Greaseproof Paper Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

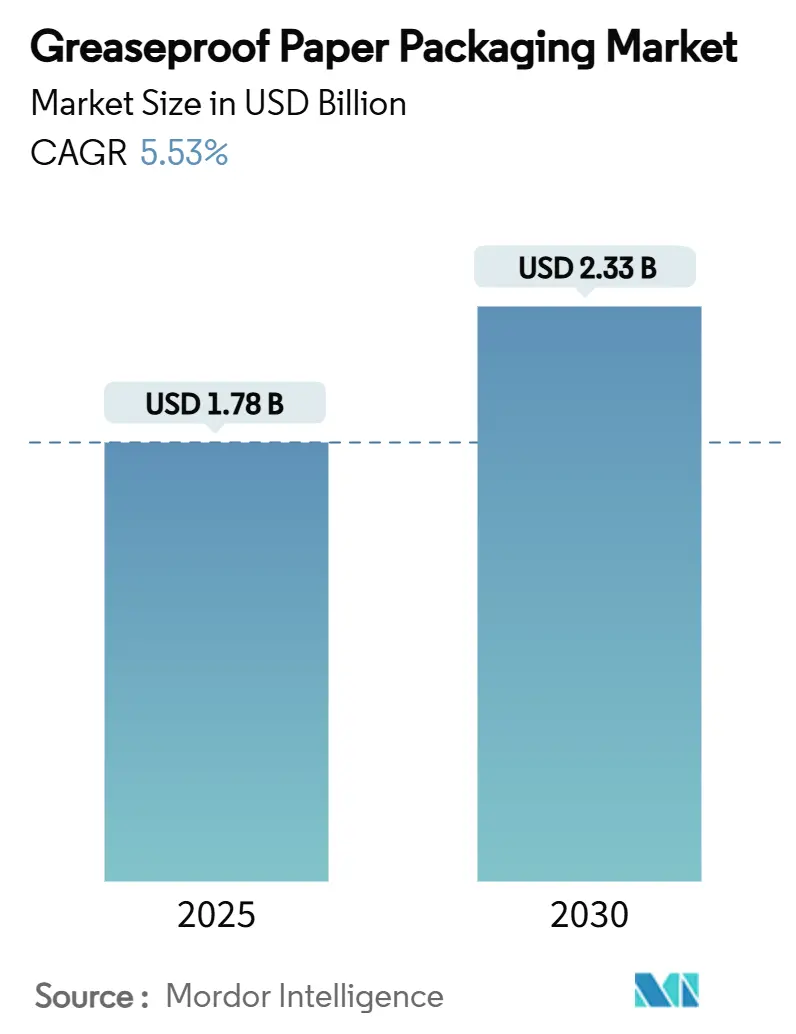

| Market Size (2025) | USD 1.78 Billion |

| Market Size (2030) | USD 2.33 Billion |

| Growth Rate (2025 - 2030) | 5.53% CAGR |

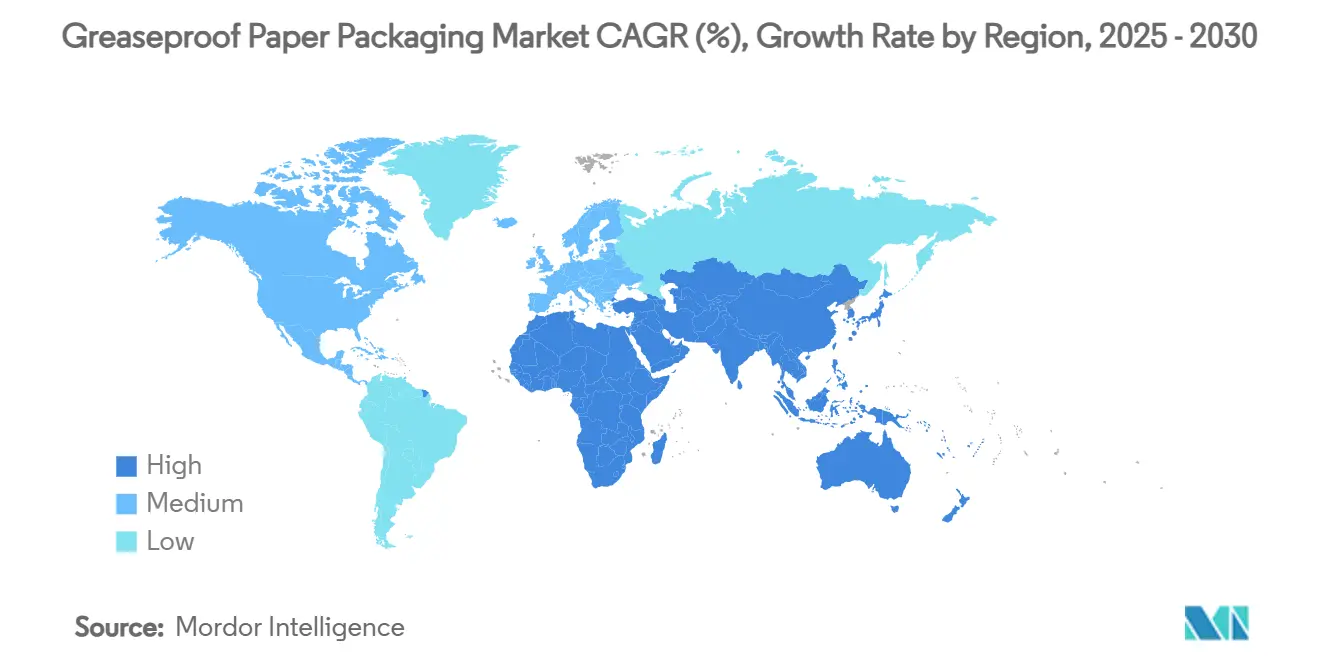

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Greaseproof Paper Packaging Market Analysis by Mordor Intelligence

The greaseproof paper packaging market size stands at USD 1.78 billion in 2025 and is forecast to reach USD 2.33 billion by 2030, translating into a 5.53% CAGR across the period. Strong replacement demand for PFAS-free barrier papers, combined with surging quick-service restaurant (QSR) volumes and e-commerce packaging needs, keeps the greaseproof paper packaging market on a steady mid-single-digit growth path. Manufacturers that scale nanocellulose, chitosan and other bio-based coatings early capture pricing premiums while lowering regulatory risk. Vertically integrated players blunt raw-material price swings by locking in certified wood pulp contracts, whereas converters without captive fiber rely on short-term sourcing and absorb wider cost volatility. Regional growth differentials remain pronounced: Asia-Pacific’s outlet expansion and app-based food delivery orders underpin the largest absolute volume gains, while North America and Europe focus on rapid PFAS compliance and recyclability upgrades. Competitive intensity rises as both incumbent European groups and cost-focused Asian suppliers race to retrofit Yankee cylinder lines and roll out unbleached substrates.

Key Report Takeaways

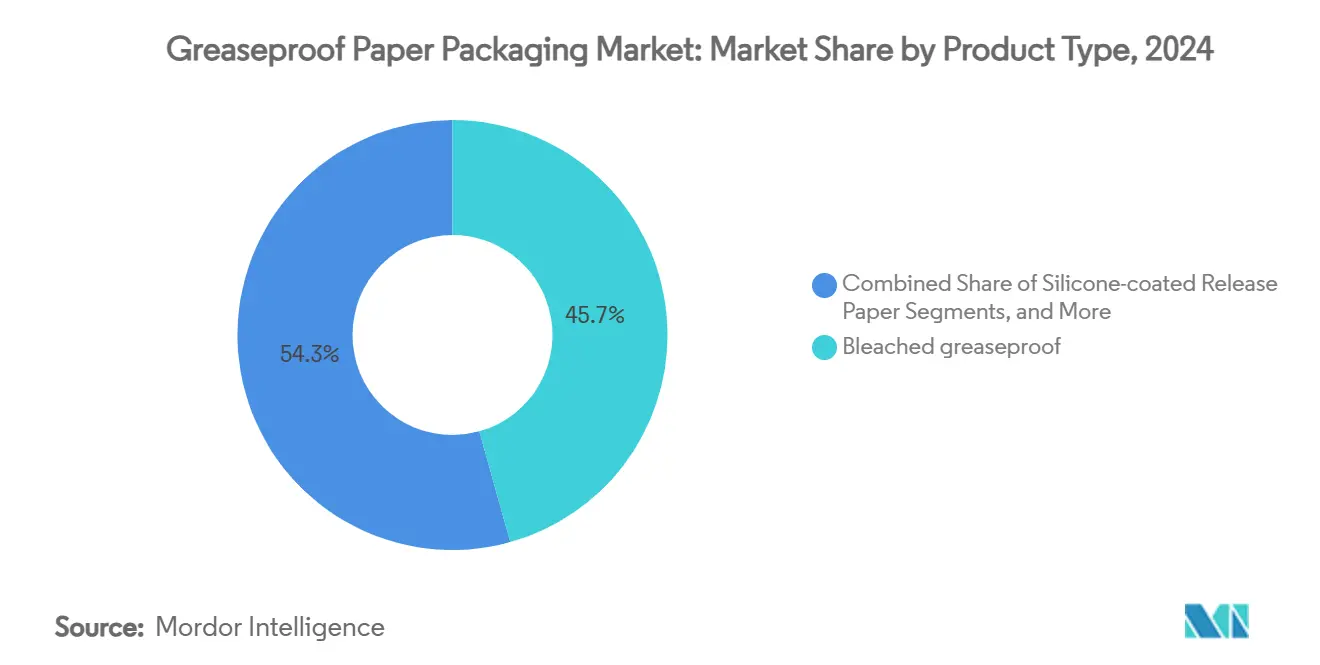

- By product type, bleached grades captured 45.67% of the greaseproof paper packaging market share in 2024.

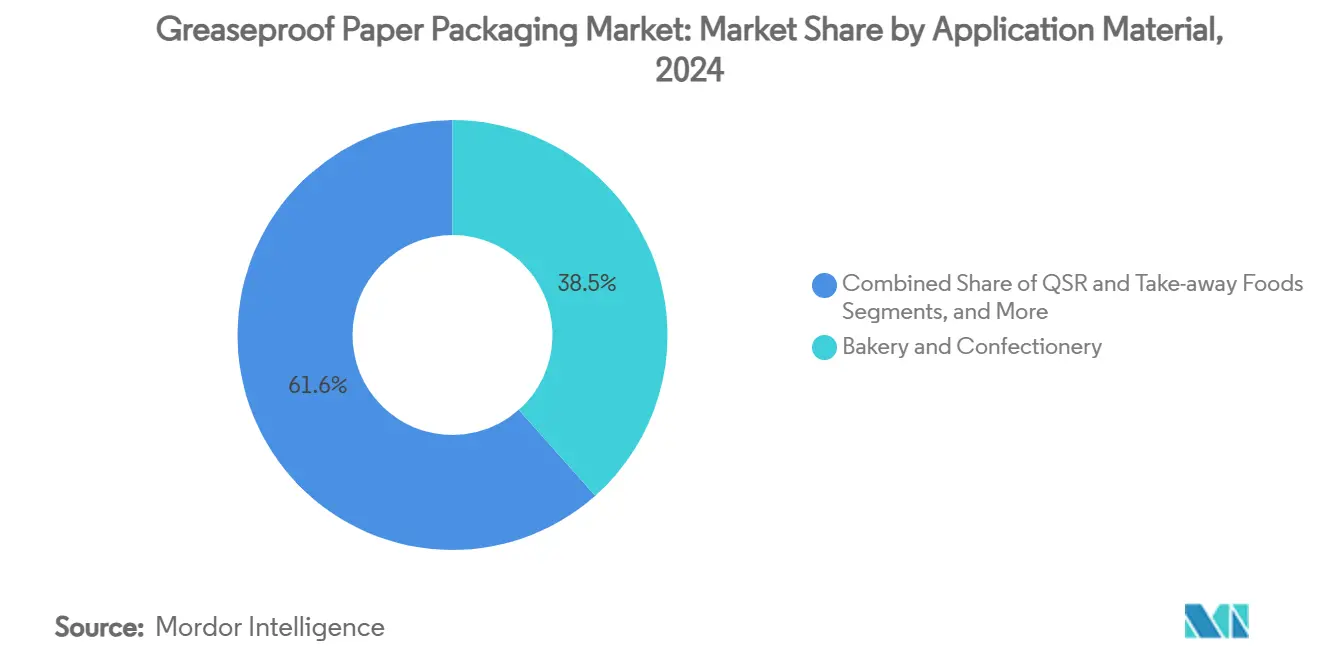

- By application, the greaseproof paper packaging market size for the QSR and take-away segment is projected to grow at 10.80% CAGR between 2025-2030.

- By geography, Asia-Pacific captured a 36.75% of the greaseproof paper packaging market share in 2024.

Global Greaseproof Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for PFAS-free food contact papers | +1.8% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Growth of QSR takeaway formats in emerging Asia | +1.2% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| E-commerce shift to curb plastic void-fill with paper | +0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| EU "Single-Use Plastics" rules tightening in 2026 | +0.7% | Europe, with regulatory spillover to other regions | Short term (≤ 2 years) |

| Commercial bakeries standardising silicone-free liners | +0.6% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Rapid uptake of microwaveable, dual-ovenable paper trays | +0.4% | North America and Europe, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for PFAS-Free Food Contact Papers

Regulators in the United States and the European Union have eliminated or sharply curtailed PFAS in food wrappers, forcing an industry-wide pivot to alternative barriers.[1]U.S. Food and Drug Administration, “FDA, Industry Actions End Sales of PFAS Used in US Food Packaging,” fda.gov The FDA ruled in March 2025 that 35 prior food-contact notifications are no longer effective, setting a June 2025 sell-through deadline, while the EU caps PFAS at 25 ppb from August 2026. Nanocellulose multilayer coatings replicate fluorochemical grease resistance without impairing recyclability, yet retrofitting existing coaters to handle bio-based slurries strains capex budgets. Temporary supply gaps emerge as lines are re-commissioned, but early movers secure multi-year supply contracts with global QSR chains. The regulatory timeline effectively future-proofs barrier investments and sets a performance baseline that ripples into other regions within two to four years.

Growth of QSR Takeaway Formats in Emerging Asia

China’s food-service revenue jumped 20.4% year-on-year to CNY 5.2 trillion (USD 720 billion) in 2023, signalling the scale at which disposable dining drives the greaseproof paper packaging market. Extended delivery times and higher-oil menu profiles require papers with stronger grease hold-out, allowing premium products to command higher margins than generic wraps. As Indonesia, Vietnam and the Philippines replicate China’s QSR expansion, converters with region-wide distribution and certified food-safety systems outflank fragmented local rivals. The driver’s long-term nature lets suppliers amortise new coating assets over larger volume bases, but puts pressure on pulp logistics as demand clusters near coastal megacities.

E-Commerce Shift to Curb Plastic Void-Fill with Paper

Online retailers increasingly replace plastic air pillows with multifunctional, grease-resistant kraft pads to reduce single-use plastic footprints. Papers designed for consumer electronics and cosmetics shipping must manage both oil and moisture migration, prompting suppliers to integrate mineral pigments or multilayer bio-based coatings that survive parcel sorting belts. Amcor’s AmFiber Performance Paper retains over 80% fibre in standard repulping trials while delivering oxygen and water-vapour barriers that rival plastic mailers.[3]Amcor, “AmFiber Performance Paper Packaging,” amcor.com This non-food channel diversifies end-use risk, but paper makers face tougher tear-strength and puncture-resistance targets than in bakery wraps, nudging them toward fibre-blend optimisation and wet-end strengthening chemistries.

EU "Single-Use Plastics" Rules Tightening in 2026

February 2025 saw the Packaging and Packaging Waste Regulation enter force, demanding that all EU-placed packaging become recyclable by 2030 and imposing interim PFAS limits by 2026. Harmonised recyclability icons and minimum recycled-content thresholds raise compliance costs for smaller sheet-fed converters but unlock scale efficiencies for pan-regional suppliers. Because fibre loops already enjoy high recovery rates in northern Europe, greaseproof paper substitutes for multilayer plastics in niche frozen-food and pet-food sachets. Large brand owners negotiate long-term offtake agreements to secure future-proof inventory before 2026, providing revenue visibility that offsets the expenditure on barrier R&D.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of bleached soft-wood pulp | -0.8% | Global, with acute impact in Europe and North America | Short term (≤ 2 years) |

| Capital intensity of upgraded Yankee cylinder machines | -0.5% | Global, concentrated in developed markets | Medium term (2-4 years) |

| PFAS substitution causing barrier-performance gaps | -0.3% | Global, most acute in high-performance applications | Short term (≤ 2 years) |

| Fragmented Asian converters lacking global FSSC 22000 | -0.2% | APAC, with quality assurance spillover effects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Bleached Soft-Wood Pulp

Wood-pulp price swings hit a Producer Price Index reading of 219.835 in May 2024, elevating cost pressures just as converters shoulder PFAS retooling expenses. Bleached grades needed for food contact have narrower supplier pools because optical brightness and microbiological thresholds tighten quality specs. European mills feel the squeeze first, given high Nordic log costs and energy premia, forcing frequent surcharge clauses in quarterly contracts. Vertically integrated Scandinavian groups absorb spikes better than Asian independents dependent on spot pulp imports. Some plants deploy biobleaching enzymes to trim chlorine dioxide dosage, but process tuning is gradual and capex heavy.

Capital Intensity of Upgraded Yankee Cylinder Machines

Transitioning from fluorochemical size-presses to multilayer curtain coaters requires wider steel Yankee dryers capable of handling higher moisture loads and alternative chemistries. Toscotec’s induction-heated models cut steam use yet cost significantly more than cast-iron predecessors, pushing payback horizons beyond five years for mid-tier mills. Companies like Billerud earmarked SEK 1.4 billion (USD 0.15 billion) to upgrade North American lines, but smaller converters defer investment, risking customer attrition when PFAS deadlines bite.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Natural Variants Accelerate Despite Bleached Dominance

Bleached grades command just under half of 2024 revenue thanks to their bright optics and legacy qualifications across global food-service chains. Even so, natural and unbleached variants post the fastest 9.30% CAGR because regulators and consumers frown on chlorine bleaching, driving purchasers to visibly brown wraps that signal low chemical intervention. In currency terms, unbleached papers move faster in Europe’s bakery aisle, whereas North American QSR chains maintain white aesthetics until migration-testing on brown stock is finalised. Silicone-coated release lines serve niche dough-sheeting and pastry applications where repeated oven cycles demand elevated temperature limits, and these products retain stable single-digit growth despite PFAS withdrawals. Quilon and other fluoro-coated grades are already in managed decline, with purchasers transitioning contracts to bio-based options and running down inventories before statutory cut-off dates.

The evolving mix pressures pulp blends: bleached eucalyptus short fibre gives smoothness, while unbleached northern softwood raises tensile for burger-wrap folds. Mills therefore juggle furnish recipes and de-inked pulp streams to hit opacity targets without over-calendering. LINTEC’s 2020 unbleached glassine launch illustrates how Japanese converters combine high-density regeneration with brown tonality to meet grease hold-out while sidestepping chlorine dioxide bridges.[2]LINTEC, “Release of Unbleached Glassine Papers That Are Neither Bleached nor Colored,” lintec-global.com Research into chitosan barrier layers shows promising oil-kit readings but struggles with scale-economies because crustacean-shell feedstock is seasonal. Over the forecast horizon, suppliers that master tandem-coater sequencing—bio-polymer prime plus mineral-filled top—secure margin resilience against raw-material cost swings.

By Application: QSR Momentum Reshapes Demand Patterns

Bakery and confectionery absorbed 38.45% of 2024 volumes, spanning croissant sheeting, muffin cups and sugar-sprinkled pastry bags that require low kit-rating yet high release. That installed base grows steadily with artisanal formats in Europe but cedes share to QSR and take-away as app-based ordering lifts unit volumes in Asia and Latin America. The QSR cohort enjoys a robust 10.80% CAGR, pushing suppliers to certify migration limits under both boiling-water simulants and hot-fat conditions, a dual prerequisite for fried chicken clamshells. In many emerging markets, franchisees require QSR packaging volumes to keep pace with menu expansion, prompting investments in local coating capacity.

Dairy and fats rely on micro-perforated wraps for butter and cheese blocks where controlled water-activity balance matters as much as grease hold-out. Meat, poultry and seafood require wet-strength and antifog treatments, placing specialty greaseproof paper packaging at the premium end of the application spectrum. E-commerce-led protective wraps infiltrate the "industrial and other" bucket, yet they already account for notable incremental tonnage, buffering mills during food-service downturns. Microwaveable and dual-ovenable paper trays straddle food and household segments, tapping into ready-meal trends among time-pressed urban consumers in developed markets.

Geography Analysis

Asia-Pacific accounted for 36.75% of global revenue in 2024 and is on track to post an 8.50% CAGR through 2030. Rapid QSR store openings, coupled with booming takeaway apps, translate restaurant revenue gains directly into greaseproof liner demand. Chinese mills such as Asia Pulp & Paper run high-speed Yankee machines close to bamboo and acacia plantations, lowering delivered fibre costs. Regional innovation is visible in unbleached grades meeting Japanese and Korean retail aesthetics and in low-basis-weight liners for India’s street-food channels, proving that the greaseproof paper packaging market adapts swiftly to local culinary requirements. Still, certification gaps persist: multinational QSR chains restrict sourcing to converters with full HACCP and FSSC 22000 validation, limiting participation among thousands of small Asian sheet-cutting plants.

North America represents a mature but strategically pivotal enclave: the FDA’s complete PFAS phase-out creates a hard compliance deadline, favouring domestic mills with already validated bio-barrier inventories. Brands rapidly de-risk supply by dual-sourcing unbleached burger wraps from Canadian and US sites, shrinking lead times and trimming freight intensity relative to trans-Pacific supply routes. E-commerce packaging shifts from plastic air pillows to waxed kraft pads, opening a non-food growth lane that partially offsets QSR demand plateaus in saturated urban markets.

Europe leans on policy-driven substitution, epitomised by the February 2025 Packaging and Packaging Waste Regulation that fixes PFAS limits at 25 ppb. Leading mills, notably Mondi and Stora Enso, funnel close to EUR 1 billion (USD 1.08 billion) into curtain-coater retrofits and unbleached kraft upgrades to serve bakery chains and ready-meal packers. Recyclability icons harmonised across 27 member states boost collection clarity, encouraging retailers to shift from laminated plastics to greaseproof wraps on deli counters. However, energy-price volatility and pulp scarcity keep European producers vigilant on variable cost recovery.

The Middle East and Africa see greaseproof consumption emerging from international coffeehouse chains and fast-growing fried-chicken outlets. Localised converting remains in its infancy, so regional distributors import jumbo rolls from Turkey, Finland and China. South America rides pulp self-sufficiency—especially in Brazil—and adds incremental capacity in Paraná and Rio Grande do Sul states to serve both domestic brands and export markets.

Competitive Landscape

Market fragmentation remains moderate, with the top five suppliers accounting for just under half of global shipments. European incumbents Mondi Group, Billerud and Stora Enso anchor premium segments, leveraging strong R&D pipelines and vertically integrated forest holdings to ensure fibre security. In March 2025, Stora Enso ramped up its EUR 1 billion (USD 1.08 billion) Oulu board line to add 750,000 tpa of folding boxboard and coated unbleached kraft capacity targeting chilled and dry foods. Mondi, meanwhile, ring-fences EUR 1.2 billion (USD 1.29 billion) for organic growth projects across Europe and South Africa to expand greaseproof grades aligned with single-use plastic legislation.

Asian challengers, chiefly Asia Pulp & Paper and Guangzhou Jieshen Paper, play cost leadership, exploiting lower labour costs and proximity to bamboo and acacia raw fibre. They court price-sensitive regional QSR chains while gradually pursuing western certifications to break into multinational procurement rosters. Equipment upgrades remain the major hurdle, given the capital intensity of steel Yankee retrofits. Amcor positions itself as a technology licensor and material innovator rather than a volume paper supplier, locking in patent protection for high-barrier AmFiber Performance Paper in January 2025. Its business model focuses on film-to-paper conversion with life-cycle-analysis validation, providing brand owners with a turnkey sustainability narrative.

Pricing power increasingly hinges on access to certified low-carbon fibre and the ability to prove recyclability under commercial mill conditions. Integrated players that control plantation forestry plus advanced coating IP shield margins even when pulp prices spike or energy costs whipsaw. Smaller converters without dedicated R&D rely on toll coaters and commodity chemistries, exposing them to abrupt regulatory bans and price wars. Mergers and acquisitions activity picked up in 2024 when International Paper acquired DS Smith, expanding its European footprint and cross-selling sustainable liner grades across North American and EMEA operations.

Greaseproof Paper Packaging Industry Leaders

Nordic Paper Holding AB

Metsä Group

Mondi Group

delfortgroup AG

Ahlstrom Holding

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stora Enso commenced operations of its new consumer board line at the Oulu site in Finland, representing a EUR 1 billion investment with annual capacity of 750,000t.

- March 2025: The FDA determined that authorization for 35 food contact notifications related to PFAS are no longer effective, setting a sell-through deadline of June 30 2025.

- February 2025: The EU Packaging and Packaging Waste Regulation entered force, mandating recyclability and PFAS limits of 25 ppb effective Aug 2026.

- January 2025: Amcor received European patent protection for its AmFiber Performance Paper, a high-barrier, recyclable solution.

Global Greaseproof Paper Packaging Market Report Scope

| Bleached Greaseproof Paper |

| Natural / Unbleached Greaseproof Paper |

| Silicone-coated Release Paper |

| Quilon / Fluoro-coated Paper |

| Bakery and Confectionery |

| QSR and Take-away Foods |

| Dairy and Fats (Butter, Cheese) |

| Meat, Poultry and Seafood |

| Industrial and Other Non-food |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Bleached Greaseproof Paper | ||

| Natural / Unbleached Greaseproof Paper | |||

| Silicone-coated Release Paper | |||

| Quilon / Fluoro-coated Paper | |||

| By Application | Bakery and Confectionery | ||

| QSR and Take-away Foods | |||

| Dairy and Fats (Butter, Cheese) | |||

| Meat, Poultry and Seafood | |||

| Industrial and Other Non-food | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the greaseproof paper packaging market?

The greaseproof paper packaging market size is USD 1.78 billion in 2025 and is projected to reach USD 2.33 billion by 2030.

Which region leads the greaseproof paper packaging market?

Asia-Pacific leads with 36.75% revenue share in 2024 and is also the fastest growing, advancing at an 8.50% CAGR through 2030.

Why are PFAS-free papers critical to market growth?

Regulatory bans in the United States and European Union mandate the removal of PFAS, prompting global food-service chains to switch to alternative barrier technologies and driving fresh demand for compliant greaseproof papers.

Which application segment is expanding the fastest?

QSR and take-away packaging is the fastest, recording a 10.80% CAGR as delivery platforms and convenience dining proliferate.

How do raw-material price swings affect manufacturers?

Volatile wood-pulp prices elevate production costs and squeeze margins, particularly for converters lacking long-term fibre contracts or vertical integration.

Page last updated on: