Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

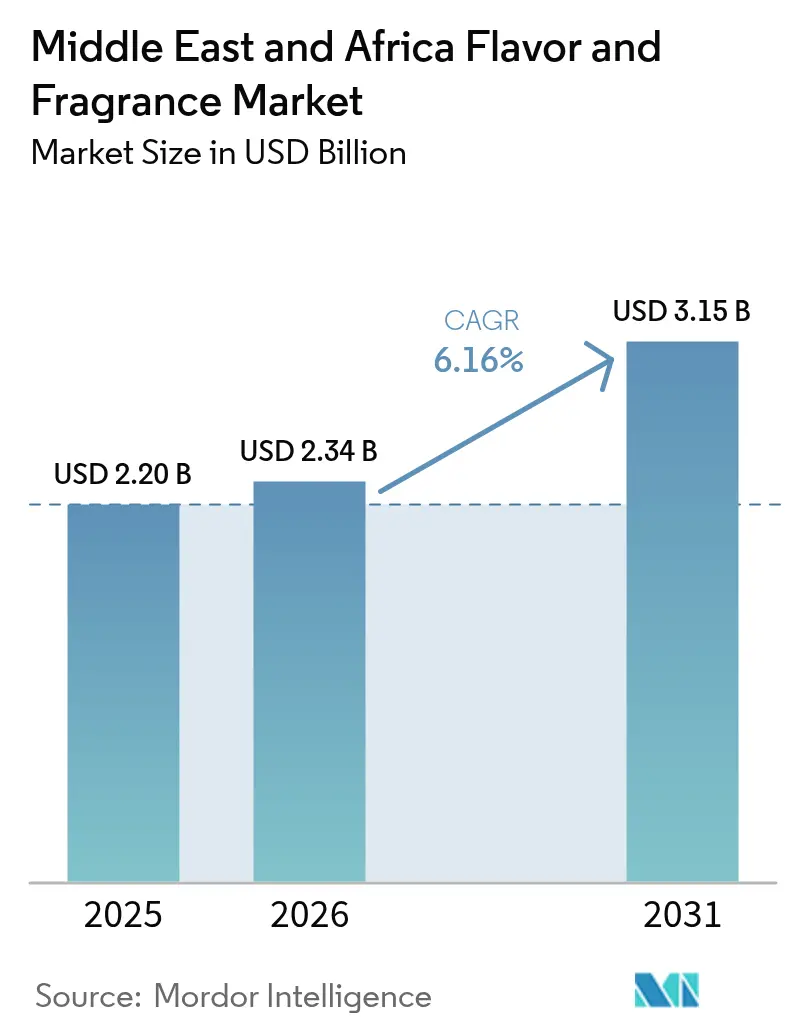

| Base Year Market Size (2025) | USD 2.20 Billion |

| Market Size (2026) | USD 2.34 Billion |

| Market Size (2031) | USD 3.15 Billion |

| Growth Rate (2026 - 2031) | 6.16% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Flavor And Fragrance Market Analysis by Mordor Intelligence

The Middle East and Africa flavor and fragrance market size is expected to grow from USD 2.20 billion in 2025 to USD 2.34 billion in 2026 and is forecast to reach USD 3.15 billion by 2031 at 6.16% CAGR over 2026-2031. Rising consumer preference for premium sensory experiences, regulation-driven reformulation, and investment in local innovation centers continue to shape the demand curve for the Middle East and Africa flavor and fragrance market. Intensifying focus on clean-label solutions, especially in Saudi Arabia and the United Arab Emirates, is channeling research and development budgets into biotechnology and regenerative agriculture. Regional infrastructure investments such as Symrise’s USD 1.16 million Dubai innovation hub and IMCD Group’s technical center underscore the growing importance of localized flavor and fragrance development. The competitive field remains moderately fragmented, with global leaders leveraging digital tools for formulation precision while regional specialists build supply partnerships to secure botanical inputs. Opportunities abound in functional beverages, halal-certified personal care, and vegan product lines, yet companies must navigate emerging sustainability mandates and the volatility of key raw materials such as vanilla beans.

Key Report Takeaways

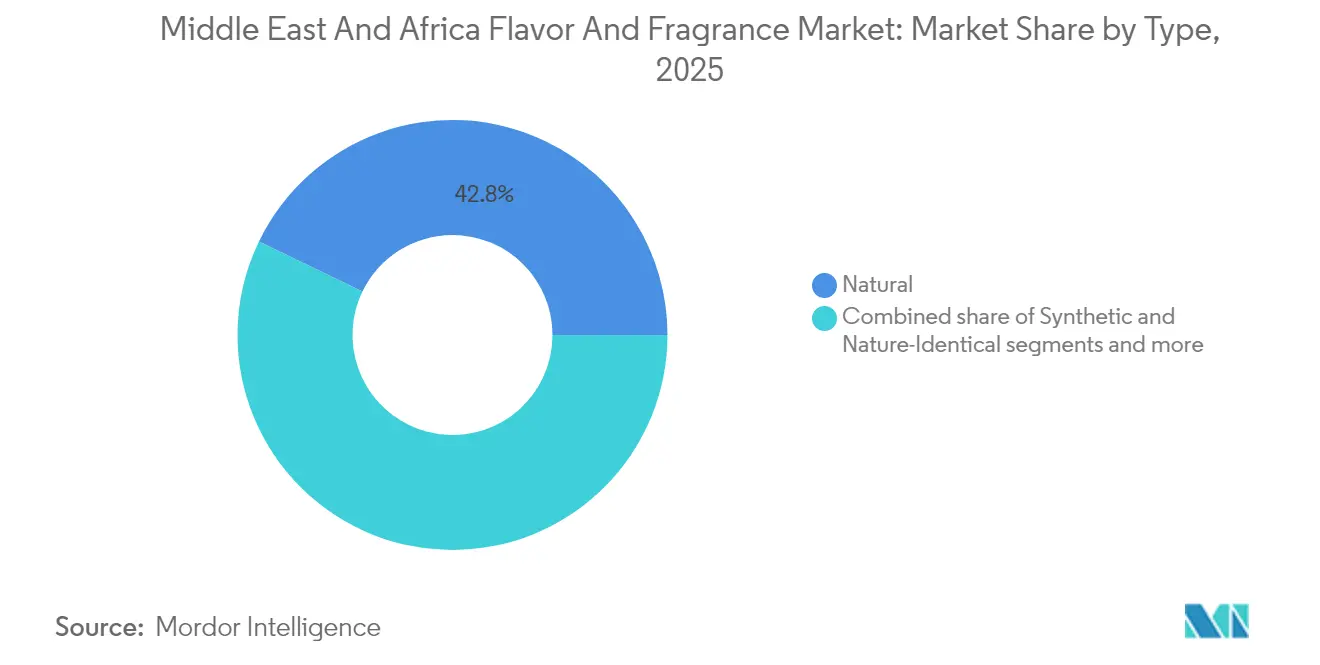

- By type, natural ingredients captured 42.83% of the Middle East and Africa flavor and fragrance market share in 2025. Natural ingredients are forecast to advance at a 6.78% CAGR between 2026-2031.

- By form, liquid formats held 33.78% share of the Middle East and Africa flavor and fragrance market in 2025, and powder formats are recording the highest projected CAGR at 6.56% through 2031.

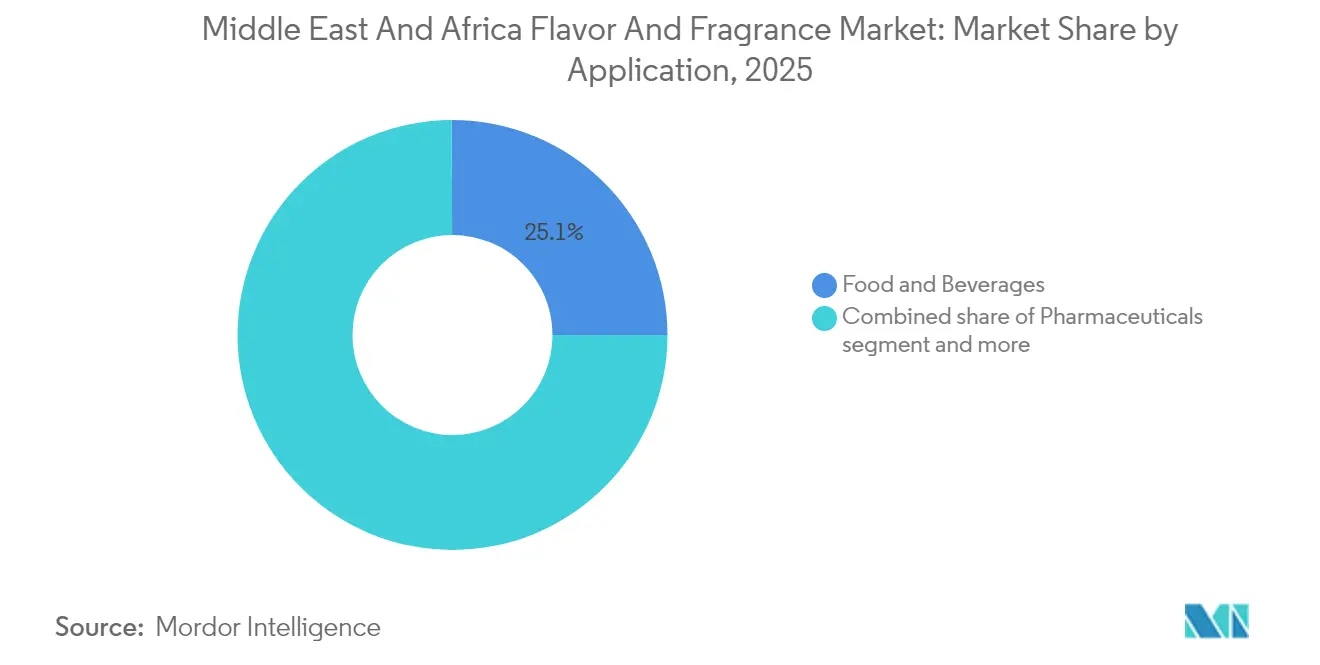

- By application, beverages accounted for 25.06% of market share in 2025, while personal care and cosmetics are advancing at a 6.29% CAGR through 2031.

- By geography, South Africa led with 35.11% of the Middle East and Africa flavor and fragrance market share in 2025. Saudi Arabia is projected to expand at a 6.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Flavor And Fragrance Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural and clean-label ingredients | +1.2% | Global, with strongest impact in Saudi Arabia and United Arab Emirates | Medium term (2-4 years) |

| Growth of functional foods, beverages, and wellness products | +0.9% | Africa-wide, particularly South Africa and Nigeria | Long term (≥ 4 years) |

| Increasing popularity of personalized and customized flavor/fragrance solutions | +0.7% | Gulf Cooperation Council countries, expanding to North Africa | Medium term (2-4 years) |

| Expansion of processed food and beverage industry | +1.1% | Saudi Arabia, United Arab Emirates South Africa | Short term (≤ 2 years) |

| Increasing use of fragrances in cosmetics and personal care products | +0.8% | United Arab Emirates, Saudi Arabia, Morocco | Medium term (2-4 years) |

| Growing interest in vegan and cruelty-free ingredients | +0.5% | Urban centers across Middle East and Africa, led by United Arab Emirates and South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for natural and clean-label ingredients

In the Middle East and Africa markets, growing consumer awareness about synthetic additives has intensified regulatory scrutiny. A study conducted in the UAE found that 61% of residents consider all food additives to be harmful, while only 26.7% possess a clear understanding of these additives. This knowledge gap presents an opportunity for natural ingredient suppliers to educate consumers and secure premium pricing. Companies are addressing this through biotechnology partnerships. For instance, DSM-Firmenich has collaborated with Interstellar Lab to improve botanical ingredient production. Their AI-powered biofarming platforms are designed to optimize resource utilization and stimulate the production of specific molecules. This movement is further supported by regulatory changes, such as South Africa's upcoming 2025 food additive regulations. These regulations prioritize Good Manufacturing Practices, limit the use of additives to essential levels, and prohibit certain substances in infant foods. Additionally, Symrise is leading a supply chain sustainability initiative focused on regenerative agriculture. This program aims to enhance biodiversity, increase carbon sequestration, and ensure a reliable supply of raw materials. At the same time, GSO standards and national authorities like the SFDA are enforcing the need for substantiated natural claims. While this creates entry barriers, it also rewards authentic innovation.

Growth of functional foods, beverages, and wellness products

The African energy drinks market is experiencing rapid growth, making it the fastest-growing segment in the soft drink industry. Innovation remains a key driver, with trends focusing on reformulated products featuring low-sugar content, reduced caffeine, and added nutrients such as B vitamins, amino acids, and minerals. Notably, 69% of consumers are willing to pay a premium for these functional benefits. Localization strategies are also critical, incorporating African botanicals like umhlonyane (African wormwood) and region-specific flavor adaptations, providing opportunities for flavor houses to create culturally relevant formulations. Regulatory frameworks for functional claims vary across MEA markets, with entities like Dubai Municipality and SFDA implementing specific guidelines for health supplement registration and nutritional labeling. The integration of traditional wellness practices with modern functional food science positions the Middle East and Africa region as a key growth area for flavor innovation, particularly in immunity, digestive health, and protein enhancement applications.

Increasing popularity of personalized and customized flavor/fragrance solutions

Consumers are showing a strong preference for oil-based fragrances due to their longevity and rich oriental notes, such as oud, musk, amber, and exotic flowers, creating significant opportunities for customization platforms. Technology is a key enabler in this personalization trend. For example, Givaudan's Bloomful platform measures and defines fragrance 'bloom' moments while enhancing compositions and ingredients using captive molecules. This technological innovation also extends to flavor applications. Symrise leverages digital tools and AI to modulate tastes, reducing sugar, salt, and fat content while improving plant-protein flavor profiles through its ProtiScan processes and PropheSY prediction tools. Regulatory compliance remains a critical factor, particularly with halal certification requirements across GCC markets. SGS Gulf Ltd provides certifications aligned with GSO standards and country-specific regulations, ensuring personalized products can effectively cater to Muslim-majority consumer segments while adhering to religious compliance [1]Source: SGS, "Halal Certification – Middle East", sgs.com.

Expansion of processed food and beverage industry

The expanding market is boosting demand for flavor and fragrance applications across beverages, dairy, and ready-to-eat products. Companies are responding to this demand, for example, Brenntag Specialties has strengthened its distribution partnerships through an exclusive agreement with Silesia Flavors, enabling the distribution of flavors for confectionery, bakery, dairy, savory, and beverages in Saudi Arabia. Regional manufacturers are also scaling up their operations. Egypt's Aromatic Flavours and Fragrances S.A.E., established in 1969, now produces flavors in various forms, including powder, liquid, encapsulated, and emulsion, catering to domestic and international markets such as the EU, USA, Latin America, and the Middle East. The regulatory framework is also fostering growth, with harmonized GCC standards and national authorities like the SFDA implementing food establishment regulations. These regulations enhance consumer transparency while creating opportunities for flavor and fragrance suppliers that comply with the standards.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations on the use of additives | -0.8% | Gulf Cooperation Council countries, South Africa | Short term (≤ 2 years) |

| Volatility in raw material prices | -0.6% | Global supply chains affecting all Middle East and Africa markets | Short term (≤ 2 years) |

| Challenges in scaling up new sustainable or biotechnology-derived ingredients | -0.4% | Technology hubs in United Arab Emirates and South Africa | Medium term (2-4 years) |

| Rising health concerns over the use of artificial flavoring | -0.5% | Urban markets across Middle East and Africa, particularly United Arab Emirates and Saudi Arabia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent regulations on the use of additives

Food Compliance International reports that the Saudi Food and Drug Authority will implement comprehensive regulations between November 2024 and July 2025 [2]Source: Food Compliance International, “SFDA Issues Three New Regulations to Promote Healthy Community Nutrition,” foodcomplianceinternational.com. These regulations require food establishments to disclose calorie counts, allergen information, caffeine content, and identify high-sodium meals. These efforts align with Saudi Vision 2030's objectives to reduce sugar, salt, and unhealthy fats, driving reformulation strategies that impact flavor and fragrance applications. In South Africa, food additive regulations effective in 2025 will enforce strict purity standards, Good Manufacturing Practices, and limit additives to essential levels while banning certain substances in infant foods, as noted by GPC. These regulatory changes increase compliance costs and extend product development timelines. For example, in Ghana, 37% of processed foods were found unregistered with authorities, and 71% contained potentially hazardous additives. Companies must address varying national implementations of GSO standards, such as the UAE's requirement for Dubai Municipality registration, Saudi Arabia's SFDA compliance enforcement, and distinct approval processes in other GCC markets. Additionally, GSO standards regulate packaging materials to prevent harmful constituent migration or changes to organoleptic properties, significantly affecting flavor and fragrance delivery systems, as outlined by the Packaging Law.

Volatility in raw material prices

In the first half of 2024, Madagascar exported 4,300 metric tons of vanilla, however, an oversupply caused a decline in extract prices. Despite the abundant availability of vanilla, government measures such as enforcing minimum prices, restricting exports, and implementing customs regulations (allowing exports only for beans priced between USD 50-70 per kilogram) have introduced additional challenges to the supply chain. This situation highlights how regulatory actions in exporting countries can disrupt price stability, even when supply and demand fundamentals remain steady. Climate change exacerbates this volatility by impacting the availability of natural ingredients. To address these risks, companies like Symrise are implementing sustainability initiatives within their supply chains, conducting long-term risk assessments on water, labor access, climate, and land with their fruit and vegetable suppliers. Furthermore, currency fluctuations create difficulties for importers in the MEA region, as many natural ingredients are priced in USD or EUR, while transactions are conducted in local currencies. To mitigate these challenges, companies are turning to vertical integration strategies and biotechnology solutions. For instance, Estée Lauder has invested in a Belgian BioTech Hub that produces bio-based raw materials through fermentation, aiming to reduce reliance on traditional supply chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Natural Ingredients Drive Premium Positioning

Natural ingredients commanded 42.83% share of the Middle East and Africa flavor and fragrance market in 2025, and the segment is forecast to grow at 6.78% CAGR through 2031. This leadership reflects premium positioning and rapid biotech cost reductions that narrow price gaps versus synthetics. Synthetic molecules still anchor cost-sensitive products, especially those needing precise isoforms not yet feasible via bio-routes. Nature-identical inputs bridge the divide by replicating exotic notes without biodiversity strain. Lallemand’s entry into yeast-based aroma production highlights fermentation’s role in delivering volume at scale. Manus Bio and Givaudan’s cell-factory deal further enhances sustainable production avenues. Halal certification frameworks across GCC markets reward natural sourcing, driving brand portfolios toward botanically verified claims.

Industry innovators apply precision fermentation to unlock minor terpenes once limited by low plant yields, improving cost efficiency without deforestation. Regulatory agencies acknowledge biotech-derived naturals as non-GMO under specific process definitions, smoothing import approvals. Price premiums are expected to persist, given consumer willingness to pay more for “real” botanical stories that carry social-impact assurances. For suppliers, transparency tools such as blockchain traceability become critical for substantiating origin, potency, and ethical handling, all of which reinforce the dominance of natural profiles in the Middle East and Africa flavor and fragrance market.

By Form: Liquid Dominance Challenged by Powder Innovation

In 2025, liquid formulations hold a 33.78% market share, valued for their easy integration and immediate sensory effects across applications such as beverages and personal care. However, powder formulations are experiencing rapid growth, with a 6.56% CAGR projected through 2031. This growth is driven by advancements in micro-encapsulation technologies, which improve stability, extend shelf life, and enable controlled release. The difference in growth rates highlights changing application needs and technological progress, going beyond simple cost factors. Micro-encapsulated formats lead innovation by providing environmental protection and precise delivery for specific applications.

The powder segment's growth is fueled by advancements in encapsulation technologies. For instance, Symrise has developed Symcap BP pea-protein capsules, a biodegradable and vegan alternative to traditional gelatin-based formulations. These innovations address sustainability concerns and dietary preferences, particularly in MEA markets where halal and vegan requirements overlap. On the other hand, liquid formulations benefit from their immediate application advantages, especially in the beverage industry, where Africa's energy drinks market is growing at a 10.06% CAGR, sustaining demand for liquid flavor systems. Regulatory frameworks, such as GSO standards, support both formats by ensuring packaging material compatibility. However, powder formulations may offer an edge in regions with challenging storage and transportation conditions. The competitive landscape indicates that both formats will continue to coexist, with powders gaining traction in applications requiring stability and controlled release, while liquids remain dominant in areas needing immediate impact.

By Application: Beverages Lead While Personal Care Accelerates

In 2025, the beverages segment holds a 25.06% market share, driven by the strong growth of Africa's energy drinks market and increasing consumer demand for functional formulations. The consumption of beverages is increasing, due to which the popularity of flavors is increasing. According to the Government of Canada data, projected per capita expenditure on non-alcoholic beverages in the UAE by 2025 was USD 236.8 . These formulations often include natural botanicals and locally inspired flavors. The personal care and cosmetics sector is experiencing rapid growth, with a 6.29% CAGR projected through 2031. This growth is primarily attributed to the rising demand for halal cosmetics, expected to grow by 15% between 2023 and 2030, and a cultural preference for premium fragrances. Food applications continue to see stable demand across categories such as dairy, bakery, confectionery, and meat. On the other hand, pharmaceutical applications represent a specialized niche, facing strict regulatory requirements. Other applications, including household care and industrial uses, exhibit moderate growth potential.

Advancements in natural and organic formulations are driving the beverages segment's progress. Notably, 69% of African consumers are willing to pay a premium for functional benefits like improved immunity and digestive health. While pharmaceutical applications encounter complex regulatory challenges, they also present high-value opportunities, particularly in halal-certified formulations. Malaysian standards play a key role in ensuring ingredient compliance across Middle Eadt and Africa markets. Regulatory requirements differ by application, for instance food and beverage sectors are regulated by the SFDA and Dubai Municipality, while cosmetics must adhere to both safety standards and cultural certifications, with halal compliance being essential for broader market accessibility.

Geography Analysis

In 2025, South Africa holds a significant 35.11% market share, leveraging its strong manufacturing infrastructure, access to botanical raw materials, and a well-structured regulatory framework that facilitates both local production and exports. Companies such as Scent Lab, which offers over 210 fine generic fragrance oils and collaborates with global suppliers, reinforce South Africa's role as a regional hub. The country's regulatory environment, including the upcoming 2025 food additive regulations, ensures consumer safety while fostering market growth. Well-established supply chains connect South Africa to global botanical sources, meeting the demands of consumers who increasingly prefer premium formulations in food, beverages, and personal care products.

Saudi Arabia is the fastest-growing market in the region, with a projected 6.34% CAGR through 2031. This growth is driven by Vision 2030 initiatives, large-scale infrastructure investments, and shifting consumer preferences toward premium products. The SFDA's updated food establishment regulations enhance market transparency and create opportunities for compliant suppliers. Cultural factors, such as increased perfume usage during Ramadan and a preference for long-lasting, rich oriental oil-based fragrances, further support market expansion. Global companies are strengthening their presence, as seen with Symrise's EUR 1 million innovation center in Dubai and DSM-Firmenich's exhibition in Riyadh.

The Middle East and Africa region encompasses a variety of markets with distinct growth trends and regulatory frameworks. While the UAE and Morocco are established markets, sub-Saharan Africa offers emerging opportunities. In the UAE, Dubai Municipality simplifies the registration process for food and cosmetic products while maintaining high safety standards. Morocco capitalizes on its natural ingredient resources, exemplified by Syensqo's acquisition of Azerys, a rosemary extraction specialist that collaborates with local cooperatives. Nigeria's energy drinks market is experiencing rapid growth, with a projected 14.14% CAGR, while Egypt's Aromatic Flavours and Fragrances S.A.E. serves both domestic and international markets. Regulatory frameworks vary widely, with GCC countries benefiting from unified GSO standards, while African markets require tailored compliance strategies due to their distinct national regulations.

Regulatory Landscape

Across the Middle East and Africa, flavor and fragrance formulation and trade are shaped by a mix of GCC harmonized standards and country-level enforcement for food additives, flavorings, labeling, and claims. Within the GCC, the Gulf Standardization Organization (GSO) issues technical regulations used by national authorities, including the Saudi Food and Drug Authority (SFDA), to set permitted substances and use conditions. GCC alignment is often anchored to international safety assessments (JECFA/Codex). A notable anchor is GSO 2834:2025, approved on 14 October 2025, which formalizes food category classification for food additives and supports more consistent interpretation of category-based limits when compiling ingredient dossiers.

In Saudi Arabia, the SFDA is a key gatekeeper for imported and locally produced food and beverage products, including compliance documentation tied to additive and flavoring use, labeling, and establishment requirements. Companies commonly manage standards access and conformity work through SFDA channels such as the Mwasfah portal, while also aligning to specific GSO technical regulations such as GSO 707:2023 for flavorings permitted for use in foodstuffs and ongoing updates linked to the Gulf technical regulation framework for additives (including GSO 2500:2025 in project/current update cycles). For suppliers, this increases documentation demands (identity, purity, specifications, and claims substantiation) and requires managing differences in national implementation and registration workflows, even when the underlying GCC standard is shared.

Value Chain Analysis

The Middle East and Africa flavor and fragrance value chain starts with upstream feedstocks, including petrochemical aroma chemicals and natural botanicals such as vanilla and regional botanicals. This is followed by extraction, distillation, fermentation and biotech production, compounding, and application development. Global flavor and fragrance houses and regional specialists typically run formulation, blending, and sensory and application labs close to demand centers, then supply finished flavors, fragrance compounds, and encapsulated systems to food and beverage manufacturers, as well as personal care and cosmetics producers, and, to a smaller extent, pharmaceutical formulators. Distribution relies heavily on import channels and regional hubs, with the UAE serving as a major consolidation and re-export point through logistics nodes such as Jebel Ali.

Midstream execution is increasingly shaped by compliance and logistics capabilities, including halal and ingredient traceability documentation, stability management for heat-sensitive naturals, and local technical service for rapid reformulation in response to additive limits and labeling requirements. Disruption risk has also been highlighted by shipping instability around key maritime corridors, including rerouting when transit constraints emerge, which increases lead times and encourages higher local inventory and regional distribution partnerships. A June 2026 example is Solevo Group being appointed as an authorized distribution partner for IFF in West and Central Africa for selected food and beverage flavor solutions, reflecting a shift toward closer-to-customer stocking, localized logistics, and shorter replenishment cycles for manufacturers.

Competitive Landscape

In the Middle East and Africa, the flavor and fragrance market showcases a high level of fragmentation. This landscape presents opportunities for both global giants and regional experts to carve out their market share using distinct strategies. Major global players, such as DSM-Firmenich, Givaudan, and Symrise, harness their technological prowess and substantial research and development investments to craft innovative solutions. In contrast, regional firms tap into their deep understanding of local markets and cultural nuances, catering to specialized segments.

Companies are increasingly focusing on sustainability, halal compliance, and localization. Many have set up regional innovation hubs and forged alliances with local suppliers, ensuring they source authentic ingredients and resonate culturally. Technology adoption emerges as a key differentiator in this competitive arena. For instance, Symrise has integrated AI and digital platforms, like Symvision AI and Scenturion, to predict tastes and tailor products to regional preferences. There's a burgeoning demand for biotechnology-sourced natural ingredients, bespoke fragrance solutions, and health-oriented food applications, especially among the health-conscious demographic.

Noteworthy disruptors are making waves, such as Manus Bio, a biotechnology firm, collaborating with industry stalwarts to bring sustainable ingredients to market. Meanwhile, regional players like AlUla Peregrina Trading Company are making headlines by harnessing exclusive local botanicals. They've successfully partnered with luxury brands, including Cartier, to make their mark on the global stage. Navigating this competitive landscape isn't without its challenges. Regulatory compliance plays a pivotal role, with many companies prioritizing halal certifications and aligning with GSO standards. These moves not only broaden their access to the expansive MEA markets but also ensure they operate efficiently amidst varied regulatory landscapes.

Middle East And Africa Flavor And Fragrance Industry Leaders

-

International Flavors & Fragrances Inc.

-

Symrise AG

-

Givaudan SA

-

Kerry Group PLC

-

DSM-Firmenich

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Localization of creation, application, and regulatory-support capabilities is where opportunity is most concentrated across the region, as customers seek faster reformulation for additive rules, clean-label positioning, and culturally aligned profiles, including halal-compliant portfolios. The market has momentum behind regional innovation footprints: Robertet inaugurated a Middle East and Africa regional headquarters at Dubai Science Park in February 2026, adding a Fragrance Creative Area and a Flavour Hub, and ADM opened a flavor creation facility in Johannesburg in April 2026 to serve multiple African sub-regions. These moves increase in-market co-creation capacity and shorten iteration cycles tied to climate, process conditions, and local taste preferences.

Supply security for natural ingredients and functional systems also creates whitespace, supported by vertical integration and local food-industry capacity build-out. Nexira acquired Morocco-based carob ingredients producer Keragum in July 2026, strengthening access to a regional natural hydrocolloid input and improving traceability for customers targeting simpler labels. On the demand side, downstream investment in food manufacturing is pulling through demand for flavors, masking systems, and compliant additive solutions, illustrated by Barakat Group starting construction of an AED 150 million baby food manufacturing facility in KEZAD in February 2026 and Saudi-listed Modern Mills announcing plans to commence work on an SAR 87.7 million food-ingredients factory in western Saudi Arabia in Q3 2026. Together, these developments point to demand for halal-ready, documentation-rich formulations and stable access to botanicals and functional ingredients under GCC and country-specific compliance workflows.

Recent Industry Developments

- February 2026: dsm-firmenich opened a new office and state-of-the-art application center in Nairobi, Kenya, to support customers across the East African region. The site strengthens local application development and troubleshooting for food, beverage, and personal care projects where reformulation speed and sensory alignment are critical.

- April 2025: International Flavors & Fragrances Inc. inaugurated the Scent Dubai Creative Center with a Perfumery Art Studio at Dubai Science Park. The 2,000-square-meter facility increases in-region fragrance creation and customer collaboration capacity, supporting faster customization for premium and culturally specific scent profiles.

- November 2024: Givaudan opened a 42,000-square-foot Innovation Hub in Dubai to serve its South Asia, Middle East, and Africa (SAMEA) markets, including laboratories and a Consumer and Sensory Insights center. The investment expands local testing and insights capabilities that help translate regulatory-driven reformulation and wellness positioning into market-ready flavor and fragrance concepts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of flavor and fragrance ingredients sold for use in finished products across the Middle East and Africa, where flavors are mainly used in food and beverages and fragrances are used in personal care, home care, and related uses.

Scope exclusions: This sizing does not count finished consumer goods pricing and focuses only on ingredient value at the flavor and fragrance supply level.

Segmentation Overview

-

Type

- Synthetic

- Natural

- Nature-Identical

-

Form

- Powder

- Liquid

- Micro-Encapsulated

-

Application

-

Food and Beverages

- Dairy products

- Bakery and Confectionery

- Snacks and Savory Products

- Meat and Meat Alternatives

- Beverages

- Other Types

- Beauty and Personal Care

- Pharmaceuticals

- Other Applications

-

Food and Beverages

-

Geography

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to frame the demand pool, country context, and input ranges before interviews started. We reviewed public sources such as UN Comtrade trade statistics, national statistics offices in key MEA countries, central bank releases for exchange rates and inflation context, and food regulator and standards bodies publications (for example, guidance that affects labeling and ingredient use).

To keep assumptions practical, we also used company annual reports, investor presentations, and reputable press coverage to understand capacity moves, distribution expansion, and application focus across food, beverages, and personal care. Where needed, paid databases that cover company financials and intelligence, patent databases, and import and export shipment-level records were used to cross-check supplier presence and directional volume movement. These examples are not exhaustive, and many other public sources were referred to for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary discussions were run with ingredient suppliers, distributors, brand-side formulation and procurement teams, and industry consultants who track food and personal care inputs across MEA. We used these inputs to confirm what is actually bought in the region, how pricing is moving by application, and which countries are showing faster adoption of natural and clean label solutions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 15% | |

| Mid tier: 49% | Functional/Unit leaders: 30% | |

| Smaller Players: 21% | Managers: 55% |

Market-Sizing & Forecasting

The core model starts with a top-down build where production, import and export signals, and country level consumption patterns are used to reconstruct the MEA demand pool for flavor and fragrance ingredients, and then it is split into realistic application baskets. To keep the totals grounded, selective bottom-up approximations were used as checks, mainly through sampled supplier and distributor revenue ranges and simple ASP times volume sanity tests for a few high-usage applications.

Inputs that mattered in this market included packaged food and beverage output trends, personal care and home care category momentum, the mix shift between synthetic and natural ingredients, typical dosage rates in key formulations, and USD pricing movement tied to FX and raw material cycles. Forecasting was built using scenario analysis supported by expert views, where the variables above were stepped forward by country and then rolled up, and any gaps in country data were handled by using proxy indicators from similar markets and then re-checked through interviews before finalizing.

Data Validation & Update Cycle

Validation was done through repeated variance checks between the model outputs and independent signals like trade direction, packaged food production trends, and country level demand narratives from interviews. When a number looked out of line, the assumptions behind application mix, price progression, or country weights were reviewed again and experts were re-contacted if the gap remained.

Before sign-off, the work goes through multi-step analyst review so that arithmetic, currency conversions, and logic consistency are confirmed. The report is refreshed annually, and interim updates are triggered when material events occur, such as regulation shifts, major capacity additions, or sharp currency moves. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Middle East and Africa Flavor and Fragrance Market Size Compared With Other Published Estimates

Published values for this market often do not match each other because each publisher chooses its own boundary, base year, and pricing approach, and then applies different ways to treat country coverage inside MEA. Differences also show up when one estimate leans more toward flavors tied to food volumes, while another gives more weight to fine fragrance and personal care value.

By tracking application-level demand indicators and refreshing FX and price assumptions country by country, Mordor Intelligence keeps the MEA total tied to ingredient value only, while some estimates blend in broader end-user scopes or use a different base-year conversion that lifts the headline number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.20 B (2025) | |

| Global Consultancy A | USD 3.27 B (2025) | Uses a broader regional and category breakup that can pull in adjacent fragrance and end-use value pools, and it also runs a longer forecast horizon that may embed a different price and mix trajectory from the start year. |

| Regional Consultancy B | USD 2.76 B (2023) | Uses a different base year and study window, which can shift the result due to FX timing and inflation effects, and the scope framing by end-user industry can lead to double counting if ingredient and finished product boundaries are not kept separate. |

The spread in the table is mainly explained by scope boundaries, base-year selection, and how pricing and currency are handled across countries. With clear inclusion rules and repeatable checks on demand signals and pricing inputs, our estimate stays easier to trace back to real application consumption and to update as market conditions change.

Key Questions Answered in the Report

How large is the flavor and fragrance market in the Middle East and Africa in 2026?

The flavor and fragrance market size reached USD 2.34 billion in 2026.

What is the projected CAGR for flavor and fragrance demand in Saudi Arabia?

Saudi Arabia is forecast to grow at a 6.34% CAGR through 2031.

Which ingredient type holds the largest share of regional sales?

Natural ingredients commanded 42.83% of 2025 revenue.

What consumer trend is accelerating personal-care fragrance growth?

Demand for halal-certified, personalized scents is pushing personal care applications at a 6.29% CAGR.

Page last updated on: