols market.

Sourcing Raw Materials Poses Challenges

In the sugar alcohols market, feedstock volatility poses a persistent challenge. Production economics are closely tied to agricultural inputs like starch and glucose. When costs for these raw materials fluctuate sharply, commodity-grade producers feel the pinch on their margins. Simultaneously, buyers grapple with uncertainties regarding contract pricing and the consistency of deliveries. Adding to this complexity are trade barriers. Procurement teams now find themselves juggling multiple factors: price, origin, compliance, and the reliability of supply. As a response, many in the sugar alcohols market are turning to dual-sourcing. While this strategy can elevate purchase costs for food and pharmaceutical manufacturers, it's seen as a necessary trade-off. Furthermore, buyers are increasingly prioritizing supplier audits, consistency in purity, and the quality of documentation. This trend tends to benefit established producers, making it harder for newcomers to gain a foothold. Consequently, in the sugar alcohols market, it's not just about availability; the focus is equally on ensuring that the supply is both usable and compliant, not merely abundant.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Sorbitol Dominance Faces Erythritol Challenge

In 2025, sorbitol accounted for 41.98% of the market, maintaining its position as the leading sugar alcohol type. Erythritol, on the other hand, is expected to grow at a strong CAGR of 6.86% through 2031. Sorbitol remains a key player in the sugar alcohols industry due to its extensive use in food, pharmaceutical, and personal care products. Its established manufacturing scale and regulatory acceptance make it a reliable choice for buyers who prioritize cost efficiency, process stability, and versatility across multiple applications. Erythritol is gaining traction because of its zero-calorie content and fermentation-based production, which align well with the growing demand for premium beverages, health-focused foods, and sugar-free confectionery. This trend highlights a clear division in the sugar alcohols market, with traditional bulk-use products like sorbitol competing against newer, premium-growth options like erythritol.

Sorbitol continues to dominate high-volume applications, while erythritol is becoming more prominent in categories where low-calorie content and clean-label ingredients influence consumer choices. Xylitol remains significant due to its anti-cavity properties, which support its use in oral care products, chewing gum, and dental formulations. Mannitol holds value in the pharmaceutical sector, where its crystalline structure makes it suitable for specialized excipient roles. Maltitol retains its importance in confectionery applications because its sweetness closely resembles sucrose, ensuring consistent taste during product reformulations. Other polyols, such as isomalt and lactitol, contribute to the sugar alcohols market by offering benefits like improved texture, stability, and processing performance, even if their overall market share is smaller.

By Form: Liquid Applications Drive Industrial Demand

In 2025, powder dominated the market, claiming a substantial 72.76% share. This dominance underscores the sugar alcohols market's deep-rooted connection to dry-process manufacturing, spanning applications from tablets and bakery mixes to chewing gum bases and powdered nutrition products. Powdered forms are the go-to choice for manufacturers prioritizing transport efficiency, dosage control, storage stability, and dry blending, all of which are pivotal to production economics. In the realm of pharmaceutical tableting, powder polyols play a crucial role, ensuring compression and formulation consistency, thus solidifying their position in oral solid dose manufacturing. Moreover, in bakery and supplement sectors, powders seamlessly integrate into existing process lines, a factor that bolsters repeat purchases in the sugar alcohols market. This trend elucidates why, despite the projected rapid growth of liquid forms, powders continue to command the largest share in the sugar alcohols market.

Liquid forms are on a trajectory to expand at a robust 7.01% CAGR through 2031, positioning them as the fastest-growing segment in the sugar alcohols market. Specifically, liquid sorbitol syrup and liquid maltitol are carving out significant roles in dairy, confectionery, sauces, and oral care sectors. Their ability to expedite dissolution and seamlessly integrate into continuous processing systems is a key advantage. Additionally, their humectant properties shine in high-moisture environments, where maintaining texture and extending shelf life are paramount. In pharmaceuticals, sorbitol syrup's relevance is underscored by its ability to balance viscosity, sweetness control, and excipient compatibility. Thus, while the sugar alcohols market is anchored by the powder form, the liquid segment is poised to carve out a larger share, especially in processing scenarios where operational efficiency is as crucial as ingredient cost.

By Application: Food and Beverage Dominates; Personal Care Accelerates

In 2025, the food and beverage sector led the sugar alcohols market, holding 62.33% of the total share. This dominance highlights the significant role of polyols in producing a wide range of products, including confectionery, bakery items, beverages, dairy products, and sugar-free snacks, catering to both mainstream and premium brands. Confectionery remains the largest demand driver, as sorbitol and maltitol are essential for maintaining sweetness, moisture, and texture in products like hard candies, gums, and chocolates. Additionally, the growing popularity of sugar-free soft drinks and energy drinks has increased the use of erythritol in beverage reformulations, thanks to its stability in acidic environments and zero-calorie benefits. While food and beverage continue to form the backbone of the sugar alcohols market, other sectors are experiencing faster growth rates.

The personal care and cosmetics segment is projected to grow at a 7.91% CAGR through 2031, making it the fastest-growing application in the sugar alcohols market. Sorbitol plays a key role in this segment, providing moisture retention and improving the texture of soaps, skincare products, and oral hygiene items. Xylitol is also gaining traction in premium oral care and skincare products, as its antimicrobial properties and freshness benefits align well with sugar-free claims. In the pharmaceutical sector, steady growth is driven by the use of mannitol in specialized dosage forms and the application of sorbitol and xylitol in excipients and oral liquid formulations. This diverse application base ensures that while food and beverage provide the market's scale, personal care and health-focused products drive faster value growth.

Geography Analysis

In 2025, Europe commanded a dominant 44.87% share of the global sugar alcohols market, underscoring its pivotal role and robust demand base. Europe's mature food production, robust pharmaceutical manufacturing, and established personal care sector collectively bolster steady polyol usage across diverse industries. Furthermore, European consumers' growing awareness of sugar reduction and clean-label trends in packaged foods amplifies the region's sugar alcohols market. Notably, the imposition of definitive anti-dumping duties on Chinese-origin erythritol in January 2025 altered Europe's procurement dynamics, steering buyers towards alternative, well-documented supply sources.

North America is projected to outpace other regions with a robust 7.45% CAGR growth rate through 2031 in the sugar alcohols market. This surge is fueled by vigorous reformulation efforts in food and beverages, a conducive environment for major polyols, and a growing preference for health-conscious packaged products. Additionally, trade actions against Chinese erythritol are spurring a trend towards dual-sourcing and an increased reliance on certified non-Chinese supplies, reshaping pricing and procurement strategies. This evolution underscores North America's significance, not just in consumption growth, but also in redefining supplier relationships within the sugar alcohols landscape.

Asia-Pacific stands as a pivotal player in the sugar alcohols arena, balancing vast production capabilities with a surge in local consumption. While China remains the linchpin of global supply, the broader Asia-Pacific region is gaining traction as buyers seek diversified sourcing and alternative fermentation avenues. The regional market is buoyed by a heightened focus on sugar reduction, the launch of functional foods, and health-centric product innovations, particularly among urban consumers. In South America, though the sugar alcohols market is relatively modest, it's witnessing growth, spurred by an uptick in the availability of reduced-sugar packaged food and beverages. Meanwhile, the Middle East and Africa, still in nascent stages, are witnessing a burgeoning sugar alcohols market, driven by local manufacturers' responses to sugar reduction demands and trends in premium food imports.

Competitive Landscape

The sugar alcohols market is concentrated at the top tier but fragmented in commodity supply. Major vertically integrated producers dominate premium segments like pharmaceuticals, nutraceuticals, and personal care by leveraging starch processing, fermentation, application support, and global distribution. In contrast, standard sorbitol and erythritol categories face intense price competition from a wide base of Asian manufacturers, making profits more secure in certified, application-specific grades than in bulk supply.

Roquette's USD 2.85 billion acquisition of IFF's Pharma Solutions business strengthened its position in excipient-led segments and expanded its pharmaceutical platform, benefiting mannitol and related polyols. This move reflects a broader industry trend of shifting from commodity exposure to high-value health applications. In 2024, Roquette also partnered with Bonumose to develop and scale tagatose, highlighting efforts to diversify sugar management portfolios beyond polyols. This diversification is critical as customers increasingly seek suppliers capable of supporting multiple reformulation needs under one partnership.

Success in the sugar alcohols market depends on purity, regulatory readiness, traceability, and support for complex reformulations. Suppliers with strong fermentation expertise and clear sourcing are well-positioned to meet growing demand for premium food and supplements, driven by trade dynamics and clean-label trends. Pharmaceutical suppliers gain an edge through lengthy qualification cycles and compliance requirements, fostering long-term customer relationships. In personal care, competition focuses on multi-functional humectants and oral care ingredients, where formulation support is as important as price. While scale and technology drive success in premium segments, the market remains open and price-sensitive in commodity grades, ensuring a diverse supplier base.

Sugar Alcohol Industry Leaders

Roquette Frères

Cargill Inc.

Archer Daniels Midland

Ingredion Incorporated

Tereos S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Roquette has completed the acquisition of IFF Pharma Solutions, representing a pivotal advancement in its goal to establish leadership within the global pharmaceutical market.

- September 2024: Tonix Pharmaceuticals presented data on TNX-102 SL formulation using mannitol as eutectic forming agent for sublingual drug delivery at Global Conference on Pharmaceutics and Novel Drug Delivery Systems.

- January 2024: Ahmedabad-based Sanstar Limited announced plans to invest ₹181 crore from its IPO proceeds to expand its maize-based specialty products manufacturing facility in Dhule, Maharashtra. This expansion will add 1,000 tons per day capacity, expected to be operational by July 2025, strengthening its position in the sugar alcohol market.

Global Sugar Alcohol Market Report Scope

| Sorbitol |

| Xylitol |

| Mannitol |

| Maltitol |

| Erythritol |

| Others |

| Powder |

| Liquid |

| Food and Beverage | Bakery |

| Confectionery | |

| Beverages | |

| Dairy | |

| Others | |

| Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Sorbitol | |

| Xylitol | ||

| Mannitol | ||

| Maltitol | ||

| Erythritol | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| By Application | Food and Beverage | Bakery |

| Confectionery | ||

| Beverages | ||

| Dairy | ||

| Others | ||

| Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in sugar alcohols demand through 2031?

Growth is being supported by sugar reduction reformulation, clean-label demand, and wider use of polyols in food, pharmaceuticals, and personal care. The market is projected to rise from USD 4.36 billion in 2026 to USD 5.95 billion by 2031 at a 6.42% CAGR.

Which product type leads current demand for sugar alcohols?

Sorbitol leads the type mix with 41.98% share in 2025 because it is widely used across food, oral care, and pharmaceutical formulations.

Which type is expected to grow fastest in the coming years?

Erythritol is expected to expand fastest at 6.86% CAGR through 2031, helped by its zero-calorie profile and fit with premium sugar-free reformulation.

Which region is growing fastest for sugar alcohols?

North America is forecast to grow fastest at 7.45% CAGR through 2031, supported by reformulation activity and sourcing changes linked to erythritol trade actions.

Page last updated on: